AMD $23M Put Sell - Institutional Closing Position Ahead of Earnings

January 12, 2026 | Unusual Activity Detected

The Quick Take

Someone just sold $23 million worth of AMD $240 puts expiring January 16th - just 4 days before expiration. This isn't a new bearish bet; it's an institutional player closing out a protective position or collecting premium as time decay accelerates. With AMD trading at $209.63 and Q4 2025 earnings on February 3rd approaching, this trade suggests the put holder believes the immediate downside risk has passed. Translation: Smart money is cashing out insurance they no longer need.

Company Overview

Advanced Micro Devices (AMD) is a global semiconductor powerhouse competing with NVIDIA in the AI accelerator market:

- Market Cap: $330.8 Billion

- Industry: Semiconductors & Related Devices

- Current Price: $209.63

- 52-Week Range: $117.32 - $267.08

- Primary Business: Data center CPUs/GPUs, PC processors, gaming graphics, embedded systems

- Key Catalyst: 6-gigawatt OpenAI partnership announced October 2025

The Option Flow Breakdown

The Tape (January 12, 2026):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:53:27 | AMD | MID | SELL | PUT $240 | 2026-01-16 | $23M | $240 | 7,500 | 27K | 7,500 | $209.63 | $30.40 |

Option Symbol: AMD20260116P240

What This Actually Means

This is a position close or premium collection trade. Here's the breakdown:

- Premium received: $23M ($30.40 per contract × 7,500 contracts × 100)

- Strike relationship: $240 puts are now deep in-the-money with AMD at $209.63

- Intrinsic value: ~$30.37 (strike $240 - spot $209.63)

- Time value: ~$0.03 - almost entirely intrinsic value

- Days to expiration: Only 4 days remain

- Open Interest: 27,000 contracts at this strike - significant existing position

What's really happening here:

With only 4 days until expiration and the puts deep ITM, there are two likely scenarios:

-

Closing a protective hedge: An institution that bought these puts as insurance on a large AMD long position is now closing out before expiration to avoid assignment. They're taking their profits ($30+ per contract) on puts that are now worth significantly more than when purchased.

-

Short put position: Less likely given the "SELL" direction, but could be selling puts to collect premium betting AMD won't drop another $30 from here.

The Z-score of 2.45 and "HIGHLY_UNUSUAL" classification confirms this is institutional activity, not retail flow. The size (7,500 contracts = 750,000 shares = ~$157M notional exposure) indicates a sophisticated player managing a significant position.

Unusual Score: MODERATE-HIGH - While the 2.45 Z-score is elevated, this appears to be position management rather than a new directional bet. The "CLOSE" volume signal supports this interpretation.

