AMD $8M LEAPS Put - Institutional Protection Before Q4 Earnings

January 26, 2026 | Unusual Activity Detected

The Quick Take

Someone just dropped $8 MILLION on AMD LEAPS puts expiring January 2027 with a $300 strike - that's almost a year out and roughly 19% above current price! This isn't a directional bearish bet; it's sophisticated portfolio insurance from an institution protecting a massive long AMD position ahead of Q4 2025 earnings on February 3rd. With AMD up nearly 90% YTD and trading at $251.60, smart money is paying up for downside protection while staying long the AI chip revolution. Translation: Big players love the AMD story but aren't taking chances with earnings 8 days away.

Company Overview

Advanced Micro Devices (AMD) is a semiconductor powerhouse competing head-to-head with Nvidia in the AI accelerator market:

- Market Cap: $422.8 Billion

- Industry: Semiconductors & Related Devices

- Current Price: $251.60 (near 52-week high of $267.08)

- Primary Business: PC/server CPUs, AI/data center GPUs, gaming graphics, embedded processors

- Employees: 28,000

- Headquarters: Santa Clara, California

AMD has evolved from a traditional CPU/GPU maker into a serious contender in AI infrastructure, validated by the landmark OpenAI partnership worth potentially $100B+ over four years. Seven of the top 10 AI model-development companies now run production workloads on AMD Instinct accelerators.

The Option Flow Breakdown

The Tape (January 26, 2026)

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | OI | Premium | Spot | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-26 | 13:34:50 | AMD | BUY | PUT $300 | 2027-01-15 | $300 | 1,000 | - | $8,000,000 | $251.60 | AMD20270115P300 |

What This Actually Means

This is a LEAPS put hedge protecting a large long equity position. Here's the breakdown:

- Massive premium: $8M for 1,000 contracts ($80 per contract, $8,000 per option)

- Deep OTM strike: $300 is 19% ABOVE current price - this is a volatility/tail-risk play

- Ultra-long duration: 354 days to expiration covers multiple earnings cycles

- Position equivalent: 100,000 shares exposure worth roughly $25M

- Unusual Score: Z-score of 28.02 (EXTREMELY UNUSUAL) - this size happens only a few times per year

What's really happening: This trader owns a substantial AMD position (likely $50M+) and is buying portfolio insurance that pays off if AMD experiences a major crash. The $300 strike seems counterintuitive since it's above current price, but LEAPS puts this far OTM capture volatility expansion and protect against tail risk scenarios. If AMD rallies to $350+ and then crashes, these puts become valuable quickly. If AMD stays flat or slowly declines, the trader loses the $8M premium but keeps their long exposure.

This is classic institutional risk management - not a bearish call on AMD fundamentals.

