🎤 AMD CES 2026 Keynote Day - Smart Money Rolling Diagonal Spreads Into Earnings! 🎯

📅 January 5, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

AMD caught unusual options flow totaling $15 MILLION this morning at 10:23:50, with institutions rolling a diagonal spread ahead of today's CES 2026 keynote (6:30 PM PT) and the critical Q4 earnings on February 3rd. The flow shows selling 7,500 contracts of March $230 calls for $14M while simultaneously closing 9,600 January $250 calls for $1M - a clear repositioning trade suggesting smart money is taking chips off the table at current levels while maintaining upside exposure through March. With AMD trading at $222 after a spectacular 2025 (+77% YTD), this defensive adjustment signals caution into binary events.

📊 Company Overview

Advanced Micro Devices (AMD) is a global semiconductor leader competing directly with Nvidia in the exploding AI accelerator market:

- Market Cap: $363.8 Billion (6th largest semiconductor company)

- Industry: Semiconductors & Related Devices

- Current Price: $222.35 (down from October 2025 all-time high of $267.08)

- Primary Business: AMD designs digital semiconductors for PCs, gaming consoles, data centers with AI capabilities, industrial, and automotive markets. The company is strengthening its position in AI GPUs while maintaining its traditional focus on CPUs and graphics processors.

💰 The Option Flow Breakdown

The Tape (January 5, 2026 @ 10:23:50):

| Date | Time | Symbol | Buy/Sell | Type | Expiration | Strike | Volume | Premium | Strategy | Z-Score | Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-05 | 10:23:50 | AMD | SELL | CALL $230 | 2026-03-20 | $230 | 7,500 | $14.0M | Diagonal Spread (Sell Leg) | 31.1 | EXTREMELY UNUSUAL |

| 2026-01-05 | 10:23:50 | AMD | BUY | CALL $250 | 2026-01-16 | $250 | 9,600 | $1.0M | Diagonal Spread (Close Buy Leg) | 3.32 | EXTREMELY UNUSUAL |

🤓 What This Actually Means

This is a sophisticated diagonal spread roll indicating defensive repositioning! Here's what happened:

- 🔄 Rolling down and out: Closing profitable January $250 calls (bought earlier when stock was higher), selling new March $230 calls

- 💸 Net credit received: $13M net credit ($14M collected - $1M paid to close) = locking in gains

- 📊 Strike positioning: New $230 short calls are 3.5% above current price ($222) - moderate bullish assumption

- ⏰ Time extension: March 20 expiration (74 days) captures Q4 earnings (Feb 3), CES announcements, and MI350/MI450 product roadmap updates

- 🎯 Size matters: 7,500 contracts represents 750,000 shares worth ~$167M notional exposure

- 🛡️ Risk management: Rather than staying naked long into binary events, they're capping upside at $230 while collecting premium

Translation for regular folks: This trader originally bought January $250 calls when AMD was likely trading in the $230-250 range (possibly during the October rally to $267 all-time highs). Now with AMD down at $222 and just 11 days until those January calls expire worthless, they're:

- Closing the losing January $250 calls for pennies ($1M / 9,600 = ~$1.04 per contract)

- Selling new March $230 calls for fat premium ($14M / 7,500 = $18.67 per contract)

- Pocketing $13M in net premium to offset the loss on the original position

This is textbook damage control and profit-taking - they're admitting AMD probably won't hit $250 by January expiration, so they're taking the L, but immediately setting up a new income-generating position at a more realistic $230 strike through March.

Unusual Score: 🔥🔥 EXTREME - The Z-score of 31.1 on the March $230 call sale means this is 31 standard deviations above normal - essentially unprecedented size for this specific strike. This happens maybe a few times per year for AMD. The January call close is also extremely unusual (Z-score 3.32), though less dramatic.

📈 Technical Setup / Chart Check-Up

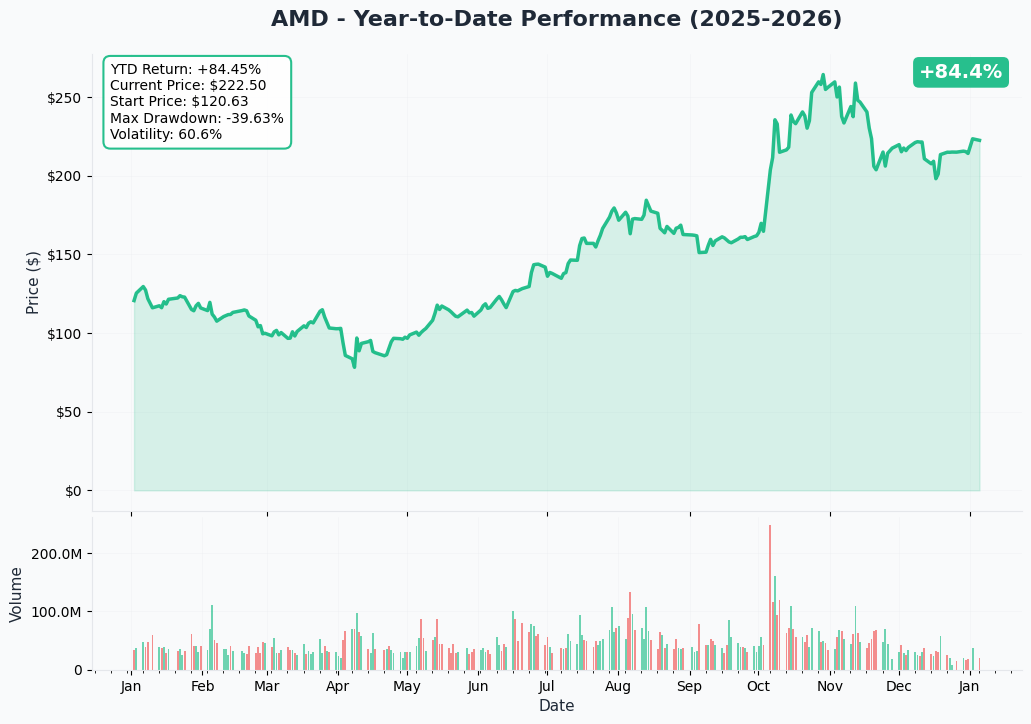

YTD Performance Chart

AMD has had a spectacular run in 2025 - currently up +77% YTD at $222.35 (started the year around $126). The chart tells the story of AMD's AI transformation - after touching a low of $76.48 in April during the broader tech selloff, the stock rocketed to an all-time high of $267.08 in late October on the explosive OpenAI partnership announcement (6 gigawatts, potentially $100B+ in revenue over 4 years).

