🛡️ ARM $4M Put Hedge - Smart Money Bracing for Uncertainty! 💰

📅 December 30, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $4 MILLION on ARM puts this morning at 11:33:17! This defensive bet bought 1,500 contracts of $120 strike puts expiring January 15, 2027 - protecting a position more than a year out with the stock at $111.80. With ARM down -15% over 52 weeks and facing a critical strategic pivot to becoming a chipmaker, institutional money is locking in long-term downside protection. Translation: Smart money thinks there's meaningful risk ARM trades below $120 over the next 12+ months!

📊 Company Overview

ARM Holdings (ARM) is the IP licensing giant behind the architecture powering 99% of the world's smartphones:

- Market Cap: $117.25 Billion (semiconductor IP licensing)

- Industry: Semiconductor intellectual property

- Current Price: $111.80 (down from 52-week high of $183.16)

- Primary Business: ARM architecture licensing, royalty revenue from chip shipments, expanding into first-party chip manufacturing for data centers

ARM isn't a traditional chipmaker - they design the instruction set architecture that powers everything from iPhones to data center servers, collecting licensing fees and per-chip royalties from manufacturers like Apple, Qualcomm, and Amazon.

💰 The Option Flow Breakdown

The Tape (December 30, 2025 @ 11:33:17):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:33:17 | ARM | ASK | BUY | PUT $120 | 2027-01-15 | $4M | $120 | 1.5K | 1.7K | 1,500 | $111.80 | $26.35 |

🤓 What This Actually Means

This is LONG-TERM portfolio insurance with serious conviction! Here's what stands out:

- 💸 Big premium paid: $4M ($26.35 per contract × 1,500 contracts)

- 🛡️ Deep protection: $120 strike is 7.3% ABOVE current price of $111.80 (this is in-the-money!)

- ⏰ Strategic timeframe: 381 days to expiration - protecting through ALL of 2025 catalysts

- 📊 Position size: 1,500 contracts = 150,000 shares worth ~$16.8M at current price

- 🔍 High conviction: Paying $26.35 for $120 puts when stock at $111.80 = already $8.20 intrinsic value, plus $18.15 time premium

What's really happening here: This trader is paying a MASSIVE premium for downside protection extending through 2025 and into early 2027. The fact they chose $120 strikes ABOVE the current $111.80 price rather than cheaper out-of-the-money puts shows they're NOT speculating - they're PROTECTING. These puts are already in-the-money by $8.20/share, meaning they have intrinsic value TODAY.

Think of this like buying comprehensive insurance on a luxury car you're worried about - you pay extra premium to protect not just from crashes, but from any depreciation below a certain value. This trader is willing to pay $26.35/share to lock in a $120 floor for the next 381 days.

Unusual Score: 🔥🔥 EXTREMELY UNUSUAL (Z-Score: 36.15) - This happens maybe a few times per year! The classification shows "EXTREMELY_UNUSUAL" activity with HIGH volume signal. With only 1,700 existing open interest, adding 1,500 contracts in a single block is MASSIVE relative positioning.

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

ARM has had a brutal 2025 - down -15.03% from December 2024 with current price of $111.53 (started at $131.79 on Dec 24, 2024). The chart tells a painful story of hype deflation after hitting all-time highs.

Key observations:

- 📉 Epic collapse: Peaked at $183.16 in 52-week range, now down 39% from those highs

- 🔻 Seven-day losing streak: Fell 7 consecutive days through December 18 with -19.2% decline over 10-day period

- 💔 Goldman downgrade damage: Goldman Sachs cut to "Sell" with $120 target on December 15 triggered massive selloff

- 📊 Below 200-day MA: Stock broke through ~$138 support (triggered by Oracle earnings disappointment on December 11)

- ⚠️ Valuation compression: Trading at 48.80-57.82x forward P/E, down from premium levels but still elevated

