💊 ASND Massive $1.1M Call Bet - Pharma Bull Betting Big on March Catalyst! 🚀

📅 December 15, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $1.1 MILLION on ASND calls targeting March 2026! This aggressive bull bet bought 500 contracts of the $230 strike calls expiring March 20th at $22.60 per contract - betting on a continued rally from the current $221 level. With ASND up +54% YTD near all-time highs and a critical FDA decision on TransCon CNP expected by November 30, 2025, this trader is positioning for a breakout through year-end earnings and into 2026 product launches.

📊 Company Overview

Ascendis Pharma A/S (ASND) is a Danish biopharmaceutical company revolutionizing rare endocrine disease treatment with its proprietary TransCon technology platform:

- Market Cap: $13.47 Billion

- Industry: Biopharmaceutical (Endocrinology & Oncology focus)

- Current Price: $221.34 (near 52-week high of $220.59)

- Primary Business: Develops long-acting prodrug therapies for rare diseases using TransCon platform; currently commercializing SKYTROFA (pediatric growth hormone deficiency) and YORVIPATH (hypoparathyroidism)

What they do: Ascendis uses its TransCon (transient conjugation) technology to create once-weekly or once-monthly injectable therapies that replace daily medications. Think of it like slow-release medicine - patients get consistent therapeutic levels with far fewer injections. They're targeting billion-dollar revenue opportunities in rare diseases where current treatments require daily pills or shots.

💰 The Option Flow Breakdown

The Tape (December 15, 2025 @ 11:23:45):

| Time | Symbol | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:23:45 | ASND | BUY | CALL $230 | 2025-12-19 | $225K | $230 | 500 | 1,600 | 500 | $221.34 | $4.50 | ASND20251219C230 |

| 11:23:45 | ASND | BUY | CALL $230 | 2026-03-20 | $1.1M | $230 | 500 | 0 | 500 | $221.34 | $22.60 | ASND20260320C230 |

🤓 What This Actually Means

This is a bullish roll forward play with major conviction! Here's the breakdown:

- 🔄 Roll structure: Trader bought the March 2026 $230 calls for $22.60 while simultaneously closing Dec 2025 $230 calls at $4.50

- 💸 Net cost: $1.1M paid for the March calls (this is the bigger bet!)

- ⏰ Extended time horizon: Pushing from 4 days out to 95 days gives time for multiple catalysts to play out

- 🎯 Same strike ($230): Keeping identical $230 strike shows conviction in specific price target

- 📊 Opening new position: 0 open interest in March $230 calls means this trade OPENED the entire position

- 🎪 Catalyst timing: March 20th expiration captures YORVIPATH US launch ramp, potential TransCon CNP approval, Q4 earnings, and MI350 product updates

What's really happening here: This trader likely held the December $230 calls and was sitting on profits (stock near $221, calls worth $4.50). Rather than taking profits before this week's expiration, they're ADDING $1.1M to roll into March - betting that ASND has significantly more upside through Q1 2026. At $22.60 per contract, they're paying substantial premium for time value, suggesting they expect major catalysts to push the stock well above $250 by March.

Unusual Score: The March call purchase is highly unusual - opening 500 contracts with 0 prior open interest in an illiquid option series. The classifier tagged this as "HIGHLY_UNUSUAL" with a Z-score of 2.25 for the December close. This isn't your typical retail flow - someone with serious capital is making a big directional bet.

📈 Technical Setup / Chart Check-Up

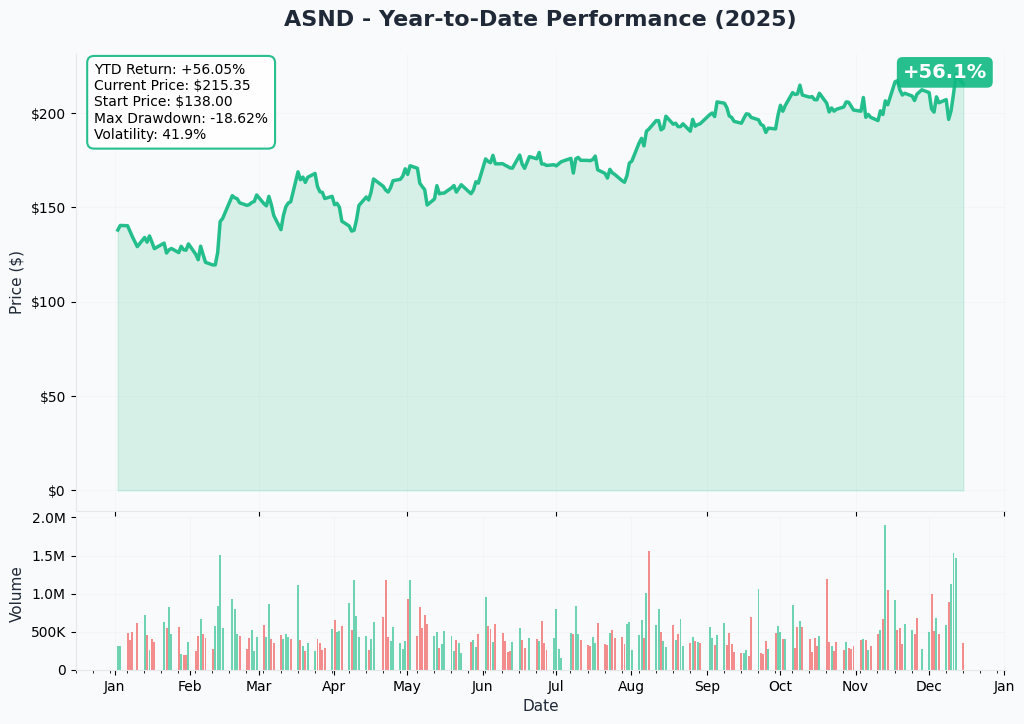

YTD Performance Chart

ASND is absolutely on fire - up +54% YTD from $136.43 at year-start to current $221.34, nearly touching the 52-week high of $220.59. The chart tells a biotech breakout story driven by commercial execution and pipeline catalysts.

