🚀 APLD HISTORIC $119M Call LEAP - Someone Betting BIG on AI Data Center Revolution! 🏭

📅 December 18, 2025 | 🔥 UNPRECEDENTED UNUSUAL ACTIVITY DETECTED

🎯 The Quick Take

Holy smokes! Someone just placed the LARGEST SINGLE OPTIONS TRADE OF THE YEAR on Applied Digital - a staggering $119 MILLION BUY of January 2028 $8 strike calls! This monster LEAP bought 65,000 contracts representing 6.5 million shares (2.3% of the entire company) with over 3 YEARS until expiration. With APLD at $23.89 and the stock already up from sub-$10 levels this year, this trader is making a massive long-term bet that Applied Digital's AI data center empire will be worth 3-5x current levels by 2028. Translation: Institutional whale believes the $16B in contracted revenue from CoreWeave and hyperscalers will transform APLD into a data center powerhouse!

📊 Company Overview

Applied Digital Corporation (APLD) has transformed from a Bitcoin mining host to a major AI/HPC infrastructure provider:

- Market Cap: $6.14 Billion (huge growth from <$1B in 2023)

- Industry: Computer Processing & Data Preparation Services (AI/HPC Data Centers)

- Current Price: $23.89 (52-week range: $3.31 - $40.20)

- Primary Business: Next-generation digital infrastructure and cloud services for high-performance computing (AI/HPC)

- Headquarters: Dallas, Texas

- Key Assets: Two massive North Dakota data center campuses (Polaris Forge 1 & 2) with ~600MW leased capacity

Applied Digital operates purpose-built data centers designed specifically for AI and high-performance computing workloads, with approximately $16 billion in contracted revenue through long-term leases with investment-grade hyperscalers including CoreWeave.

💰 The Option Flow Breakdown

The Tape (December 18, 2025 @ 09:33:04):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:33:04 | APLD | ASK | BUY | CALL $8 | 2028-01-21 | $119M | $8 | 65K | 100 | 65,309 | $23.89 | $18.20 |

🤓 What This Actually Means

This is an EPIC LONG-TERM BULL BET on Applied Digital's AI data center transformation! Here's the breakdown:

- 💸 Massive premium: $119M ($18.20 per contract × 65,000 contracts) - this is INSTITUTIONAL SIZE

- 🎯 Ultra-deep in-the-money: $8 strike vs $23.89 current price = $15.89 intrinsic value (87% of option price is already "in the money")

- ⏰ SUPER LONG duration: 1,129 days (3.1 YEARS) to expiration - this is NOT a short-term trade

- 📊 Gigantic position: 65,000 contracts = 6.5 million shares worth $155M at current price (2.3% of entire company!)

- 🏦 High confidence signal: Deep ITM LEAPs with 87% intrinsic value = "I want stock-like exposure with leverage but I'm NOT gambling on crazy price moves"

What's really happening here:

This trader is essentially buying 6.5 million shares of APLD with 5.5x leverage through 2028. Here's the beautiful math:

- Stock currently at $23.89, they're paying $18.20 for $8 strike calls

- Only paying $2.31 in time premium ($18.20 - $15.89 intrinsic) over 3+ years = 0.6% per year

- If APLD stays flat at $23.89 until expiration, calls worth $15.89 = 87% return of premium

- Breakeven is just $26.20 (only 9.7% above current price over 3 years!)

- The upside is UNLIMITED - if APLD hits $50-60 by 2028 (which they're clearly betting on), these calls worth $42-52 = 2.3-2.9x return on $119M investment = $274-345M position!

Why deep ITM calls instead of stock?

- Capital efficiency: Control $155M worth of stock with only $119M (saves $36M cash)

- Leverage: Every $1 stock move = $1 option gain, but with only 77% of capital deployed

- Flexibility: Can roll, adjust, or take profits without complicated stock sales

- Institutional advantage: Likely using portfolio margin, making this MUCH more capital efficient than stock

Unusual Score: 🔥🔥🔥 OFF THE CHARTS (8,183x average size!) - This is a ONCE-A-YEAR trade for APLD. The Z-score of 8,183 means this is literally the largest APLD options trade by volume in months. Based on historical data, there have been ZERO similar trades in recent weeks.

Translation for regular folks: Some fund manager or billionaire just staked $119 MILLION on Applied Digital's AI infrastructure story playing out over the next 3 years. This isn't a gamble - this is a calculated, high-conviction bet that the $16B in contracted revenue from CoreWeave and hyperscalers will transform APLD from a $6B company to potentially $15-20B+ by 2028 as data centers come online and revenue ramps.

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

Current Price: $23.89

Applied Digital has been on an ABSOLUTE ROLLER COASTER this year! Starting at $7.36, the stock exploded to all-time highs of $40.20 in August (+446% from 52-week low of $3.31 in December 2023) before pulling back 40% to current levels.

Key observations from the chart:

- 🚀 Massive run-up: From $7 in January to $40 by August on CoreWeave partnership news and AI infrastructure hype

- 📉 Sharp correction: -40% pullback from $40 peak as market pulled back from AI infrastructure valuations in November-December

- 🎢 Extreme volatility: Stock trades with 7.10 beta - moves are WILD (not for the faint of heart!)

- 📊 Volume explosion: Recent weeks show massive institutional interest (26.64M average daily volume)

- ⚠️ High short interest: 28-31% of float is shorted (80.34M shares) - bears betting against the AI thesis

What the chart tells us: The stock has proven it CAN reach $40+ when AI infrastructure sentiment is strong. The recent pullback to $24 represents a 40% discount from peak, creating an attractive entry point for long-term bulls who believe in the revenue story. The January 2028 call buyer clearly sees this pullback as temporary - betting the stock revisits $40-50+ levels as data centers go live over next 2-3 years.

