🏠 ABNB: Someone Just Bet $1.6M on Airbnb Breaking Out by February!

📅 December 19, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

A trader just loaded up on 2,500 call contracts betting $1.6 million that Airbnb explodes past $140 by February 20, 2026. This wasn't some retail YOLO - the z-score of 30.93 means this trade is 555x the average size for these contracts. With ABNB currently at $136.82 and facing a critical resistance test at $140, someone with deep pockets thinks the stock is about to break out. Let's dig into what they might know that we don't... 👀

💼 Company Overview

Airbnb, Inc. (ABNB) is the world's largest online alternative accommodation travel agency, pioneering the short-term rental revolution since 2008. The platform now extends beyond home rentals into boutique hotels, curated experiences, and in-home services - transforming from a simple booking site into a comprehensive travel ecosystem.

Key Stats:

- 💰 Market Cap: $81.24 billion

- 📊 Current Price: $136.82

- 🏢 Industry: Services to Dwellings & Other Buildings

- 🌍 Market Position: 44% global short-term rental market share (up from 28% in 2019)

💰 The Option Flow Breakdown

📊 What Just Happened

Here's the trade that caught everyone's attention this morning:

| Field | Details |

|---|---|

| Date/Time | December 19, 2025 at 11:45:15 AM |

| Ticker | ABNB |

| Trade Type | 🟢 BUY TO OPEN |

| Contract Type | 📞 CALL |

| Strike Price | $140.00 |

| Expiration | February 20, 2026 (63 days out) |

| Volume | 2,500 contracts |

| Premium | $1,600,000 ($1.6M) |

| Strategy | Long Call (Bullish Standalone) |

| Z-Score | 30.93 (EXTREMELY UNUSUAL) |

| Signal | OPEN (New Position) |

🤓 What This Actually Means

Translation for us regular folks:

This trader is betting $1.6 million that Airbnb climbs at least 2.3% from current levels ($136.82 → $140) by mid-February. But here's the kicker - they don't just need it to touch $140, they need it to blow past it to make real money.

The z-score of 30.93 is what makes this wild - it means this trade is 555 times larger than the typical bet on these exact contracts. This definitely isn't your neighbor Bob trading on Robinhood between meetings. 🐋

What makes this interesting:

✅ Size matters: $1.6M premium shows serious conviction ✅ Timing is everything: 63 days gives enough runway for catalysts to play out ✅ Strike selection: $140 is exactly where major gamma resistance sits ✅ Fresh position: This is a new bet, not rolling existing positions

The bullish case: This whale thinks one or more catalysts (Q4 earnings, buyback execution, new vertical traction) will push ABNB through resistance and into a sustained rally by February.

The skeptical view: They're paying hefty premium right into resistance - if ABNB stalls at $140, these calls could bleed theta quickly.

