NFLX Massive $104M Call Spread Roll - Smart Money Repositioning Post-Earnings!

January 22, 2026 | Unusual Activity Detected

The Quick Take

Institutional players just moved $104 MILLION in NFLX options today, rolling their August call positions into September expirations while collecting premium. This is NOT a bullish or bearish bet - it's sophisticated portfolio management 2 days after Netflix's Q4 earnings beat. With NFLX trading at $83.24 (down ~30% from 2025 highs) and the massive $72 billion Warner Bros. Discovery acquisition pending, smart money is extending their exposure while locking in some profits. Translation: They're playing the long game through the April WBD shareholder vote!

Company Overview

Netflix (NFLX) is the world's largest streaming entertainment service with over 325 million global subscribers:

- Market Cap: $362.1 Billion

- Industry: Services - Video Streaming

- Current Price: $83.24 (near 52-week low of $82.11)

- Primary Business: Netflix's business model involves its streaming service, operating the biggest television entertainment subscriber base globally with strong positions in both U.S. and international markets.

The Option Flow Breakdown

The Tape (January 22, 2026):

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:51:09 | NFLX | SELL | CALL | 2026-09-18 | $34M | $100 | 122K | - | 122,000 | $83.24 | - | NFLX20260918C100 |

| 12:51:09 | NFLX | SELL | CALL | 2026-08-21 | $17M | $110 | 73K | - | 73,000 | $83.24 | - | NFLX20260821C110 |

| 12:51:09 | NFLX | SELL | CALL | 2026-09-18 | $12M | $120 | 121K | - | 121,000 | $83.24 | - | NFLX20260918C120 |

| 12:51:09 | NFLX | SELL | CALL | 2026-08-21 | $6M | $130 | 71K | - | 71,000 | $83.24 | - | NFLX20260821C130 |

| 10:31:57 | NFLX | SELL | CALL | 2026-09-18 | $9.4M | $120 | 50K | - | 50,000 | $83.24 | - | NFLX20260918C120 |

| 10:31:57 | NFLX | BUY | CALL | 2026-09-18 | $26M | $100 | 50K | - | 50,000 | $83.24 | - | NFLX20260918C100 |

What This Actually Means

This is a complex position roll and restructure happening right after Q4 earnings! Here's the breakdown:

Morning Session (10:31:57):

- Bull Call Spread: Bought $100 strike calls ($26M), Sold $120 strike calls ($9.4M) = NET $16.6M bullish bet

- Expiration: September 18, 2026 (Triple Witch)

- Max profit potential: $20 per share if NFLX above $120 at expiration

Afternoon Session (12:51:09):

- Closing August positions: Selling $110 calls ($17M) and $130 calls ($6M) to close - this is taking profits/exiting

- Opening new September positions: Selling $100 calls ($34M) and $120 calls ($12M) - premium collection or covered call writing

- Combined volume: 487,000+ contracts representing control of 48.7 MILLION shares!

Unusual Score Analysis:

- $100 strike September: Z-Score 1184.8 (EXTREMELY UNUSUAL - happens a few times per YEAR)

- $120 strike September: Z-Score 558.85 (EXTREMELY UNUSUAL)

- High activity ratios (33-81x normal volume) suggest this is a single institutional player or coordinated hedge fund activity

Translation for regular folks: Someone managing a MASSIVE Netflix position is restructuring their exposure after earnings. They're closing August calls (taking profits from existing positions) and opening September calls through the WBD shareholder vote in April. This is sophisticated portfolio management, not a directional bet.

