🌶️ MKC: Bears Closing Shop — $6.4M Put Position Unwound at $65 Strike

📅 March 12, 2026 | 🔥 Unusual Options Activity Detected

🎯 The Quick Take

Someone just spent $6.4 million buying to close a massive put position on McCormick at the $65 strike — and that's actually a bullish signal in disguise. This trader had been betting MKC would fall hard (below $65), and today they're cashing in or cutting losses on that bearish bet, with the stock now trading near $57.94 — already well below their put strike. With Q1 FY2026 earnings due March 31, closing out a deep-in-the-money put position now suggests this trader no longer sees additional downside worth holding for.

📊 Company Overview

McCormick & Company (NYSE: MKC) is the world's largest spice and seasoning company — the Old Bay, Frank's RedHot, Cholula, and French's Mustard brand under one roof:

- Market Cap: ~$16.09 Billion

- Industry: Miscellaneous Food Preparations & Kindred Products (Consumer Staples)

- Primary Business: Two segments: Consumer (retail spices, herbs, condiments, and sauces — including McCormick, Frank's RedHot, Cholula, French's, and Old Bay) and Flavor Solutions (custom flavor compounds and ingredients sold to food manufacturers and QSR chains)

- Market Position: Holds approximately 26% of the U.S. spices and seasonings market — about 4x its nearest competitor — and roughly 20% of the $19B global spices and herbs market

- Dividend: 40th consecutive year of dividend increases; $1.92/share annual payout (~3.3% yield at current price)

💰 The Option Flow Breakdown

📊 The Tape (March 12, 2026 @ 14:26:30)

| Field | Detail |

|---|---|

| Date / Time | 2026-03-12 / 14:26:30 |

| Symbol | MKC |

| Side | MID |

| Buy / Sell | BUY |

| Call / Put | PUT |

| Strike | $65 |

| Expiration | 2026-04-17 |

| Option Symbol | MKC20260417P65 |

| Premium | $6.4M |

| Volume | 8,300 |

| Open Interest | 8,900 |

| Size | 8,318 |

| Spot Price | $57.94 |

| Option Price | $7.70 |

| Strategy | Buy to Close (BTC) — Closing Long Put |

| Vol / OI Ratio | 0.93 (MEDIUM confidence) |

🤓 What This Actually Means

This trade is easy to misread, so let's be clear about what's really going on here.

Plot twist: The "BUY" label here does NOT mean someone is opening a new bearish position. This is a Buy to Close — the trader who previously opened a large put position at the $65 strike is now buying back those contracts to exit the trade.

Here's the math that tells the story:

- 📊 OI vs. Volume: Open Interest is 8,900 contracts. Volume today is 8,300 — that's 93% of OI. When volume approaches or matches OI like this, it almost always means someone is closing most (or all) of an existing position, not opening a new one.

- 💰 The put is deep in the money: MKC is trading at $57.94, and the strike is $65. That means the $65 put has approximately $7.06 in intrinsic value — it's already profitable for whoever held it. The option price of $7.70 confirms it's mostly intrinsic value with a thin time premium.

- 🛡️ $6.4 million to exit: At $7.70 per contract × 8,318 contracts × 100 shares = roughly $6.4M. This is a significant closing transaction, not a new bet.

What this signals:

The original holder opened this $65 put position when MKC was trading higher — likely above $65 — expressing a bearish view that the stock would fall. That view has largely played out: MKC is now about 11% below the $65 strike. By closing today, the trader is either:

- Taking profits on a winning bearish position (MKC already dropped well below $65), or

- Limiting further risk before the March 31 earnings report, where additional downside is uncertain

Either way, closing a large bearish put position suggests this trader no longer sees sufficient additional downside to justify holding through the Q1 earnings print 19 days from now. That's worth paying attention to — it's a subtle but real shift in sentiment.

Translation for regular folks: Imagine you bet $6M that your neighbor's house would flood. The basement is already underwater. Instead of holding the bet, you're cashing out before the weather forecast changes. That's what just happened here.

