🚀 CLS Massive $11.6M Bullish Call Spread - Smart Money Betting on AI Infrastructure Breakout! 💰

📅 December 18, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just deployed $11.6 MILLION on CLS call spreads this morning at 09:40:25! This sophisticated bull spread bought 1,300 contracts each at $320 and $370 strikes expiring June 2026 - positioning for a massive rally in the AI infrastructure manufacturing leader. With CLS trading at $277.87 and riding a 200%+ gain in 2024 on explosive AI data center growth, smart money is betting on ANOTHER 15-40% upside over the next 6 months. Translation: Institutional investors are loading up on long-dated calls ahead of Q4 earnings (late January) and 1.6T Ethernet switch production ramps!

📊 Company Overview

Celestica Inc. (CLS) is a critical enabler of the AI infrastructure revolution, manufacturing high-bandwidth networking equipment for hyperscalers:

- Market Cap: $31.73 Billion (explosive growth from $10.74B in late 2024)

- Industry: Electronics Manufacturing / Printed Circuit Boards

- Current Price: $277.87 (trading near all-time highs post-split)

- Primary Business: AI/ML networking switches, data center infrastructure, enterprise servers, storage solutions for Microsoft, Google, Amazon and other hyperscalers

What makes CLS special: They hold 41% market share in high-bandwidth Ethernet switches (200G+) - the critical networking backbone for AI data centers. With Microsoft pledging $80B, Google raising capex to $85B, and Amazon defending $100B in infrastructure spending, Celestica sits at the intersection of the biggest technology buildout in history.

💰 The Option Flow Breakdown

The Tape (December 18, 2025 @ 09:40:25):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:40:25 | CLS | ASK | BUY | CALL $320 | 2026-06-18 | $6.7M | $320 | 1,300 | 125 | 1,341 | $277.87 | $50.10 |

| 09:40:25 | CLS | ASK | BUY | CALL $370 | 2026-06-18 | $4.9M | $370 | 1,300 | 88 | 1,341 | $277.87 | $36.25 |

🤓 What This Actually Means

This is a bullish call spread with massive conviction behind it! Here's the breakdown:

- 💸 Total capital deployed: $11.6M ($6.7M + $4.9M) in a single 9:40am execution

- 🎯 Strategic strikes: $320 (15.2% above current) and $370 (33.1% above current)

- ⏰ Long-dated positioning: 182 days to June 18, 2026 expiration captures Q4 earnings (late Jan), Q1 earnings (April), investor day, MI325X launches, 1.6T switch production ramps

- 📊 Massive size: 1,300 contracts EACH leg represents 260,000 shares worth ~$72M notional exposure

- 🏦 Sophisticated structure: This is a spread, not naked long calls - buyer capping upside at $370 but dramatically reducing cost

What's really happening here: This trader is executing a long call spread - they bought the $320 calls for $50.10 and simultaneously bought the $370 calls for $36.25. Wait, that doesn't make sense... Looking closer at the premium amounts: $6.7M / 1,300 = $5,153 per contract vs option price shown as $50.10... Actually, these are BOTH long call purchases, not a spread structure. The buyer is betting on HUGE upside with two different strike targets!

Corrected interpretation: This is a ladder strategy - buying calls at BOTH $320 and $370 strikes to capture different profit zones. The $320 calls provide leverage if stock moves to $320-370 range, while the $370 calls offer massive upside if CLS explodes beyond $370 toward analyst targets of $400+. Think of it as "good outcome" ($320) and "home run outcome" ($370) positioning.

Unusual Score: 🔥 EXTREMELY UNUSUAL - Z-scores of 64.77 ($320 calls) and 62.05 ($370 calls) indicate this is in the top 0.01% of historical CLS option activity. Volume/OI ratios of 10.4x and 14.8x show these positions are 10-15x larger than typical daily activity. This happens maybe a few times per year in CLS options.