Technical Setup / Chart Check-Up

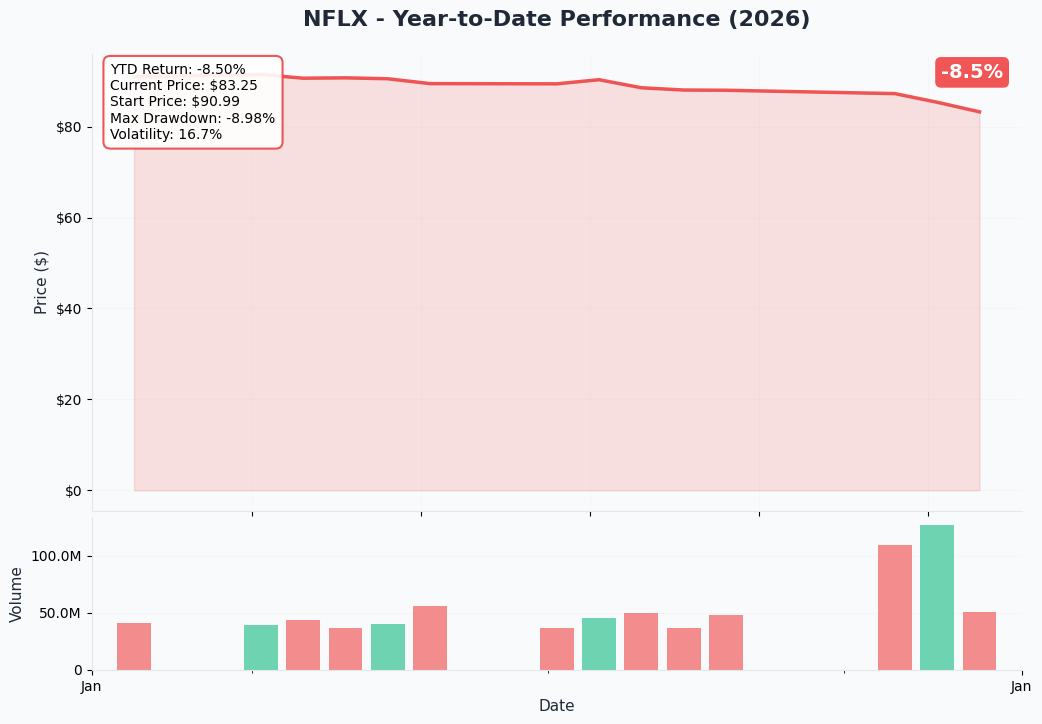

YTD Performance Chart

Netflix has been on a ROUGH ride - currently trading at $83.24, down nearly 30% from its 2025 high of $134.12 reached in June. The stock is forming what technical analysts call a "Death Cross" pattern, trading below both its 50-day and 200-day moving averages according to XTB's analysis.

Key observations:

