💎 GOOG $13.8M Put Hedge - Smart Money Buying Insurance on $4 Trillion Giant! 🛡️

📅 January 29, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $13.8 MILLION on GOOG puts across two rapid-fire trades this morning! A total of 7,234 contracts of the $320 strike May 15th puts were bought on the ask in back-to-back executions at 10:12 and 10:13 - with volume hitting 14,700 against just 190 open interest. With GOOG up +76.8% YTD and sitting at a $4 trillion market cap, this looks like a massive institutional hedge ahead of Q4 earnings on February 4th. Translation: A big player is paying nearly $14M for downside protection on one of the largest companies on earth - just 6 days before earnings.

📊 Company Overview

Alphabet Inc. (GOOG) is the parent company of Google, the world's dominant internet platform:

- Market Cap: $4,057.9 Billion (one of only four companies above $4T)

- Industry: Services - Computer Programming, Data Processing

- Current Price: ~$337 (near all-time high of $341.20)

- Primary Business: Google Search (~90% of revenue from advertising), Google Cloud, YouTube, Waymo self-driving cars

💰 The Option Flow Breakdown

The Tape (January 29, 2026 - Two Trades, Same Contract):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:13:34 | GOOG | ASK | BUY | PUT $320 | 2026-05-15 | $9.1M | $320 | 10,000 | 190 | 4,769 | $331.20 | $19.00 |

| 10:12:53 | GOOG | ASK | BUY | PUT $320 | 2026-05-15 | $4.7M | $320 | 4,700 | 190 | 2,465 | $331.10 | $19.00 |

Combined: $13.8M total premium | 7,234 contracts | Volume 14,700 vs OI 190

🤓 What This Actually Means

This is a defensive hedge on a massive long GOOG position! Here's the breakdown:

- 💸 Huge premium paid: $13.8M ($19.00 per contract x 7,234 contracts across two fills)

- 🛡️ Protection strike: $320 provides 5.0% downside cushion below the ~$337 current price

- ⏰ Strategic timing: 3.5 months to expiration (May 15) captures Q4 earnings (Feb 4), Q1 2026 earnings (late April), DOJ mandate impact, and capex guidance uncertainty

- 📊 Size matters: 7,234 contracts represents 723,400 shares worth ~$244M in underlying exposure

- 🏦 Institutional execution: Two back-to-back fills 41 seconds apart, both lifted on the ask at the same $19.00 price - this is a single player building a position fast

- 🔥 Volume/OI ratio: 14,700 volume vs 190 open interest = 77x ratio - these are brand new positions, not rolling or closing

What's really happening here: This trader likely manages a very large long position in GOOG stock - potentially $500M+ worth given the hedge size. After a 76.8% YTD run and with GOOG hitting the $4 trillion club, they're paying $19.00 per share for May 15th $320 puts as insurance going into earnings and the first half of 2026. If GOOG drops below $320 by May 15th, these puts pay off dollar-for-dollar. Think of it as a $13.8M insurance policy on a portfolio position worth hundreds of millions.

Unusual Score: 🔥 EXTREME - Volume 14,700 vs OI of just 190 means the daily volume is 77x the existing open interest. This is clearly a new position being opened, and the back-to-back execution with identical pricing signals a single institutional actor.