Key observations:

- 🚀 Explosive rally: Vertical move from $155 in August to $220+ in December on YORVIPATH FDA approval and Novo Nordisk partnership

- 📈 Breakout confirmed: Smashed through $180 resistance in October, never looked back

- 🎢 High volatility: This isn't a sleepy biotech - massive swings on clinical/regulatory news

- 📊 Volume surge: October-December institutional accumulation on commercial de-risking

- ⚠️ Near ATH: Trading within 1% of all-time high - near-term consolidation likely before next leg

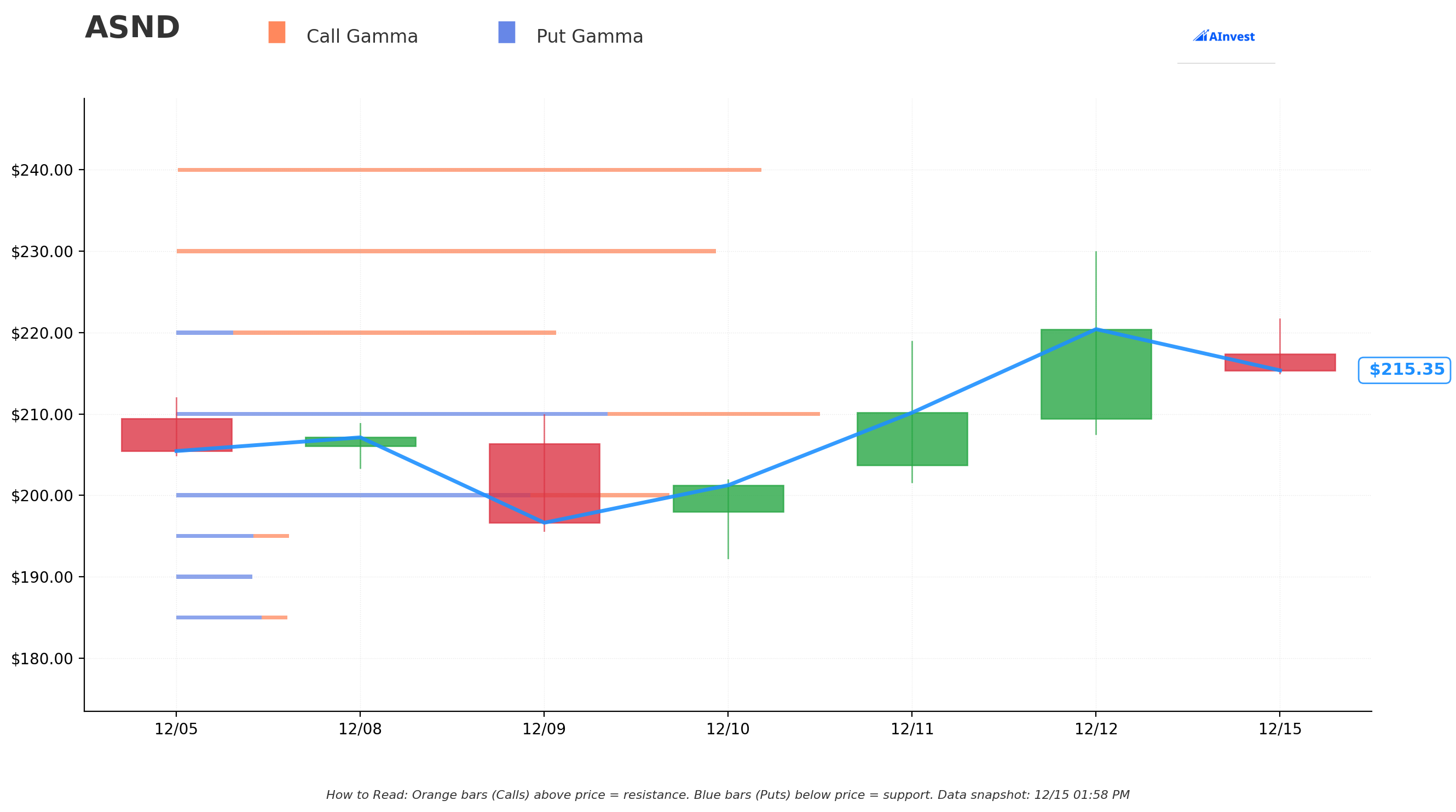

Gamma-Based Support & Resistance Analysis

Current Price: $215.59

The gamma exposure map reveals critical price magnets and barriers governing near-term action:

🔵 Support Levels (Put Gamma Below Price):

- $210 - Immediate support with 0.834B total gamma (strongest nearby floor!) just 2.6% below current price

- $200 - Secondary support at 0.639B gamma (dealers will defend aggressively here)

- $195 - Tertiary support at 0.146B gamma (9.5% below current)

- $190 - Extended floor at 0.105B gamma

- $185 - Deep support zone with 0.144B gamma

- $180 - Disaster floor at 0.017B gamma (previous breakout level)

🟠 Resistance Levels (Call Gamma Above Price):

- $220 - Immediate ceiling with 0.492B gamma (STRONGEST RESISTANCE - just 2% above) where market makers will sell into rallies

- $230 - MAJOR TARGET STRIKE with 0.699B gamma (this is where both trades are struck! Not coincidental) at 6.7% above current price

- $240 - Secondary ceiling at 0.758B gamma (THE HIGHEST LEVEL - 11.3% above current)

- $250 - Extended upside target at 0.496B gamma (16% rally required)

What this means for traders: ASND is sitting in a narrow band between solid $210 support and crushing $220 resistance. The gamma data shows the $230 strike (where our call buyer is positioned) has massive 0.699B call gamma - meaning if the stock can break above $220, momentum could accelerate toward $230 quickly as dealers hedge their short calls by buying stock. The $240 level with 0.758B gamma is THE ultimate ceiling - highest gamma concentration on the board.

