💎 CLS $2.4M Call Bet - Smart Money Bullish on AI Infrastructure Leader! 🚀

📅 January 5, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $2.4 MILLION on CLS calls at 09:32:24 this morning! This massive bullish bet bought 500 contracts of $360 strike calls expiring June 18th - betting on a 24% rally over the next 5 months as Celestica rides the AI server and networking boom. With CLS up +360% over the past year at $289 and Q4 earnings scheduled for February 4th, this institutional player is positioning for the next leg higher. Translation: Big money expects the AI infrastructure story to accelerate!

📊 Company Overview

Celestica Inc. (CLS) is a leading supply chain solutions provider dominating the AI infrastructure hardware space:

- Market Cap: $34.79 Billion (explosive growth from AI tailwinds!)

- Industry: Electronics Manufacturing Services - Printed Circuit Boards

- Current Price: $289.30 (trading near all-time high of $363.40)

- Primary Business: Two segments -

- CCS (Connectivity & Cloud Solutions): Servers, storage, networking for hyperscalers (76% of revenue!)

- ATS (Advanced Technology Solutions): Aerospace, defense, industrial, healthtech equipment

Celestica is essentially the picks-and-shovels play on AI infrastructure buildout - they manufacture the 800G/1.6T Ethernet switches and rack-level solutions that power Google TPU deployments and major hyperscaler data centers. Think of them as the company MAKING the hardware that runs AI, rather than designing the chips.

💰 The Option Flow Breakdown

The Tape (January 5, 2026 @ 09:32:24):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order_Type | Option_Strategy | Confidence | Z_Score | Z_Classification | Vol_OI_Ratio | Vol_OI_Signal |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-05 | 09:32:24 | CLS | BUY | CALL $360 | 2026-06-18 | $360 | 500 | $2,400,000 | BTO | Long Call | MEDIUM | 94.6 | EXTREMELY_UNUSUAL | 5.814 | HIGH_ACTIVITY |

🤓 What This Actually Means

This is a massive bullish bet on CLS continuing its AI infrastructure momentum! Here's what went down:

- 💸 Huge premium paid: $2.4M ($4,800 per contract × 500 contracts)

- 🚀 Aggressive strike: $360 is 24.4% above current price - expects significant rally

- ⏰ Strategic timing: 164 days to expiration captures Q4 earnings (Feb 4), Q1 earnings (April), 1.6T program ramps, and Google TPU expansion

- 📊 Size matters: 500 contracts represents 50,000 shares worth ~$14.5M

- 🏦 High conviction: Z-score of 94.6 (EXTREMELY_UNUSUAL) - this happens very rarely

- 📈 Opening position: Vol/OI ratio of 5.814 signals HIGH_ACTIVITY with fresh money entering

What's really happening here: This trader is betting that CLS will rally from $289 to well above $360 by June expiration. With the stock already up +360% in the past year driven by hyperscaler AI demand, they're expecting the momentum to CONTINUE. Think about it - CLS has 41% market share in 800G/1.6T Ethernet switches and manufactures Google TPU rack solutions. As AI infrastructure spending accelerates in 2026 with projected revenue growth of 31% to $16B, this is a bet that Q4 earnings and 2026 guidance will blow minds.

Unusual Score: 🔥 EXTREMELY_UNUSUAL (94.6 Z-Score) - This trade is 94.6 standard deviations above average! We're talking about activity that happens maybe a few times per year for CLS. The Vol/OI Signal of HIGH_ACTIVITY confirms this is fresh institutional money, not existing positions being adjusted.

Why June 18 expiration?

- Captures Q4 2025 earnings on February 4 (analyst consensus $1.77 EPS, $3.45B revenue)

- Captures Q1 2026 earnings likely in late April

- Allows time for multiple 1.6T switching program ramps throughout 2026

- Positions for Google TPU expansion (3 million TPUs in 2026, 5 million in 2027)

- Gives runway through 1.6T DS6000/DS6001 switch commercial availability later in 2026