Technical Setup / Chart Check-Up

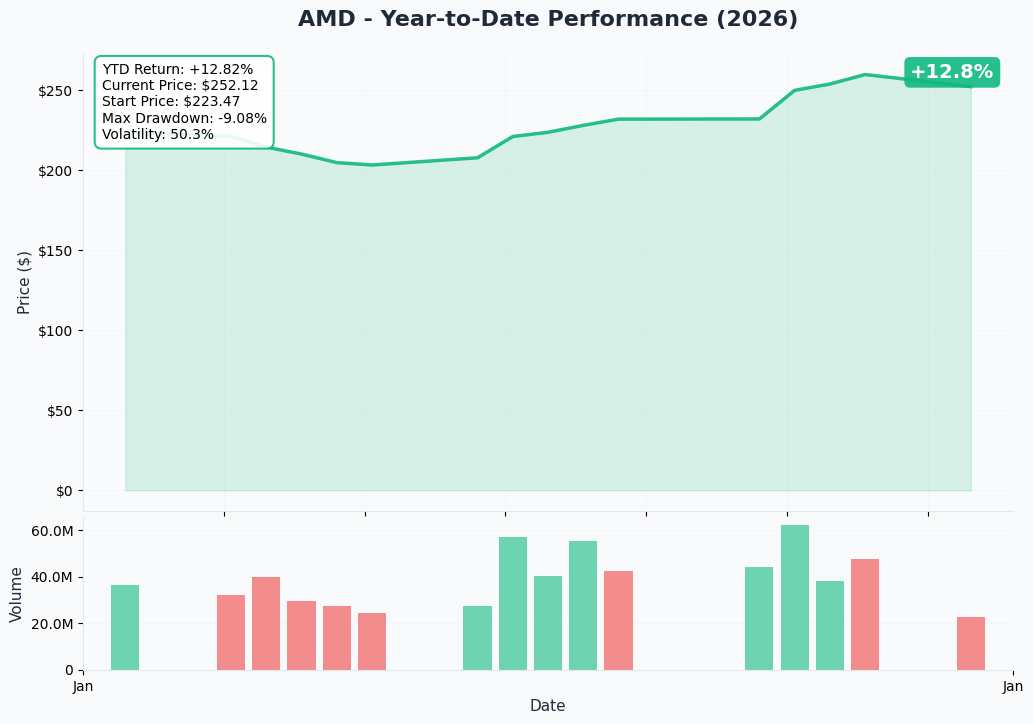

YTD Performance Chart

AMD has delivered impressive gains in 2025-2026, up approximately 89% YTD from $122.63 to current levels around $251.60. The chart shows:

- Recovery rally: Bounced hard from April 2025 lows of $76.48 (driven by China export restriction charges)

- All-time high: Reached $267.08 in late October 2025 following the OpenAI partnership announcement

- Consolidation zone: Trading in $220-260 range since November 2025

- Key level: Currently testing the $250 support/resistance zone

The stock has shown resilience despite broader semiconductor volatility, supported by the transformational OpenAI partnership and strong data center momentum.