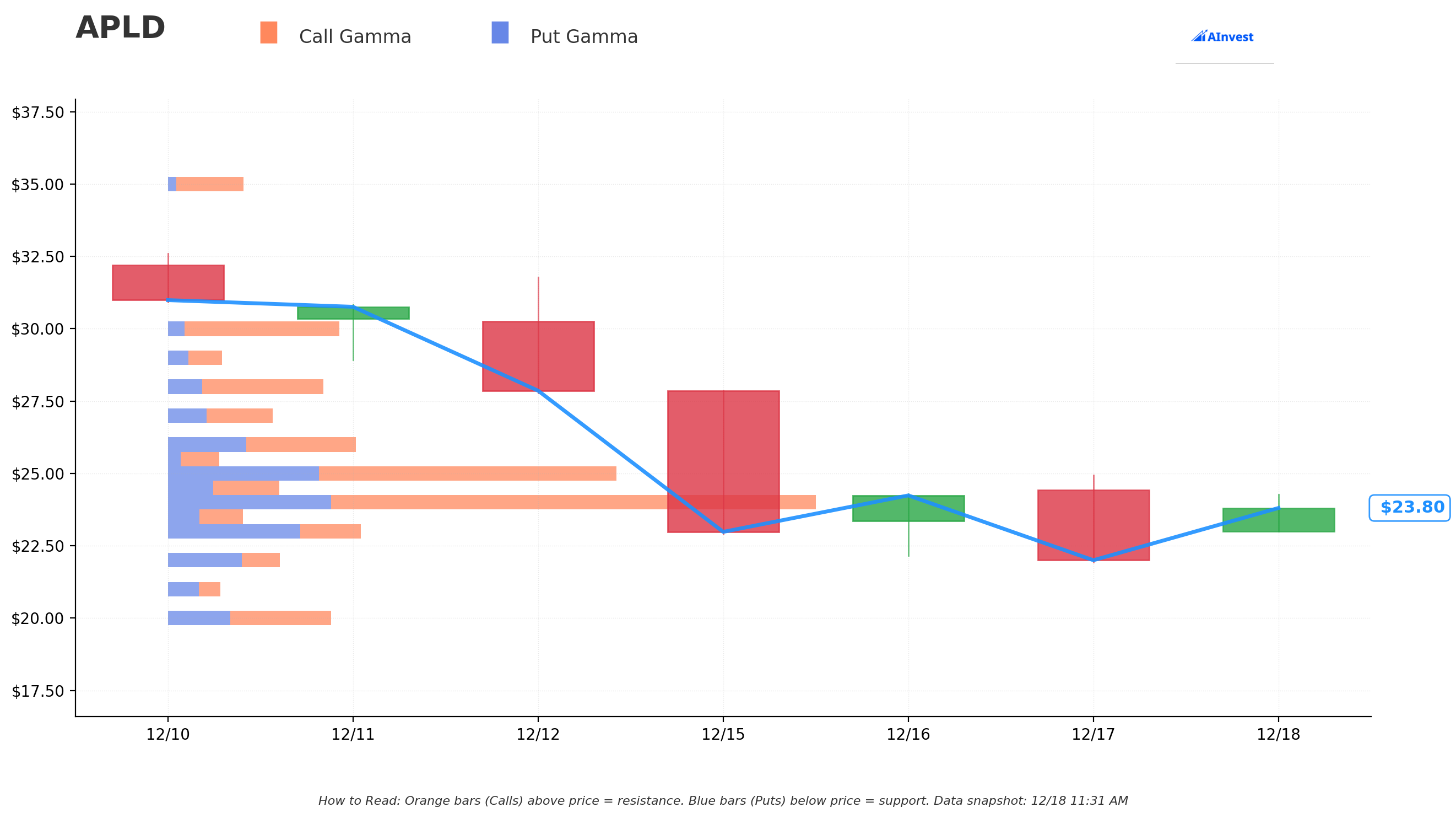

Gamma-Based Support & Resistance Analysis

Current Price: $23.80

The gamma exposure map reveals where market makers and option traders have placed their bets:

🔵 Support Levels (Put Gamma Below Price):

- $23.50 - Immediate support with 1.4B total gamma (nearest floor, only 1.3% below current)

- $23.00 - Secondary support at 3.6B gamma (strongest put gamma nearby! Dealers will defend this level)

- $22.00 - Major structural floor with 2.1B gamma

- $20.00 - Deep support at 3.1B gamma (psychological round number + gamma support)

🟠 Resistance Levels (Call Gamma Above Price):

- $24.00 - Immediate ceiling with 12.4B gamma (STRONGEST SINGLE LEVEL!) - this is THE wall to break

- $24.50 - Secondary resistance at 2.1B gamma (only 2.9% overhead)

- $25.00 - Major round number resistance with 8.4B gamma (next big hurdle)

- $26.00 - Extended resistance at 3.5B gamma

- $27.00 - Higher resistance zone with 1.9B gamma

- $28.00 - Distant target at 2.9B gamma (17.6% above current)

What this means for traders:

APLD is trading RIGHT AT a critical decision point. The massive $24 resistance (12.4B gamma - by far the largest level) is creating a ceiling that needs serious buying pressure to break through. Think of it like this: market makers are sitting on HUGE call positions at $24, so they need to sell stock/hedge as price approaches to stay neutral - creating natural resistance.

However, the $23 support (3.6B put gamma) is also significant. The stock is essentially in a $23-24 sandwich waiting for a catalyst to break out.

Net GEX Bias: BULLISH (43.2B call gamma vs 21.9B put gamma = 2:1 ratio) - Overall positioning heavily skewed bullish, which aligns perfectly with the massive $119M call LEAP. Options traders are betting on UPSIDE over time, not downside.

Notice the pattern? The call buyer struck at $8 - WAY below all these levels - because they want pure upside exposure with minimal time decay risk. They're not playing these near-term gamma games; they're playing the LONG GAME (revenue ramp through 2028).