📈 Technical Setup / Chart Check-Up

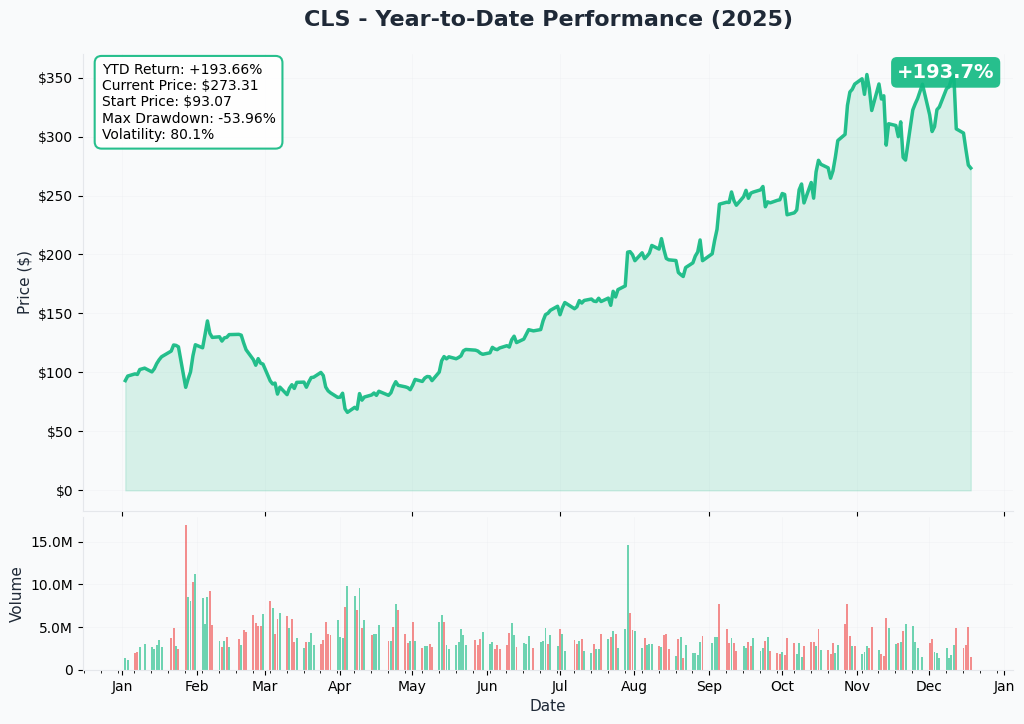

YTD Performance Chart

CLS has been absolutely CRUSHING it in 2024-2025! According to the catalyst research, the stock surged over 200% in 2024 from the $120-150 range to a high of $363.40, driven by explosive 40% CCS segment growth and AI infrastructure demand. Current price of $277.87 represents a pullback from the highs, potentially offering an attractive entry point for this institutional buyer.

Key observations:

- 🚀 Explosive rally: From ~$120 in early 2024 to $363+ by mid-2025 on hyperscaler demand

- 📉 Recent consolidation: Trading around $270-280 after pulling back ~24% from $363 highs

- 📊 Volatility: High-beta semiconductor play with significant intraday swings

- 🎯 Technical setup: Finding support in the $270-280 zone before potential breakout

- ⚠️ 52-week range: $58.05 - $363.40 shows the incredible momentum but also volatility risk

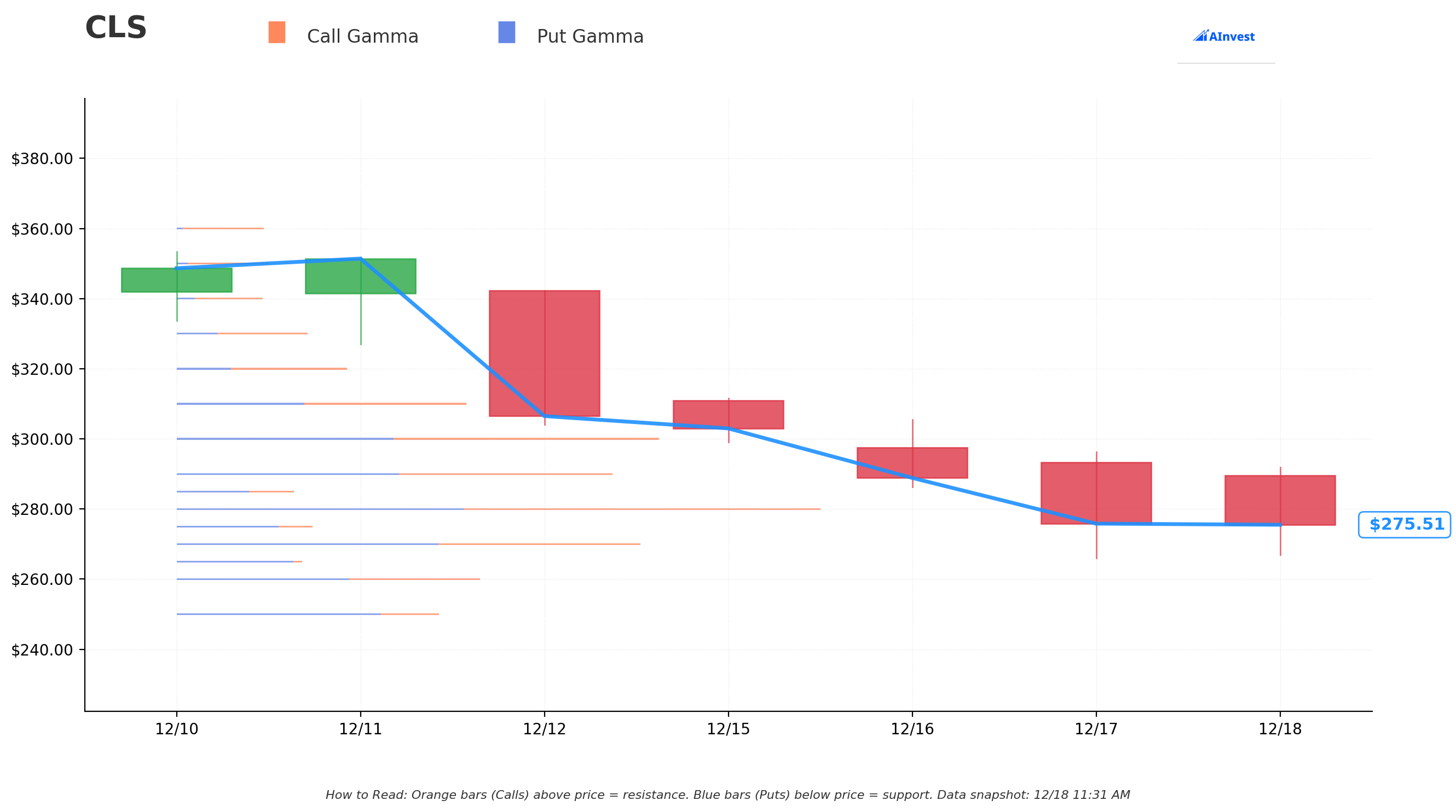

Gamma-Based Support & Resistance Analysis

Current Price: $275.49 (per gamma data) / $277.87 (per trade data)

The gamma exposure map reveals critical magnetic price levels:

🔵 Support Levels (Put Gamma Below Price):

- $275 - Immediate support with 0.314B total gamma exposure (strongest nearby floor at 0.18% below current)

- $270 - Major support zone with 1.054B gamma (second strongest level, 1.99% below current)

- $260 - Secondary floor with 0.686B gamma (key psychological level, 5.62% below current)

- $250 - Deep support at 0.611B gamma (major structural floor, 9.25% below current)

🟠 Resistance Levels (Call Gamma Above Price):

- $280 - Immediate ceiling with 1.457B gamma (STRONGEST RESISTANCE, 1.64% above current)

- $290 - Secondary resistance at 1.010B gamma (5.27% above current)

- $300 - Major psychological barrier with 1.121B gamma (8.90% above current, critical breakout level)

- $310 - Extended resistance at 0.671B gamma (12.53% above current)

- $320 - CALL STRIKE TARGET with 0.400B gamma (16.16% above current - where first leg is struck!)