Notice anything? The call buyer struck EXACTLY at $230 where there's significant call gamma clustering. They're betting that once ASND breaks $220, dealer hedging flows will propel it to $230+ by March. Smart positioning.

Net GEX Bias: Bullish (3.02B call gamma vs 1.50B put gamma = 2:1 bullish bias) - Overall positioning remains solidly bullish with call skew dominating the options complex.

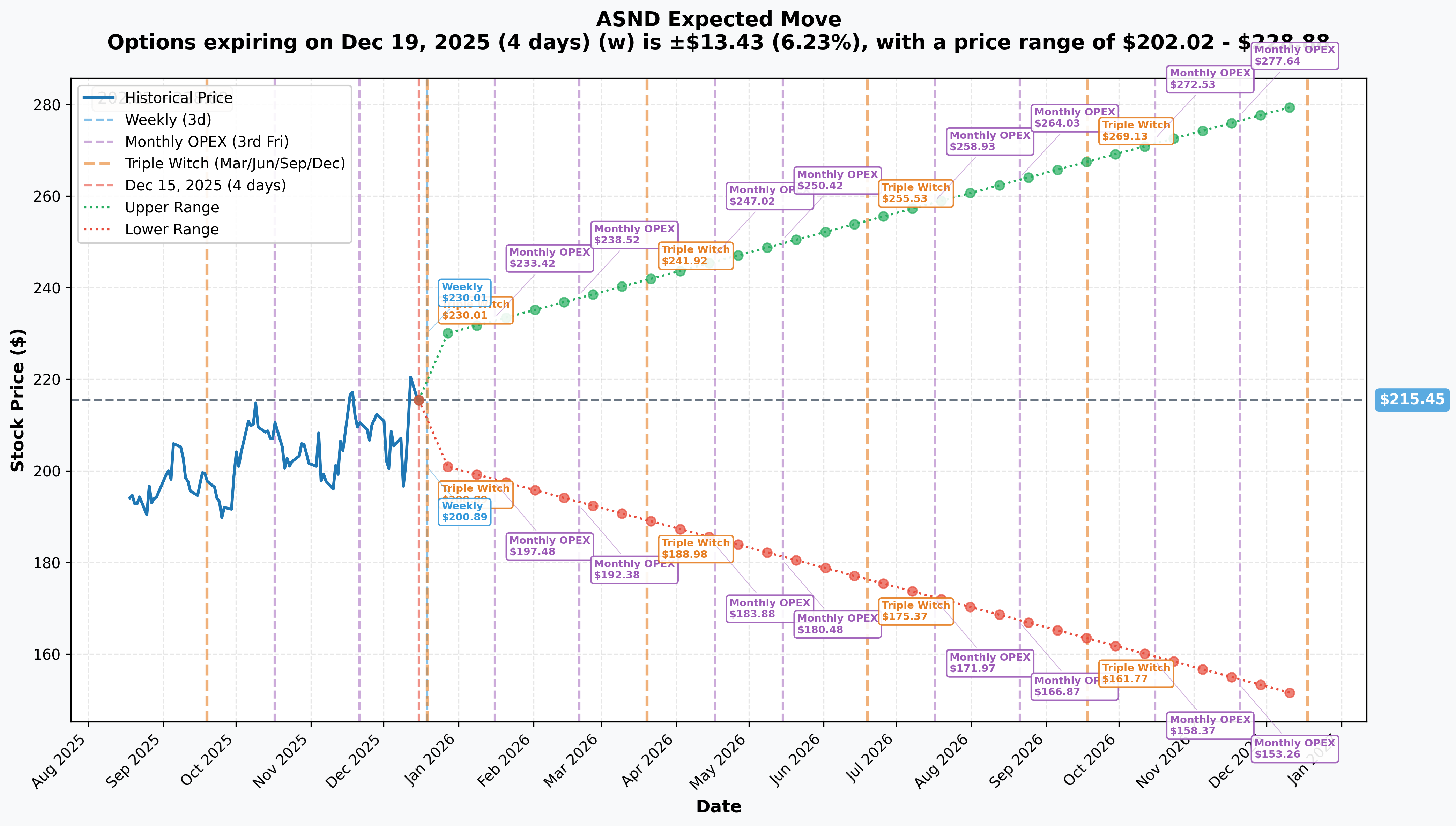

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 4 days): ±$13.43 (±6.23%) → Range: $202.02 - $228.88

- 📅 Monthly OPEX (Jan 16 - 32 days): ±$17.97 (±8.34%) → Range: $197.48 - $233.42

- 📅 Quarterly Triple Witch (Mar 20 - 95 days - THIS TRADE!): ±$26.47 (±12.28%) → Range: $188.98 - $241.92

- 📅 LEAPS (Dec 18, 2026 - 368 days): ±$65.02 (±30.18%) → Range: $150.43 - $280.47

Translation for regular folks: Options traders are pricing in a 6.2% move ($13) by Friday for weekly expiration, and a MASSIVE 12.3% move ($26) through March OPEX which includes Q4 earnings, YORVIPATH launch metrics, and potential TransCon CNP approval. The market expects REAL CATALYSTS to drive volatility!

The March 20th expiration (when this $1.1M trade expires) has an upper range of $241.92 - meaning the market thinks there's a legitimate possibility ASND could trade as high as $242 over the next 95 days (12% rally). This aligns PERFECTLY with the call buyer's thesis: capitalize on the YORVIPATH US launch ramp and potential CNP approval catalyst to push above $230 by March.