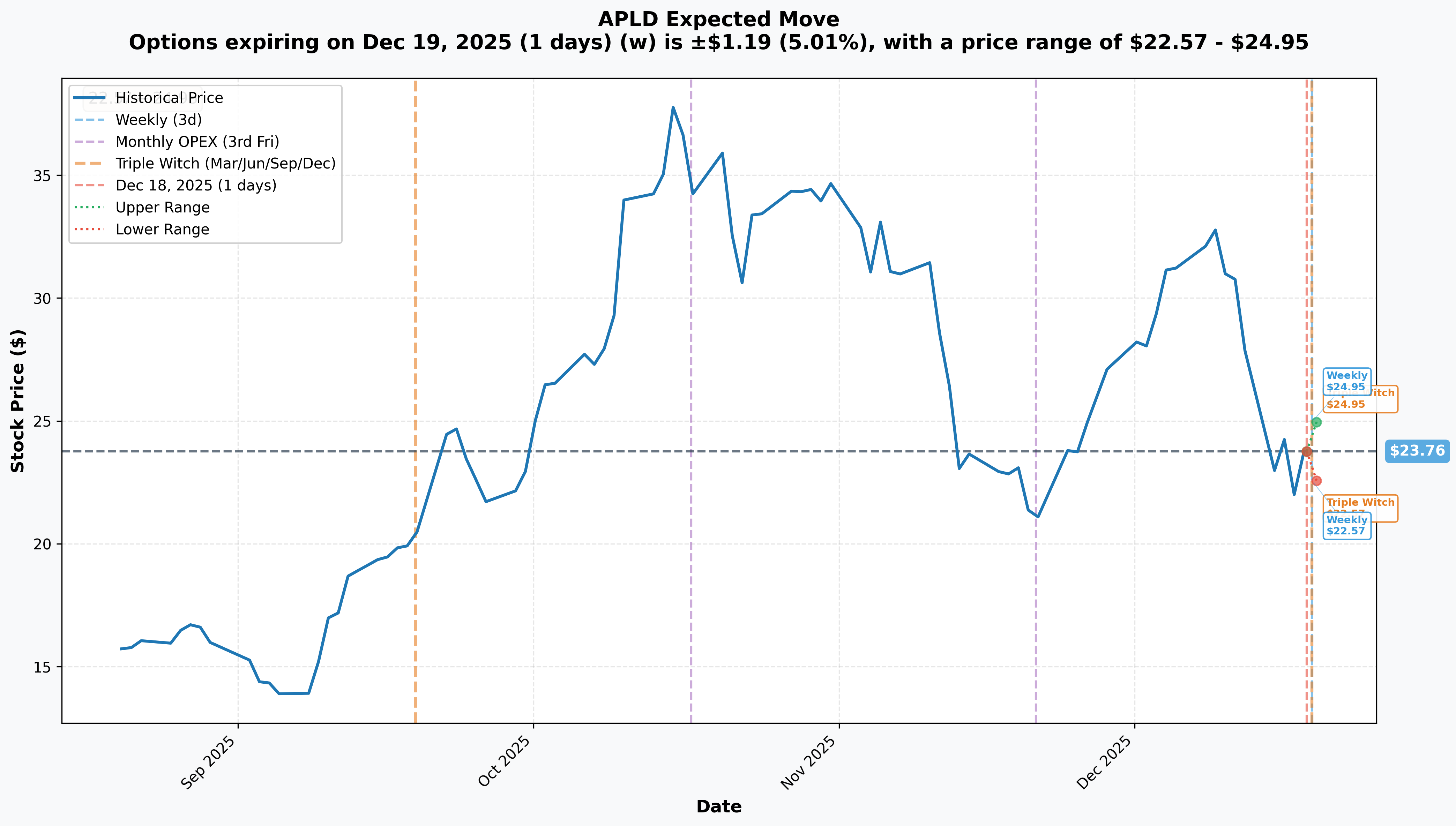

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 1 day - TOMORROW!): ±$1.19 (±5.01%) → Range: $22.57 - $24.95

- 📅 Monthly OPEX (Dec 19 - 1 day - SAME AS WEEKLY!): ±$1.19 (±5.01%) → Range: $22.57 - $24.95

- 📅 Quarterly Triple Witch (Dec 19 - 1 day!): ±$1.19 (±5.01%) → Range: $22.57 - $24.95

Key insight: ALL expirations converge on December 19th (TOMORROW!) which is a quarterly triple witch - a MASSIVE options expiration event. The market is pricing a 5% move by Friday close which translates to a $22.57-$24.95 range.

What this tells us:

- ⚡ High near-term volatility: 5% expected move in 1 day shows market expects NEWS or significant price action

- 📊 Quarterly OPEX significance: Triple witch creates mechanical pressures as dealers unwind hedges

- 🎯 Upper bound aligns with gamma resistance: $24.95 implied move top matches exactly with $25 gamma resistance

- 🛡️ Lower bound provides support: $22.57 suggested floor with $23 gamma support nearby

Why this matters for the LEAP trade: The call buyer completely IGNORES these near-term moves. They have 1,129 days until expiration. A 5% move tomorrow is NOISE. They're betting on 100-200% moves over the next 2-3 years as Polaris Forge 1 ($11B CoreWeave revenue) and Polaris Forge 2 ($5B hyperscaler revenue) come online and generate massive cash flow.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Q2 FY2026 Earnings - January 20, 2026 (33 DAYS AWAY!) 📊

Applied Digital reports fiscal Q2 2026 results on Monday, January 20, 2026 before market open. This is THE near-term catalyst that will show progress on data center revenue ramp:

- 📊 Revenue Forecast: $75-85M (company guidance) vs $64.2M in Q1 FY2026

- 💰 Consensus Revenue: $86.67M according to Nasdaq

- 📈 EPS Estimate: -$0.11 (range: -$0.28 to -$0.02)

- 🏭 Key metric: Cloud Services revenue growth (was up 523% YoY in Q2 FY2025!)

- 🎯 What to watch: Commentary on 100MW Polaris Forge 1 building ready-for-service timing (Q4 2025 target)

- 🤖 Critical update: Progress on CoreWeave lease implementation and customer pipeline

Why this matters: Q2 will show whether APLD is on track with the first 100MW building going live. Any positive surprises on revenue ramp or accelerated timeline could reignite the stock toward $30-35. Conversely, delays or weak guidance could pressure stock toward $20.

