🐋 AMD $11M LEAP Call Bet - Institutional Money Goes All-In on AI Chip Growth!

📅 February 25, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just loaded up on $11 MILLION in AMD November $260 calls - buying 4,000 LEAP contracts 9 months out that need AMD to rally +23% from here to break even. This is a major institutional conviction bet that AMD's two transformative hyperscaler deals (OpenAI + Meta, combined ~$120B potential) and the MI450 launch in H2 2026 will push the stock well above $260 by November. With Vol/OI at 2.35x, this is a brand new position opening - not rolling or hedging.

📊 Company Overview

Advanced Micro Devices (AMD) is the semiconductor giant going toe-to-toe with Nvidia in the AI accelerator race:

- 💻 What they do: Designs digital semiconductors for PCs, gaming consoles, data centers (including AI), industrial, and automotive applications

- 💰 Market Cap: $348.6B

- 🏢 Sector: Semiconductors & Related Devices

- 📈 Exchange: NASDAQ

- 📊 Current Price: ~$211.58

- 🤖 Key Story: Just secured two landmark 6-gigawatt GPU deals with OpenAI and Meta worth up to ~$120B combined over five years

💰 The Option Flow Breakdown

📊 The Tape

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:11:22 | AMD | MID | BUY | CALL $260 | 2026-11-20 | $11M | $260 | 4,000 | 1,700 | 4,000 | $211.58 | $27.14 | AMD20261120C260 |

🤓 What This Actually Means

Let me break this down in plain English:

- 💸 $11 million spent: 4,000 contracts at $27.14 each ($27.14 x 100 shares x 4,000 = ~$10.9M)

- 📈 Strike $260 is 23% above current price - this is a significantly out-of-the-money bet requiring a big move

- ⏰ 9 months to expiration (November 20, 2026) - this is a LEAP, giving plenty of time for catalysts to play out

- 📊 Volume/OI ratio = 2.35x - volume is over double the existing open interest of 1,700, confirming this is a Buy-to-Open (new position, not closing or rolling)

- 🤝 MID fill - executed at the midpoint of the bid-ask spread, a hallmark of institutional negotiation (not retail market-ordering)

- 🎯 Breakeven at expiration: $287.14 ($260 strike + $27.14 premium paid) = needs a +35.7% rally from current levels

What's the thesis here?

This trader is betting that AMD's AI revenue ramp - fueled by MI450 GPU shipments to OpenAI and Meta starting H2 2026 - will drive the stock well above $260 before the November OPEX. At $27.14 per share, they're paying roughly 12.8% of the stock price for 9 months of upside exposure. That's not cheap, but it's a leveraged bet with defined risk: the absolute worst case is losing the $11M premium if AMD stays below $260.

Why $260? The strike aligns with the $250 gamma resistance area and sits right in the middle of the analyst price target range ($220-$328). The consensus average target is ~$260. This trader is essentially betting AMD hits the Street's target - and likely overshoots it.