Key insight: The $230 strike sits near the center of the March implied move range ($189-$242), suggesting the market sees it as a reasonable outcome rather than a heroic bet. The trader is paying $22.60 (10% of stock price) for exposure to upside above $252.60 breakeven.

🎪 Catalysts

🔥 Already Happened (Recent Wins Building Momentum)

Q3 2024 Earnings - November 14, 2024 📊

Ascendis reported strong Q3 results demonstrating accelerating commercial traction:

- 💰 Total Revenue: €57.8M (+20.4% YoY vs €48.0M in Q3 2023)

- 💊 YORVIPATH Revenue: €8.5M (first full quarter post-European launch, >60% sequential growth!)

- 💵 SKYTROFA Revenue: €47.2M (flat YoY due to €2.5M prior period adjustment, but fundamentals solid)

- 📈 9-Month SKYTROFA: €138.5M (+21% YoY)

- 💸 Cash Position: €625.5M (strong balance sheet heading into US YORVIPATH launch)

- 🎯 2024 SKYTROFA Guidance: €200-220M maintained

Why this matters: Demonstrated that YORVIPATH European launch is EXCEEDING expectations with >60% quarter-over-quarter growth. This de-risks the upcoming US launch and validates commercial execution capabilities.

Novo Nordisk Strategic Partnership - November 4, 2024 🤝

Landmark deal validating TransCon platform in metabolic diseases:

- 💰 Upfront + Near-Term: Up to $285M for lead once-monthly GLP-1 program

- 🎯 Lead Program: Once-monthly GLP-1 receptor agonist for obesity/type 2 diabetes

- 💵 Per Product: Up to $77.5M per additional program in milestones

- 📊 Economics: Tiered royalties on global net sales + sales-based milestones

- ✅ Status: Transaction closed before end of 2024; $100M upfront received January 2025

Why this matters: External validation of TransCon platform BEYOND rare diseases. Proves technology has applications in multi-billion dollar obesity/diabetes markets. The $100M upfront received in January provides non-dilutive capital to fund pipeline without shareholder dilution.

TransCon hGH Adult GHD FDA Acceptance - December 12, 2024 🏥

FDA accepted supplemental BLA for SKYTROFA in adult growth hormone deficiency:

- 📅 PDUFA Date: July 27, 2025

- 📊 Clinical Support: Phase 3 foresiGHt trial (259 adults aged 23-80)

- 💰 Revenue Potential: Adult indication could drive SKYTROFA toward blockbuster status (>$1B revenue)

- 🎯 Market Opportunity: Adult GHD affects thousands requiring lifelong daily injections; once-weekly offers massive convenience

Why this matters: Expands SKYTROFA addressable market significantly. If approved, positions SKYTROFA as one of three blockbuster products by 2030 (Vision 2030 strategic plan).

🚀 Upcoming Catalysts (What This Trade is Betting On!)

YORVIPATH US Commercial Launch - January 2025 Ongoing ⭐ HIGHEST IMPACT

First and only FDA-approved treatment for hypoparathyroidism now ramping in the US:

- 📅 Product Availability: Late December 2024 (commercially available NOW)

- 📈 Early Adoption (as of February 7, 2025): 908 prescriptions, 539 unique prescribing providers

- 💰 Q1 2025 Revenue: €44.7M (3.3x sequential growth from Q4!)

- 🎯 Reimbursement: Company expects 70-80% approval rate

- 🌍 European Performance: ~700 patients on treatment by end of 2024

- 💵 Pricing: European pricing ~€105,000 ($114,700) annually

Market Opportunity:

- 👥 US Patient Population: 70,000-90,000 people with hypoparathyroidism

- 🏆 Competitive Position: FIRST AND ONLY FDA-approved treatment (monopoly!)

- 📊 Clinical Data: Phase 3 PaTHway trial showed 79% achieved primary endpoint vs 5% placebo (p<0.0001)

- 💪 Differentiation: Once-daily subcutaneous injection replaces multiple daily oral calcium/vitamin D supplements

Why this is THE catalyst: YORVIPATH US launch represents Ascendis's transition from pure-play rare disease biotech to commercial-stage biopharma with REAL revenue growth. Q1 2025 revenue of €44.7M (already reported) demonstrates explosive uptake. The March expiration captures Q4 2024 earnings (full launch quarter) and early visibility into Q1 2026 trajectory. If launch continues exceeding expectations, this stock goes MUCH higher.

TransCon CNP NDA Submission - Q1 2025 ⭐ HIGHEST IMPACT

Achondroplasia (dwarfism) treatment heading to FDA:

- 📅 Pre-NDA Meeting: Completed per Q4 2024 earnings call

- 📝 NDA Submission: On track for Q1 2025 (January-March 2025) - could happen ANY DAY

- 🎯 FDA PDUFA Date: November 30, 2025 (Priority Review granted!)

- 🌍 European MAA: Expected Q3 2025

- ✅ Expected Approval: Q4 2025 / Q1 2026

Clinical Data (Results published in JAMA Pediatrics):

- 📊 Primary Endpoint: Annualized Growth Velocity 5.89 cm/year (TransCon CNP) vs 4.41 cm/year (placebo); treatment difference 1.49 cm/year (p<0.0001)

- 🎯 Safety: ZERO discontinuations due to adverse events

- 💪 Patient Retention: 100% of completers continuing in open-label extension

Market Opportunity:

- 👥 Prevalence: Most common form of dwarfism; affects 1 in 25,000 births

- 🏆 Competition: BioMarin's Voxzogo (approved 2021) - TransCon CNP offers once-weekly dosing vs daily injection

- 💰 Revenue Potential: Analyst 2027 projections >€500M from CNP + YORVIPATH combined

Why this matters for the March trade: The NDA submission expected in Q1 2025 (January-March) falls EXACTLY within the March 20 expiration window! If Ascendis announces NDA submission in January or February, the stock could rally 10-20% on de-risking of this blockbuster program. The call buyer is perfectly positioned to capture this catalyst.

