CDE $1.4M Call Bet - Mining Giant on Major M&A Transformation!

📅 November 6, 2024 | 🔥 Extreme Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $1.4 MILLION on Coeur Mining January 2026 calls at 10:46 AM today! This sophisticated player bought 4,767 contracts of $12.50 strike calls with 14 months to expiration - betting big on CDE's transformation into a North American precious metals powerhouse. With two massive acquisitions pending ($8.7B combined), gold at all-time highs near $2,650/oz, and the stock already up 72% YTD, smart money is positioning for the next leg higher as these deals close in 2025-2026. Translation: Major institutional bet on CDE's M&A supercycle!

📊 Company Overview

Coeur Mining, Inc. (CDE) is a metals producer focused on mining precious minerals in the Americas, involved in the discovery and mining of gold and silver:

- Market Cap: $9.11 Billion

- Industry: Gold and Silver Ores

- Current Price: $14.47 (November 6, 2024)

- Primary Operations: 5 mines across US and Mexico (Palmarejo, Rochester, Kensington, Wharf, Las Chispas)

- Major Transformation: Two pending acquisitions totaling $8.7B to create top-tier North American producer

💰 The Option Flow Breakdown

The Tape (November 6, 2024 @ 10:46:16):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:46:16 | CDE | MID | BUY | CALL | 2026-01-16 | $1.4M | $12.50 | 4.8K | 10K | 4,767 | $14.47 | $2.98 |

🤓 What This Actually Means

This is a massive bullish bet on CDE's transformation through major acquisitions! Here's the breakdown:

- 💸 Huge premium commitment: $1.4M ($2.98 per contract × 4,767 contracts)

- 🎯 Strategic strike selection: $12.50 strike is 13.6% below current $14.47 price = already $1.97 in-the-money

- ⏰ Long-dated position: 14 months to January 2026 expiration

- 📊 Massive exposure: 4,767 contracts represents 476,700 shares worth ~$6.9M

- 🏦 Institutional-sized play: This is NOT retail, this is sophisticated money

What's really happening here:

This buyer is positioning for CDE's transformation through two major acquisitions - $1.7B SilverCrest Metals (closing Q1 2025) and $7B New Gold (closing H1 2026). The January 2026 expiration perfectly captures both deal closings and the production ramp to 1.25M gold equivalent ounces annually. With gold near all-time highs and CDE trading at $14.47, this player expects significant upside as the combined entity delivers $3B EBITDA and $2B free cash flow in 2026.

Unusual Score: 🔥 EXTREME (1,255x average size) - This happens maybe a few times a year at most! We're talking about a position size that's unprecedented for CDE options, ranking at the 100th percentile of all historical trades.