📈 Technical Setup / Chart Check-Up

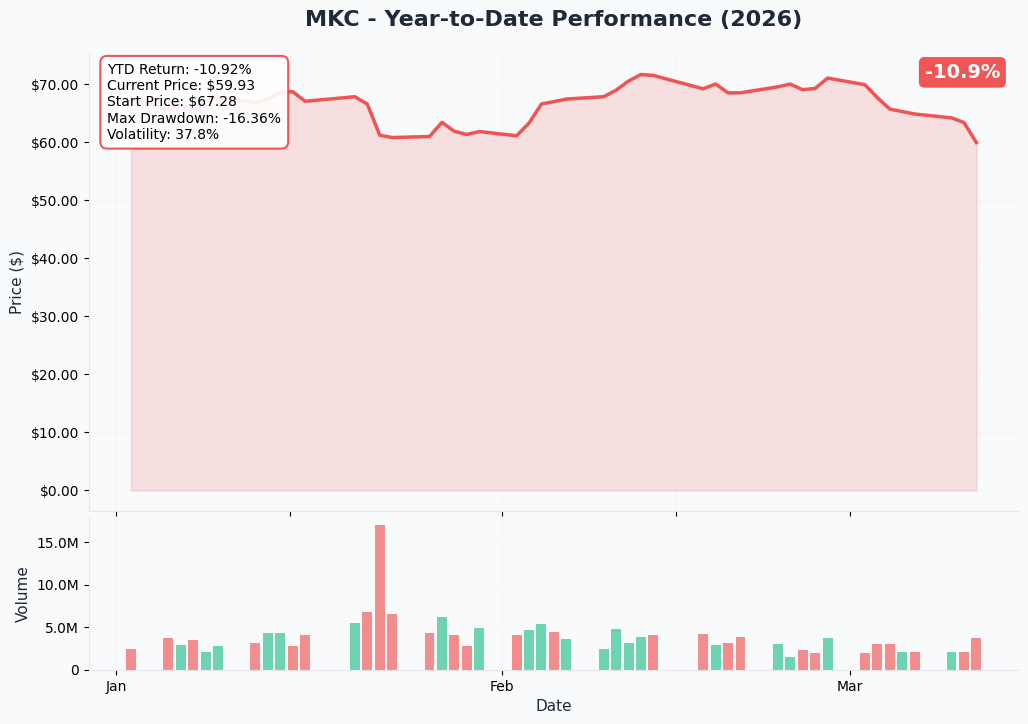

YTD Performance

MKC has had a rough 2026. The stock entered the year around $78–80 and has been on a persistent downward trajectory, now trading near $57.94 — a decline of roughly 27–28% year-to-date. The sell-off was triggered by the January 22 earnings report where adjusted EPS came in $0.01 short of consensus, management issued FY2026 EPS guidance of $3.05–$3.13 (below prior Street consensus), and the Zacks "Strong Sell" downgrade on March 11 added another layer of pressure.

Key observations:

- 📉 Sustained downtrend: No meaningful bounce since the post-earnings gap lower in late January

- 🎢 Near 52-week low: Trading near the $59.20 52-week low floor

- 📊 Volume has been elevated on down days: Institutional distribution pattern, confirmed by former CEO Kurzius selling 100,000 shares in two tranches

- 👀 At a decision point: Q1 earnings on March 31 are the next major inflection catalyst