TransCon hGH Adult GHD FDA Decision - July 27, 2025

Adult growth hormone deficiency approval decision:

- 📅 PDUFA Date: July 27, 2025 (after March expiration, but guidance/expectations could be set earlier)

- 📊 Clinical Support: Phase 3 foresiGHt trial data strong enough for FDA acceptance

- 💰 Revenue Add: Could add $200-400M annually by 2027-2028

- 🎯 Strategic Value: Critical to achieving SKYTROFA blockbuster status (>$1B revenue)

Why this matters: While the actual decision comes after March expiration, any pre-approval manufacturing announcements, FDA panel scheduling, or positive regulatory updates in Q1 2026 could provide upside catalysts.

Q4 2024 / Full Year 2024 Earnings - February 2025

Expected reporting: February 12, 2025 (already reported, but key metrics inform March trade thesis):

- 💰 Full Year 2024 SKYTROFA Revenue: €202M (within guidance)

- 💊 Full Year 2024 YORVIPATH Revenue: €28.7M

- 📊 Total 2024 Revenue: €230.9M

- 💵 Cash Position: €559.5M + $100M Novo upfront = ~€650M pro forma

- 📈 Net Loss: €378.1M (improved from €481.4M in 2023)

2025 Guidance to Watch:

- YORVIPATH US revenue trajectory (this is THE number everyone will focus on)

- Path to cash flow breakeven timeline

- CNP launch timing expectations

Why this matters for March trade: Earnings will be reported ~4-5 weeks before March expiration. Strong YORVIPATH US launch metrics and bullish 2025 guidance could provide the fundamental catalyst to push stock from $220 to $240+.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, upcoming catalysts, and analyst consensus ($260 average target), here are the scenarios through March 20th expiration:

📈 Bull Case (35% probability)

Target: $250-$270

How we get there:

- 🚀 YORVIPATH CRUSHES: Q4 earnings show US launch exceeding expectations with >1,500 patients enrolled, reimbursement rates 75-80% as guided

- 📝 CNP NDA FILED: TransCon CNP NDA submission announced in January/February, de-risking November approval

- 💰 2025 Guidance STRONG: Management guides to €400M+ total revenue for 2025 (vs €230.9M in 2024) driven by YORVIPATH ramp

- 🤝 Novo Partnership Progress: Updates on once-monthly GLP-1 development, potential additional program announcements

- 📊 Analyst Upgrades: Street raises price targets from current $260 average to $280-300 range on launch success

- 📈 Technical Breakout: Stock breaks through $220 resistance, gamma squeeze toward $230, then momentum to $240 ceiling

- 🏥 Adult GHD Positive Signals: Any FDA communication or panel scheduling for July PDUFA creates anticipation

Key metrics needed:

- YORVIPATH revenue run-rate tracking toward $500M+ annually (€100M+ per quarter)

- CNP NDA submission confirmed

- European YORVIPATH patient count >1,000

- Gross margins expanding (proving pricing power)

Probability assessment: 35% because it requires strong execution but all pieces are in place. YORVIPATH launch already showing 3.3x sequential growth in Q1. Analysts have $260 average target (21% upside from current $215). Gamma structure supports move to $230-240 once $220 breaks.

🎯 Base Case (45% probability)

Target: $210-$230 (CHOPPY UPTREND)

Most likely scenario:

- ✅ Solid YORVIPATH performance: US launch meeting expectations but not fireworks - 800-1,200 patients enrolled

- 📊 CNP on track: NDA submission happens but no major surprise (expected event)

- 💵 Guidance conservative: Management guides in-line, citing execution focus over aggressive targets

- 🌍 European steady: YORVIPATH Europe continues growing but no major new market announcements

- 🎯 Valuation digestion: Stock consolidates recent 54% YTD gains, trading $210-230 range for weeks

- 📉 Volatility compression: Post-earnings IV crush, options premiums decline 30-40%

- ⏰ Wait for CNP approval: Market in "show me" mode waiting for November FDA decision

Why 45% probability: This is the consensus scenario. Ascendis executes on plan, delivers solid but not spectacular results, stock trades in line with biotech sector. The $230 strike represents ~7% upside from current $215 - reasonable for a biotech with strong catalysts but already up 54% YTD.

Call P&L in Base Case:

- Stock at $230 on Mar 20: Calls worth $0 (at-the-money), loss = -$22.60/share × 500 = -$1.13M (100% loss!)

- Stock at $240 on Mar 20: Calls worth $10.00, loss = -$12.60/share × 500 = -$630K (56% loss)

- Stock at $250 on Mar 20: Calls worth $20.00, loss = -$2.60/share × 500 = -$130K (12% loss)

📉 Bear Case (20% probability)

Target: $180-$210 (SIGNIFICANT PULLBACK)

What could go wrong:

- 😰 YORVIPATH disappoints: Reimbursement rates come in 50-60% (below 70-80% guidance), patient uptake slower than expected

- 🚨 CNP delays: NDA submission pushed to Q2 2025, raising concerns about approval timeline

- 💸 Guidance weak: Management provides conservative 2025 outlook, highlights competitive pressure or pricing challenges

- 🇪🇺 European headwinds: YORVIPATH European growth stalls, raising questions about US trajectory

- 🔬 Clinical setback: Safety signal in open-label extensions or other pipeline program

- 📉 Biotech selloff: Broader sector weakness (risk-off, interest rate fears) drags all biotechs lower

- 💰 Cash burn concerns: Burn rate higher than expected, questions about path to profitability

- 🛡️ Break below $210: Gamma support at $210 fails, momentum accelerates toward $200, then $195

Critical support levels:

- 🛡️ $210: Major gamma floor (0.834B) - MUST HOLD or technical damage done

- 🛡️ $200: Secondary support (0.639B gamma) - previous breakout level

- 🛡️ $195: Extended floor (0.146B gamma) - disaster scenario

Probability assessment: Only 20% because fundamentals remain strong. YORVIPATH is first-in-class with no competition, CNP has strong Phase 3 data with Priority Review, and Novo partnership validates platform. Would require multiple negative catalysts or broader market crash. However, biotech is volatile and any execution hiccup at current valuation could trigger sharp correction.

