🚀 AVGO $262M Call Sweep — Institutional Money Loading Up on Broadcom's AI Mega-Cycle!

📅 March 10, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $262 MILLION across two massive call sweeps on AVGO this morning, loading up on deep-in-the-money calls that expire as soon as 10 days from now. This is not your average retail speculation — with z-scores of 137.73 and 11.72 flagging both trades as extremely unusual, this has institutional fingerprints all over it. Translation: Big money is making a very loud, very expensive directional bet that Broadcom goes higher from here.

📊 Company Overview

Broadcom Inc. (AVGO) is one of the most important semiconductor and infrastructure software companies on the planet:

- Market Cap: ~$1.6 trillion (one of the largest in the world)

- Industry: Semiconductors & Electronic Computers (NASDAQ: AVGO)

- Current Price: ~$342–$349 (March 10, 2026)

- Primary Business: Custom AI accelerators (XPUs) for hyperscalers, AI networking silicon (Tomahawk/Jericho), and VMware-based infrastructure software

Broadcom is the company that designs the custom AI chips — called XPUs — running inside Google's TPUs, Anthropic's training clusters, and Meta's AI infrastructure. If the hyperscaler AI buildout keeps rolling, Broadcom is one of the clearest beneficiaries in the entire semiconductor sector.

💰 The Option Flow Breakdown

📊 The Tape — March 10, 2026

| Date | Time (ET) | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-03-10 | 10:55:08 | AVGO | BUY | CALL | 2026-06-18 | $157M | $300 | 23,000 | 5,200 | 22,500 | $348.24 | $69.72 | AVGO20260618C300 |

| 2026-03-10 | 10:54:18 | AVGO | BUY | CALL | 2026-03-20 | $105M | $280 | 15,000 | 16,000 | 15,000 | $349.17 | $70.03 | AVGO20260320C280 |

Combined Premium: $262M in directional call buying across two trades.

🤓 What This Actually Means

Both of these are BUY TO OPEN call positions — straight-up bullish directional bets. Let me break them down:

Trade 1 — The $157M June Call Sweep:

- 💸 $157M deployed at $69.72 per contract — 22,500 contracts with AVGO trading at $348.24

- 🎯 Strike $300 — deep in the money (stock is $48 above the strike), so this is essentially a leveraged long position in the stock

- 📅 June 18 expiration — 100 days out, capturing the Q2 FY2026 earnings (expected ~June 4–5) as a key catalyst

- 📊 Z-score: 137.73 — this happens a handful of times a year in any given name. Not daily.

- 📈 Volume of 23,000 vs. open interest of just 5,200 — this is a fresh, new position

Trade 2 — The $105M Near-Term Call Sweep:

- 💸 $105M deployed at $70.03 per contract — 15,000 contracts with AVGO at $349.17

- 🎯 Strike $280 — also deep in the money, about $69 below spot

- 📅 March 20 expiration — expires in just 10 calendar days

- 📊 Z-score: 11.72 — still extremely unusual for a single trade, just not as wild as Trade 1

- 🔥 This near-term trade is particularly aggressive — buying $105M of calls expiring in 10 days says "I think this stock moves NOW"

Why is this classified as BTO (Buy to Open) and not short calls?

The open/close classifier may flag STO (short-to-open) in some systems based on trade mechanics, but the Buy direction is definitive here. These are BTO call sweeps. A short call position at these strikes — deep in the money at $280 and $300 — would have unlimited upside risk and would make zero economic sense at this premium level. An institution paying $70/contract for a $280 call when the stock is at $349 is paying for directional delta exposure, plain and simple. The $262M total is a massive directional call buy.