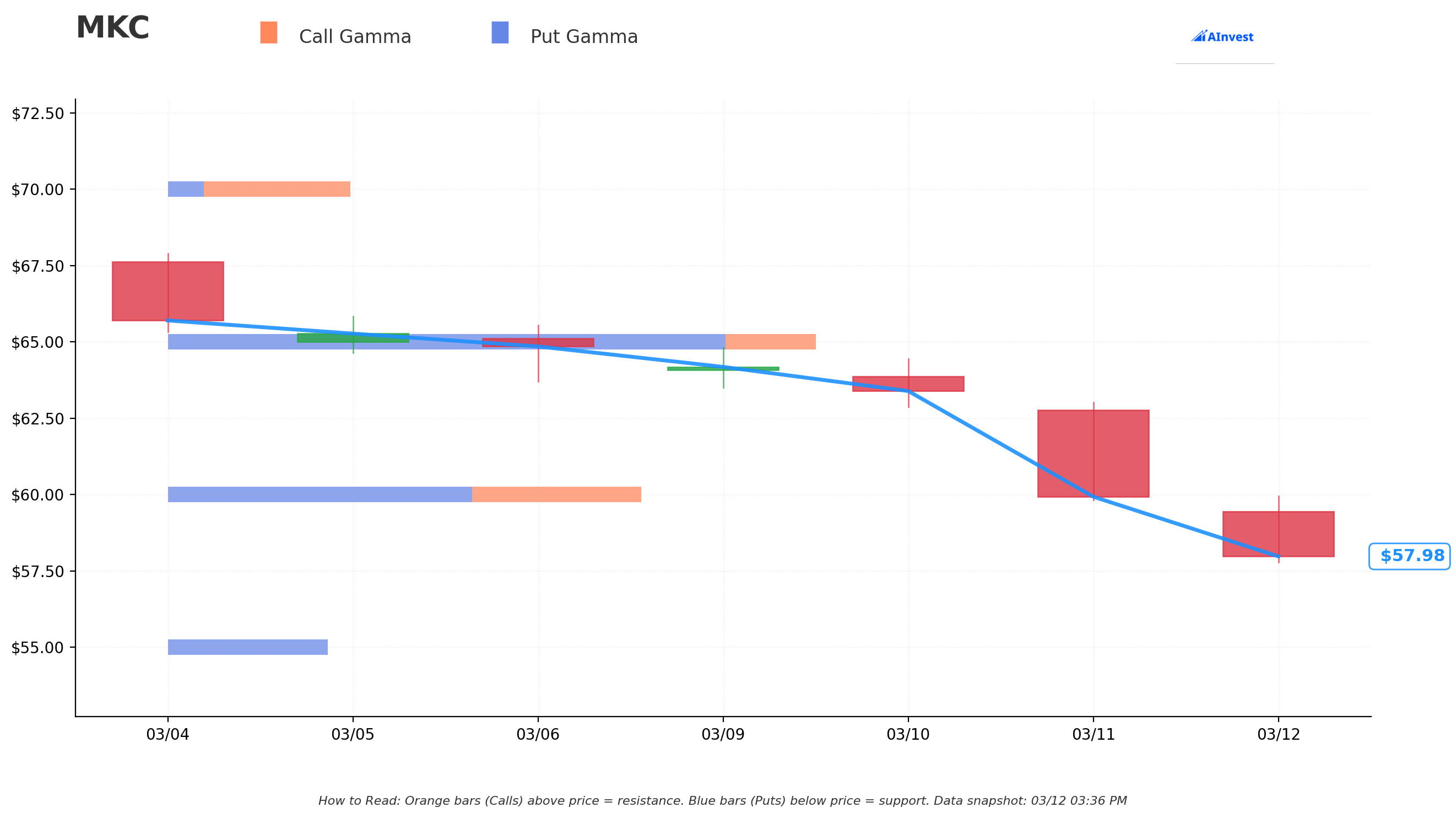

Gamma-Based Support & Resistance

Current Price: $58.05

The gamma exposure (GEX) data gives us a clear picture of where market makers are positioned and where price is likely to find friction:

🔵 Support Levels (Put Gamma Below Price):

- $55.00 — Strongest nearby support; put GEX of 0.61. If MKC breaks below $57–58, market makers will be buyers near $55 as they hedge their put exposure, creating a natural floor

- This is approximately a 5.3% decline from current levels

🟠 Resistance Levels (Call Gamma / Total GEX Above Price):

- $60.00 — First resistance; total GEX of 1.83. About 3.4% above current price; market makers have significant exposure here, creating selling pressure on any rally attempt

- $65.00 — Heavy resistance; total GEX of 2.51. This is precisely where today's closed put was struck — a clear signal that this level had significant options interest and acted as a gravitational anchor for positioning

Net GEX Bias: Bearish — Put GEX at 4.21 exceeds Call GEX at 2.16, meaning overall dealer hedging flows are slightly tilted to support the stock on down moves, but the market structure remains skewed bearish.