Call P&L in Bear Case:

- Stock at $200 on Mar 20: Calls expire worthless, loss = -$22.60/share × 500 = -$1.13M (100% loss)

- Stock at $180 on Mar 20: Calls expire worthless, loss = -$22.60/share × 500 = -$1.13M (100% loss)

Breakeven Analysis for March $230 Calls:

- Breakeven Price: $252.60 (strike $230 + premium paid $22.60)

- Required Move: +17% from current $215.59 price

- Above Implied Move: $252.60 is near the top end of March implied range ($189-$242), meaning trader needs better-than-expected outcome

💡 Trading Ideas

🛡️ Conservative: Wait for CNP NDA Submission Announcement

Play: Stay on sidelines until TransCon CNP NDA submission is confirmed, then enter on any pullback

Why this works:

- ⏰ NDA submission expected Q1 2025 (January-March) - don't speculate, wait for actual news

- 📊 Stock at $215 already up 54% YTD near all-time highs - limited margin of safety

- 💸 The $1.1M call buy signals smart money is BULLISH, but they have different risk tolerance than retail

- 🎯 Better entry likely on post-earnings consolidation or any biotech sector weakness

- 📈 Once CNP NDA is filed, regulatory risk decreases significantly (approval odds >80% with Priority Review)

- 🤔 Let the big money take the risk - you join after catalyst is confirmed

Action plan:

- 👀 Watch for Ascendis press release on CNP NDA submission (likely January-February)

- 🎯 Look for pullback to $200-210 gamma support post-announcement for stock entry with 5-10% margin of safety

- ✅ Need to see YORVIPATH Q4 revenue >€15M (showing continued sequential growth)

- 📊 Monitor analyst revisions post-earnings - upgrades to $270-280 targets would confirm bull thesis

- ⏰ Revisit mid-2025 when CNP approval decision approaches (November 30 PDUFA)

Position sizing: Start with 2-3% portfolio allocation to stock (not options) once entry criteria met

Risk level: Low (patient approach) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -15-20% drawdown if launch disappoints or biotech sector corrects. Get cleaner entry with fundamental catalyst confirmed. Participate in CNP approval run into November 2025 PDUFA.

⚖️ Balanced: February Earnings Call Spread (Defined Risk Play)

Play: After YORVIPATH launch metrics are visible, play earnings with defined-risk call spread

Structure: Buy $220 calls, Sell $240 calls (February 20 expiration - captures Q4 earnings)

Why this works:

- 📊 Defined risk spread ($20 wide = $2,000 max profit per spread)

- 🎯 Targets realistic move from $215 current to $230-240 on strong earnings

- 💰 Much cheaper than buying naked calls like the whale trade

- ⏰ February 20 expiration gives time for earnings (Feb 12) to play out plus 8 days for momentum

- 🎪 Captures THE key catalyst: YORVIPATH US launch metrics and 2025 guidance

- 🛡️ Limited downside if earnings disappoint - max loss is debit paid

Estimated P&L:

- 💰 Pay ~$8-10 net debit per spread (current pricing, adjust closer to entry)

- 📈 Max profit: $10-12 if ASND above $240 at February expiration (100-150% ROI)

- 📉 Max loss: $8-10 if ASND below $220 (defined and limited)

- 🎯 Breakeven: ~$228-230

- 📊 Risk/Reward: ~1:1.2 which is favorable for defined-risk bullish play

Entry timing:

- ⏰ Enter 5-7 days before earnings (around Feb 5-7) once implied volatility starts rising

- 🎯 Only enter if stock trading $210-220 range (gives room for spread to work)

- ❌ Skip if stock already above $230 (spread too close to short strike)

Position sizing: Risk only 3-5% of portfolio (this is directional speculation on earnings)

What you're betting on:

- YORVIPATH Q4 revenue >€15M (vs €8.5M in Q3)

- 2025 revenue guidance €350-400M+ (significant growth from €230.9M in 2024)

- Reimbursement rates meeting 70-80% guidance

- CNP NDA submission timing confirmed for Q1

Exit strategy:

- 🎯 If stock rallies to $235-240 within 2-3 days post-earnings, TAKE PROFITS (don't get greedy)

- 📉 If stock drops below $210 post-earnings, close for loss and reassess thesis

- ⏰ Don't hold to expiration unless deeply in-the-money - theta decay accelerates final week

Risk level: Moderate (defined risk, earnings binary event) | Skill level: Intermediate

🚀 Aggressive: Replicate the Whale with Smaller Size (ADVANCED!)