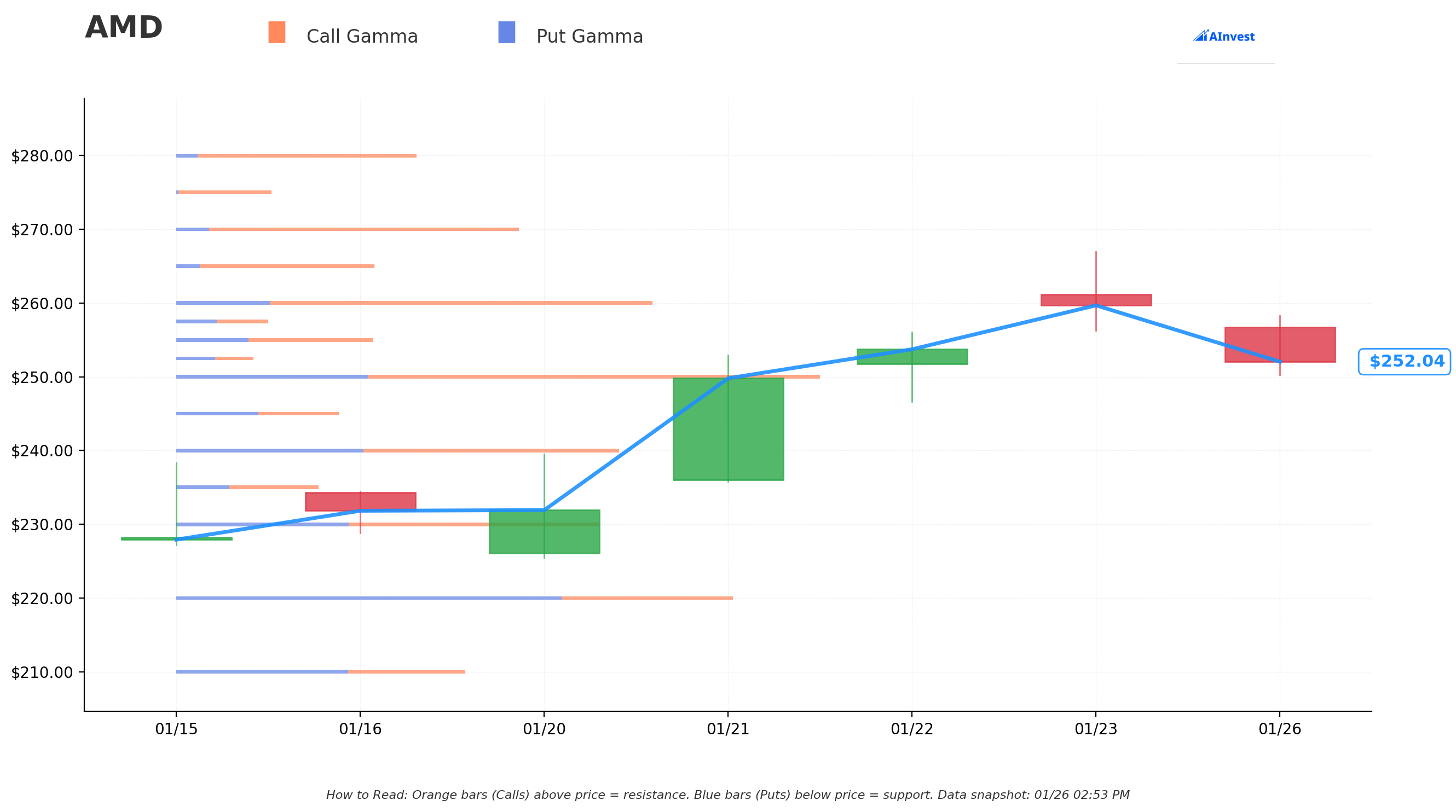

Gamma-Based Support & Resistance Analysis

Current Price: $251.60

The gamma exposure map reveals where market makers are heavily positioned and where price is likely to find support or resistance:

Support Levels (Put Gamma - Blue Bars):

| Strike | Net GEX | Total GEX | Distance |

|---|---|---|---|

| $250 | +7.34B | 18.1B | 0.6% - IMMEDIATE FLOOR |

| $240 | +1.91B | 12.5B | 4.6% - Secondary support |

| $230 | +2.18B | 12.0B | 8.6% - Extended support |

| $220 | -5.96B | 15.8B | 12.6% - Major structural floor |

| $210 | -1.56B | 8.2B | 16.5% - Disaster scenario |

Resistance Levels (Call Gamma - Orange Bars):

| Strike | Net GEX | Total GEX | Distance |

|---|---|---|---|

| $260 | +8.12B | 13.4B | 3.3% - IMMEDIATE CEILING |

| $265 | +4.22B | 5.5B | 5.3% - Secondary resistance |

| $270 | +7.77B | 9.6B | 7.3% - Major barrier |

| $280 | +5.54B | 6.7B | 11.3% - Extended resistance |

| $300 | +7.29B | 8.1B | 19.2% - PUT STRIKE LEVEL |

What this means for traders:

AMD is trading in a tight range between $250 support (strongest nearby gamma floor with 18.1B total exposure) and $260 resistance (8.12B net gamma creating selling pressure). The $250 level is critical - a break below could accelerate moves toward $240, then $230.

Notice that the put buyer's $300 strike aligns with significant gamma resistance at that level. If AMD rallies to $300 and then reverses, the puts would gain value rapidly as the stock falls through multiple gamma levels.

Net GEX Bias: Bullish (131B call gamma vs 82B put gamma) - Overall positioning remains bullish, but near-term upside is capped by the $260 ceiling.