What this means for traders: MKC is sandwiched. Support at $55 provides a near-term floor, but the $60 level will likely cap any meaningful rally attempt before earnings. The $65 strike — where today's $6.4M put was closed — represented a key anchor for institutional positioning that is now being cleared out.

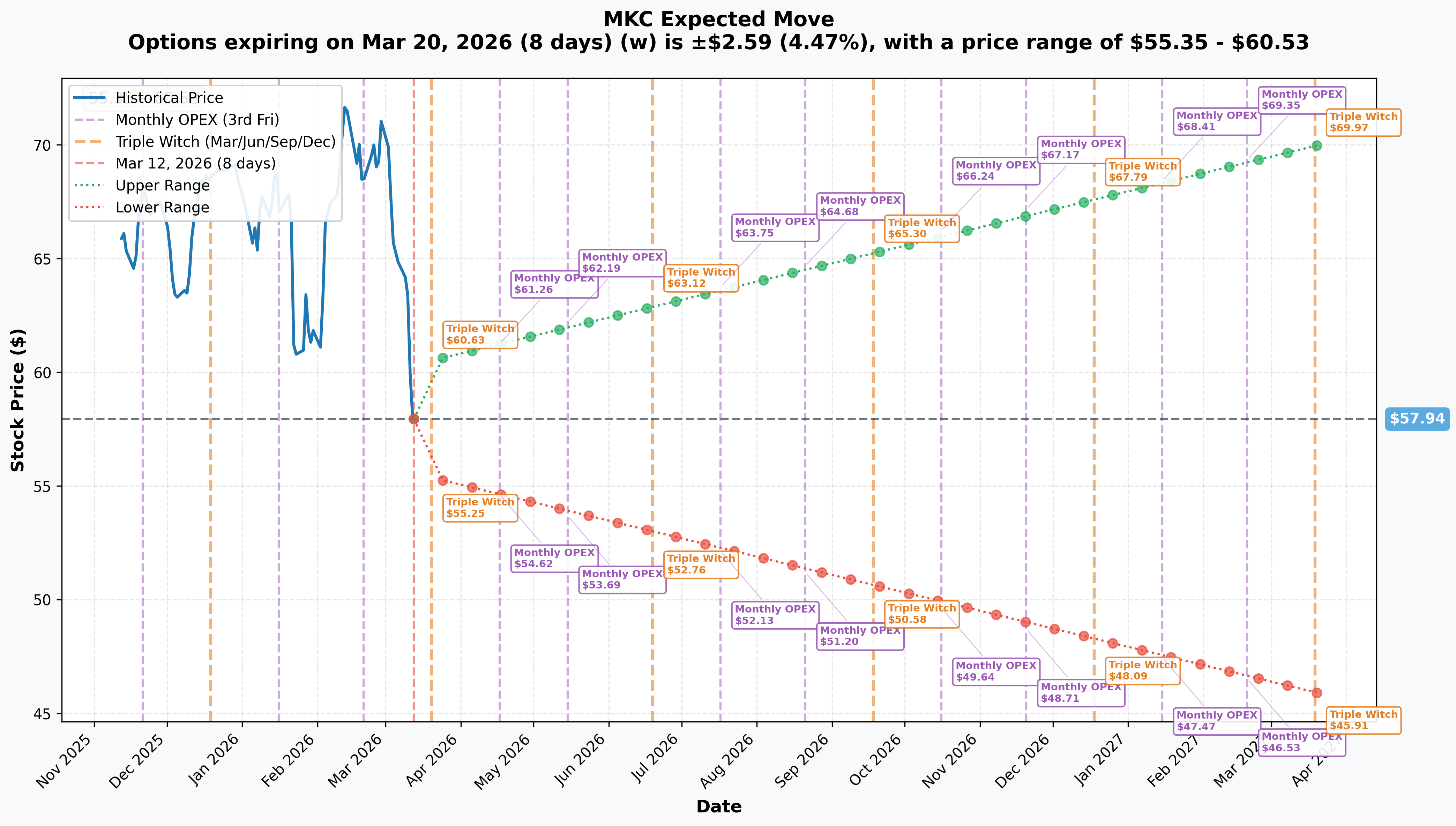

Implied Move Analysis

The options market is pricing the following moves for upcoming expirations:

| Expiration | Event | Implied Move | Range |

|---|---|---|---|

| Mar 20, 2026 | Monthly OPEX (Triple Witch) | ±4.47% / ±$2.59 | $55.35 – $60.53 |

| Apr 17, 2026 | April OPEX — THIS TRADE | ±11.4% / ±$6.64 | $54.62 – $61.26 (approx.) |

| Mar 2027 | Yearly LEAPs | ±20.76% / ±$12.03 | $45.91 – $69.97 |

Translation: The market is pricing about a 4.5% move through March 20 Triple Witch expiration — a relatively tight range of $55.35 to $60.53. That means the gamma levels at $55 and $60 align almost perfectly with the implied move floor and ceiling over the next 8 days. The April 17 expiration — where today's trade was positioned — bakes in a wider swing of roughly $54.62 to $61.26, capturing the full Q1 earnings event on March 31.

Key insight: The $65 put was comfortably outside the implied move upper range for April. With the stock at $57.94, the April implied move doesn't price any path back to $65 in the next 36 days. The trader who closed this position was sitting on intrinsic value gains and made a rational choice to exit before earnings volatility could cut that value either way.

🎪 Catalysts

🔥 Upcoming Catalysts (Near-Term)

Q1 FY2026 Earnings Report — March 31, 2026 (19 Days Away) 📊

This is the single most important near-term catalyst for MKC. McCormick confirmed the Q1 earnings date as before market open on March 31, 2026.

Q1 FY2026 (fiscal quarter ending February 28, 2026) will be the first quarter to fully consolidate McCormick de Mexico — the 25% stake acquired for $750M in the JV with Grupo Herdez, closed January 2, 2026. That acquisition adds approximately $810M in annual sales and is expected to contribute 11–13% to reported net sales growth.

Key items the market will be watching:

- 📊 Consensus Revenue: ~$1.79B (MarketBeat)

- 💰 Consensus EPS: $0.62–$0.69

- 🌮 Mexico consolidation: Does the acquired business contribute as guided?

- 📉 Gross margin trajectory: After a 120-bps decline in Q4 FY2025, any stabilization would be welcome

- 🚨 Tariff mitigation progress: Management committed to a $50M incremental tariff headwind in FY2026 — how much have they offset through pricing and alternative sourcing?

- 📈 Full-year guidance: Any revision to the $3.05–$3.13 adjusted EPS guidance range

Annual Shareholder Meeting — April 2026

McCormick confirmed its 2026 Annual Shareholder Meeting for April 2026.

📅 Recent Catalysts (Past 3 Months)

January 22, 2026 — FY2025 Earnings Report (Already Happened)

MKC reported Q4 and full-year FY2025 results on January 22:

- FY2025 Net Sales Growth: +2% organic ✅

- Q4 Adjusted EPS: $0.86 (missed consensus of $0.87 by $0.01) ❌

- FY2026 Adjusted EPS Guidance: $3.05–$3.13 (below prior Street consensus) ❌

- Shares fell approximately 5.8% in pre-market on the guidance miss

January 2, 2026 — McCormick de Mexico Acquisition Closed

McCormick completed the $750M acquisition of an additional 25% stake in McCormick de Mexico from Grupo Herdez, bringing its ownership to 75% in the joint venture formed in 1947. The business generates ~$810M/year in net sales. The deal was announced August 21, 2025 and closed January 2, 2026.

February 17, 2026 — CAGNY Conference Presentation

CEO Brendan Foley and CFO Marcos Gabriel presented McCormick's "Flavor-Driven Growth Strategy" at the Consumer Analyst Group of New York conference, reaffirming long-term targets of 4–6% net sales growth, 7–9% operating income growth, and 8–11% EPS growth.