Play: Copy the institutional March $230 call structure with appropriate position sizing

Structure: Buy $230 calls (March 20 expiration - SAME as $1.1M trade)

Why this could work:

- 🐋 Following smart money: Institutional trader with $1.1M conviction is betting on multi-catalyst setup

- 🎪 Extended time: 95 days to expiration captures YORVIPATH launch ramp, Q4 earnings, CNP NDA submission

- 📊 At-the-money strike: $230 is just 7% above current price - not a heroic bet, reasonable target

- 🚀 Multiple shots on goal: Don't need just ONE catalyst - could get YORVIPATH surprise, CNP NDA, earnings beat, analyst upgrades

- 📈 Gamma acceleration: If stock breaks $220 resistance, gamma squeeze toward $230-240 creates explosive upside

- ⏰ Time for thesis: Unlike weekly/monthly options, March expiration gives thesis time to develop

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: $22.60 per contract ($2,260 per call) - nearly 10% of stock price paid as premium

- ⏰ High breakeven: Need stock at $252.60 to breakeven (17% rally required from current $215)

- 😱 Time decay: Theta burns ~$0.20-0.30/day - losing $20-30 per contract daily

- 📉 YORVIPATH risk: If US launch disappoints (reimbursement issues, slower uptake), stock could drop to $180-190

- 🎢 Biotech volatility: Sector corrections, FDA policy changes, or competitive threats could trigger 20-30% selloff

- 💰 100% loss possible: If stock below $230 at March expiration, calls expire worthless

- ⚠️ Already extended: Stock up 54% YTD at all-time highs - buying into strength is dangerous

Estimated P&L:

- 💰 Cost: $22.60 per call (use current pricing or better)

- 📈 Profit scenario: Stock at $260 by March = $30.00 intrinsic - $22.60 cost = $7.40 profit (33% ROI)

- 🚀 Home run: Stock at $280 by March = $50.00 intrinsic - $22.60 cost = $27.40 profit (121% ROI)

- 🎯 Modest win: Stock at $245 by March = $15.00 intrinsic - $22.60 cost = -$7.60 loss (34% loss)

- 📉 Loss scenario: Stock at $220-230 range = expire near/at-the-money = -$15 to -$22.60 loss (65-100% loss)

- 💀 Total loss: Stock below $230 = -$22.60 (100% loss)

Breakeven: $252.60 (need 17% rally from current $215)

CRITICAL WARNINGS - DO NOT attempt unless you:

- ✅ Can afford to lose 100% of premium (realistic scenario!)

- ✅ Understand biotech binary event risk (clinical/regulatory surprises move stocks 20-30% instantly)

- ✅ Have traded biotech options before and know the sector's volatility characteristics

- ✅ Accept that even with strong catalysts, timing could be wrong (stock rallies in April/May after expiration)

- ✅ Won't panic sell on normal -5-10% biotech volatility swings

- ⏰ Have plan to take profits if stock hits $245-250 early (don't hold for max profit and watch it evaporate)

Position sizing:

- Risk ONLY 2-5% of portfolio maximum

- For $100K portfolio: Buy 2-4 contracts max ($4,520-9,040 at risk)

- For $50K portfolio: Buy 1-2 contracts max ($2,260-4,520 at risk)

- For $25K portfolio: DO NOT ATTEMPT - position too risky for small account

Exit strategy:

- 🎯 Target 1: Stock hits $245 = close 50% of position for 33% loss (protect against total wipeout)

- 🎯 Target 2: Stock hits $260 = close another 30% for 33% profit (take some risk off)

- 🚀 Let 20% run: Hold final 20% for home run to $270-280 if momentum continues

- 📉 Stop loss: If stock breaks below $200 = close all for loss (thesis broken)

- ⏰ Time stop: Don't hold past March 10 unless deeply in-the-money (final 10 days theta is brutal)

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~35% (need strong execution + favorable timing)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🏥 YORVIPATH launch execution risk: Company expects 70-80% reimbursement approval rate - any shortfall could slow patient uptake dramatically. Commercial launch in rare disease requires physician education, patient identification, and payer acceptance. If ANY of these pieces fail, stock could drop 20-30%. Current Q1 data shows 908 prescriptions but sustainability unknown.

-

📝 CNP NDA submission/approval risk: While Phase 3 data is strong (1.49 cm/year improvement, p<0.0001), FDA could request additional safety data, impose restrictive labeling, or delay approval. BioMarin's Voxzogo already approved gives physicians "good enough" option - TransCon CNP must prove SUPERIORITY to win market share. Any setback pushes revenue out 1-2 years.

-

💰 Path to profitability unclear: €378M net loss in 2024 with burn rate ~€100M/quarter. Cash position €559.5M + $100M Novo upfront = €650M gives runway into 2026-2027, but commercialization costs for YORVIPATH/CNP could exceed expectations. Dilutive capital raise possible if launch underperforms.

-

🎯 Valuation at $13.47B with limited revenue: Trading at premium valuation despite only €230.9M in 2024 revenue. Stock is pricing in YORVIPATH reaching $500M+ and CNP reaching $300M+ by 2027. If EITHER product disappoints, valuation could compress 30-40%. At current price, there's zero margin for error.

-

🌍 Geographic concentration risk: YORVIPATH European launch provides only €28.7M in 2024 revenue despite ~700 patients. US launch accounts for 70-80% of revenue potential - if US underperforms, no geographic diversification to offset. Single country (US) driving entire thesis.

-

🔬 Pipeline dependency on TransCon platform: All products use same TransCon technology. If safety signal emerges in ANY program (YORVIPATH, SKYTROFA, CNP, IL-2), could raise questions about entire platform. TransCon IL-2 oncology data shows early promise but oncology is higher risk - any severe adverse event could create overhang.

-

💊 Adult GHD approval dependency (July 2025): SKYTROFA adult indication PDUFA July 27 represents $200-400M revenue opportunity. Approval not guaranteed - FDA could request additional data or impose age restrictions. Failure would remove key pillar of Vision 2030 blockbuster thesis.

-

🏦 Smart money hedging aggressively: The fact that an institutional trader is rolling OUT of December into March (extending duration) rather than simply taking profits suggests they see BOTH upside potential AND significant risk. They're willing to pay $22.60 for March exposure rather than hold stock unhedged - that's a CAUTION FLAG about near-term volatility expectations.

-

📊 Biotech sector volatility: Small/mid-cap biotech highly correlated to market sentiment, interest rates, and risk appetite. If broader market corrects or sector rotation away from growth stocks accelerates, ASND could drop 20-30% regardless of fundamentals. YTD gain of 54% makes it vulnerable to profit-taking.