📈 Technical Setup / Chart Check-Up

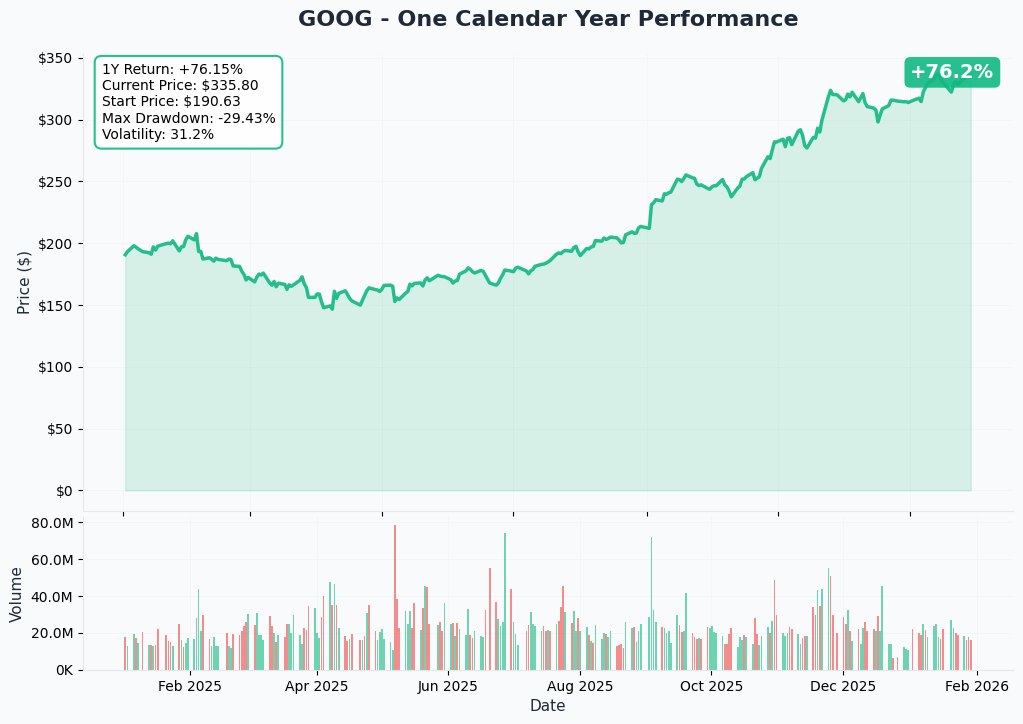

One Calendar Year Chart

GOOG has been on a tear - up +76.8% YTD with the current price around $337. The stock joined the exclusive $4 trillion market cap club on January 13, 2026, alongside Apple, Microsoft, and NVIDIA. The 2025 rally was fueled by three major tailwinds: the favorable antitrust ruling in September (no forced Chrome/Android divestiture), Gemini 3 AI model leadership, and the Apple-Gemini Siri integration deal.

Key observations:

- 🚀 Strong uptrend: Consistent march higher throughout 2025, best annual performance since 2009

- 📈 All-time high: Hit $341.20 on January 13, 2026 - currently just 1.2% below that peak

- 🏛️ $4T milestone: Only fourth company in history to reach this valuation level

- 📊 Relative value play: Despite the rally, GOOG trades at ~30x forward P/E - the second cheapest Magnificent Seven stock

- ⚠️ Extended run: +76.8% in a single year for a $4T company is exceptional - mean reversion risk is real

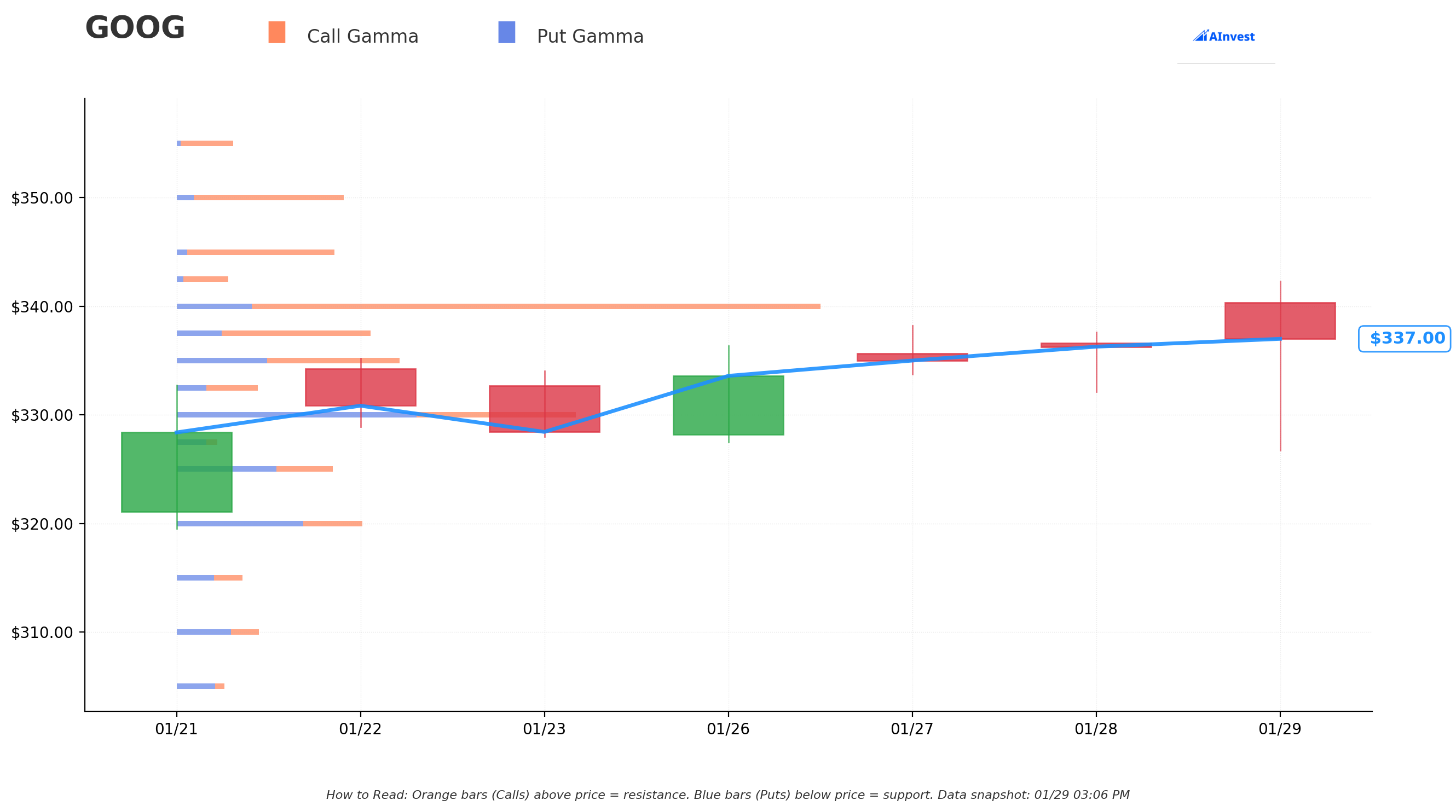

Gamma-Based Support & Resistance Analysis

Current Price: $337.01

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $335 - Immediate support (first line of defense for bulls)

- $330 - Secondary support with significant put gamma concentration

- $325 - Intermediate floor zone

- $320 - Major structural support (EXACTLY WHERE THIS PUT TRADE IS STRUCK!)