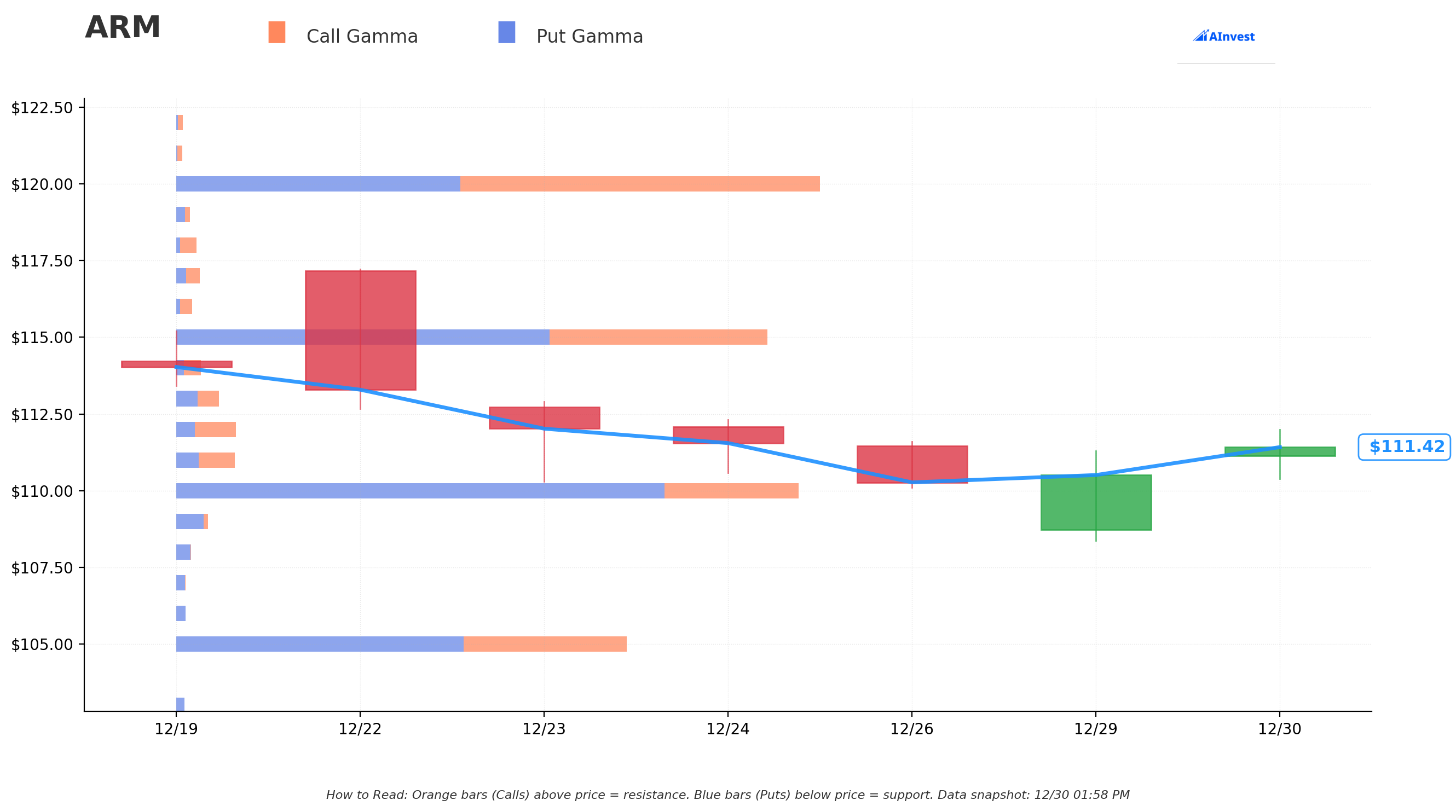

Gamma-Based Support & Resistance Analysis

Current Price: $111.53

The gamma exposure map reveals critical price magnets that could govern near-term action:

🔵 Support Levels (Put Gamma Below Price):

- $110 - Very strong support with 13.16B total gamma exposure (STRONGEST NEARBY FLOOR!)

- $105 - Strong secondary support at 9.00B gamma (dealers will defend aggressively)

- $100 - Deep support zone at 6.23B gamma

- $95 - Extended floor (not shown but implied from structure)

🟠 Resistance Levels (Call Gamma Above Price):

- $115 - Very strong immediate ceiling with 12.57B gamma (just 3% overhead)

- $120 - Very strong resistance at 13.74B gamma (EXACTLY where this put is struck! 🎯)

- $125 - Secondary ceiling at 5.61B gamma

- $130 - Major resistance zone with 5.53B gamma (17% rally required)

What this means for traders: ARM is trading in a narrow channel between massive $110 support and crushing $115 resistance. The gamma data shows the stock is PINNED - market makers have huge positions at both levels creating mechanical pressure to keep price contained.

Notice anything CRITICAL? The put buyer struck at $120 where there's 13.74B gamma resistance - one of the two strongest levels on the entire chart! They're betting ARM can't sustainably break above $120 over the next 381 days. That $120 level has been tested and represents a massive options barrier where dealers will sell into rallies.

If ARM breaks below the $110 support wall (13.16B gamma), the next stop is $105, then potentially a flush to $100. Conversely, breaking above $115 faces immediate resistance at $120.