Technical Setup

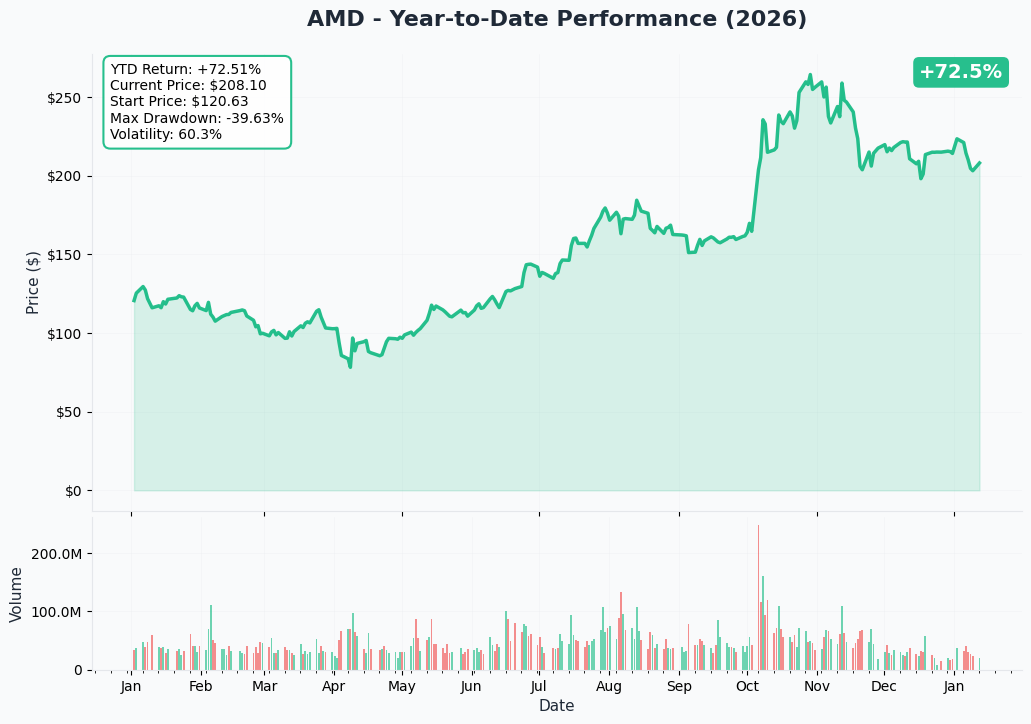

YTD Performance Chart

AMD has had a volatile 2025, currently trading at $209.63 - down significantly from its October 2025 highs near $267 after the OpenAI partnership announcement:

Key YTD observations:

- YTD 2025 Performance: +77% (outpaced NVIDIA's +34%)

- 52-Week High: $267.08 (October 2025 post-OpenAI deal)

- 52-Week Low: $117.32

- Current Pullback: -21% from highs

- Major Support Tested: $200 psychological level held in recent sessions

The chart shows AMD rallied aggressively through mid-2025 on AI momentum, peaked in October with the OpenAI partnership (+34% surge on announcement), and has since corrected as the market digests the aggressive valuation (55x forward P/E). The current consolidation between $200-$220 suggests the market is waiting for Q4 earnings confirmation on February 3.

