IBRX Options Activity Analysis

January 16, 2026

Trade Tape

| Field | Value |

|---|---|

| Time | 10:22:05 ET |

| Ticker | IBRX |

| Direction | SELL |

| Type | CALL |

| Expiration | January 21, 2028 |

| Strike | $3.50 |

| Spot Price | $5.13 |

| Option Price | $2.70 |

| Size | 10,000 contracts |

| Premium | $2,700,000 |

| Volume | 10,000 |

| Open Interest | 6,700 |

| Option Symbol | IBRX20280121C3.5 |

| Strategy | Covered Call - Closing Position (STC) |

What Just Happened

Someone just closed out a massive covered call position on ImmunityBio, pocketing $2.7 million in the process. This is a Sell to Close (STC) transaction, meaning the trader is unwinding an existing position rather than opening a new one.

Here is the key detail: the volume of 10,000 contracts exceeds the open interest of 6,700. That tells us this position was likely built over time, and the trader is now taking profits after IBRX's explosive 99% YTD rally. With the stock at $5.13 and the strike at $3.50, these calls are deep in-the-money with over two years until expiration.

Why close now? The timing is notable. IBRX has been on a tear with 10 consecutive up days and just reported 700% year-over-year revenue growth 1. The trader may believe the stock has reached a near-term top, or they simply want to lock in gains after the Saudi FDA approvals sent shares soaring 76% in a single week 2.

Unusual Score

Score: 8.2/10 - EXTREMELY UNUSUAL

[================== ]

Plain English: This is an exceptionally rare trade. A $2.7 million single-ticket options transaction on a $3.89 billion market cap biotech represents approximately 0.07% of market cap in a single trade. For context, IBRX typically sees average daily options volume in the tens of thousands of dollars, making this roughly 50-100x larger than normal activity.

Size Context: Large institutional allocation. This is not retail activity - we are looking at fund-level capital deployment or unwinding.

Company Snapshot

ImmunityBio, Inc. (IBRX) is an integrated clinical-stage biotechnology company focused on discovering, developing, and commercializing next-generation immunotherapies and cellular therapies. The company operates three therapeutic platforms: antibody-cytokine fusion proteins, vaccine development (DNA, RNA, and recombinant protein), and cell therapies.

| Metric | Value |

|---|---|

| Sector | Biotechnology |

| Industry | Biological Products |

| Market Cap | $3.89 billion |

| Shares Outstanding | 984.97 million |

| Employees | 673 |

| Headquarters | San Diego, California |

| IPO Date | March 10, 2021 |

| Primary Exchange | NASDAQ |

Lead Product: ANKTIVA - an IL-15 superagonist antibody-cytokine fusion protein, FDA-approved for BCG-unresponsive non-muscle invasive bladder cancer (NMIBC) with carcinoma in situ.

Why This Matters

The Bull Case

ImmunityBio is executing one of the most impressive commercial launches in recent biotech history. ANKTIVA generated $113 million in FY2025 revenue - a staggering 700% increase year-over-year 1. The company has momentum on multiple fronts:

-

Global Regulatory Expansion: Approvals now span the U.S. (April 2024), UK (July 2025), EU conditional authorization (December 2025), and Saudi Arabia for both bladder cancer and NSCLC (January 2026) 345

-

Clinical Pipeline Advancing: The BCG-naive NMIBC trial (QUILT-2.005) is 85% enrolled with interim data showing 84% complete response vs 52% for BCG alone 6

-

NSCLC Opportunity: First global approval for IL-15 superagonist + checkpoint inhibitor combination opens a multi-billion dollar lung cancer market 5

The Bear Case

The massive position unwind suggests sophisticated money may be taking chips off the table:

-

Cash Runway Concerns: With approximately $242.8 million in cash and a $234.6 million nine-month burn rate, the company has roughly 1.6 years of runway 78. Dilution is likely.

-

Competitive Threats: J&J's INLEXZO (approved September 2025) shows 82% complete response vs ANKTIVA's 62-71% 9. Big pharma has superior commercial infrastructure.

-

Valuation Stretched: After a 99% YTD gain, IBRX trades at a significant premium to revenue. The easy money may have been made.