📈 Technical Setup / Chart Check-Up

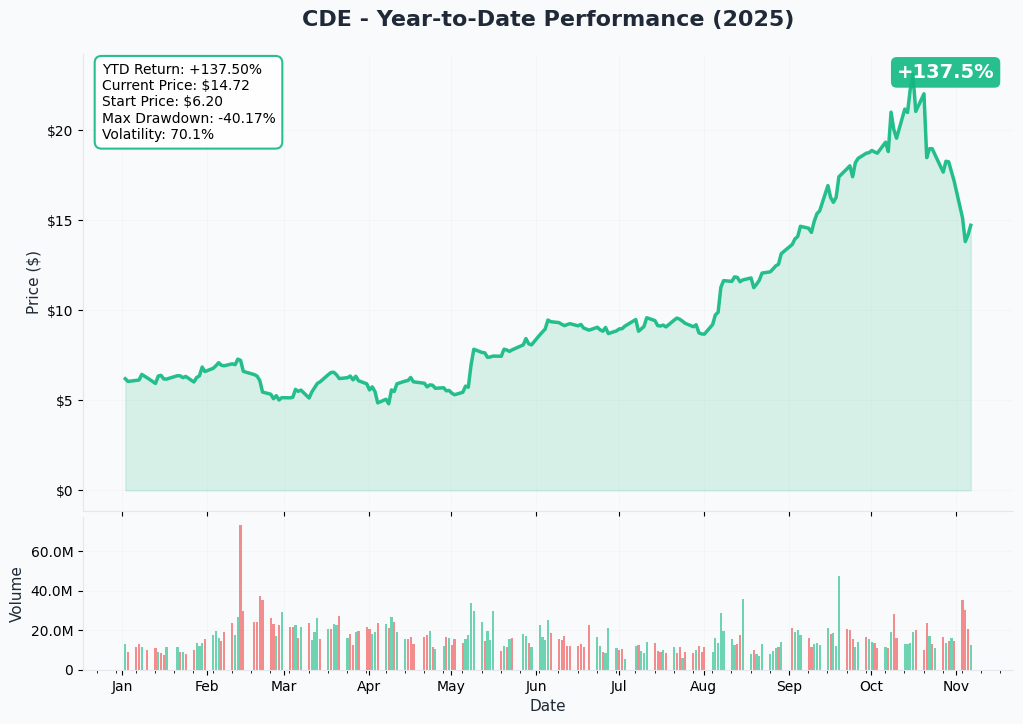

YTD Performance Chart

Coeur Mining has had an exceptional year, up +72% YTD through Q3 2024. The chart shows a massive breakout story - CDE has rallied from under $4 earlier this year to current levels around $14.47, driven by record production at expanded Rochester mine, gold hitting all-time highs, and two transformational M&A announcements.

Key observations:

- 📈 Explosive momentum: Multi-year breakout above $10 resistance in October 2024

- 💹 Acquisition catalyst: Stock surged on $1.7B SilverCrest deal (October 4) and $7B New Gold merger (November 3)

- 🎯 Gold tailwinds: Precious metals rally with gold near $2,650/oz supporting mining stocks

- 📊 Volume explosion: Institutional buying drove CDE to top 500 trading volume rank