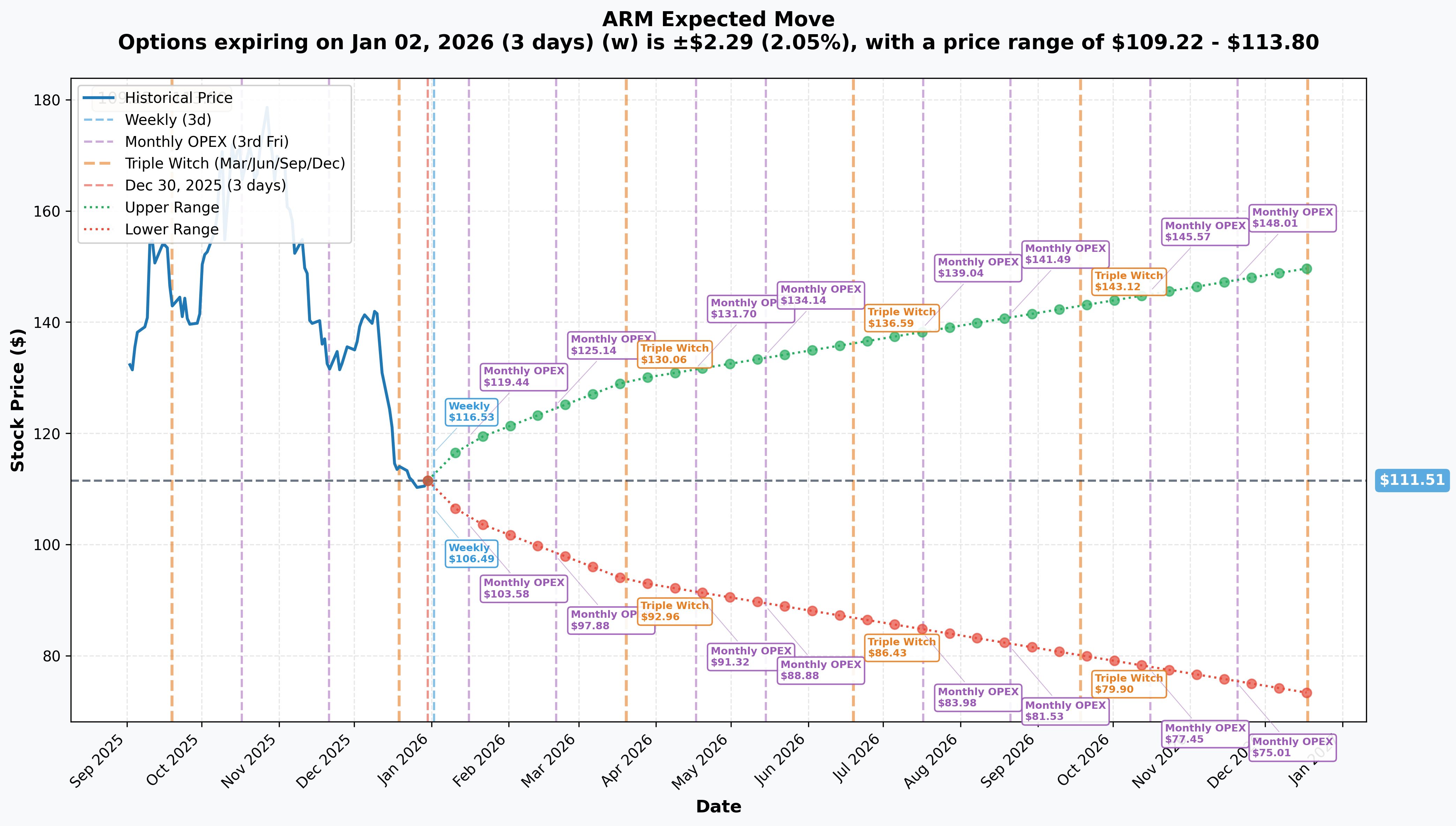

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 2, 2026 - 3 days): ±$2.29 (±2.05%) → Range: $109.22 - $113.80

- 📅 Monthly OPEX (Jan 16, 2026 - 17 days): ±$7.06 (±6.33%) → Range: $104.45 - $118.57

- 📅 Quarterly Triple Witch (March 20, 2026 - 80 days): ±$17.96 (±16.1%) → Range: $93.55 - $129.47

- 📅 Yearly LEAPS (Dec 18, 2026 - 353 days): ±$38.21 (±34.26%) → Range: $73.30 - $149.72

Translation for regular folks: Options traders are pricing in a 2% move ($2.29) by Friday for weekly expiration, but a much larger 16% move ($18) through March quarterly expiration. The market expects meaningful volatility as catalysts unfold.

The LEAPS expiration (closest to this January 2027 trade) has a lower range of $73.30 - meaning the market thinks there's a real possibility ARM could trade as low as $73 over the next year. That's a 34% downside move from current levels! This aligns with the put buyer's defensive thesis: protect against significant deterioration if the first-party chip strategy backfires or data center share gains stall.

Key insight: The massive increase from 2% (weekly) to 34% (yearly) implied move shows the market is pricing SUBSTANTIAL uncertainty about ARM's strategic transformation over the next 12 months.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened - Last 90 Days)

Q2 FY2026 Earnings Beat - November 5, 2025 ✅

ARM delivered strong results that initially boosted sentiment:

- 📊 Revenue: $1.14B, up 34% YoY, exceeding guidance midpoint by $75M

- 💰 Royalty Revenue: $620M, up 21% YoY (record high)

- 🏭 Licensing Revenue: $515M, up 56% YoY

- 🎯 Non-GAAP EPS: $0.39 vs $0.33 consensus (18% beat)

- 📈 Operating Margin: 41.1% vs 38.6% prior year

- 🇨🇳 China Revenue: 22% of total sales - record high

- 🤝 CSS Momentum: Three new ARM Compute Subsystems licenses signed, bringing total to 19 licenses with 11 companies

- 🚀 Neoverse Growth: Business more than doubled YoY

Why the stock still fell: Despite the beat, stock couldn't hold gains due to concerns about valuation, Goldman downgrade, and skepticism about AI leverage.