📈 Technical Setup / Chart Check-Up

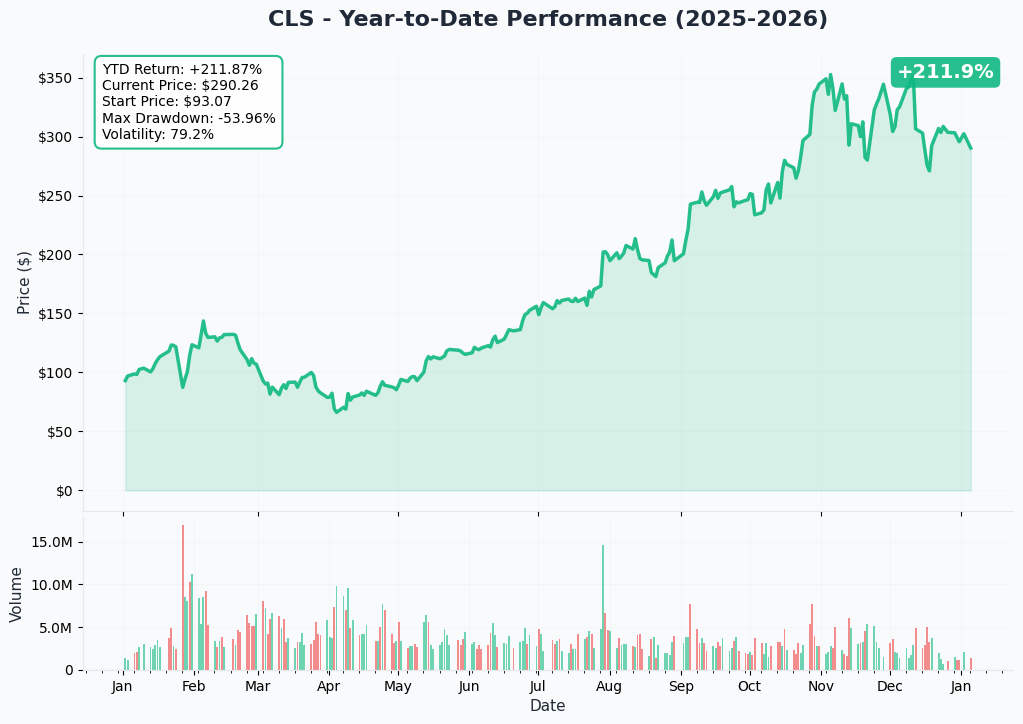

YTD Performance Chart

CLS has been an absolute MONSTER - the chart tells an incredible AI infrastructure growth story! Starting 2025 around $120, the stock rocketed to an all-time high of $363.40 on November 5, 2025, representing a 202% gain in less than a year.

Key observations:

- 🚀 Parabolic rally: Explosive move from $240 in mid-August to $363 peak in early November following Q3 earnings beat and 2026 guidance announcement

- 📊 Post-peak pullback: Currently at $289, about 20% off the November highs - healthy consolidation after huge run