- Current price sitting near 52-week low of $82.11

- Significant decline from $134.12 highs on WBD acquisition concerns

- Q4 earnings beat failed to spark meaningful rally

- Technical indicators suggest continued near-term weakness

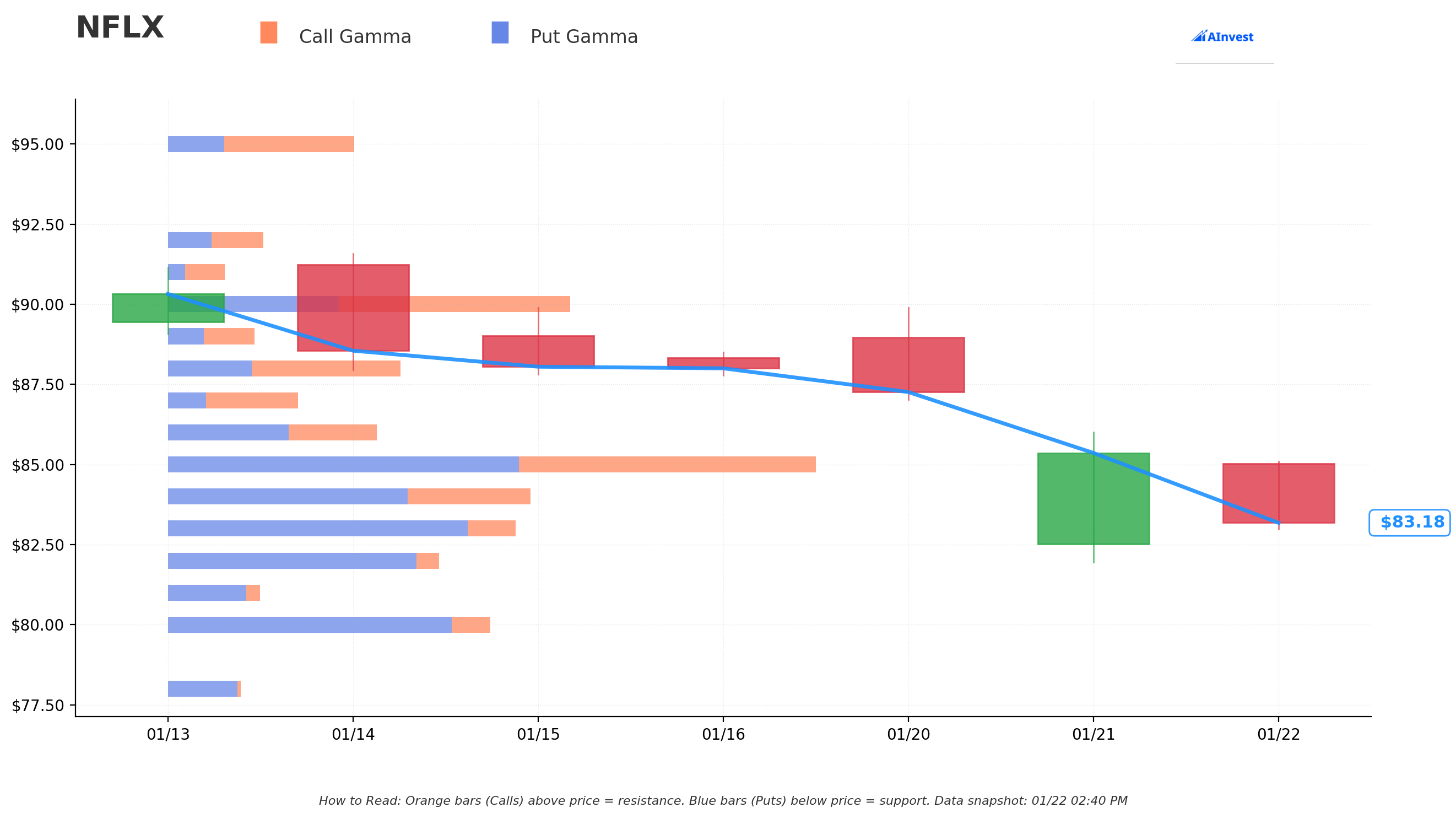

Gamma-Based Support & Resistance Analysis

Current Price: $83.24

The gamma exposure map reveals critical price levels where market maker hedging creates natural support and resistance:

Support Levels (Put Gamma Below Price):

- $83 - IMMEDIATE support with 45.0B total gamma exposure (0.28% below current - critical floor!)

- $82 - Secondary support at 35.0B gamma (1.48% below)

- $80 - Major structural floor with 41.8B gamma (3.89% below - if this breaks, watch out!)

Resistance Levels (Call Gamma Above Price):

- $84 - Immediate ceiling with 47.7B gamma (0.92% above - first hurdle)

- $85 - Secondary resistance at 85.6B gamma (2.12% above - STRONGEST LEVEL)

- $86-$88 - Moderate resistance zone

- $90 - Key psychological level with 55.3B gamma (8.13% above)

- $95 - Extended upside target at 24.7B gamma (14.13% above)

Net GEX Bias: BEARISH (305.9B call gamma vs 385.0B put gamma)

What this means for traders: NFLX is pinned in a tight range between $83 support and $85 resistance. The gamma data shows overwhelming put positioning below current price, creating a "magnet" effect that pulls the stock lower. The $85 level with 85.6B gamma is THE critical resistance - breaking above that could trigger a squeeze to $90. But right now, the path of least resistance is sideways to lower.