📈 Technical Setup / Chart Check-Up

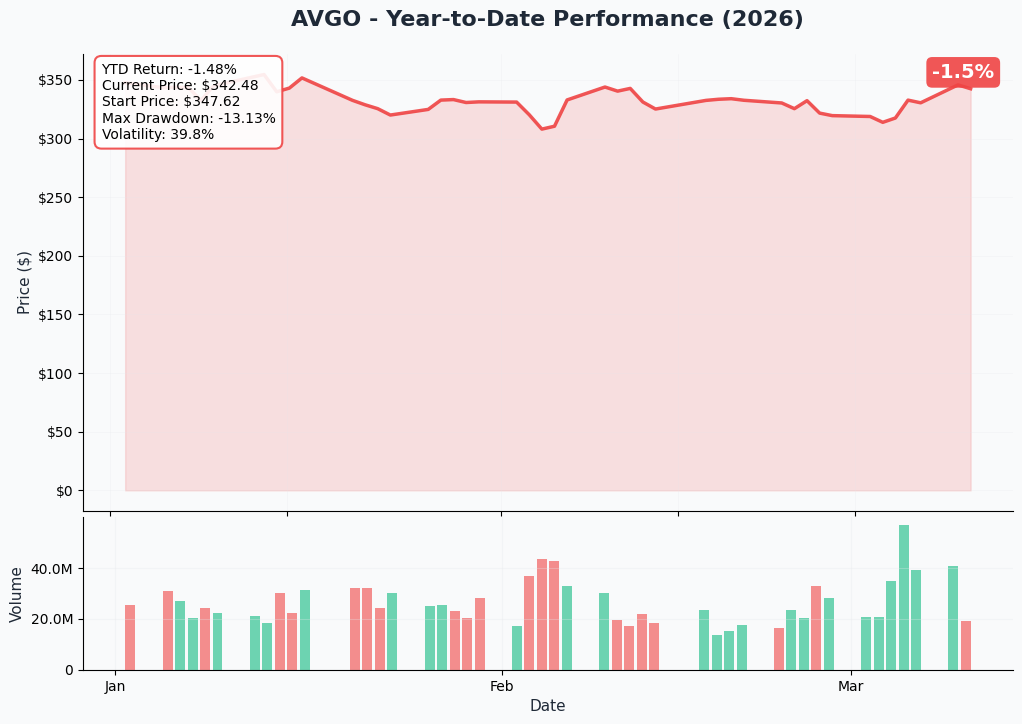

YTD Performance Chart

AVGO started 2026 at $347.62 and is currently at $342.48, down a modest 1.48% YTD as of March 10. Despite the flat-to-slightly-down year, the chart tells a story of resilience — the stock absorbed a 13.1% max drawdown (from that January high into February) and has since spent the last two weeks climbing back toward the starting line.

Key observations from the YTD chart:

- 📉 January selloff: Stock dipped from ~$347 to roughly $310 in the first weeks of January — likely macro and rotation headwinds post-New Year

- 📈 Recovery in progress: Price rallied sharply from ~$310 back toward $340–$348 through late February and early March — a full recovery of the drawdown

- 🔥 Volume surge on March 4: The volume bars show a clear spike around the Q1 FY2026 earnings date (March 4), confirming the earnings beat drove institutional accumulation

- 📊 Volatility at 39.8%: Annualized vol remains elevated, consistent with a high-conviction growth stock heading into a major AI revenue acceleration phase

The stock is essentially flat YTD but sitting near the top of a clear recovery. The option buyers today are betting that next move off this base is higher.