📈 Chart Check-Up

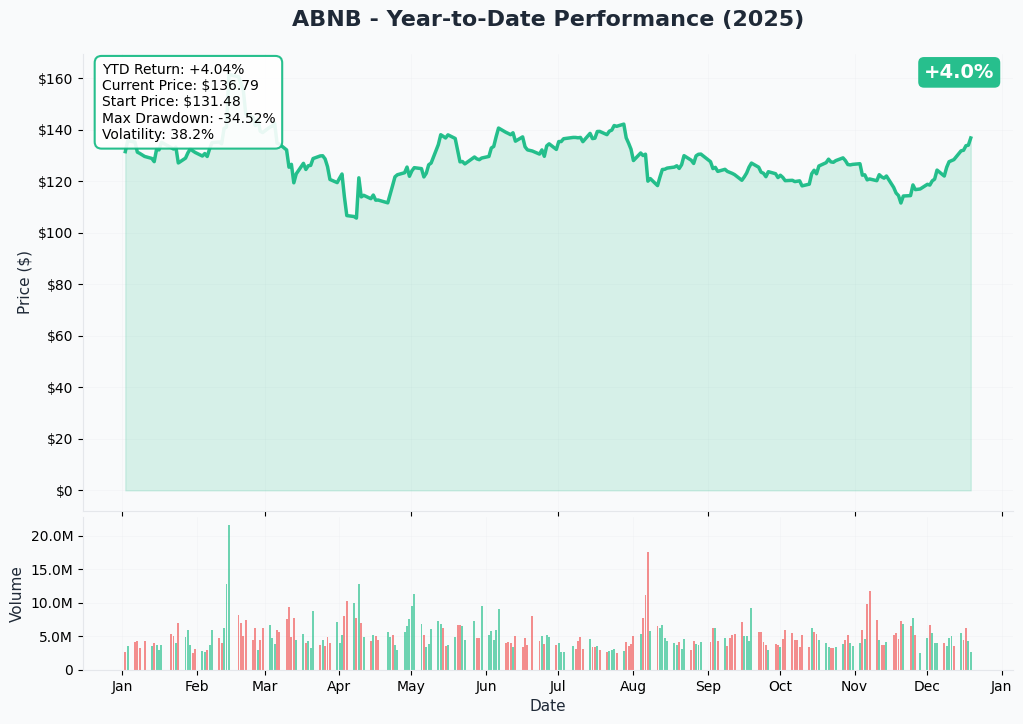

YTD Performance Analysis

What the chart tells us:

The year-to-date picture shows Airbnb's rollercoaster 2025. After testing lows near $100 earlier in the year (during the Q1 earnings growth scare), the stock has mounted a strong recovery, climbing 6 consecutive days recently and posting +11.4% gains over the past two weeks.

Currently trading at $136.82, ABNB sits just below the critical $140 resistance level - exactly where our whale placed their strike. The stock has been consolidating in the $130-140 range, setting up for either a breakout above $140 or a rejection back toward support.

Key Technical Observations:

- 📈 Momentum shift: 9 out of last 10 days green - bulls are gaining control

- 📊 Volume profile: Increasing buying pressure into the $135+ zone

- 🎯 Critical test: $140 represents both technical resistance AND psychological round number