Key observations:

- 🚀 Historic rally: Surged from $76 in April to $267 in October - a 249% move in 6 months driven by the OpenAI deal and record Q3 earnings ($9.25B revenue, up 36% YoY)

- 📉 Recent pullback: Down 16.7% from October highs to current $222 level - giving back some gains as investors digest valuation

- 📊 Key support tested: Currently trading right near the $220 level which served as resistance in early October before the OpenAI breakout

- ⚡ High volatility: Sharp moves in both directions characteristic of sentiment-driven AI stock

- 🎯 Critical juncture: Sitting between major support ($220) and overhead resistance ($230-240) heading into today's CES keynote

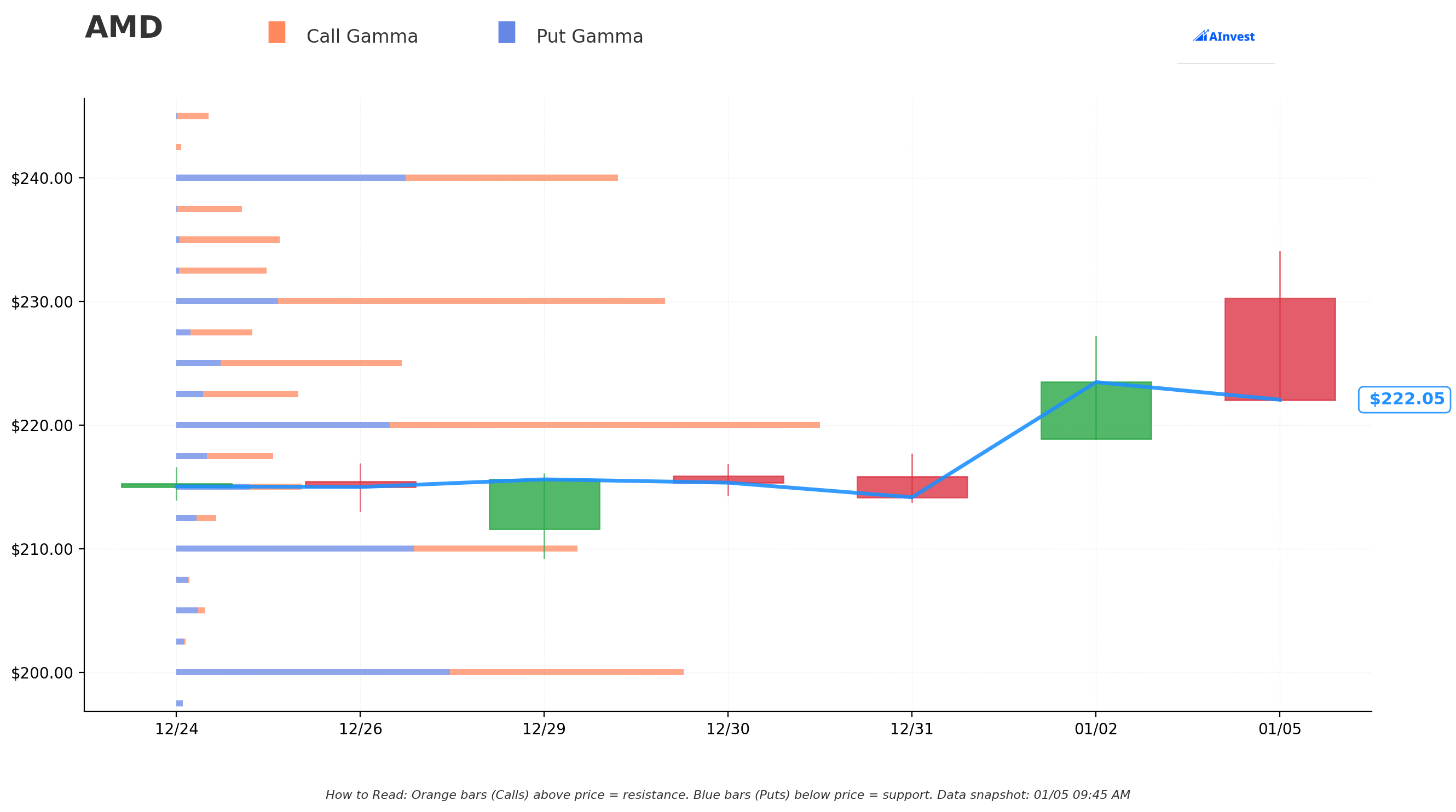

Gamma-Based Support & Resistance Analysis

Current Price: $221.86 (as of market open)

The gamma exposure map reveals critical price magnets where options positioning creates natural support and resistance:

🔵 Support Levels (Put Gamma Below Price):

- $220 - STRONGEST NEARBY SUPPORT with 28.1B total gamma (9.5B net) - just 0.84% below current price

- This is where market makers will aggressively buy dips to hedge their put exposure

- Break below this and next stop is $210

- $210 - Secondary support at 17.6B total gamma (5.3% below) - major institutional strikes

- $200 - Deep support zone at 22.2B total gamma (9.9% below) - psychological round number

- $195 - Extended floor at 6.3B gamma (12.1% below)

- $190 - Disaster support at 6.7B gamma (14.4% below)

🟠 Resistance Levels (Call Gamma Above Price):

- $225 - Immediate ceiling with 9.8B total gamma (1.4% overhead) - first test

- $230 - MAJOR RESISTANCE at 21.2B total gamma, 12.4B net (3.7% above) - THIS IS WHERE THE SHORT CALLS ARE!

