💰 BABA $4.2M Call Position Closed - Smart Money Exits Before Earnings!

📅 January 22, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just cashed out $4.2 MILLION from BABA call options this morning at 10:02:30! This massive trade sold 2,200 contracts of the $185 strike calls expiring June 18th - locking in profits just 28 days before Q3 earnings on February 19th. With BABA surging +5.25% pre-market to $177.50 on Apple AI partnership momentum, smart money is taking chips off the table after an incredible run from $85 lows. Translation: Institutional investors are ringing the register at the peak!

📊 Company Overview

Alibaba Group Holding Limited (BABA) is the world's largest online and mobile commerce company transforming into an AI-first infrastructure powerhouse:

- Market Cap: $402.7 Billion

- Industry: E-commerce, Cloud Computing, Digital Services

- Current Price: $178.02 (up from $168.67 close)

- 52-Week Range: $84.96 - $192.67

- Primary Business: Chinese e-commerce platforms (Taobao, Tmall), Alibaba Cloud, logistics services, digital media

💰 The Option Flow Breakdown

The Tape (January 22, 2026 @ 10:02:30):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order Type | Strategy | Z-Score | Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-22 | 10:02:30 | BABA | SELL | CALL $185 | 2026-06-18 | $185 | 2,200 | $4.2M | STC | Close Short Call | 11.54 | EXTREMELY UNUSUAL |

🤓 What This Actually Means

This is a profit-taking exit from a bullish position! Here's what went down:

- 💸 Massive premium collected: $4.2M (~$19.09 per contract x 2,200 contracts)

- 🎯 Strike above current price: $185 is 3.9% above current $178 level

- ⏰ Strategic timing: Exiting 28 days BEFORE Q3 earnings (Feb 19) - avoiding binary event risk

- 📊 Z-Score of 11.54: This trade is EXTREMELY UNUSUAL - 11.5 standard deviations above normal activity

- 🏦 Vol/OI Ratio of 18.3: HIGH_ACTIVITY classification confirms institutional-sized flow

- 🔔 Signal: CLOSE position - they're taking profits, not adding exposure

What's really happening here:

This trader likely accumulated BABA calls during the stock's recovery from $85 lows in 2024. With BABA now trading near $178 and surging on Apple AI partnership news, they're locking in significant gains before the February 19th earnings report creates uncertainty. The June expiration gave them time, but why risk giving back profits when you can exit at multi-year highs?

Unusual Score: 🔥 EXTREMELY UNUSUAL (11.54 Z-Score) - This happens maybe a few times per month on BABA. The trade size of 2,200 contracts controlling 220,000 shares (worth ~$39M) signals sophisticated institutional activity. Not your neighbor's Robinhood account!