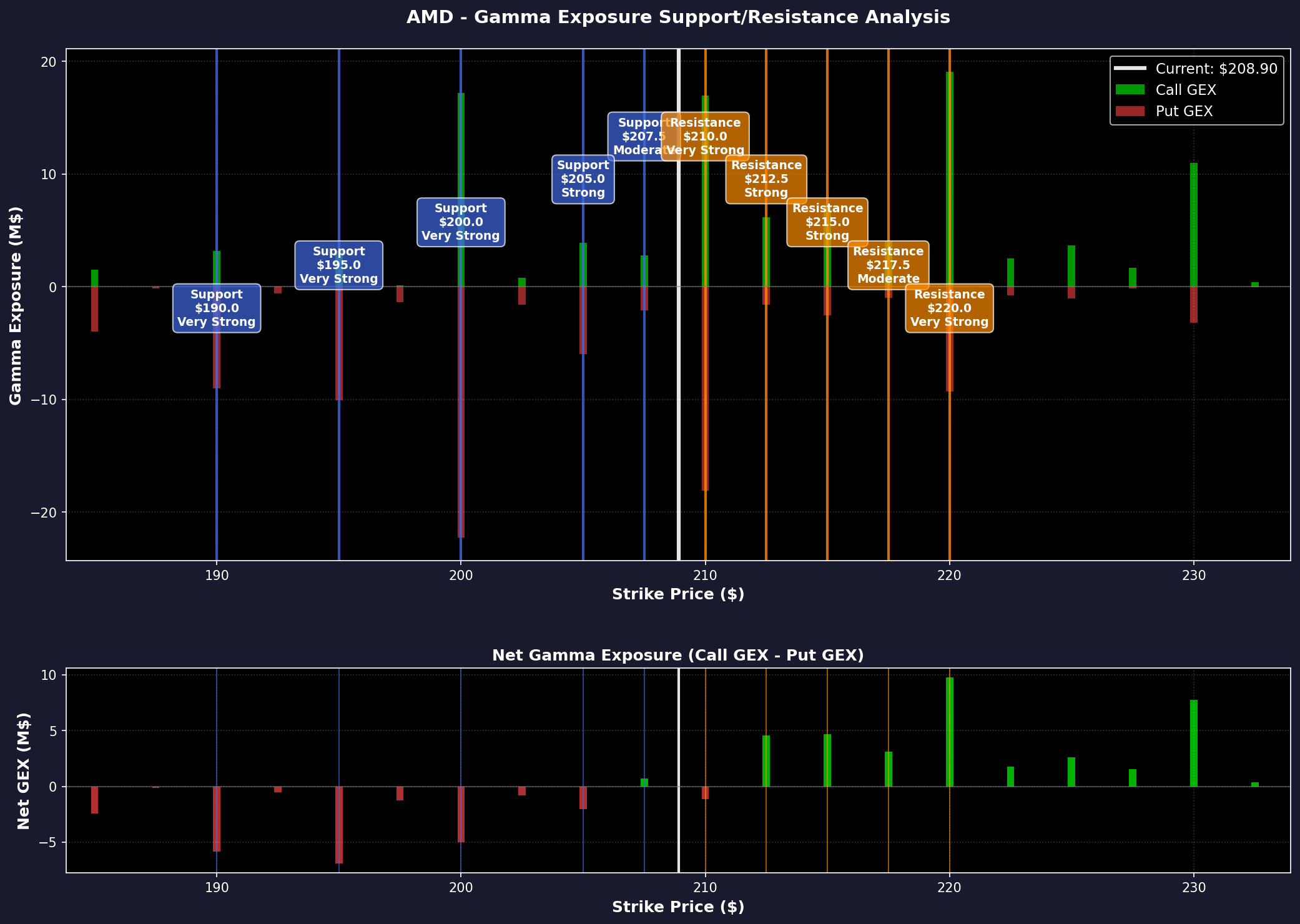

Gamma-Based Support & Resistance Analysis

Current Price: $208.98

Support Levels (Put Gamma Below Price):

- $205 - Immediate support with 9.84B total gamma (1.9% below)

- $200 - Major psychological floor with 39.37B gamma (4.3% below) - STRONGEST SUPPORT

- $195 - Secondary support at 13.23B gamma (6.7% below)

- $190 - Extended support at 12.13B gamma (9.1% below)

- $180 - Deep floor at 10.78B gamma (13.9% below)

Resistance Levels (Call Gamma Above Price):

- $210 - Immediate ceiling with 34.98B gamma (0.5% above) - STRONGEST RESISTANCE

- $215 - Secondary resistance at 9.81B gamma (2.9% above)

- $220 - Major resistance zone with 28.38B gamma (5.3% above)

- $230 - Extended ceiling at 14.18B gamma (10.1% above)

- $250 - Distant target at 8.91B gamma (19.6% above)

Net GEX Bias: Bullish (160.8B call gamma vs 137.0B put gamma)

What this means: AMD is trading in a tight consolidation zone with massive resistance at $210 and critical support at $200. The gamma structure suggests price will likely oscillate between these levels until a catalyst (earnings Feb 3) provides direction. The put seller at $240 is WAY above current price - this was a protective position that's now being closed as the risk window has passed.