- Notice the diagonal spread seller struck exactly at the biggest gamma resistance level

- 16.8B call gamma here creates mechanical selling pressure as stock approaches

- This is the level smart money thinks AMD will struggle to break through March

- $240 - Secondary resistance at 19.1B gamma (8.2% above)

- $250 - Extended resistance at 14.1B gamma (12.7% above) - where the original January calls were struck

What this means for traders: AMD is in a tight consolidation zone between strong $220 support (28.1B gamma) and massive $230 resistance (21.2B gamma). The gamma data suggests the stock is likely to trade in a $220-230 range through the next few weeks unless a major catalyst (CES announcements today or earnings on Feb 3) provides directional conviction.

The diagonal spread makes perfect sense in this context: The trader is selling premium at exactly the level ($230) where options positioning creates the strongest resistance. They're betting AMD gets stuck below $230 through March, allowing them to keep the $14M in premium collected. If AMD does rally above $230, their gains are capped but they still profit up to that strike.

Net GEX Bias: Bullish (156.6B call gamma vs 99.1B put gamma = 57.5B net bullish) - Overall positioning leans moderately bullish, but immediate price action constrained by overhead $230 resistance.

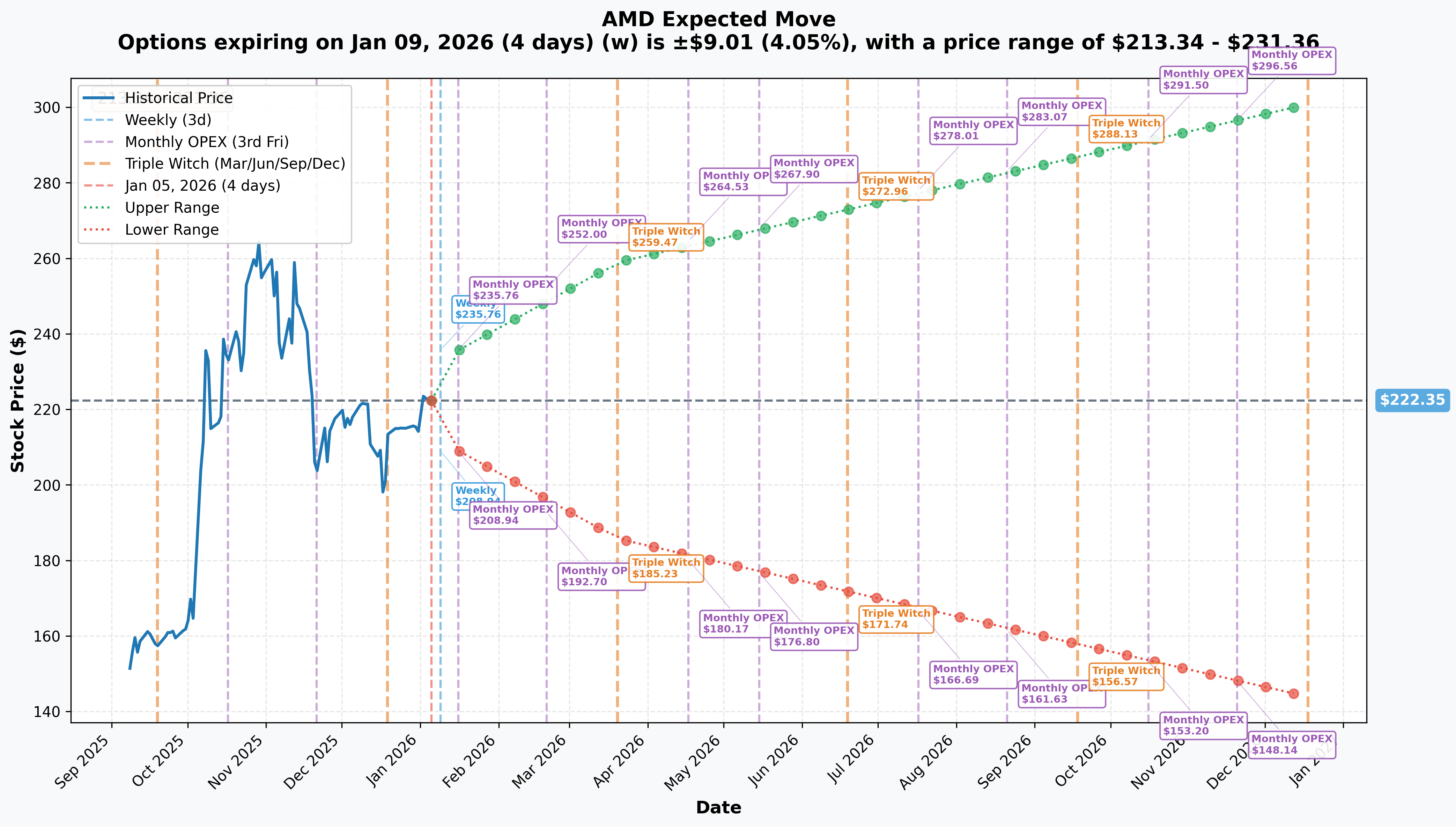

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 9 - 4 days): ±$9.01 (±4.05%) → Range: $213.34 - $231.36

- 📅 Monthly OPEX (Jan 16 - 11 days): ±$13.41 (±6.03%) → Range: $208.94 - $235.76

- 📅 Quarterly Triple Witch (Mar 20 - 74 days - THIS TRADE!): ±$36.66 (±16.49%) → Range: $185.69 - $259.01

- 📅 Yearly LEAPS (Dec 18 - 347 days): ±$78.50 (±35.3%) → Range: $143.85 - $300.85

Translation for regular folks: Options traders are pricing in a 4% move ($9) through this Friday's weekly expiration (capturing today's CES keynote), a 6% move ($13) through January monthly OPEX, and a MASSIVE 16.5% move ($37) through the March quarterly expiration when the diagonal spread expires.