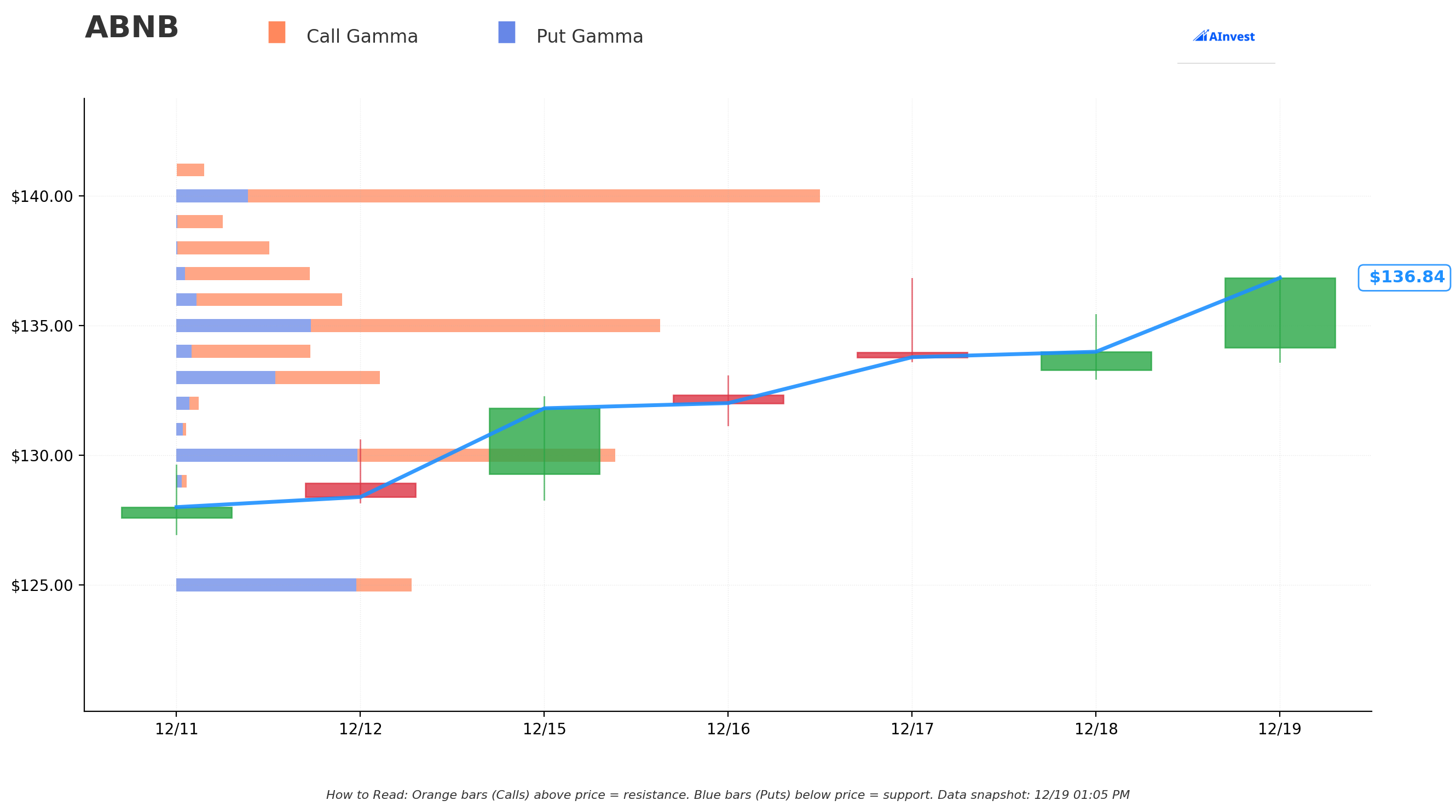

Gamma-Based Support & Resistance Analysis

Translation: This chart shows where options dealers have to buy (blue bars = support) and sell (orange bars = resistance) to hedge their positions. Think of it as a heat map of where price action tends to get "sticky."

Support Levels (Put Gamma - Blue Bars):

🔵 $135 - STRONG Support Major put gamma wall just below current price. If ABNB dips here, market makers will buy stock to hedge their short puts, creating natural buying pressure. This acts as a floor in the near-term.

🔵 $130 - STRONG Support Secondary support zone with heavy put positioning. A break here would be concerning, but significant buyer demand should emerge at this level.

Resistance Levels (Call Gamma - Orange Bars):

🟠 $140 - VERY STRONG Resistance This is THE level to watch - massive call gamma wall exactly at our unusual trade's strike price! As price approaches $140, dealers need to short stock to hedge their long calls, creating natural selling pressure. Breaking through this wall would trigger explosive upside as dealers flip to buying.

🟠 $145 - MODERATE Resistance Secondary resistance if ABNB clears $140. Less pronounced than the $140 wall, but still represents a speed bump for bulls.

What this means for our $140 call buyer: They're betting big that ABNB can break through the largest gamma wall on the board. If successful, the move could be violent to the upside. If not, they're fighting against structural dealer hedging flow.