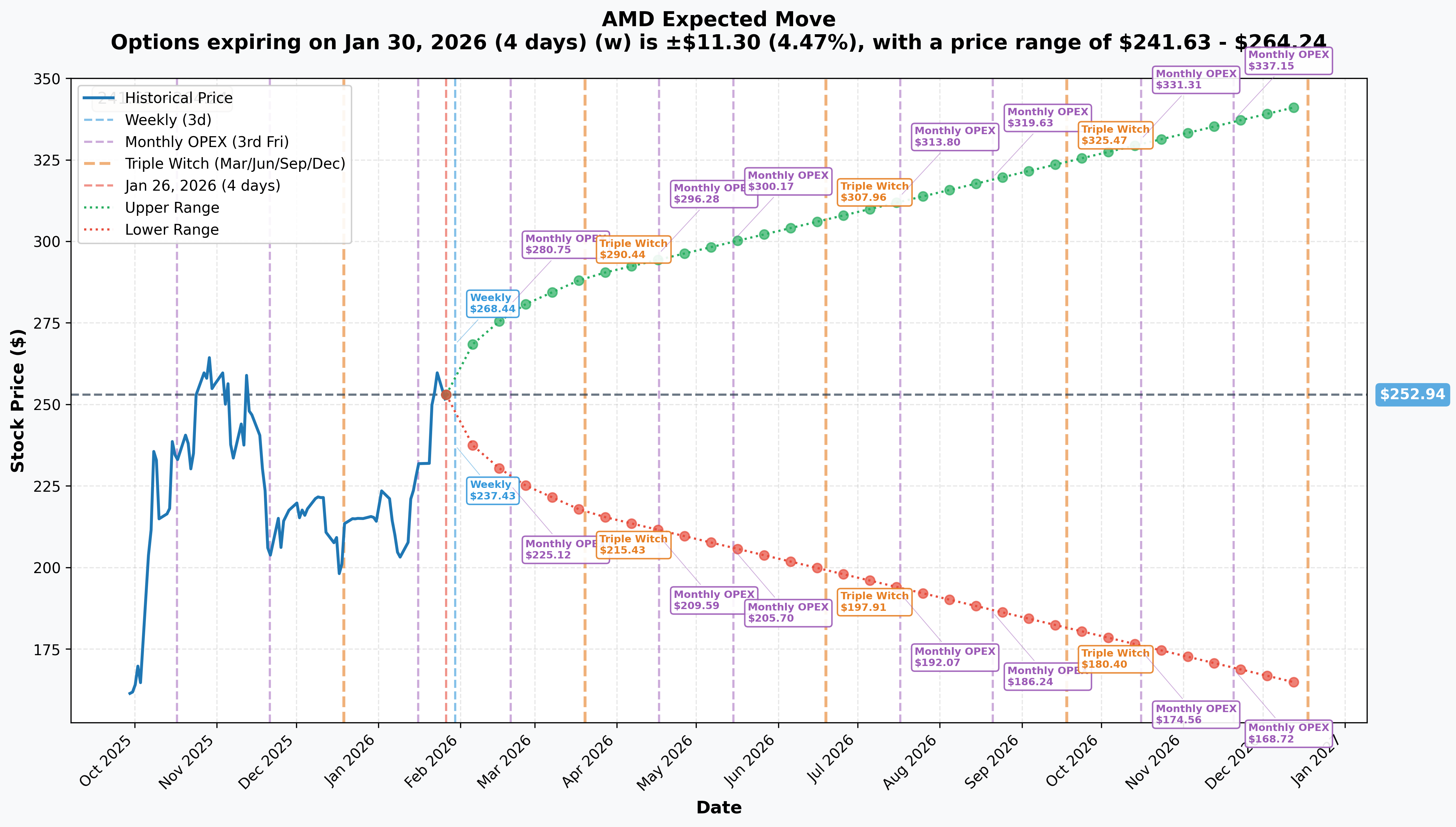

Implied Move Analysis

Options market expectations across key timeframes:

| Expiration | Days | Implied Move | Upper Range | Lower Range |

|---|---|---|---|---|

| Weekly (Jan 30) | 4 | +/-4.47% ($11.30) | $264.24 | $241.63 |

| Monthly OPEX (Feb 20) | 25 | +/-10.28% ($26.01) | $278.94 | $226.93 |

| Triple Witch (Mar 20) | 53 | +/-14.29% ($36.15) | $289.08 | $216.79 |

| LEAPS (Dec 18) | 326 | +/-35.29% ($89.27) | $342.21 | $163.66 |

Translation for regular folks:

The options market is pricing in a 4.5% move ($11) by end of this week and a 10% move ($26) through February OPEX - which includes the critical Q4 earnings on February 3rd. That's significant volatility for a $420B market cap company!