The March implied range of $185.69-$259.01 is critical for analyzing this trade:

- Upper range: $259.01 is well above the $230 short call strike - suggesting only 15-20% probability stock finishes above $230

- Current price: $222.35 sits right in the middle of the range

- Lower range: $185.69 represents 16.5% downside risk - significant given upcoming earnings

Key insight for the diagonal spread: The options market is pricing March implied vol at 16.5% annualized (~28% IV), which translates to fat premium on the $230 calls the trader sold. By selling at-the-money-ish calls in a high IV environment, they're collecting maximum time decay while the March expiration captures both Q4 earnings volatility (Feb 3) and any CES announcements today.

The trader is essentially saying: "I think AMD stays below $230 through March, and I'm willing to collect $18.67 per share to cap my upside there while the market expects big swings."

🎪 Catalysts

🔥 Immediate Catalysts (Next 7 Days)

CES 2026 Keynote - TONIGHT at 6:30 PM PT! 🎤

Dr. Lisa Su delivers the opening keynote at CES 2026 in just hours. According to AMD's corporate events page and coverage from WCCFTech, the keynote is expected to unveil major product announcements:

Expected announcements:

- 🎮 Ryzen 9 9950X3D and 9900X3D launch - AMD claims 20% faster gaming performance than Intel's Arrow Lake

- 💻 Ryzen AI 400 family for laptops - next-gen mobile processors targeting consumer AI workloads

- 🎯 Ryzen 7 9850X3D details - expanding the popular X3D gaming lineup

- 🤖 AI-related Instinct and EPYC updates - potentially MI350/MI450 roadmap teasers

- 🖼️ FSR Redstone upscaling technology - AMD's answer to Nvidia DLSS 4

- 🚀 Zen 6 Venice server CPUs preview - next-generation data center architecture

Why this matters: CES keynotes historically move AMD stock 3-5% if product announcements exceed expectations or disappoint. The 4.05% weekly implied move suggests options traders are pricing in volatility tonight. However, consumer/gaming product launches typically have less impact than data center AI announcements, so the reaction may be muted unless Lisa Su drops surprise MI450 details or major customer wins.

Upside scenario: Strong consumer product reception + surprise AI accelerator news could push AMD toward $230-235 Downside scenario: Lackluster announcements or delays to MI350 timeline could test $215-220 support

🚀 Near-Term Catalysts (Next 30 Days)

Q4 2025 Earnings - February 3, 2026 (29 DAYS AWAY!) 📊

This is THE catalyst that will make or break AMD's near-term trajectory. Confirmed for February 3, 2026 after market close per MarketBeat and Nasdaq.

Wall Street consensus expectations:

- 📊 Revenue: $9.32-9.6B (company guided $9.6B ± $300M in Q3 report) vs Q4 2024 $6.17B - up 52-56% YoY

- 💰 EPS: $1.31 consensus vs $0.77 last year - up 70% YoY

- 🤖 Data Center Revenue: Expected $4.5-5.0B (continuing Q3's record $4.3B) - analysts watching MI350 ramp closely

- 💻 Client Revenue: Expected $2.6-2.8B following record Q3 $2.8B - Ryzen momentum continuing

- 📈 Gross Margin: Target 54.5% (guided by company in Q3) - critical for profitability trajectory

What to watch:

- MI350/MI355X ramp progress: Early customer feedback and production volumes will validate competitiveness vs Nvidia

- OpenAI deployment timeline update: Any details on the 6GW partnership and first 1GW MI450 deployment (H2 2026)

- MI308 China revenue: Following July 2025 restart of shipments, Alibaba reportedly considering 40,000-50,000 MI308 units per 247 Wall St

- 2026 full-year guidance: Street looking for revenue growth guidance in 25-30% range

- Data center AI revenue trajectory: Management targeting >80% CAGR for AI revenue - need proof of execution

Historical context: AMD has shown volatility on earnings with ±8-12% moves even on beats due to guidance sensitivity. The 6.03% monthly implied move suggests options traders expect smaller reaction this time, possibly due to already subdued stock price (-16% from October highs).

Risk for the diagonal spread: If earnings catastrophically disappoint and AMD breaks below $220 support, the trader's short $230 calls would be safe but their overall equity position (if they own stock) would suffer. Conversely, a massive beat driving AMD above $250 would result in capped gains at $230.

📊 Strategic Developments (Q1 2026 and Beyond)

OpenAI Partnership: The $100B+ Game-Changer 🤝

AMD's landmark partnership with OpenAI announced October 6, 2025 remains the most transformative catalyst in company history:

- 🏭 6 gigawatts of AMD GPUs to be deployed across multiple generations

- 💰 First deployment: 1 GW of MI450 GPUs beginning H2 2026

- 📊 Revenue impact: CEO Lisa Su stated each gigawatt represents "significant double-digit billions of revenue" for AMD

- 🎯 Total opportunity: Analysts project $100+ billion in revenue over four years from OpenAI and derivative customers

- 🚀 Validation: OpenAI choosing AMD to compete with Nvidia infrastructure validates technology competitiveness at the highest level

Why this matters for March: The diagonal spread expires March 20th, well before the H2 2026 MI450 deployment begins. This suggests the trader isn't positioning for OpenAI execution risk but rather for nearer-term catalysts (earnings, CES, MI350 launch).