- 📈 Strong support: Stock finding buyers around $280-290 range

- 💪 Momentum intact: Still up +360% over past year despite recent pullback

- 🎢 High volatility: This is a momentum stock prone to 10-15% swings

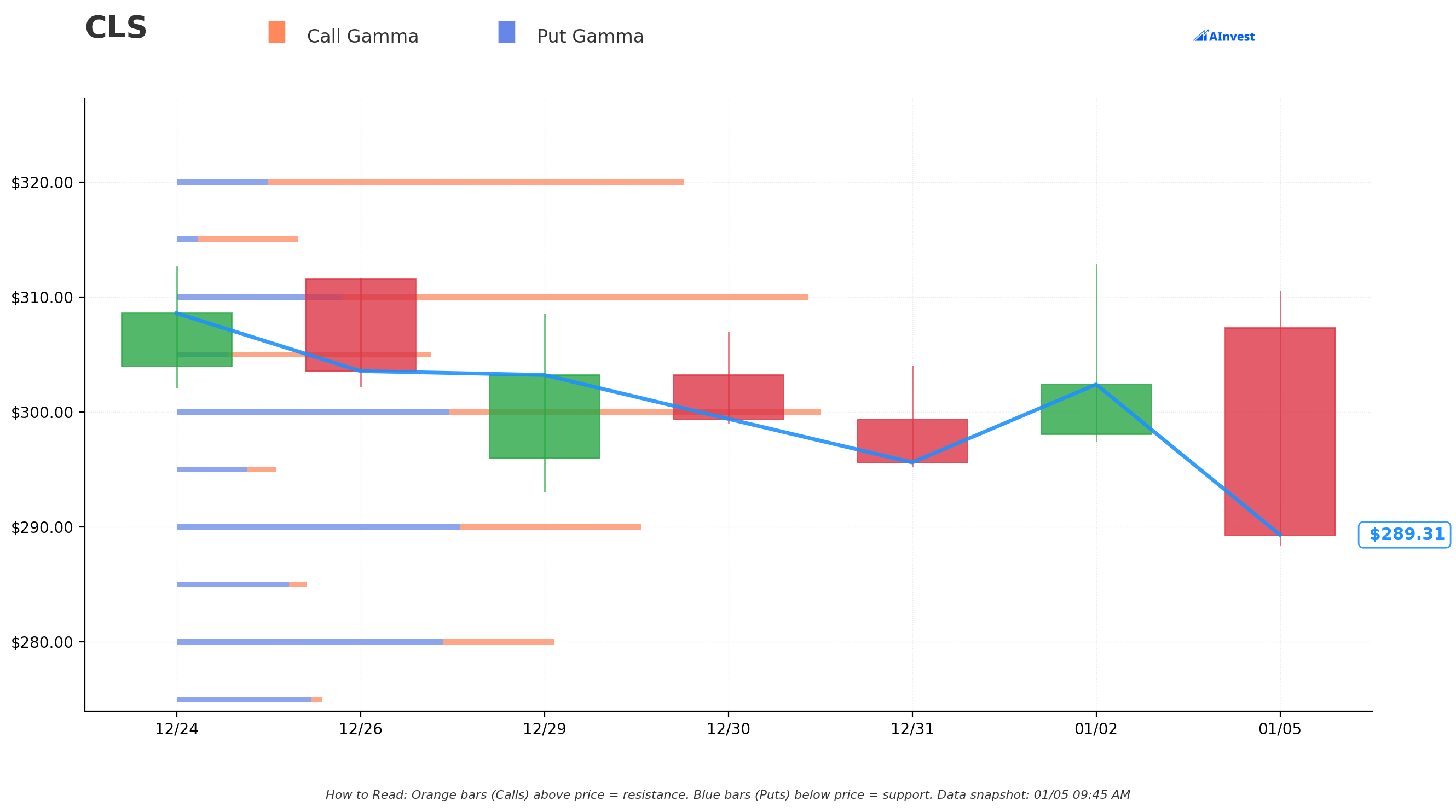

Gamma-Based Support & Resistance Analysis

Current Price: $289.30

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $280 - Strongest immediate support with 0.54B total gamma exposure (0.38B put gamma) - this is THE FLOOR

- $270 - Secondary support at 0.52B gamma (0.42B put gamma) - major structural level

- $260 - Deep support at 0.38B gamma (0.29B put gamma)

- $250 - Extended floor with 0.32B gamma (0.19B put gamma)

🟠 Resistance Levels (Call Gamma Above Price):

- $290 - Immediate ceiling with 0.67B gamma (0.40B put gamma - still net bearish here)

- $300 - Major resistance at 0.93B gamma (0.54B call gamma - STRONGEST LEVEL, big gamma flip!)

- $305 - Secondary resistance at 0.37B gamma (0.30B call gamma)

- $310 - Significant ceiling zone with 0.92B gamma (0.68B call gamma)

- $320 - Extended upside barrier at 0.74B gamma (0.60B call gamma)

- $330 - Major resistance at 0.69B gamma (0.65B call gamma)

What this means for traders: CLS is sitting RIGHT at a critical inflection point. The stock just reclaimed the $290 level which has been acting as both support and resistance. The gamma data shows $300 is THE big battleground with 0.93B total gamma (highest level on the entire map). This is where call buyers and put sellers have drawn the line - if CLS breaks decisively above $300, there's a clear path to $310-$320 as gamma flips bullish.

Notice anything? The call buyer struck WELL above at $360, beyond the visible gamma levels. They're not looking for a grind to $310-320 - they're betting on a BREAKOUT move that smashes through all resistance levels on major positive catalysts (earnings beat, guidance raise, hyperscaler wins).

Net GEX Bias: Bullish (5.86B call gamma vs 4.28B put gamma = +1.58B net) - Overall positioning leans bullish, supporting the upward bias.