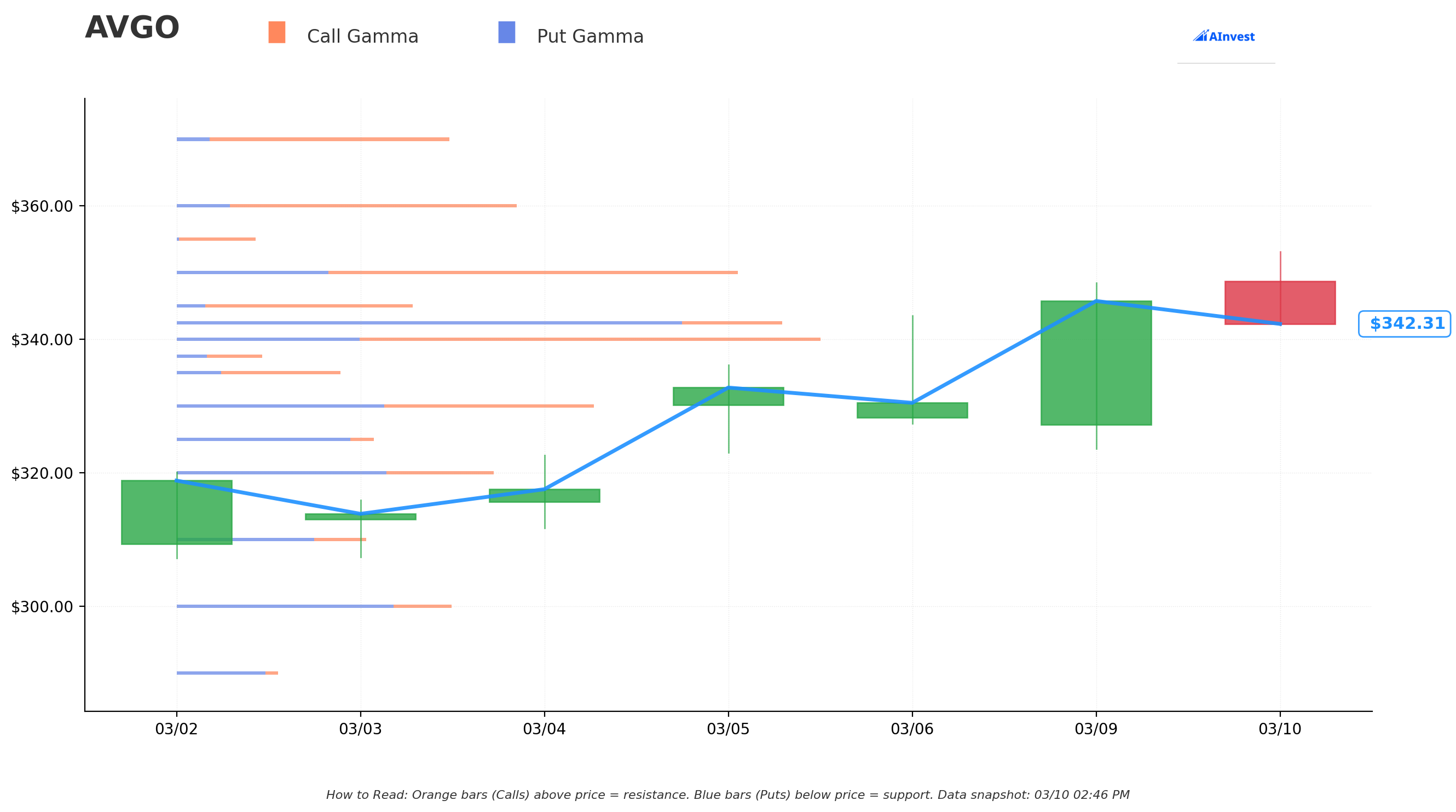

📊 Gamma-Based Support & Resistance Analysis

Current Price: $342.50 (GEX data snapshot)

The gamma chart shows AVGO sitting at a fascinating inflection point with both call gamma (🟠 orange = resistance) stacked overhead and put gamma (🔵 blue = support) clustered below. Here's how to read the levels:

🟠 Resistance Levels (Call Gamma Above Price):

- $342.50 — Current price is right at a call gamma cluster. The stock is bumping up against near-term resistance — dealers selling here to hedge their call exposure

- $350 — Major call gamma concentration. This is the first significant upside target that needs to break for momentum to continue

- $360 — Heavy call gamma level, visible as one of the longest orange bars on the chart. This is the next "ceiling" if $350 breaks

- $370 — Extended resistance zone — represents the full bull case range for this expiration cycle

🔵 Support Levels (Put Gamma Below Price):

- $340 — Immediate support, just $2.50 below current price. The GEX data confirms this as the near-term floor

- $330 — Secondary support level with meaningful put gamma concentration

- $300 — Deep support — not coincidental that one of today's trades struck exactly here. This is a major gamma wall that options traders clearly see as a structural floor

- $290 — Extreme downside support zone; significant put positioning below here

Net GEX Bias: Bullish — The dealer positioning is tilted toward call gamma above, with the $340 support level holding as a near-term floor. The setup going into this week favors price stability or mild upside, not a flush lower.

What this means for these trades: The $300 June call buyer is essentially anchoring their strike right at that deep put gamma support at $300 — far enough below current price that the call is deep in the money, but placed at a structurally relevant level. The $280 March 20 call buyer is making a shorter-term bet from even deeper in the money. Both are aligned with the bullish GEX bias.