Polaris Forge 1 First Building Ready-for-Service (Q4 Calendar 2025 - NOW!) 🏭

The first 100MW building at Ellendale (Polaris Forge 1) for CoreWeave expected ready-for-service in Q4 2025 - meaning RIGHT NOW! This is a MASSIVE inflection point:

- 🎯 First major revenue-generating data center coming online

- 💰 Part of $11B total contracted revenue over ~15 years with CoreWeave

- 🚀 Once fully operational, Polaris Forge 1 could support ~$500M annual net operating income

- 📊 Building reached substantial completion in July 2025 - should be generating revenue NOW

Construction milestones achieved:

- ✅ December 2024: Successful energization of on-site main substation transformer

- ✅ January 2025: West chiller plant nearing completion, fiber and network rooms powered on

- ✅ July 2025: Building 1 (100MW) reached substantial completion

🚀 Near-Term Catalysts (Q1-Q2 2026)

Macquarie Asset Management Financing Milestone ($5B Facility) 💰

Applied Digital's $5B partnership with Macquarie has already achieved first funding:

- ✅ Initial $112.5M funded October 7, 2025

- 🎯 Structure: $2.25M per 1MW of capacity, up to $900M for full 400MW Ellendale build-out

- 💼 Macquarie receives perpetual preferred equity + 15% common equity; APLD retains 85% ownership

- 📈 12.75% annual dividend on preferred equity (paid in kind or cash)

- 🏦 Proceeds expected to complete 400MW Ellendale buildout, repay ~$180M bridge debt, recover >$300M equity

Why this matters: This financing REMOVES the #1 execution risk (capital constraints). APLD now has institutional backing to complete both campuses without diluting shareholders or taking on risky debt. Additional drawdowns coming as leases execute.

Polaris Forge 1 Second Building Completion (Mid-2026) 🏗️

150MW data center expected operational mid-2026:

- 🎯 Part of 400MW total CoreWeave lease generating $11B over ~15 years

- 📈 Proportional revenue contribution starting mid-2026

- 🚀 Demonstrates execution capability and de-risks remaining buildout

- 💰 With building 1 + building 2 operational (250MW total), annual revenue run-rate could hit $300-400M

Polaris Forge 2 Initial Operations (2026) 🏭

APLD's second campus near Harwood, North Dakota is ramping:

- 🎯 $3B total investment, 280MW AI Factory announced August 2025

- 🏗️ Groundbreaking September 2025

- 💰 200MW lease with U.S. investment-grade hyperscaler, $5B revenue over ~15 years announced October 2025

- 🚀 Initial operations beginning 2026

- 🎯 Hyperscaler holds first right of refusal for additional 800MW (total 1GW potential!)

The 1GW expansion option is MASSIVE: If hyperscaler exercises their 800MW expansion right, Polaris Forge 2 alone could generate $15-20B+ additional contracted revenue. This is the "call option" within the January 2028 call option trade.

🎯 Medium-Term Catalysts (2026-2027)

Polaris Forge 2 Full Capacity (Early 2027) 🏭

280MW campus reaches full capacity early 2027:

- 💰 $5B contracted revenue starts flowing at full capacity

- 🎯 Expected to employ >200 full-time staff

- 📊 With both campuses near full capacity (~600MW), APLD could be generating $700M-1B+ annual revenue

- 🚀 Profitability inflection point as revenue scales but costs stay relatively fixed

This is when the January 2028 calls start looking GENIUS: If APLD is generating $1B annual revenue with 40-50% EBITDA margins by 2027 (~$400-500M EBITDA), the company could be valued at 15-20x EBITDA = $6-10B market cap just from existing contracted business. Add in growth optionality (Polaris Forge expansion, new customers) and you're looking at $40-60/share stock price. The call buyer paid $18.20 for $8 strikes - if stock hits $50, these calls worth $42 = 2.3x return. If stock hits $60, calls worth $52 = 2.9x return. That's the bet.

Polaris Forge 1 Third Building (2027) 🏗️

150MW building currently in planning, CoreWeave holds option, anticipated 2027:

- 🎯 If exercised, completes full 400MW campus buildout

- 💰 Adds proportional revenue to $11B total CoreWeave contract

- 📈 Would bring Polaris Forge 1 to full capacity generating $500M+ annual NOI

Additional Customer Diversification 🌐

Currently one customer represents 62% of revenue (likely CoreWeave) - this is a KEY risk factor:

- 🎯 Management actively seeking additional hyperscaler leases to diversify

- 📊 Polaris Forge 2 hyperscaler represents FIRST major diversification win

- 🚀 Campus designed to scale to >1GW power capacity - room for multiple customers

- 💼 Working on 40+ sovereign AI projects worldwide - enterprise/government diversification underway

Nvidia Partnership Advantage 🤝

APLD's strategic advantage:

- 💰 $160M private placement with Nvidia and institutional investors (September 2024)

- 📊 Nvidia holds approximately 7.72M shares (~3% of outstanding stock)

- 🏗️ Nvidia engineers helped design Ellendale data center

- 🎯 Validates APLD's infrastructure as Nvidia-approved for highest-end AI workloads

⚠️ Risk Catalysts (What Could Go Wrong)

Execution Risks 🚧

Building AI/HPC data centers at this scale is HARD:

- ⏰ Construction delays: Q4 FY2025 gross margins fell to 13% vs projected 19% due to high fit-out costs - margins under pressure

- 🏭 Supply chain risks: Macroeconomic headwinds and supply chain complexities could delay critical components

- 💰 Cost overruns: First major deployment at this scale - unproven execution track record

- 📉 Profitability timeline: Overall profitability not expected until fiscal year 2028 - burning cash until then

Financial Risks 💸

- 🏦 High debt load: $700.21M total debt

- 📊 Convertible notes: $450M convertible notes due 2030 with $9.75 conversion price - dilution risk if stock performs well

- 💰 Macquarie preferred dividend: 12.75% annual dividend on preferred equity, increasing 87.5bps on 5th and 6th anniversaries

- 📉 Negative cash flow: Continued losses through FY2028 require additional capital

Market & Competition Risks 🤺

- 🏢 Competing against giants: Equinix (EQIX) and Digital Realty Trust (DLR) have massive scale and capital advantages

- 🎯 Customer concentration: 62% revenue from one customer - if CoreWeave relationship deteriorates, it's catastrophic

- 📉 Recent stock decline: Stock crashed 16-17% recently on AI infrastructure valuation pullback

- 🐻 High short interest: 28-31% of float shorted (80.34M shares) - bears betting against execution