NVIDIA NVLink Fusion Partnership - November 17, 2025 🤝

ARM announced integration of NVIDIA NVLink Fusion into the Neoverse platform:

- ⚡ Enables seamless connectivity between ARM CPUs and NVIDIA GPUs in AI data centers

- 🎯 Removes bandwidth bottlenecks limiting AI performance

- 💪 NVIDIA CEO Jensen Huang: "NVLink Fusion is the connective fabric of the AI era"

- 📈 Validates ARM's competitiveness in AI infrastructure

Goldman Sachs Downgrade to SELL - December 15, 2025 😰

The catalyst that triggered the recent selloff:

- 📉 Rating: Neutral → Sell

- 💰 Price Target: $160 → $120 (25% cut)

- 🎯 Rationale: Limited leverage to AI cycle vs direct AI hardware plays; higher R&D spending expected to reduce financial leverage

- 📊 Impact: Triggered 7-day losing streak and -19.2% decline over 10 days

Other Analyst Activity:

- Bank of America: Maintained Buy, but cut target $205 → $145 (29.3% reduction) on December 16

- Loop Capital: Raised target $155 → $180 (16.1% increase) on November 12, maintaining Buy

Current Consensus: Average price target $165.46 (range: $80-$225), rating: Buy (45% Strong Buy, 45% Buy)

Strategic Partnerships Announced:

- 🤝 Meta partnership spanning AI wearables to data centers (October 2025)

- 🚗 Rivian autonomy breakthrough built with ARM (December 11, 2025)

- 🇰🇷 South Korea educational facility MOU (December 5, 2025)

🚀 Upcoming Catalysts (Next 12 Months - Through Put Expiration)

Q3 FY2026 Earnings - February 4, 2026 (35 DAYS!) 📊

The next major binary event:

- 📊 Consensus Revenue: $1.225B (+/- $50M), ~25% YoY growth

- 💰 Consensus EPS: $0.41 (+/- $0.04)

- 🎯 Key Metrics to Watch:

- Data center royalty growth trajectory (needs to accelerate from 21% YoY)

- CSS license momentum (need more than 3 new licenses)

- China revenue stability amid RISC-V competition

- Progress updates on first-party chip development

- Commentary on 50% data center market share target

Upside potential: Strong MI325X adoption by hyperscalers, additional CSS wins, China revenue resilience Downside risk: Any guidance disappointment, first-party chip timeline delays, margin compression concerns

First-Party Data Center Chip Launch - Summer 2025/Early 2026 🏭

ARM CEO Rene Haas expected to unveil ARM's first in-house server CPU:

- 🎯 Target Market: AI workloads and high-performance computing in data centers

- 🤝 First Customer: Meta reportedly secured as launch customer

- 🏭 Manufacturing Partner: TSMC

- 💰 Strategic Shift: Represents move to capture higher margins in $700B semiconductor market

- ⚠️ Customer Conflict Risk: Directly competes with licensees (Qualcomm, MediaTek, Samsung)

Why this matters for the put: This is THE make-or-break catalyst. If the first-party chip disappoints technically or alienates key licensee customers, the entire strategic thesis unravels. Success could send stock to $150+, but failure could crater it to $80-90 range. The January 2027 expiration captures this entire lifecycle.

Q4 FY2026 & Full Year Earnings - May 6, 2026 📅

- 📈 Will provide FY2027 guidance and long-term roadmap updates

- 🎯 Critical for understanding multi-year revenue trajectory from first-party chips

- 💰 Investors will scrutinize margin impact of chip manufacturing vs pure IP licensing

Stargate Project Progress - Ongoing Through 2026 🌟

ARM is key technology partner in $500B Stargate initiative with SoftBank and OpenAI:

- 🏗️ Five new U.S. AI data center sites announced, targeting 7 gigawatts total capacity

- 💰 Over $400B committed next three years

- 🎯 Full $500B, 10-gigawatt plan on track for end of 2025

- ⚠️ SoftBank Risk: SoftBank has $8.5B margin loan against ARM shares, with capacity for $11.5B more - creates forced selling risk if parent faces liquidity issues

50% Data Center Market Share Target - End of 2025 🎯

ARM aims to capture 50% of data center CPU market among top hyperscalers (up from 15% in 2024):

Progress indicators:

- ✅ AWS: 50% of processors are ARM Graviton CPUs

- ✅ Google Axion, Microsoft Cobalt, Oracle Cloud building on Neoverse

- ✅ NVIDIA Grace CPUs with 144 ARM Neoverse V2 cores power GB200/GB300 AI servers

Reality check: Analysts like Omdia estimate ARM reaches only 20-23% by end of 2025, citing x86's entrenched ecosystem. If ARM misses this target badly, it undermines credibility and could hurt stock significantly.

