🔬 ASML: $8.5M Deep ITM Call Exit — Smart Money Unwinding a Stock-Replacement Position!

📅 March 13, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just closed out $8.5 MILLION worth of deep in-the-money ASML calls at 14:35 today — two massive trades selling the $310 and $410 strike calls expiring next Friday, March 20. With ASML trading at $1,349.61, these strikes are more than $900 and $1,000 below the stock price — this is not a speculative bet getting cut, it's an institution unwinding a stock-replacement position they've been holding since ASML was trading near $310–$410. Translation: this is a whale cashing out a multi-year winner, not a bear making a move. 👀

📊 Company Overview

ASML Holding NV is one of the most irreplaceable companies on the planet — and that's not hype:

- Market Cap: ~$540 Billion

- Industry: Semiconductor Capital Equipment (Photolithography Systems)

- Current Price: ~$1,349.61

- What they do: ASML is the world's sole manufacturer of EUV (Extreme Ultraviolet) lithography machines — the equipment that every cutting-edge chipmaker (TSMC, Intel, Samsung) absolutely must use to build the most advanced semiconductors. Without ASML's machines, there are no NVDA H200s, no Apple M4 chips, no modern AI processors. Period.

- 2026 Revenue Guidance: €34–39 billion with a €38.8 billion order backlog

- Monopoly status: No other company in the world makes EUV machines. It took ASML 30 years and billions in R&D to build this. There is no competitor coming.

Think of ASML as the company that makes the printing presses for all the world's chips. You can't print chips without their machines. That's why the stock rallied 30%+ in January 2026 alone.

💰 The Option Flow Breakdown

The Tape (March 13, 2026 @ 14:35:58):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 14:35:58 | ASML | MID | SELL | CALL $310 | 2026-03-20 | $4.5M | $310 | 43 | 0 | 43 | $1,349.61 | $1,040.38 |

| 14:35:58 | ASML | MID | SELL | CALL $410 | 2026-03-20 | $4.0M | $410 | 43 | 0 | 43 | $1,349.61 | $940.45 |

Total Premium: ~$8.5M | Contracts: 43 each | OI on both: 0

🤓 What This Actually Means — The Stock-Replacement Strategy Explained

This is not a normal options trade. Let me break it down in plain English because this one is genuinely unusual. 👇

What is a stock-replacement strategy?

Instead of buying 100 shares of a $400 stock (costing $40,000), a sophisticated investor might instead buy a DEEP in-the-money call option with a $10 strike price that trades almost exactly like owning the shares — but ties up far less capital. This is called a synthetic stock position or stock-replacement strategy.

Back when ASML was trading at $310–$410 (a couple of years ago), an institution likely did exactly this: they bought these deeply in-the-money $310 and $410 strike calls as a cheaper way to control ASML shares, effectively owning ASML synthetically. The calls had a delta of ~1.0, meaning they moved dollar-for-dollar with the stock.

Fast forward to today: ASML is now at $1,349.61. Those calls are worth $1,040.38 and $940.45 per share respectively — almost entirely intrinsic value (pure profit). There's virtually zero "optionality premium" left. The calls are so deep in the money that they're just acting like stock.

What does SELL mean here?

When these trades show as SELL with OI = 0, this means the institution is closing a long position they already held — also called "selling to close" (STC). They're not opening a new short position — they're cashing out their old long.

-

💡 Translation for regular folks: Imagine you bought a lottery ticket years ago that said "you can buy ASML at $310 anytime until March 20, 2026." Now ASML is $1,350. Your ticket is worth $1,040 of pure profit. You're simply selling that ticket back before it expires. That's what happened here — times 43 contracts ($4.3 million worth of stock exposure each).

-

📊 Why 43 contracts? Each contract controls 100 shares. 43 contracts × 100 shares × $1,040.38 = $4.5M for the $310s. Small contract count but massive per-contract value — classic institutional portfolio management, not a retail YOLO trade.

-

⚠️ OI = 0 confirms this is a close: Zero open interest means these specific contracts weren't already sitting in the market. The institution held them in their own account. Now they're selling them back to the market (or directly to a dealer).

Why now? With only 7 days until March 20 expiration, these calls are racing toward worthlessness in terms of time value. The institution is simply cleaning house — converting their synthetic ASML position back to cash (or back to actual stock) before the contracts expire. This is textbook portfolio management. Nothing bearish about ASML here.