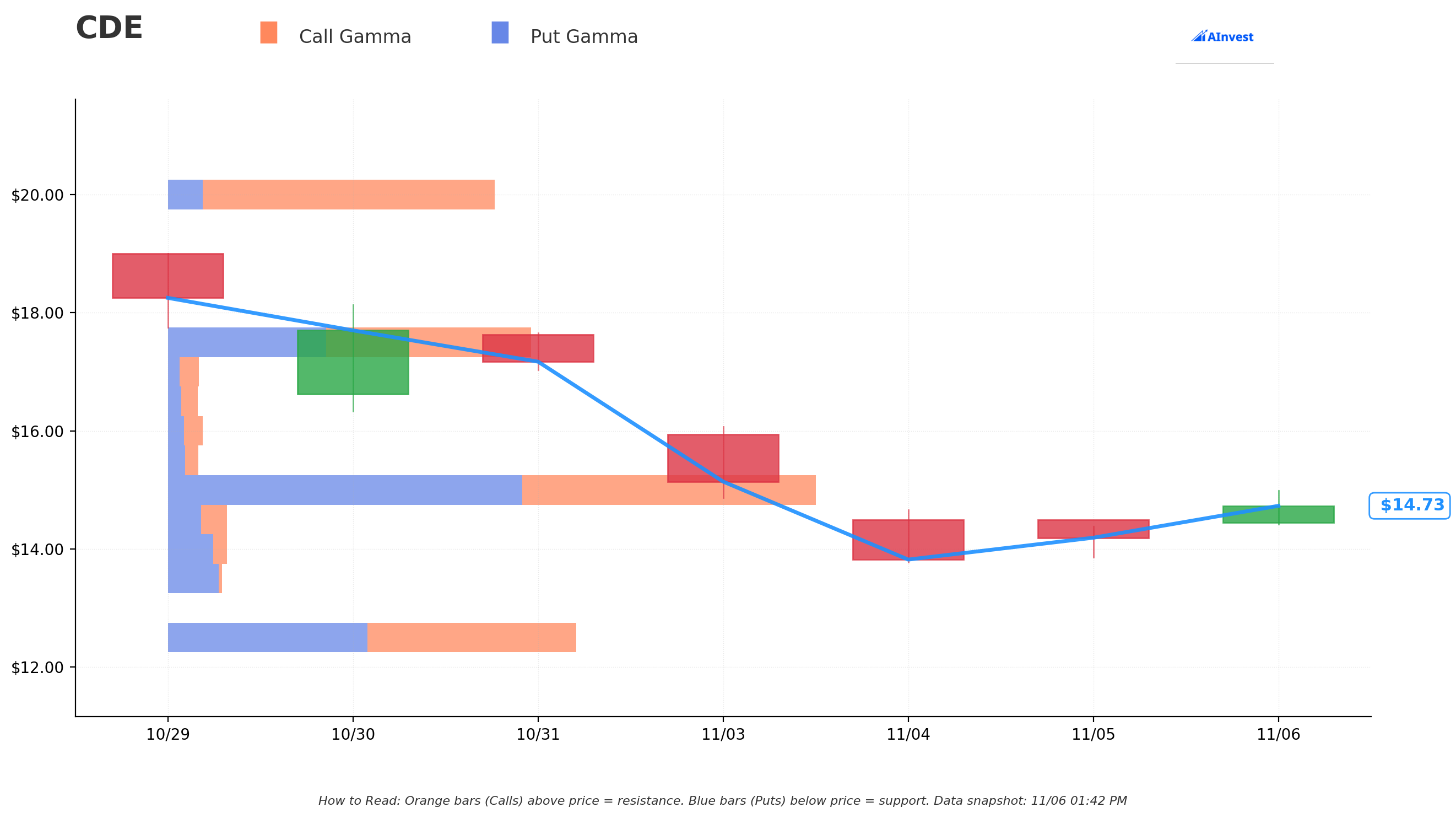

Gamma-Based Support & Resistance Analysis

Current Price: $14.73

The gamma exposure map reveals critical price magnets and defensive walls for CDE:

🔵 Support Levels (Put Gamma Below Price):

- $14.50 - Immediate support with 0.48B total gamma exposure (balanced put/call)

- $14.00 - Strong floor with 0.47B gamma (0.36B put-heavy)

- $13.50 - Secondary support at 0.43B gamma (0.41B put protection)

- $12.50 - MAJOR support zone with 3.29B gamma (1.60B put wall) - THIS IS THE STRIKE IN THE UNUSUAL TRADE!

🟠 Resistance Levels (Call Gamma Above Price):

- $15.00 - STRONGEST resistance with 5.23B total gamma exposure (2.84B put + 2.38B call)

- $15.50 - Minor resistance at 0.25B gamma

- $16.00 - Secondary ceiling with 0.28B gamma

- $17.50 - Extended resistance zone with 2.95B gamma (significant barrier)

What this means for traders:

The gamma data shows CDE has massive support at $12.50 (the exact strike of this unusual trade!), with 3.29B in gamma creating a strong floor. This buyer clearly identified this technical level as the downside protection. The immediate resistance at $15.00 with 5.23B gamma is the strongest level, where market makers will hedge by selling stock as price approaches. However, if CDE breaks through $15 on strong news (acquisition closings, strong earnings, gold rally), the path to $17.50 opens up. The net positioning suggests range-bound trading between $14-$15 in the near term, with major catalysts needed to break resistance.

🎪 Catalysts

🔥 Immediate Catalysts (Already Announced/In Progress)

Historic Two-Deal M&A Transformation (October-November 2024) 💼

CDE announced two massive acquisitions within 30 days, creating a transformational growth story:

-

SilverCrest Metals Acquisition - $1.7B (October 4, 2024)

- Deal structure: 1.6022 CDE shares per SilverCrest share (18% premium)

- Strategic asset: High-grade Las Chispas mine in Sonora, Mexico

- Cost advantage: Operations ~40% below CDE corporate average costs

- Expected close: Late Q1 2025

- Regulatory progress: Mexican antitrust approval received February 2025

- Production impact: Contributing to 2025 target of 21M oz silver production

-

New Gold Mega-Merger - $7B (November 3, 2024)

- Deal value: $7B all-stock merger creating ~$20B combined entity

- Transaction terms: 0.4959 CDE shares per New Gold share

- New mines: Adds Rainy River (Ontario) and New Afton (BC) operations

- Scale transformation: Production jumps to 1.25M GEO (900K oz gold, 20M oz silver)

- Expected close: First half of 2026

- Shareholder votes: Q1 2026 special meetings (need 66⅔% approval)

- Pro forma targets: $3B EBITDA and $2B free cash flow in 2026

Gold at All-Time Highs - Favorable Macro Backdrop 🥇

Precious metals are experiencing a historic rally supporting mining company valuations:

- Gold trading near $2,648/oz, up 30% in 2024

- Silver broke through $30/oz, industrial and investment demand strong

- Fed rate cuts supporting non-yielding assets

- Central bank buying (particularly China) providing structural demand

Rochester Mine Expansion Success (2024 Achievement) ⚙️

- Commercial production achieved March 31, 2024

- New crusher exceeded 88,000 tons/day nameplate capacity within 4 months

- Delivered 70% production growth and 20% cost reductions

- On track for full-year guidance of 4.8-6.6M oz silver, 37K-50K oz gold

🚀 Near-Term Catalysts (Next 6 Months)

Q4 2024 Earnings (Already Reported February 21, 2025) 📊

Historical reference showing strong execution:

- Revenue: $305M, Net income: $38M ($0.08/share)

- $80M debt paid down during 2024

- Adjusted EBITDA more than doubled to $339M full-year

- Capital expenditures cut in half

Q1 2025 Earnings Announcement 📅

- Scheduled: May 7, 2025 after market close, conference call May 8 at 11:00 AM ET

- Key metrics to watch: Production at Las Chispas integration, Rochester continued performance, debt reduction progress

- Historical Q1 2025 showed $360M revenue and $68M operating cash flow

SilverCrest/Las Chispas Transaction Close (Q1 2025) 🔒

- Expected timing: Late Q1 2025

- Mexican antitrust approval already received (February 2025)

- Immediate production accretion from high-grade, low-cost asset

- Cornerstone of 2025 target of 21M oz silver production

New Gold Shareholder Votes (Q1 2026) 🗳️

- Special meetings in Q1 2026

- Need 66⅔% New Gold shareholder approval

- CDE stockholders must approve share issuance and charter amendments

- Market impact: Positive votes remove key uncertainty, negative vote creates major risk event

2025 Production Targets 🎯

Updated guidance showing growth trajectory:

- Gold: 380K-440K oz (+12% YoY, revised up 3K oz in Q3 2025)

- Silver: 16.7-20.3M oz (+44% YoY)

- CASK guidance reduced by $125/oz in Q3 update - costs improving

Continued Debt Reduction Milestones 💪

- Target: $80-100M quarterly free cash flow starting Q2 2025

- Net leverage improved to 0.9x (March 2025) from 4.1x (June 2023)

- Priority: Eliminate revolving credit facility before reinvestment

Reserves and Resources Growth (February 2025 Report) 📈

- Year-end 2024: 3.6M oz gold (+22% YoY at Kensington), 270.5M oz silver

- 5-year growth: Gold reserves +40%, silver reserves +48%

- $55M exploration investment in 2024 supporting future growth

⚠️ Risk Catalysts (What Could Go Wrong)

Integration Execution Risks ⚙️

- Simultaneously digesting two major acquisitions ($8.7B combined) creates operational complexity

- Historical mining M&A typically sees 12-18 months of elevated costs

- Different mine geological profiles and operating cultures require careful management

- $3B EBITDA and $2B FCF 2026 targets depend on successful synergy realization

Valuation Concerns 📊

- Trading at 52.1x PE vs. peer average 16.6x after 208% rally

- Cantor Fitzgerald downgraded to Neutral citing valuation (November 2024)

- Limited margin for error if execution stumbles

Precious Metals Price Risk 🌊

- No hedging program = full exposure to gold/silver price fluctuations

- Fed policy changes could pressure metals if rates rise in late 2025/2026

- Dollar strength typically inversely correlated with gold prices

Permitting and Regulatory Delays 🏛️

- US permitting averages 7-10 years vs. 2-year global benchmarks

- Mexican operations face regulatory unpredictability

- Canadian exposure adds provincial regulations and indigenous consultation requirements

🎲 Price Targets & Probabilities

Using gamma levels, catalyst timeline, and precious metals backdrop, here are the scenarios:

📈 Bull Case (35% probability)

Target: $18-$22

How we get there:

- 🎯 SilverCrest deal closes smoothly in Q1 2025, immediate cost synergies realized

- 🥇 Gold pushes toward $3,000/oz on continued Fed easing and geopolitical uncertainty

- 🗳️ New Gold shareholders vote YES in Q1 2026 with strong margin (>75%)

- 💪 Q2/Q3 2025 earnings show $80-100M quarterly free cash flow materializing

- 📈 Rochester and Las Chispas exceed production targets

- 🔓 Successfully breaks through $15 and $17.50 gamma resistance on sustained buying

- 🎊 Analysts upgrade to reflect $3B EBITDA 2026 trajectory

Option profit at $20: $7.50 per contract (252% return on $2.98 premium) = $3.57M total profit on $1.4M investment