- 😰 Insider selling: Persistent insider selling near highs has concerned investors

Valuation & Sentiment Risks 📊

- 📈 Already up big: Stock up from $3.31 low to current $23.89 = 6.2x move in past year

- 💰 -1.41% net margin vs profitable competitors like GoDaddy (17.01%), Okta (6.08%)

- 🎢 Beta of 7.10 = EXTREME volatility (stock can move 20-30% on no news)

- ⚠️ Market sentiment shift: AI infrastructure names seeing valuation compression as reality sets in

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, catalyst timeline, and the call buyer's thesis, here are scenarios through January 2028:

📈 Bull Case (40% probability)

Target: $50-70 by January 2028

How we get there:

- 🏗️ Flawless execution: Both Polaris Forge campuses come online on schedule without major cost overruns

- 💰 Revenue ramp exceeds: By 2027, APLD generating $800M-1B+ annual revenue from $16B contracted base

- 📈 EBITDA inflection: Achieve 45-50% EBITDA margins as revenue scales (typical for data center hosting)

- 🎯 Customer diversification: Win 2-3 additional hyperscaler leases, reducing CoreWeave concentration to <40%

- 🚀 Polaris Forge 2 expansion: Hyperscaler exercises 800MW expansion option, adding $15B+ contracted revenue

- 🤝 Nvidia partnership deepens: Additional design wins, potential strategic investment increase

- 💼 Government/enterprise wins: 40+ sovereign AI projects materialize into $2-3B additional contracted revenue

- 📊 Profitability in sight: Path to FY2028 profitability becomes clear with $400-500M EBITDA

- 🏦 Institutional validation: Major funds initiate/increase positions as de-risking occurs

Key metrics needed:

- Q2 FY2026 revenue $80M+ (showing strong ramp)

- Polaris Forge 1 first building generating revenue by February 2026

- Gross margins improving from 13% back toward 19%+ target

- Customer count increasing (not just CoreWeave)

- No major construction delays or cost overruns

Valuation math:

- By 2027: $1B revenue × 8-10x EV/Sales = $8-10B market cap

- OR: $500M EBITDA × 15-20x = $7.5-10B market cap

- Current market cap: $6.14B

- Implied stock price: $50-70/share (vs $23.89 current)

Call option P&L in Bull Case:

- Stock at $50: Calls worth $42.00, profit = $23.80/share × 65,000 = $154.7M gain (130% ROI on $119M!)

- Stock at $60: Calls worth $52.00, profit = $33.80/share × 65,000 = $219.7M gain (185% ROI!)

- Stock at $70: Calls worth $62.00, profit = $43.80/share × 65,000 = $284.7M gain (239% ROI!)

Probability assessment: 40% because it requires solid execution across multiple years but doesn't require perfection. The contracted revenue is REAL ($16B with investment-grade hyperscalers). APLD "just" needs to deliver on time and on budget. The Macquarie financing removes capital risk. Nvidia involvement validates technology. This is the BASE CASE the call buyer is betting on.

🎯 Base Case (35% probability)

Target: $30-45 by January 2028 (Solid but not spectacular)

Most likely scenario:

- ✅ Execution decent but not perfect: Some construction delays (2-3 months), minor cost overruns, but ultimately deliver

- 📊 Revenue ramps to $600-800M by 2027 (slower than bull case but still growing)

- 💰 Margins compressed: Achieve 35-40% EBITDA margins (lower than hoped due to cost pressures)

- ⚖️ Customer concentration persists: Win 1 additional customer but CoreWeave still 50%+ of revenue

- 📉 Polaris Forge 2 expansion delayed: Hyperscaler doesn't exercise 800MW option immediately (waits to see results)

- 🤔 Market remains skeptical: Stock gets RE-rated from deep discount to fair value but not premium

- ⏰ Profitability pushed out: FY2028 profitability target slides to FY2029

- 💤 Sentiment neutral: Neither hot growth story nor disaster - just steady infrastructure play

What this means:

- APLD becomes a $8-12B company (up from $6B current) but not the $15-20B+ bull case

- Stock trades at 10-15x EBITDA vs 20x in bull case

- Market applies "execution discount" due to stumbles along the way

Call option P&L in Base Case:

- Stock at $30: Calls worth $22.00, profit = $3.80/share × 65,000 = $24.7M gain (21% ROI - not terrible for 3 years!)

- Stock at $35: Calls worth $27.00, profit = $8.80/share × 65,000 = $57.2M gain (48% ROI)

- Stock at $40: Calls worth $32.00, profit = $13.80/share × 65,000 = $89.7M gain (75% ROI)

- Stock at $45: Calls worth $37.00, profit = $18.80/share × 65,000 = $122.2M gain (103% ROI)

Probability assessment: 35% because this represents "muddling through" - not great, not terrible. APLD has execution risk but also has locked-in revenue with blue-chip customers. Barring catastrophic failure, they'll likely deliver SOMETHING. This scenario still profitable for the call buyer but not the home run they're hoping for.

📉 Bear Case (25% probability)

Target: $10-20 by January 2028 (Thesis breaks)

What could go wrong:

- 😰 Major execution failure: Construction delays 6-12+ months, cost overruns 30-50%, quality issues require rework

- 💔 CoreWeave relationship deteriorates: Primary customer renegotiates terms, reduces capacity, or terminates (nightmare scenario)

- 🚨 Hyperscaler backs out: Polaris Forge 2 customer reduces commitment or exercises termination clauses

- 📉 Margin catastrophe: Gross margins stay at 10-15% instead of improving to 40-50% - business model doesn't work

- 💸 Capital crisis: Burn through Macquarie facility, can't raise additional capital, forced into dilutive financing

- 🏢 Competition crushes: Equinix/Digital Realty price APLD out or win the hyperscaler customers APLD needs

- 🌍 Macro collapse: Recession hits, AI spending growth stalls, hyperscalers cut capex dramatically

- 🐻 Short thesis proves right: 28-31% short interest represents smart money seeing fatal flaws

- ⚡ Technology obsolescence: AI workload requirements change, APLD's infrastructure becomes less relevant

- 💰 Profitability never arrives: Continue burning cash through 2028 and beyond, equity value destroyed