- $310 - Deep support level

- $300 - Round-number psychological floor with heavy gamma

🟠 Resistance Levels (Call Gamma Above Price):

- $337.50 - Immediate ceiling (right at current price - creating chop)

- $340 - Near-term resistance zone

- $345 - Secondary ceiling

- $350 - Major psychological and options resistance barrier

What this means for traders: GOOG is trading right against the $337.50 gamma resistance, which explains the current price stalling near all-time highs. The support structure is layered from $335 down to $300, with a particularly significant concentration at $320 - the exact strike chosen by the institutional put buyer. This is NOT a coincidence. The put buyer positioned at a major gamma support level, betting that if GOOG breaks below $325, it could flush quickly toward $320 where dealer hedging flows would create a natural floor.

Notice anything? The $320 put strike sits precisely at a key gamma support level. This institutional player chose that strike deliberately - it represents a ~5% pullback from current levels and aligns with where market maker hedging activity would intensify. If GOOG falls through $330 and $325, the next major floor is $320. Smart strike selection.

Net GEX Bias: Bullish - Overall dealer gamma positioning favors upside, but the put buyer is hedging against the possibility that the bullish regime breaks down post-earnings.

Implied Move Analysis

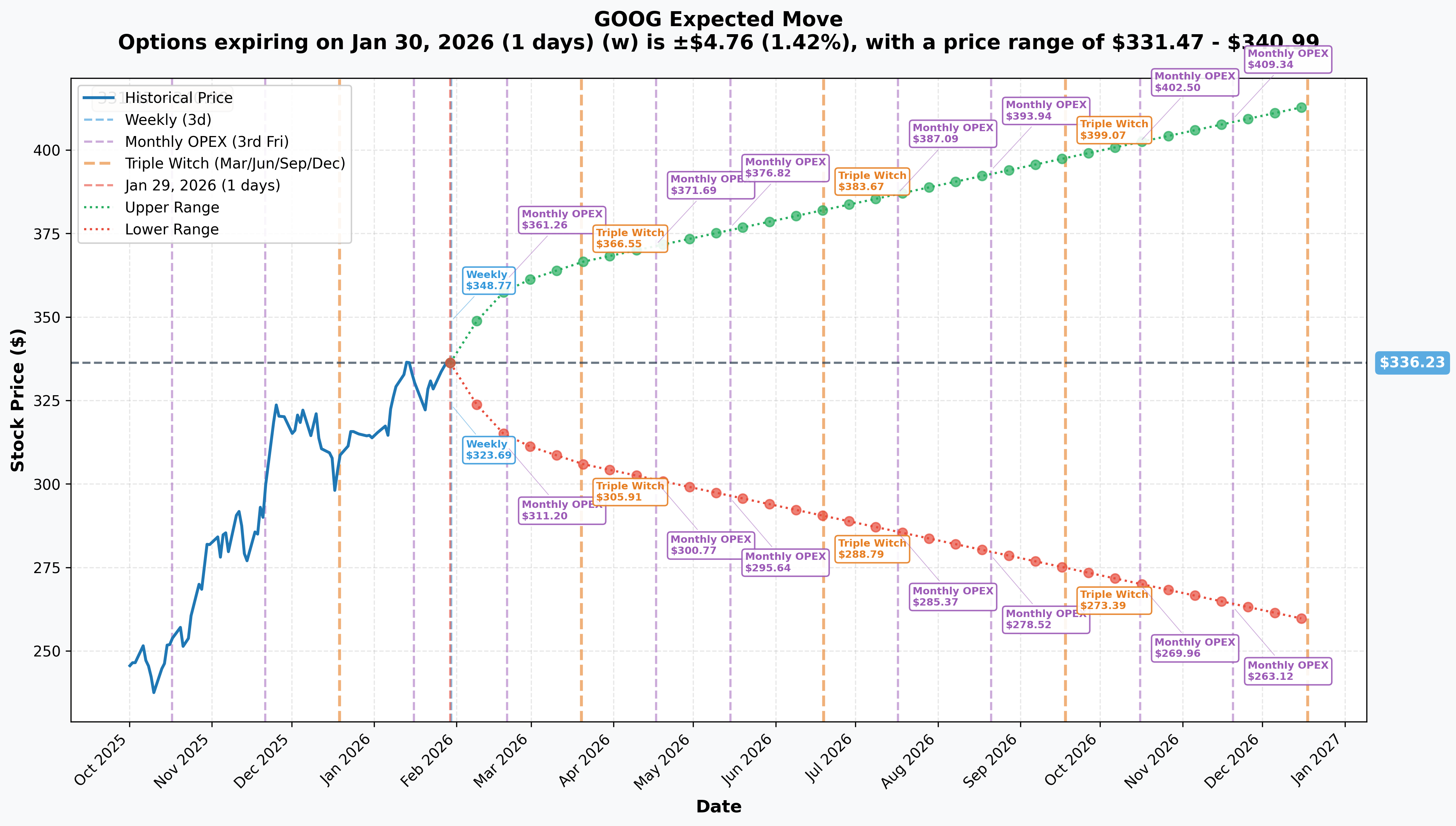

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 30 - 1 day): +/-$4.76 (+/-1.42%) -> Range: $331.47 - $340.99

- 📅 Monthly OPEX (Feb 20 - 22 days): +/-$22.91 (+/-6.81%) -> Range: $313.32 - $359.14

- 📅 Quarterly (Mar 20 - 50 days): +/-$30.32 (+/-9.02%) -> Range: $305.91 - $366.55

- 📅 Yearly LEAPs: +/-$89.35 (+/-26.6%) -> Range: $246.88 - $425.58

Translation for regular folks: The options market is pricing in a modest 1.4% move ($4.76) by tomorrow, but a significant 6.8% move ($23) through February monthly OPEX which captures the February 4th earnings report. For a $4 trillion company, a 6.8% implied move represents roughly $276 billion in market cap swinging either way - that is enormous.

The May 15th expiration (when this $13.8M trade expires) falls between the quarterly and yearly implied move windows. The market suggests GOOG could trade anywhere from roughly $305 to $370 over the next 3.5 months. The put buyer's $320 strike sits comfortably within the implied downside range, meaning the market considers this level reachable - it is not a lottery ticket, it is a realistic hedge.