📈 Technical Setup / Chart Check-Up

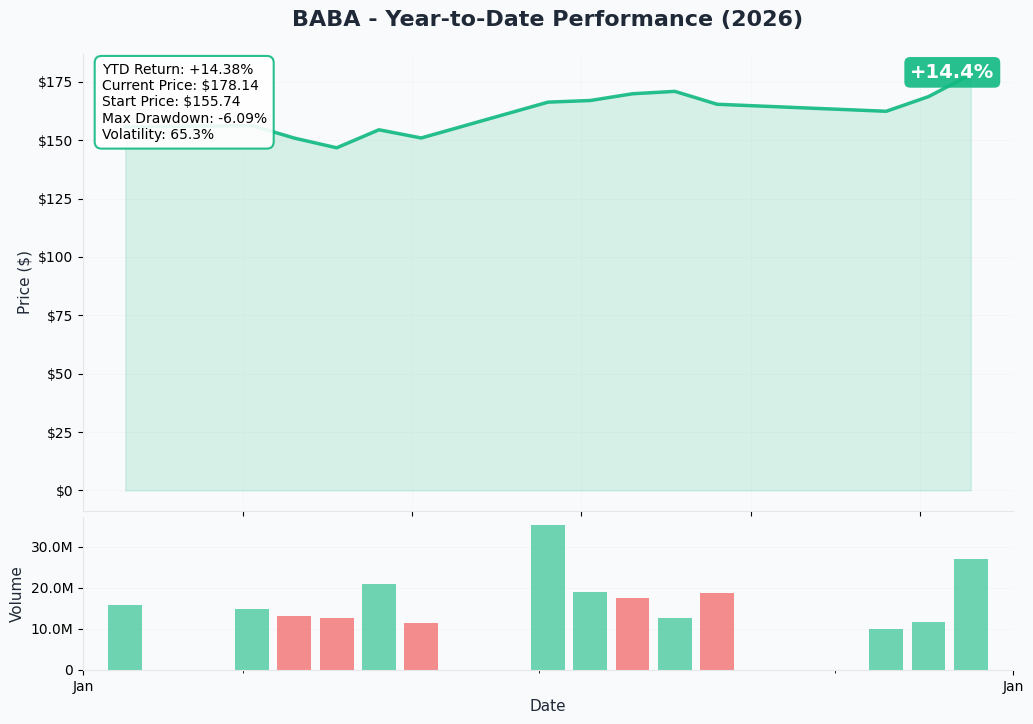

YTD Performance Chart

BABA has staged an incredible comeback - recovering from brutal 2024 lows below $85 to trade near $178 today. The chart tells a transformation story from beaten-down e-commerce giant to AI infrastructure leader.

Key observations:

- 🚀 Massive recovery: Stock more than doubled from 2024 lows around $84.96

- 📈 Breakout confirmed: Smashed through $150-$160 consolidation zone

- 🔥 Today's catalyst: +5.25% pre-market on continued Apple partnership momentum

- ⚠️ Near 52-week highs: Trading just 8% below $192.67 peak - potential resistance ahead