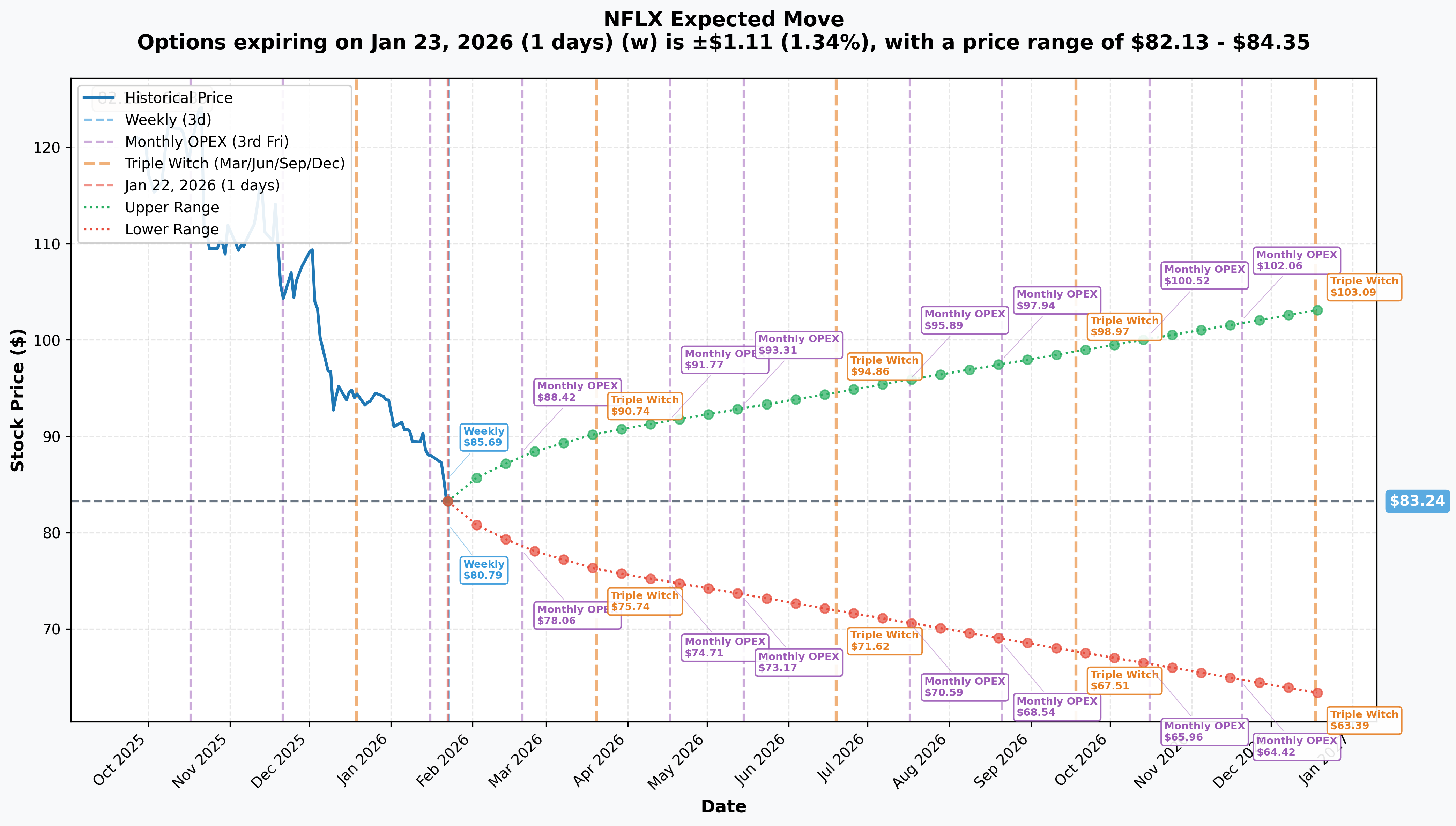

Implied Move Analysis

Options market pricing for upcoming expirations:

| Timeframe | Expiry Date | Days | Implied Move % | Range |

|---|---|---|---|---|

| Weekly | 2026-01-23 | 1 | +/- 1.34% | $82.13 - $84.35 |

| Monthly OPEX | 2026-02-20 | 29 | +/- 5.84% | $78.38 - $88.10 |

| Triple Witch | 2026-03-20 | 57 | +/- 8.50% | $76.16 - $90.32 |

| September Witch | 2026-09-18 | 239 | ~+/- 19% | $67.51 - $98.97 |

| LEAPS | 2026-12-18 | 330 | +/- 23.84% | $63.39 - $103.09 |

Translation for regular folks: Options traders are pricing in relatively LOW near-term volatility (only 1.34% this week) now that earnings are behind us, but SIGNIFICANT uncertainty through September expiration when these massive trades are positioned. The September 18th expiration (where most of today's activity is concentrated) has implied range of roughly $67.50 to $99 - that's a 38% spread!

