🚀 CLS: $5.7M Diagonal Call Spread Signals AI Infrastructure Breakout Play!

📅 December 22, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $5.7 MILLION on a sophisticated CLS diagonal call spread this morning! This isn't some random retail YOLO - this is a calculated institutional bet that Celestica (the AI server manufacturing powerhouse) is headed higher through mid-2026, with $300M+ in total premium positioning the stock for a breakout from current levels around $301. Let's decode what the smart money is seeing... 👀

💰 The Option Flow Breakdown

📊 What Just Happened

Today's unusual activity shows $5.7M in total premium flowing into CLS options with a clear bullish structure:

| Time | Type | Exp | Strike | Volume | Premium | Chart |

|---|---|---|---|---|---|---|

| 09:44:34 | 🟢 BUY CALL | 2026-03-20 | $350 | 1,000 | $2.70M | Chart |

| 09:44:34 | 🔴 SELL CALL | 2026-06-18 | $420 | 1,000 | $3.00M | Chart |

Total Premium Deployed: $5.70M (net cost: -$300K after premium collected)

🤓 What This Actually Means

This is a diagonal call spread - a sophisticated strategy that combines:

✅ Long March 2026 $350 calls ($2.7M) - Bullish bet that CLS trades above $350 by Q1 2026 ❌ Short June 2026 $420 calls ($3.0M) - Collecting premium by selling upside at $420

Translation for us regular folks: Someone with deep pockets believes CLS is heading to $350+ by March earnings (16% upside from $301), but wants to cap gains at $420 (39% upside) while collecting $3M in premium to fund the position. This creates a synthetic "sweet spot" where maximum profit occurs if CLS trades between $350-$420 through June 2026.

Why this setup is bullish:

- 🎯 They're risking net $300K to make potentially $70M if CLS hits $420

- 📅 March expiration aligns with Q1 2025 earnings (April 24-25) catalyst

- 🐋 $2.7M call purchase shows conviction in AI infrastructure thesis

- 💡 Diagonal structure suggests they expect steady climb, not a spike

📈 Technical Setup / Chart Check-Up

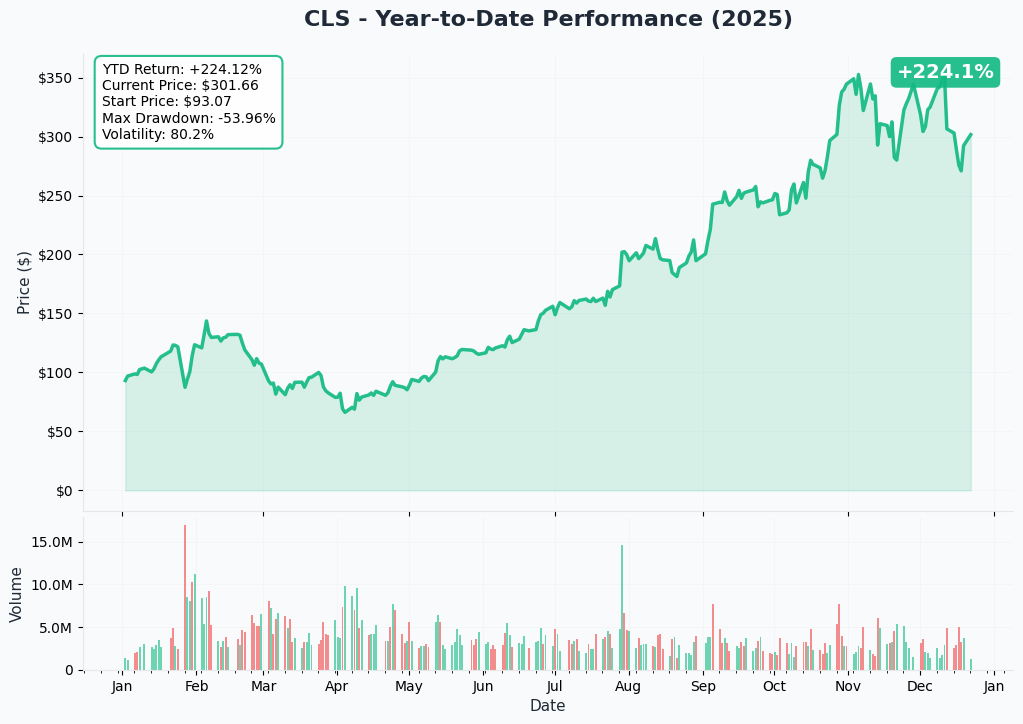

YTD Chart Analysis

Celestica has been on an absolute tear in 2024, surging 360% over the past year from the $80s to current levels around $301. The stock has demonstrated strong momentum with 165.87% YTD returns as market cap exploded from $4.04B to $10.74B.

Current price action shows consolidation around $300 after the recent parabolic move, with institutional ownership at 75% of shares providing strong support. This diagonal spread suggests the next leg higher toward $350-$420 is in play.

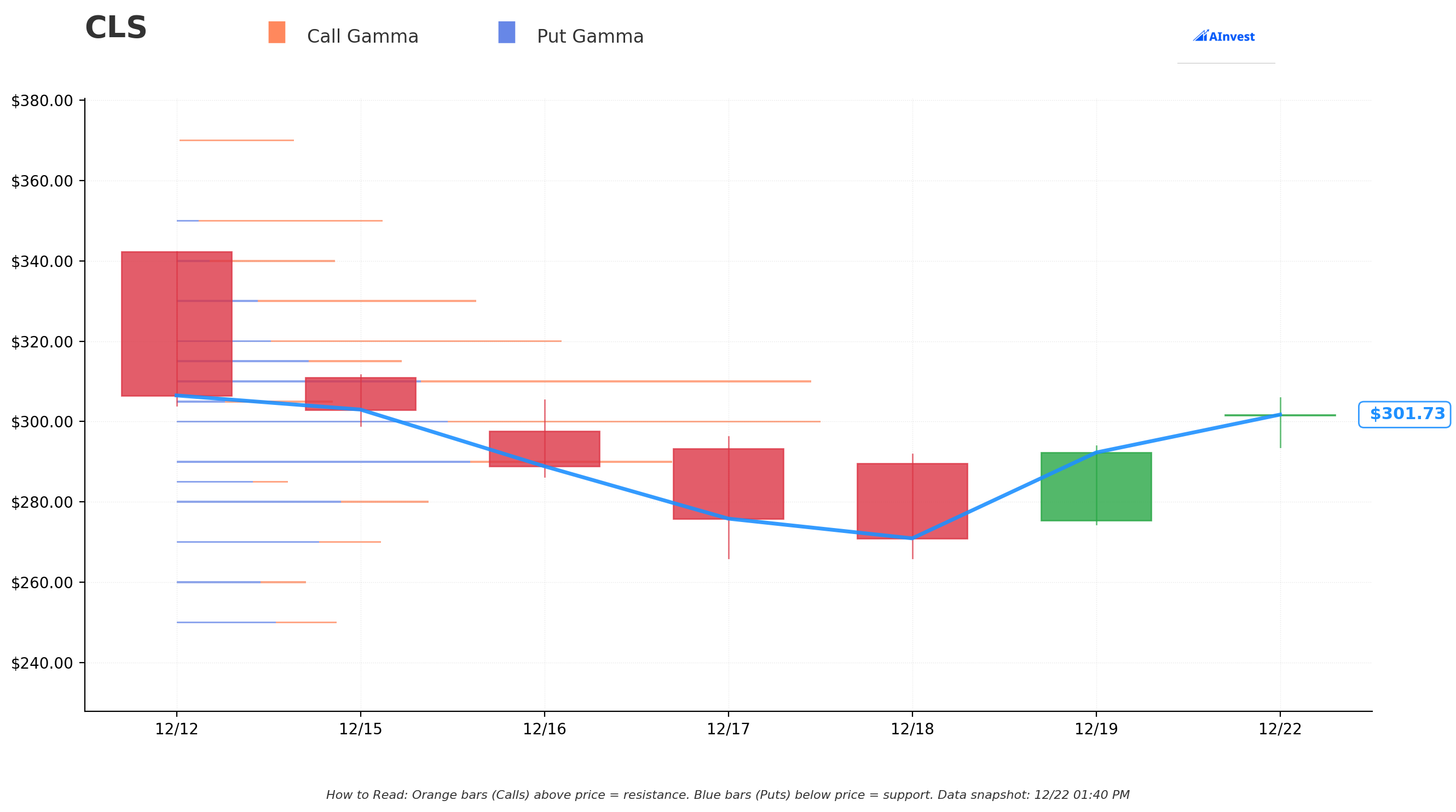

📊 Gamma-Based Support & Resistance Analysis

Gamma positioning reveals critical battle zones:

🛡️ Support Levels (Put Gamma Protection):

- $300 - Strongest support (1.10 total GEX, just 0.47% away) - This is THE line in the sand

- $290 - Secondary support (0.85 GEX, -3.8% away) - First major pullback target

- $280 - Strong put base (0.43 GEX, -7.1% away) - Deep retest zone

- $270 - Fallback support (0.35 GEX, -10.4% away) - Bear case floor

- $250 - Ultimate support (0.27 GEX, -17.1% away) - Major breakdown level

🚀 Resistance Levels (Call Gamma Walls):

- $310 - Immediate resistance (1.09 total GEX, +2.8% away) - First breakout target

- $315 - Minor resistance (0.39 GEX, +4.5% away) - Stepping stone

- $320 - Moderate wall (0.66 GEX, +6.2% away) - Key psychological level

- $330 - Major resistance (0.50 GEX, +9.5% away) - Big options cluster

- $350 - Heavy call wall (0.35 GEX, +16.1% away) - Target of today's long call position

Net GEX Bias: BULLISH - Call gamma (5.55) exceeds put gamma (4.35) by 27%, suggesting dealers are positioned for upside and will need to chase rallies.

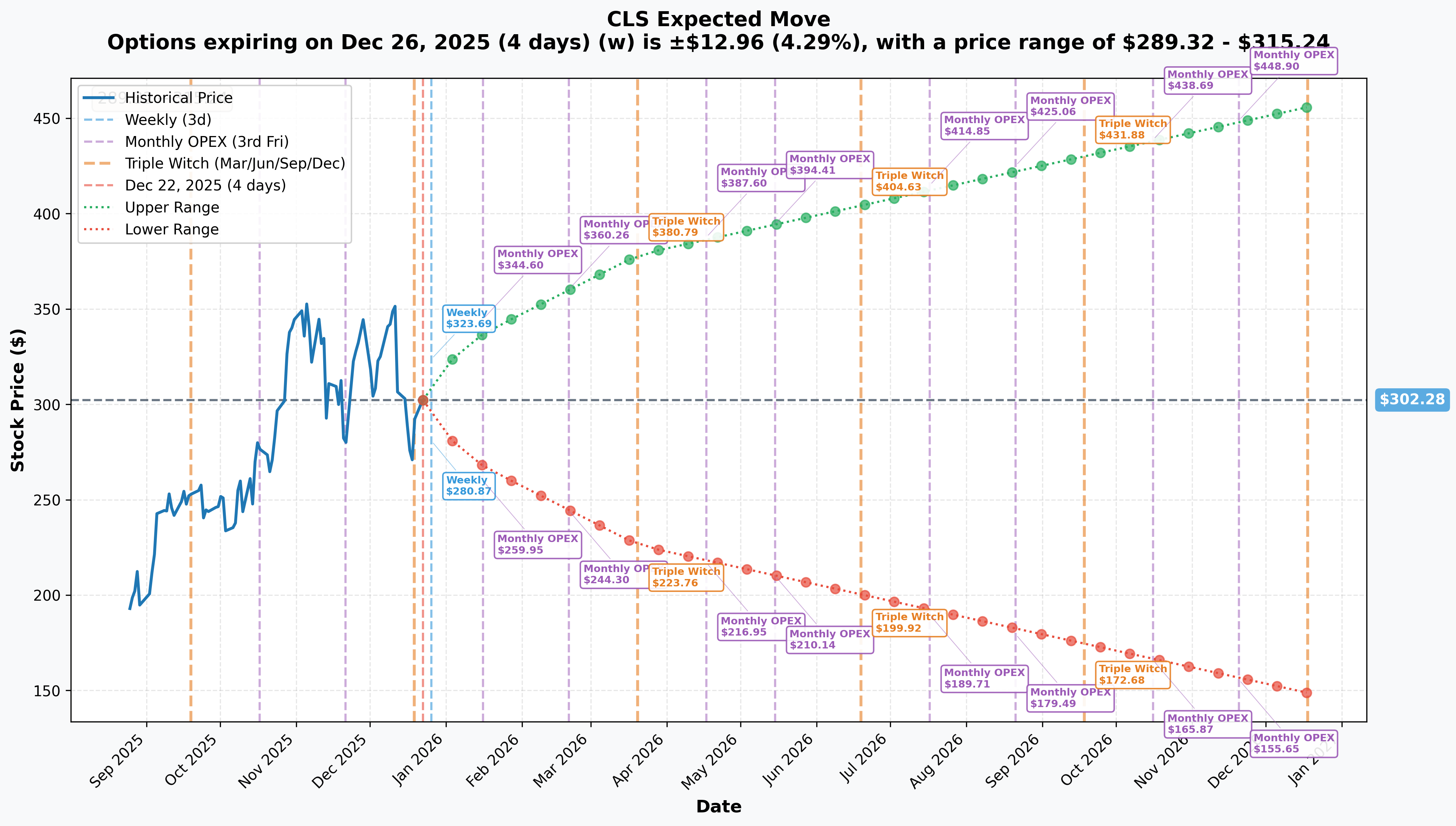

📈 Implied Move Analysis

Options market pricing these ranges:

📅 Weekly (Dec 26 expiry - 4 days): $289-$315 (±4.3%) 📅 Monthly OPEX (Jan 16 - 25 days): $267-$337 (±11.6%) 📅 Quarterly Triple Witch (March 20 - 88 days): $226-$379 (±25.2%) 📅 Yearly LEAPS (Dec 18, 2026 - 361 days): $149-$456 (±50.9%)

Real talk: The March expiration implied move of $226-$379 is EXACTLY where this diagonal spread is positioned. The $350 long call sits right in the upper half of expected range, while the $420 short call is above the quarterly expected move but well within LEAPS territory. This suggests the trader believes CLS will outperform quarterly expectations but wants to lock in gains before getting too extended.