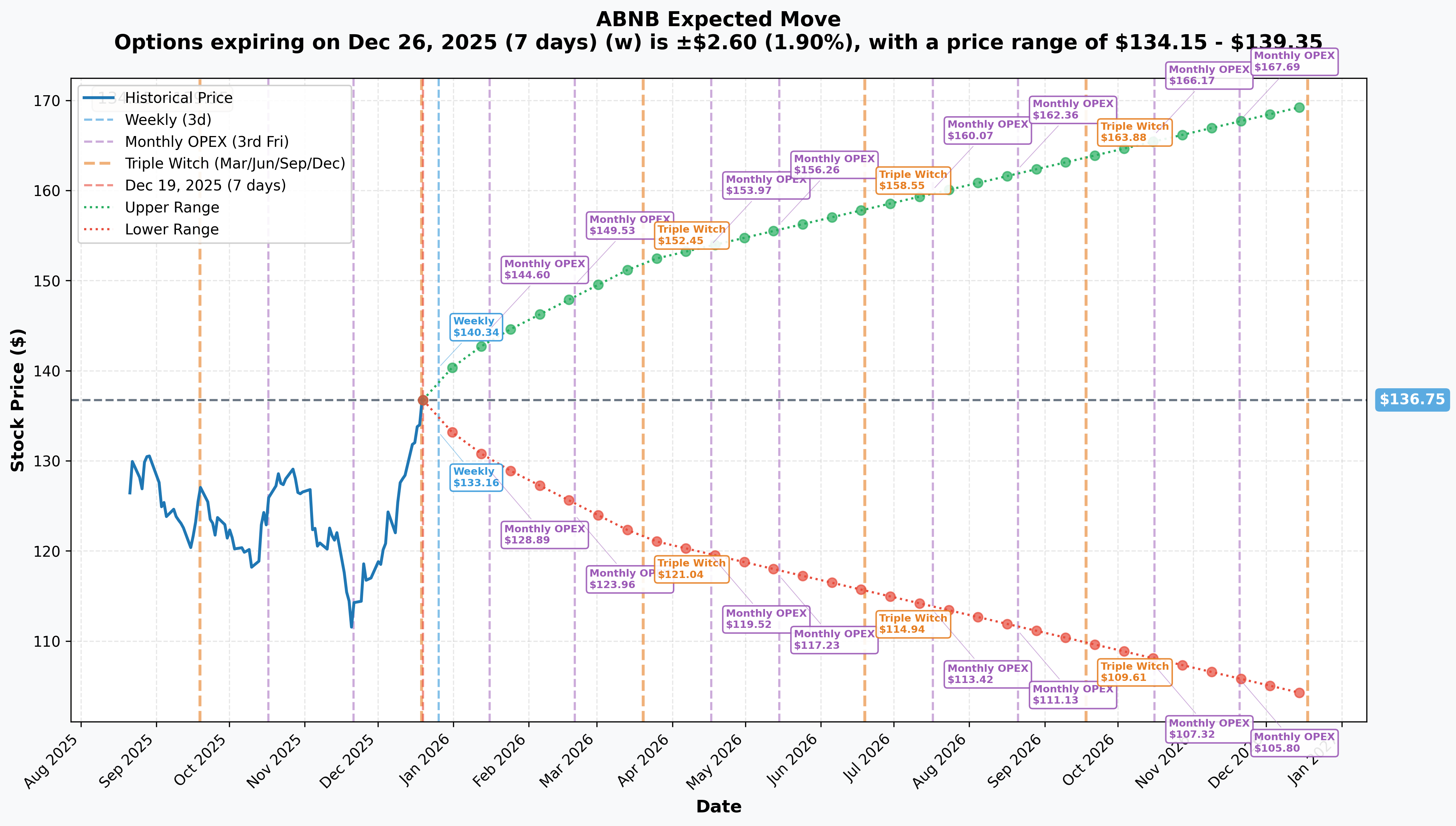

Implied Move Analysis

What the options market is pricing in:

The implied volatility surface tells us what kind of movement options traders are betting on:

📅 Weekly (Dec 26 OPEX): ±1.9% move Range: $134.15 - $139.35 Translation: Next week's expiration expects choppy, range-bound trading. No breakout anticipated in the immediate term.

📅 Monthly (Jan 16 OPEX): ±4.94% move Range: $129.99 - $143.50 Translation: By mid-January, options are pricing in a wider range that DOES include our $140 strike. The market sees a reasonable chance of testing that level.

📅 Quarterly (Mar 20 OPEX): ±11.25% move Range: $121.36 - $152.13 Translation: By March (after our February calls expire), the market expects significant movement in either direction. This wide range reflects earnings volatility and new business vertical uncertainty.

What's interesting: The February 20 expiration sits right between monthly and quarterly windows. Our whale is giving themselves enough time to capture Q4 earnings (likely mid-February) but not overpaying for the full quarterly move.

🎪 Catalysts: What Could Move the Stock

🔜 Upcoming Catalysts (What's Ahead)

Q4 2025 Earnings - Expected February 17, 2026 📊 Timing: 4 weeks before option expiration

This is likely THE catalyst our call buyer is positioning for. Q4 typically represents Airbnb's seasonal low, but here's what could surprise to the upside:

- Holiday travel rebound: Pent-up demand for winter destinations and holiday travel

- Services revenue contribution: First full quarter of meaningful revenue from the new Services vertical launched in May

- Hotel pilot metrics: Management will likely share early traction data from NYC/LA/Madrid hotel expansion

- Buyback execution: Updates on the $6 billion repurchase program (already deployed $1B in Q2 alone)

- Margin guidance: Any indication that the "heavy investment period" is ending could spark a re-rating

According to Zacks earnings calendar, consensus expects $0.26 EPS for Q1 2026 (reported in May), but Q4 results could reset expectations if growth re-accelerates.

$6 Billion Share Repurchase Program Execution 💸 Ongoing through 2026

Announced in August 2025, this massive buyback program has already reduced share count from 673M to 652M. With $11.4 billion cash on the balance sheet, management has plenty of firepower to continue aggressive repurchases.

Why it matters: Each $1B in buybacks reduces share count by ~1.5% at current prices, providing automatic EPS lift even if revenue growth stays muted. If they maintain the Q2 pace, another $1-2B could be deployed before February expiration.

AI Platform Enhancements Rollout 🤖 Continuous through Q1 2026

Airbnb is treating AI as its "fourth pillar" with multiple features launching:

- Conversational search: Natural language queries like "cozy apartment for two in Lisbon with ocean view"

- Personalized recommendations: Machine learning boosted booking conversion by 25% in initial testing

- Enhanced AI support: Chatbot now handles cancellations and date changes across North America

According to AInvest's analysis, these features contributed to Q2's 13% revenue growth. Further adoption could surprise on conversion rates in Q4 results.