⚠️ Risk Catalysts (Why Someone Bought $4M of Protection)

RISC-V Competition & China Headwinds 🇨🇳

The existential threat:

- 🚨 Chinese government preparing formal guidelines to promote RISC-V as ARM alternative

- 📉 China was 19% of ARM's FY2025 revenue, with only 7.5% YoY growth signaling competitive pressure

- 🌐 RISC-V is open-source, royalty-free - threatens ARM's licensing model in price-sensitive markets

- ⚖️ ARM CEO warned U.S. export controls "threaten to slow overall tech advances"

First-Party Chip Customer Conflict 😰

Becoming a fabless chipmaker contradicts ARM's "Switzerland" neutral licensing model:

- 💔 Qualcomm, MediaTek, Samsung could reduce ARM engagement

- 📊 Licensing revenue (56% growth in Q2) at risk if customers see ARM as competitor

- ⚖️ Delicate balance between chip revenue upside and licensing revenue downside

AMD Data Center Competition 💻

While ARM targets 50% data center share, AMD is rapidly gaining ground:

- 📈 AMD expected to become largest x86 supplier in 2026 at ~40% market share

- 💪 x86 software ecosystem advantages remain powerful

- 🎯 Intel weakness creates opportunity for BOTH AMD and ARM, but AMD positioned to capture more

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are scenarios through January 15, 2027 expiration:

📈 Bull Case (20% probability)

Target: $150-$170

How we get there:

- 🚀 First-party chip launch in mid-2025 CRUSHES expectations with major hyperscaler orders beyond Meta

- 📊 Q3/Q4 earnings beats demonstrate accelerating data center royalty growth (30%+ YoY)

- 🤝 Data center market share reaches 35-40% by end of 2025 (not quite 50%, but impressive)

- 💰 Licensing revenue proves resilient despite customer concerns - new CSS wins continue

- 🇨🇳 China RISC-V threat contained, ARM maintains market dominance

- 🌟 Stargate deployment proceeds on schedule with ARM as cornerstone

- 💪 Margins expand to 45%+ as chip business scales with favorable mix

Key metrics needed:

- Data center revenue growing >35% YoY

- First-party chip revenue ramping to $500M+ run-rate

- Gross margins stable or expanding despite chip business mix

- Market share gains validated by third-party data

Probability assessment: Only 20% because requires flawless execution on risky strategic pivot while maintaining existing licensing business. Stock currently at $111.80 with Goldman at $120 target - needs major positive surprise to reach $150+.

🎯 Base Case (50% probability)

Target: $95-$125 range (CHOPPY WITH DOWNWARD BIAS)

Most likely scenario:

- ✅ Q3/Q4 earnings meet or slightly beat consensus, but don't wow

- 📱 First-party chip launches on time but adoption measured - not explosive

- ⚖️ Data center market share reaches 25-30% (solid but well short of 50% target)

- 📉 Some licensee customer friction emerges but manageable

- 🇨🇳 China revenue plateaus or declines slightly due to RISC-V competition

- 💰 Margins compress slightly (39-40%) due to chip business ramp costs

- 🎢 Stock trades volatile range between $110 gamma support and $120 gamma resistance

- 😰 Sentiment remains mixed - bulls point to AI growth, bears cite valuation and execution risk

This is the put buyer's target: Stock muddles through $95-125 range for 12 months. The $120 puts provide partial protection if stock drifts toward $100-105, and full protection if it breaks lower. The $4M is insurance premium for wealth preservation on a large long position.

Why 50% probability: Company fundamentals intact but stock at inflection point. Success not guaranteed, disaster not imminent. Most likely outcome is "steady progress without fireworks" which doesn't justify premium valuation re-rating.

📉 Bear Case (30% probability)

Target: $75-$95 (MEANINGFUL DRAWDOWN)

What could go wrong:

- 😰 First-party chip disappoints - technical issues, limited customer interest, or timeline delays to late 2026

- 💔 Major licensee customer (Qualcomm, Samsung) reduces ARM engagement due to conflict of interest

- 🇨🇳 China RISC-V adoption accelerates - ARM loses 5-10 percentage points market share

- 📉 Data center market share stalls at 20-25%, well short of 50% target

- 💸 Q3 or Q4 earnings miss with weak guidance - investors lose patience

- 🚨 SoftBank forced to sell ARM shares due to margin loan pressure or Stargate funding needs

- 📊 Broader semiconductor downturn or AI capex slowdown hits royalty revenue

- ⚖️ Margins compress to 36-37% as chip business requires heavy investment without commensurate revenue

- 🔨 Break below $110 gamma support triggers cascade to $105, then $100

- 😱 Goldman's $120 target proves optimistic - realistic fair value closer to $90

Critical support levels:

- 🛡️ $110: Very strong gamma floor (13.16B) - MUST HOLD or momentum shifts bearish

- 🛡️ $105: Strong secondary support (9.00B gamma)

- 🛡️ $100: Deep support zone (6.23B gamma) - testing this would be disaster scenario

- 🛡️ $95: Psychological and technical breakdown level

Probability assessment: 30% because multiple risk factors could align. Strategic pivot is genuinely risky - becoming chipmaker while maintaining neutral IP licensing role is difficult. RISC-V threat real. Valuation still elevated at 48-58x forward P/E. The $4M put buyer clearly thinks this scenario has >30% odds or they wouldn't pay such rich premium for in-the-money protection.