📈 Technical Setup / Chart Check-Up

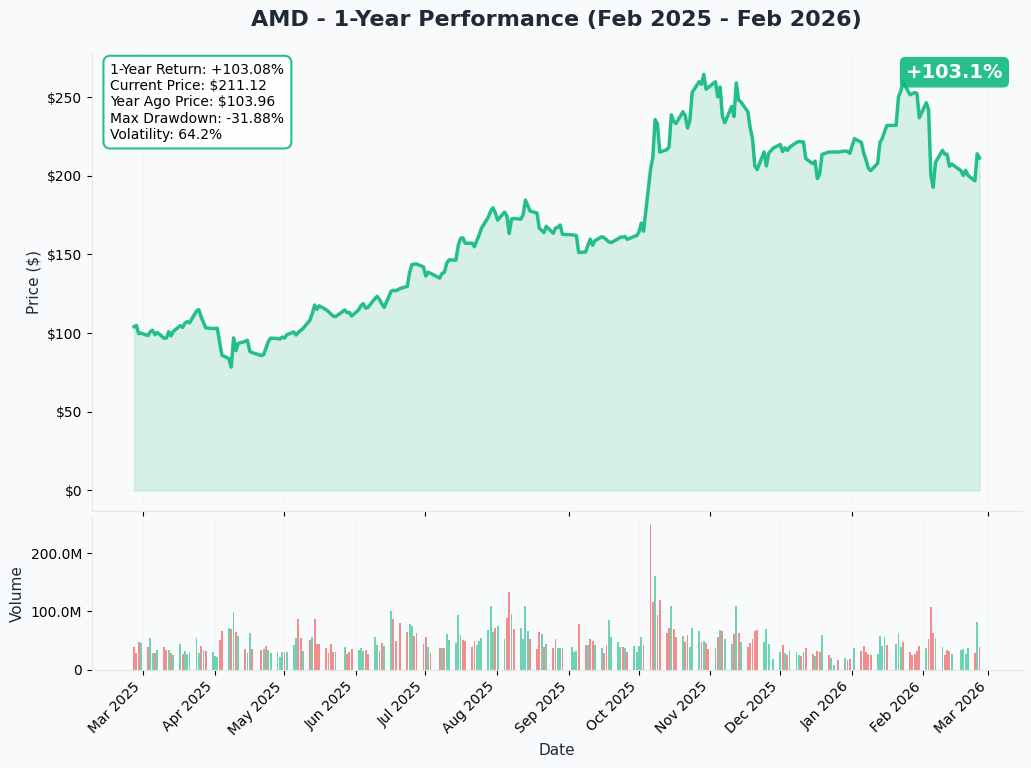

YTD Performance

AMD is up +75.4% YTD with the current price at ~$211.63 (started 2025 at $120.63). The chart tells a dramatic AI growth story with sharp swings:

- 🚀 Massive rally: From $120 to the $267 peak in late October 2025 on the OpenAI deal euphoria

- 📉 Sharp correction: Pulled back -23% from $267 to the $197 area after soft Q1 2026 guidance in early February

- 📈 Bounce back: Meta deal on February 24 sparked a +8.8% single-day rally back above $211

- 🎢 High volatility: 62.1% annualized vol - this stock swings hard in both directions

- 📊 Max drawdown: -39.6% - a reminder that AMD can drop fast when sentiment turns

- 💪 Volume spike: Massive buying volume on the Meta deal day shows institutional conviction

Key takeaway: AMD is in recovery mode after the Q4 earnings selloff. The Meta deal provided a catalyst floor, and the stock is trading mid-range between its $187 low and $267 high. Plenty of room to run if MI450 execution delivers.