- 📊 Volume surge: Heavy institutional accumulation on AI/cloud thesis rotation

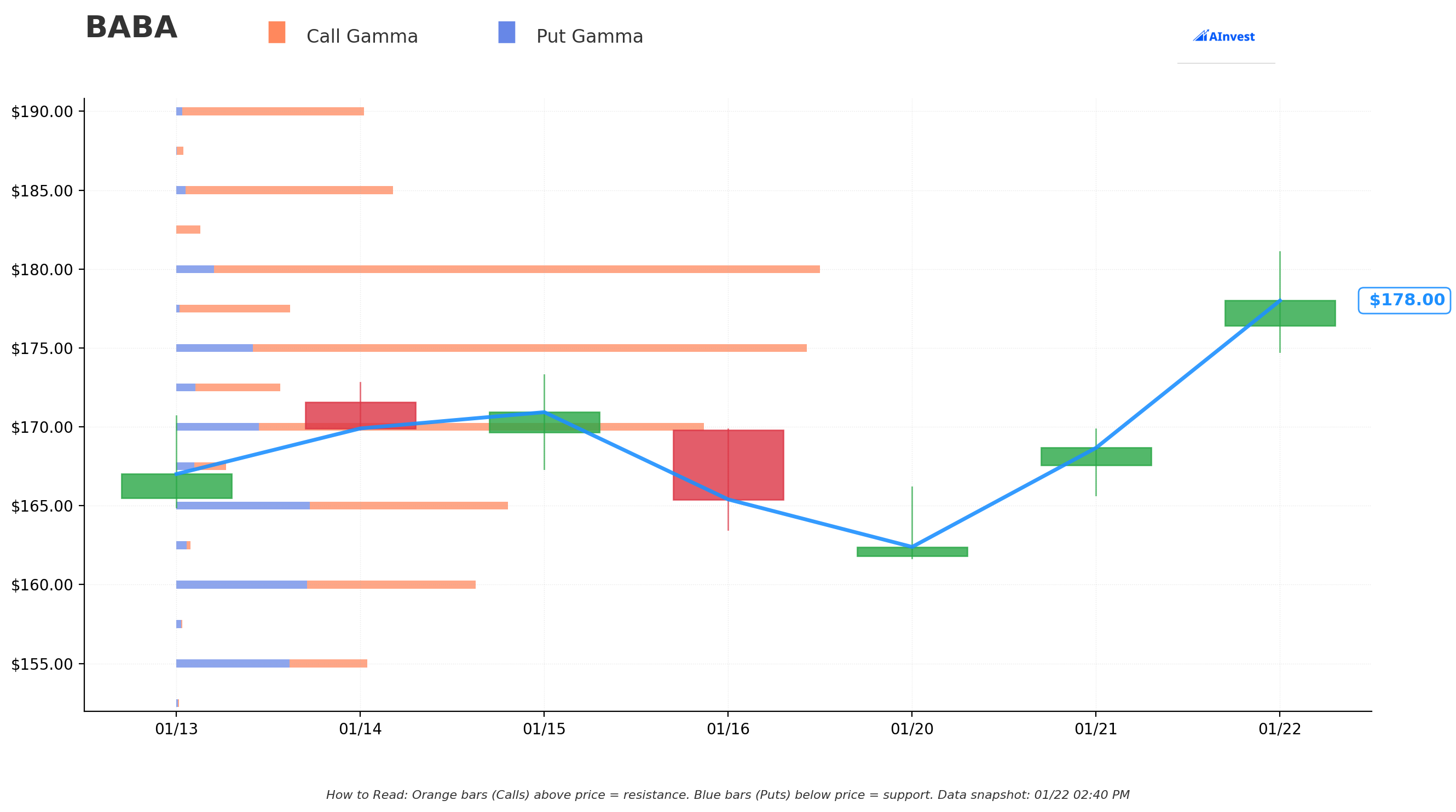

Gamma-Based Support & Resistance Analysis

Current Price: $178.02

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $175 - Immediate support with 30.9B total gamma exposure (strongest nearby floor!)

- Distance: 1.7% below current price

- Net GEX: +23.3B (positive = dealers buy dips)

- $170 - Secondary support at 26.2B gamma

- Distance: 4.5% below current price

- Net GEX: +18.0B (strong floor)

- $165 - Structural floor with 17.1B gamma

- Distance: 7.3% below current price

- Net GEX: +3.9B (weaker but still support)

- $160 - Deep support at 15.6B gamma

- Distance: 10.1% below current price

- $155 - Extended support zone with 9.6B gamma (Net GEX turns negative here: -1.6B)

- $150 - Disaster floor at 10.5B gamma (Net GEX: -2.4B)

🟠 Resistance Levels (Call Gamma Above Price):

- $180 - Immediate ceiling with 31.8B gamma (STRONGEST LEVEL - dealers will sell into rallies!)

- Distance: 1.1% overhead

- Net GEX: +28.0B (massive call gamma creates resistance)

- $185 - Secondary resistance at 10.6B gamma (THIS IS THE TRADE'S STRIKE!)

- Distance: 3.9% above current price

- Net GEX: +9.7B

- $190 - Major ceiling zone with 9.2B gamma

- Distance: 6.7% above current price

- $200 - Extended upside target at 19.7B gamma

- Distance: 12.3% above current price

- Net GEX: +19.0B (significant call positioning)

What this means for traders:

BABA is trading in a TIGHT range between massive $175 support and crushing $180 resistance. The gamma data shows market makers holding enormous positions at $180 (31.8B - the single largest level) which creates natural selling pressure as price approaches. This setup suggests consolidation before the next big move.

Notice anything? The call seller struck at $185 - exactly at the next major resistance level after $180. They're betting the stock struggles to break through $180-185 before June, especially with earnings uncertainty ahead. Smart positioning.

Net GEX Bias: BULLISH (191.8B call gamma vs 64.9B put gamma) - Overall positioning remains bullish, but immediate price action constrained by $180 overhead resistance.