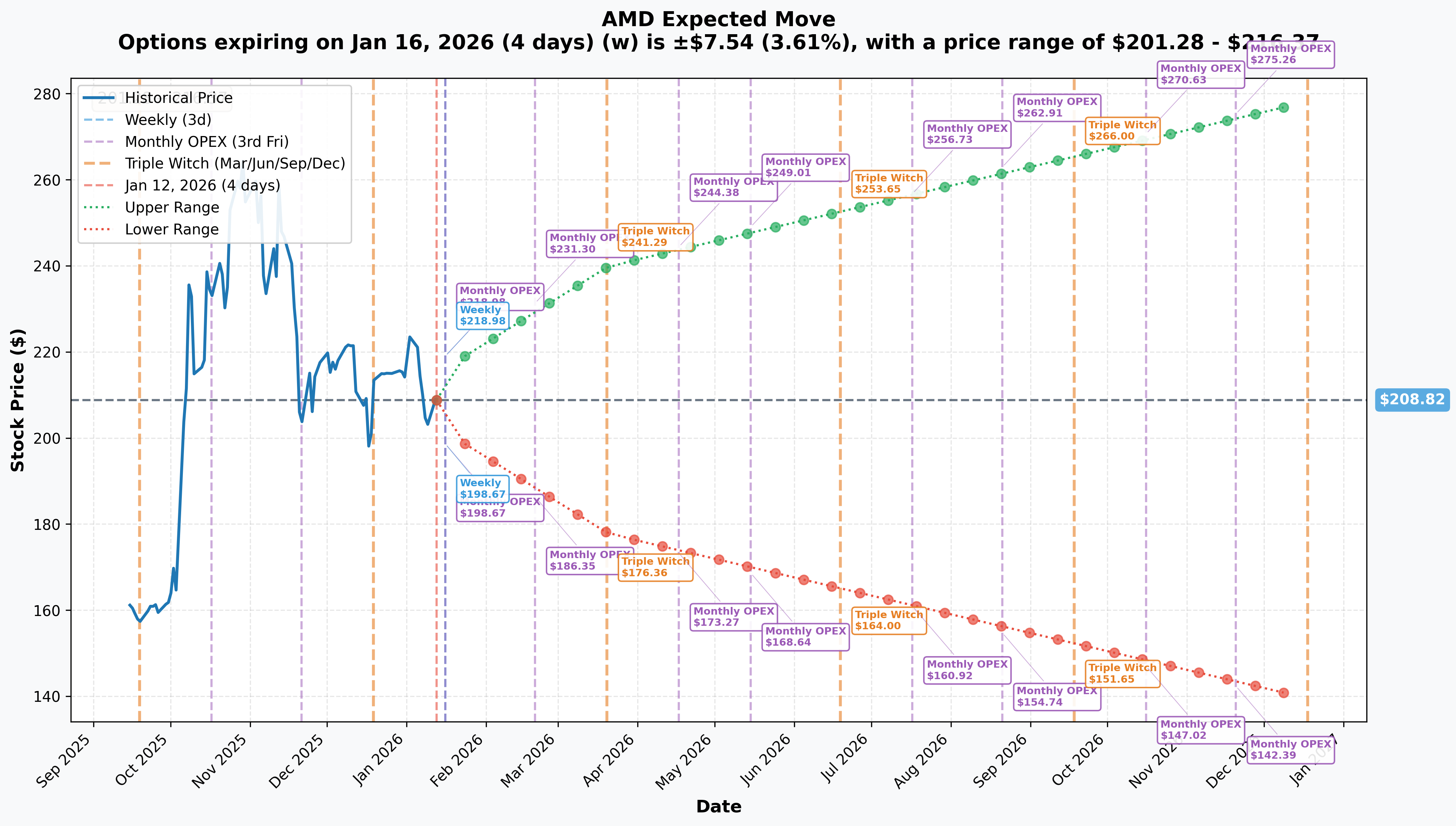

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 16 - 4 days): ±3.61% (±$7.54) → Range: $201.28 - $216.37

- Monthly OPEX (Feb 20): ±10.76% (±$22.48) → Range: $186.35 - $231.30

- Quarterly Triple Witch (Mar 20): ±14.88% (±$31.07) → Range: $177.76 - $239.89

- Yearly LEAPS (Dec 18): ±33.22% (±$69.38) → Range: $139.44 - $278.21

Translation:

The options market is pricing a relatively calm week (±3.6%) but expects significant volatility around February earnings (±10.8% monthly). The $240 put strike sits above the weekly implied upper range ($216.37) - confirming these puts were deep ITM hedges being closed, not active bets on further downside.

The quarterly implied range ($177.76 - $239.89) encompasses the full bull and bear scenarios through Q1 2026, with the Q4 earnings on February 3rd being the primary catalyst.