🎯 Base Case (45% probability)

Target: $15-$18 range

Most likely scenario:

- ✅ SilverCrest closes in Q1 2025 with normal integration challenges

- 📊 Gold remains elevated in $2,500-$2,800 range supporting valuations

- ⚖️ New Gold vote passes but with some shareholder opposition (66-70% approval)

- 💰 Continued debt reduction shows progress but leverage stays around 0.7-0.9x through 2025

- 🏭 Production meets guidance but doesn't significantly exceed

- 🔒 Trading mostly between $14-$17.50, occasional tests of $18

- 📈 Breaks $15 resistance but consolidates before attacking $17.50 gamma wall

- 🕐 Market waits for actual New Gold closing in H1 2026 before major re-rating

Option profit at $17: $4.50 per contract (151% return) = $2.15M total profit

This aligns with the trade thesis: Buyer expects successful M&A execution and strong precious metals environment to drive steady appreciation through 2025-2026, with January 2026 calls capturing the value creation from both deal closings.

📉 Bear Case (20% probability)

Target: $12-$14

What could go wrong:

- 😰 Integration challenges emerge at Las Chispas, costs exceed projections

- 🥇 Gold corrects to $2,200-$2,400 on hawkish Fed pivot or dollar strength

- ❌ New Gold shareholder vote FAILS or faces significant opposition, deal uncertainty

- 📉 Q1-Q2 2025 earnings disappoint, free cash flow below $80M target

- ⚠️ Operational issues at Rochester or other mines

- 🌊 Broader mining sector selloff on China demand concerns

- 💸 Elevated 52.1x PE multiple compresses toward peer average 16-20x

- 🛡️ Falls to $12.50 support (the strike price!) but gamma wall holds

Option outcome at $13: Breakeven around $15.48 ($12.50 + $2.98), so at $13 the calls expire worthless = -$1.4M total loss (100% of premium)

Important note: The buyer has significant cushion with $12.50 strike. Stock would need to fall ~14% from current $14.47 just to reach the strike, and another 17% to breakeven. The massive 3.29B gamma support at $12.50 suggests strong technical floor.

💡 Trading Ideas

🛡️ Conservative: Wait for SilverCrest Close Confirmation

Play: Stay on sidelines until Q1 2025 SilverCrest deal closes, then evaluate entry

Why this works:

- ⏰ Deal expected to close late Q1 2025 - reduces M&A execution risk

- 📊 Confirmation of smooth integration provides visibility on cost synergies

- 💎 Post-close pullback may offer better entry point than current elevated levels

- 🎯 Less risk of paying premium for deal uncertainty

- ⚖️ Can assess Las Chispas production contribution to 21M oz silver target before committing

Action plan:

- 👀 Monitor Q1 2025 closing announcements and integration updates

- 🎯 Look for entry on any post-close dip toward $13-$14 (near $12.50 gamma support)

- ✅ Confirm Q1 2025 earnings (May 7) show Las Chispas positive impact

- 📈 Consider stock position or longer-dated calls (September 2025+) after integration clarity

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

⚖️ Balanced: May 2025 Call Spread Targeting New Gold Vote

Play: Buy bull call spread around Q1 2025 shareholder votes

Structure: Buy $15 calls, Sell $17.50 calls (May 16, 2025 expiration)

Why this works:

- 🗳️ New Gold shareholder votes in Q1 2026 - May expiration captures vote anticipation buildup

- 📊 Defined risk spread ($2.50 wide = $250 max risk per spread)

- 🎯 Targets move from current $14.47 through $15 resistance to $17.50 gamma level

- ⏰ 6 months gives time for SilverCrest close and positive catalyst accumulation

- 💰 Cheaper than buying outright calls, limits downside risk

Estimated P&L:

- 💰 Net debit: ~$1.50-$1.80 per spread (pay $1.50-1.80, collect on short $17.50 calls)

- 📈 Max profit: ~$0.70-$1.00 per spread if CDE at/above $17.50 at May expiration (39-56% return)

- 📉 Max loss: $1.50-$1.80 per spread if CDE below $15 (defined and limited)

- 🎯 Breakeven: ~$16.50-$16.80

Entry timing: Wait for any consolidation or dip to $14.00-$14.50 for better risk/reward

Risk level: Moderate (defined risk) | Skill level: Intermediate

🚀 Aggressive: Mirror the Whale - January 2026 Calls (HIGH RISK!)