-

🎢 Post-earnings volatility crush: Current implied volatility likely elevated heading into February earnings. Even if results are GOOD, IV crush could cause options to lose 30-50% of value overnight. The March calls at $22.60 have significant time premium that evaporates if stock trades sideways.

-

⚖️ Competition emerging: While YORVIPATH has no direct competition NOW, rare disease attracts new entrants if markets prove lucrative. CNP faces established BioMarin Voxzogo with 3+ years head start. Physician/patient switching costs high in rare disease - incumbency advantage real.

-

🇪🇺 European pricing/reimbursement pressure: €105,000 annual price in Europe faces increasing scrutiny. If US payers demand lower pricing or utilization management restrictions, margins could compress below expectations. Company hasn't disclosed US YORVIPATH pricing yet - uncertainty remains.

🎯 The Bottom Line

Real talk: Someone with deep pockets just committed $1.1 MILLION to March $230 calls on ASND, betting that the YORVIPATH US launch and TransCon CNP NDA submission will drive the stock from $215 to $250+ by March. This isn't a gamble - it's a calculated bet on multiple high-probability catalysts converging in Q1 2026.

What this trade tells us:

- 🎯 Sophisticated player expects SIGNIFICANT VOLATILITY through March (positioning for 17% upside to breakeven)

- 💰 They're confident enough in YORVIPATH launch trajectory to pay $22.60/share for March exposure (10% of stock price!)

- ⚖️ The extended time frame (95 days) shows they need MULTIPLE catalysts to play out - not betting on single binary event

- 📊 They rolled FROM December $230s INTO March $230s rather than taking profits - that's CONVICTION in continued upside

- ⏰ March 20 expiration perfectly captures Q4 earnings (Feb 12), potential CNP NDA submission (Q1 2025), and YORVIPATH momentum data

This is NOT a "YOLO into biotech" signal - it's a "multiple catalysts de-risking over coming months" signal.

If you own ASND:

- ✅ Hold core position through earnings (February 12) - YORVIPATH data should be strong

- 📊 Consider adding 10-20% on any pullback to $200-210 support (gamma floor)

- ⏰ Set mental stop at $195 (major support) to protect if thesis breaks

- 🎯 If CNP NDA submitted in January/February, consider trimming 25% at $240-250 to lock profits

- 🛡️ Don't get shaken out by normal -5-10% biotech volatility - focus on fundamental execution

If you're watching from sidelines:

- ⏰ Don't chase current $215 level - stock up 54% YTD at all-time highs, wait for entry

- 🎯 Best entry: Post-earnings pullback to $200-210 OR on CNP NDA submission announcement

- 📈 Looking for confirmation of: YORVIPATH Q4 revenue >€15M, reimbursement rates 70-80%, 2025 guidance €350M+

- 🚀 Longer-term (12-18 months), CNP approval (Nov 2025) and adult GHD approval (July 2025) are legitimate catalysts for $280-320

- ⚠️ Current valuation requires flawless execution - one stumble and it's back to $180-190

If you're considering the March calls:

- 🎯 Only for ADVANCED traders with biotech experience who can lose 100% of premium

- 📊 Breakeven at $252.60 requires 17% rally - not impossible but needs strong catalysts

- ⏰ Don't enter until late December/early January to see YORVIPATH enrollment trends

- 📉 Watch for break below $210 - that's signal thesis is broken, don't force the trade

- ⚠️ Position size MAXIMUM 2-5% of portfolio (this is speculation, not core holding)

Mark your calendar - Key dates:

- 📅 December 19 (Friday) - Weekly expiration (implied ±6.2% move)

- 📅 January 16, 2026 - Monthly OPEX

- 📅 February 12, 2026 - Q4 2024 / Full Year 2024 Earnings (YORVIPATH US launch metrics!)

- 📅 March 20, 2026 - Quarterly triple witch, expiration of this $1.1M call trade

- 📅 Q1 2025 (Jan-Mar) - TransCon CNP NDA submission expected

- 📅 July 27, 2025 - TransCon hGH adult GHD PDUFA date

- 📅 November 30, 2025 - TransCon CNP PDUFA date (Priority Review)

Final verdict: ASND's multi-product story is INCREDIBLY compelling - YORVIPATH monopoly in hypoparathyroidism, CNP competing for achondroplasia market, Novo Nordisk validation of TransCon platform, and Vision 2030 targeting three $1B+ products. The 14 Buy ratings with $260 average price target (21% upside) reflects Street confidence.

BUT, at $215 near all-time highs with $13.47B market cap on €230.9M revenue, you're paying for PERFECTION. The $1.1M institutional call buy signals bullish conviction, but the $252.60 breakeven shows even smart money needs significant upside to profit.

Be selective with entry. Wait for CNP NDA filing or post-earnings dip. Let the catalysts come to you. Biotech rewards patience and punishes FOMO.

This is a 12-18 month story, not a 3-month trade. Position accordingly. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. Biotech companies face binary event risk from clinical trials, FDA decisions, and commercialization execution. The March $230 calls have high breakeven ($252.60) requiring 17% rally from current levels - probability of profit is uncertain. Always do your own research and consider consulting a licensed financial advisor before trading. The institutional trader may have complex portfolio hedging needs, access to non-public information through expert networks, or risk tolerance not applicable to retail traders.

About Ascendis Pharma A/S: Ascendis Pharma AS is a biopharmaceutical company that applies its TransCon technology platform to develop treatments for endocrinology and oncology, with a market cap of $13.47 billion. The company commercializes SKYTROFA (pediatric growth hormone deficiency) and YORVIPATH (hypoparathyroidism) with three potential blockbuster products targeting >$1B revenue each by 2030.