Key insight: The February monthly OPEX implied move of 6.8% is significantly elevated due to earnings uncertainty. The put buyer chose May expiration specifically to survive any post-earnings volatility crush and still have protection through Q1 earnings and DOJ mandate impact.

🎪 Catalysts

🔥 Immediate Catalysts (Next 7 Days)

Q4 2025 Earnings - February 4, 2026 (6 DAYS AWAY!) 📊

GOOG reports fiscal Q4 2025 results on Wednesday, February 4, 2026 after market close. This is THE catalyst that the put buyer is hedging against. Wall Street consensus and key expectations:

- 📊 Revenue: $111.43B (+15.5% YoY) - driven by search advertising, cloud, and YouTube

- 💰 EPS: $2.59-$2.64 (+20.5% YoY from $2.15)

- ☁️ Google Cloud: Analysts watching for continued 30%+ growth after $15.2B in Q3 (+33.5% YoY)

- 🔑 2026 CapEx Guidance: The single most important number - analysts expect >$110B, up from ~$93B in 2025

- 🤖 AI Monetization: Any commentary on Gemini revenue, AI Overviews ads penetration, and Apple-Gemini deal progress

- 💵 Free Cash Flow: How much capex is eating into FCF - BofA estimates AI capex consuming up to 94% of operating cash flows by 2026

Upside surprise potential: Q3 beat on both revenue ($102.35B vs $99.89B consensus) and EPS ($2.87 vs $2.29 consensus) by wide margins. If Q4 follows the same pattern with cloud growth accelerating and margins holding, stock could push through $340 resistance toward $350+.

Downside risk factors: The biggest fear is capex guidance. If 2026 capex comes in at $120B+ without corresponding revenue acceleration, the market may punish the stock for margin compression. CEO Sundar Pichai himself acknowledges "elements of irrationality" in AI spending levels - if the CEO sounds cautious on ROI, bears pounce.

🚀 Near-Term Catalysts (Q1-Q2 2026)

DOJ Antitrust Mandates - Now In Effect 🏛️

The comprehensive DOJ antitrust mandates took effect January 1, 2026, reshaping how Google operates its search business:

- ⚖️ Exclusive search distribution contracts banned; data-sharing with competitors required

- 🔍 6-year technological oversight committee established to monitor compliance

- 🤖 Requires transparency on Gemini AI models, potentially exposing copyright-related liabilities

- 📈 While the September 2025 ruling was seen as "almost a best-case scenario" (no forced Chrome/Android sale), the DOJ is reviewing whether to seek additional relief

- ⚠️ A separate ad-tech antitrust case already found Google guilty; remedies are still pending and could be more severe

Why this matters for the put trade: The May 15th expiration captures the first full quarter of DOJ mandate implementation. If Q1 2026 earnings (late April) show ANY revenue leakage from search distribution changes, the stock could correct meaningfully.