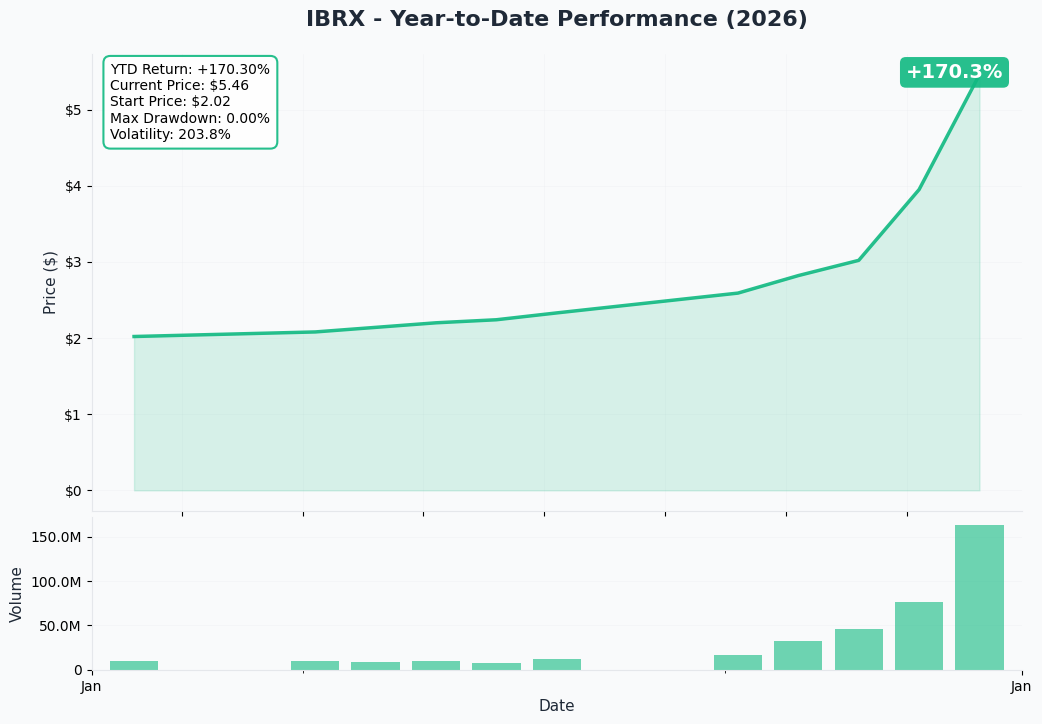

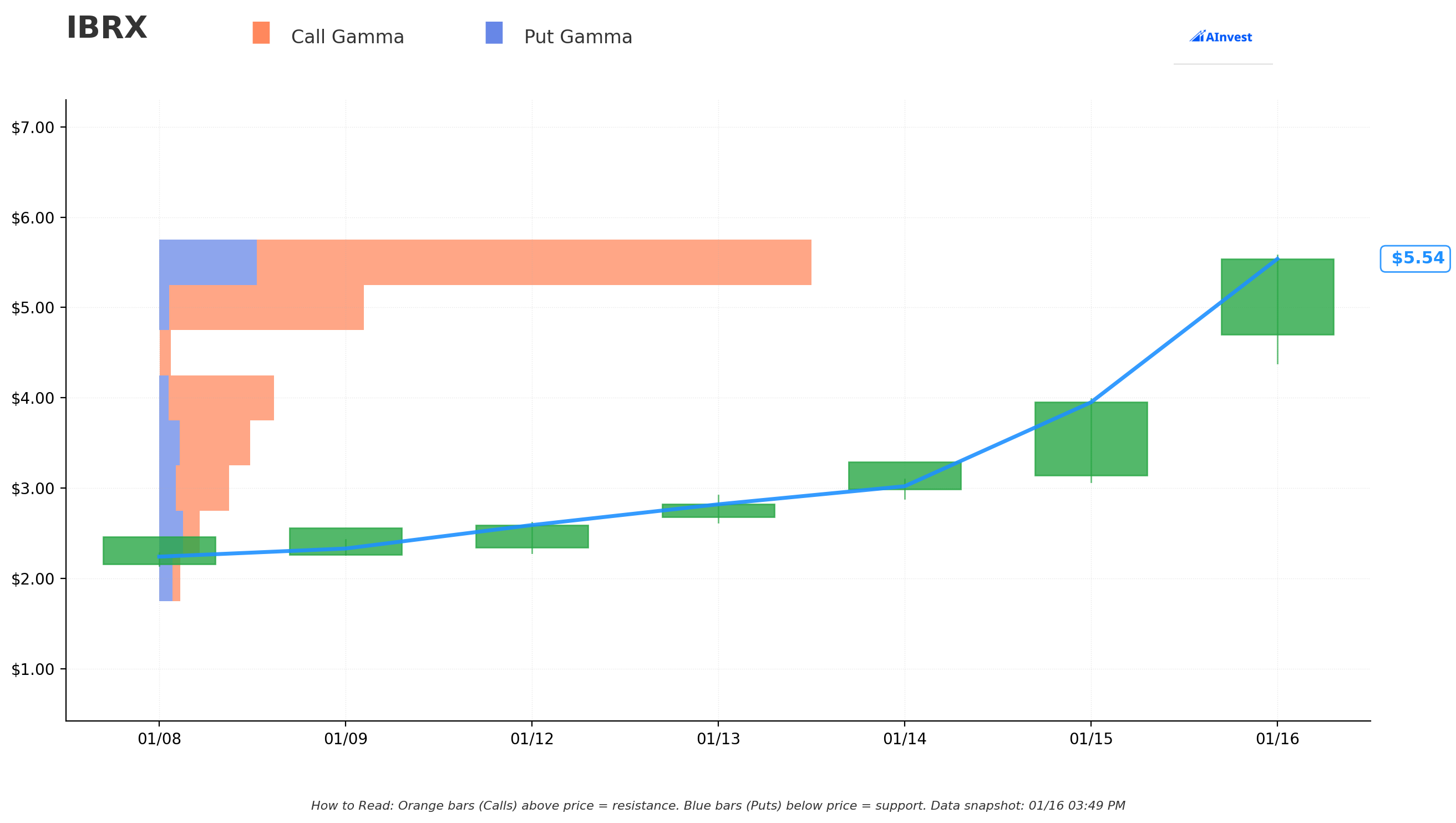

Technical Picture

The stock has been on an absolute tear, posting 10 consecutive up days and gaining 99% year-to-date in just two weeks 10. This type of vertical move typically needs consolidation before continuing higher.

Key gamma levels to watch:

- Major Support: $4.00-$4.50 (high put open interest, dealer long gamma)

- Resistance: $5.50-$6.00 (call wall forming)