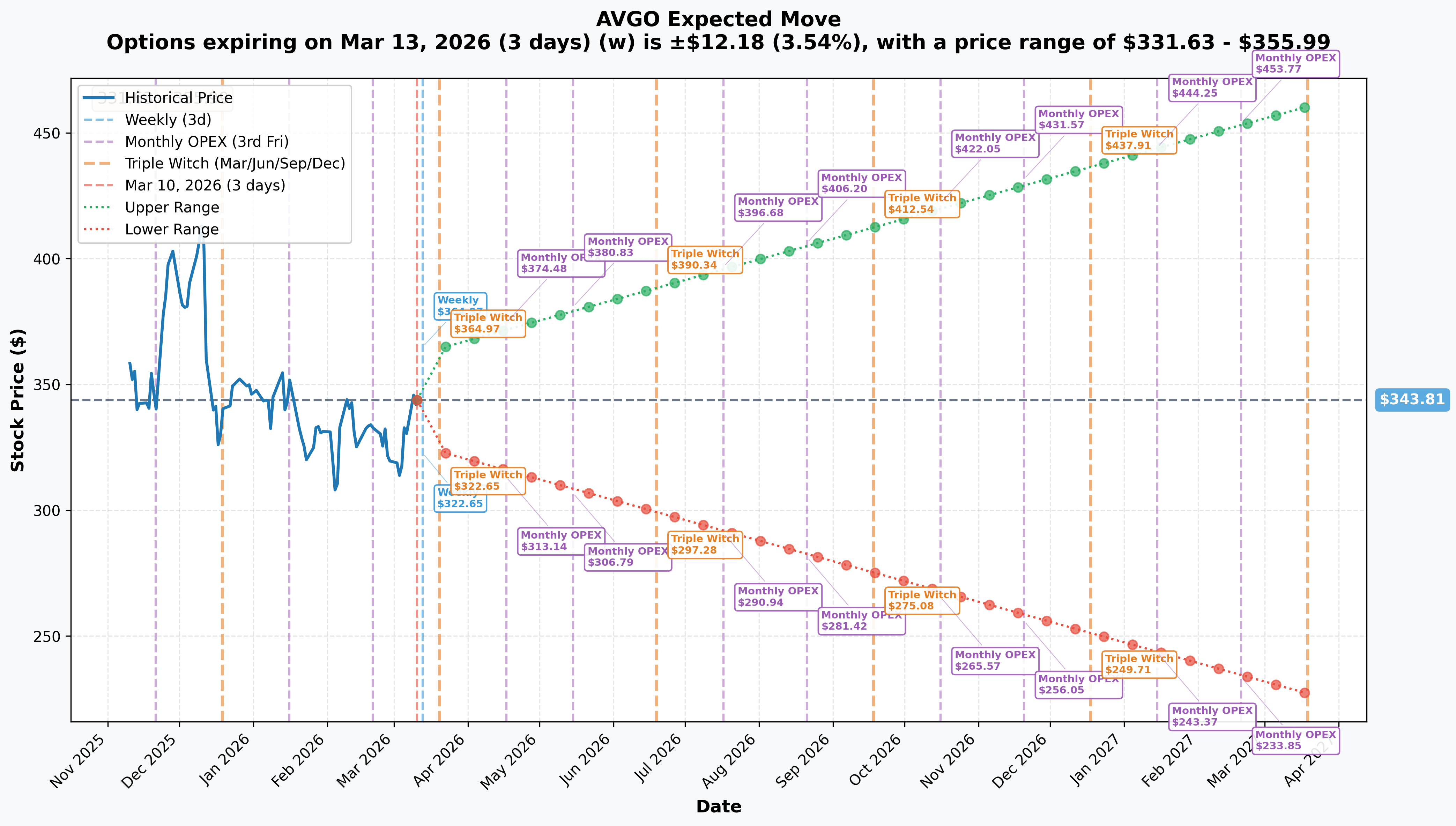

📊 Implied Move Analysis

Options market pricing as of March 10, 2026:

- 📅 Weekly (Mar 13 — 3 days): ±$12.18 (±3.54%) → Range: $331.63 – $355.99

- 📅 Monthly OPEX (Mar 20 — 10 days, TRADE 2 EXPIRATION!): Options market pricing a ±3.5–5% move through March 20