Gemini 3 AI Leadership & Apple-Gemini Deal 🤖

GOOG's AI strategy is firing on all cylinders:

- 🧠 Gemini 3 positioned as the leading frontier AI model; OpenAI CEO Sam Altman reportedly declared a "code red" in response

- 📱 Apple will use Google's Gemini AI to upgrade Siri - a massive distribution win that puts Gemini on billions of devices

- 🏛️ Pentagon selected Alphabet to lead GenAI.mil platform using Gemini for government AI tools

- 💰 Google denied plans for Gemini ads in 2026, but AI Overviews already showing ads in search results

Capex Ramp & Margin Pressure 💸

The elephant in the room - Alphabet's AI infrastructure spending is accelerating at a staggering pace:

- 🏗️ 2026 capex expected >$110B (up from ~$93B in 2025) - ~60% servers, ~40% data centers

- 📉 AI-related capex projected to consume up to 94% of operating cash flows by 2026 (BofA estimate)

- ⚠️ Rising depreciation from massive capex build-out expected to compress operating margins in 2026-2027

- 🤔 The market needs to see REVENUE from this spending, not just spending promises - any signals of delayed AI monetization would hurt

Waymo Expansion - The Hidden Value Driver 🚗

Waymo is entering its breakout year:

- 🌆 Launched Miami service in January 2026 (6th market)

- 🗺️ Targeting 15 cities by end of 2026 including Dallas, Denver, Detroit, Houston, Las Vegas, Orlando

- 🌍 London launch planned for 2026 (first international market)

- 📈 Targeting 1M rides/week by end of 2026 (4x current volume) after serving 14M trips in 2025

- 🏭 Manufacturing expansion: 2,000+ vehicles at Arizona plant by end of 2026

- ⚠️ Risk: U.S. probe into Waymo after robotaxi incident involving a child could slow expansion

📊 Analyst Sentiment

| Firm | Action | Price Target | Date |

|---|---|---|---|

| Cantor Fitzgerald | Upgraded to Overweight | $370 (from $310) | Jan 2026 |

| Scotiabank | Raised PT | $375 (from $336) | Jan 9, 2026 |

| Citi | Raised PT, Top Pick | $350 (from $343) | Dec 2025 |

| Seeking Alpha Analyst | Downgraded to Hold | -- | Jan 2026 |

- Consensus: 44 analysts, Strong Buy rating, average PT $316.47

- Second cheapest Magnificent Seven stock at <30x forward earnings

- Notable: Average analyst PT of $316 is BELOW current price of ~$337 - the stock has run past Street targets

⚠️ Risk Catalysts (Negative)

Valuation & FCF Pressure 📊

Despite being the "cheapest" Mag 7 name, GOOG is not cheap in absolute terms:

- 📈 Stock up 65% in 2025 with EV/EBITDA at 26x trailing, near multi-decade highs

- 💸 Stock has now rallied 76.8% YTD and trades above the average analyst price target ($316)

- 📉 One Seeking Alpha analyst downgraded to Hold citing valuation concerns and weakening free cash flow

- ⚠️ At ~30x forward P/E, any deceleration in growth or margin compression from capex ramp could reset the multiple

Competitive Pressure in AI and Cloud 🤖

- ⚔️ OpenAI, Microsoft, and Anthropic aggressively competing in AI models and enterprise AI

- ☁️ AWS and Azure still hold larger cloud market share despite Google Cloud's 33.5% growth rate

- 🚗 Tesla robotaxi and Amazon Zoox emerging as Waymo competitors

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through the May 15th expiration:

📈 Bull Case (30% probability)

Target: $350-$375

How we get there:

- 💪 Q4 earnings CRUSH expectations with revenue toward $115B+ and cloud growth accelerating above 35%

- 🤖 2026 capex guidance is large ($110B+) BUT paired with clear AI monetization metrics and revenue visibility

- 📱 Apple-Gemini Siri integration launches with strong user adoption data

- 🚗 Waymo expansion on track - 10+ cities launched by May with improving unit economics

- 📊 Analyst upgrades cascade as PTs raised to $370-400 range

- ⚖️ DOJ mandate implementation proves manageable with minimal search revenue impact

- 📈 Breakout above $340-345 gamma resistance triggers technical momentum toward $360-375

Probability assessment: 30% because GOOG has consistently beaten earnings expectations (Q3 beat by massive margins) and the AI story is legitimate. However, the stock has already run 76.8% and sits above most analyst targets, limiting further upside without significant new catalysts.

🎯 Base Case (45% probability)

Target: $315-$345 range (CONSOLIDATION)

Most likely scenario:

- ✅ Solid Q4 earnings meeting or slightly beating consensus (~$111-113B revenue, ~$2.60-2.70 EPS)

- ☁️ Cloud growth steady at 30-33% but not accelerating - meets but doesn't wow

- 💸 Capex guidance comes in at $110-115B range with limited ROI visibility - market digests

- ⚖️ DOJ mandates create some noise but no material revenue impact in Q1 2026

- 🚗 Waymo expansion progressing but still pre-revenue at scale

- 🔄 Stock trades in a range between $315-345 as market digests massive 2025 gains

- 📊 Volatility crush post-earnings (IV drops 30-40%) as uncertainty resolves

This is the put buyer's insurance scenario: Stock consolidates in the $315-345 range, puts expire with minimal or no value, but the protection served its purpose during the earnings and DOJ uncertainty window. The $13.8M is the cost of sleeping at night while holding hundreds of millions in GOOG stock.

