AR Unusual Options Activity - $5M Bullish Call Bet Ahead of Q4 Earnings and $2.8B Acquisition Close

January 26, 2026 | Unusual Activity Detected

The Quick Take

Someone just dropped $5 MILLION on AR March $38 calls, buying 40,000 contracts in a single trade. This is an extremely unusual trade for Antero Resources - with a Z-score of 656.78, you might see activity like this only a few times per year in this stock. The timing is notable: Q4 2025 earnings on February 11th, the $2.8B HG Energy acquisition expected to close in Q2 2026, and natural gas prices surging to $8.15/MMBtu amid winter demand. Let's dig into what this could mean.

Company Overview

Antero Resources (AR) is a Denver-based natural gas and NGL producer operating in the Appalachian Basin:

- Market Cap: $10.58 Billion

- Industry: Crude Petroleum & Natural Gas

- Current Price: $35.14

- 52-Week Range: $29.10 - $44.02

- Business: Explores for and produces natural gas and natural gas liquids in the United States and Canada, with 17.9 trillion cubic feet of proven reserves and daily production averaging 3,424 MMcfe (35% liquids, 65% natural gas)

The Option Flow Breakdown

What Just Happened

| Date | Time | Symbol | Side | Type | Expiration | Strike | Volume | Premium | OI Signal | Z-Score |

|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-26 | 10:54:51 | AR | BUY | CALL $38 | 2026-03-20 | $38 | 40,000 | $5M | OPEN | 656.78 |

What This Actually Means

This is a straight-up bullish bet expecting AR to move higher over the next 53 days. Here's the breakdown:

- $5M premium paid: $1.25 per contract times 40,000 contracts = serious conviction

- Strike at $38: That's 8.1% above current price of $35.14 - needs meaningful upside to profit

- March 20 expiration (Triple Witch): Captures Q4 earnings (Feb 11), potential Utica divestiture close (Q1), and extended exposure to natural gas price strength

- Vol/OI Ratio of 33.3x: Volume massively exceeds open interest - this is new positioning, not rolling or adjusting

- Z-Score 656.78: Extremely unusual - this size of trade happens maybe a few times per year in AR

- Classification: STANDALONE long call - no complex multi-leg structure, just a directional bet

Translation: This trader is betting AR breaks out above $38 by mid-March. Given the $38 strike is at the high end of recent trading and just below the 52-week high of $44.02, they're positioned for a meaningful move higher - likely catalyzed by earnings, deal closings, or continued natural gas price strength.