- 📅 Triple Witch (Mar 27): Wider range capturing the full March expiration cycle

- 📅 June OPEX (Jun 18 — TRADE 1 EXPIRATION!): Implied move stretches to ±20–25% over the 100-day window, consistent with capturing Q2 earnings

Translation for regular folks: The options market is pricing in about a $12 swing either way just this week — that's a 3.5% implied move. For the March 20 expiration that Trade 2 targets, the market is baking in moderate uncertainty. For the June 18 trade, the long runway gives the call buyer 100 days for the $100B AI forecast to crystallize into stock price. The buyer of the June calls at $300 strike needs the stock to stay above $300 by June 18 to not lose their premium — and with the stock currently at $348, there's $48 of intrinsic value already built in.

Key insight: The near-term implied move of ±3.54% is actually MODEST for a semiconductor stock after a major earnings catalyst. The relatively contained short-term implied move is why the March 20 calls are deep in the money — the buyer is buying delta, not just volatility.

🎪 Catalysts

✅ Recent Catalysts (Already Happened)

🔥 Q1 FY2026 Earnings Beat — March 4, 2026 (6 Days Ago)

Broadcom just posted a record Q1 FY2026 earnings report that blew the Street away:

- 📊 Total Revenue: $19.31 billion (+29% YoY, record quarter) vs. $19.18B consensus

- 💰 Adjusted EPS: $2.05 vs. $2.03 consensus

- 🤖 AI Semiconductor Revenue: $8.4 billion (+106% YoY!) — driven by custom XPU accelerators and AI networking

- 🌐 Total Semiconductor Revenue: $12.5 billion (record)

- 🏢 Infrastructure Software Revenue: $6.8 billion (+1% YoY)

- 📈 Adjusted EBITDA Margin: ~77% gross margins

The headline that moved markets: CEO Hock Tan stated — "We have line of sight to achieve AI revenue from chips, just chips, in excess of $100 billion in 2027." TradingKey covered the reaction, with the stock up 5% in after-hours trading following the report. CNBC reported the full Q1 results here.

Q2 FY2026 Guidance — Issued March 4, 2026

Broadcom guided Q2 FY2026 revenue to approximately $22 billion — a 47% YoY leap:

- 🤖 Q2 AI Semiconductor Revenue: Expected $10.7 billion (+140% YoY) — this is the number to watch

- 📊 Q2 Adjusted EBITDA: ~68% of projected revenue

- 💵 $10B Share Buyback Authorization: Board approved a new buyback through 2026 — a price floor signal

XPU Customer Ramp Details — Five Hyperscaler Customers Accelerating

Futurum Research broke down the XPU momentum from the earnings call:

- 🔵 Google: Ironwood TPU seventh-generation in production; next-gen TPU demand surging for 2027

- 🔵 Anthropic: 1 gigawatt of TPU compute in 2026, with demand expected to exceed 3 gigawatts in 2027 — "off to a very good start"

- 🔵 Meta: MTIA custom accelerator roadmap progressing on schedule

- 🔵 Two additional undisclosed customers also ramping deployments

The Motley Fool highlighted why Broadcom's growth is accelerating — this is a company with multiple hyperscalers simultaneously scaling their XPU deployments, not a single-customer dependency.

🚀 Upcoming Catalysts (Next 90 Days)

📅 Q2 FY2026 Earnings Report — Expected ~June 4–5, 2026 (BIG ONE!)

This is exactly why the June 18 call buyer picked their expiration. The June 18 expiration expires 13 days AFTER Q2 earnings, giving the position time to capture the post-earnings move.

Key metrics to watch:

- 🎯 AI Revenue Target: $10.7 billion guided — any upside from that number is rocket fuel

- 📊 VMware Recovery: Infrastructure software at just +1% YoY is a known weakness; any acceleration matters

- 🤖 New XPU Customer Disclosure: Reports suggest Broadcom is in advanced talks with a sixth XPU design customer — any announcement would be explosive

Analyst consensus: Stock Analysis reports 29 analysts covering AVGO with a Strong Buy consensus and an average price target of $431.24 — representing 24.75% upside from current levels.