Critical failure modes:

- 🛡️ Break below $20: Gamma support evaporates, momentum turns sharply negative

- 🛡️ Fall to $15: Original IPO levels, market loses faith in turnaround

- 🛡️ Crash to $10: Near $8 strike of this trade - would be devastating but call buyer still has $2 intrinsic value

- 🛡️ Worst case $5-8: Company survives but equity nearly worthless, calls expire with minimal value

Call option P&L in Bear Case:

- Stock at $20: Calls worth $12.00, LOSS = -$6.20/share × 65,000 = -$40.3M loss (-34% - ouch but not total loss)

- Stock at $15: Calls worth $7.00, LOSS = -$11.20/share × 65,000 = -$72.8M loss (-61%)

- Stock at $10: Calls worth $2.00, LOSS = -$16.20/share × 65,000 = -$105.3M loss (-88%)

- Stock at $8 or below: Calls expire WORTHLESS, LOSS = -$18.20/share × 65,000 = -$118.3M loss (-99%!)

Why this is "only" 25% probability: While execution risk is REAL and APLD is unproven at scale, they have major advantages working in their favor:

- ✅ $16B contracted revenue with investment-grade customers is REAL (not speculative)

- ✅ $5B Macquarie financing removes immediate capital risk

- ✅ Nvidia involvement validates technology and design

- ✅ Buildings are already under construction (not vaporware)

- ✅ First 100MW building substantially complete as of July 2025

For total catastrophe, would need MULTIPLE negative catalysts to align simultaneously. More likely is base case (solid but unspectacular) or bull case (execution delivers). But the 25% bear risk is why this is a RISKY trade despite the massive size.

💡 Trading Ideas

🛡️ Conservative: Wait and Watch (Smart Money Play)

Play: Stay in cash until Q2 FY2026 earnings (January 20) and post-earnings clarity

Why this works:

- ⏰ De-risk earnings: Avoid binary event risk with company reporting in 33 days

- 📊 See proof of concept: Need confirmation first 100MW building is generating revenue and margins improving

- 💸 High volatility: Beta of 7.10 means stock can drop 10-20% on any negative surprise - avoid catching falling knife

- 🎯 Better entry likely: If earnings disappoint, could get $18-20 entry (25% discount from current)

- 🐻 Respect the shorts: 28-31% short interest means bears have conviction - they may know something

- 😰 Insider selling concern: Persistent insider selling is a red flag

Action plan:

- 👀 Watch January 20 earnings for: revenue vs $75-85M guidance, gross margin trends, Polaris Forge 1 building status

- 📈 Look for post-earnings pullback to $20-22 gamma support for entry with 15-20% margin of safety

- ✅ Need to see: revenue >$80M, margins improving from 13% toward 19%, customer pipeline expanding

- ⏰ If execution solid post-earnings, enter position in February with better visibility through mid-2026

- 🚫 If earnings show delays or margin compression, stay away - bear case may be playing out

Risk level: Minimal (cash) | Skill level: Beginner-friendly | Time horizon: 1-3 months

Expected outcome: Avoid potential -20-30% drawdown if earnings disappoint. Get better entry if stock consolidates. Maintain optionality for bull thesis once de-risked.

⚖️ Balanced: Small LEAP Position (Copy the Whale at Scale)

Play: Buy small position in January 2027 or 2028 calls, mimicking institutional structure but at retail size

Structure: Buy APLD January 2027 $15 calls OR January 2028 $10 calls

Why this works:

- 🤝 Copy smart money: Institutional player just bet $119M with 3-year horizon - you can do same at smaller scale

- 📊 Deep ITM = lower risk: Using strikes closer to current price ($15 or $10 strikes vs $8) gives more intrinsic value

- ⏰ Time on your side: 2-3 years allows multiple catalysts to play out (both campuses, profitability inflection)

- 💰 Defined risk: Know maximum loss upfront (premium paid), unlimited upside if thesis correct

- 🎯 Leverage without margin: Control $20-30K worth of stock with $5-10K investment

- 🚀 Asymmetric payoff: Risk 1x to make 3-5x if APLD executes on $16B contracted revenue

Estimated pricing (adjust based on current IV):

- January 2027 $15 calls: ~$11-13 (stock at $23.89) = ~$8.89 intrinsic + $2-4 time premium

- January 2028 $10 calls: ~$15-17 = ~$13.89 intrinsic + $1-3 time premium

Example position sizing:

- 💼 Risk $5,000-10,000 (5-10% of $100K portfolio)

- 📊 Buy 5-10 contracts of Jan 2027 $15C or Jan 2028 $10C

- 🎯 Target exit: $40-50 stock price (2-3x return on options)

- 🛡️ Stop loss: -50% (cut position if drops to half value, indicating thesis breaking)

P&L scenarios (using Jan 2027 $15C at $12 cost):

- 📈 Stock at $40 by Jan 2027: Calls worth $25, profit = $13/contract = 108% ROI

- 🚀 Stock at $50 by Jan 2027: Calls worth $35, profit = $23/contract = 192% ROI

- 📉 Stock at $20 by Jan 2027: Calls worth $5, loss = -$7/contract = -58% loss

- 💀 Stock below $15 by Jan 2027: Calls expire worthless, loss = -$12/contract = -100% loss

Entry timing:

- 🎯 Best: Wait until after January 20 earnings for volatility crush

- ⚖️ Alternative: Scale in 1/3 now, 1/3 post-earnings, 1/3 after Polaris Forge 1 revenue confirmation

- 📊 Avoid: Buying right before earnings (IV spike makes options expensive)

Management rules:

- ✅ Take partial profits if stock hits $35-40 (sell 1/3-1/2 to lock gains)

- ❌ Cut position -50% if thesis breaking (margins staying at 13%, revenue disappointments)

- ⏰ Review quarterly after each earnings to ensure execution on track

- 🎯 Final exit by mid-2027 (don't hold to expiration, avoid time decay acceleration)

Risk level: Moderate (can lose 100% of premium) | Skill level: Intermediate | Time horizon: 18-36 months

Probability of profit: ~40-50% (requires stock above breakeven ~$27-28 for Jan 2027 $15C)