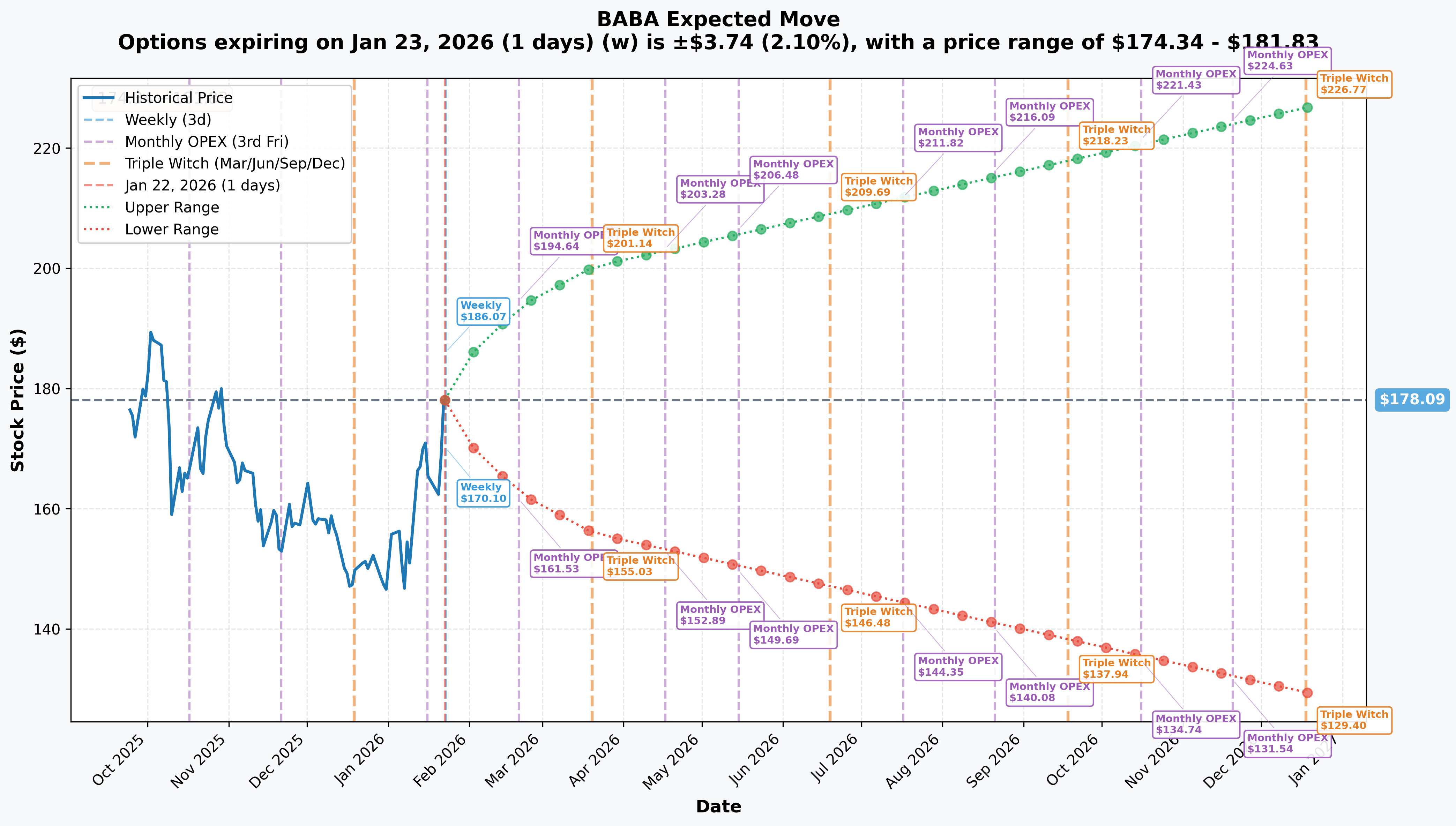

Implied Move Analysis

Options market pricing for upcoming expirations:

| Timeframe | Expiry Date | Days | Implied Move % | Implied Move $ | Upper Range | Lower Range |