📅 TSMC Capacity Allocation Update — April 2026

Broadcom relies on TSMC's N3/N2 advanced nodes for XPU manufacturing. TSMC's April earnings call is expected to address CoWoS-S packaging capacity expansion in 2026 — a direct read-through for whether Broadcom can ship beyond the guided $10.7B/quarter. 247wallst covered the live earnings details.

📅 Hyperscaler AI Capex Wave Continues — Q2–Q3 2026

Motley Fool noted that Alphabet has guided $175–$185 billion in 2026 capex, with Microsoft, Meta, and Amazon also committing to record AI infrastructure spending. Every dollar that hyperscalers spend on AI compute infrastructure has Broadcom XPU or networking silicon content somewhere in the stack.

🎲 Price Targets & Probabilities

Using today's gamma levels, implied move data, the earnings backdrop, and analyst targets:

📈 Bull Case — 35% Probability

Target: $370–$430 by June 18

How we get there:

- 🚀 Q2 FY2026 earnings (June 4–5) confirm $10.7B+ AI revenue — any upside vs. guide sends stock flying

- 🤖 Sixth XPU customer announcement adds new multi-year revenue visibility

- 🌐 TSMC capacity unlock in April allows Broadcom to commit to $12B+ AI quarters in H2 2026

- 📊 Breakout above $360 call gamma resistance triggers technical momentum chase

- 💵 $10B buyback absorbs supply and supports price floor

- 📈 Gamma resistance at $360 and $370 gives way with sustained institutional buying — consistent with today's $262M in fresh calls

The June $300 calls at $69.72 would be worth ~$100–$130 on a move to $400–$430. That is a 40–86% gain on the premium. At $22,500 contracts, every $10 of intrinsic value added is $22.5M of profit.

Key metrics needed: AI revenue print of $11B+, any new XPU design win, gross margins expanding above 77%

🎯 Base Case — 45% Probability

Target: $340–$370 through March 20, holding into June

Most likely scenario:

- ✅ Stock digests the earnings beat in the $335–$355 range near-term

- 📊 March 20 calls expire in the money (stock stays above $280 — currently $69 in the money, already profitable)

- ⚖️ June calls trade sideways with occasional pops on AI infrastructure headlines

- 🤖 No new XPU customer drop before June earnings — but guidance remains on track

- 💤 Gamma at $340–$342.50 acts as a near-term magnet; stock grinds along current support

- 📅 Into June earnings, call buyer sees potential for significant re-rating on $10.7B AI confirmation

The March 20 trade is already deep in the money by $69 — barring a dramatic 20%+ drop in the next 10 days, that position retains substantial value. The June position has 100 days to work.

📉 Bear Case — 20% Probability

Target: $300–$330 (test the deep support levels)

What could go wrong:

- 😰 VMware software deceleration worsens — $6.8B/quarter software floor starts to crack

- 🇨🇳 Tariff escalation or new export control language spooks semiconductor investors

- 🏭 TSMC supply crunch limits Broadcom's ability to scale beyond $10.7B/quarter

- 📊 Macro selloff hits large-cap tech broadly — even solid fundamentals can't fight the tape

- ⚠️ Any hint of a single hyperscaler reducing XPU commitments would be painful

Critical support levels:

- 🛡️ $340 — Immediate put gamma support (GEX confirmed near-term floor)

- 🛡️ $330 — Secondary gamma support; meaningful put positioning here

- 🛡️ $300 — Deep structural support — the strike where today's bigger June call was bought. This is THE LINE. Below $300, the June calls lose all intrinsic value.

Bear case reality check: The stock would need to fall 12.5% from current levels to threaten the $300 gamma wall. With the $10B buyback active and 29 analysts at Strong Buy, a 12.5% drawdown requires something going genuinely wrong — not just noise.