📈 Technical Setup / Chart Check-Up

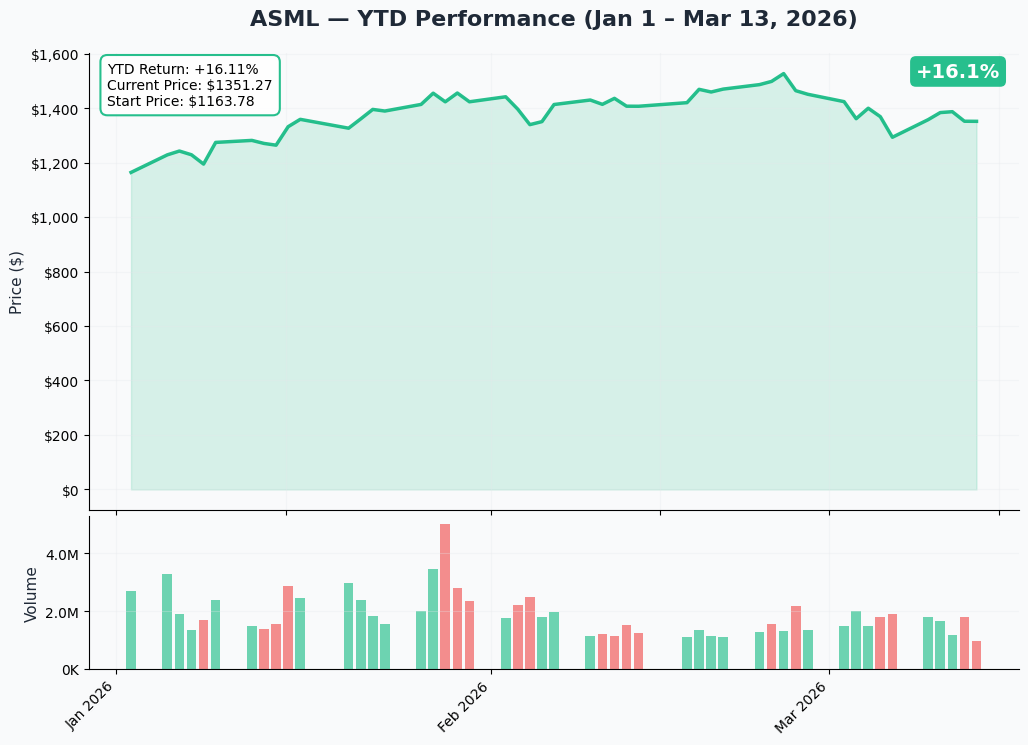

YTD Performance Chart

ASML has been on an absolute tear. The stock surged 30%+ in January 2026 following blowout Q4 2025 earnings with record bookings of €13.2 billion — 144% sequentially. After that rocket launch, shares have pulled back modestly from the January highs, with the stock sitting near $1,349 today following a recent 5.3% pullback triggered by China rare earth export control concerns (more on that in Catalysts).

Key observations from the chart:

- 🚀 Explosive January breakout: The January move was powered by record EUV bookings and multiple analyst upgrades, with Aletheia Capital flipping from Sell to Buy with a $1,500 target

- 📉 Healthy pullback in progress: After the January spike, the current ~$1,350 level represents a natural consolidation — still up massively on the year

- 📊 Still outperforming peers: AI capex super-cycle demand from TSMC, Samsung, and SK Hynix keeps the fundamental demand story intact

- ⚠️ China overhang creating near-term pressure: Rare earth restrictions announced March 3 added uncertainty that is holding shares below recent highs