Oracle Cloud Partnership - 50,000 MI450 GPUs (Q3 2026 deployment)

Oracle announced October 14, 2025 it will deploy 50,000 AMD Instinct MI450 GPUs:

- First hyperscaler to offer publicly available AI supercluster powered by MI450

- Deployment begins Q3 2026

- Oracle first to deploy MI355X GPUs via OCI Supercluster

MI350 Series Launch - Mid-2025 (PULLED FORWARD!) 🚀

AMD accelerated the MI350 timeline from H2 2025 to mid-year to improve competitive positioning:

- 🔬 Based on 3nm CDNA 4 architecture with 288GB HBM3E and 8TB/s bandwidth

- 💥 Offers 35x generational increase in AI inference performance over MI300 series

- 🎯 Critical product that must DELIVER to justify valuation

- 📅 Launch timing (mid-2025) falls just after the March diagonal spread expiration

Execution risk: Any MI350 delays or performance issues would be catastrophic given the stock has already priced in success. The March $230 short calls suggest the trader thinks AMD stays range-bound until MI350 actually launches and proves itself.

AMD Financial Analyst Day (November 11, 2025) - Long-Term Targets

At the NYC Financial Analyst Day on November 11, 2025, AMD unveiled ambitious targets:

- 📈 Revenue CAGR: Greater than 35% over next 3-5 years

- 💰 EPS target: Greater than $20 non-GAAP (vs current ~$4-5 range)

- 🤖 AI revenue CAGR: Greater than 80% over 3-5 years

- 🌐 Market opportunity: AMD targeting $1 trillion data center TAM by 2030

Product roadmap highlights:

- MI450/Helios rack-scale systems: Q3 2026

- MI500 series: 2027

- Venice (Zen 6) and Verano CPUs

⚠️ Risk Catalysts (Negative)

Nvidia Competition - Blackwell/Rubin Dominance 🏆

Despite AMD gains, Nvidia maintains 80-92% AI GPU market share while AMD has just 7-10%:

Nvidia's advantages:

- 🔥 Blackwell platform shipping in volume - driving record data center revenue per Financial Content

- 🚀 Rubin architecture launching H2 2026 - same window as AMD MI450 (direct competition)

- 📊 Blackwell Ultra (GB300) expected to ship 60,000+ racks in 2026

- 💪 CUDA ecosystem dominance - 6M+ developers vs ROCm's nascent adoption

- 📈 Yearly release cadence keeps competitors in "generational lag"

AMD's challenges:

- ⚖️ Software ecosystem gap: CUDA remains industry standard, ROCm improving but still behind

- 🔗 Scalability limitations: 8-GPU clusters vs Nvidia's 72-GPU solutions

- 🏭 Manufacturing capacity constraints competing for TSMC 3nm production

China Export Controls Risk 🇨🇳

AMD faced $800M in charges in Q2 2025 from export restrictions on MI308 to China, though restrictions were lifted in July 2025:

- 🚨 Ongoing geopolitical tensions create uncertainty (historically 15-20% of revenue)

- ⚖️ Future export controls could hit MI325X/MI350 without warning

- 💸 Estimated $1.5-1.8B full-year 2025 revenue impact from restrictions

- 🇨🇳 New regulations (SAFE Chips Act proposed) could lock restrictions for 30 months

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through March 20th expiration (diagonal spread):

📈 Bull Case (30% probability)

Target: $250-260

How we get there:

- 🎤 CES keynote TONIGHT delivers surprise AI announcements (MI450 customer wins, MI350 early launch)

- 💪 Q4 earnings (Feb 3) CRUSH expectations with revenue toward $9.6B high-end and gross margins expanding to 55%+

- 🚀 MI350 launches ahead of schedule in Q1 2026 with strong early customer validation

- 🤖 Data center revenue confirms >80% AI CAGR trajectory, validating long-term targets

- 📊 OpenAI provides concrete deployment timeline details, removes uncertainty

- 🇨🇳 China MI308 orders materialize (Alibaba 40,000-50,000 units confirmed)

- 📈 Breakout above $230 gamma resistance triggers technical rally to $250

Key metrics needed:

- Data center revenue >$5B in Q4 (vs $4.3B in Q3)

- MI350 production ramp confirmed for Q1

- Gross margins expanding (proving pricing power vs Nvidia)

- Server CPU market share continuing to climb (34%+)

Impact on diagonal spread:

- Stock finishes $250-260: Short $230 calls get exercised, trader caps gains at $230

- They collected $14M in premium but miss out on the $20-30 rally above $230

- Still profitable overall but leaves money on the table

Probability assessment: Only 30% because it requires multiple positive catalysts aligning perfectly. AMD already gave back 16% from October highs - market showing some skepticism. The massive $230 gamma resistance (21.2B) creates mechanical headwinds.

🎯 Base Case (50% probability)

Target: $215-230 range (CHOPPY CONSOLIDATION) - DIAGONAL SPREAD WINS!

Most likely scenario:

- 🎤 CES keynote solid but not spectacular - gaming/consumer products well-received, no major AI surprises

- ✅ Q4 earnings meet consensus ($9.3-9.5B revenue, $1.25-1.35 EPS)

- 📱 MI350 launch timing confirmed for mid-2025, progressing as expected but not pulled forward further

- ⚖️ Guidance in-line to slightly conservative (normal seasonality, awaiting MI350 ramp)

- 🤖 AI revenue growing but not enough to expand valuation multiple from current levels

- 🇨🇳 China remains question mark - neither major positive nor catastrophic negative

- 🔄 Trading within gamma support ($220) and resistance ($230) bands for weeks

- 💤 Volatility compression as market digests 2025 gains, waits for MI350/MI450 proof points

This is EXACTLY what the diagonal spread trader wants:

- Stock stays below $230 through March 20 expiration

- Short $230 calls expire worthless

- They keep the full $14M premium collected

- Meanwhile, they offset the $1M loss from closing the January $250 calls

- Net profit: $13M for managing the position defensively

The $220 gamma support (28.1B) should hold on any dips, while $230 resistance (21.2B) caps rallies. Stock likely chops in this range until MI350 actually launches and proves competitive.

Why 50% probability: Stock at technical inflection point between major support/resistance levels. Fundamentals solid but valuation has compressed from October highs. Most institutional players will hold and wait for earnings clarity before making big moves. The options market implied move of 16.5% for March suggests wide range ($185-259) but most of that distribution falls in the $215-235 zone.