Why 45% probability: GOOG's fundamentals are strong (search dominance, cloud growth, AI leadership), but the stock price already reflects these positives. Consolidation after a 76.8% run is the most natural outcome.

📉 Bear Case (25% probability)

Target: $280-$320 (TEST THE PUT STRIKE!)

What could go wrong:

- 😰 Q4 earnings disappoint on revenue deceleration or margin compression from capex ramp

- 💸 2026 capex guidance shocks at $120-130B+ with vague AI monetization timeline - FCF concerns spike

- ⚖️ Ad-tech antitrust case remedies come in severe (potential structural breakup of ad business)

- 📉 DOJ data-sharing mandates begin hurting search market share in Q1 2026

- 🤖 AI competition intensifies: OpenAI or Anthropic releases model that leapfrogs Gemini 3

- 🚗 Waymo incident or regulatory setback slows expansion plans

- 💰 Broader tech selloff as AI spending ROI skepticism grows across the sector

- 🔨 Break below $330 support triggers cascade through $325 to $320 put strike level

Critical support levels:

- 🛡️ $330: Secondary gamma support - first real test for bulls

- 🛡️ $325: Intermediate floor zone

- 🛡️ $320: Major gamma support + this put strike - likely aggressive buying here

- 🛡️ $310: Deep support if $320 breaks - would represent ~8% correction

- 🛡️ $300: Psychological floor - would represent ~11% correction

Probability assessment: 25% because it requires multiple negative catalysts aligning. GOOG's fundamental dominance in search (90%+ share), strong cloud growth (33.5%), and AI leadership with Gemini 3 provide a solid floor. But the capex-to-FCF concern and dual antitrust overhang are legitimate risks that the put buyer is clearly worried about.

Put P&L in Bear Case:

- Stock at $310 on May 15: Puts worth $10.00, loss = -$9.00/share x 7,234 = -$6.5M (still a loss, hedge partially offsets)

- Stock at $300 on May 15: Puts worth $20.00, profit = $1.00/share x 7,234 = $723K (breakeven zone)

- Stock at $280 on May 15: Puts worth $40.00, profit = $21.00/share x 7,234 = $15.2M (110% ROI!)

- Stock at $320 on May 15: Puts worth $0 (at-the-money), loss = -$19.00/share x 7,234 = -$13.7M (near total loss)

Breakeven: $301 ($320 strike - $19.00 premium). Stock needs to fall 10.7% for the puts to profit on their own. But remember - as a hedge, the puts protect a much larger long stock position. Even a loss on the puts is "worth it" if the stock drops 10%+ and the hedge limits portfolio damage.

💡 Trading Ideas

🛡️ Conservative: Wait for Earnings Clarity

Play: Stay on sidelines until after February 4th earnings volatility settles

Why this works:

- ⏰ Earnings in 6 days creates binary event risk with +/-6.8% implied move through February OPEX

- 💸 Implied volatility elevated pre-earnings - options are EXPENSIVE right now

- 📊 Stock trading above average analyst PT of $316 - limited margin of safety at $337

- 🎯 Better entry likely post-earnings after IV crush reduces option premiums 40-50%

- 🤔 The $13.8M institutional put buy signals sophisticated players see risk ahead - why fight that?

- ⚖️ Capex guidance is a genuine wildcard - $110B vs $130B changes the entire narrative

Action plan:

- 👀 Watch February 4th earnings closely for: revenue growth rate ($111B+ target), 2026 capex guidance (the KEY number), cloud margins, AI monetization commentary

- 🎯 Look for pullback to $315-320 gamma support post-earnings for stock entry with 5-6% margin of safety

- ✅ Need to see capex-to-revenue relationship making sense before committing capital

- 📊 Monitor DOJ mandate impact commentary - any revenue leakage concerns?

- ⏰ If earnings are strong and stock pushes above $340 resistance, consider buying the breakout with tight stop

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 5-10% drawdown if earnings or guidance disappoint. Get better entry if stock consolidates. Maintain optionality.

⚖️ Balanced: Post-Earnings Put Spread (Follow the Smart Money)

Play: After earnings, buy a put spread targeting the institutional hedge zone

Structure: Buy $325 puts, Sell $315 puts (May 15 expiration - SAME as the $13.8M trade)

Why this works:

- 🎢 IV crush after earnings makes put spreads much cheaper - buy AFTER volatility drops

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 🎯 Targets the gamma support zone at $315-$325 where institutional positioning is concentrated

- 🤝 Mirrors the smart money positioning at better prices post-IV crush

- ⏰ 3+ months to expiration gives time for DOJ mandate impact, capex concerns, or broader tech rotation to materialize

- 🛡️ Protects against "sell the news" scenario even if earnings beat

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Pay ~$3-4 net debit per spread post-earnings (vs $5-6 now)