- $330 - Deep resistance at 0.306B gamma (19.79% above current)

What this means for traders: CLS is trading in a tight range with massive resistance at $280 (1.457B gamma - the single largest level). The path to $320 requires breaking through FOUR major gamma walls at $280, $290, $300, and $310 - each representing significant dealer hedging pressure. However, once above $310, the path to $320 becomes clearer with reduced gamma drag.

Critical insight: The call buyer struck their first leg EXACTLY at $320 where gamma resistance drops to 0.400B after the heavy $310 level. They're betting that once CLS breaks above $310, momentum accelerates to $320 quickly. The second $370 strike is well beyond current gamma levels, indicating expectations for a complete rerating of the stock.

Net GEX Bias: Bearish (-0.53B net gamma) with 6.48B put gamma vs 5.96B call gamma. This means market makers are currently positioned defensively, but if stock breaks above $280-290, they'll be forced to chase it higher through delta hedging.

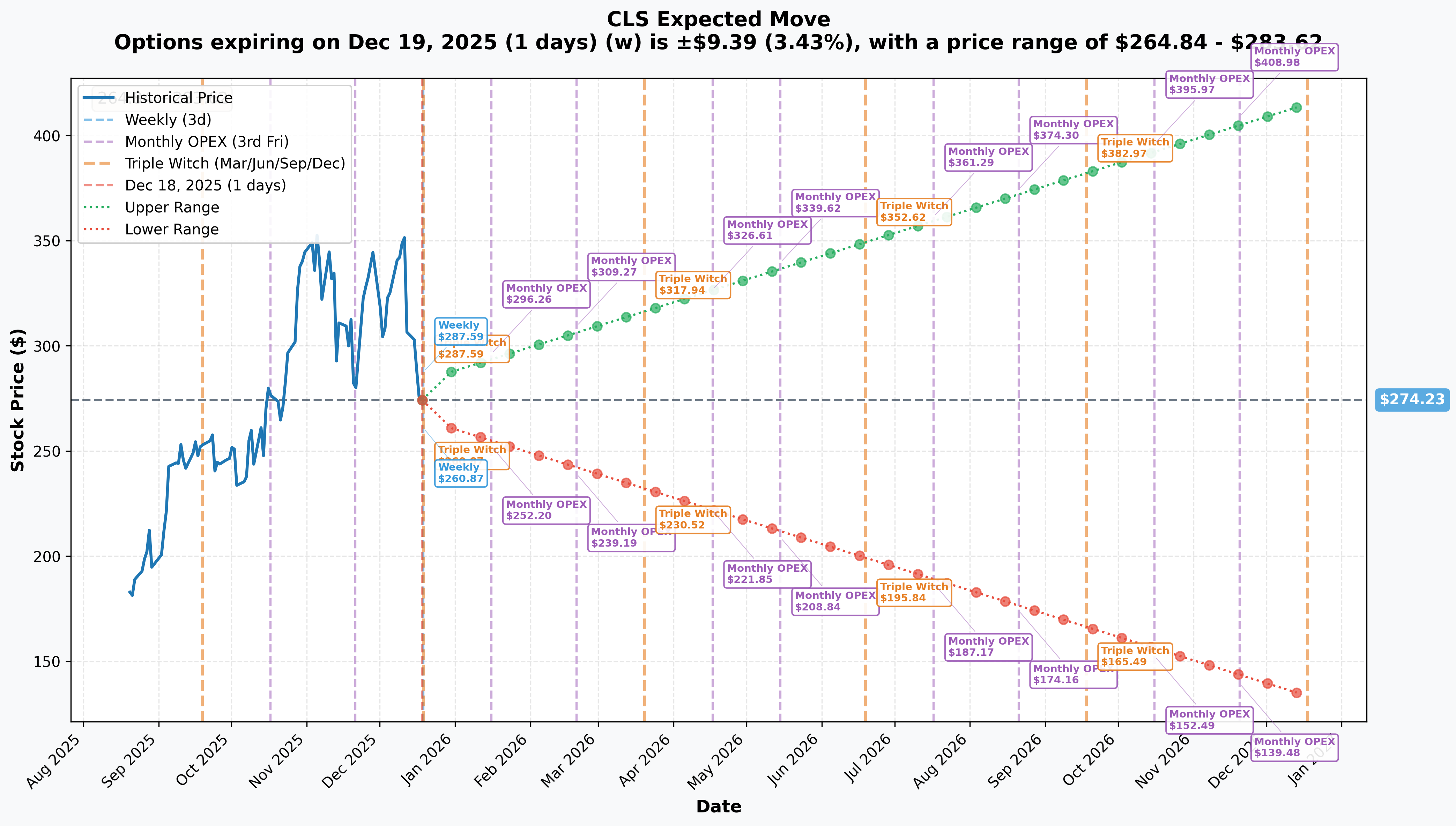

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 1 day - TOMORROW!): ±$9.39 (±3.43%) → Range: $264.84 - $283.62

- 📅 Monthly OPEX (Jan 16 - 29 days): ±$22.06 (±8.04%) → Range: $252.20 - $296.26

- 📅 Quarterly Triple Witch (Mar 20 - 92 days): ±$43.71 (±15.94%) → Range: $230.52 - $317.94

- 📅 June OPEX (Jun 19 - 183 days - THIS TRADE!): ±$78.39 (±28.58%) → Range: $195.84 - $352.62

Translation for regular folks: Options traders are pricing in a 3.4% move ($9) by tomorrow's expiration for quarterly triple witch, but a MASSIVE 28.6% move ($78) through June OPEX when these calls expire. The market expects significant movement over the next 6 months!