Tax Benefits Starting 2026 💰 Begins impacting Q1 2026 margins

CFO Ellie Mertz confirmed that the "One Big Beautiful Bill" will "materially reduce our effective tax rate due to preferential changes to tax on foreign earnings" starting in 2026.

Impact: Lower tax rate = higher net income and EPS, even without revenue growth. This could provide a positive surprise in Q1 2026 guidance during the February earnings call.

Analyst Price Target Updates 📈 Recent momentum building

December has seen a wave of analyst upgrades:

- RBC Capital (Dec 15): Upgraded to Outperform with $170 price target (+24% upside)

- Jefferies: Upgraded to Buy with $165 target

- DA Davidson (Dec 5): Reaffirmed Buy at $155

The RBC upgrade specifically cited "increasingly attractive brand monetization story" and strength in the consumer AI landscape - exactly the narrative our call buyer might be betting on.

✅ Already Happened (Context Building)

Q3 2025 Earnings Beat - Reported November 7, 2024 📊

- Revenue: $3.7B, up 10% YoY (beat expectations)

- Net Income: $1.4B with 37% margin

- Free Cash Flow: $1.1B in quarter; $4.1B trailing twelve months

- Key metric: Average Daily Rate increased 1% to $164

Q2 2025 Strong Performance - Reported August 6, 2025 💪

- Revenue: $3.10B, up 13% YoY (beat estimates)

- Net Income: $642M, up from $555M prior year

- Immediate buyback: $1.0 billion repurchased in Q2 alone

2025 Summer Release - Launched May 13, 2025 🚀

The most significant platform transformation in Airbnb's 15-year history, per official announcement:

-

Airbnb Services: New $200-250M investment launching 10 service categories in 260 cities (chefs, photographers, spa treatments, personal training). According to CNBC coverage, management expects this to become a "significant revenue driver."

-

Reimagined Experiences: Rebuilt platform in 650 cities with celebrity-hosted "Airbnb Originals"

-

App Redesign: Complete ground-up rebuild for first time since 2010

Hotel Business Expansion - Announced November 2025 🏨

CEO Brian Chesky confirmed plans to "go significantly more aggressively into hotels" with pilot programs in NYC, LA, and Madrid. He sees potential for a "multibillion dollar business" leveraging boutique and independent hotels.

FIFA Partnership - Announced June 2025 ⚽

Three-year deal covering 2026 FIFA Club World Cup, 2026 Men's World Cup (US/Canada/Mexico), and 2027 Women's World Cup, per Tracxn profile. This brings massive exposure during global sporting events.

🎲 Price Targets & Scenarios

Using gamma levels, implied move probabilities, and upcoming catalysts, here's how this could play out:

🚀 Bull Case: $145-150 Target (25% probability)

The Perfect Storm Scenario:

Q4 earnings in mid-February show:

- ✅ Services revenue contribution beats expectations (faster adoption than anticipated)

- ✅ Hotel pilot showing strong early traction with path to scale

- ✅ Margin expansion guidance as investment phase ends

- ✅ Acceleration in nights booked growth vs. Q3's 10% rate

- ✅ Aggressive buyback execution continues ($1B+ in Q4)

Technical setup: ABNB breaks through the massive $140 gamma wall, triggering dealer covering and short squeeze dynamics. Once $140 falls, path opens to $145 resistance, and momentum could carry to $150 (RBC's $170 target comes into view).

Catalyst alignment: Tax benefit news in February guidance, plus positive commentary on AI feature adoption, creates bullish narrative shift from "growth stalling" to "re-acceleration beginning."

What our call buyer makes: At $145, the $140 calls would be worth ~$5.00 per contract minimum = $1.25M profit on $1.6M bet (78% return). At $150, they could see 2x-3x return.

Realistic? Requires multiple things to go right, but not impossible. The recent 11.4% two-week rally shows ABNB can move fast when momentum builds. Analyst upgrades and buyback support provide fundamental backing.

📊 Base Case: $138-142 Range (50% probability)

The Choppy Grind Scenario:

Q4 earnings are... fine. Not great, not terrible:

- Revenue growth stays in the 8-10% range (meets low expectations)

- Services and Hotels showing promise but not yet material to results

- Margins compress slightly but management reiterates 2026 improvement story

- Buyback execution continues as expected (~$1B in Q4)

Technical setup: ABNB tests the $140 gamma resistance multiple times through January-February. Price action stays choppy in the $135-142 range, never decisively breaking out but also not collapsing. Implied move for monthly OPEX ($129.99-$143.50) plays out.