Catalysts

Immediate Catalysts (Next 30 Days)

Q4 2025 Earnings - February 3, 2026

AMD reports fiscal Q4 results on February 3, 2026 after market close. This is the most significant near-term catalyst:

- Revenue Consensus: ~$9.6B (+25% YoY) per company guidance

- EPS Consensus: $1.10-$1.31 per analyst estimates

- Key Focus Areas:

- Data Center GPU revenue trajectory (MI350 is "fastest ramping product in AMD history")

- OpenAI deployment timeline updates

- 2026 revenue guidance and AI contribution targets (CEO Lisa Su targets "tens of billions in annual revenue in 2027")

- Embedded segment recovery confirmation (eight consecutive quarters of YoY decline per Q3 financials)

- China export restriction impact quantification ($1.5-1.8B estimated 2025 revenue impact)

Why this matters for the trade: The put seller is closing out 4 days before expiration (Jan 16) but 3 weeks before the major earnings catalyst (Feb 3). They've decided the near-term risk has diminished enough to exit their hedge.

Near-Term Catalysts (Q1-Q2 2026)

MI450 OpenAI Deployment - H2 2026

The 6-gigawatt OpenAI partnership announced October 2025 includes:

- First 1GW deployment of MI450 GPUs beginning H2 2026 (OpenAI partnership details)

- Estimated $90B+ cumulative hardware revenue over the partnership; AMD expects $100B+ in total revenue over four years

- 160 million share warrant for OpenAI tied to AMD achieving $600/share targets

- Validates AMD as credible NVIDIA alternative at hyperscale (shares surged 34% on announcement)

Product Launches (Q1-Q2 2026):

- Q1 2026: Ryzen AI 400/PRO 400 Series PCs from Acer, ASUS, Dell, HP, GIGABYTE, Lenovo

- Q2 2026: Ryzen AI Halo developer mini-PC for local LLM development

- Q3 2026: Helios platform launch (competing with NVIDIA NVL72)

Risk Catalysts (Negative)

Export Restrictions & Geopolitical Risk

AMD faces ongoing China exposure concerns per multiple reports:

- $800M charge in Q2 2025 for MI308 inventory write-down and canceled orders

- $1.5-1.8B estimated 2025 revenue impact from export controls

- Pending license application "for a few quarters" per CEO Su (AInvest analysis)

- Potential SAFE Chips Act legislation blocking exports until 2028

NVIDIA Competitive Response

NVIDIA's Vera Rubin architecture launching H2 2026 with:

- Microsoft, AWS, Google, CoreWeave partnerships

- CUDA ecosystem maintaining 18+ years of developer investment

- ROCm still 10-30% behind CUDA in compute-intensive workloads; parity projected for 2026-2027

- NVIDIA maintains 80-92% AI accelerator market share vs AMD's <10%

Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timing:

Bull Case (30% probability)

Target: $240-$260

How we get there:

- Q4 earnings beat ($9.8B+ revenue) with strong 2026 guidance

- MI350 adoption accelerating ahead of expectations

- OpenAI deployment on track for H2 2026

- Server CPU share exceeds 40% (currently 27.8%)

- Break above $220 gamma resistance triggers momentum to $230-$250

Key metrics needed:

- Data center revenue >$4.5B for Q4

- AI revenue trajectory toward "tens of billions" confirmed

- Gross margins stable at 54%+

Base Case (50% probability)

Target: $195-$225 range (Consolidation)

Most likely scenario:

- Q4 earnings in-line with guidance (~$9.6B)

- MI350 ramp progressing but not spectacular

- Stock trades between $200 support and $220 resistance through Q1

- Waits for OpenAI deployment proof points in H2 2026

- Put seller's thesis validated - no near-term crash, position closed profitably

Bear Case (20% probability)

Target: $160-$190

What could go wrong:

- Q4 earnings miss or weak 2026 guidance

- MI350 delays or competitive concerns vs Blackwell

- China export restrictions expand

- OpenAI deployment timeline pushed out

- Break below $200 gamma support triggers cascade to $180

Trading Ideas

Conservative: Wait for Earnings Clarity

Play: Stay on sidelines until February 3rd Q4 earnings

Why this works:

- 55x forward P/E leaves no margin for error

- Earnings in 3 weeks creates binary event risk

- Better entry at $195-200 support if tested

- Current price in no-man's land between support/resistance

Risk level: Minimal | Skill level: Beginner-friendly

Balanced: Post-Earnings Put Spread

Play: If earnings disappoint, buy $210/$195 put spread (March expiration)