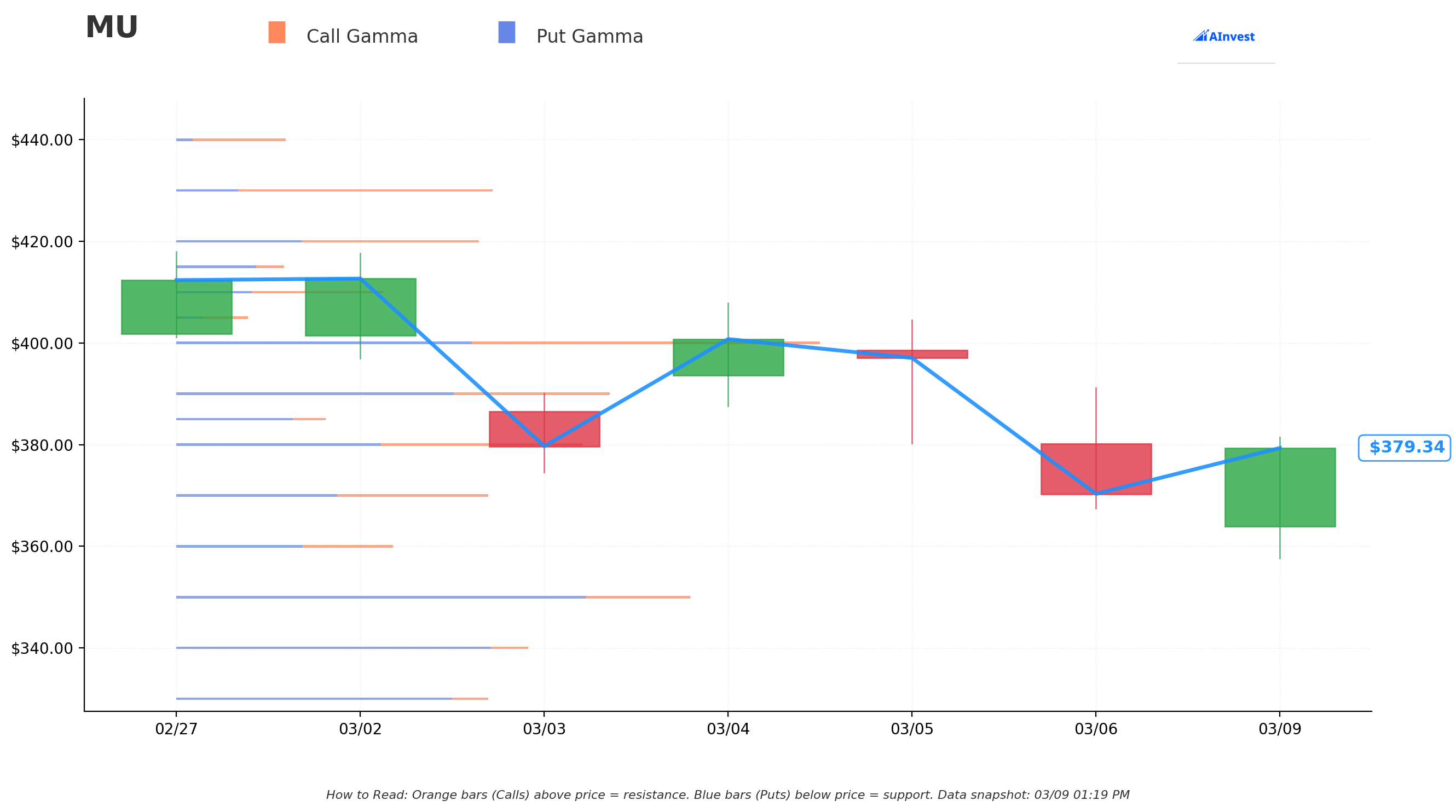

Gamma-Based Support & Resistance Analysis

Current Price: $1,349.61 | Net GEX Bias: Bearish

Reading the gamma exposure map, here's where the real battleground sits for ASML:

🔵 Support Levels (Put Gamma Below Price):

- $1,350 — Immediate support with 3.56B total gamma exposure (strongest nearby floor — note: price is sitting right at this level as of this writing)

- $1,345 — Secondary cushion at 0.64B gamma (thin, would likely not hold a strong sell-off alone)

- $1,340 — Decent floor at 1.45B gamma with net put gamma (-0.88B net), dealers will defend this level

- $1,335 — Secondary support at 0.62B gamma

- $1,300 — Major structural floor at 0.87B gamma (~3.8% below current price) — this is the key support level to watch

- $1,220 — Deep support at 0.85B gamma (~9.7% below current) — the disaster floor

🟠 Resistance Levels (Call Gamma Above Price):

- $1,355 — Immediate ceiling at 1.18B gamma, just 0.3% overhead — stock needs to break through this first

- $1,360 — Key resistance at 1.71B gamma (strongest nearby call gamma level, 0.68% above price) — this is the near-term target to watch

- $1,400 — Major overhead resistance at 1.69B gamma (~3.6% above current) — would signal a resumption of the uptrend

- $1,500 — Extended bull case target at 0.71B gamma (~11% away) — analysts see this level as achievable by year-end

What this means for traders:

ASML is essentially pinned at the $1,350 level — sitting right on top of its strongest immediate support. The net GEX is bearish (total put gamma 16.24B vs call gamma 12.09B), meaning market makers' positioning provides more gravitational pull to the downside right now.

The critical number to watch is $1,300. If ASML loses the $1,340–$1,350 support zone with conviction, the next meaningful gamma floor isn't until $1,300. On the upside, getting through $1,360 (the strongest single resistance level above) would be a positive signal for a return toward the January highs.