Technical Setup / Chart Check-Up

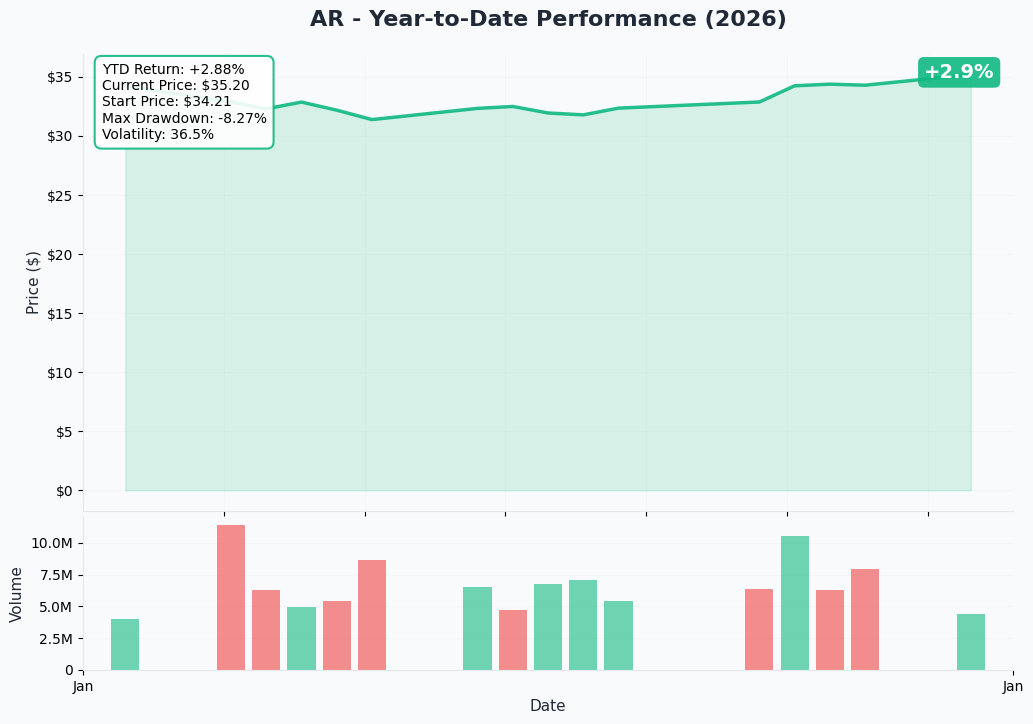

YTD Performance Chart

AR has been trading in a relatively tight range, currently sitting at $35.14 after recovering from lows around $29. The stock is roughly 20% below its 52-week high of $44.02, suggesting potential upside if catalysts materialize. Recent volatility has been elevated due to the HG Energy acquisition announcement and natural gas price swings.

Key observations:

- Stock trading mid-range between 52-week extremes

- Recent support established around $34-35 level

- Resistance zone in the $37-40 area from previous trading

- Volume picking up as natural gas prices surge on winter demand

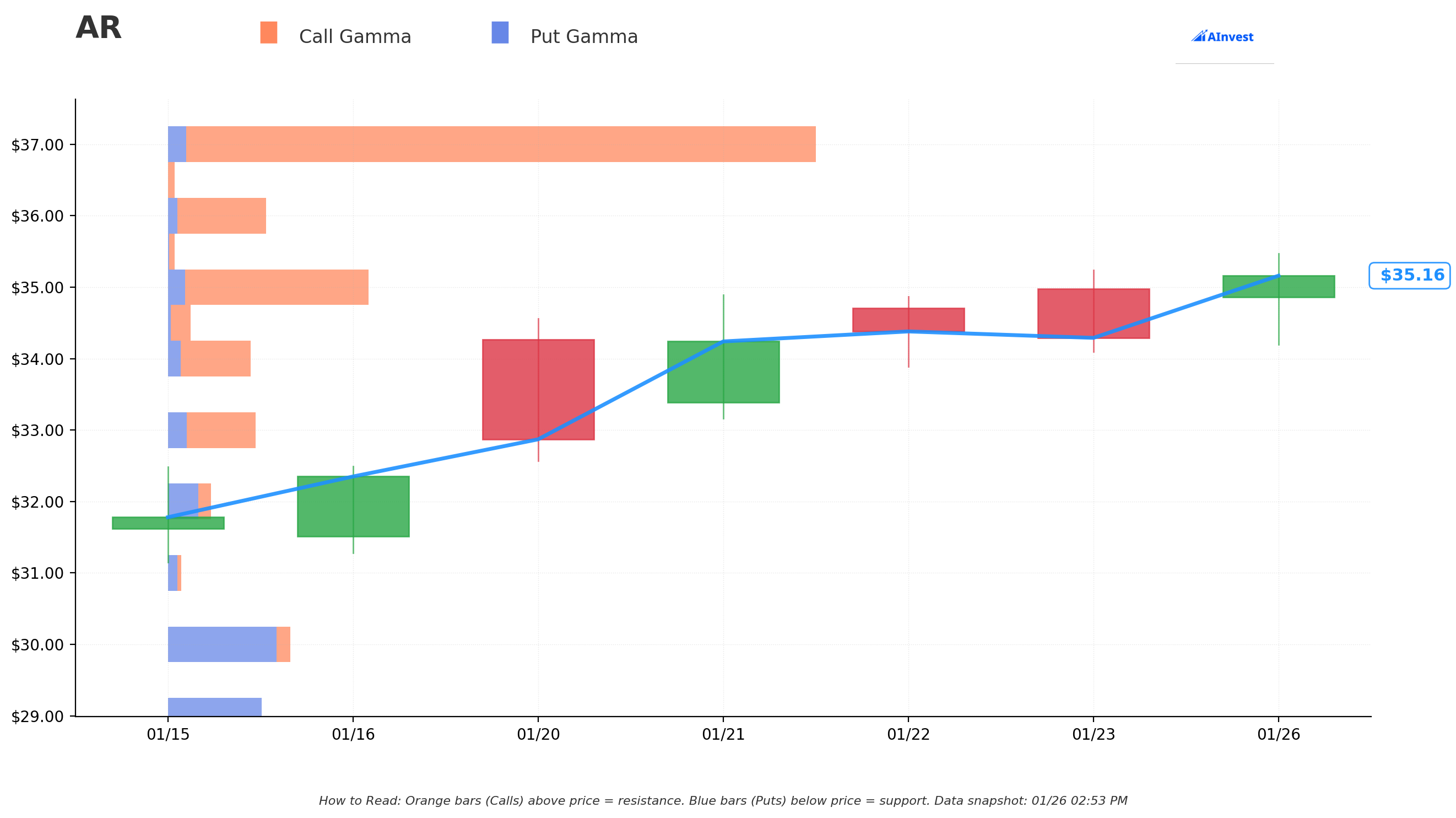

Gamma-Based Support & Resistance Analysis

Current Price: $35.12

The gamma exposure map reveals where market makers have significant positioning that could influence price action:

Support Levels (Blue Bars - Put Gamma Below Price):

- $35.00 - Immediate support (0.3% below) with 4.48B total gamma exposure - dealers will defend this level

- $34.00 - Secondary support (3.2% below) with 1.84B gamma

- $33.00 - Deeper support (6.0% below) with 1.96B gamma

- $30.00 - Major structural floor (14.6% below) with 2.75B gamma (heavy put activity)

- $29.00 - Extended support (17.4% below) with 2.09B gamma

Resistance Levels (Orange Bars - Call Gamma Above Price):

- $36.00 - First ceiling (2.5% above) with 2.19B gamma

- $37.00 - MAJOR RESISTANCE (5.4% above) with 14.38B gamma - this is the BIG ONE

- $38.00 - Secondary resistance (8.2% above) with 1.22B gamma - the CALL STRIKE from this trade

- $39.00 - Extended resistance (11.0% above) with 1.70B gamma

- $40.00 - Psychological barrier (13.9% above) with 4.89B gamma

What this means for traders: The massive 14.38B gamma wall at $37 is the key level to watch. AR needs to break through $37 convincingly for the $38 calls to pay off. The good news: $35 support is solid with positive net gamma, and overall positioning shows bullish bias (35.3B call gamma vs 9.9B put gamma). If AR can clear $37, the path to $38-40 opens up quickly.

The call buyer struck at $38 - just above the monster $37 gamma wall. They're betting the positive catalysts (earnings, deals, nat gas prices) provide enough buying pressure to punch through that resistance.