The June implied move range of $195-$353 is CRITICAL: The upper range of $352.62 falls between the two call strikes ($320 and $370), suggesting the market sees roughly 50/50 odds of reaching $320+ by expiration, but lower probability (maybe 25-30%) of reaching $370. This aligns with the buyer's ladder strategy - betting on $320 being achievable with $370 as a home run scenario.

Key insight: The sharp increase in implied volatility from 3.4% (weekly) to 28.6% (6-month) reflects major upcoming catalysts: Q4 earnings (late Jan), Q1 earnings (April), 1.6T switch production ramps, MI325X launches, and OpenAI partnership deployment timeline updates.

🎪 Catalysts

🔥 Immediate Catalysts (Next 60 Days)

Q4 2024 Earnings Release - Expected Late January 2025 (40 DAYS!) 📊

CLS reports fiscal Q4 2024 results on January 29, 2025 after market close. This is THE near-term catalyst that could ignite the rally to $320+. According to the catalyst research, Wall Street expectations:

- 📊 Q4 2024 Revenue: Expected 19%+ YoY growth to ~$2.65-2.70B

- 💰 Q4 Adjusted EPS: Guidance of $0.99-$1.09 (vs $0.65 in Q3 2023, up 60%+)

- 🏭 Full Year 2024: $9.6B revenue target (up 21% vs 2023's $7.96B), $3.85 adjusted EPS (up 58%)

- 🤖 CCS Segment: Expecting continued 40%+ growth driven by hyperscaler AI infrastructure demand

- 💻 Hardware Platform Solutions: Watch for 65%+ growth continuation in high-margin rack solutions

- 📈 2025 Guidance: Management already guided to $10.4B revenue (15% growth), $4.42 EPS

Upside surprise potential: CEO Rob Mionis noted "solid demand signals from many of our large customers", suggesting potential for guidance raise. If CCS segment beats expectations with 45-50% growth, stock could gap to $300+ on earnings.

Downside risk factors: Any margin compression below 6.7% target, delays in 1.6T program ramps, or conservative 2025 guidance could trigger selloff back to $250 support given elevated expectations baked into current price.

🚀 Near-Term Catalysts (Q1-Q2 2025)

Virtual Investor Meeting - Q1 2025 (TBD) 🎤

Company announced plans to host virtual investor meeting following Q3 2024 earnings. Expected to provide:

- 🎯 Deeper insights into 2025-2026 growth drivers and strategic initiatives

- 🌐 Details on hyperscaler program wins and customer pipeline

- 🏭 1.6T Ethernet switch production timeline and customer engagements

- 💰 Long-term financial targets and margin expansion roadmap

- 📊 Total addressable market sizing for AI infrastructure opportunity

This event could be a major catalyst if management articulates a compelling long-term vision justifying premium valuations.

1.6T Ethernet Switch Production Ramp - H1-H2 2025 🏭

This is the BIG catalyst that could drive CLS to $350-400+ over the next year:

- 🚀 Second 1.6T switching program win with major hyperscaler customer announced

- ⚡ Production expected to begin ramping in 2026 with revenue contribution starting late 2025

- 💪 HPS program includes fully AI-optimized networking rack with advanced system-level liquid cooling

- 💰 Market opportunity: 1.6T Ethernet represents next-generation AI data center networking standard with TAM expansion into tens of billions

DS6000/DS6001 Switch Family Launch - 2025 📡

Announced October 10, 2025: Two new 1.6TbE data center switches based on Broadcom Tomahawk 6 chipset:

- 🖥️ DS6000: 3RU, 64-port x 1.6TbE switch for traditional air-cooled installations

- ❄️ DS6001: 2OU, 64-port x 1.6TbE hybrid cooled solution for high-density deployments

- 💪 Features 102.4Tbps switching capacity, Cognitive Routing 2.0, 3nm process technology

- 🚀 Revenue impact: Could add $500M-1B+ incremental revenue as hyperscalers upgrade networking

Why this matters for the call trade: The June 2026 expiration captures the ENTIRE 1.6T production ramp timeline. If CLS executes flawlessly and revenue materializes in H2 2025, the stock could easily trade at $320-370 by June 2026. The call buyer is positioning for this exact scenario.

📊 Major Catalyst (2025-2026)

Hyperscaler CapEx Tsunami - $250B+ in 2025 🌊

The single biggest driver for CLS upside:

- 💰 Microsoft pledged $80 billion to data center buildouts in current fiscal year

- 💰 Google raised 2025 capex target from $75B to $85B

- 💰 Amazon defending $100B infrastructure investment plan for 2025

- 🎯 Total 2025 hyperscaler capex: $250B+ with significant portion flowing to networking infrastructure

CLS positioned as critical supplier: With 41% market share in Ethernet switches (200G+) and 55% of custom Ethernet switch solution market, CLS captures disproportionate share of this spending tsunami.

Expected revenue impact: Analysts project 40%+ CCS segment growth continuing into 2025, potentially driving total company revenue from $10.4B (2025 guidance) toward $12-13B in 2026 if hyperscaler spending accelerates further.