|---|---|---|---|---|---|---|

| 📅 Weekly | 2026-01-23 | 1 | ±2.1% | ±$3.74 | $181.83 | $174.34 |

| 📅 Monthly OPEX | 2026-02-20 | 29 | ±8.77% | ±$15.62 | $193.70 | $162.47 |

| 📅 Triple Witch | 2026-03-20 | 57 | ±12.46% | ±$22.18 | $200.27 | $155.90 |

| 📅 June OPEX (This Trade!) | 2026-06-19 | 148 | ~17.5% | ~$31.15 | $209.69 | $146.48 |

| 📅 LEAPS | 2026-12-18 | 330 | ±27.34% | ±$48.68 | $226.77 | $129.40 |

Translation for regular folks:

Options traders are pricing in a 2.1% move ($3.74) by tomorrow for weekly expiration, but a MASSIVE 8.77% move ($15.62) through February OPEX which includes Q3 earnings on February 19th. The market expects FIREWORKS around earnings - that's a significant implied move!

The June 18th expiration (when this $4.2M trade expires) has an implied range of roughly $146-$210. The call seller is betting BABA stays below $185 through June - a reasonable bet given the $180 gamma wall overhead and 66% ADR delisting probability per Goldman Sachs.

Key insight: The February OPEX implied move of ±8.77% reflects massive earnings uncertainty. Smart money is taking profits NOW rather than gambling on the binary event.

🎪 Catalysts

🔥 Upcoming Catalysts (Next 6 Months)

Q3 Fiscal Year 2026 Earnings - February 19, 2026 (28 DAYS AWAY!) 📊

BABA reports fiscal Q3 results on Thursday, February 19, 2026 before market open. This is THE catalyst that could make or break the recovery rally. Wall Street consensus:

- 📊 Revenue: RMB 250.38B expected

- 🤖 Cloud Intelligence: Watch for continued 30%+ growth trajectory

- 💻 AI Revenue: Triple-digit growth for 10th consecutive quarter?

- 🍔 Food Delivery: Path to profitability after regulatory intervention

- 📈 Margin Recovery: EBIT margin dropped to 2% last quarter - improvement needed

Alibaba Cloud Infrastructure Deployment (Throughout 2026):

- 🌍 New data centers opening in Mexico, Japan, South Korea, Malaysia, Dubai

- 💰 $5+ billion quarterly CAPEX run rate continuing

- 🤖 AI infrastructure buildout supporting $53B three-year investment

AI Model Releases & Qwen Updates:

- 🚀 Continued Qwen model updates - already most downloaded open-source AI model globally

- 🤝 Expanded Nvidia partnership for model training

- 🔬 Development of in-house AI chips through T-Head semiconductor division

✅ Recent Catalysts (Already Happened)

Apple Partnership for iPhone AI in China (February 2025):

Apple chose Alibaba to power AI features for iPhones in China after evaluating Baidu, Tencent, ByteDance, and DeepSeek. This partnership is critical:

- 📱 Apple experienced 11% YoY drop in iPhone sales in China

- 🚀 Deal sent BABA to three-year high upon announcement

- ⚠️ Partnership drawing scrutiny from Washington - potential risk factor

$53 Billion AI Infrastructure Investment (February 2025):

Alibaba announced plans to invest at least RMB 380 billion ($53B) over three years on cloud and AI infrastructure - described by Citigroup as "the largest investment ever by Chinese private enterprises."