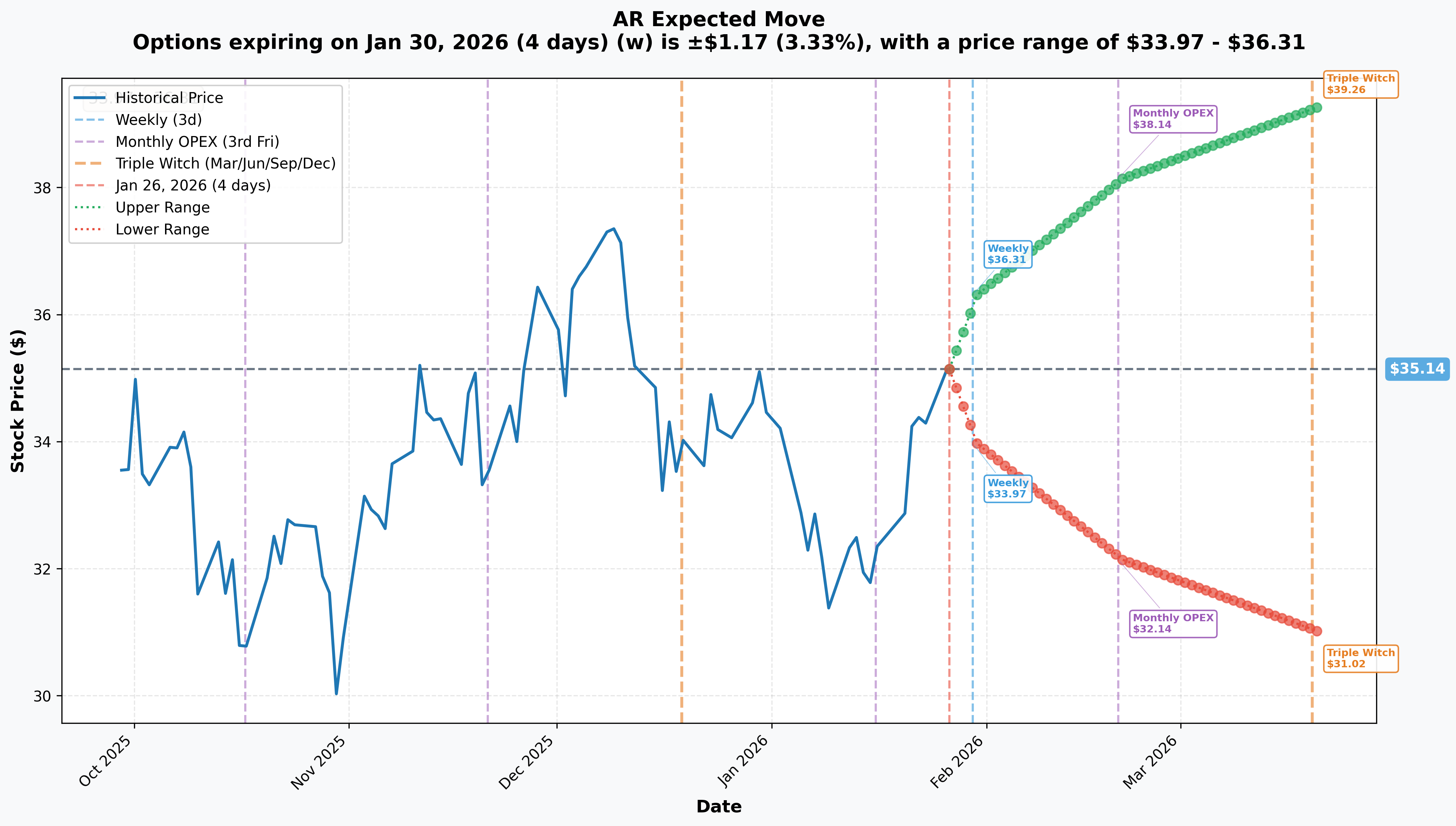

Implied Move Analysis

Options market pricing for upcoming expirations:

| Timeframe | Expiry | Days | Implied Move | Price Range |

|---|---|---|---|---|

| Weekly | Jan 30 | 4 | +/-3.33% ($1.17) | $33.97 - $36.31 |

| Monthly OPEX | Feb 20 | 25 | +/-8.53% ($3.00) | $32.14 - $38.14 |

| Triple Witch | Mar 20 | 53 | +/-11.73% ($4.12) | $31.02 - $39.26 |

Translation: The options market is pricing a potential move of nearly 12% (about $4) by the March 20 expiration. The upper range of $39.26 puts the $38 calls solidly in-the-money if AR moves toward the bullish scenario. The market is acknowledging there's real potential for meaningful moves here.

Key insight: The $38 strike sits within the upper implied range ($39.26), meaning the market views this as achievable but not a layup. This is a reasonable directional bet, not a lottery ticket.

Catalysts

Upcoming Catalysts (Next 2 Months)

Q4 2025 Earnings - February 11, 2026 (16 DAYS)

AR's Q4 earnings release is scheduled for after market close with the conference call February 12 at 9:00 AM MT.

- Production Guidance: 3.5 - 3.525 Bcfe/d expected

- Free Cash Flow Estimate: $245M (up from $70M in Q3)

- Key Watch Items: MI325X production commentary, HG integration updates, hedging position updates

Senior Notes Offering Close - January 28, 2026 (2 DAYS)

The $750M senior notes offering closes in two days, securing funding for the HG acquisition.

Utica Divestiture - Expected Q1 2026

The $800M sale to Infinity Natural Resources should close this quarter, adding significant cash to the balance sheet.

Dry Gas Pad Turn-in-Line - Q1 2026

First dry gas pad expected online in Q1, demonstrating capability to supply data centers and power generation - a strategic proof of concept.

HG Energy Acquisition Close - Expected Q2 2026

The transformative $2.8B acquisition adds 850 MMcfe/d production and 385,000 net Marcellus acres. This is the biggest catalyst on the horizon.

Recent Catalysts (Already Happened)

Natural Gas Price Surge - January 2026

Henry Hub spot reached $8.15/MMBtu during the historic winter storm, with prices above $6/MMBtu for the first time since December 2022. Winter demand knocked 10% of U.S. gas production offline temporarily.

HG Energy Acquisition Announced - December 8, 2025

The $2.8B deal adds massive Marcellus acreage directly south of AR's existing footprint, with estimated $950M in synergies over 10 years.