🎪 Catalysts

🔥 Upcoming Catalysts

Q1 2025 Earnings - April 24-25, 2025 🎯 The BIG one that aligns with the March call spread! Celestica is guiding for $10.85B revenue (+20% YoY) with $5.00 EPS (+42% YoY) in 2025. Key metrics to watch:

- CCS segment growth (AI datacenter focus)

- HPS revenue trajectory (Hardware Platform Solutions)

- Hyperscaler concentration risk

- Margin expansion story

2025 Investor and Analyst Day - October 28, 2025 📊 Combined with Q3 2025 earnings, this event will unveil long-term AI infrastructure strategy, hyperscaler pipeline visibility, and multi-year margin targets. Could be a major re-rating catalyst.

Production Ramps (2025-2026): 🏭

- Early 2025: Groq AI/ML server and rack solutions begin production

- 2026: 1.6Tbps switching program with second hyperscaler ramps

- Late 2026: Full rack AI-optimized system with digital native customer begins production

✅ Recent Catalysts (Already Priced In)

Q4 2024 Earnings - Reported January 30, 2025 💪 Crushed it with $2.55B revenue (+19% YoY) and operating margin expansion to 8.0% (vs 5.1% prior year). Full year 2024 delivered $9.65B revenue (+21.17% YoY) and $428M earnings (+75.12% YoY).

Analyst Upgrades Frenzy 📈

- JPMorgan raised PT to $388 from $305

- UBS raised PT to $350 from $208

- RBC Capital raised PT to $115, maintained Outperform

- Average price target: $308.77 (range: $120-$440)

Major Hyperscaler Wins 🎯 New 1.6 Terabyte switching program awarded by second hyperscaler with fully AI-optimized networking rack and advanced liquid cooling. Production ramp expected in 2026. Additionally, new full rack AI system solution with leading digital native company begins production late 2026.