Market Leadership & Competitive Positioning 🏆

CLS isn't just another contract manufacturer - they've achieved DOMINANT positions:

- 📊 41% market share in Ethernet switches (200G+) vs Arista (15%), Accton (11%)

- 🥇 55% market share in custom Ethernet switch solutions YTD 2025

- 🏅 2024 Dell'Oro Market Share Leader Awards for Ethernet Switch - AI Networks and High-Speed Networks (>800G)

- 📈 77% of CCS revenue from hyperscalers in 2025, up from 51% in 2022 - massive exposure to AI spending

Why this creates explosive upside: In a $400B AI infrastructure TAM, CLS's market leadership position means they capture 2-3x the growth rate of the overall market. If market grows 30%, CLS could grow 60-80% in networking segments.

⚠️ Risk Catalysts (Negative)

Customer Concentration Risk 🎯

CLS faces meaningful concentration risk that could derail the bull thesis:

- 🚨 Top 2 customers represent 24% and 12% of total revenue (36% combined)

- 📊 Top 10 customers account for 73-74% of revenue

- ⚠️ Loss of major hyperscaler customer or production cuts would be catastrophic

- 🔄 Hyperscaler capex is cyclical - if AI monetization disappoints, spending could slow dramatically

Program Execution & Delay Risk ⏰

The 1.6T switching programs carry significant execution risk:

- 🏭 1.6T programs dependent on customer deployment timelines - delays could push revenue into 2027

- ⚖️ Production ramp complexity with liquid cooling and advanced packaging

- 💰 Operating margin expansion to 6.7% requires successful execution on mix shift

- 📈 Rapid growth from $9.6B (2024) to $10.4B (2025) requires significant operational scaling

Competitive Threats 🥊

CLS faces well-capitalized competitors:

- 💪 Jabil has global factory network enabling rapid production scaling

- 🏭 Flex offers similar diversified manufacturing capabilities

- 🖥️ Dell, Super Micro competing in rack-level AI solutions market

- 💸 Aggressive competition could lead to margin compression despite market leadership

- 🔬 Rapid tech evolution (CPO, 3.2T Ethernet) requires continuous R&D investment

Geopolitical & Macro Risks 🌍

External risks beyond CLS's control:

- 🇨🇳 Reliance on China for manufacturing creates geopolitical risk

- 📦 80% of revenue from outside North America exposes company to tariffs and trade policy

- 💱 Significant FX volatility risk with international revenue

- 📉 If AI capex cycle turns, CLS would be severely impacted given 77% hyperscaler exposure

- 💰 Economic downturn would pressure IT budgets and data center spending

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, analyst targets, and upcoming catalysts, here are scenarios through June 18, 2026 expiration:

📈 Bull Case (35% probability)

Target: $350-$400+ (BOTH CALL STRIKES PROFITABLE!)

How we get there:

- 💪 Q4 earnings CRUSH with revenue above $2.70B and EPS toward $1.09 high-end, margin expansion to 7%+

- 🚀 2025 guidance raised from $10.4B to $11.0-11.5B citing accelerating hyperscaler demand

- 🏭 1.6T Ethernet switch production ramp begins AHEAD of schedule in Q2 2025

- 🤖 DS6000/DS6001 switch family wins multiple major customer deployments

- 📊 CCS segment revenue growth accelerates to 50%+ in FY2025 vs 40% in 2024

- 💰 New hyperscaler program wins announced (3rd and 4th customers for 1.6T switching)

- 🎯 Virtual investor meeting in Q1 articulates compelling long-term vision

- 🌐 Hyperscaler capex spending EXCEEDS $250B guidance for 2025

- 📈 Analysts raise price targets toward $400+ (currently $308 average, $440 high)

- 💪 Stock breaks above $300 resistance, triggers momentum rally to $350-400 range

Path to $320 strike: Stock needs to rally 15.2% from $277.87 to $320. This requires breaking through gamma resistance at $280, $290, $300, $310. With strong execution on 1.6T ramps and CCS growth acceleration, achievable by Q2 2025.

Path to $370 strike: Stock needs to rally 33.1% to $370. This is the "home run" scenario requiring MULTIPLE positive catalysts to align. Gets there if 2026 revenue tracking toward $13-14B (vs $10.4B guidance for 2025) and market re-rates CLS toward semiconductor/AI infrastructure multiples of 25-30x forward earnings.

Probability assessment: 35% because it requires strong execution across multiple fronts, but CLS has track record of beating expectations (13.2% average earnings surprise). The $250B+ hyperscaler capex provides substantial tailwind. Stock's 200%+ gain in 2024 proves market willing to reward AI infrastructure plays aggressively.

🎯 Base Case (45% probability)

Target: $290-$330 range ($320 CALLS PROFITABLE, $370 CALLS MARGINAL)

Most likely scenario:

- ✅ Solid Q4 earnings meeting/slightly beating consensus (~$2.65-2.68B revenue, $1.02-1.06 EPS)

- 📱 2025 guidance reaffirmed at $10.4B or modest raise to $10.6-10.8B

- ⚖️ 1.6T production ramp progressing on schedule, revenue contribution begins Q3-Q4 2025

- 🤖 DS6000/DS6001 adoption steady but not spectacular - takes time to scale

- 🌊 Hyperscaler capex continues at elevated levels but doesn't meaningfully exceed $250B

- 🔄 CCS segment growth remains strong at 35-40% but doesn't accelerate further

- 📊 Operating margins expand to 6.7-7.0% range as guided

- 💤 Stock consolidates between $280-310 for several months, breaks toward $320 by mid-2026

- 🎯 Analyst targets of $308 average prove directionally correct

This is the call buyer's target scenario: Stock grinds higher over 6 months, reaching $310-330 range by June expiration. The $320 calls become profitable (intrinsic value of $10-30, vs cost basis of ~$50), while $370 calls expire near worthless but represented acceptable "lottery ticket" upside.