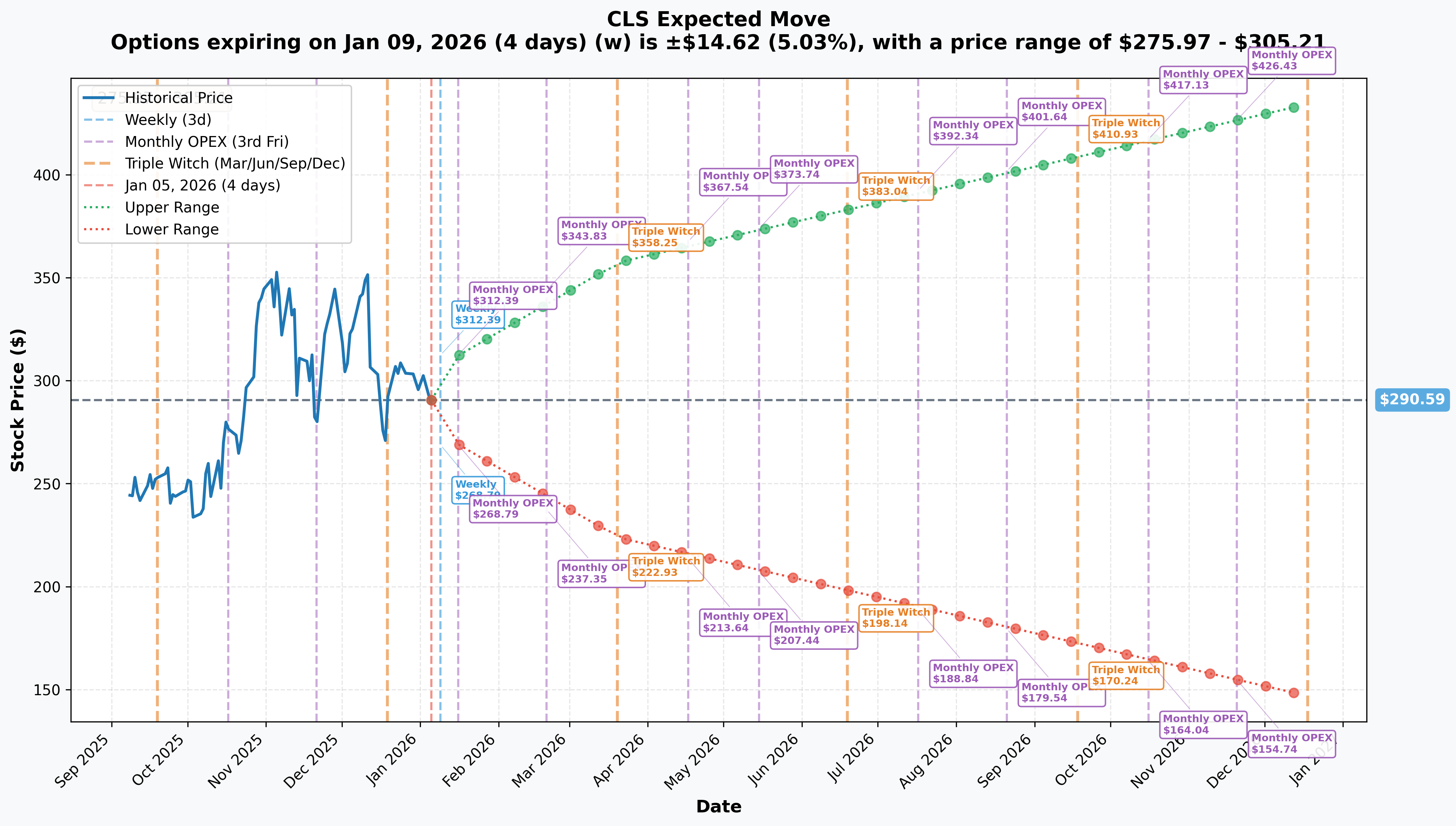

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 9 - 4 days): ±$14.62 (±5.03%) → Range: $275.97 - $305.21

- 📅 Monthly OPEX (Jan 16 - 11 days): ±$21.80 (±7.50%) → Range: $268.79 - $312.39

- 📅 Quarterly Triple Witch (Mar 20 - 74 days): ±$66.81 (±22.99%) → Range: $223.78 - $357.40

- 📅 June OPEX (Jun 19 - THIS TRADE! 165 days): Implied move ~±35% → Range: $188-$393 estimated

Translation for regular folks: Options traders are pricing in a 5% move ($15) by this Friday for weekly expiration - pretty tame. But the market expects 7.5% volatility ($22) through January OPEX which includes the critical Q4 earnings on February 4th. The real fireworks start with the quarterly expiration showing 23% implied move ($67) through March - the market knows earnings could be explosive!

For the June 18th expiration when this $2.4M call trade expires, we're looking at implied volatility suggesting the stock could reasonably trade anywhere from $190 to $390+. The $360 strike sits right at the top end of the expected range - aggressive but NOT crazy given CLS hit $363 just two months ago.

Key insight: The relatively low near-term implied move (5% weekly) vs high longer-term move (23% quarterly) suggests the market is waiting for earnings to provide direction. Post-earnings, if results crush expectations, the $360 strike could come into play FAST.

🎪 Catalysts

🔥 Immediate Catalysts (Already Happened - Past 3 Months)

Q3 2025 Earnings Beat - October 27, 2025 (MASSIVE WIN!) 📊

CLS demolished expectations in Q3 2025, triggering the rally to all-time highs:

- 💰 Revenue: $3.19B vs $3.04B consensus (up 28% YoY) - BEAT by 5%

- 📈 Adjusted EPS: $1.58 vs $1.47-$1.49 consensus - BEAT by 7.5%

- 🚀 Guidance RAISED: FY2025 revenue to $12.2B (from $11.55B), Adjusted EPS to $5.90 (from $5.50)

- 🎯 2026 Outlook Announced: Revenue $16.0B (+31% growth!), Adjusted EPS $8.20 (+39%), FCF $500M

- 💪 CCS Segment: $2.41B, up 43% YoY, 8.3% margin (this is the AI/cloud segment driving growth)

- 📊 Stock reaction: Surged 8.97% during trading, then another 16.82% in premarket - total 25%+ move!

Why this matters for the call trade: This Q3 beat set the tone - CLS is CRUSHING IT. If Q4 delivers similar upside surprise and management raises 2026 guidance again, $360 is absolutely in play.

1.6T Networking Switch Launches - October 2025 🌐

Celestica introduced the DS6000/DS6001 family of 1.6TbE data center switches based on Broadcom's Tomahawk 6 chipset:

- 🔥 Capacity: Up to 102.4Tbps switching capacity (double the bandwidth of 800G!)