Q3 2025 Results - October 30, 2025

Revenue of $1.21B (up 15% YoY), Adjusted EBITDAX of $318M (up 70% YoY), and quarterly record of 14.5 completion stages per day. Free cash flow swung positive to $90M.

Wells Fargo Tactical Pick - January 5, 2026

Added AR to Q1 2026 Tactical Ideas list with Buy rating and $49 price target (55.5% upside).

Price Targets & Probabilities

Based on gamma levels, implied moves, and catalyst density, here are the scenarios through March 20 expiration:

Bull Case (35% probability)

Target: $40-$44

How we get there:

- Q4 earnings beat expectations with strong FCF and confident 2026 guidance

- Natural gas prices remain elevated ($5-6 range) through winter

- HG acquisition on track for Q2 close with positive integration commentary

- Utica divestiture closes, adding $800M cash

- Analysts raise targets following Wells Fargo's lead

- Break above $37 gamma wall triggers momentum buying to $40+

Why 35%: Multiple positive catalysts align, natural gas fundamentals supportive, Wells Fargo's $49 target suggests significant Street optimism. The call buyer's positioning suggests they see this scenario as realistic.

Base Case (45% probability)

Target: $35-$38 range (CONSOLIDATION)

Most likely scenario:

- Earnings meet consensus, no major surprises

- Natural gas prices normalize from winter spike but remain supportive ($3.50-4.50)

- Deals progress as expected without acceleration or delays

- Stock trades between $35 support and $37 resistance

- Call buyer's position gains modest value but doesn't hit home run

Why 45%: Stock already reflects deal announcements and nat gas tailwinds. Market waiting for execution proof points. $37 gamma resistance limits upside without major catalyst surprise.

Bear Case (20% probability)

Target: $30-$34

What could go wrong:

- Natural gas prices collapse post-winter (EIA forecasts modest 2% decline in 2026)

- NGL weakness continues (propane at 68 cents vs 90 cents year ago)

- HG integration concerns emerge or deal timeline slips

- Earnings disappoint on margins or FCF

- Break below $35 support triggers selling toward $30 gamma floor

Why 20%: Strong hedging ($3.22 floor), committed deal financing, and winter demand support prices near-term. Would require multiple negative surprises to break below $33.

Trading Ideas

Conservative: Wait for Breakout Confirmation

Play: Watch the $37 level - only enter if AR breaks and holds above

Why this works:

- The $37 gamma wall is the key resistance - no need to guess if it holds

- Q4 earnings February 11 provides clarity on fundamentals

- Let the $5M trade work first - if smart money is right, you'll still catch most of the move

- Avoid being stuck if stock consolidates in $35-37 range

Action plan:

- Set alert at $37.50 (confirmation of breakout)

- If triggered, consider buying shares or March $39-40 calls

- Risk 3-5% of portfolio maximum

- Stop loss at $35 (gamma support)

Risk level: Low | Skill level: Beginner-friendly

Balanced: Bull Call Spread Targeting Gamma Breakout

Play: Buy the $37 call, Sell the $40 call (March 20 expiration)

Why this works:

- Defined risk spread caps maximum loss at debit paid

- Targets the $37 breakout zone this large trade is betting on

- Lower cost than outright call purchase

- Max profit if AR reaches $40 by March expiration

- Captures earnings catalyst and potential deal news

Estimated P&L:

- Cost: ~$1.00-1.30 per spread ($100-130 per contract)

- Max profit: $3.00 per spread ($300 per contract) if AR at or above $40

- Max loss: Premium paid

- Breakeven: ~$38.00-38.30

- Risk/Reward: Approximately 2.3:1

Position sizing: Risk 2-5% of portfolio (5-10 spreads for a $10K account)

Risk level: Moderate | Skill level: Intermediate

Aggressive: Follow the Flow - Long March $38 Calls

Play: Buy the March $38 calls (same trade as the whale)

Why this could work:

- Riding alongside a $5M institutional bet with 656x Z-score

- 53 days to expiration captures multiple catalysts

- If AR breaks $37 resistance, $38 calls could double quickly

- Upper implied range ($39.26) puts this strike in-the-money in bull scenario

- Natural gas tailwind with winter demand ongoing

Why this could fail (REAL RISKS):

- $37 gamma wall could cap upside through expiration

- Natural gas prices could normalize, removing enthusiasm

- Need 8%+ move just to break even (strike + premium)