The positioning in $100-$120 strikes makes sense: institutions are betting NFLX can recover to the implied upper range ($99-$103) by September, which would be roughly 20% upside from here.

Catalysts

Already Happened (Recent Past)

Q4 2025 Earnings - January 20, 2026 (2 DAYS AGO)

Netflix reported Q4 results that beat expectations on January 20, 2026:

- Revenue: $12.05B vs $11.97B consensus (+16.7% YoY) - BEAT

- EPS: $0.56 vs $0.55 consensus - BEAT by 1.82%

- Global Paid Subscribers: 325 million (up ~23M from 301M at end of 2024)

- Ad Revenue (Full Year 2025): $1.5B (up 2.5x from 2024) - first-ever ad revenue disclosure

- Full Year 2025 Revenue: $45.2B (+16% YoY)

- Operating Profit Growth: 30% in FY 2025

- Free Cash Flow 2025: ~$9 billion

Why the stock hasn't rallied: Despite the beat, analysts note the 2026 outlook "spooked investors" - guidance for 12-14% revenue growth represents a slowdown from 2025's 16%. The massive WBD acquisition overhang continues to pressure shares.

Warner Bros. Discovery Acquisition - Announced December 2025

Netflix's $72 billion all-cash acquisition of Warner Bros. Discovery is the elephant in the room:

- Deal Value: $82.7B enterprise value ($72B equity at $27.75/share)

- Assets: HBO Max streaming, Warner Bros. film studios

- Margin Impact: Management flagged ~0.5 percentage point drag on operating margins in 2026

- Several analysts downgraded post-announcement, with Pivotal Research calling the deal "expensive"

Upcoming Catalysts (What To Watch)

WBD Shareholder Vote - Expected April 2026

This is THE catalyst that explains today's September positioning! The WBD shareholder vote expected in April 2026 will determine if this transformative deal proceeds:

- Regulatory Status: U.S. and European authorities have signaled concerns about market power, creative concentration, and consumer impact

- Competing Interest: Paramount Skydance launched hostile effort to acquire all of WBD

- Binary Outcome: Deal approval = potential relief rally; Deal blocked = uncertainty continues

Q1 2026 Earnings - Expected April 16, 2026

Next earnings report expected April 16, 2026 will be crucial:

- Consensus EPS: $0.55

- Key metrics: Ad revenue trajectory toward $3B goal, subscriber retention post-price increases, WBD integration cost updates

Price Increases Throughout 2026

Netflix noted "increases in membership and pricing" expected in 2026 - specific countries and timing not disclosed. Current U.S. pricing after January 2025 increase:

- Ad-supported: $7.99/month

- Standard: $17.99/month

- Premium: $24.99/month

Advertising Product Launches - Q2 2026

New ad formats rolling out globally:

- Interactive Video Ads: Testing in U.S./Canada, global Q2 2026

- Pause Ads and Interactive Mid-Rolls: Powered by generative AI

- Ad revenue target: ~$3B for 2026 (doubling from $1.5B)

Major Content Releases 2026

Strong content slate ahead according to Netflix Life:

- Bridgerton Season 4: January/February 2026 (two parts)

- Beef Season 2: April 16, 2026 (Oscar Isaac, Carey Mulligan)

- Narnia (Greta Gerwig): 2026

- The Witcher Final Season: 2026

- One Piece Season 2: 2026

Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timeline, here are the scenarios through September 18th expiration:

Bull Case (30% probability)

Target: $100-$120

How we get there:

- WBD shareholder vote APPROVES deal in April - removes major overhang

- Regulatory concerns resolved favorably in U.S. and Europe

- Ad revenue tracking toward $3B target validates monetization thesis

- Price increases stick without meaningful subscriber churn

- Content slate (Bridgerton, Beef S2) drives engagement growth

- Stock breaks above $85-$90 gamma resistance, triggering technical rally

Key metrics needed:

- Q1 2026 revenue growth maintaining 12%+ trajectory

- Ad tier reaching 200M+ monthly active users

- Operating margins stable despite WBD integration costs

- Successful integration roadmap presentation

Why this matches the trade: The September $100-$120 call spread structure positions for this exact scenario - capturing upside if NFLX recovers to pre-acquisition levels.