- 💧 Advanced cooling: DS6001 incorporates direct-to-chip liquid cooling technology

- 🏆 Market validation: Won Dell'Oro Market Share Leader Awards for Ethernet Switch - AI Networks

- 📅 Timeline: Availability expected later in 2026

Second 1.6T Program Win with Major Hyperscaler 🏆

CEO Rob Mionis confirmed Celestica was awarded a second 1.6T switching program with another large hyperscaler:

- 🚀 Ramp timing: Program ramping throughout 2026

- 🖥️ Scope: Designing and producing AI-optimized networking rack with advanced cooling

- 💰 Revenue impact: Multiple hyperscaler programs = diversified revenue stream

Analyst Upgrades Post-Q3 (BULLISH WALL STREET!) 📈

Major banks raised price targets aggressively after Q3 beat:

| Firm | Price Target | Rating |

|---|---|---|

| Goldman Sachs | $440 (from $340) | Buy |

| JPMorgan Chase | $360 (from $295) | Overweight |

| UBS Group | $350 (from $208) | Neutral |

| New Street Research | $400 | N/A |

| BMO Capital Markets | $370 | Outperform |

Consensus: 15 Buy ratings, 2 Hold ratings. Average price target: $336-$372. Notice the $360 call strike sits right in the middle of Wall Street's target range!

🚀 Upcoming Catalysts (Next 6 Months - WHERE THE MONEY IS!)

Q4 2025 Earnings Release: February 4, 2026 (30 DAYS AWAY!) 📊

This is THE catalyst that could launch CLS toward the $360 strike! Q4 earnings scheduled for before market open on February 4, 2026:

Company Guidance for Q4 2025:

- 📊 Revenue: $3.325B to $3.575B (midpoint $3.45B)

- 💰 Adjusted EPS: $1.65 to $1.81 (midpoint $1.73)

- 🎯 Analyst Consensus: $1.77 EPS

Key Metrics to Watch:

- 📈 CCS segment growth: Looking for continued 40%+ YoY growth (AI/cloud tailwinds)

- 🌐 800G/1.6T program commentary: Customer wins, deployment timelines, pricing dynamics

- 👥 Hyperscaler concentration: Revenue mix from top 3 customers (currently 59% from 3 hyperscalers)

- 🛠️ ATS segment stabilization: Need to see this segment stop declining

- 💵 Free cash flow: Progress toward $425M FY25 target

- 🎯 2026 GUIDANCE UPDATE: Any raise to the $16B revenue/$8.20 EPS targets would be MASSIVE

Upside surprise potential: If CLS beats like Q3 (5-7% revenue beat, 7-8% EPS beat) AND raises 2026 guidance, stock could gap 15-20% toward $330-340 immediately. Add in positive hyperscaler commentary about 1.6T deployments accelerating, and you're looking at potential breakout to $350+.

Risk factors: Any disappointment in hyperscaler spending, margin compression from competitive pricing, or conservative 2026 guidance could trigger sharp selloff back to $250-270 support levels.

1.6T Switch Program Ramps Throughout 2026 🚀

Multiple 1.6T switching programs expected to ramp in 2026, representing SIGNIFICANT revenue catalyst:

- 💪 Double the capacity: 1.6T offers 2x bandwidth vs 800G products

- 🏭 Volume production: Transition from pilot programs to mass deployment

- 💰 Revenue scale: Each hyperscaler program can add hundreds of millions annually

- 📊 Market share: CLS already has 55% market share in custom Ethernet switch solutions YTD 2025

Why this matters: The June call expiration perfectly captures the 2026 ramp timeline. As these programs move from development to production throughout Q1-Q2 2026, CLS should see accelerating revenue and positive analyst revisions.

Google TPU Rack Solutions Expansion (2026-2027) 🤖

Goldman Sachs analysts noted Celestica is the leading provider of Google TPU rack level solutions:

- 🖥️ Volume estimates: ~3 million TPUs in 2026, ~5 million TPUs in 2027

- 💰 Revenue potential: Potentially $500M per incremental 1 million TPUs

- 🔌 Optical Circuit Switch: Google needs ~15,000 units of 300-port OCS switches in 2026, with ~12,000 units contract-manufactured by Celestica

- 🎯 Strategic customer: Google is one of CLS's top 3 hyperscaler customers (14-15% of revenue)

Texas Facility Expansion Completion (Through 2027) 🏭

The Texas expansion will increase square footage by over 100% and power capacity by 10x by 2027:

- ⚡ Capacity: Support massive AI/ML program growth

- 📍 Location advantage: North American manufacturing for hyperscaler customers

- 🇺🇸 Nearshoring trend: Reduced China dependency, increased Mexico/Texas production

- 💪 Competitive edge: Allows CLS to take on larger programs competitors can't handle

DS6000/DS6001 1.6TbE Switch Commercial Availability (Late 2026) 📦

The new 1.6TbE switch family expected to become available later in 2026:

- 🔥 Performance: 102.4Tbps switching capacity

- 🏆 Market leadership: Dell'Oro Market Share Leader Award winner

- 💧 Differentiation: Direct-to-chip liquid cooling in DS6001 variant

- 📈 Margin expansion: Higher ASPs on new technology products

Full Year 2026 Outlook - THE BIG PICTURE 🎯

Management provided aggressive 2026 guidance at October Investor Day:

| Metric | FY2025 Outlook | FY2026 Outlook | YoY Growth |

|---|---|---|---|

| Revenue | $12.2B | $16.0B | +31% 🚀 |

| Adjusted EPS | $5.90 | $8.20 | +39% 💰 |

| Free Cash Flow | $425M | $500M | +18% 💵 |

| Operating Margin | 7.4% | 7.8% | +40bps 📈 |

| CCS Revenue Growth | ~35% | ~40% | Accelerating 🔥 |

What this tells us: CLS is projecting ACCELERATION in 2026, not deceleration. The CCS segment (AI/cloud) growing at 40% is the engine. At current $289 price with $8.20 FY2026 EPS guidance, CLS trades at 35x forward P/E - expensive but not crazy for 31% revenue growth company with 40%+ segment growth.

Path to $360: If CLS executes this 2026 plan and trades at 40-45x forward earnings (justified by growth acceleration), you get $8.20 × 40-45 = $328-$369 fair value. The $360 call strike is betting on high-end execution and multiple expansion!

⚠️ Risk Catalysts (Negative - What Could Go Wrong)

Recent Analyst Downgrades (Late December 2025) 📉

Not all analysts are believers at current valuation:

- ❌ Zacks Research: Downgraded from Strong-Buy to Hold (December 31, 2025)

- ❌ Wall Street Zen: Downgraded from Buy to Hold (December 6, 2025)

- 🎯 Reasoning: Valuation concerns after 360% run - stock priced for perfection

Customer Concentration Risk 👥

59% of Q3 2025 revenue came from just 3 hyperscaler customers (30%, 15%, 14%):

- ⚠️ Any single customer spending pause could crater revenue

- 📉 Hyperscaler capex cycles are unpredictable

- 🔄 Customer dependency creates volatility

Tariff and Trade Risks 🌍

Company guidance assumes no material changes from October 27, 2025 tariff environment:

- 🇨🇳 China production becoming less cost-competitive

- 🚚 Customer programs being transferred to Thailand and other regions

- 💸 Any new tariffs could impact margins if not passed through to customers

Competitive Intensity 🥊

Jabil, Flex, Foxconn, and Sanmina all pursuing AI infrastructure opportunities:

- 💰 Price wars could erode margins (CLS operating margin 8.18% vs EMS sector average 18.23%)

- 🎯 Must maintain technological edge in 1.6T transition

- 📊 Market share gains require continued R&D investment

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, catalyst timeline, and current valuation, here are the scenarios through June 18th expiration:

📈 Bull Case (35% probability)

Target: $340-$380 (CALL TRADE WINS BIG!)

How we get there:

- 💪 Q4 earnings CRUSHES - Revenue at high-end $3.57B (up 33% YoY), EPS $1.85+ (beats $1.77 consensus by 5%+)

- 🚀 2026 guidance RAISED - Revenue to $16.5B (from $16B), EPS to $8.50+ (from $8.20)

- 🏆 New hyperscaler wins announced - Third or fourth 1.6T switching program with major cloud provider

- 🌐 Market share expansion confirmed - 800G/1.6T share climbing toward 50-60% as competitors struggle

- 📈 1.6T program ramps AHEAD of schedule - Q1 2026 revenue contribution from new programs exceeds expectations

- 💰 Margin expansion - Operating margin trending toward 8.5-9.0% on favorable mix shift to high-value networking

- 🔥 Google TPU deployment acceleration - Commentary about 2026 TPU volumes tracking ahead of 3M estimate

- 📊 Analyst upgrades - Goldman's $440 target gains traction, others raise to $380-420 range

- 🎯 Technical breakout - Clear above $300 gamma resistance triggers momentum to $330, then $360+

Key metrics needed:

- CCS segment revenue growth >45% YoY (vs 43% in Q3)

- Gross margins holding or expanding (proof of pricing power)

- Free cash flow trending toward $500M+ for 2026

- Customer concentration improving (adding 4th/5th major hyperscaler)

Probability assessment: 35% because it requires excellent execution but CLS has proven track record of beating/raising. The AI infrastructure tailwinds are REAL - hyperscaler capex isn't slowing down. Stock hit $363 just 2 months ago, so $360-380 is achievable on positive catalysts. Multiple Wall Street targets at $370-440 support this case.

Call P&L in Bull Case:

- Stock at $360 on Jun 18: Calls worth ~$5-10 intrinsic, LOSS of -$4,300 to -$4,550/contract (still underwater at strike!)

- Stock at $380 on Jun 18: Calls worth $20 intrinsic, profit = +$15,200/contract × 500 = $7.6M gain (317% ROI!)

- Stock at $400 on Jun 18: Calls worth $40 intrinsic, profit = +$35,200/contract × 500 = $17.6M gain (733% ROI!)