- Pin Risk: $5.00 strike likely to act as magnet near term

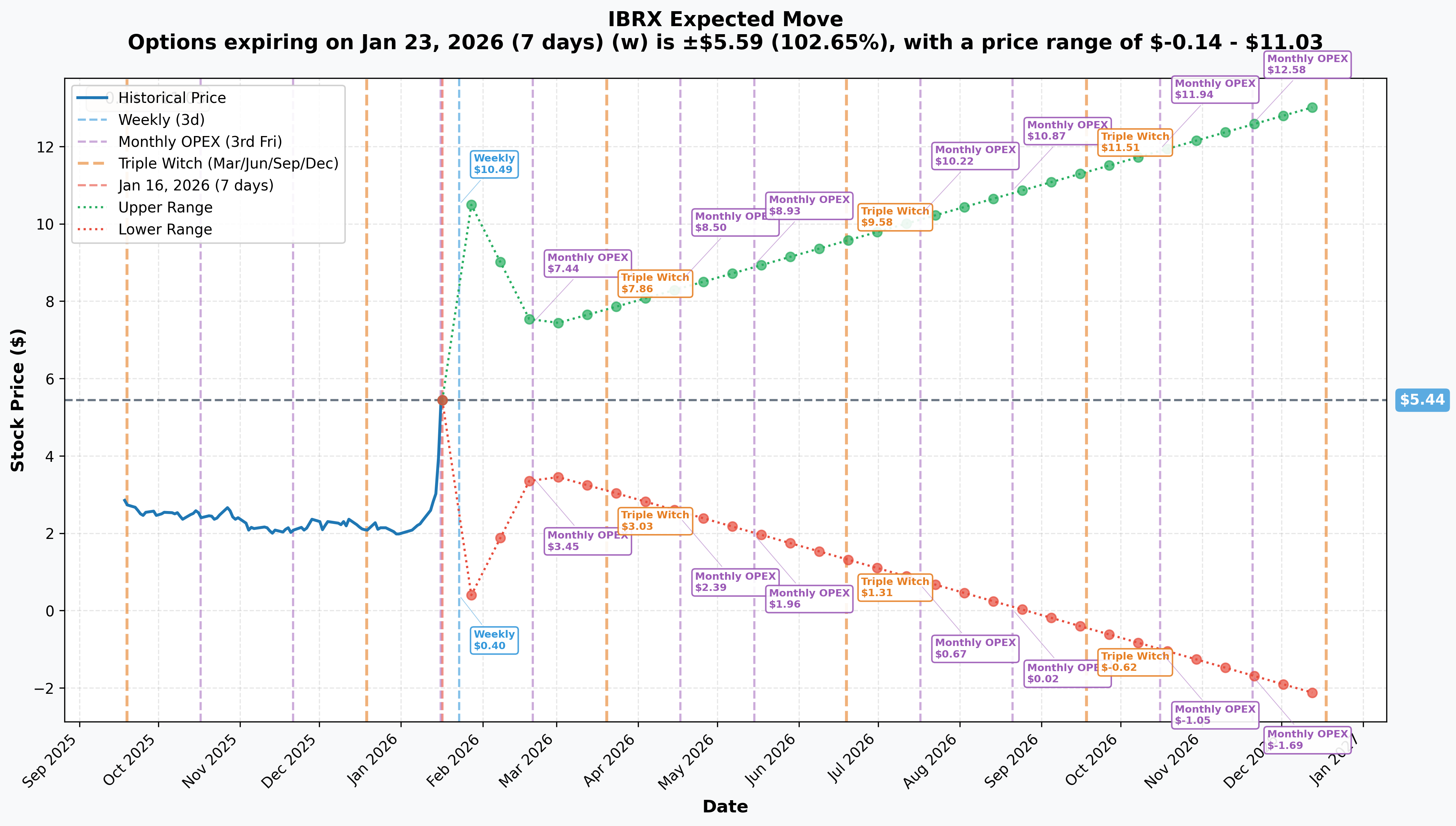

Implied Move Analysis

The options market is pricing in extreme volatility across all timeframes:

| Timeframe | Expiry | Implied Move | Range |

|---|---|---|---|

| Weekly | Jan 23 | +/- 102.65% | $0.40 - $10.49 |

| Monthly OPEX | Feb 20 | +/- 33.57% | $3.45 - $7.44 |

| Triple Witch | Mar 20 | +/- 43.33% | $3.03 - $7.86 |

| LEAPS | Dec 18 | +/- 141.23% | -$2.24 - $13.13 |

The 102% weekly implied move is extraordinary - the market expects IBRX could potentially double or get cut in half within a week. This reflects the binary nature of biotech catalysts and the stock's recent volatility.

Price Targets

Based on gamma positioning, implied move ranges, and analyst targets:

| Target | Price | Probability | Rationale |

|---|---|---|---|

| Bullish | $7.50 - $8.00 | 30% | Upper monthly implied range, breakout continuation on NCCN inclusion or BCG-naive data |

| Base Case | $4.50 - $5.50 | 45% | Consolidation around current levels, profit-taking absorbs enthusiasm |

| Bearish | $3.00 - $3.50 | 25% | Cash concerns resurface, competitive pressure, retest of breakout level |

Analyst Consensus:

- Average 12-month target: $10.40-$11.73 11

- Range: $5.05 - $25.20 12

- D. Boral Capital maintains $24 target 13

Trading Strategies

Conservative: Cash-Secured Put