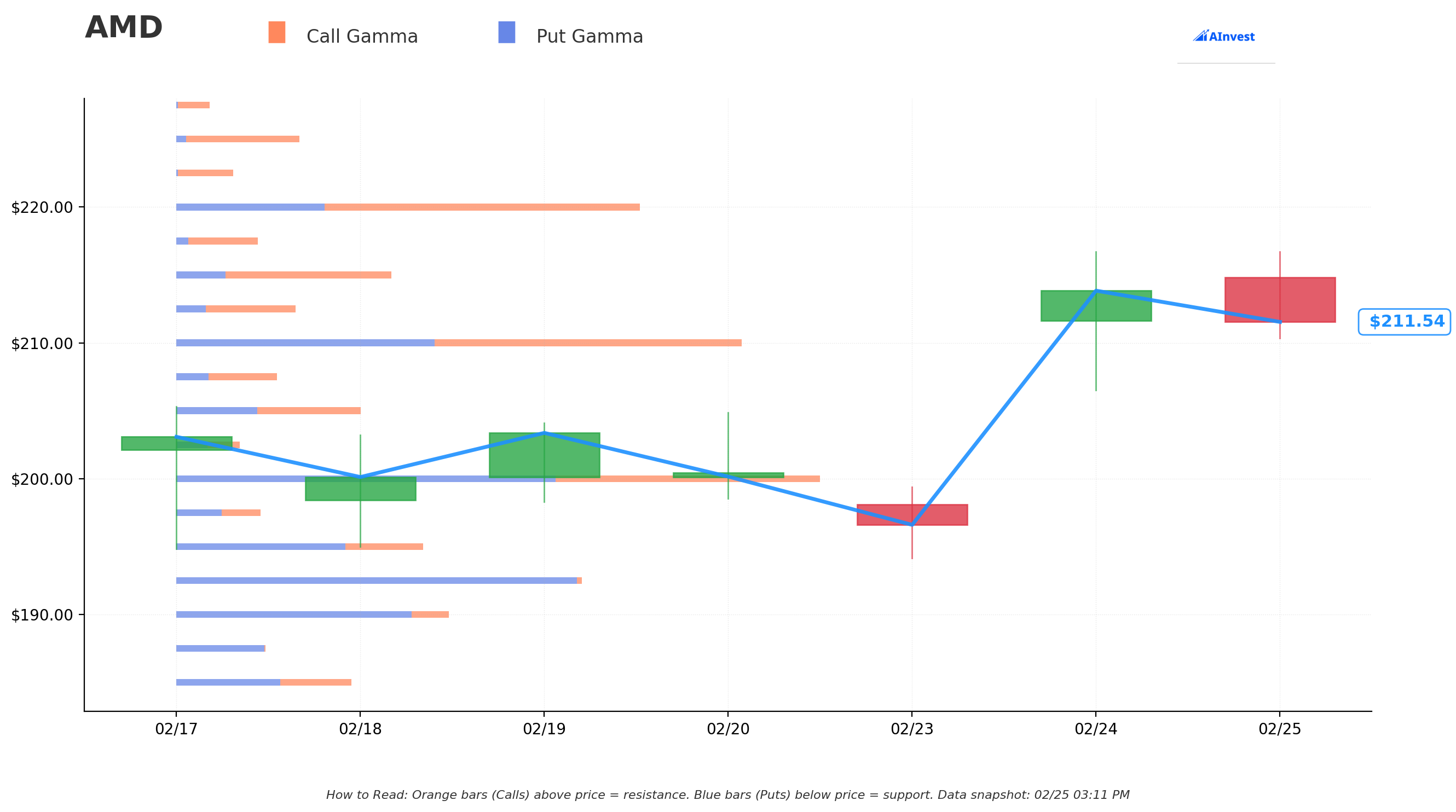

Gamma-Based Support & Resistance Analysis

Current Price: $211.72

The gamma exposure map reveals where options market makers have concentrated positions, creating natural price magnets and barriers:

🔵 Support Levels (Put Gamma Below Price):

- $210 - Strongest immediate support with 25.8B total gamma exposure (less than 1% below current price - tight floor!)

- $200 - Major structural support with 29.4B total gamma (5.5% below - this is the LINE IN THE SAND)

- $195 - Secondary support at 11.2B gamma

- $192.50 - Deep support with 18.2B gamma (strong put concentration)

- $190 - Extended floor at 12.4B gamma (10% below current)

- $180 - Disaster scenario support at 9.9B gamma

🟠 Resistance Levels (Call Gamma Above Price):

- $215 - First resistance at 9.9B gamma (just 1.5% overhead - easily reachable)

- $220 - Significant resistance at 21.3B gamma (3.9% above - key near-term hurdle)

- $230 - Strong resistance at 17.4B gamma (8.6% above)

- $250 - Extended resistance at 11.5B gamma (18% above - gateway to the $260 call strike!)

What this means for traders: AMD has tight support at $210 just below and first resistance at $215 just above. The near-term battlefield is the $210-$220 range. A break above $220 opens the door to $230, and clearing $230 opens the path toward $250. The $260 strike on this call trade sits above all current gamma resistance levels, reinforcing that this is a longer-term conviction play, not a short-term trade.

Net GEX Bias: Bullish (158.5B total call gamma vs 151.0B total put gamma) - overall dealer positioning leans slightly bullish, supporting the thesis that the floor is close at $210.