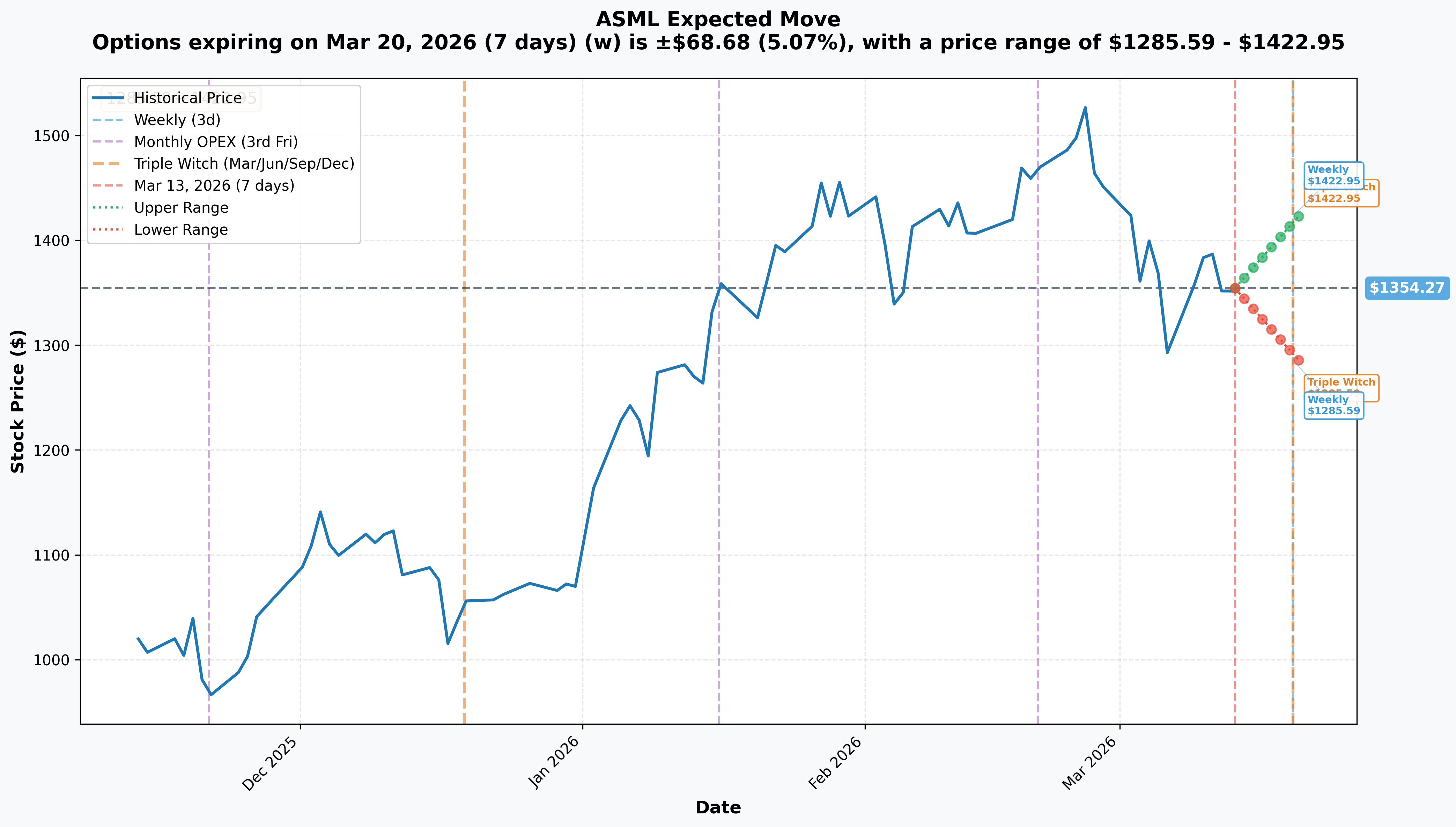

Implied Move Analysis

Options market pricing for the March 20 expiration (7 days away):

| Expiration | Days | Implied Move | Upper Range | Lower Range |

|---|---|---|---|---|

| 📅 2026-03-20 (Weekly / Monthly OPEX / Triple Witch) | 7 days | ±$68.68 (±5.07%) | $1,422.95 | $1,285.59 |

Translation for regular folks:

Options traders are pricing in a 5.07% swing ($68.68) in just the next 7 days for ASML. That's a wide window for a $540B mega-cap — this is NOT a boring blue-chip earnings scenario. The market is effectively saying:

- 📈 Bull case by March 20: ASML hits ~$1,423 — would represent recovery toward January highs

- 📉 Bear case by March 20: ASML drops to ~$1,286 — would confirm a breakdown below key support

- ⚡ Why is the implied move so large? Because March 20 is a Triple Witch expiration (options, futures, and index options all expire simultaneously), AND it falls right in the window of NVIDIA's GTC 2026 conference (March 16–19) — a massive AI hardware event that directly affects ASML's EUV demand narrative. The market is pricing in meaningful event risk over the next week.