Setup: Sell the February 20, 2026 $4.00 Put

- Rationale: Collect premium while waiting for pullback to attractive entry. The $4.00 strike represents 22% downside from current levels and sits at the lower implied range.

- Max Gain: Premium collected (estimate $0.40-$0.60 per contract)

- Max Risk: Assignment at $4.00 (own shares at effective basis of ~$3.50)

- Best For: Investors who want to own IBRX at lower prices and get paid to wait

Balanced: Bull Call Spread

Setup: Buy the March 20 $5.00 Call / Sell the March 20 $7.50 Call

- Rationale: Defined risk exposure to continued upside with reduced cost basis vs outright call purchase

- Max Gain: $2.50 spread width minus net debit

- Max Risk: Net debit paid

- Best For: Traders who believe momentum continues but want to limit volatility exposure

Aggressive: Long Stock + Covered Call

Setup: Buy 100 shares at $5.13, Sell February $6.00 Call

- Rationale: Participate in upside to $6.00 while generating income to reduce cost basis

- Max Gain: Call premium + $0.87 appreciation

- Breakeven: Stock purchase price minus premium received

- Best For: Bullish traders who believe near-term upside is capped around $6.00

Key Catalysts

Near-Term (Next 30 Days)

- NCCN Guideline Decision (February 2026) - Critical for commercial adoption 14

- Q4 2025 Earnings (March 3, 2026) - Revenue confirmation and 2026 guidance 15

Medium-Term (1-6 Months)