🎲 Price Targets & Probabilities

Using gamma levels, implied move bands, and catalyst timing, here's what the options market is pricing:

🐂 Bull Case: $350-$420 (March-June 2026)

Target: $350 by March 20 OPEX, potentially $420 by June 18 Probability: 45-50% (within quarterly implied move upper range) Catalysts:

- ✅ Q1 earnings beat on April 24-25 with raised guidance

- ✅ Groq production ramp exceeds expectations in early 2025

- ✅ New hyperscaler program announcements

- ✅ Continued AI capex surge from Microsoft, Meta, Alphabet

- ✅ Analyst upgrades extending to $400+ price targets

What needs to happen: CCS segment revenue growth accelerates above 30%, HPS revenue hits $1B+ quarterly run rate, and management confirms multiple 2026 program ramps with >8% operating margins. This is exactly what the diagonal spread is positioned for.

😐 Base Case: $300-$330 (Range-Bound)

Target: Consolidation between current gamma support ($300) and first major resistance cluster ($320-$330) Probability: 35-40% Catalysts:

- ⚖️ In-line Q1 earnings that meet but don't exceed raised guidance

- ⚖️ Groq ramp on track but not material to 2025 numbers yet

- ⚖️ Hyperscaler concentration concerns limit multiple expansion

- ⚖️ AI infrastructure spending continues but at moderating pace

What happens: Stock trades in tight range as market digests 360% rally and waits for concrete 2026 production revenue. Time decay hurts the long $350 calls but short $420 calls also decay, making the spread a scratch.

😰 Bear Case: $250-$280 (Pullback to Support)

Target: Retest of $280 gamma support or deeper to $250 Probability: 15-20% Catalysts:

- ❌ Q1 earnings miss or guided lower on inventory digestion

- ❌ Hyperscaler capex warnings from MSFT, META, or GOOGL

- ❌ Customer concentration blowup (two customers = 36% of revenue)

- ❌ 2026 program delays or competitive losses to Foxconn/Flex

- ❌ Tariff escalation or China supply chain disruptions

- ❌ Broader market correction takes high-flyers down

What happens: Valuation compression hits momentum names hardest. Stock drops to $250-$280 range where put support kicks in. The long $350 calls become worthless, but net loss capped at ~$300K position cost.

💡 Trading Ideas

🛡️ Conservative: "Wait for the Dip"

Strategy: Cash-secured puts at gamma support levels Specific Trade: Sell CLS March 2026 $290 puts for ~$15-20/contract Max Risk: Assignment at $290 (but you want to own it there anyway) Max Reward: Keep premium if CLS stays above $290 Why this works: You're getting paid $1,500-$2,000 per contract to potentially buy CLS at a 3.8% discount to current price, right where gamma support sits. If you get assigned, you own a top-tier AI infrastructure play at a better entry than today. If stock stays above $290, you pocket the premium. Probability of Success: 65-70% (based on implied move)

⚖️ Balanced: "Follow the Smart Money"

Strategy: Replicate the diagonal spread at smaller scale Specific Trade:

- Buy 10x CLS March 2026 $320 calls for ~$18/contract ($18,000 cost)

- Sell 10x CLS June 2026 $370 calls for ~$14/contract ($14,000 credit)

- Net cost: $4,000 for $50K potential profit

Max Risk: $4,000 net premium paid Max Reward: $50,000 if CLS hits $370 by June (23% upside from here) Why this works: You're playing the same thesis as the whale but with strikes closer to current price, improving your probability. March earnings catalyst gives the long calls momentum, while the June short calls fund most of the trade. You profit anywhere between $320-$370. Probability of Success: 50-55%

🚀 Aggressive: "Full Send on April Earnings"

Strategy: Pure call buying ahead of Q1 earnings Specific Trade: Buy CLS April 2026 $330 calls for ~$12-15/contract Max Risk: 100% of premium paid Max Reward: Unlimited above $345 breakeven Why this works: You're betting on a blow-out Q1 earnings report on April 24-25 that sends CLS through $330 resistance. The April expiry is right after earnings, giving you maximum gamma exposure to the event. If CLS gaps to $360-380 on earnings, these calls could 3-4x. Probability of Success: 40-45% (this is a bet, not an investment)

Pro Tip: Consider trimming half your position if CLS hits $340 before earnings to lock in gains and let the rest ride.