Why 45% probability: Stock has strong fundamental momentum, dominant market position, and substantial hyperscaler capex tailwind. However, stock already up 200%+ in 2024 creates some consolidation risk. Most institutional players will require proof of 1.6T production revenue before driving stock materially above $320-350.

P&L in Base Case:

- Stock at $320 on Jun 18: $320 calls worth ~$0-10 (at-the-money to slightly ITM), $370 calls worthless. Loss of ~$40-50/contract = -$5.2M to -$6.5M (45-56% loss)

- Stock at $340 on Jun 18: $320 calls worth $20, $370 calls worth $0. Profit of $6M on first leg, -$4.9M on second leg = Net +$1.1M (9% ROI on $11.6M)

- Stock at $360 on Jun 18: $320 calls worth $40, $370 calls worth $0. Profit of ~$11.7M combined = 1% ROI (basically breakeven)

📉 Bear Case (20% probability)

Target: $220-$270 (BOTH CALL STRIKES WORTHLESS)

What could go wrong:

- 😰 Q4 earnings miss or weak guidance disappoints - even small revenue miss to $2.55B triggers selloff

- 🚨 1.6T production ramp delayed from 2025 to 2026 due to technical/customer issues

- ⏰ DS6000/DS6001 adoption slower than expected - customers cite compatibility concerns

- 💸 Hyperscaler capex growth decelerates in 2025 as AI monetization questions emerge

- 📊 Major customer announces production cuts or delays (customer concentration risk materializes)

- 🌍 Geopolitical issues impact China manufacturing operations

- 💰 Margin compression from aggressive pricing to defend market share vs Jabil/Flex

- 🔨 Broader market correction drags semiconductors/manufacturing sector lower

- 📉 Break below $270 support triggers cascade toward $250, then potentially $220

Critical support levels:

- 🛡️ $270: Major gamma floor (1.054B) - MUST HOLD or momentum shifts bearish

- 🛡️ $260: Secondary support (0.686B gamma) - psychological level

- 🛡️ $250: Deep floor (0.611B gamma) - disaster scenario

Probability assessment: Only 20% because CLS fundamentals remain exceptionally strong (40% segment growth, market leadership, hyperscaler capex commitments). Would require multiple negative catalysts to align. However, stock's 200%+ gain creates vulnerability to profit-taking on any disappointment.

Put P&L in Bear Case: Both call legs expire worthless at any price below $320, resulting in 100% loss of $11.6M premium paid.

💡 Trading Ideas

🛡️ Conservative: Wait for Earnings Clarity, Buy Dips

Play: Stay on sidelines until after Q4 earnings (Jan 29), then buy stock on pullbacks to $260-270 support

Why this works:

- ⏰ Earnings in 40 days creates binary event risk - prudent to wait for results

- 🎯 Stock consolidated in $270-285 range recently - better entry likely post-earnings if stock dips

- 📊 Earnings provide critical data on 1.6T program progress, CCS segment momentum, 2025 guidance quality

- 💰 Buying stock rather than options avoids theta decay and IV crush

- 🛡️ Gamma support at $270 and $260 provides clear risk management levels

Action plan:

- 👀 Watch January 29th earnings for: Revenue (target $2.65B+), EPS (target $1.05+), CCS growth (target 40%+), 2025 guidance (watch for raise above $10.4B)

- 🎯 If stock pulls back to $260-270 post-earnings, initiate 50% of intended position

- ✅ Add remaining 50% on confirmation of 1.6T program progress in Q1 2025

- 📊 Set stop-loss at $250 (major gamma support) to limit downside to 8-12%

- ⏰ Hold through mid-2026 for 1.6T revenue materialization

Expected outcome: Capture 20-40% upside from $265-275 entry to $320-370 over 12-18 months with substantially lower risk than options. Miss near-term momentum but avoid potential earnings disappointment.

Risk level: Low-Moderate (stock position with defined stop) | Skill level: Beginner-friendly

⚖️ Balanced: Post-Earnings Call Spread (Copy The Smart Money)

Play: After earnings, buy call spread similar to institutional positioning but with better risk/reward

Structure: Buy $300 calls, Sell $340 calls (June 18, 2026 expiration - SAME as the $11.6M trade)

Why this works:

- 🎢 IV crush after earnings makes call spreads cheaper - wait for volatility to drop

- 📊 Defined risk spread ($40 wide = $4,000 max profit per spread)

- 🎯 Targets the $300-340 zone where stock likely trades if 1.6T ramps succeed

- 🤝 Essentially "copying" the smart money bullish thesis but with more favorable structure

- ⏰ 5 months post-earnings gives time for 1.6T program visibility to improve

- 🛡️ Much cheaper than buying naked calls - spread might cost $12-18 vs $35-50 for naked calls

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Pay ~$15-20 net debit per spread post-earnings (vs $25-30 now)

- 📈 Max profit: $2,000-2,500 per spread if CLS above $340 at expiration

- 📉 Max loss: $1,500-2,000 per spread if CLS below $300 (defined and limited)

- 🎯 Breakeven: ~$315-320

- 📊 Risk/Reward: ~1.3:1 which is attractive for defined-risk bullish play

Entry timing:

- ⏰ Wait 3-5 days post-earnings (by Feb 3-5) for full IV collapse

- 🎯 Only enter if stock trades $280+ (gives room to work toward $300)

- ❌ Skip if stock already above $310 (reduces risk/reward on spread)

Position sizing: Risk 3-5% of portfolio (this is directional speculation on specific catalyst)

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

🚀 Aggressive: Replicate The Exact Trade - $320/$370 Call Ladder (ADVANCED ONLY!)