Structure: Buy $210 put, Sell $195 put

Why this works:

- Defined risk ($15 wide = $1,500 max risk per spread)

- Targets gamma support zone $195-$200

- March expiration captures Q4 reaction and Q1 developments

- IV crush post-earnings reduces entry cost

Entry timing: Wait 2-3 days post-Feb 3 earnings

Risk level: Moderate | Skill level: Intermediate

Aggressive: Earnings Straddle

Play: Buy $210 straddle for February expiration

Why this could work:

- ±10.8% monthly implied move suggests significant volatility expected

- Q4 results + 2026 guidance create multiple binary outcomes

- OpenAI deployment updates could surprise either direction

Serious risks:

- IV crush post-earnings could cause loss even if stock moves

- Requires >12% move to profit after theta decay

- 55x P/E means stock punished severely on any miss

Risk level: HIGH | Skill level: Advanced only

Risk Factors

Critical risks to monitor:

-

Valuation stretched at 55x forward P/E: Stock priced for perfect execution. Any disappointment in Q4 earnings, guidance, or product ramp magnified 3-4x at current multiple. The 21% pullback from highs reflects market uncertainty about AI monetization timeline.

-

NVIDIA competitive moat remains dominant: Despite OpenAI partnership, AMD still <10% AI accelerator market share vs NVIDIA's 80-90%. CUDA ecosystem creates powerful lock-in that ROCm hasn't overcome. MI350 must prove competitive with Blackwell.

-

China export restrictions wildcard: $1.5-1.8B 2025 revenue impact already priced in, but further restrictions possible. Geopolitical tensions with Taiwan (TSMC manufacturing) add tail risk.

-

OpenAI execution risk: $90B+ revenue projection depends on successful H2 2026 deployment. Any delays, technical issues, or scope reduction could significantly impact valuation multiple.

-

Embedded segment weakness: Eight consecutive quarters of YoY decline. Recovery expected but not confirmed. Represents drag on overall growth narrative.

The Bottom Line

Real talk: This $23M put sale is not a new directional bet - it's an institution closing out a protective position that's now deep in the money with only 4 days left. The trade tells us:

- Risk window has passed (for now): The put holder believes the immediate downside risk they were hedging against (likely earnings-related from Q3) has diminished

- Position management, not prediction: They're taking profits on puts worth $30+ and moving on

- Consolidation expected: With AMD trapped between $200 support and $220 resistance, big moves require a catalyst

- February 3rd is the next big date: Q4 earnings will determine if AMD breaks out toward $240 or retests $180

If you own AMD:

- Consider trimming 20-30% at $215-$220 resistance tests

- Set mental stop at $195 (below major gamma support)

- February 3rd earnings is your decision point - have a plan before the number

If you're watching from sidelines:

- Wait for Q4 earnings clarity before initiating

- $195-200 would be excellent entry with gamma support

- Need to see MI350 customer wins and strong 2026 guidance to justify current valuation

If you're bearish:

- Post-earnings put spreads offer better risk/reward than current timing

- Watch for break below $200 gamma support as confirmation signal

- 55x P/E creates amplified downside on any execution stumble

Key dates:

- January 16, 2026 - Weekly OPEX (this put expires)

- February 3, 2026 - Q4 2025 earnings (after market close)

- February 20, 2026 - Monthly OPEX

- H2 2026 - OpenAI MI450 deployment begins

Final verdict: This put sale signals institutional positioning is shifting from "hedge against crash" to "wait and see." AMD's long-term AI story remains compelling - OpenAI partnership, server CPU gains, aggressive product roadmap. But at 55x forward P/E with earnings 3 weeks away, the risk/reward favors patience. Let Q4 results clarify the trajectory before committing capital.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Always do your own research and consider consulting a licensed financial advisor before trading.

About Advanced Micro Devices: Advanced Micro Devices designs digital semiconductors for PCs, gaming consoles, data centers (including AI accelerators), industrial, and automotive applications. The company competes with Intel in CPUs and NVIDIA in GPUs, with a market cap of $330.8 billion.