- 📈 Max profit: $600-700 if GOOG below $315 at May expiration

- 📉 Max loss: $300-400 if GOOG above $325 (defined and limited)

- 🎯 Breakeven: ~$321-322

- 📊 Risk/Reward: ~1.5:1 which is attractive for defined-risk bearish play

Entry timing:

- ⏰ Wait 2-3 days post-earnings (by Feb 6-7) for full IV collapse

- 🎯 Only enter if stock still trades above $325 (gives spread room to work)

- ❌ Skip if stock already below $320 (spread too close to at-the-money, limited R/R)

Position sizing: Risk only 2-5% of portfolio (this is directional speculation, not core holding)

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

🚀 Aggressive: Earnings Straddle - Bet on BIG Movement

Play: Buy a straddle betting on post-earnings volatility exceeding the implied move

Structure: Buy $335 calls + Buy $335 puts (February 20 expiration)

Why this could work:

- 💥 Implied move of 6.8% ($23) through Feb OPEX, but capex guidance creates potential for larger move

- 🎰 Multiple binary catalysts in one earnings call: revenue, cloud, capex, AI monetization, DOJ commentary

- 📊 At $4 trillion market cap, any surprise in capex guidance ($110B vs $130B) could swing stock 8-10%

- 🤖 Apple-Gemini deal progress update could add fuel in either direction

- ⚡ Need stock to move >7-8% either way to profit after IV crush

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Straddle costs ~$20-25 ($2,000-2,500 per straddle) due to elevated pre-earnings IV

- ⏰ TIME DECAY KILLER: Theta accelerates with only 22 days to expiration

- 😱 IV CRUSH: Even if stock moves 5-6%, IV collapse could still result in LOSS on both legs

- 📊 Consolidation risk: Stock could stay in $325-345 range and straddle loses 40-60%

- ⚠️ GOOG is a $4T mega-cap - it takes a LOT to move this stock more than 7-8%

Estimated P&L:

- 💰 Cost: ~$20-25 per straddle

- 📈 Profit scenario: Stock moves to $360 or $310 (7-8%+ move) = $3-5 gain (15-25% ROI)

- 🚀 Home run: Stock moves to $370 or $300 (10%+ move) = $10-15 gain (50-75% ROI)

- 📉 Loss scenario: Stock ends $325-345 range = lose $10-20 (40-80% loss)

- 💀 Total loss: Stock flat at $335 = lose entire $20-25 (100% loss)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded straddles through earnings before and understand IV crush mechanics

- ✅ Can afford to lose ENTIRE premium (real possibility for a $4T stock!)

- ✅ Can monitor position Wednesday after-hours post-earnings and Thursday morning

- ✅ Plan to close position within 24-48 hours post-earnings (don't hold to expiration)

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Earnings binary event in 6 days: Results Wednesday February 4th after close create significant volatility risk. Options pricing +/-6.8% implied move through February OPEX. The capex guidance number alone ($110B vs $120B vs $130B) could swing the stock 5%+ in either direction. Revenue, cloud growth, and AI monetization commentary add additional binary risk layers. The put buyer clearly sees enough risk to spend $13.8M on protection.

-

💸 AI capex consuming free cash flow: This is the bear case in a single bullet point. 2026 capex expected >$110B, with BofA estimating AI capex consuming up to 94% of operating cash flows. CEO Sundar Pichai himself acknowledges "elements of irrationality" in AI spending levels. If the market decides the ROI on this spending is unclear, GOOG becomes a "show me" story trading at a lower multiple.

-

⚖️ Double antitrust overhang: While the search antitrust case resolved favorably (no Chrome/Android breakup), the DOJ mandates are now in force requiring data-sharing with competitors. MORE importantly, a separate ad-tech antitrust case already found Google guilty with remedies pending - these could be MORE severe than the search case. The Apple-Gemini deal itself could face antitrust scrutiny. Regulatory risk is far from over.

-

📊 Stock trading above analyst consensus: With 44 analysts averaging a $316.47 price target and the stock at ~$337, GOOG has already exceeded Wall Street expectations. When a stock trades 6% above average PT, it means the "easy money" has been made. Upside requires analysts to chase the stock higher with new targets, which depends on February 4th earnings delivering.

-

🐋 Smart money buying $13.8M insurance at peak: This institutional put purchase signals sophisticated players are concerned about downside despite strong fundamentals. Two back-to-back executions totaling 7,234 contracts against just 190 open interest - this is a major, deliberate new hedge position. When funds sitting on massive gains pay $13.8M for protection rather than staying fully exposed into earnings, that is a caution flag worth respecting.

-

🚗 Waymo execution and safety risk: U.S. probe into Waymo after a robotaxi incident involving a child could slow expansion. Scaling from 6 to 15+ cities in a single year carries enormous operational risk. A single high-profile safety incident could set the entire program back years and remove an important "hidden value" catalyst.

-

🤖 AI competition intensifying: OpenAI, Microsoft/Copilot, and Anthropic are all aggressively competing in frontier AI and enterprise AI. While Gemini 3 currently leads, the AI model race moves fast - a competitor breakthrough could erode GOOG's AI premium quickly.