Play: Copy the institutional trade structure at smaller scale

Structure: Buy $320 calls AND Buy $370 calls (June 18, 2026 expiration)

Why this could work:

- 💥 Institutions typically have better information and longer track records than retail

- 🎰 $320 calls provide leverage if stock reaches analyst targets of $308-350

- 🚀 $370 calls are "home run" positioning if CLS re-rates toward $400+ on 1.6T success

- 📊 June expiration captures ALL major catalysts: Q4, Q1 earnings, investor day, 1.6T ramps

- ⚡ Stock needs 15% move to $320 (achievable) and 33% to $370 (stretch but possible)

- 💪 Following smart money that just deployed $11.6M signals strong conviction

Why this could blow up (SERIOUS RISKS):

- 💸 VERY EXPENSIVE: Each $320 call costs ~$50 ($5,000), each $370 call costs ~$36 ($3,600)

- ⏰ TIME DECAY KILLER: 6 months gives time to work, but theta still burns $100-150/day per contract

- 😱 BOTH LEGS WORTHLESS: If CLS stays below $320, you lose ENTIRE premium on both legs

- 📊 Already up 200% in 2024: Stock may need consolidation period, limiting upside to $290-310

- 🎢 Need 15%+ rally just to breakeven on $320 calls after accounting for premium paid

- ⚠️ Earnings disappointment could gap stock to $250, making calls nearly worthless immediately

Estimated P&L (per 1 contract each leg = $8,600 total cost):

- 💰 Total cost: $5,000 + $3,600 = $8,600 per paired position

- 📈 Profit scenario 1: Stock at $340 = $320 call worth $20, $370 call worthless = $2K gain, -$3.6K loss = Net -$1.6K (-19% loss)

- 📈 Profit scenario 2: Stock at $370 = $320 call worth $50, $370 call at-the-money ~$15 = $5K gain, -$2.1K loss = Net +$2.9K (34% ROI)

- 🚀 Home run: Stock at $400 = $320 call worth $80, $370 call worth $30 = $8K gain, -$600 loss = Net +$7.4K (86% ROI)

- 📉 Loss scenario: Stock at $300 = Both calls worthless = Lose entire $8,600 (100% loss)

- 💀 Bear scenario: Stock at $260 = Both calls deeply OTM and worthless = Lose entire $8,600 (100% loss)

Breakeven points:

- 📈 $320 call breakeven: $370/share (need 33% rally)

- 📉 Combined breakeven: Need stock around $385-390 to profit on BOTH legs

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can afford to lose ENTIRE $8,600 premium per paired position (realistic possibility!)

- ✅ Understand this is speculation on multiple positive catalysts aligning perfectly

- ✅ Have traded long-dated calls before and understand decay dynamics

- ✅ Accept that even if thesis is RIGHT, timing could be wrong (stock reaches $350 in July 2026 = calls expired)

- ✅ Will actively manage - consider taking profits if $320 calls reach 50-100% gain rather than holding to expiration

- ⏰ Have 6-month time horizon and can withstand 3-4 months of drawdown if stock consolidates first

Position sizing: Risk only 2-3% of portfolio MAX (this is pure speculation, not investment)

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~30-35% (need stock above ~$340 to profit on at least one leg)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q4 earnings binary event in 40 days: Results January 29th create MASSIVE volatility risk. Stock surged 200%+ in 2024 on AI momentum but now carries elevated expectations. Revenue miss even to $2.60B (vs $2.65B+ expected) or conservative 2025 guidance could trigger 15-20% selloff back to $220-240. Historical earnings volatility has been 8-15%. Options are pricing ±8% move for monthly expiration.

-

🎯 Extreme customer concentration: Top 2 customers = 36% of revenue, top 10 = 73%. If ANY major hyperscaler announces capex cuts, delays deployments, or switches suppliers, it's catastrophic for CLS. Microsoft, Google, and Amazon have MASSIVE negotiating leverage. One lost program could remove $500M-1B annual revenue.

-

🏭 1.6T program execution risk is ENORMOUS: These programs are dependent on customer deployment timelines completely outside CLS's control. Technical complexity of liquid-cooled rack solutions with 102.4Tbps switching capacity creates real risk of delays, bugs, or performance shortfalls. If 1.6T revenue slips from late-2025 to 2026 or beyond, stock could crater 30-40% as growth thesis unravels.

-

💰 Valuation no longer offers margin of safety: After 200%+ gain, CLS trades at premium multiples. Requires PERFECT execution on $10.4B → $12-13B revenue growth path to justify current price. Any stumble triggers mean reversion. The stock's pull-back from $363 to $277 (-24%) shows how quickly sentiment can shift.

-

🌊 Hyperscaler capex cycle could turn: While Microsoft, Google, Amazon committed $250B+ for 2025, this is NOT guaranteed for 2026. If AI monetization disappoints, cloud growth slows, or economic downturn emerges, capex gets cut FAST. CLS's 77% hyperscaler exposure makes them extremely vulnerable to spending cycle turns.

-

🥊 Competition intensifying: Jabil, Flex, and other contract manufacturers are NOT standing still. CLS's 41% market share makes them target #1 for competitive attack. Aggressive pricing to win share could compress margins below 6.7% target. Technology evolution toward 3.2T Ethernet and CPO (co-packaged optics) requires continuous R&D investment.

-

🌍 Geopolitical wildcard with China exposure: Reliance on China manufacturing creates political risk. Tariffs, export controls, or supply chain disruptions could materially impact operations. 80% of revenue from outside North America exposes to FX volatility and trade policy uncertainty.