March 11, 2026 — Zacks Downgrades to "Strong Sell"

Zacks Research downgraded MKC to "Strong Sell" on March 11, 2026 — one day before this options trade. This downgrade added pressure to a stock already sitting near its 52-week low, and provides important context for why a bearish put position had been accumulated in the first place.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and the March 31 earnings catalyst:

📈 Bull Case (25% probability) — Target: $62–$65

How we get there:

- ✅ Q1 FY2026 earnings beat on revenue with Mexico contributing as guided

- ✅ Management provides early evidence that the $50M tariff headwind is being mitigated better than feared

- ✅ Gross margin shows stabilization or early signs of recovery (vs. the 120-bps Q4 decline)

- ✅ Full-year EPS guidance maintained or narrowed to the top of $3.05–$3.13 range

- 📈 Relief rally targets the $60 gamma resistance level first, then potential extension toward $65 (which has 2.51 total GEX — the heaviest resistance level)

Why only 25%: The stock needs a meaningful positive earnings surprise to overcome active Zacks "Strong Sell" downgrade, HSBC and UBS price target cuts, and the weight of a -27% YTD drawdown. The average analyst price target of ~$73–$75 implies potential upside, but the path requires execution on multiple fronts simultaneously.

🎯 Base Case (50% probability) — Target: $55–$60 (Sideways Chop)

Most likely scenario:

- ✅ Earnings meet lowered expectations — revenue around $1.79B, EPS in the $0.62–$0.69 range

- ⚖️ Mexico consolidation adds revenue as guided but with fair-value inventory step-up costs that pressure margins in the near term

- 📊 Tariff headwind acknowledged but not measurably better than feared

- 🔄 Stock trades in the implied move range of $54.62–$61.26 through April expiration

- 💤 The closed $65 put trade reflects this outcome — the position was opened when MKC was higher, played out with MKC falling well below $65, and is now being exited because further downside through earnings is uncertain

Why 50%: MKC is a Dividend Aristocrat with a dominant market position. Consumer volumes have increased for seven consecutive quarters. The stock has already priced in a lot of bad news from $80 down to $58. A "nothing changes" outcome likely means rangebound behavior between $55 gamma support and $60 gamma resistance.

📉 Bear Case (25% probability) — Target: $52–$55

What could go wrong:

- 😰 Q1 earnings disappoint — Mexico integration costs are higher than flagged, gross margin declines further

- ❌ Management cuts full-year EPS guidance below $3.05 lower end

- 🚨 Tariff exposure escalates (U.S.–Mexico trade tensions are genuinely unpredictable given the size of the Mexico business post-acquisition)

- 📉 Break below $57 current support accelerates toward the $55 gamma floor (put GEX 0.61)

- 🐻 Institutional sellers continue distribution; former CEO insider selling pattern extends

Critical support to watch: $55.00 is the strongest nearby put gamma level. A sustained break below $55 opens the door to the lower end of the April implied move at $54.62 and beyond.

💡 Trading Ideas

🛡️ Conservative: Dividend Accumulation at Support — "Sleep Well Strategy"

Play: Buy MKC shares on any dip toward the $55 gamma support level; collect the dividend while waiting for the earnings catalyst to clarify direction

Why this works:

- 🛡️ $55 represents the strongest nearby support per gamma data, and it aligns with the March 20 implied move lower bound ($55.35)

- 💰 At $55, MKC would yield approximately 3.5% annually on the $1.92/share dividend — not bad for a 137-year-old company on its 40th consecutive year of dividend increases

- 📊 Analyst consensus price target of $73–$76 implies 30–40% upside from $55 levels

- 🎯 Risk is defined: set a mental stop at $52 (below the April implied move floor)

Sizing: No more than 2–4% of portfolio at current uncertainty levels; consider averaging in if earnings disappoint and the stock overshoots lower