Q2 FY2026 Results (November 2025):

- 📊 Revenue: RMB 247.8B ($34.9B), up 5% YoY, beating consensus

- 🤖 Cloud Intelligence: RMB 39.8B ($5.59B), up 34% YoY - significantly beat

- 😰 Non-GAAP EPS: RMB 4.36, down 71% YoY - missed expectations

- 📈 AI-Related Revenue: Triple-digit growth for ninth consecutive quarter

Antitrust Rectification Complete (August 2024):

China's SAMR officially ended its three-year antitrust review, praising Alibaba for compliance. Major regulatory overhang removed.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through June 18th expiration:

📈 Bull Case (30% probability)

Target: $190-$210

How we get there:

- 💪 Q3 earnings CRUSH expectations with cloud revenue accelerating past 35% growth

- 🚀 AI revenue continues triple-digit growth for 10th consecutive quarter

- 🤝 Apple partnership expansion announcements drive momentum

- 📊 Food delivery market rationalization improves margins (70-80% probability per catalysts)

- 🌐 International commerce exceeds 30% of revenue

- 📈 Breakout above $180 gamma resistance triggers technical rally to $200+ (implied move upper range)

- 🇺🇸 ADR delisting fears subside, removing valuation discount

Key metrics needed:

- Cloud Intelligence revenue growth >30% YoY

- EBIT margin improvement from 2% toward 8-10%

- Food delivery segment path to profitability

- Qwen ecosystem continued dominance driving cloud adoption

Probability assessment: 30% because it requires multiple positive catalysts aligning. The $180 gamma wall creates significant overhead resistance, and 66% embedded ADR delisting probability caps upside potential.

🎯 Base Case (45% probability)

Target: $165-$185 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ Solid earnings meeting consensus (~RMB 250B revenue)

- 📱 Cloud growth remains strong (30-35%) but market already pricing it in

- ⚖️ Food delivery losses continue but improving trajectory

- 🤖 AI narrative maintains valuation but doesn't expand multiple

- 🇨🇳 Geopolitical uncertainty keeps investors cautious

- 🔄 Trading within gamma support ($175) and resistance ($180-185) bands

- 📊 Market digests gains, waits for delisting clarity and margin recovery proof points

- 💤 Volatility normalizes post-earnings

This is the call seller's target scenario: Stock consolidates in $165-185 range, calls expire worthless or significantly reduced, and they keep most of the $4.2M premium. Smart trade.

Why 45% probability: Stock at technical inflection point between major gamma levels. Strong fundamental story (AI/cloud) offset by execution risks (margins, geopolitics). Most institutional players will hold and wait for clearer signals.

📉 Bear Case (25% probability)

Target: $145-$165

What could go wrong:

- 😰 Q3 earnings miss or weak guidance - margin compression continues

- 🚨 ADR delisting concerns intensify - Goldman's 66% probability materializes

- 🇨🇳 145% reciprocal tariffs escalate, hitting international commerce

- 💸 Food delivery subsidy war continues draining cash (RMB 100B industry-wide in 2025)

- ⚖️ Apple partnership draws regulatory action from Washington

- 📊 Domestic e-commerce share losses accelerate to PDD Holdings

- 🔨 Break below $175 gamma support triggers cascade to $165, then $155

Critical support levels:

- 🛡️ $175: Major gamma floor (30.9B) - MUST HOLD or momentum shifts bearish

- 🛡️ $170: Secondary support (26.2B gamma)

- 🛡️ $165: Structural floor (17.1B gamma)

- 🛡️ $155-$160: Extended support zone - disaster scenario

Probability assessment: 25% because it requires multiple negative catalysts - margin miss, geopolitical escalation, OR delisting action. Alibaba's fundamental cloud/AI growth provides floor, but VIE structure risk and geopolitics create real tail risk.

💡 Trading Ideas

🛡️ Conservative: Wait for Post-Earnings Clarity

Play: Stay on sidelines until after February 19th earnings settles

Why this works:

- ⏰ Earnings in 28 days creates binary event risk with ±8.77% implied move

- 💸 Options expensive pre-earnings - better entry points after IV crush

- 📊 Stock near multi-year highs after doubling from lows - profit-taking natural

- 🎯 Better entry likely post-earnings after volatility crush reduces premiums 40-50%

- 🤔 The $4.2M institutional exit signals smart money is DERISKING - why fight them?