Catalyst alignment: No major surprises either way. The market already expects moderate performance and continues to price ABNB as "show me" story until new verticals prove out.

What our call buyer makes: At $141, the $140 calls are worth $1.00-2.00 per contract = breakeven to small profit. Time decay becomes a factor as expiration approaches. They likely exit early if stock stalls around $140-141 in late January.

Realistic? This is the highest probability outcome. ABNB has been a range-bound grinder lately, and breaking decisively out of patterns requires a strong catalyst. Q4 results might not be that catalyst if growth stays muted.

📉 Bear Case: $128-133 Range (25% probability)

The Disappointment Scenario:

Q4 earnings disappoint on key metrics:

- ❌ Revenue growth decelerates further (mid-single digits)

- ❌ Services vertical showing weak adoption - still too small to matter

- ❌ Hotel business faces integration challenges or regulatory pushback

- ❌ Margins compress more than expected due to continued investments

- ❌ Management unable to provide clear path to re-acceleration

Technical setup: ABNB fails at the $140 gamma wall and rolls over. Support at $135 gets tested and potentially breaks, bringing the $130 level into play. The stock trades down toward the lower end of the quarterly implied move range ($129.99).

Catalyst alignment: Broader market weakness, travel sector concerns, or regulatory headlines (new city bans, housing market backlash) add to fundamental disappointment. Analyst downgrades follow weak results.

What our call buyer makes: These calls expire worthless or close to it. Maximum loss of $1.6M. Even if stock stabilizes at $135, the $140 calls would be worth pennies by February expiration due to time decay.

Realistic? ABNB did show growth stalling concerns with Q1's slowest post-pandemic growth (6% revenue, 8% nights booked). If this trend continues, the bear case activates. However, recent stock momentum (+11.4% in 2 weeks) and analyst upgrades suggest market isn't positioned for this scenario.

🎯 What the Smart Money Might Know

Why would someone bet $1.6M on the $140 strike specifically?

Three theories:

-

Gamma squeeze setup: They see the massive call gamma wall at $140 and think a catalyst could trigger a short-covering rally that blows through it. Once $140 breaks, momentum algorithms pile in.

-

Insider-adjacent information: Not illegal insider trading, but perhaps industry channel checks showing strong holiday travel trends, robust Services adoption, or positive hotel pilot feedback that isn't yet public.

-

Volatility play: With implied volatility relatively low heading into earnings, they're buying cheap optionality on a binary event (Q4 results). Even if stock doesn't reach $140, they could sell at a profit if IV expands into earnings.

Base case probability: I'd assign 60% chance ABNB trades between $135-143 through February expiration, 25% chance of bull scenario ($145+), and 15% chance of bear case ($130 or below).

💡 Trading Ideas

If you're intrigued by this setup but don't want to bet $1.6M, here are ways to play it at different risk levels:

🛡️ Conservative: "Show Me the Earnings" Strategy

The Play: Wait for Q4 earnings announcement (likely Feb 17) and buy shares on any post-earnings dip below $135.

Why this works:

- No theta decay eating your position

- Ability to hold through volatility without expiration pressure

- Strong support at $135 (gamma) and $130 (technical) limits downside

- Buyback program provides fundamental bid under the stock

Entry: $132-135 on earnings weakness Target: $145-150 over 3-6 months Stop: $128 (below support levels) Risk/Reward: 4-6% downside vs. 10-14% upside

Who this is for: Investors who like the long-term story (new verticals, buyback, AI moat) but want to avoid options complexity. You're betting Airbnb executes on its platform expansion over time.

⚖️ Balanced: "Gamma Breakout" Bull Call Spread

The Play:

- Buy ABNB Feb 20, 2026 $137 calls (near the money)

- Sell ABNB Feb 20, 2026 $145 calls (resistance level)

- Net cost: ~$3.50-4.00 per spread

Why this works:

- Mimics the whale's bullish bet but caps your risk at the spread cost

- Profits if ABNB breaks through $140 gamma wall and heads toward $145

- Selling the $145 call reduces cost and theta decay

- Breakeven around $140.50-141 (need same move as whale but cheaper)

Max Profit: $4-4.50 per spread (100-125% return) if ABNB closes above $145 Max Loss: $3.50-4.00 per spread if ABNB closes below $137 Breakeven: ~$140.50

Who this is for: Swing traders who think the unusual activity is a signal worth following, but want defined risk. You're betting on the Q4 earnings catalyst and gamma breakout thesis.