Key insight: The implied move range perfectly brackets the gamma levels. The upper bound of $1,423 aligns with the $1,400 call gamma zone, while the lower bound of $1,286 sits near the $1,300 support level. This is the options market doing its job — telling you where the biggest positioning battles are.

🎪 Catalysts

🔥 Upcoming Catalysts (Next 30 Days — CRITICAL WINDOW)

NVIDIA GTC 2026 Conference — March 16–19 (3 DAYS AWAY!) 🤖

This is the elephant in the room for ASML right now. NVIDIA's GPU Technology Conference is where Jensen Huang will reveal the latest AI chip roadmap — including GB300 Blackwell Ultra and potentially Rubin architecture details. Why does this matter for ASML?

- 🔬 ASML machines make NVIDIA chips possible: Every next-gen NVIDIA GPU requires TSMC's most advanced nodes, which require ASML's EUV (and increasingly High-NA EUV) lithography tools

- 📦 More AI chip demand = more ASML orders: If NVIDIA announces aggressive production ramp plans or new chip timelines, TSMC will accelerate its capex — which flows directly to ASML equipment orders

- 📈 HBM4 memory in GB300: SK Hynix's HBM4 production for GB300 requires expanded EUV capacity — another direct ASML tailwind

- 🎯 Market sentiment driver: GTC has historically moved semiconductor equipment stocks meaningfully in the days following the keynote

This is a binary event for near-term ASML price action. Strong NVIDIA AI chip roadmap confirmation = ASML demand narrative strengthened. Disappointment = potential further pullback.

March 20 Triple Witch Options Expiration 📅

The same date as these two trades' expiration is also a major market structure event. Massive open interest rolls off, which can create above-average volatility in both directions. Gamma exposure shifts dramatically post-expiration, removing some of the current price magnetism at $1,350.

Q1 2026 Earnings — Expected Mid-April 2026 📊

The first quarterly read on ASML's 2026 guidance execution. Key things to watch:

- Revenue tracking toward €7.5–8.5B range (Q1 seasonality expected)

- Bookings: Will Q1 come anywhere close to Q4's record €13.2B? Even €7B+ would be healthy

- High-NA EUV shipment commentary — this is the €350M+ per unit machine that will drive the next revenue step-change

- Gross margin trajectory as High-NA EUV (initially lower margin) begins scaling

✅ Past Catalysts (Already Happened — Baked Into Price)

Record Q4 2025 Earnings — January 2026 Blowout

ASML's Q4 2025 was genuinely historic:

- Net Sales: ~€9.7 billion

- Net Bookings: €13.2 billion — record quarterly figure, up 144% sequentially

- EUV Orders alone: €7.4 billion

- Year-end backlog: €38.8 billion (~$45B), which alone nearly covers the low-end of full-year 2026 guidance

- Result: Stock ripped 30%+ in January 2026, accompanied by a wave of analyst upgrades

Analyst Upgrades — Price Targets Sharply Higher

- Citi raised target to €1,200, citing AI demand driving estimate revisions

- Cantor Fitzgerald target raised to €1,300, maintained Overweight

- Aletheia Capital (Warren Lau): Upgraded from Sell to Buy, target $1,500

- Average 12-analyst target: $1,625.24 — implying ~20% upside from here

- UBS forecasts 23% revenue growth in 2026, 14% in 2027

2026 Revenue Guidance Raised

ASML raised full-year 2026 guidance to €34–39 billion with gross margins of 51–53%. The €38.8B backlog provides extraordinary forward revenue visibility — the order book is already essentially full.

China Rare Earth Export Controls — March 3, 2026 ⚠️

Beijing restricted exports of rare earth elements critical for manufacturing lithography machines, effective March 3. This spooked investors because ASML relies on specialty materials in its machine manufacturing process. This news, combined with ongoing EUV export restrictions to China, triggered the recent 5.3% pullback from January highs.

China already represents a declining revenue share as DUV export restrictions have tightened — but total elimination of Chinese revenue (historically ~30% of sales) remains a tail risk.