Implied Move Analysis

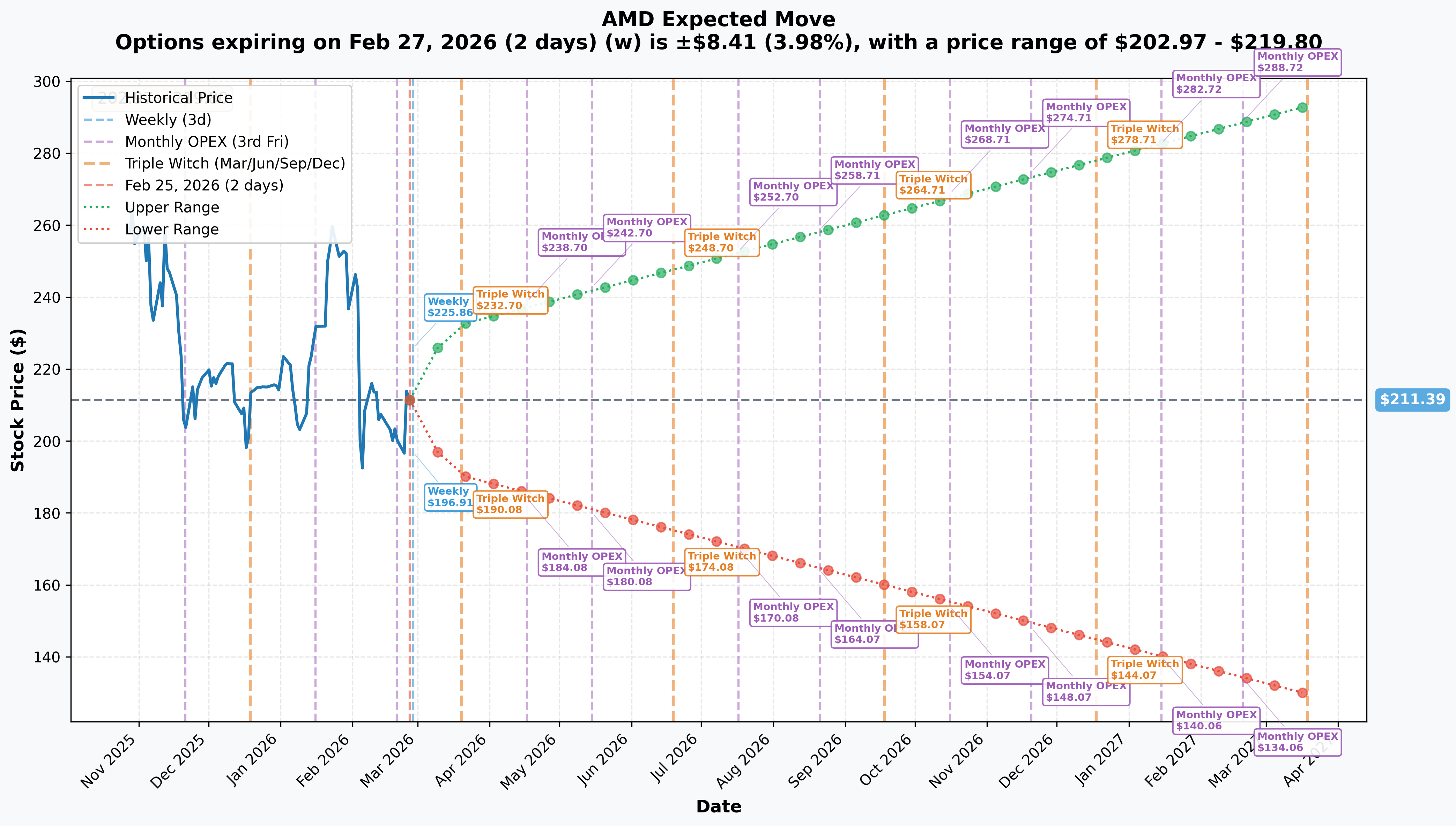

Options market pricing for upcoming expirations:

- 📅 Weekly (Feb 27 - 2 days): ±$8.41 (±4.0%) --> Range: $203 - $220

- 📅 Monthly OPEX / Triple Witch (Mar 20 - 23 days): ±$21.14 (±10.0%) --> Range: $190 - $233

- 📅 November 20 OPEX (THIS TRADE!): Upper range $274.71, Lower range $148.07

- 📅 Yearly LEAPs (Mar 2027): ±$81.83 (±38.7%) --> Range: $130 - $293

Translation: The options market expects AMD could move anywhere from $148 to $275 by the November 20 expiration. That's a massive range reflecting both the enormous upside potential from AI deal execution and the downside risk from dilution/competition. The $260 strike on this call sits within the implied upper range of $275 - meaning the market views $260 as achievable, though far from guaranteed.

Key insight: The weekly 4% implied move is elevated (Meta deal follow-through + Nvidia earnings this week). The November OPEX range stretching to $275 validates this trader's thesis that $260 is reachable within the expected distribution.

🎪 Catalysts

🔥 Upcoming Catalysts

Q1 2026 Earnings - Expected May 5, 2026 📊

This is the next major checkpoint. AMD guided Q1 2026 revenue to ~$9.8B (+32% YoY but -5% sequentially). Key things to watch:

- 📊 Data Center segment trajectory (following $5.4B record in Q4)

- 🤖 MI350 ramp progress and MI450 production readiness commentary

- 🇨🇳 Impact of China export controls on Instinct GPU sales

- 📈 Any updates on Meta/OpenAI deal milestones

- 💻 Client segment resilience with AI PC refresh cycle

MI450 "Helios" Rack-Scale Launch - H2 2026 🚀

This is THE catalyst that makes or breaks this $11M call trade. AMD confirmed Helios racks and MI450 GPUs on track for H2 2026 production:

- 🏭 Custom MI450 for Meta: First gigawatt deployment shipments begin H2 2026

- 🤖 Custom MI450 for OpenAI: Parallel 1GW deployment also H2 2026

- 💪 Architecture: CDNA 5 with 432GB HBM4 memory at 19.6 TB/s bandwidth

- 📈 Expected to double AI compute performance over MI350 series

If AMD nails this launch on schedule, it directly validates the two biggest deals in company history. The November expiration gives just enough time to capture initial deployment announcements and early revenue recognition.

Q2 2026 Earnings - Expected Late July / Early August 2026 📊

- First quarter to potentially reflect pre-shipment Meta/OpenAI partnership activity

- MI450 production readiness for H2 ramp will be THE key data point

Computex / Industry Events - June 2026 🎤

- Likely venue for MI450 deep-dive benchmarks and competitive positioning

- AMD historically uses Computex for major product showcases

Potential Additional Hyperscaler Deals 🤝

- With OpenAI and Meta locked in, Microsoft Azure and Google Cloud are potential next targets

- Each incremental deal could be worth tens of billions and would supercharge the stock

✅ Recent Catalysts (Already Happened)

Meta 6GW GPU Deal - February 24, 2026 (YESTERDAY!) 🤝

The single most significant recent catalyst. Meta signed a multi-year partnership to deploy up to 6 gigawatts of AMD Instinct GPUs:

- 💰 Estimated value: up to $60-100B over five years

- 📈 AMD surged +8.77% on the news (from $196.60 to $213.84)

- ⚠️ AMD issued Meta a warrant for up to 160 million shares (~10% dilution) at $0.01 exercise price, vesting tied to milestones

Q4 2025 Earnings - February 3, 2026 📊

Record results but soft guidance: Revenue $10.3B (+34% YoY), Non-GAAP EPS $1.53 (beat by $0.21), Data Center segment $5.4B record. But Q1 guidance disappointed at $9.8B (-5% QoQ), triggering a selloff from the $230s to sub-$200.

OpenAI 6GW GPU Deal - October 6, 2025 🤖

Nearly identical structure to Meta: 6GW of AMD Instinct GPUs, warrant for 160M shares, first 1GW deployment of MI450 beginning H2 2026. This was the deal that launched AMD from $155 to $267.