Risk level: Lower (stock position, not options) | Skill level: Beginner-friendly

Expected outcome: Dividend income while waiting for the post-earnings recovery narrative to develop over H1 2026

⚖️ Balanced: Bull Call Spread After Earnings — "Wait for the Dust to Settle"

Play: After March 31 earnings, buy a call spread targeting recovery toward $60 resistance

Structure: Buy MKC May $58 Call / Sell MKC May $62 Call (approximately 45–50 days to expiration post-earnings)

Why this works:

- ⏰ Entering after earnings eliminates the binary event risk; let the print happen first, then assess

- 📉 Implied volatility will likely crush post-earnings, making call spreads meaningfully cheaper than today

- 🎯 A $58–$62 spread targets the implied move range upper end and the first gamma resistance level at $60

- 💰 Defined risk: maximum loss is the net debit paid; maximum gain is the width of the spread (~$4 per spread = $400 per contract)

Estimated cost: Approximately $1.50–$2.00 net debit post-earnings IV crush (vs. potentially $2.50–$3.00 today pre-earnings)

Entry criteria: Only enter if the stock holds above $55 after earnings (confirms support is intact) and the earnings report doesn't include a further EPS guidance cut below $3.00

Risk level: Moderate (defined risk, requires correct direction) | Skill level: Intermediate

🚀 Aggressive: Short-Term Earnings Strangle — "Bet on the Move, Not the Direction"

Play: Before March 31 earnings, buy an OTM call and OTM put to profit from any large move in either direction

Structure: Buy MKC April 17 $62 Call + Buy MKC April 17 $54 Put (approximately 19 days to expiration; straddle/strangle around current price and implied move extremes)

Why this could work:

- 💥 The April implied move range is $54.62–$61.26. A strangle positioned just outside those bounds benefits if the actual earnings move is larger than the market expects

- 📊 MKC has moved 5.8% on the last earnings print (January 22) — if Q1 surprises in either direction, the strangle profits

- 🎰 With the Zacks "Strong Sell" on one side and a Dividend Aristocrat with 26% market share on the other, there's a legitimate argument the market is underestimating the range of outcomes

Why this could blow up (SERIOUS RISKS):

- 💸 Theta decay: With 19 days to earnings, time decay is working against you from day one

- 😱 IV crush post-earnings: Even if MKC moves 5%, implied volatility collapsing from elevated pre-earnings levels to normal levels could still result in a net loss on both legs

- ⚠️ MKC is a Consumer Staples stock: It doesn't typically move 10–15% on earnings; the $57.94 stock rarely gaps violently in either direction

- 📉 If MKC trades flat post-earnings, you could lose 50–80% of the premium paid on both legs

Estimated P&L:

- 💰 Cost: Approximately $2.50–$3.50 combined net debit (both legs together)

- 📈 Profit scenario: MKC moves to $63+ or $52– on earnings = meaningful gain on one leg

- 📉 Loss scenario: MKC stays in $56–$60 range = lose most or all of premium

DO NOT attempt unless you understand IV crush mechanics and can afford to lose the full premium.

Risk level: High (can lose 100% of premium on both legs) | Skill level: Advanced only

⚠️ Risk Factors

What could go wrong — honestly:

-

⏰ Q1 earnings binary event (March 31): This is 19 days away and represents the biggest near-term risk to any MKC position. If gross margins disappoint further or the $3.05–$3.13 EPS guidance gets cut, the stock could test new lows below $55. If the Mexico consolidation contributes more costs than revenue in Q1, the reaction could be sharp.

-

🚨 Tariff and trade policy risk: MKC has flagged a $50M incremental tariff headwind in FY2026, up from the $70M gross exposure they reduced to $20M net in FY2025. With the Mexico acquisition, McCormick now has deeper exposure to U.S.–Mexico trade dynamics. Supply Chain Dive has covered how tariff escalation could push that number higher than forecast.

-

🇲🇽 Mexico acquisition integration: The $750M deal to acquire a 25% incremental stake in McCormick de Mexico is transformational, but it introduces fair-value inventory step-up costs, Mexican peso currency exposure, and execution risk in the near term. Any shortfall in the expected 11–13% top-line contribution would pressure guidance.