The February monthly expiration (which covers earnings) shows expected range of $227-$279. If AMD misses expectations, a drop to $230 is within the realm of options-market expectations. If they crush it, $280 is the implied upside.

For the LEAPS expiration (December 2026), options are pricing in potential moves to as low as $164 or as high as $342 - a massive range reflecting AI market uncertainty.

Catalysts

Upcoming Catalysts

Q4 2025 Earnings - February 3, 2026 (8 DAYS AWAY!)

AMD reports fiscal Q4 2025 results on Tuesday, February 3, 2026 after market close. This is THE catalyst driving near-term volatility.

Consensus Estimates:

| Metric | Consensus | YoY Growth |

|---|---|---|

| Revenue | $9.6-$9.63B | +25-26% |

| EPS (Non-GAAP) | $1.10-$1.31 | +21-25% |

Key Metrics to Watch:

- Data center revenue trajectory (Q3 was record $4.3B)

- MI350 series ramp commentary and customer adoption

- OpenAI deployment timeline updates

- China revenue outlook post-export policy changes

- Full-year 2026 guidance

Source: AMD Investor Relations, Nasdaq Earnings

MI450 Production Ramp - H2 2026

AMD's next-generation Instinct MI450 accelerators begin mass production in H2 2026:

- CDNA 5 architecture with 432GB HBM4 memory

- 19.6TB/s bandwidth, up to 40 petaflops FP4 performance

- First deployment: OpenAI 1-gigawatt commitment starting H2 2026

- Oracle AI supercluster with 50,000 GPUs launching Q3 2026

Helios Rack-Scale Platform Launch - 2026

AMD's Helios rack architecture delivers up to 3 AI exaflops per rack:

- 72 MI400 series GPUs per rack

- 260 TB/s scale-up bandwidth

- EPYC Venice CPUs and Pensando Vulcano AI NICs

Recent Catalysts (Already Happened)

Q3 2025 Earnings Beat (November 4, 2025)

AMD delivered record Q3 results that exceeded expectations:

- Revenue: $9.25B (vs $8.74B consensus, +36% YoY)

- EPS: $1.20 (vs $1.17 consensus, +58% YoY)

- Data Center Revenue: Record $4.3B (+23% YoY)

- Gross Margin: 54%

Source: CNBC Q3 Report

OpenAI Strategic Partnership (October 6, 2025)

The landmark multi-year partnership represents AMD's most transformative catalyst:

- 6 gigawatts of AMD GPUs to be deployed across multiple generations

- First 1-gigawatt MI450 deployment starting H2 2026

- Revenue potential: Tens of billions annually, potentially $100B+ cumulative over four years

- AMD issued OpenAI warrants for up to 160 million shares (~10% of outstanding)

Source: AMD Press Release, CNBC

CES 2026 Keynote (January 5, 2026)

Dr. Lisa Su unveiled major product announcements at CES 2026:

- Helios Rack-Scale Platform: "World's best AI rack" with MI455X GPUs

- MI500 Series Preview: 1,000x AI performance vs MI300X, launching 2027

- Ryzen AI 400 Series: 60 TOPS NPU, shipping January 2026

Source: Tom's Hardware

Financial Analyst Day (November 11, 2025)

AMD unveiled aggressive long-term targets:

- Data Center AI Revenue CAGR: >80%

- Company Revenue CAGR: >35% over 3-5 years

- Operating Margin Target: >35% non-GAAP

- EPS Target: Exceeding $20 over 3-5 years

- 2030 Data Center Revenue Goal: $100B annually

Price Targets & Probabilities

Based on gamma levels, implied move data, and upcoming catalysts:

Bull Case (30% probability)

Target: $280-$300

How we get there:

- Q4 earnings CRUSH expectations with revenue toward $10B

- MI350 customer wins announced beyond OpenAI/Oracle

- 2026 guidance surprises to upside ($45B+ revenue)

- Breakout above $270 gamma resistance triggers momentum buying

- Market share gains accelerate to 10%+ vs Nvidia

Key validation needed:

- Data center revenue growth >30% YoY

- Gross margins expanding toward 55%

- Clear MI450 production timeline confirmation

Base Case (50% probability)

Target: $240-$270 range (Consolidation)

Most likely scenario:

- Solid Q4 earnings meeting consensus (~$9.6B revenue)

- MI350/MI450 ramp progressing as expected

- Guidance in-line with Street expectations

- Stock trades within gamma support ($250) and resistance ($260-$270)

- Volatility settles post-earnings, stock consolidates gains

This is likely what the put buyer expects - the stock chops around while they maintain long exposure with downside protection.