🎲 Price Targets & Probabilities

Using the gamma map, implied move data, analyst targets, and the upcoming GTC/OPEX catalysts to frame the scenarios over the next 30 days:

📈 Bull Case (35% probability)

Target: $1,400–$1,423

How we get there:

- 🤖 NVIDIA GTC 2026 (March 16–19) delivers a blowout roadmap with aggressive GB300/Rubin production timelines — TSMC capex accelerates, ASML order narrative strengthened

- 📊 No escalation in China rare earth restrictions — the concern fades without additional government action

- 📅 Post-Triple Witch gamma shift (March 20) removes downward price pressure at $1,350, allowing a relief rally

- 🏗️ TSMC's N2 entering high-volume manufacturing in H1 2026 gets positive production commentary, confirming ASML equipment demand

- 💰 Gamma resistance at $1,360 gets cleared, opening path to the implied move upper target of $1,423

- 📈 Average analyst target of $1,625 provides long-term gravitational pull toward higher levels

Key metrics needed: $1,360 gamma resistance broken with volume, no new China restriction escalation, positive NVIDIA AI capex commentary at GTC

Probability note: The 38.8B backlog provides a strong fundamental floor, but macro/China headwinds limit short-term probability of a quick sprint to new highs.

🎯 Base Case (45% probability)

Target: $1,285–$1,360 (Range-Bound Consolidation)

Most likely scenario:

- ✅ GTC 2026 provides solid AI roadmap updates — no massive surprise, no disappointment

- ⚖️ China rare earth situation remains as-is — concerning but not escalating

- 📊 ASML trades in a choppy range between the $1,340 gamma support and $1,360 resistance

- 🔄 Triple Witch expiration on March 20 creates some short-term volatility but doesn't establish a new direction

- 📅 Market waits for Q1 2026 earnings in mid-April for the next meaningful catalyst

- 🌍 Options market's ±$68.68 implied move mostly resolves without hitting either extreme

Why 45%: ASML is in a fundamentally strong position but faces near-term crosswinds (China risk, post-rally consolidation, no immediate earnings catalyst for 4+ weeks). The gamma setup with strong $1,350 support and nearby $1,360 resistance screams sideways for the near term.

📉 Bear Case (20% probability)

Target: $1,220–$1,285 (Test the Deep Support)

What could go wrong:

- 😰 China escalates rare earth restrictions further — ASML issues supply chain warning, stock gaps down

- 🤖 NVIDIA GTC disappoints AI investors — chip production timeline delays, fewer EUV orders implied

- 📉 Broader semiconductor sector sell-off (macro fears, export control escalation) drags ASML below $1,340 support

- 💸 Post-Triple Witch gamma unwind accelerates selling as the $1,350 gamma pin expires

- 🔨 Break below $1,340 support triggers momentum selling toward $1,300 (major gamma floor) and potentially $1,285 (implied move lower bound)

Critical support levels to watch:

- 🛡️ $1,350 — Current pin zone (strongest support, now being tested)

- 🛡️ $1,340 — Secondary defense (1.45B total gamma, net put gamma dominant)

- 🛡️ $1,300 — Major structural floor, 3.8% below current

- 🛡️ $1,220 — Extended support zone, 9.7% below — would only reach here on significant negative news

Note: The bear case does NOT make ASML a bad company — it's a correction within a long-term secular growth story. Average analyst target of $1,625 with a high target of $1,911 suggests multi-year upside remains intact.

💡 Trading Ideas

🛡️ Conservative: "The Patience Play" — Wait for Post-OPEX Entry

Play: Watch the March 20 Triple Witch expiration from the sidelines, then look for an entry in the $1,300–$1,340 zone if the stock dips

Why this works:

- ⏰ Triple Witch (March 20) + GTC 2026 (March 16–19) creates near-term binary event risk — implied move is ±5%, too much uncertainty to chase

- 📊 Options are relatively expensive with this much event risk priced in — premiums will be cheaper next week after OPEX

- 🎯 If ASML pulls back to $1,300–$1,340 post-OPEX, you're getting a 3–8% discount with major gamma support beneath you AND the next catalyst (Q1 earnings mid-April) as the next potential re-rating event

- 📈 With analysts averaging $1,625 price target, even a conservative entry at $1,320 gives you 23% upside to target

- 🐋 The deep ITM call unwind today suggests institutional rebalancing is happening — wait for that to fully digest

Action plan:

- 👀 Watch GTC 2026 keynote (March 16–19) closely for AI capex commentary

- 📅 Let March 20 OPEX pass

- 🎯 Look for stock entry at $1,300–$1,340 with a stop below $1,220

- ✅ Confirm: no new China rare earth escalation before pulling the trigger

Risk level: Low (waiting for better entry, no options exposure) | Skill level: Beginner-friendly

⚖️ Balanced: "The April Earnings Setup" — Bull Call Spread

Play: After March 20 OPEX, buy a bull call spread targeting recovery toward analyst targets ahead of Q1 earnings in mid-April

Structure: Buy ASML April $1,360 Call / Sell ASML April $1,450 Call (after OPEX, when IV cools)

Why this works:

- 🎯 The $1,360 strike is right at the key gamma resistance — if ASML breaks through it with any momentum from GTC catalysts, this spread is in the money