Put P&L in Bear Case:

- Stock at $95 on Jan 15, 2027: Puts worth $25.00, profit = -$1.35/share × 1,500 = -$2M loss (50% loss on premium)

- Stock at $85 on Jan 15, 2027: Puts worth $35.00, profit = $8.65/share × 1,500 = $13M gain (216% ROI!)

- Stock at $75 on Jan 15, 2027: Puts worth $45.00, profit = $18.65/share × 1,500 = $28M gain (700% ROI!)

- Stock at $110 on Jan 15, 2027: Puts worth $10.00, loss = -$16.35/share × 1,500 = -$24.5M (61% loss)

Key insight: The put buyer paid for puts already $8.20 in-the-money. They're protected NOW at $120, but paying $18.15 in time premium betting stock doesn't sustainably break above $120 and could fall significantly below it.

💡 Trading Ideas

🛡️ Conservative: Avoid Until Clarity Emerges

Play: Stay sidelined until first-party chip launch and Q3 earnings (Feb 4) provide clarity

Why this works:

- ⏰ Major catalysts in next 35-90 days create binary event risk - too unpredictable

- 😰 Goldman Sachs "Sell" rating at $120 vs current $111.80 suggests limited upside

- 📊 Stock in technical no-man's land - not clearly breaking out or breaking down

- 💸 Valuation still elevated (48-58x forward P/E) despite selloff - no margin of safety

- 🎯 Better entry likely if stock consolidates to $100-105 or breaks above $125 with momentum

- 🤔 The $4M institutional put buy signals smart money worried - why fight the trend?

Action plan:

- 👀 Monitor February 4th Q3 earnings for revenue growth, margin trends, first-party chip updates

- 🎯 Watch for first-party chip launch details (customer names, pricing, technical specs)

- ✅ Need validation of 25-30% data center market share progress before considering entry

- 📊 Look for break above $120 gamma resistance with volume as bullish confirmation

- ⏰ Revisit in 3-6 months when strategic pivot clarity improves

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 15-25% drawdown if execution disappoints. Get better entry if stock consolidates. Preserve capital during uncertainty.

⚖️ Balanced: Post-Earnings Put Spread (Defined Risk Downside)

Play: After February 4th earnings, sell put spread if stock fails to impress

Structure: Buy $110 puts, Sell $100 puts (June 20, 2026 expiration - 171 days out)

Why this works:

- 🎢 Post-earnings IV crush makes put spreads cheaper to establish

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 🎯 Targets gamma support zone at $100-110 where significant put gamma sits

- ⏰ June expiration captures Q4 earnings, first-party chip launch fallout, mid-year assessment

- 🛡️ Protects against "meet but don't beat" earnings scenario that disappoints bulls

- 📈 Better risk/reward than buying straight puts due to defined risk

Estimated P&L (adjust based on post-earnings IV):

- 💰 Pay ~$3.50-4.50 net debit per spread post-earnings

- 📈 Max profit: $550-650 if ARM below $100 at June expiration

- 📉 Max loss: $350-450 if ARM above $110 (defined and limited)

- 🎯 Breakeven: ~$106-107

- 📊 Risk/Reward: ~1.3:1 which is acceptable for bearish defined-risk play

Entry timing:

- ⏰ Wait 2-3 days post-Q3 earnings (by Feb 6-7) for full IV collapse

- 🎯 Only enter if stock trades $113+ (gives room to work down to put strikes)

- ❌ Skip if stock already below $108 (spread too close to current price)

- 📉 Best setup: Earnings "meets" consensus but guidance disappoints - stock drifts lower

Position sizing: Risk only 2-4% of portfolio (directional speculation, not core holding)

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

🚀 Aggressive: Long-Dated Call Spread on Breakout (WAIT FOR SETUP!)

Play: IF stock breaks above $120 gamma resistance with conviction, play momentum to $130

Structure: Buy $125 calls, Sell $135 calls (September 18, 2026 expiration - 262 days)

Why this could work:

- 🚀 Breaking above $120 gamma resistance (13.74B) would be MAJOR technical event

- 📊 Would likely signal first-party chip success or major data center share gains

- 💪 Call spread caps risk while providing 4:1 reward/risk potential

- ⏰ September expiration gives time for momentum to build through summer

- 🎯 Targets $130-135 range which represents next major gamma resistance zone

Why this could fail (SERIOUS RISKS):

- ⚠️ WAIT FOR TRIGGER: Do NOT enter unless stock cleanly breaks $120 with volume!