-

📉 Below-consensus EPS guidance already set: The FY2026 adjusted EPS guidance of $3.05–$3.13 already came in below prior Street consensus. A further cut would likely drive additional institutional selling. Zacks "Strong Sell" downgrade on March 11 followed by a Jefferies Buy rating ($81 target) shows the analyst community is genuinely split.

-

🏪 Private label competition: The most persistent structural risk to McCormick's consumer business is retailer store brands. In a consumer price-sensitivity environment, trade-down to private label in the spice aisle is a real and ongoing threat. Morningstar has noted that McCormick must continue investing in innovation and marketing to maintain its premium positioning.

-

👤 Insider selling: Former CEO Lawrence Kurzius sold 100,000 shares across two tranches in January and February 2026 totaling approximately $7.16M. While these may reflect routine financial planning, large insider sales near a multi-year price low are worth noting.

-

💧 Flavor Solutions volume softness: Flavor Solutions volumes softened late in FY2025 despite strong profit improvement. If QSR customers continue cutting promotional activity, this segment — a key growth engine beyond Mexico — could underperform. Yahoo Finance covers the Q4 earnings call dynamics in detail.

🎯 The Bottom Line

Here's the deal: Today's $6.4M options transaction is not a new bearish bet — it's a closing of an old one. The trader who held $65 puts on MKC came into this week with a winning position (MKC at $57.94 means those puts are deep in the money), and they chose to exit before March 31 Q1 earnings rather than hold for potentially more downside.

What this tells us:

- 👀 Someone sophisticated enough to build an 8,300-contract put position is now satisfied with the bearish trade's outcome and isn't pressing further downside bets into earnings

- 🎯 The $65 strike — which coincides with the heaviest gamma resistance in the GEX data (2.51 total GEX) — is now being cleared out as an overhang on the options market

- ⚖️ This doesn't make MKC a buy automatically. But it does remove one meaningful bearish positioning signal from the tape

If you already own MKC:

- ✅ The $55 gamma support level is your first line of defense — watch that level heading into and through March 31 earnings

- 💰 The 40th consecutive year of dividend increases and 7 consecutive quarters of consumer volume gains are real anchors; this isn't a structurally broken company

- 📅 Mark March 31 on your calendar — Q1 earnings before market open is the next big inflection point

If you're watching from the sidelines:

- ⏰ Do not initiate new positions before March 31 earnings — the implied move of ±$6.64 through April 17 expiration means the market is expecting a real move

- 🎯 A post-earnings hold of $55–$57 with improving gross margin commentary would be a healthier entry point than chasing it before the print

- 📊 The analyst consensus target of ~$73–$76 implies 26–31% upside from current levels if the thesis plays out — but that's a 12-month view, not a 2-week one

If you're still bearish:

- 🐻 The $55 gamma support and the April implied move lower bound of ~$54.62 are the key levels to watch

- ⚠️ With the large put position now closed, options market structure is slightly less bearish than it was yesterday — one less headwind for the bulls

- 📉 A break below $55 on meaningful volume, particularly on disappointing earnings, would be the next meaningful bearish signal

Final thought: McCormick has a 26% domestic market share in spices, 40 straight years of dividend growth, and now $810M in annual sales added via McCormick de Mexico. The bears had a strong case from $80 down to $58, and someone just took $6.4M off the table to prove it. The question for the next chapter is whether the Mexico acquisition and clean-label reformulation tailwind (McCormick is actively benefiting from food companies racing to remove synthetic dyes) give the bulls something to work with at these prices.

Patient investors will let March 31 provide the answer.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational and informational purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Past performance does not guarantee future results. The unusual options activity described here reflects observed market data and represents one possible interpretation of market participants' activity — it does not imply any trade will be profitable or that you should replicate it. Always do your own research and consider consulting a licensed financial advisor before making investment decisions. Earnings events create binary risk with the potential for significant price gaps in either direction. Position sizing and risk management are your responsibility.