Play: Follow the unusual trade - buy $12.50 calls (January 16, 2026 expiration)

Why this could work:

- 🐋 Sophisticated institutional money just committed $1.4M to this exact position

- 📅 Perfect timing: Captures SilverCrest close (Q1 2025), New Gold votes (Q1 2026), and potential H1 2026 close

- 💎 Already $1.97 in-the-money with 14 months of time value

- 🛡️ Strike at massive 3.29B gamma support level = technical floor

- 🚀 Leverage to $3B EBITDA, $2B FCF 2026 transformation

- 🥇 Long duration benefits from sustained gold/silver bull market

Why this could blow up (SERIOUS RISKS):

- 💸 HIGH PREMIUM: $2.98 per contract = $298 per option, need move above $15.48 to profit

- 😱 Integration execution risk from $8.7B combined acquisitions - unprecedented scale for CDE

- ❌ New Gold shareholder vote could FAIL (need 66⅔% approval) = deal termination risk

- 📉 Extreme 52.1x PE valuation vulnerable to multiple compression on any disappointment

- 🌊 Gold price correction to $2,200-$2,400 would pressure all mining stocks

- ⏰ Time decay: Losing ~$0.15-$0.20 per month in theta even if stock stays flat

- 💰 Already up 72% YTD - some mean reversion risk

Estimated P&L:

- 💰 Entry cost: $2.98 per contract ($298 per option)

- 📈 Bull case profit at $20: $7.50 per contract (252% return) = $750 profit per option

- 🎯 Base case profit at $17: $4.50 per contract (151% return) = $450 profit per option

- 📉 Bear case loss at $13: Total loss of premium = -$298 per option (100% loss)

- 🔑 Breakeven: $15.48 ($12.50 strike + $2.98 premium)

Position sizing: If following this trade, use NO MORE than 2-5% of portfolio - the institutional player may have risk management tools and hedges you don't have!

Risk level: HIGH (100% loss possible) | Skill level: Advanced only

⚠️ WARNING: DO NOT attempt this trade unless you:

- Can afford to lose 100% of the premium ($298 per contract minimum)

- Understand the complex M&A timeline and integration risks

- Have conviction on gold/silver bull market continuing through 2025-2026

- Can hold through volatility from earnings, shareholder votes, and deal updates

- Recognize this is a 14-month bet requiring patience and risk tolerance

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🔨 Dual acquisition execution risk: Integrating $8.7B of acquisitions simultaneously (SilverCrest Q1 2025, New Gold H1 2026) creates operational complexity and distraction. Historical mining M&A typically sees 12-18 months of elevated costs. Any stumbles could trigger sharp selloff.

-

💎 Shareholder vote uncertainty: New Gold deal requires 66⅔% shareholder approval in Q1 2026 - failure would be catastrophic for thesis. Activist shareholders or competing bids could complicate vote. This is binary event risk.

-

📊 Extreme valuation leaves no room for error: Trading at 52.1x PE vs. 16.6x peer average after 208% YTD rally. Cantor Fitzgerald already downgraded to Neutral on valuation concerns. Any disappointment magnified.

-

🥇 Full exposure to precious metals prices: No hedging program means 100% exposure to gold/silver fluctuations. If Fed pivots hawkish or dollar strengthens, gold could correct 15-20% quickly. CDE would follow.

-

🏔️ Operational hazards inherent to mining: Pit wall failures, underground collapses, equipment breakdowns, weather disruptions, water management issues, labor challenges. Any major incident at Rochester or other key mine impacts production and stock price.

-

🌍 Geopolitical and regulatory risks: Mexican operations (Palmarejo, Las Chispas) face resource nationalism risk. Canadian mines post-merger add provincial regulations. US permitting averages 7-10 years limiting expansion.

-

🏦 Debt and financial leverage: Despite improvement to 0.9x net leverage, still carrying $351M long-term debt. Integration capex and acquisition financing could pressure balance sheet.

-

🎢 High volatility stock amplifies option risk: Mining stocks are volatile. CDE could easily swing 20-30% on earnings, deal news, or metals moves. Options buyers face rapid premium decay on adverse moves.

-

⏰ Long time horizon for thesis to play out: January 2026 expiration means 14 months of waiting. Multiple quarters of potential disappointment, market selloffs, or competitive developments. Requires patience and conviction.