⚠️ Risk Factors

Customer Concentration is SCARY 🎯 Two customers represented 36% of Q4 revenue (24% + 12%). If either hyperscaler slows orders or shifts production to competitors, this stock could drop 30-50% overnight. The diagonal spread trader is clearly comfortable with this risk, but you should understand it.

Valuation Stretched After 360% Run 📈 Trading at premium multiples relative to historical EMS peers. Any guidance miss could trigger significant correction as momentum traders exit. This isn't a value play - it's a growth story that needs to keep delivering.

Geopolitical and Tariff Wildcard 🌍 Management guidance assumes "no material changes to tariffs or trade restrictions" as of October 2025. If Trump 2.0 brings tariff chaos or China tensions escalate, the global manufacturing footprint could be both an asset and liability.

2026 Production Ramps Could Delay ⏰ The entire bull thesis hinges on 1.6Tbps switching and full rack AI systems ramping in 2026. Supply chain constraints, technical issues, or customer timeline changes could push revenue out 6-12 months, killing the March/June option plays.

Macro Recession Risk 😰 If we get a 2025 recession, hyperscaler capex will get cut first. AI infrastructure spending could slow if Big Tech earnings disappoint, taking CLS down with it despite strong fundamentals.

🎯 The Bottom Line

Real talk: This $5.7M diagonal call spread is one of the smartest AI infrastructure plays I've seen. The trader is betting on steady appreciation from $301 to $350-$420 range through mid-2026, which aligns perfectly with:

✅ Q1 2025 earnings catalyst (April 24-25) ✅ Groq production ramps (early 2025) ✅ 1.6Tbps hyperscaler program (2026 ramp) ✅ Analyst price targets averaging $308.77 ✅ Bullish gamma positioning and implied move bands

If you own CLS: Hold strong with a stop around $280 (gamma support). The AI server manufacturing thesis is intact, and 2025 guidance of $10.85B revenue (+20%) with $5.00 EPS (+42%) gives multiple expansion runway. Consider selling covered calls at $330-$350 to collect premium.

If you're watching: Wait for a pullback to $290-$300 support zone or use the "Balanced" diagonal spread strategy to get leveraged exposure with defined risk. The April earnings setup is too juicy to ignore if you believe in the AI datacenter buildout story.

If you're bearish: You'd need to see hyperscaler capex warnings or customer concentration blow up to make the bear case work. The $300 gamma support is STRONG, so waiting for a breakdown below that level before shorting makes sense. Otherwise, you're fighting institutional positioning and AI momentum.

Mark your calendar: 📅

- December 26: Weekly option expiry - watch for bounce off $300 support

- January 16: Monthly OPEX - test of $310 resistance

- April 24-25: Q1 2025 earnings - THE catalyst for this spread

- October 28: Investor Day + Q3 earnings - longer-term re-rating opportunity

Bottom line verdict: The smart money just showed us their hand with this diagonal spread. They're not expecting a moonshot - they're positioning for a methodical climb to $350-$420 as AI infrastructure revenue materializes. That's a trade structure I can respect. Just don't forget that customer concentration risk lurking in the shadows. 👀

⚠️ Disclaimer: Options trading involves substantial risk and is not suitable for all investors. The strategies discussed can result in loss of entire premium paid or more. This analysis is for educational purposes only and does not constitute financial advice. Past performance (like CLS's 360% run) does not guarantee future results. Do your own research and consider your risk tolerance before trading.

📊 Data Sources:

- Option flow data: Real-time unusual options activity

- Catalyst research: Company filings, analyst reports, news sources (see inline citations)

- Technical levels: Gamma exposure analysis and implied volatility modeling

- Current price: $301.43 as of December 22, 2025

Analysis by AInvest OptionLabs | Follow us for daily unusual options activity alerts