🚀 Aggressive: Stock + Covered Calls (Income on Volatility)

Play: Buy APLD stock at current levels, sell near-term covered calls to reduce cost basis

Structure:

- Buy 100-500 shares at $23-24

- Sell weekly or monthly $25-27 strike calls against position

Why this could work:

- 🎢 Monetize volatility: Stock has 7.10 beta and huge daily swings - sell expensive calls repeatedly

- 💰 Income generation: With high IV, can collect 3-5% monthly premium selling OTM calls

- 📊 Reduce cost basis: If stock stays below strikes, keep premium and reduce effective entry price

- ⚖️ Participation in upside: Still benefit from moves to $30-35 before getting called away

- 🛡️ Better than naked stock: Covered call strategy reduces risk vs pure stock ownership

- 🔄 Repeatable: Can do this monthly, continuously lowering cost basis over time

Example trade mechanics:

- 🏦 Buy 100 shares at $24 = $2,400 investment

- 📞 Sell 1 contract Jan 2026 $27 call for $1.50 = collect $150 premium (6.25% income!)

- 🎯 If stock stays below $27 by Jan expiration: Keep stock + $150, repeat next month

- 📈 If stock rallies above $27: Get called away at $27 ($300 gain on stock + $150 premium = $450 total = 19% return)

- 💵 Effective cost basis after first month: $24 - $1.50 = $22.50

Income potential:

- 📊 Selling $2-3 OTM calls monthly can generate 5-10% monthly income

- ⏰ Over 3-6 months, could reduce cost basis from $24 to $18-20

- 💰 If stock stays rangebound $22-26, this strategy CRUSHES pure stock ownership

Risks:

- 📈 Miss big moves: If APLD rockets to $40, you get called away at $27 (opportunity cost)

- 📉 Downside unprotected: Stock can still fall to $15-18 - covered call only reduces loss slightly

- ⏰ Management intensive: Need to roll/adjust calls regularly

- 😰 Assignment risk: Could get assigned early if stock gaps through strike

Position sizing:

- 🎯 Start with 100-200 shares ($2,400-4,800)

- 📊 Scale up to 300-500 shares ($7,200-12,000) if strategy working

- 🛡️ Never more than 10-15% of portfolio (this is volatile!)

When to use this strategy:

- ✅ Stock in $22-26 range (rangebound consolidation)

- ✅ Implied volatility elevated (calls expensive)

- ✅ Believe in 2-3 year thesis but expect near-term choppiness

- ❌ Skip if expecting imminent breakout to $35+ (you'll miss it)

Risk level: HIGH (stock ownership + covered calls don't protect downside below current price) | Skill level: Intermediate-Advanced | Time horizon: 3-12 months

Expected outcome: Generate 5-15% monthly income selling volatility while maintaining upside exposure to $30-35. Works best in sideways/slightly up markets.

⚠️ Risk Factors

Don't underestimate these landmines:

-

⏰ Q2 FY2026 earnings in 33 days (January 20): Results will show progress on 100MW building revenue ramp and margin improvement. Any disappointment vs $75-85M guidance or continued margin weakness (stuck at 13%) could trigger -15-25% gap down. Historical precedent shows APLD moves violently on earnings. With beta of 7.10, expect massive volatility.

-

🏗️ First major deployment execution risk: APLD has NEVER operated data centers at this scale (100MW, then 150MW, then 280MW). Q4 FY2025 gross margins crashed to 13% vs projected 19% due to "high fit-out costs" - if they can't improve margins, the business model doesn't work at any revenue level. Company is learning as they build - mistakes WILL happen.

-

💔 Customer concentration catastrophe risk: One customer (likely CoreWeave) represents 62% of revenue. If CoreWeave reduces capacity, renegotiates terms, or exercises termination clauses in the 15-year $11B lease, APLD's entire thesis collapses. This is single-customer dependency at its most extreme. CoreWeave itself is a startup competing in tough AI infrastructure market.

-

🏢 David vs Goliath competition: APLD is fighting Equinix (EQIX) and Digital Realty Trust (DLR) - giants with DECADES of experience, thousands of customers, global footprints, and market caps 10-20x larger. If hyperscalers can get better terms from established players, APLD loses. Core Scientific (CORZ) already has $10.2B CoreWeave contract competing directly.

-

💸 Cash burn and debt crisis risk: $700M debt load, $450M convertible notes, 12.75% Macquarie preferred dividend, and profitability not expected until FY2028 create MASSIVE financial obligations while revenue still ramping. If construction delays or cost overruns, could blow through $5B Macquarie facility and face dilutive financing.

-

📉 Recent 40% crash from peak: Stock fell from $40.20 in August to $23.89 currently (-40%) as market experienced "AI infrastructure sentiment shift". This wasn't company-specific - entire AI data center sector got re-rated lower as investors questioned valuations. Could re-test $20 or even $15 if sector sentiment deteriorates further.

-

🐻 28-31% short interest screams danger: 80.34M shares short (28-31% of float) is MASSIVE bearish positioning. Shorts are sophisticated - they've likely identified execution risks, margin problems, or customer concentration issues retail doesn't see. When nearly 1/3 of float is short, there's smoke (and maybe fire). That said, also creates short squeeze potential if execution delivers.

-

😰 Insider selling at highs is a RED FLAG: Management and insiders have been selling stock near $30-40 levels. If they believed in $50-70 bull case, why sell? Either they needed liquidity (fine) or they think current valuation is rich (concerning). Always watch what insiders DO, not what they SAY.

-

🎢 Extreme volatility with 7.10 beta: This stock can move 10-20% on NO NEWS. Max drawdown of 39.6% in past year shows how fast sentiment can shift. Stock went from $40 to $24 (-40%) in 4 months. Could easily see $18-20 if next earnings disappoints or $30-35 if beats. This volatility is NOT for conservative investors - you need iron stomach.

-

💰 Convertible notes dilution at $9.75: $450M convertible notes with $9.75 conversion price and capped call at $14.72. If APLD rallies above $14.72 before 2030, noteholders convert and shareholders face 15-20% dilution. The $119M call buyer factored this in, but retail investors often don't understand convertible math.