- 💸 Premium expensive if entered too early before breakout confirmed

- 📉 False breakout could reverse quickly back to $110-115 range

- 😰 Requires bullish catalysts to materialize - earnings beats, chip success, share gains

- ⏰ Time decay significant on 9-month spread if stock stalls

Estimated P&L (IF breakout occurs):

- 💰 Cost: ~$3.50-4.50 per spread (after breakout, with IV elevated)

- 📈 Max profit: $550-650 if ARM above $135 at September expiration (145% ROI)

- 📉 Max loss: $350-450 if ARM below $125 (100% loss on premium)

- 🎯 Breakeven: ~$128.50-129.50

- 📊 Risk/Reward: 1:1.5 (acceptable for momentum play with catalyst confirmation)

CRITICAL ENTRY RULES - DO NOT enter unless:

- ✅ Stock closes above $122 for 2-3 consecutive days with volume >20M shares/day

- ✅ Q3 earnings (Feb 4) showed strong results justifying breakout

- ✅ Technical indicators (RSI, MACD) confirm bullish momentum

- ✅ No negative news on first-party chip or customer relationships

- ⏰ Plan to close position if stock falls back below $118 (failed breakout)

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced

Probability of profit: ~35% (requires multiple bullish catalysts to align)

Alternative aggressive play: If you believe in long-term bull thesis but want better entry, consider selling cash-secured puts at $100-105 strikes for March/April expiration. Collect premium while waiting to get "paid to buy" ARM at 10-15% discount to current price.

⚠️ Risk Factors

Don't get blindsided by these potential landmines:

-

🏭 First-party chip execution risk: Becoming a chipmaker represents ARM's biggest strategic shift ever. Contradicts the "Switzerland" neutral IP model that enabled ecosystem success. ANY delays, technical issues, or weak customer adoption would be catastrophic for thesis. Manufacturing chips requires different expertise than designing IP - not ARM's core competency. Success not guaranteed despite hype.

-

💔 Customer conflict spiral: Qualcomm, MediaTek, Samsung, and others have built empires on ARM architecture. If they perceive ARM as competitor rather than neutral supplier, they could reduce engagement or explore alternatives (RISC-V, custom architectures). Licensing revenue (56% growth in Q2) could decelerate rapidly if customer relationships sour. This is existential risk that market may be underestimating.

-

🇨🇳 RISC-V and China defection: Chinese government actively promoting RISC-V as strategic alternative to ARM. With China representing 19% of revenue and only 7.5% growth, competitive pressure already visible. RISC-V is open-source and royalty-free - powerful value proposition for cost-sensitive markets. If China market share drops from 19% to 10-12%, removes billions in revenue opportunity.

-

🎯 50% market share target wildly optimistic: ARM targets 50% data center CPU share by end of 2025, but analysts expect only 20-23%. x86 ecosystem advantages (software compatibility, decades of enterprise relationships) remain formidable. Missing this target by 30+ percentage points would damage credibility and investor confidence significantly.

-

📉 Goldman Sachs $120 target may be optimistic: Goldman downgraded to Sell with $120 price target citing "limited AI cycle leverage vs direct hardware plays". With stock at $111.80, even Goldman's bearish case implies limited downside. BUT some analysts see intrinsic value closer to $70-80 if execution disappoints. Valuation at 48-58x forward P/E still elevated for a company facing major execution risks.

-

🏦 SoftBank margin loan overhang: Parent SoftBank has $8.5B margin loan against ARM shares with capacity for another $11.5B. SoftBank's $22.5B OpenAI commitment by year-end creates potential forced ARM selling if funding falls short. This creates unpredictable technical selling pressure unrelated to fundamentals. Major shareholder liquidation risk.

-

📊 Q3 earnings binary event (Feb 4): Results in 35 days could move stock 10-15% either direction. Consensus $1.225B revenue, $0.41 EPS - in line with run-rate but needs beat to maintain confidence. Any guidance disappointment or negative first-party chip commentary would trigger selloff. Conversely, strong results with raised guidance could break stock above $120 resistance.

-

💰 Margin compression from chip business: Pure IP licensing carries 50%+ gross margins. Manufacturing chips (even fabless) typically generates 35-45% margins due to costs. As chip revenue scales, overall margins could compress to 38-40% range, disappointing investors expecting margin expansion. This mix shift risk not fully appreciated by market.

-

🎢 AMD/Intel/NVIDIA competitive dynamics: ARM isn't operating in vacuum. AMD gaining x86 data center share rapidly (targeting 40% by 2026), Intel fighting to regain ground, NVIDIA Grace CPUs with ARM cores competing directly. Success of competitors could limit ARM's expansion opportunity even if execution solid.

-

😰 Already down 39% from 52-week highs: Stock peaked at $183.16, now $111.53 - massive correction already occurred. But this doesn't mean bottom is in. Further drawdown to $95-100 or lower entirely possible if catalysts disappoint. Catching falling knife risk for new longs.

-

🐋 Institutional put buyer knows something: $4M bet on downside protection through Jan 2027 with Z-score 36.15 (EXTREMELY UNUSUAL) signals sophisticated player is WORRIED. When funds managing hundreds of millions spend $4M on insurance at in-the-money strikes rather than staying fully long, it's major caution flag. They may have information or analysis retail investors lack.