Base Case (45% probability)

Target: $78-$90 range (Choppy Consolidation)

Most likely scenario:

- WBD deal progresses but with regulatory conditions/delays

- Earnings meet expectations without major surprises

- Stock oscillates between gamma support ($80-$83) and resistance ($85-$90)

- Market waits for deal clarity before meaningful re-rating

- Implied volatility gradually declines as uncertainty resolves

- Stock ends September between implied move bounds ($76-$90)

This is why institutions are rolling positions: They expect sideways chop for several months while waiting for deal clarity. By extending to September, they capture any eventual upside while collecting premium in the meantime.

Bear Case (25% probability)

Target: $65-$78

What could go wrong:

- WBD deal BLOCKED or significantly restructured by regulators

- Competing Paramount bid creates prolonged uncertainty

- Subscriber growth disappoints amid competition from Disney+ bundle

- Ad revenue ramp slower than projected

- Integration costs higher than expected

- Macro weakness impacts consumer discretionary spending

- Stock breaks below $80 gamma support, cascading to $75-$70 levels

Critical support levels:

- $83: Immediate floor (gamma support)

- $80: Major structural support - MUST HOLD

- $76: Extended implied move lower bound through March

- $67.50: September implied move lower bound - disaster scenario

Trading Ideas

Conservative: Wait and Watch Until April

Play: Stay on sidelines until WBD shareholder vote clarity

Why this works:

- Binary event risk (deal approval/rejection) creates asymmetric outcomes

- Stock near 52-week lows offers limited near-term downside buffer

- Implied volatility will remain elevated until deal resolved

- Better entry likely post-vote if deal approved (buy the confirmation)

- If deal rejected, catch falling knife at $65-70 support

Action plan:

- Mark calendar for April 2026 WBD shareholder vote

- Watch Q1 earnings April 16 for execution metrics

- Look for entry on pullback to $75-78 gamma support zone

- Or wait for breakout above $90 to confirm bull trend

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Balanced: Sell Cash-Secured Puts at Support

Play: Sell $75 puts expiring April/May to collect premium or get shares at discount

Structure: Sell NFLX $75 puts (April 17 expiration)

Why this works:

- $75 strike is below current price AND below key gamma support at $80

- Elevated IV means rich premium (likely $4-6 per contract)

- If assigned, you own NFLX at ~$69-71 effective cost (near implied move lower bound)

- If stock stays above $75, keep entire premium (~7% return on capital)

- Timing captures WBD vote - get paid to wait for clarity

Estimated P&L:

- Collect: ~$4-6 premium per contract ($400-600 per 100 shares)

- Breakeven: ~$69-71 (excellent entry if assigned)

- Max profit: Premium collected if NFLX above $75 at expiration

- Capital required: $7,500 per contract (cash-secured)

Risk level: Moderate (stock ownership risk) | Skill level: Intermediate

Aggressive: Follow The Institutional Flow - September Call Spread

Play: Replicate the institutional bull call spread

Structure: Buy NFLX $100 calls, Sell NFLX $120 calls (September 18 expiration)

Why this could work:

- Following $26M+ institutional positioning (smart money)

- 239 days to expiration captures WBD vote, two earnings cycles, and content releases

- Defined risk spread with known max loss

- Stock needs to rally ~20% to $100 strike - achievable if deal approved

- Max profit at $120+ would be ~44% rally - ambitious but possible in recovery scenario

Why this could blow up:

- Stock currently $83, needs significant rally just to reach $100 strike

- Deal rejection could send stock to $65-70, making calls worthless

- Time decay works against you over 239 days

- Need to be RIGHT on both direction AND timing

Estimated P&L:

- Cost: ~$8-12 per spread ($800-1,200 per spread)

- Max profit: $20 per spread (if NFLX above $120) - ~100-150% ROI

- Max loss: Full premium paid if NFLX below $100 at expiration

- Breakeven: ~$108-112

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

Risk Factors

Don't get caught by these potential landmines:

-

WBD acquisition binary outcome: The $72 billion deal faces regulatory scrutiny from U.S. and European authorities concerned about market power and creative concentration. Deal rejection or significant restructuring could trigger 15-20% selloff. Competing Paramount Skydance hostile bid adds complexity.