- 🇨🇳 Geopolitical risks remain elevated - 66% ADR delisting probability

Action plan:

- 👀 Watch February 19th earnings closely for cloud growth (30%+ needed), margin recovery, and guidance

- 🎯 Look for pullback to $165-170 gamma support post-earnings for stock entry

- ✅ Need to see margin improvement and geopolitical clarity before committing capital

- 📊 Monitor unusual options activity - if institutions add MORE exits, stay defensive

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

⚖️ Balanced: Post-Earnings Covered Call Strategy

Play: After earnings, buy stock and sell covered calls

Structure:

- Buy 100 shares at ~$170-175 (target post-earnings dip)

- Sell 1 June $190 call for premium income

Why this works:

- 🎢 Captures upside to $190 (14% above entry) while collecting premium

- 📊 $190 sits above major gamma resistance - unlikely to break through

- 🎯 Premium income provides 5-8% buffer on downside

- ⏰ June expiration gives time for multiple catalysts to play out

- 🤝 Essentially joining the institutional trade's thesis - capping upside for income

Estimated P&L:

- 💰 Stock entry: ~$170-175

- 💰 Call premium: ~$8-12 per share

- 📈 Max profit: $190 - $170 + $10 premium = ~$30 (18% return if called away)

- 📉 Downside protected to: ~$160-162 breakeven

Risk level: Moderate (stock ownership risk) | Skill level: Intermediate

🚀 Aggressive: Earnings Straddle (ADVANCED ONLY!)

Play: Buy straddle betting on post-earnings volatility exceeding implied move

Structure:

- Buy $175 calls + Buy $175 puts (February 20 expiration)

Why this could work:

- 💥 Implied move of ±8.77% but BABA has shown 10-15% earnings moves historically

- 🎰 Betting the Street is UNDERPRICING earnings volatility

- 📊 Multiple catalysts converging: earnings, Apple partnership updates, cloud growth

- 🚀 Binary outcome potential - beat sends it toward $190+, miss drops it to $160

- ⚡ Only need stock to move >10% either way to profit

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Straddle costs significant premium

- ⏰ TIME DECAY: Theta burns rapidly as earnings approaches

- 😱 IV CRUSH: Even if stock moves 6-8%, IV collapse could result in LOSS

- 📊 Two-way risk: Stock could land in $168-182 range and you lose entire premium

- 🇨🇳 China wildcards: Geopolitics could overshadow earnings in either direction

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded straddles through earnings before

- ✅ Can afford to lose ENTIRE premium

- ✅ Understand IV crush mechanics

- ✅ Can monitor position and exit quickly post-earnings

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🇨🇳 ADR Delisting Risk: Goldman Sachs ADR Delisting Barometer shows 66% probability of delisting risk embedded in Chinese ADRs. If regulators use April 2025 as year one, delisting could occur as soon as 2026. 26% of BABA shares held by US institutions, 40% by retail - significant forced selling risk.

-

🌐 US-China Trade War: Reciprocal tariffs reached 145% with China retaliating at 125%. International commerce segment (30%+ of revenue target) directly exposed.

-

💸 Margin Compression: EBIT margin dropped to just 2% in Q2 FY2026 as heavy AI CAPEX ($5.4B last quarter) and food delivery subsidies (RMB 100B industry-wide) crush profitability. Net income fell 53% YoY.

-

⚖️ VIE Structure Risk: US investors do not directly own equity in Alibaba's core Chinese operating companies. Structure vulnerable to Chinese government pressure.

-

🏢 Domestic E-commerce Competition: PDD Holdings market share rose to 23% as "involution" competition intensifies. Alibaba's 10% dip in adjusted earnings reflects margin pressure.

-

🤝 Apple Partnership Regulatory Risk: Apple's AI deal with Alibaba drawing scrutiny from Washington with Defense Department examining Alibaba's ties to Chinese government. Could face restrictions.

-

📊 Gamma Ceiling at $180: Massive 31.8B call gamma at $180 creates mechanical selling pressure. Market makers will systematically SELL into rallies to hedge - breakouts difficult without sustained buying.