- 💸 Post-OPEX IV crush will make the spread cheaper — wait until after March 20 to enter

- 📅 The April expiration captures Q1 2026 earnings (~mid-April) — the next fundamental re-rating event

- 📊 Defined risk: maximum loss is the debit paid (capped downside), maximum gain if ASML returns toward $1,400–$1,450 zone

- 🏗️ TSMC N2 HVM entry in H1 2026 and HBM4 demand narrative provide fundamental tailwinds for this timeframe

- 💰 Estimated cost: ~$25–35 per spread (rough estimate, verify post-OPEX after IV normalizes)

Position sizing: Risk only 2–4% of your portfolio (this is a directional bet with earnings binary risk)

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

🚀 Aggressive: "The GTC Gamma Squeeze" — Weekly Call Before March 20

Play: Small lottery-ticket call position betting GTC 2026 NVIDIA keynote ignites AI semi momentum this week

Structure: Buy ASML March 20 $1,380 or $1,400 Call — cheap weekly OTM call expiring on Triple Witch

Why this could work:

- 💥 GTC is a known catalyst for the entire AI semiconductor stack — ASML moves when NVIDIA announces big things

- ⚡ Options market pricing ±5.07% move — breakout to $1,423 (the upper implied move) is within the priced-in window

- 🎰 With 7 days to expiration, OTM calls are cheap (high leverage on a big move) — cost might be $5–15 per contract

- 🚀 If NVIDIA announces aggressive Blackwell/Rubin timelines at GTC, ASML could gap up $50–100 on TSMC capex excitement

Why this is DANGEROUS:

- ⚠️ 7 days to expiration — theta burns fast, every day of sideways action destroys premium

- 😰 If GTC underwhelms OR China news spooks the market further, these expire worthless

- 📉 The net GEX bias is bearish — gamma headwinds favor downside, not upside

- 💸 OTM calls with a week left are pure volatility plays — you could lose 100% easily

CRITICAL WARNING: Only consider this if you:

- ✅ Can afford to lose the entire premium (real probability!)

- ✅ Have traded short-dated event plays before and understand time decay

- ✅ Plan to sell within 24–48 hours of GTC keynote (do NOT hold into expiration)

- ✅ Keep position size to 1% of portfolio maximum

Risk level: EXTREME (can lose 100%) | Skill level: Advanced only

⚠️ Risk Factors

Don't sleep on these potential landmines:

-

🇨🇳 China rare earth supply chain risk — the #1 near-term threat: Beijing's rare earth export restrictions effective March 3 represent a real supply chain headache. ASML uses specialty materials in lithography machine manufacturing. If China escalates these restrictions further, ASML faces cost increases and potential production bottlenecks. This was the primary trigger for the recent 5.3% pullback and is unresolved.

-

🌏 China revenue concentration risk: China historically represented ~30% of ASML's revenue. Export control restrictions have been tightening, and ASML cannot sell its most advanced EUV systems to China at all. If China revenue falls faster than expected while non-China demand doesn't fully compensate, 2026 guidance could be at risk. This would be a significant negative re-rating catalyst.

-

🤖 GTC 2026 binary event risk (March 16–19): NVIDIA's conference in 3 days is a double-edged sword. Strong AI chip roadmap = ASML demand narrative strengthened. Any disappointment, production delays, or NVIDIA-specific concerns could drag the entire AI semi ecosystem lower. ASML doesn't report until mid-April, so GTC is the next major sentiment catalyst.

-

📅 Triple Witch gamma unwind (March 20): The expiration of massive open interest positions on March 20 removes the current gamma "pin" at $1,350. Post-OPEX, the gamma support that's been holding the stock near current levels evaporates. This can amplify moves in either direction — don't assume the $1,350 level remains sticky after Friday.

-

🏗️ High-NA EUV ramp execution risk: ASML's next-gen EXE:5000 High-NA EUV machine (€350M+ per unit) is expected to begin volume shipments in 2H 2026. These machines initially carry lower gross margins as manufacturing scales. If the ramp is slower than expected — whether from yield issues, customer adoption delays, or Intel 18A problems — the gross margin trajectory and the thesis for a revenue step-change could be pushed out.

-

💰 Valuation at $540B market cap: At current levels, ASML trades at a premium multiple reflecting the AI capex super-cycle narrative. If semiconductor capital spending pauses (historically cycles run 18–24 months), even a monopoly equipment maker isn't immune to a multiple compression event. ASML hit a 52-week low of ~$630 before the current rally — that's how far premium multiples can compress in a bad cycle.