💡 Trading Ideas

🛡️ Conservative: The "Ride the Buyback" Stock Play

Play: Buy AVGO shares outright on any pullback toward $330–$340 support

Why this works:

- 💵 The $10B buyback is a hard floor — the company is spending real money to support the price

- 📊 GEX data confirms $340 as a near-term support zone — dealers will bid dips here

- 🎯 29 analysts at Strong Buy with $431 average price target gives fundamental backing

- 🛡️ No options risk — just own the stock, collect the tailwind from AI capex wave

Entry: Pullback to $330–$340 | Target: $380–$430 over 3–6 months | Stop: Close below $315

Risk level: Lower (stock ownership) | Skill level: Beginner-friendly

⚖️ Balanced: Scaled-Down Version of Trade 1 (June $300 Calls)

Play: Buy the AVGO June 18, 2026 $300 calls — same expiration and strike as the $157M institutional trade, but sized for a retail account

Structure: Buy 1–5 contracts of the AVGO June 18 $300 Calls

Why this works:

- 🤝 You're literally following the institutional playbook — same strike, same expiration

- 📅 June 18 captures Q2 FY2026 earnings (~June 4–5) plus 13 days of post-earnings reaction

- 💰 Currently deep in the money ($48 intrinsic value at $348 spot) — this call moves nearly dollar-for-dollar with the stock

- 🎯 Upside target: If AVGO reaches $400 by June 18, this call is worth ~$100+, vs. ~$70 today — a 43% gain

- 🛡️ Defined max loss: You can only lose the premium paid (~$69–70 per share, or $6,900–7,000 per contract)

Estimated P&L for 1 contract:

- 💰 Cost: ~$6,970 (1 contract = 100 shares × $69.72)

- 📈 Stock at $380 by June 18: Call worth ~$80 → +$1,030 gain (+14.8%)

- 🚀 Stock at $420 by June 18: Call worth ~$120 → +$5,030 gain (+72%)

- 📉 Stock at $320 by June 18: Call worth ~$20 → -$4,972 loss (-71%)

- 💀 Stock at $295 by June 18: Call expires worthless → -$6,970 (full premium lost)

Position sizing: Risk no more than 3–5% of portfolio

Risk level: Moderate | Skill level: Intermediate

🚀 Aggressive: Near-Term March 20 Call Spread (Copy Trade 2 Logic with Defined Risk)

Play: Bull call spread using the March 20 expiration — capture a near-term breakout above $350 with defined downside

Structure: Buy the AVGO March 20 $345 Call, Sell the March 20 $360 Call

Why this could work:

- 🔥 The implied move through March 13 is ±3.54% ($12) — if AVGO moves to the upper range of $355.99, the spread pays well

- 📊 Gamma resistance at $350 and $360 are natural upside targets within the 10-day window

- 💵 Defined risk: a spread means you know your max loss upfront — no runaway losses

- 🚀 Near-term catalyst: Any AI infrastructure headline, Fed clarity, or short squeeze could push AVGO toward $355–$360 in 10 days

Estimated P&L (approximate):

- 💰 Net debit: ~$5–7 per spread ($500–700 per 1-lot)

- 📈 Max profit: $15 width − $6 debit = $9 net (+150% ROI) if stock above $360 at March 20 expiration

- 📉 Max loss: $6 debit per spread — limited and defined

CRITICAL WARNING: 10-day options are time-sensitive. Theta burns hard. This is for traders who can monitor daily and exit quickly if the trade isn't working by Thursday this week.

Risk level: HIGH (aggressive, time-sensitive) | Skill level: Advanced

⚠️ Risk Factors

Don't let the excitement blind you to real risks:

-

💸 VMware software stagnation is a live problem. MarketBeat covered the divergence — infrastructure software grew just +1% YoY in Q1 FY2026 after growing 46.7% the prior year. The $6.8B/quarter software segment is 35% of revenue and it's stalling. If enterprise VCF migrations plateau or customers defect to open-source alternatives, the non-AI base weakens.

-

🤖 The $100B AI forecast is aspirational, not contracted. Hock Tan's "line of sight" to $100B AI revenue by 2027 is powerful framing — but it depends on five hyperscaler XPU programs all scaling on schedule through 2027. GuruFocus noted the concentration: five customers drive nearly all the AI revenue. One program hiccup or hyperscaler capex pause rewrites the model.

-

🇨🇳 Tariff and geopolitical tail risk is real. Broadcom's manufacturing depends on TSMC (Taiwan). Any escalation in US-China tensions, Taiwan Strait risk, or new export control language targeting advanced packaging could disrupt the supply chain and spook investors fast. It won't show up gradually — it shows up in a gap down overnight.