AMD-Cisco-HUMAIN Joint Venture - November 2025 🌍

Joint venture with Cisco and Saudi Arabia's HUMAIN to deploy 1GW of AI infrastructure over 5 years, part of a broader $10B commitment.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, analyst targets, and the catalyst calendar, here are the scenarios through the November 20, 2026 expiration:

📈 Bull Case (30% probability)

Target: $275-$330

How we get there:

- 🚀 MI450 launches on schedule in H2 2026 with strong performance benchmarks

- 💪 Q1 and Q2 earnings beat expectations, Data Center revenue inflects higher

- 🤝 Third hyperscaler deal announced (Microsoft or Google)

- 📊 Analyst upgrades push consensus target above $300 (Evercore already at $328)

- 🤖 ROCm software gains traction, narrowing CUDA gap

- 📈 Stock breaks through $220, $230, $250 gamma resistance levels in sequence

Call trade P&L at $300: Calls worth $40/share, profit = $12.86/share x 4,000 contracts = $5.1M gain (47% ROI) Call trade P&L at $330: Calls worth $70/share, profit = $42.86/share x 4,000 contracts = $17.1M gain (157% ROI)

This is the scenario where AMD delivers on the AI promise and the market re-rates the stock toward the high end of analyst targets. The implied move upper range of $275 for the November OPEX supports this as within the expected distribution.

🎯 Base Case (45% probability)

Target: $220-$260 range

Most likely scenario:

- ✅ MI450 on track but revenue recognition mostly pushed to Q4 2026 / Q1 2027

- 📊 Earnings meet expectations but don't blow away estimates

- ⚖️ Market gradually prices in the Meta/OpenAI deal value minus dilution concerns

- 🔄 Stock grinds higher through gamma resistance at $215, $220, $230 over months

- 📈 Analyst consensus (~$260 average target) acts as natural magnet

Call trade P&L at $260: At-the-money at expiration, calls worth ~$0 (time value gone), loss = -$10.9M (-100%) Call trade P&L at $245: OTM, calls expire worthless, loss = -$10.9M (-100%)

In this scenario, the call trade most likely loses money unless the stock pushes solidly above $260 before expiration. However, the trader could sell the calls before expiration if the stock rallies to $240-250, recovering a meaningful portion of premium via remaining time value.

📉 Bear Case (25% probability)

Target: $170-$200

What could go wrong:

- 😰 MI450 launch delayed or performance disappoints vs Nvidia's Vera Rubin

- 🚨 China export controls tighten further - removing revenue

- 💸 20% warrant dilution overhang weighs on shares as vesting milestones approach

- 📉 Broader tech selloff drags semiconductors lower

- ⚖️ Meta and/or OpenAI scale back deployment timelines

- 🏭 TSMC supply chain disruptions or 25% tariff impact on margins

- 📊 Break below $200 gamma support triggers cascade toward $190-$180

Call trade P&L: Calls expire worthless, loss = -$10.9M (-100%)

The $200 level with 29.4B total gamma is the critical support. A break below opens the path to $190 and even $180. The trader loses the entire $11M premium but the loss is capped at that amount - no additional downside.

💡 Trading Ideas

🛡️ Conservative: "Piggyback the Whale" - Debit Call Spread

Play: Buy the AMD March 2027 $220 calls, sell the March 2027 $260 calls

Structure: $220/$260 bull call spread, 12+ months to expiration

Why this works:

- 📊 Captures the same directional thesis as the $11M trade but with MUCH lower cost

- 🛡️ Defined risk: you can only lose the net debit paid (roughly $18-22 per spread)

- 💰 Max profit: $40 per spread minus debit paid (~$18-22 gain) if AMD above $260 at expiry

- ⏰ Extra time (March 2027 vs November 2026) gives more room for MI450 ramp

- 📈 The $220 strike is only 4% away - easier to get in-the-money quickly

- ⚖️ Analyst consensus at $260 aligns perfectly with the short strike

Position sizing: Risk no more than 3-5% of portfolio. 10 spreads at ~$20 each = ~$20,000 risk for ~$20,000 max profit.