-

🌍 Macro recession risk: If economy weakens in 2026-2027, hyperscaler capex gets CUT FIRST. AI infrastructure spending is discretionary investment, not mission-critical operations. Even with signed leases, customers may slow deployments, renegotiate, or exercise termination clauses if their businesses struggle. APLD has ZERO recession protection at current valuation.

-

⚡ Technology obsolescence wildcard: AI/HPC workload requirements evolving rapidly. What if next-gen AI models need different infrastructure (quantum, photonic, neuromorphic)? APLD's purpose-built facilities designed for current GPU-based AI could become legacy infrastructure in 5-7 years. Long-term risk but real.

🎯 The Bottom Line

Real talk: Someone with DEEP POCKETS just bet $119 MILLION that Applied Digital's AI data center transformation is THE REAL DEAL. This isn't a day trade, swing trade, or even a year-long trade - this is a 3+ YEAR STRATEGIC INVESTMENT in the belief that $16B in contracted revenue from CoreWeave and hyperscalers will transform APLD from a $6B company to a $15-20B+ data center infrastructure powerhouse.

What this trade tells us:

- 🎯 This trader believes APLD trades at $40-60+ by January 2028 (needs 70-150% upside to make trade worthwhile)

- 💰 They're using deep ITM $8 strike calls for stock-like exposure with 5.5x leverage (controlling $155M stock with $119M)

- ⏰ The 3.1-year horizon captures EVERY major catalyst: both campuses online, revenue ramp, profitability inflection, customer diversification

- 📊 They're paying just $2.31 in time premium over 3 years (0.6% per year) - essentially betting intrinsic value grows as company executes

- 🏦 This is sophisticated institutional positioning, not retail gambling - likely a fund with 9-figure AUM making strategic allocation

This is NOT a "buy everything now" signal - it's a "here's the bull thesis, proceed with caution" signal.

If you're bullish on APLD:

- ⏰ Be patient - wait for January 20 earnings to see proof of concept (revenue ramp, margin improvement)

- 🎯 Look for entry at $20-22 if stock pulls back post-earnings (gamma support + better risk/reward)

- 📊 If buying now at $24, position size appropriately (5-10% of portfolio MAX given execution risk)

- 🤝 Consider copying the trade structure: buy 2-3 year deep ITM calls instead of stock for leverage

- 🛡️ Set mental stop at $18-20 (major support breach = thesis breaking)

- ✅ Success requires: 100MW building revenue generating by Q2, margins improving to 35-40%+, customer diversification progressing

If you're skeptical:

- 🐻 28-31% short interest represents massive bearish conviction - bears may see execution risks or margin problems

- 😰 Insider selling and 40% crash from peak warrant caution

- 💰 $700M debt, negative cash flow through FY2028, and 62% revenue from one customer are REAL risks

- 🏗️ First deployment at scale - lots can go wrong with construction, costs, margins

- ⚖️ Wait for multiple quarters of execution proof before dismissing bear case

If you're on the sidelines:

- 👀 This is a SPEC PLAY, not a core holding - only for investors comfortable with 30-50% volatility

- 📅 January 20, 2026 earnings is THE near-term catalyst - mark your calendar!

- 🎯 Watch for: Revenue >$80M, gross margins >15% (improving from 13%), Polaris Forge 1 revenue contribution

- 🚀 Bull thesis REQUIRES execution over 2-3 years: both campuses online, $600M-1B revenue, 40-50% EBITDA margins, path to FY2028 profitability

- 📉 Bear thesis triggers: Revenue misses, margins stuck at 10-15%, construction delays, customer concentration worsens, CoreWeave relationship issues

Mark your calendar - Key catalysts:

- 📅 December 19 (TOMORROW!) - Triple witch options expiration (±5% move expected)

- 📅 January 20, 2026 - Q2 FY2026 earnings (CRITICAL - first look at 100MW building revenue)

- 📅 Q1-Q2 2026 - Polaris Forge 1 first building full revenue ramp

- 📅 Mid-2026 - Polaris Forge 1 second building (150MW) operational

- 📅 2026 - Polaris Forge 2 initial operations begin

- 📅 Early 2027 - Polaris Forge 2 reaches full 280MW capacity

- 📅 FY2027-2028 - Profitability inflection as revenue scales to $600M-1B+

- 📅 January 21, 2028 - Expiration of this $119M call LEAP - judgment day!

Final verdict: Applied Digital's long-term AI infrastructure story is INCREDIBLY compelling - $16B contracted revenue with investment-grade hyperscalers, Nvidia partnership, $5B Macquarie financing, and ~600MW capacity under construction. If they execute flawlessly over next 2-3 years, $50-70 stock price is VERY achievable (2-3x from current levels).

BUT - and this is a BIG but - execution risk is MASSIVE. Gross margins at 13% vs 19% target, profitability not until FY2028, 62% revenue concentration, 28% short interest, and $700M debt create SUBSTANTIAL downside risk. Stock already down 40% from peak at $40.

The $119M call buyer is taking a calculated, high-conviction bet that the risk/reward is favorable over 3+ years. For retail investors, this trade signals the bull thesis is alive - but proceed with caution, position size conservatively, and be prepared for EXTREME volatility along the way.

This is a marathon, not a sprint. APLD either becomes the next great AI infrastructure success story ($40-70 by 2028) or flames out spectacularly ($10-15 if execution fails). The $119M bet says the odds favor success. Time will tell. 🚀

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. The unusual score (8,183x average) reflects this trade's massive size but does not guarantee profitability or suggest you should follow it. APLD carries extreme execution risk, high debt load, customer concentration, and volatility (7.10 beta). Company not expected profitable until FY2028. Can lose 100% of option premium. Past performance doesn't guarantee future results. Always do your own research and consider consulting a licensed financial advisor before trading. This is a speculative, high-risk investment.

About Applied Digital Corporation: Applied Digital is a designer and developer of next-generation digital infrastructure and cloud services for high-performance computing (AI/HPC), operating two North Dakota data center campuses with ~600MW leased capacity and approximately $16 billion in contracted revenue over 15-year lease terms with investment-grade hyperscalers. Market cap: $6.14 billion. Industry: Computer Processing & Data Preparation Services.