-

📈 Gamma ceiling at $120 creates mechanical resistance: Massive 13.74B call gamma at $120 strike means market makers will systematically SELL into rallies approaching that level to hedge exposure. Makes breakout above $120 difficult without sustained institutional buying. Current price $111.53 sitting $8 below this ceiling - breakout requires real catalyst, not just momentum.

🎯 The Bottom Line

Real talk: Someone just spent $4 MILLION on long-term ARM downside protection with the stock already down 39% from highs. This isn't a short-term earnings hedge - this is 381-day insurance extending through the entirety of ARM's risky strategic transformation from pure IP licensor to chipmaker.

What this trade tells us:

- 🎯 Sophisticated player expects sustained uncertainty through 2026 - not a quick resolution

- 💰 They're worried enough about $111.80 → $100 (or lower) scenario to pay $26.35/share for protection (23.6% of stock price!)

- ⚖️ The $120 strike ABOVE current price shows they're protecting against stock NOT breaking out sustainably, plus insurance if it falls significantly

- 📊 Timing captures ALL major catalysts: Q3 earnings (Feb 4), Q4 earnings (May 6), first-party chip launch (mid-2025), data center share assessment (year-end 2025), early 2026 reality check

- ⏰ January 2027 expiration provides maximum flexibility to assess strategic pivot success or failure

This is NOT a "sell everything" signal - it's a "meaningful downside risk exists over next 12 months" signal.

If you own ARM:

- ✅ Consider trimming 30-50% at $111-115 levels to reduce concentration risk during uncertain period

- 📊 If holding through catalysts, set MENTAL STOP at $105 (below major gamma support) to protect capital

- ⏰ Don't marry the position - ARM's strategic shift is genuinely risky and could go either way

- 🎯 If first-party chip succeeds AND stock breaks $125, could re-enter trimmed shares with confirmation

- 🛡️ Consider buying 1-2 long-dated protective puts per 100 shares if holding concentrated position (copy trade structure)

If you're watching from sidelines:

- ⏰ February 4, 2026 Q3 earnings is first major litmus test - DO NOT enter before seeing results

- 🎯 Best entry scenarios: (1) Stock consolidates to $100-105 with supportive catalysts, or (2) Breaks cleanly above $125 with volume confirming first-party chip success

- 📈 Looking for confirmation of: Data center royalty acceleration, first-party chip customer wins, 25-30% market share progress, margin stability, China revenue resilience

- 🚀 Longer-term (12-18 months), if ARM executes flawlessly, $150-170 achievable - but that's big "if"

- ⚠️ Current setup offers poor risk/reward - either wait for lower entry or bullish breakout confirmation

If you're bearish:

- 🎯 Don't short stock outright - borrow costs likely high and timing uncertain

- 📊 Post-Q3 earnings put spreads ($110/$100 for June expiration) offer defined-risk approach after IV crush

- ⚠️ Support at $110 (13.16B gamma), then $105 (9.00B gamma), critical floor $100 (6.23B gamma)

- 📉 Watch for break below $105 - that's trigger for potential cascade to $95-100 range

- ⏰ Be patient - let catalysts play out rather than fighting potential dead-cat bounces

Mark your calendar - Key dates:

- 📅 January 2, 2026 (Friday) - Weekly OPEX (±2% implied move)

- 📅 January 16, 2026 - Monthly OPEX (±6% implied move window)

- 📅 February 4, 2026 (Wednesday after close) - Q3 FY2026 earnings report (CRITICAL!)

- 📅 March 20, 2026 - Quarterly triple witch (±16% implied move)

- 📅 May 6, 2026 - Q4 FY2026 and full-year earnings (FY2027 guidance)

- 📅 Mid-2025 (May-July) - First-party data center chip launch expected

- 📅 End of 2025 - Assessment of 50% data center market share target

- 📅 January 15, 2027 - Expiration of this $4M put trade

Final verdict: ARM's transformation from pure IP licensor to chipmaker is genuinely uncertain - could unlock $150+ upside if executed perfectly, or crater to $75-90 if it backfires. The $4M institutional put position with Z-score 36.15 (EXTREMELY UNUSUAL) signals smart money sees meaningful downside risk over next 12 months. With stock at $111.80 after 39% decline from highs, we're at an inflection point - not clearly oversold bargain, not clearly broken story.

Current risk/reward favors patience. Wait for Q3 earnings and first-party chip details before committing significant capital. If you must be involved, use small position sizes and defined-risk strategies. This is a "show me" situation for ARM - let them prove the strategic pivot works rather than betting on hope.

The AI and data center growth opportunity is real, but execution risk is equally real. Protect your capital. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-score 36.15 and "EXTREMELY UNUSUAL" classification reflects this specific trade's size relative to recent ARM history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Strategic pivots create genuine business risk with potential for significant downside. The put buyer may have complex portfolio needs not applicable to retail traders.

About ARM Holdings: ARM Holdings is the IP owner and developer of the ARM architecture used in 99% of the world's smartphone CPU cores, operating as a licensing firm charging royalties per chip shipped while expanding into first-party chip manufacturing for data centers, with a market cap of $117.25 billion.