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

⚖️ Balanced: "Ride the AI Wave" - Nov 2026 Call Butterfly

Play: Buy 1x $240 call, sell 2x $260 calls, buy 1x $280 call (all November 20, 2026 expiration)

Why this works:

- 🎯 Targets the $240-$280 zone where this institutional trade is concentrated

- 💸 Much cheaper than outright calls - butterfly costs roughly $4-6 per spread

- 📊 Max profit zone right around $260 (the whale's strike!) = ~$14-16 per spread

- ⏰ Same November 20 expiration mirrors the institutional positioning

- 📈 Risk/reward roughly 3:1 if AMD settles near $260

- 🤖 Profits from both the rally AND from time decay on the short legs

Position sizing: 20-50 spreads at ~$5 each = $10,000-$25,000 risk for $30,000-$80,000 max profit.

Risk level: Moderate (defined risk, needs precision) | Skill level: Intermediate-Advanced

🚀 Aggressive: "Full Send" - Nov 2026 $250 Calls

Play: Buy AMD November 20, 2026 $250 calls outright

Why this works (and why it's risky):

- 💥 Lower strike ($250 vs $260) means higher delta - more responsive to price moves

- 📊 $250 aligns with gamma resistance level and analyst consensus zone

- ⏰ Same 9-month timeframe captures all major catalysts (earnings, MI450, Computex)

- 🚀 If AMD hits $300, these calls would be worth ~$50, roughly tripling a ~$35 entry

- 📈 Follows the institutional thesis at a slightly more favorable strike

Why it could blow up:

- 💸 Still paying ~$35 per contract ($3,500 per contract) - expensive

- ⏰ 9 months of time decay eating at your premium every single day

- 📉 If AMD stays below $250, you lose everything

- 🎢 Needs +18% move just to reach the strike, +35% to breakeven at expiration

Position sizing: Risk ONLY what you can afford to lose completely. 5 contracts = ~$17,500 at risk.

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

📉 Strike is 23% OTM: The $260 strike requires a massive rally from $211.58. While 9 months is a generous timeframe, AMD needs to break through four gamma resistance levels ($215, $220, $230, $250) before reaching $260. That's a LOT of overhead supply to absorb.

-

💸 20% potential warrant dilution: The combined OpenAI + Meta warrants could dilute existing shareholders by up to 320 million shares at $0.01 exercise price. Even partial vesting creates meaningful EPS dilution. Market has partially priced this in but may re-evaluate as milestones approach.

-

🏭 MI450 execution risk is REAL: H2 2026 launch is AMD's most critical product cycle ever. Must deliver custom GPUs at hyperscaler scale for OpenAI and Meta simultaneously. Any delay or performance shortfall could crater the stock AND these calls.

-

⚔️ Nvidia's Vera Rubin arrives 2026: Nvidia's next-gen architecture offers 5x Blackwell performance. If Vera Rubin significantly outperforms MI450, hyperscaler enthusiasm for AMD could cool. Nvidia still commands ~80-86% AI accelerator market share with deep CUDA ecosystem lock-in.

-

🇨🇳 China export controls wildcard: AMD already took an $800M charge on halted MI308 shipments and estimates $1.5-1.8B in lost 2025 revenue. Further restrictions could hit new products without warning.

-

📊 Valuation stretched at ~80x trailing P/E: While forward P/E compresses to ~31-35x for CY2026, Morningstar's DCF fair value sits at just $145. AMD is priced for near-perfect execution - one stumble and the stock could revisit $180-190.

-

🌍 TSMC supply chain concentration: All AMD AI chips are manufactured through TSMC in Taiwan. The 25% tariff on Taiwan-manufactured chips hits margins, and geopolitical risk remains an existential tail risk.