- Earnings could disappoint on NGL weakness or margin compression

- Time decay works against you daily

Estimated P&L:

- Cost: ~$1.25 per contract ($125 per contract)

- Profit scenario (AR at $42): ~$2.75 profit (220% ROI)

- Profit scenario (AR at $40): ~$0.75 profit (60% ROI)

- Loss scenario (AR below $38): Lose entire premium

Position sizing: Risk only 1-2% of portfolio - this is a directional bet

Risk level: High | Skill level: Advanced

Risk Factors

Don't overlook these potential headwinds:

-

Natural gas price volatility: Prices surged to $8.15 on winter demand but EIA forecasts modest decline to ~$3.50 in 2026. If weather normalizes and prices retreat, AR loses tailwind support.

-

NGL weakness persists: JPMorgan downgraded AR on NGL concerns, with propane at 68 cents vs 90 cents year ago. NGLs represent significant revenue exposure.

-

HG acquisition integration risk: $2.8B deal increases leverage with $1.5B term loan. Synergy realization ($950M over 10 years) is uncertain. If deal hits snags, stock suffers.

-

$37 gamma ceiling: Massive 14.38B gamma exposure at $37 creates mechanical selling pressure. Needs sustained buying to break through - not guaranteed even with good earnings.

-

Mixed analyst sentiment: While Wells Fargo has $49 target, Bank of America cut to $39 and Barclays remains at Hold. Consensus is Moderate Buy but not unanimous.

-

Earnings execution risk: February 11 earnings could disappoint on margins, FCF, or 2026 guidance. Stock already reflects deal optimism - limited room for error.

-

Macro headwinds: Higher interest rates affect capital allocation, inflation pressures drilling costs. Recession concerns could hit energy demand.

The Bottom Line

Here's the deal: A trader just committed $5 million to AR $38 calls expiring March 20, betting on meaningful upside over the next 53 days. This is an unusually large trade for Antero - Z-score of 656 means you see activity like this only a few times per year in this name.

What this trade tells us:

- They expect AR to break above $38 by mid-March (currently $35.14)

- They're positioned for Q4 earnings (Feb 11), deal closings, and continued natural gas strength

- The March 20 Triple Witch expiration maximizes exposure to multiple catalysts

- They're willing to pay $1.25 per contract for this bet - that's conviction

The setup makes sense: AR has real catalysts ahead - $2.8B transformative acquisition, $800M divestiture, strong natural gas prices, and earnings in 16 days. The $37 gamma wall is the key obstacle - break that and $38-40 becomes achievable.

But stay grounded: This is still a directional bet that needs multiple things to go right. Natural gas could normalize, NGL weakness could persist, earnings could disappoint. The trade is interesting, not a guarantee.

If you want to follow:

- Consider the bull call spread ($37/$40) for defined risk exposure

- Wait for $37 breakout confirmation before committing capital

- Size appropriately - 1-2% of portfolio maximum on aggressive plays

- Set stop losses at $35 gamma support

If you already own AR:

- Consider selling calls against your position to reduce cost basis

- $38-40 strikes could monetize this activity if you're willing to cap upside

- Q4 earnings February 11 is the next major decision point

Key dates to watch:

- January 28 - Senior notes offering closes ($750M)

- February 11 - Q4 2025 earnings (after close)

- February 12 - Earnings conference call

- Q1 2026 - Utica divestiture expected to close ($800M)

- March 20 - Triple Witch OPEX (this trade expires)

- Q2 2026 - HG Energy acquisition expected to close ($2.8B)

Final verdict: This is a reasonable bullish bet on a company with legitimate near-term catalysts and favorable natural gas dynamics. The trade size is notable and the thesis is clear - AR benefits from deal execution and commodity tailwinds. But it needs $37 to break and earnings to deliver. Watch, learn, and size appropriately if you follow.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual activity score reflects this specific trade's size relative to recent AR history - it does not imply the trade will be profitable or that you should follow it. Natural gas prices are volatile and can move sharply in either direction. Always do your own research and consider consulting a licensed financial advisor before trading.

About Antero Resources: Antero Resources, based in Denver, explores for and produces natural gas and natural gas liquids in the United States and Canada. The company holds 17.9 trillion cubic feet of proven reserves with daily production averaging 3,424 MMcfe. Market cap of $10.58 billion in the Crude Petroleum & Natural Gas industry.