-

🏛️ Semiconductor capex cycle sensitivity: ASML's revenue is ultimately driven by how much TSMC, Samsung, Intel, and the memory companies spend on new fabs. If AI capex expectations get revised down (hyperscaler spending cuts, NVIDIA demand shock), ASML's order book could stall meaningfully in late 2026 or 2027.

🎯 The Bottom Line

Real talk: What happened today is NOT a bearish signal on ASML. This is an institution closing out a multi-year synthetic stock position — they bought deep ITM calls when ASML was trading at $310–$410 as a capital-efficient way to own the stock, rode it to $1,349, and are now cashing out $8.5M before next Friday's expiration. It's a winner taking chips off the table, not a whale betting against ASML.

What this trade tells us:

- 💰 Someone entered ASML deep ITM calls back when the stock was in the $300–$400 range — they've made 3–4x returns on those positions

- 🎯 The clean execution at mid-price (no urgency, no panic) confirms this is orderly position management, not a distress trade

- ⚠️ OI = 0 on both tells us these were privately held contracts — not layered on the existing order book

- 📊 43 contracts each is small by institutional standards — this could be one sleeve of a much larger ASML position still intact

If you own ASML:

- ✅ Hold your conviction — the fundamental story (EUV monopoly, €38.8B backlog, AI capex super-cycle) is intact

- 📅 Watch GTC 2026 (March 16–19) for NVIDIA AI roadmap — this is your near-term price catalyst

- 🎯 If ASML holds $1,340–$1,350 through OPEX next Friday, that's a healthy base for a Q2 run toward $1,400+

- ⚠️ Keep an eye on China rare earth developments — that's the one wildcard that could pressure shares meaningfully

- 📊 With average analyst target of $1,625 and a high target of $1,911, there's plenty of runway if the AI capex thesis continues executing

If you're watching from the sidelines:

- ⏰ March 20 OPEX is your entry opportunity window — let the gamma pin expire, then look for dips

- 🎯 $1,300–$1,340 post-OPEX would be a high-quality entry zone with gamma support and a 20%+ analyst upside target

- 📅 Mark mid-April on your calendar for Q1 2026 earnings — the next hard fundamental catalyst

- 🏗️ Longer-term (6–12 months): High-NA EUV volume ramp in 2H 2026 is the next potential earnings step-change

If you're bearish:

- 📉 Watch $1,340 support carefully — a close below there opens the $1,300 and $1,285 targets

- 🇨🇳 China rare earth escalation is your most credible catalyst for a deeper pullback

- 🛡️ The €38.8B backlog and EUV monopoly make ASML incredibly hard to be short for more than a trade — fundamental gravity eventually wins

Mark your calendar — Key dates:

- 📅 March 16–19 — NVIDIA GTC 2026 conference (huge AI hardware catalyst)

- 📅 March 20 — ASML options expiration / Triple Witch (today's trade expires, gamma pin lifts)

- 📅 Mid-April 2026 — Q1 2026 Earnings (next hard fundamental re-rating event)

- 📅 H2 2026 — High-NA EUV volume shipments begin (the big multi-year revenue step-change)

- 📅 2026 Full Year — €34–39B revenue guidance execution — the overarching storyline

Here's the deal: ASML is the picks-and-shovels company of the AI chip revolution. You can't build AI chips without their machines. You can't build their machines anywhere else. The €38.8B backlog means customers have already committed — this revenue is coming. Today's trade is a winner cashing out a long-held position, not an institution abandoning ship. The noise is China rare earth risk and near-term OPEX volatility. The signal is a monopoly company with a record backlog in the middle of a generational AI chip demand cycle, with analysts targeting $1,625–$1,911.

Don't mistake institutional portfolio management for a bearish signal. Play the setup accordingly. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and is not financial advice. Past performance does not guarantee future results. The trades analyzed here represent institutional-level deep in-the-money call closures — these are sophisticated transactions not suitable for direct replication by retail investors. Deep ITM options carry unique risks including assignment risk, liquidity risk, and near-expiration time decay dynamics. The "stock-replacement strategy" concept described is for educational context only. Always conduct your own due diligence and consider consulting a licensed financial advisor before trading. ASML is a Dutch company with ADR-specific risks including currency exposure, foreign regulatory risks, and geopolitical considerations specific to semiconductor equipment export controls.

About ASML Holding NV: ASML Holding N.V. is the world's sole manufacturer of EUV (Extreme Ultraviolet) lithography machines — the essential equipment used by TSMC, Samsung, Intel, and all leading chipmakers to produce the most advanced semiconductors. With a ~$540 billion market cap, €38.8 billion order backlog, and 2026 revenue guidance of €34–39 billion, ASML occupies a unique monopoly position at the center of the global AI chip supply chain.