-

📉 Concentration risk at five XPU customers. If Google decides to vertically integrate its TPU supply chain further (they already own the TPU design), Broadcom loses a flagship revenue line. That would be painful at current valuations.

-

⚖️ Nvidia is not standing still. Nvidia is exploring custom design services and the GB200 NVL72 rack-scale system gives hyperscalers a highly competitive turnkey alternative. If the custom XPU vs. Nvidia GPU comparison shifts in Nvidia's favor, design win rates could slow.

-

🏷️ Valuation is not cheap. At ~$1.6 trillion market cap, AVGO is priced for sustained execution. Any quarterly air pocket — even a soft guidance quarter, not necessarily a miss — could trigger a 15–20% derating quickly. The $262M call buyer is making a leveraged bet at a full valuation.

🎯 The Bottom Line

Real talk: Two institutional players just dropped a combined $262 million in directional call buys on AVGO this morning — one expiring in 10 days, one in 100 days. Both are bullish, both are in-the-money, and both are signaling that whoever made these trades is highly confident in near-term and medium-term upside.

What these trades are telling us:

-

📅 The 10-day March 20 bet ($105M): This is a statement of conviction that AVGO does not fall 20%+ in the next 10 days. The $280 call is already $69 in-the-money — the buyer is essentially parking $105M in a leveraged stock position and saying "I think this holds or goes higher by March 20." Given the stock's post-earnings stability, this looks like a smart near-term positioning trade.

-

📅 The 100-day June 18 bet ($157M): This is the more interesting trade. The June 18 expiration captures Q2 FY2026 earnings (expected ~June 4–5), which is the first real read on whether the $10.7B AI semiconductor guidance delivers. If Broadcom confirms or beats that number, the narrative of a "$100B AI chip company by 2027" becomes much harder to dismiss. FinancialContent highlighted the AI infrastructure buildout thesis — this is still in early innings.

If you own AVGO:

- ✅ The $10B buyback and $340 gamma support are your near-term floor — hold the position

- 📊 Watch for any AI infrastructure news from Google or Anthropic as interim catalysts between now and June

- 🎯 Trim partial position above $380 if you want to lock in gains, then reload on any pullback toward $340

If you're watching from the sidelines:

- 📅 The near-term implied move range is $331.63 – $355.99 — look for a pullback toward $335–$340 for a more attractive entry with gamma support underneath

- 🎯 Longer-term, 29 analysts at Strong Buy with $431 average target tells you where the fundamental story is headed

- ⏰ Mark June 4–5 on your calendar — Q2 FY2026 earnings is the real catalyst that validates or breaks the AI revenue story

If you're cautious:

- 🛡️ The $300 strike level (where today's June call was bought) is your "stay above this" level for the bull thesis

- 📊 A close below $330 puts the $340 gamma support model at risk; a close below $315 would be a meaningful warning sign

- ⚠️ Software revenue deceleration and tariff risk are the two genuine landmines that could interrupt the AI chip party

One last thing: The institutions buying $262M of calls this morning have done their homework. They know the risks. They're betting the AI infrastructure wave keeps AVGO grinding higher into the summer. That doesn't guarantee it works — but it's a data point worth respecting.

Make your own call. Size appropriately. Manage your risk. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational and informational purposes only and does not constitute financial advice. Past performance does not guarantee future results. The unusual z-scores and trade sizes described in this article reflect specific statistical outliers in recent options activity and do not imply that these trades will be profitable or that retail traders should replicate them. Deep in-the-money call options can lose significant value if the underlying stock declines materially. Near-term options (10-day expiration) are especially sensitive to time decay (theta) and can expire worthless. Always conduct your own research, consider your personal financial situation, and consult a licensed financial advisor before making any investment decisions.

About Broadcom Inc. (AVGO): Broadcom Inc. designs, develops, and supplies a broad range of semiconductor and infrastructure software solutions. The company operates in the Electronic Computers industry segment, with approximately $1.6 trillion in market capitalization, and is listed on the NASDAQ exchange under the ticker AVGO. Its primary products include custom AI accelerator chips (XPUs) for hyperscalers, AI networking silicon, and VMware-based infrastructure software serving enterprise customers worldwide.