Bear Case (20% probability)

Target: $200-$240

What could trigger this:

- Q4 earnings miss or conservative 2026 guidance

- MI350 adoption slower than expected due to CUDA ecosystem lock-in

- New China export restrictions hitting MI325X/MI350

- Broader tech selloff or recession fears

- Break below $250 gamma support triggers cascade to $230, then $220

Critical support levels:

- $250: Major gamma floor - MUST HOLD

- $240: Secondary support, aligns with implied move lower bound

- $230: Extended floor, would represent ~9% drawdown

- $220: Disaster scenario, significant put gamma at this level

Trading Ideas

Conservative: Cash-Secured Put at Support

Play: Sell February 21 $240 put (25 DTE)

Why this works:

- $240 strike sits at strong gamma support with 12.5B total exposure

- Implied volatility elevated pre-earnings = higher premium collection

- If assigned, you own AMD at ~$235 effective cost basis (10% below current)

- If AMD stays above $240 (likely base case), keep premium as income

- Earnings binary risk is captured in premium pricing

Estimated Premium: $6-8 per contract ($600-800 per 100 shares)

Max Loss: $23,200-$23,400 per contract (if AMD goes to zero, which it won't)

Realistic Risk: AMD at $220 = $1,200 loss per contract after premium

Best for: Investors who want to own AMD at lower prices anyway

Balanced: Call Spread for Earnings Pop

Play: Buy February 21 $255/$275 call spread (25 DTE)

Structure:

- Buy AMD $255 call

- Sell AMD $275 call

Why this works:

- Captures upside through $270 gamma resistance if earnings beat

- Defined risk - max loss is debit paid

- February expiration gives time for post-earnings follow-through

- $275 short call reduces cost and provides realistic upside target

- Implied move suggests $279 upper range is achievable

Estimated Cost: $8-10 per spread ($800-1,000 risk)

Max Profit: $2,000 per spread if AMD above $275 at expiration

Breakeven: ~$263-265 (depending on entry)

Best for: Traders bullish on earnings but wanting defined risk

Aggressive: LEAPS Call for AI Thesis

Play: Buy January 2027 $280 call (matching the put buyer's timeframe)

Why this works:

- If the $8M put buyer is hedging a massive long, they expect AMD higher long-term

- LEAPS timeframe captures MI450 launch, OpenAI deployment, potential $300+ move

- Implied move to December 2026 shows $342 upper range possible

- Management targets >35% revenue CAGR support thesis

- ROCm software improvements closing gap with CUDA

Estimated Cost: $40-50 per contract ($4,000-5,000 per option)

Breakeven: ~$320-330 by January 2027

Target: AMD at $350 = ~$70 value, 40-75% gain

Risks:

- AI spending slowdown could crush valuation

- Nvidia competitive moat remains formidable

- China export policy uncertainty

- Premium expensive at current IV levels

Best for: Aggressive traders with high conviction on AMD's AI opportunity

Risk Factors

Don't get caught by these potential landmines:

-

Earnings binary event in 8 days: Q4 results on February 3rd could move the stock 10%+ either direction. Options pricing in +/-10% move through February OPEX. Even solid results could trigger "sell the news" given 89% YTD gains.

-

Valuation requires flawless execution: At 34-39x forward P/E (down from peak but still premium), AMD is priced for aggressive AI growth. Management's >35% revenue CAGR target is ambitious. Any execution stumble gets punished severely at this multiple.