Exit plan: Take profits at 50-75% of max gain ($2-3 spread value) if ABNB clears $143 in late January. Don't hold into the last week of expiration unless deep in-the-money.

🚀 Aggressive: "Ride with the Whale" Pure Call

The Play: Buy ABNB Feb 20, 2026 $140 calls (same strike as the unusual trade)

Why this works:

- Direct exposure to the exact bet that triggered the alert

- Unlimited upside if bull case plays out

- Leverage to Q4 earnings surprise and $140 breakout

- If smart money is right, this could be a multi-bagger

Current premium: ~$0.64 per contract ($64 per call) Breakeven: $140.64 at expiration Max Loss: 100% of premium paid Profit potential: Unlimited (5-10x possible if stock rallies to $150+)

Position sizing: Never risk more than 2-3% of portfolio on any single options trade. If you're trading a $50K account, that's $1,000-1,500 max = 15-23 contracts.

Who this is for: YOLO traders with high risk tolerance who believe the unusual activity represents actionable intelligence. You're comfortable losing the entire premium for a shot at outsized gains.

Exit plan:

- Set alerts at $142 (take partial profits, let rest ride)

- Hard stop if ABNB breaks below $133 (thesis invalidated)

- Final decision point: Week of Feb 10-13 based on Q4 results

⚠️ Risk Reality Check:

Even the aggressive strategy here is a leveraged bet with binary outcomes. Options can expire worthless. Don't bet money you can't afford to lose. The whale who dropped $1.6M likely has a $100M+ portfolio - adjust your sizing accordingly!

⚠️ Risk Factors: What Could Go Wrong

Let's be brutally honest about what could derail this trade:

📉 Growth Deceleration Continues

The Problem: Airbnb's revenue growth dropped from 13% (Q2) to 10% (Q3) in 2024, and Q1 2025 showed just 6% growth with the slowest nights-booked growth since pandemic. If Q4 results continue this trend, the stock could get hammered.

Why it matters: At a 30.5x P/E ratio, ABNB is priced for growth re-acceleration, not further deceleration. If new verticals (Services, Hotels) aren't moving the needle yet, analysts will slash estimates.

Probability: Moderate (30%). Management has had three quarters to stabilize growth, but macro pressures (consumer spending, travel saturation) are real.

🏛️ Regulatory Headwinds Intensify

The Problem: Cities worldwide are cracking down on short-term rentals. New York City's strict host registration requirements, Barcelona's tourist limits, and Greece freezing new licenses all constrain supply in key markets.

Why it matters: Regulatory restrictions directly limit listing growth and create compliance costs. If major cities announce new crackdowns between now and February, sentiment could turn negative fast.

Probability: Low-Moderate (20%). Regulatory risk is ongoing but tends to be priced in. A major new ban in a top-10 market would be needed to derail the stock.

💸 Margin Compression from Investments

The Problem: Airbnb is investing $200-250M in the Services vertical and expanding into Hotels - both unproven businesses that pressure margins. Q1 2025 EBITDA margin was 18% vs. 20% year-ago.

Why it matters: If margins keep compressing through Q4 without clear revenue payoff from new verticals, investors will question the strategy. The stock trades partly on best-in-class profitability - deterioration hurts the thesis.

Probability: Moderate (35%). This is the biggest near-term risk. Management says they're "through the heaviest investment period," but Q4 will test that claim.

🌊 Macroeconomic Weakness Hits Travel

The Problem: Rising interest rates, inflation, and economic uncertainty could reduce discretionary travel spending. If consumers pull back on vacations and experiences, Airbnb's nights booked will suffer.

Why it matters: Travel is a cyclical industry. A recession or even a "soft landing" with reduced consumer confidence would hit ABNB harder than defensive sectors.

Probability: Moderate (30%). Macro environment is uncertain. Holiday travel trends through Q4 will be the early indicator.

🏨 Competitive Pressures from Booking.com and Vrbo

The Problem: Booking.com grew share to 48% in Europe while Vrbo added 1M urban listings targeting city travelers. Both competitors are gaining ground.

Why it matters: Airbnb's valuation assumes continued market dominance. Losing share to better-funded competitors (Booking.com's parent has massive hotel inventory) would force multiple compression.

Probability: Low-Moderate (25%). Airbnb still holds commanding 44% global share and has brand moat, but competition is real and intensifying.

💀 The $140 Gamma Wall Holds Firm

The Problem: Our entire bull thesis rests on breaking through massive resistance at $140. If dealers defend that level aggressively and sellers show up, the stock could ping-pong in the $135-140 range through February.