📉 Bear Case (20% probability)

Target: $185-210 (TEST MAJOR SUPPORT)

What could go wrong:

- 😰 CES disappoints - MI350 delayed, no major AI announcements, consumer products underwhelm

- 🚨 Q4 earnings miss or weak guidance - even small miss at current valuation could trigger -10-15% gap

- ⏰ MI350 launch pushed from mid-2025 to H2 2025 or later - credibility hit with investors

- 🇨🇳 New China export restrictions announced on MI325X/MI350, removing revenue upside

- 💸 Broader tech selloff drags semis lower (Nvidia weakness, macro recession fears)

- 📊 Nvidia Blackwell significantly outperforms AMD products, widens competitive gap

- 🤖 OpenAI deployment timeline pushed out or scaled back from 6GW plan

- 🔨 Break below $220 gamma support triggers cascade to $210, then $200

Critical support levels:

- 🛡️ $220: Strong gamma floor (28.1B) - MUST HOLD or momentum shifts bearish

- 🛡️ $210: Secondary support (17.6B gamma) - 5.3% below current

- 🛡️ $200: Major psychological floor (22.2B gamma) - 9.9% below current

Impact on diagonal spread:

- Stock finishes $185-210: Short $230 calls expire worthless (good for trader)

- They keep the $14M premium from selling the calls

- However, if they own underlying stock, they're down $12-37 per share on equity

- The diagonal spread provides some income cushion but doesn't fully protect against major decline

Probability assessment: Only 20% because it requires multiple negative catalysts. AMD's fundamentals remain strong (OpenAI partnership, government contracts, EPYC market share gains, product roadmap). However, the 16.5% March implied move does suggest a $185 lower range is possible. The trader clearly sees this risk, which is why they're taking defensive action.

💡 Trading Ideas

🛡️ Conservative: Wait for CES/Earnings Clarity

Play: Stay on sidelines until after CES keynote (tonight) and Q4 earnings (Feb 3) volatility settles

Why this works:

- ⏰ CES keynote in HOURS creates binary event risk with 4% weekly implied move - coin flip

- 💸 Implied volatility elevated at 16.5% for March - options expensive pre-events

- 📊 Stock down 16% from October highs but still up 77% YTD - valuation unclear

- 🎯 Better entry likely post-earnings after IV crush reduces option premiums 30-40%

- 📉 Diagonal spread flow signals even sophisticated players are REDUCING risk into events

- 🤔 When institutions roll out of long calls and sell premium, it's a caution flag

Action plan:

- 👀 Watch CES keynote tonight for MI350/MI450 roadmap updates and customer announcements

- 📊 Monitor reaction - if stock rallies >5% on CES news, stay patient for pullback

- 🎯 Mark calendar for Feb 3 earnings - this is THE catalyst that sets Q1 2026 direction

- ✅ Look for pullback to $210-220 gamma support post-earnings for stock entry with margin of safety

- ⏰ Revisit mid-2025 when MI350 launch provides next major de-risking catalyst

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential whipsaw from CES/earnings volatility. Maintain optionality. Get clearer entry signal after dust settles.

⚖️ Balanced: Post-CES Call Credit Spread (Copy The Pros)

Play: After CES keynote, sell call credit spread mirroring the institutional diagonal spread positioning

Structure: Sell $230 calls, Buy $240 calls (March 20 expiration - SAME as the institutional trade)

Why this works:

- 🎯 Targets exact same $230 resistance level where 21.2B gamma creates mechanical selling pressure

- 🤝 Essentially "copying" the smart money positioning at their chosen strike/expiration

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- ⏰ 74 days to expiration gives time for mean reversion if stock spikes on CES news

- 🛡️ Protects against "sell the news" scenario even if CES announcements are positive

- 💰 Captures high implied volatility (16.5%) before it compresses post-earnings

Estimated P&L (adjust after seeing post-CES pricing):

- 💰 Collect ~$3-4 credit per spread if entered Tuesday Jan 6 (after CES)

- 📈 Max profit: $300-400 if AMD stays below $230 at March expiration (50% probability per our base case)

- 📉 Max loss: $600-700 if AMD above $240 (defined and limited)

- 🎯 Breakeven: ~$233-234

- 📊 Risk/Reward: ~1:1.5 to 1:2 which is favorable for defined-risk neutral play

Entry timing:

- ⏰ Wait until Tuesday Jan 6 after CES keynote reaction settles

- 🎯 Only enter if stock trades $225 or below (gives cushion to $230 resistance)

- ❌ Skip if stock breaks above $230 on CES news (thesis invalidated)

Position sizing: Risk only 2-3% of portfolio per spread (this is directional speculation, not core holding)

Why this is "balanced": You're taking a defined-risk bearish/neutral stance (betting stock stays below $230) but you're not outright shorting or buying puts. If wrong, max loss is capped at $600-700 per spread. If right, you collect $300-400 for doing nothing.

Risk level: Moderate (defined risk, neutral-to-bearish) | Skill level: Intermediate

🚀 Aggressive: CES Earnings Iron Condor - Bet on Range (ADVANCED ONLY!)