-

Nvidia's 85% market share and CUDA moat: Despite AMD's gains, Nvidia dominates with 85%+ AI GPU share. CUDA ecosystem creates powerful lock-in that ROCm hasn't fully overcome. The 10-30% performance gap (down from 40-50%) still matters for enterprise adoption.

-

China export controls remain wildcard: AMD took $800M charge in Q2 2025 from MI308 restrictions. Future export controls could hit MI325X/MI350 without warning. The SAFE Chips Act could lock in restrictions through 2028.

-

Intel-NVIDIA partnership creates new competitive risk: AMD cited this partnership in Q3 2025 10-Q as material business risk. Potential for integrated RTX SoC threatening AMD's APU advantage in client segment. Tom's Hardware analysis

-

MI450 execution risk: First major deployment for OpenAI in H2 2026. Must achieve volume production and reliability for 50,000+ GPU deployments. TSMC 2nm capacity allocation competition. Any delays or performance issues could derail momentum.

-

HBM4 memory pricing pressure: Fixed pricing terms ending in 2026 may impact GPU costs. Memory pricing dynamics could pressure margins.

-

Insider selling pattern: Recent insider selling through 2025 (routine/programmatic) with no open-market buying in last 3 months. GuruFocus data

The Bottom Line

Here's the deal: Someone just paid $8 MILLION for LEAPS put protection on a massive AMD position - and they chose a $300 strike that's 19% above current price with almost a year to expiration. This isn't a bearish bet; it's sophisticated institutional risk management from someone who wants to stay long AMD through the AI revolution but isn't taking chances with Q4 earnings 8 days away.

What this trade tells us:

- Big money is BULLISH long-term (they own the stock/calls) but CAUTIOUS short-term (buying expensive protection)

- They expect volatility through 2026 - multiple earnings cycles, MI450 launch, OpenAI deployment

- The $300 strike suggests they're protecting against tail risk, not near-term weakness

- Z-score of 28.02 means this size is extremely rare - someone with serious conviction and capital

If you own AMD:

- Consider the institutional playbook: maintain exposure but add some protection ahead of earnings

- The $250 gamma support level is your mental stop - a break below gets concerning

- Don't panic on a pullback to $240 - that's where strong institutional support sits

- Mark February 3rd on your calendar - be prepared for volatility

If you're watching from sidelines:

- Wait for earnings to clear before initiating new positions

- A pullback to $240-250 post-earnings would be a solid entry opportunity

- Look for confirmation: revenue beat, margin expansion, bullish 2026 guidance

- The AI thesis remains intact - OpenAI partnership validates AMD at the highest level

If you're bearish:

- Don't fight the tape into earnings - wait for the event

- Post-earnings put spreads offer defined-risk downside exposure after IV crush

- Watch for break below $250 - that's the trigger for acceleration lower

- Key bear case triggers: guidance miss, MI350 delays, China export escalation

Key dates to mark:

- February 3, 2026: Q4 2025 earnings (8 days!)

- February 20, 2026: Monthly OPEX

- H2 2026: MI450 production ramp and OpenAI 1GW deployment begins

- Q3 2026: Oracle 50,000 GPU supercluster launch

- January 2027: This $8M put trade expires

Final verdict: AMD's long-term story remains compelling - the OpenAI partnership, government contracts, and aggressive product roadmap create a legitimate path to challenging Nvidia's dominance. But at current valuation after 89% YTD gains with earnings imminent, the risk/reward favors patience. The $8M institutional put buy signals smart money agrees: stay long the thesis, but protect against near-term volatility.

Be patient. Let earnings clear. If you're already long, consider some protection. If you're not, wait for a better entry at $240-250 with margin of safety.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-score of 28.02 reflects this trade's unusual size relative to recent AMD options history - it does not imply the trade will be profitable. Always do your own research and consider consulting a licensed financial advisor before trading.

About Advanced Micro Devices: AMD designs digital semiconductors for PCs, gaming consoles, data centers, AI applications, industrial, and automotive markets. With a market cap of $422.8 billion, AMD has emerged as a prominent player in AI GPUs and related hardware, competing directly with Nvidia for the $400B+ AI accelerator market.