Why it matters: Range-bound trading is the death of call options. Even if ABNB doesn't collapse, theta decay will erode the $140 calls if the stock doesn't move decisively higher.

Probability: Moderate-High (40%). This is actually the most likely outcome. Gamma walls are real, and breaking through requires a strong catalyst and momentum follow-through.

📊 Earnings Disappoint on Key Metrics

The Problem: If Q4 results show weak Services adoption, hotel pilot challenges, or guidance for continued margin pressure, the stock could gap down 10%+ overnight.

Why it matters: The February call options expire just DAYS after Q4 earnings. A big miss could instantly destroy the position with no time to recover.

Probability: Low-Moderate (25%). Management has been conservative on guidance lately, setting low bars. But execution risk on new verticals is real.

Bottom Line on Risks:

This is not a "safe" trade. The unusual activity tells us someone with resources thinks the odds are favorable, but z-scores don't guarantee winners. Multiple risks could derail the bullish thesis, and options magnify both gains AND losses. Trade accordingly.

🎯 The Bottom Line

Here's the deal:

Someone just dropped $1.6 million betting that Airbnb breaks through critical resistance at $140 by February 20, 2026. The trade's z-score of 30.93 (555x average size) tells us this isn't retail speculation - it's institutional-scale conviction.

What they might be seeing:

✅ Catalyst-rich setup: Q4 earnings (mid-Feb), $6B buyback execution, new verticals gaining traction ✅ Technical breakout potential: $140 gamma wall represents THE inflection point ✅ Valuation support: Trading 45% below estimated fair value with 2026 tax tailwinds ahead ✅ Analyst momentum: Recent upgrades from RBC ($170 target) and Jefferies ($165)

What could go wrong:

❌ Growth deceleration continues (6-8% revenue growth vs. double-digit history) ❌ Margins stay compressed from Services/Hotels investments with no clear payoff ❌ Macro weakness hits discretionary travel spending ❌ The $140 gamma wall holds firm and stock ranges through February

Your action plan depends on your style:

📍 If you already own ABNB: Consider this unusual activity a bullish signal. The buyback program and upcoming catalysts support holding through Q4 earnings. Set alerts at $140 (potential breakout) and $133 (support breakdown).

📍 If you're watching from the sidelines: Mark your calendar for Q4 earnings (likely Feb 17). That's the key binary event. If results surprise positive and stock breaks $140, consider entry on pullbacks to $141-143. If results disappoint, wait for $130-132 support.

📍 If you're bearish: The counter-trade is selling call spreads (sell $140 calls, buy $145 calls) betting the gamma wall holds. But be careful - if you're wrong and ABNB rips through $140, losses could mount quickly.

My take:

The unusual activity is interesting and the z-score is objectively extreme, but I'd want confirmation from price action before going all-in. If ABNB can close above $138-139 on strong volume over the next week, it would validate the bullish setup. If it chops around $135-137, the thesis is weaker.

The February timing is smart - long enough to capture earnings but not paying for full quarterly volatility. The $140 strike is aggressive (needs 2.3% move just to get to breakeven) but strategic (right at the gamma inflection point).

Final word:

Options trading is a game of probabilities, not certainties. Even a $1.6M bet from smart money can lose. Use proper position sizing, know your exit plan, and never risk more than you can afford to lose.

But if you believe Airbnb's platform expansion story and think Q4 earnings could surprise... this unusual activity might be telling you something worth paying attention to. 👀

📚 Additional Resources

🔗 View ABNB Live Stock Data 🔗 Track Real-Time Option Flow 🔗 Read Full Catalyst Analysis 🔗 Check Latest Analyst Ratings

⚠️ Risk Disclaimer:

Options trading involves substantial risk and is not suitable for all investors. The strategies discussed here are for educational purposes only and do not constitute financial advice. You can lose 100% of your investment in options. Past performance does not guarantee future results. The unusual activity identified is informational and should not be interpreted as a recommendation to buy or sell. Always conduct your own research and consider consulting a licensed financial advisor before making investment decisions. Trade at your own risk.

💼 About This Analysis:

This report analyzes unusual options activity detected on December 19, 2025 at 11:45:15 AM for ABNB. Data sources include real-time option flow monitoring, gamma exposure analysis, implied volatility surfaces, and catalyst research from public filings and financial news outlets. The z-score calculation measures how many standard deviations this trade size deviates from the historical average for these specific contracts.

Analysis generated December 19, 2025 | ABNB trading at $136.82 | Premium paid: $1,600,000