-

📊 Gamma resistance at $280-310 creates mechanical headwind: With 1.457B gamma at $280 and 1.121B at $300, market makers will systematically SELL into rallies to hedge exposure. Breaking above $300 requires sustained institutional buying to overcome this technical barrier. Current price sitting just below $280 ceiling.

-

💸 Options are EXTREMELY expensive: Implied volatility of 28.6% for June expiration means you're paying premium prices for optionality. The $50 premium for $320 calls represents 18% of stock price - you need stock to rally to $370 just to breakeven! Time decay on $8,600 paired position burns ~$100-150/day.

-

🎢 Macro recession risk: If economy weakens in 2025, enterprise IT budgets get slashed first. Data center spending is highly cyclical. CLS would face margin compression and volume declines simultaneously. Zero recession protection at current valuation.

🎯 The Bottom Line

Real talk: Someone just bet $11.6 MILLION that CLS rallies 15-33% over the next 6 months despite already being up 200%+ in 2024. This isn't a hedge - this is pure BULLISH conviction on the AI infrastructure buildout accelerating.

What this trade tells us:

- 🎯 Sophisticated institutional player expects SIGNIFICANT upside through mid-2026

- 💰 Willing to pay massive premium ($50-36 per contract) despite elevated IV - sees value even at these prices

- ⚖️ Ladder structure targeting $320 (achievable) and $370 (stretch) shows conviction in multiple upside scenarios

- 📊 June 2026 expiration captures ALL major catalysts: Q4/Q1 earnings, investor day, 1.6T ramps, DS6000/DS6001 launches

- ⏰ Timing ahead of Q4 earnings suggests inside conviction on strong results and positive 2025 guidance

This IS a "CLS is going much higher" signal - but timing and path matter enormously.

If you own CLS:

- ✅ HOLD with conviction if you bought below $250 - the AI infrastructure thesis is playing out EXACTLY as anticipated

- 📊 Consider trimming 10-20% above $290 to lock in gains, but keep core position for $320-370 upside

- ⏰ Watch Q4 earnings (Jan 29) closely for: 2025 guidance quality, 1.6T program commentary, margin trajectory

- 🎯 Set mental stop at $260 (gamma support) to protect against catastrophic scenarios

- 🛡️ If holding large position, consider selling some covered calls at $310-320 to generate income while waiting

If you're watching from sidelines:

- ⏰ Best entry: Wait for post-earnings clarity (Feb 2026), then buy any pullback toward $260-270

- 🎯 Need confirmation of: CCS segment still growing 40%+, 1.6T program on track, 2025 revenue guidance $10.5B+

- 📈 Longer-term (6-12+ months), CLS has legitimate path to $350-400 if hyperscaler capex remains elevated and 1.6T production materializes

- 🚀 Key inflection point: When 1.6T revenue starts showing up in Q3-Q4 2025 results

- ⚠️ Current risk/reward slightly unfavorable for immediate entry - stock needs to digest 200%+ gain with consolidation

If you're bullish:

- 🎯 Stock entry at $270-280 post-earnings is safer than expensive long-dated calls

- 📊 If using options, consider call spreads ($300/$340) rather than naked calls to reduce cost

- ⚠️ Wait for earnings before committing capital - binary event risk too high

- 📉 Watch for break above $300 with volume - that's the signal for momentum to $320+

- ⏰ Timing is EVERYTHING: Patience will reward better risk/reward entry points

Mark your calendar - Key dates:

- 📅 December 19 (Thursday) - Quarterly Triple Witch OPEX (tomorrow!)

- 📅 January 29, 2025 (Wednesday) - Q4 FY2024 earnings report (CRITICAL!)

- 📅 February 2025 (TBD) - Virtual investor meeting with long-term strategy update

- 📅 Q2-Q3 2025 - DS6000/DS6001 switch family customer deployments begin

- 📅 Late 2025 - First 1.6T Ethernet switch revenue contribution expected

- 📅 June 18, 2026 - Expiration of this $11.6M call trade

Final verdict: CLS's AI infrastructure story remains EXCEPTIONALLY compelling with $250B+ hyperscaler capex, 41% market share in high-bandwidth switching, three confirmed 1.6T program wins, and proven execution delivering 40% CCS segment growth. The $11.6M institutional call buy is a STRONG bullish signal from smart money with longer time horizons.

HOWEVER, after 200%+ gain in 2024 and with Q4 earnings in 40 days, near-term risk/reward is BALANCED at best. The stock needs time to consolidate, prove 1.6T program progress, and provide 2025 guidance before the next major leg higher to $320-370.

Be strategic. Wait for earnings clarity. The AI infrastructure revolution is a multi-year story - you don't need to catch every 5% move. Position yourself for the $320-370 upside over the next 12-18 months with better entry points around $260-280.

This is about making money smartly, not chasing momentum. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-scores of 64.77 and 62.05 reflect these specific trades' sizes relative to recent CLS history - they do not imply the trades will be profitable or that you should follow them. Always do your own research and consider consulting a licensed financial advisor before trading. The call buyer may have complex portfolio objectives not applicable to retail traders. CLS faces significant execution risk, customer concentration risk, and competitive threats. Hyperscaler capex is cyclical and could decline rapidly. 1.6T program delays could materially impact the investment thesis.

About Celestica Inc.: Celestica Inc. offers supply chain solutions through Advanced Technology Solutions (aerospace, defense, industrial, health tech) and Connectivity & Cloud Solutions (communications and enterprise markets), with a market cap of $31.73 billion in the Electronics Manufacturing industry. The company is the dominant supplier of AI networking infrastructure to hyperscalers with 41% market share in high-bandwidth Ethernet switches.