-

📉 Mean reversion after +76.8% YTD: No $4 trillion company rallies 77% in a year without at some point experiencing significant consolidation or pullback. Market history shows mega-cap stocks following massive rallies tend to experience 10-15% corrections within the following 3-6 months. The question is not IF but WHEN.

🎯 The Bottom Line

Real talk: Someone just spent $13.8 MILLION protecting a massive GOOG position 6 days before the most important earnings report of the year. This is not a bearish bet on Alphabet's future - it is textbook institutional risk management by a player who has made enormous money on the 76.8% YTD rally and does not want to give it back in one bad earnings print or capex guidance shock.

What this trade tells us:

- 🎯 Sophisticated player expects potential VOLATILITY through May (not necessarily a crash, but protecting against 5-10% downside scenario)

- 💰 They're worried enough about $337 to $320 move to pay $19.00/share for insurance (5.6% of stock price!)

- ⚖️ The timing (6 days pre-earnings) shows they see binary risk in capex guidance, AI monetization commentary, and DOJ mandate impact

- 📊 They structured at $320 strike which sits exactly at a major gamma support level - not random, very deliberate

- ⏰ May 15th expiration captures TWO earnings cycles (Q4 Feb 4, Q1 late April) plus DOJ mandate implementation - maximum catalyst coverage

This is NOT a "sell everything" signal - it is a "smart money is managing risk at all-time highs" signal.

If you own GOOG:

- ✅ Consider trimming 15-25% at $335-340 levels (lock in massive gains, reduce concentration risk)

- 📊 If holding through earnings, mentally mark $320 as your floor - that is where major gamma support and institutional protection sits

- ⏰ Do not get greedy - you are up 77% YTD on a $4 trillion stock. Protecting profits is smart, not fearful

- 🎯 If earnings beat AND stock breaks above $345 resistance, could re-enter trimmed shares

- 🛡️ Consider buying 1-2 protective puts per 100 shares if holding a large position (mirror this trade at smaller scale)

If you're watching from sidelines:

- ⏰ Wednesday February 4th after close is the moment of truth - DO NOT enter before earnings

- 🎯 Post-earnings pullback to $315-320 would be an EXCELLENT entry (5-7% off highs with gamma support)

- 📈 Looking for: 2026 capex guidance <$115B, cloud revenue growth 30%+, clear AI monetization roadmap, manageable DOJ mandate impact

- 🚀 Longer-term (6-12 months), Waymo expansion to 15 cities, Apple-Gemini Siri launch, and cloud backlog conversion are legitimate catalysts for $360+

- ⚠️ Current price above average analyst PT ($316) means you are paying full price - patience pays

If you're bearish:

- 🎯 Wait for earnings before initiating shorts - fighting 77% momentum at all-time highs is dangerous

- 📊 First support at $335, then $330, major floor at $320 (put strike + gamma level)

- ⚠️ Post-earnings put spreads ($325/$315 or $320/$310 May expiration) offer defined-risk downside exposure after IV crush

- 📉 Watch for break below $325 - that is the trigger for acceleration toward the $320 put strike and potentially $310

- ⏰ Capex guidance is your best friend: if $120B+ with unclear ROI, bears take control of the narrative

Mark your calendar - Key dates:

- 📅 February 4 (Wednesday) after market close - Q4 FY2025 earnings report (6 DAYS!)

- 📅 February 5 (Thursday) - Post-earnings price action and analyst reactions

- 📅 February 20 - Monthly OPEX (+/-6.8% implied move window closes)

- 📅 March 20 - Quarterly expiration

- 📅 Late April 2026 - Q1 2026 earnings (first look at DOJ mandate impact on revenue)

- 📅 May 15, 2026 - Expiration of this $13.8M put trade

- 📅 Throughout 2026 - Waymo expansion to 15 cities + London launch

Final verdict: Alphabet's long-term position is powerful - dominant in search (90%+ share), leading in AI with Gemini 3, growing fast in cloud ($155B backlog), and leading the robotaxi revolution with Waymo. BUT, at all-time highs after 76.8% YTD gains with capex consuming nearly all free cash flow, dual antitrust overhangs, and earnings in 6 days, the near-term risk/reward favors PATIENCE over aggression. The $13.8M institutional put buy confirms: smart money is derisking at the peak.

Be patient. Let earnings clear. Focus on the capex number. If GOOG pulls back to $315-320, that is where the real opportunity begins.

This is a marathon, not a sprint. Protect your capital. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The extreme volume/OI ratio (77x) reflects this specific trade's unusual nature - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for 5-10% gaps either direction. The put buyer may have complex portfolio hedging needs not applicable to retail traders.

About Alphabet Inc.: Alphabet is a holding company that wholly owns internet giant Google. The company derives approximately 90% of revenue from Google services (primarily advertising across Search, YouTube, and its ad network). Alphabet also operates Google Cloud, the YouTube platform, and Waymo self-driving cars, with a market capitalization of $4,057.9 billion in the Services - Computer Programming, Data Processing industry.