Play: Bet that AMD stays trapped in $215-235 range through March using iron condor

Structure:

- Sell $235 calls / Buy $245 calls (call spread)

- Sell $215 puts / Buy $205 puts (put spread)

- March 20 expiration (captures both CES and earnings volatility)

Why this could work:

- 📊 Gamma data shows HUGE resistance at $230 (21.2B) and strong support at $220 (28.1B)

- 🎯 Range is $215-235 = $20 wide, giving 3-6% cushion on each side from current $222 price

- 💰 Selling BOTH puts and calls in high IV environment (16.5%) maximizes premium collection

- ⏰ 74 days of time decay working IN your favor on both sides

- 🔄 Thesis: AMD consolidates after 77% YTD rally, waiting for MI350 launch to break out

- 📉 Even if CES/earnings cause spikes, stock likely reverts to middle of range by March

Why this could blow up (SERIOUS RISKS):

- 💸 TWO-WAY RISK: Can lose on EITHER side if stock breaks out or breaks down

- ⚡ Earnings binary event: Feb 3 earnings could gap stock +/- 10-15%, blowing through strikes

- 😱 IV CRUSH REVERSAL: High IV now helps, but after earnings IV collapses, spreads widen dangerously

- 🚀 CES catalyst: Tonight's keynote could gap stock outside range before you even enter trade

- 📊 Whipsaw risk: Stock could violate both sides at different times, creating losses on both spreads

- ⚠️ Capital intensive: Need margin to hold both credit spreads simultaneously

Estimated P&L:

- 💰 Total credit collected: ~$6-8 per iron condor (depends on exact entry timing)

- 📈 Max profit: $600-800 if AMD finishes $215-235 at March expiration (our 50% base case range!)

- 📉 Max loss: $1,200-1,400 if AMD finishes above $245 or below $205

- 🎯 Breakevens: ~$209-211 (downside) and ~$241-243 (upside)

- 💀 Worst case: $1,400 loss (7x the max profit) - ugly risk/reward

CRITICAL WARNINGS - DO NOT attempt unless you:

- ✅ Have traded iron condors through earnings before and understand gap risk

- ✅ Can afford to lose ENTIRE max loss amount ($1,200-1,400 per condor)

- ✅ Understand you're fighting TWO binary events (CES tonight + earnings Feb 3)

- ✅ Have buying power to hold margin requirements for dual credit spreads

- ✅ Can monitor position daily and adjust if stock approaches strikes

- ⏰ Have plan to close profitable side after earnings IV crush and manage remaining spread

Management rules if you enter:

- Close entire iron condor if you capture 50-60% of max profit early

- If stock threatens one side (within $2 of short strike), consider buying back that spread for loss and hold the other

- DO NOT hold to expiration - close 1-2 weeks early to avoid gamma risk

- Set stop loss at 2x max profit (e.g., if collected $7, close at -$14 loss)

Risk level: EXTREME (can lose max on either side) | Skill level: Advanced only

Probability of profit: ~55-60% (slightly better than coin flip due to gamma support/resistance)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ CES keynote TONIGHT at 6:30 PM PT creates immediate volatility risk. Dr. Lisa Su's announcements on Ryzen 9 9950X3D, MI350/MI450 roadmap updates, and potential OpenAI customer wins could move the stock 3-5% after-hours. WCCFTech notes expectations are high for gaming CPU launches and AI teasers. If you enter positions before the keynote, you're gambling on unknown news. The 4.05% weekly implied move suggests options market is pricing binary outcome.

-

📊 Q4 earnings on February 3rd (29 days) is THE make-or-break catalyst. Consensus expects $9.32-9.6B revenue and $1.31 EPS, but at current valuation any miss on revenue, gross margins (need 54.5%+), or forward guidance could trigger -10-15% gap down. MarketBeat's earnings preview highlights that data center revenue trajectory and MI350 ramp commentary will be critical. The diagonal spread rolling OUT to March suggests even institutional money wants distance from this binary event.

-

💸 Stock down 16% from October all-time high of $267 - sentiment has shifted. After the explosive rally from $155 to $267 on the OpenAI partnership announcement, AMD has given back significant gains. This pullback suggests some investor skepticism about near-term execution or valuation concerns. The $220-230 trading range could persist until MI350 actually launches and proves competitive vs Nvidia.

-

🏆 Nvidia competitive moat remains MASSIVE despite AMD gains. Nvidia maintains 80-92% AI GPU market share while AMD has just 7-10%. Blackwell platform shipping in volume and Rubin launching H2 2026 (same window as AMD MI450) creates head-to-head competition. CUDA ecosystem with 6M+ developers vs ROCm's limited adoption means enterprise switching costs favor Nvidia. AMD's 8-GPU scalability limitation vs Nvidia's 72-GPU solutions prevents winning the largest datacenter deals.

-

🇨🇳 China export control uncertainty lingers despite July 2025 MI308 restart. AMD took $800M charge in Q2 2025 from export restrictions, with estimated $1.5-1.8B full-year revenue impact. While restrictions were lifted in July, future controls could hit MI325X/MI350 without warning. Proposed SAFE Chips Act could lock restrictions for 30 months. China historically represents 15-20% of AMD revenue - ongoing geopolitical risk.

-

🚀 MI350 execution risk with accelerated timeline from H2 to mid-2025. AMD pulled forward launch to improve competitive position, but compressed development increases delay/bug risk. Competing for same TSMC 3nm capacity as Apple and Nvidia creates supply constraints. The claimed 35x performance improvement vs MI300 needs real-world validation. ANY disappointment vs Nvidia Blackwell would crater the AI growth thesis.

-

📉 Massive gamma resistance at $230 (21.2B) creates mechanical ceiling. The diagonal spread trader sold calls at EXACTLY this level - not coincidental. Market makers holding 16.8B call gamma at $230 will systematically SELL into rallies to hedge exposure. This creates natural selling pressure making breakouts difficult. Would need sustained institutional buying or major catalyst to overcome. Notice how stock struggled at $230 in early October before OpenAI news broke it higher.

-

🎢 Institutional money rolling OUT of long calls into credit spreads signals defensive positioning. The $15M diagonal spread (closing January $250 calls, selling March $230 calls) shows sophisticated players REDUCING directional exposure and COLLECTING premium rather than staying naked long. When smart money shifts from "betting on upside" to "selling upside" mode, retail should pay attention. This is profit-taking behavior, not accumulation.

-

💰 OpenAI partnership expectations potentially priced in after October rally. Stock surged 34% on the announcement day and climbed from $200 to $267 (33% gain) in the following weeks. Market already pricing in $100B+ revenue over 4 years from the deal. ANY reduction in scope, timeline delays beyond H2 2026, or performance issues could crush stock 15-20%. First deployment not until mid-2026 - long time for thesis to unravel.