🎯 Base Case (40% probability)

Target: $300-$340 (GRINDING HIGHER)

Most likely scenario:

- ✅ Solid Q4 earnings - Meet/slightly beat consensus ($3.45B revenue, $1.75-1.80 EPS)

- 📱 2026 guidance CONFIRMED - Reiterate $16B revenue, $8.20 EPS (no raise, but no cut either)

- ⚖️ 1.6T programs on track - Steady progress, no major delays but no major acceleration either

- 🤖 Hyperscaler spending solid - Continued AI infrastructure buildout but at expected pace

- 📊 Margins stable - Operating margin in 7.5-8.0% range (consistent with guidance)

- 🔄 Trading in range - Consolidation between $280 support and $320-340 resistance for months

- 💤 Waiting for catalysts - Market digests massive 2025 gains, needs proof points from 2026 execution

- 📈 Gradual grind higher - Slow climb toward $320-340 by June on steady fundamental progress

This is the "show me" scenario: Stock at technical inflection point. Fundamentals solid but valuation requires flawless execution. Investors want to see 2026 guidance DELIVERED, not just projected. CLS needs to prove it can sustain 30%+ growth rates.

Why 40% probability: Most balanced scenario. Stock consolidating after huge run. Earnings likely solid but not spectacular. 2026 guidance probably confirmed without major changes. Slow grind higher makes sense given elevated valuation (35x forward P/E) and need for proof of concept.

Call P&L in Base Case:

- Stock at $320 on Jun 18: Calls expire worthless, LOSS = -$4,800/contract × 500 = -$2.4M (100% loss)

- Stock at $340 on Jun 18: Calls expire worthless, LOSS = -$4,800/contract × 500 = -$2.4M (100% loss)

Note: In base case, even with stock grinding to $340, the $360 calls expire worthless. This is why aggressive OTM calls are risky - you need the BULL case to materialize, not just "okay" results.

📉 Bear Case (25% probability)

Target: $220-$270 (PULLBACK TO SUPPORT)

What could go wrong:

- 😰 Earnings miss or weak guidance - Q4 revenue at low-end $3.33B, EPS $1.65, or 2026 guidance CUT to $15B revenue

- 🚨 Hyperscaler spending slowdown - Major customer reduces orders or delays 1.6T deployments

- ⏰ 1.6T program delays - Technical issues, customer acceptance problems, timeline pushed to 2027

- 🇨🇳 New tariffs announced - Trade tensions escalate, impacting margins and China revenue

- 💸 Margin compression - Competitive pricing pressure drives operating margin below 7% target

- 📊 Customer concentration concerns - Loss of major hyperscaler account or spending reduction from top customer

- 💰 Broader tech selloff - Recession fears, rate hikes, or AI investment slowdown drags semis/hardware lower

- 🤖 AI infrastructure spending pause - Hyperscalers digest existing capacity, delay new data center builds

- 🔨 Break below $280 gamma support - Triggers cascade selling to $260, then $250

Critical support levels:

- 🛡️ $280: Immediate gamma floor (0.54B) - MUST HOLD or momentum shifts bearish

- 🛡️ $270: Major structural support (0.52B gamma) - likely significant buying here

- 🛡️ $260: Deep support (0.38B gamma) - psychological level (prior breakout point)

- 🛡️ $250: Extended floor - disaster scenario

Probability assessment: 25% because it requires multiple negative catalysts. CLS fundamentals remain strong (proven execution, hyperscaler partnerships, market share leadership), but valuation offers little margin for error at 48x trailing P/E. Recent analyst downgrades to Hold signal some profit-taking risk. Any disappointment could trigger sharp correction.

Call P&L in Bear Case:

- Stock at $270 on Jun 18: Calls expire worthless, LOSS = -$4,800/contract × 500 = -$2.4M (100% loss)

- Stock at $220 on Jun 18: Calls expire worthless, LOSS = -$4,800/contract × 500 = -$2.4M (100% loss)

💡 Trading Ideas

🛡️ Conservative: Wait for Q4 Earnings Clarity

Play: Stay on sidelines until February 4th earnings volatility settles, then reassess

Why this works:

- ⏰ Earnings in 30 days creates binary event risk - too dangerous to chase at $289

- 💸 Stock up 360% in past year - massive gains already captured, limited upside vs downside

- 📊 Recent analyst downgrades signal valuation concerns - smart money taking profits

- 🎯 Better entry likely post-earnings if stock pulls back to $270-280 gamma support

- 📉 Historical pattern: High-flyers often consolidate even after beats (profit-taking)

- 🤔 At 35x forward P/E, small earnings miss could trigger -15-20% gap down

Action plan:

- 👀 Watch February 4th earnings for revenue quality (CCS segment growth), margin trends, and 2026 guidance update

- 🎯 Look for pullback to $270-280 post-earnings for stock entry with 10-15% margin of safety

- ✅ Need to see 1.6T program momentum and hyperscaler spending commentary before committing

- 📊 If stock GAPS UP on earnings to $320-330, accept you missed the move - don't chase

- ⏰ Revisit after Q1 2026 earnings when 2026 trajectory becomes clearer

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential drawdown if earnings disappoint. Get better entry if stock consolidates. Sleep better at night.