-

🐋 Smart Money Exiting: This $4.2M call exit signals sophisticated players are DERISKING at multi-year highs rather than adding exposure into earnings. When institutions take profits, retail should pay attention.

🎯 The Bottom Line

Real talk: Someone just cashed out $4.2 MILLION from BABA calls at multi-year highs, 28 days before the most important earnings report since the AI transformation began. This isn't bearish on BABA's long-term story - it's smart risk management by institutions who've made HUGE money on the recovery from $85 and don't want to give it back on geopolitical headlines or an earnings miss.

What this trade tells us:

- 🎯 Sophisticated player expects VOLATILITY but not necessarily higher prices through June

- 💰 They're confident enough to exit $185 strikes - betting stock struggles to break $180-185 resistance

- ⚖️ The timing (28 days pre-earnings) shows they see binary risk - not worth gambling $4.2M on

- 📊 The Z-Score of 11.54 (EXTREMELY UNUSUAL) confirms this is institutional activity, not retail

- ⏰ June expiration would have given plenty of time - but they're not waiting

This is a "take profits and reassess" signal.

If you own BABA:

- ✅ Consider trimming 25-40% at $175-180 levels (lock in recovery gains)

- 📊 If holding through earnings, set MENTAL STOP at $170 (major gamma support)

- ⏰ Don't get greedy - you've already won big if you bought the $85 lows!

- 🎯 If earnings beat AND stock breaks $185, could re-enter trimmed shares

- 🛡️ Consider selling covered calls against long position to generate income

If you're watching from sidelines:

- ⏰ February 19th before market open is the moment of truth - patience recommended

- 🎯 Post-earnings pullback to $165-170 would be EXCELLENT entry with gamma support

- 📈 Looking for: Cloud growth 30%+, margin improvement from 2%, food delivery progress, guidance confidence

- 🚀 Longer-term, Apple partnership, $53B AI investment, and Qwen dominance are legitimate catalysts for $200+

- ⚠️ 66% ADR delisting probability creates real tail risk - size positions accordingly

If you're bearish:

- 🎯 Wait for earnings before initiating shorts - fighting momentum into highs is dangerous

- 📊 First resistance at $180 (gamma ceiling), support at $175, deeper at $170

- ⚠️ Post-earnings put spreads offer defined-risk way to play downside after IV crush

- 📉 Watch for break below $175 - that's the trigger for cascade to $165

Mark your calendar - Key dates:

- 📅 January 23 (Tomorrow) - Weekly OPEX, ±2.1% implied move

- 📅 February 19 (Thursday) - Q3 FY2026 earnings before market open

- 📅 February 20 - Monthly OPEX (±8.77% implied move through earnings)

- 📅 March 20 - Quarterly Triple Witch

- 📅 June 18 - This call trade's expiration

- 📅 Throughout 2026 - Data center openings in Mexico, Japan, South Korea, Malaysia, Dubai

Final verdict: BABA's AI transformation story is COMPELLING - Apple partnership, 34% cloud growth, Qwen dominance, and $53B infrastructure commitment are all real. BUT, at multi-year highs with 66% ADR delisting probability, 145% tariffs, and earnings in 28 days, the risk/reward is NO LONGER favorable for aggressive new positioning. The $4.2M institutional exit is a CLEAR signal: smart money is derisking at the peak.

Be patient. Let earnings clear. Look for better entry points at $165-170. The AI revolution will still be here in a month, and you'll sleep better at night.

This is about protecting capital, not chasing highs. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 11.54 Z-Score reflects this specific trade's unusualness relative to recent BABA history - it does not imply the trade will be profitable or that you should follow it. Chinese ADRs carry unique risks including VIE structure and delisting concerns. Always do your own research and consider consulting a licensed financial advisor before trading.

About Alibaba Group Holding Limited: Alibaba is the world's largest online and mobile commerce company, operating major Chinese e-commerce platforms (Taobao, Tmall) with expanding cloud computing, logistics, digital media, and AI services. Market cap of $402.7 billion, transforming from e-commerce utility into AI-first infrastructure company.