-

Valuation concerns persist: Despite 30% decline from highs, NFLX still trades at 43.94x P/E which analysts consider expensive relative to earnings. Price-to-book ratio of 15.47 elevated. WACC at 11.43% increases cost of capital for acquisitions.

-

Growth deceleration: 2026 revenue guidance of 12-14% growth represents slowdown from 2025's 16%. Currency-neutral growth (11-13%) below prior year. Market already pricing in slower trajectory.

-

Competition intensifying: Disney+ combination with Hulu now exceeds Netflix's U.S. market share at 25% combined. Netflix lost 1 percentage point U.S. share in Q3 2025. Amazon Prime Video's e-commerce integration provides competitive advantage.

-

Integration execution risk: WBD integration presents significant operational complexity. Cultural integration of legacy Hollywood studio with tech-first Netflix uncertain. Expected 0.5 percentage point margin drag in 2026.

-

Technical weakness: Stock forming "Death Cross" pattern, trading below 50-day and 200-day moving averages. Near 52-week low of $82.11. Bearish gamma exposure suggests continued downward pressure.

-

Ad revenue execution: While targeting $3B in ad revenue for 2026 (doubling from $1.5B), Netflix trails established players like Disney which consistently generates over $3B annually. New ad formats need to prove effectiveness without alienating subscribers.

The Bottom Line

Real talk: Institutional investors just moved $104 MILLION in NFLX options 2 days after earnings, and the pattern tells a clear story: they're NOT abandoning Netflix, but they're extending their timeline and managing risk through the WBD deal uncertainty.

What this trade tells us:

- Smart money believes NFLX can recover to $100-$120 range, but NOT immediately

- They're willing to hold through September (239 days!) to capture eventual upside

- The August position closures show profit-taking from existing positions

- September positioning captures WBD shareholder vote, multiple earnings cycles, and content releases

- Z-scores of 558-1184x show this is HIGHLY unusual activity (happens a few times per year)

This is a "patience" signal, not a "panic" or "pile in" signal.

If you own NFLX:

- Consider holding through the WBD shareholder vote in April for clarity

- Set mental stop at $80 (major gamma support) to protect downside

- The institutions aren't selling - they're rolling forward, suggesting confidence in eventual recovery

- Current levels ($83) near 52-week lows offer limited downside vs potential upside post-deal

If you're watching from sidelines:

- April 2026 is the key date - WBD shareholder vote determines near-term direction

- Better entry likely if deal approved and stock breaks above $90 resistance

- Or catch pullback to $75-78 support zone with cash-secured puts

- Don't rush - 30% off highs is significant, but regulatory uncertainty warrants patience

If you're bearish:

- Stock already down 30% from highs - most of the bad news is priced in

- Shorting into 52-week lows is dangerous - risk/reward unfavorable

- If playing downside, use defined-risk put spreads ($80/$70) rather than naked shorts

- Watch for break below $80 gamma support as trigger for accelerated decline

Mark your calendar - Key dates:

- February 20 - Monthly OPEX (implied move: +/- 5.84%)

- March 20 - Triple Witch (implied move: +/- 8.50%)

- April 16 - Q1 2026 earnings expected

- April 2026 - WBD shareholder vote (THE catalyst!)

- September 18 - Triple Witch, expiration of $104M institutional positioning

Final verdict: Netflix's long-term story remains compelling - 325M subscribers, $9B free cash flow, doubling ad revenue, and the WBD acquisition could create an unmatched content powerhouse. BUT the stock is in "show me" mode until the deal receives regulatory approval. The $104M institutional positioning in September expirations tells you smart money expects a resolution and recovery - they're just giving it time to play out.

Be patient. Wait for the April vote. The smart money is playing the long game, and you should too.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-scores of 558-1184x reflect these specific trades' size relative to recent NFLX history - they do not imply the trades will be profitable or that you should follow them. Always do your own research and consider consulting a licensed financial advisor before trading. The WBD acquisition creates binary event risk that could result in significant stock price gaps in either direction.

About Netflix: Netflix is the world's largest streaming entertainment service with over 325 million global subscribers across 190+ countries. The company offers a wide variety of TV series, documentaries, feature films and mobile games across a wide variety of genres and languages, with a market cap of $362.1 billion in the Services - Video Streaming industry.