-

⏰ Time decay on a 9-month $27 premium: At $27.14 per contract, the trader is paying roughly $3/month in time decay. If AMD doesn't make meaningful progress toward $260 by mid-summer, the calls could lose 50%+ of value even if the stock is flat.

🎯 The Bottom Line

Here's the deal: Someone with deep pockets just put $11 million on the table betting AMD breaks $260 by November 2026. This is not a hedge - it's a pure directional conviction play. They're betting that the Meta and OpenAI 6-gigawatt deals, the MI450 launch, and the continued AI spending boom will push AMD well above current levels.

What this trade tells us:

- 🎯 Institutional money sees AMD reaching the $260 analyst consensus target - and likely above it - within 9 months

- 💰 They're willing to risk $11M on this thesis, suggesting they've done serious due diligence on MI450 readiness and deal milestones

- ⏰ The November expiration is strategic: it captures Q1 earnings (May), Q2 earnings (July/Aug), MI450 launch (H2), and Computex - all the major catalysts in one trade

- 📊 The 2.35x Vol/OI confirms this is fresh capital entering, not repositioning

This IS a bullish signal, but with important context: The $260 strike is still 23% away. This trader has time on their side, but they also need multiple things to go right: MI450 on schedule, no major macro shocks, continued AI spending, and no competitive surprises from Nvidia. The PEG ratio of 0.66 suggests AMD is undervalued relative to growth - but that growth needs to materialize.

If you're bullish on AMD:

- ✅ Consider defined-risk strategies (call spreads, butterflies) rather than naked calls to limit downside

- 📊 The $210 gamma support is your near-term floor - set alerts if the stock breaks below

- ⏰ Mark May 5 (Q1 earnings) as your first major checkpoint for thesis validation

- 💡 Watch for MI450 production updates at Computex in June - that's the make-or-break moment

If you're watching from the sidelines:

- 🎯 A pullback to the $200-$205 area (strong gamma support) would offer a better risk/reward entry point

- 📊 Wait for Q1 earnings confirmation before committing capital

- 📈 The analyst consensus average target of $260 with a high of $328 from Evercore ISI shows the Street sees meaningful upside

- ⏰ H2 2026 MI450 production milestones will be the stock's biggest single catalyst this year

If you're cautious:

- ⚠️ The 20% dilution overhang from OpenAI + Meta warrants is real and could cap upside

- 📉 A break below $200 gamma support would change the technical picture significantly

- 🛡️ Consider collar strategies (long stock + put protection + covered call) to play the range while staying protected

Key dates to mark:

- 📅 May 5, 2026 (estimated) - Q1 2026 earnings (first post-Meta-deal report)

- 📅 June 2026 - Computex (likely MI450 showcase and benchmarks)

- 📅 July/August 2026 - Q2 2026 earnings (MI450 ramp guidance)

- 📅 H2 2026 - MI450/Helios production begins - first shipments to OpenAI and Meta

- 📅 November 20, 2026 - THIS TRADE EXPIRES - moment of truth for the $11M bet

Final verdict: AMD's AI story is as compelling as it gets in semiconductors right now - two confirmed $60B+ hyperscaler deals, record revenue, and a credible path to multi-year earnings growth. The $11M LEAP call buy reflects genuine institutional conviction. But at $211 with a $260 target, you're paying for a lot of perfect execution. The smarter retail play is to use defined-risk strategies that participate in the upside while capping your downside. Let the institutions take the big swings - you ride along at a fraction of the risk.

Be patient. Let the MI450 story unfold. And remember: $27 per share in premium means this trader needs AMD above $287 to make money at expiration. That's a high bar - even for the #2 AI chip company in the world. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. LEAP calls are high-risk instruments that can lose 100% of premium if the stock doesn't reach the strike by expiration. Always do your own research and consider consulting a licensed financial advisor before trading.

About Advanced Micro Devices: Advanced Micro Devices designs a variety of digital semiconductors for markets such as PCs, gaming consoles, data centers (including artificial intelligence), industrial, and automotive applications, with a market cap of $348.6B in the Semiconductors & Related Devices industry.