🎯 The Bottom Line

Real talk: A sophisticated player just made a massive $1.4M bet on CDE's transformation story at a critical inflection point. With $1.7B SilverCrest closing in Q1 2025 and $7B New Gold merger pending H1 2026, CDE is executing the largest M&A strategy in its history. The winner? A combined entity producing 1.25M gold equivalent ounces with $3B EBITDA and $2B free cash flow. The risk? Trying to digest $8.7B of acquisitions while gold trades at all-time highs and the stock is up 72% YTD.

What this trade tells us:

- 🎯 Institutional conviction that CDE successfully executes dual acquisitions through 2025-2026

- 💰 Belief that gold stays elevated >$2,500 supporting premium mining valuations

- 🛡️ Strike at $12.50 (3.29B gamma support) shows buyer expects technical floor but upside to $17-$22

- ⏰ 14-month timeframe captures all major milestones without overpaying for excessive time value

- 📊 Smart money positioning ahead of multiple catalyst inflection points

If you own CDE:

- ✅ Consider taking some profits at these levels (up 72% YTD) - you've already won big

- 🎯 If holding for M&A story, set mental stop at $12.50 support (3.29B gamma) to protect gains

- 📊 Q1 2025 earnings (May 7) and SilverCrest close are next key tests

- 🚀 Bull case targets $18-$22 if all acquisitions execute smoothly and gold stays strong

- 🔔 Watch New Gold shareholder vote closely in Q1 2026 - FAILURE would be major negative

If you're watching from sidelines:

- ⏰ Late Q1 2025 - Watch for SilverCrest close announcement

- 🎯 Best entry: Pullback to $13.50-$14.00 support after any integration concerns or gold weakness

- ✅ Look for confirmation that Las Chispas integration proceeding smoothly in Q1 2025 earnings

- 📈 For long-term investors (6-12 months), M&A transformation story is compelling IF you believe in gold bull market

- ⚠️ Current 52.1x PE valuation requires perfect execution - high risk/high reward

If you're bearish:

- 🎯 First resistance is $15 (5.23B gamma) - watch for rejection there

- 📊 Elevated valuation (52.1x PE) after 72% rally vulnerable to compression

- ⚠️ Integration execution missteps or shareholder vote concerns would be triggers for selling

- 📉 Put spreads ($15/$12.50 or $14/$12.50) offer defined risk way to play downside

- 🥇 Gold correction below $2,400 would pressure entire mining sector including CDE

- ⏰ Be patient - wait for confirmation of integration challenges before shorting momentum

Mark your calendar - Key dates:

- 📅 Late Q1 2025 - SilverCrest/Las Chispas transaction expected close

- 📅 May 7, 2025 - Q1 2025 earnings after market close

- 📅 Q1 2026 - New Gold shareholder special meetings and votes

- 📅 H1 2026 - New Gold transaction expected close

- 📅 January 16, 2026 - Expiration of this $1.4M unusual call position

Final verdict: This trade is a sophisticated bet on CDE's M&A-driven transformation at a pivotal moment. The risk/reward is compelling IF you believe: (1) gold stays elevated >$2,500 through 2026, (2) management successfully integrates two major acquisitions worth $8.7B, (3) $3B EBITDA targets for 2026 are achievable, and (4) New Gold shareholders vote YES. However, at 52.1x PE after a 208% rally, there's ZERO margin for error. This is not a buy-and-forget play - it requires active monitoring of deal milestones, earnings execution, and precious metals trends. The institutional buyer likely has hedges and risk management we can't see. For retail traders, consider smaller position sizes, defined-risk spreads, or waiting for better entry points around support levels. This is a high-conviction, high-risk opportunity best suited for experienced options traders with strong views on precious metals and M&A execution.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 1,255x unusual score reflects this specific trade's size relative to recent history - it does not imply the trade will be profitable or that you should follow it. Mining stocks are highly volatile and sensitive to commodity price fluctuations. M&A transactions carry significant execution risk and may not close as expected. Always do your own research and consider consulting a licensed financial advisor before trading.

About Coeur Mining, Inc. (CDE): Coeur Mining Inc is a metals producer focused on mining precious minerals in the Americas, involved in the discovery and mining of gold and silver with a $9.11 billion market cap in the Gold and Silver Ores industry.