-

📊 Trading in no-man's-land between major support ($220) and resistance ($230-240). Gamma data shows 28.1B support at $220 (0.84% below current) and 21.2B resistance at $230 (3.7% above). Stock likely to chop in this $10 range until a catalyst provides directional conviction. This is EXACTLY the environment where iron condors and credit spreads win while directional trades get chopped up. The base case 50% probability scenario of $215-230 consolidation reflects this technical setup.

-

⚡ High implied volatility (16.5% for March) means expensive options BUT also means market expects big moves. The March $185-259 implied range represents -16% to +17% from current levels - suggesting significant two-way risk. While selling premium in high IV is attractive, it also means if you're wrong the moves will be VIOLENT. The February 3 earnings sits right in the middle of the March expiration window, creating binary event risk.

🎯 The Bottom Line

Real talk: Smart money just spent $14 MILLION selling March $230 calls on AMD while simultaneously closing out their January $250 calls for a loss. This diagonal spread roll tells us everything we need to know about institutional sentiment heading into CES (TONIGHT!) and Q4 earnings (Feb 3).

What this trade signals:

🎯 They're taking chips off the table at current levels ($222) - By selling $230 calls, they're capping upside at just 3.5% above current price through March. If they were truly bullish, they'd stay long without selling calls.

⚖️ They expect AMD to stay range-bound ($215-230) through March - The gamma data confirms this: massive resistance at $230 (21.2B) and strong support at $220 (28.1B). Stock likely chops in this zone until MI350 launches mid-2025.

⏰ They're worried about CES/earnings volatility - Rolling OUT from January to March expiration and choosing to SELL premium rather than stay long shows they want distance from binary events. When institutions go from "betting on direction" to "collecting theta" mode, it's a risk-off signal.

💰 They're locking in gains from the 2025 rally - AMD is up 77% YTD but down 16% from October highs. The trader is admitting "we rode this from $150s to $260s, let's protect profits rather than get greedy."

This is NOT a bearish signal on AMD's long-term story - it's smart risk management.

If you own AMD:

- ✅ Consider covered calls at $230 strike March expiration to copy this trade (collect ~$18-19/share)

- 🎯 Set mental stop at $220 (major gamma support) to protect against breakdown

- ⏰ Don't hold naked long through BOTH CES (tonight) and earnings (Feb 3) - too much binary risk

- 📊 If CES disappoints and stock drops to $215-218, consider adding at support

- 🛡️ At minimum, trim 20-30% at current levels to lock in YTD gains and reduce risk

If you're watching from sidelines:

- ⏰ WAIT for CES keynote tonight (6:30 PM PT) before making ANY moves

- 📊 Look for reaction: If stock rallies >5% on CES news, stay patient for pullback

- 🎯 Post-earnings pullback to $210-220 would be EXCELLENT entry with gamma support

- 📈 Ideal entry confirms: MI350 launch on track (mid-2025), Q4 earnings beat with strong guidance, data center revenue >$5B

- 🚀 Longer-term (6-12 months), OpenAI partnership and MI350/MI450 execution are legitimate catalysts for $270-300+ if delivery is flawless

If you're bearish:

- 🎯 First resistance at $225 (9.8B gamma), major resistance at $230 (21.2B gamma wall)

- 📊 Post-CES call credit spreads ($230/$240) offer defined-risk way to fade rallies

- ⚠️ Don't fight the long-term trend - AMD's AI story is real, just consolidating after huge run

- ⏰ Be patient: Better short setups emerge if stock breaks $220 support (then target $210-215)

Mark your calendar - Key events:

- 📅 January 5 (TONIGHT) 6:30 PM PT - CES 2026 Keynote by Dr. Lisa Su (gaming CPUs, AI roadmap teasers expected)

- 📅 January 9 (Friday) - Weekly options expiration (4% implied move through this)

- 📅 January 16 (Thursday) - Monthly OPEX (6% implied move window closes)

- 📅 February 3, 2026 (Monday after close) - Q4 FY2025 EARNINGS (THE BIG ONE!)

- 📅 March 20 (Friday) - Quarterly triple witch, diagonal spread expiration (16.5% implied move)

- 📅 Mid-2025 (May-June) - MI350 series launch expected

- 📅 H2 2026 - OpenAI first 1GW MI450 deployment begins

Final verdict: AMD's AI transformation story remains INCREDIBLY compelling for 2026 and beyond - the OpenAI 6GW partnership ($100B+ revenue potential), EPYC server market share gains (now 27.8% unit share), and aggressive MI350/MI450 roadmap are all real catalysts. However, after a 77% YTD rally followed by a 16% pullback, the stock is in consolidation mode between $220 support and $230 resistance.

The diagonal spread flow confirms this: Institutions are shifting from "buy and hold" to "sell premium and wait" mode. They're not bearish - they're just not aggressive bulls anymore at these levels. They want to see MI350 actually launch and prove competitive before paying up.

Be patient. Watch CES tonight for MI350/MI450 updates. Let earnings (Feb 3) clear the binary risk. Look for dips to $215-220 for entries with gamma support. AMD will still be here in 2-3 months, and you'll sleep better buying at $218 instead of chasing at $228.

The AI revolution is a marathon, not a sprint. Protect your capital. Let the setup come to you. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The diagonal spread discussed represents institutional hedging/income generation and may not be appropriate for retail traders. CES keynote (tonight) and earnings (Feb 3) create binary event risk with potential for 5-15% gaps either direction. Always do your own research and consider consulting a licensed financial advisor before trading.

About Advanced Micro Devices: Advanced Micro Devices designs digital semiconductors for PCs, gaming consoles, data centers with AI capabilities, industrial, and automotive markets. The company is strengthening its position in AI GPUs while maintaining its traditional focus on CPUs and graphics processors, with a market cap of $363.8 billion in the Semiconductors & Related Devices industry.