- EU Final Marketing Authorization (Q1 2026) 4

- QUILT-2.005 Full Enrollment (Q2 2026) - BCG-naive indication [^5_1]

- ResQ201A Phase 3 Interim Data (H2 2026) - NSCLC confirmatory trial [^9_4]

Long-Term

Risk Factors

-

Dilution Risk: 1.6-year cash runway makes equity raise highly probable 18

-

Competitive Pressure: J&J's INLEXZO approval with superior efficacy data threatens market share 9

-

Regulatory Uncertainty: FDA refused to file papillary NMIBC sBLA despite prior guidance 19

-

Single Product Dependency: ANKTIVA accounts for essentially all product revenue 20

-

Legal Overhang: Ongoing class action and Sorrento lawsuit create headline risk 2122

-

Valuation Risk: 99% YTD gain prices in significant execution success

The Bottom Line

This $2.7 million covered call unwind is a fascinating window into institutional thinking. Someone with deep pockets is locking in profits after IBRX's explosive rally, choosing to take money off the table rather than ride the momentum higher.

For Bulls: The fundamental story remains compelling. ANKTIVA's commercial launch is exceeding expectations, global regulatory momentum is building, and the BCG-naive indication could meaningfully expand the addressable market. Analyst targets suggest significant upside if execution continues.

For Bears: The easy gains are behind us. Cash runway concerns, competitive threats from J&J, and stretched valuation create meaningful headwinds. The trader closing this position may know something about near-term price action.

Action Plan:

-

If bullish: Wait for pullback to $4.50-$4.80 gamma support before adding. Alternatively, sell puts to establish position at lower prices.

-

If neutral: The risk/reward is balanced here. Consider defined-risk strategies like spreads rather than directional bets.

-

If bearish: Avoid shorting into momentum. If positioned short, use call spreads to define risk given potential catalyst upside.

-

Key dates to watch: February NCCN decision, March 3 earnings, Q2 BCG-naive enrollment completion.

The market is pricing in extreme moves in both directions. Trade small, use defined risk, and respect the volatility.

References

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Options trading involves substantial risk of loss. Past performance is not indicative of future results. Always conduct your own due diligence before making investment decisions.

Footnotes

-

Business Wire, "ImmunityBio Reports Continued Execution and Sales Momentum With $113 Million of Preliminary Net Product Revenue", January 15, 2026 ↩ ↩2

-

Simply Wall St, "ImmunityBio Up 76.3% After Saudi Approvals", January 2026 ↩

-

ImmunityBio, "UK MHRA Approves ANKTIVA Plus BCG", July 2025 ↩

-

ImmunityBio, "EMA Conditional Marketing Authorization Recommendation", December 12, 2025 ↩ ↩2

-

ImmunityBio, "Saudi FDA Grants Accelerated Approval for NSCLC", January 14, 2026 ↩ ↩2

-

Stock Titan, "ANKTIVA + BCG extends CR in BCG-naive trial", January 16, 2026 ↩

-

Yahoo Finance, "ImmunityBio Revenue Surge and Narrowed Losses", January 2026 ↩

-

Simply Wall St, "ImmunityBio Balance Sheet Analysis", January 2026 ↩

-

Johnson & Johnson, "INLEXZO FDA Approval", September 2025 ↩ ↩2

-

Stock Invest, "Immunitybio Stock Price Forecast", January 2026 ↩

-

Fintel, "IBRX Forecast and Price Target", January 2026 ↩

-

Investing.com, "ImmunityBio Reprices Higher", January 2026 ↩

-

Public.com, "D. Boral Capital $24 Price Target", January 2026 ↩

-

Nasdaq, "ImmunityBio Price Target Increased", January 14, 2026 ↩

-

Seeking Alpha, "ImmunityBio Earnings Dates", January 2026 ↩

-

Seeking Alpha, "BLA submission expected by year end", January 2026 ↩

-

ImmunityBio, "Regulatory Update on FDA Submissions", 2025 ↩

-

ImmunityBio, "$80 Million Equity Financing", July 2025 ↩

-

ImmunityBio, "FDA Meeting Request Following RTF Letter", May 2025 ↩

-

AInvest, "ImmunityBio's 30% Surge Analysis", January 2026 ↩

-

StocksToTrade, "ImmunityBio Legal Troubles", April 2025 ↩

-

StocksToTrade, "ImmunityBio Stock Faces Turbulence", March 2025 ↩