⚖️ Balanced: Post-Earnings Bull Put Spread

Play: After earnings clarity, sell bull put spread to generate income in support zone

Structure: Sell $280 puts, Buy $270 puts (March 20 expiration - after Q4 earnings digested)

Why this works:

- 🎯 Targets strongest gamma support zone at $270-$280 where institutions are positioned

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 💰 Collect premium betting stock STAYS ABOVE $280 (currently $289 - gives 3% cushion)

- ⏰ March 20 expiration gives 74 days for thesis to play out after earnings volatility settles

- 🛡️ If earnings beat and stock rallies, spread profits from premium decay

- 📈 Even if stock consolidates in $280-320 range, you win as long as it stays above $280

Estimated P&L (enter AFTER Feb 4 earnings):

- 💰 Collect ~$2.50-3.50 credit per spread (adjust based on post-earnings IV)

- 📈 Max profit: $250-350 if CLS stays above $280 at March 20 expiration (keep full credit)

- 📉 Max loss: $650-750 if CLS below $270 (defined and limited)

- 🎯 Breakeven: ~$277-277.50

- 📊 Risk/Reward: ~2:1 (solid for defined-risk bullish play)

Entry criteria:

- ⏰ Wait 2-3 days post-earnings (by Feb 6-7) for IV to settle

- 🎯 Only enter if stock trading $285+ (maintains cushion to support)

- ❌ Skip if stock already below $280 (too close to short strike)

- ✅ Confirm earnings showed continued CCS growth and 2026 guidance intact

Position sizing: Risk only 5-10% of portfolio (directional income strategy, not core holding)

Risk level: Moderate (defined risk, bullish bias) | Skill level: Intermediate

Probability of profit: ~60-65% (stock needs to stay above $280 - reasonable given gamma support)

🚀 Aggressive: COPY THE TRADE - Buy June $360 Calls (EXPERT ONLY!)

Play: Buy the same $360 calls expiring June 18 that the institutional player just loaded

Why this could work:

- 🐋 Smart money validation - Institutional trader just paid $2.4M for this exact position

- 📊 Multiple catalysts - Captures Q4 earnings, Q1 earnings, 1.6T ramps, Google TPU expansion

- 🎯 Wall Street targets support - Goldman $440, JPM $360, multiple targets $370-420

- 💪 Proven momentum - Stock hit $363 just 2 months ago, $360 strike already proven achievable

- 🚀 AI infrastructure tailwinds - Hyperscaler spending on data center networking accelerating through 2026

- 📈 June expiration - Enough time for 2026 guidance to be DELIVERED (Q1 results), not just projected

- 🔥 Execution track record - CLS has history of beating/raising consistently

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Each call costs $4,800 (5-10 contracts = $24K-48K investment)

- ⏰ TIME DECAY: Theta burns ~$25-30/contract per day - that's $750-900/month!

- 😱 NEEDS BIG MOVE: Stock must rally to $380+ just to BREAKEVEN after premium paid

- 📊 OTM Strike Risk: $360 is 24% above current price - most options expire worthless

- 🎢 Binary earnings risk: Q4 earnings in 30 days could gap stock DOWN 15-20% on disappointment

- ⚠️ Valuation stretched: At 35x forward P/E, ANY execution stumble magnified 3-4x

- 💰 All-or-nothing: Unlike stock, options can go to ZERO - you could lose 100% of premium

Estimated P&L:

- 💰 Cost: $4,800 per call contract

- 📉 Total loss scenario: Stock below $360 on Jun 18 = LOSE entire $4,800/contract (100% loss - MOST LIKELY)

- 📈 Breakeven: Stock needs to reach $384.80 (~33% rally from current $289)

- 🚀 Home run: Stock at $420 = $60 intrinsic value, profit = +$55,200/contract (1,150% ROI!)

- 💎 Moonshot: Stock at $440 (Goldman target) = $80 intrinsic, profit = +$75,200/contract (1,567% ROI!)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can afford to lose ENTIRE premium (real possibility - most OTM calls expire worthless!)

- ✅ Understand this is SPECULATION, not investing

- ✅ Have experience with long-dated OTM call options

- ✅ Accept you're betting stock rallies 24-33% in 5 months (requires perfect execution + multiple expansion)

- ✅ Won't panic sell on normal pullbacks to $270-280

- ✅ Have a plan to take profits if stock reaches $340-360 early (don't get greedy!)

Position sizing: Risk ONLY 1-3% of total portfolio - this is lottery ticket territory!

Risk level: EXTREME (can lose 100%) | Skill level: Advanced only

Probability of profit: ~25-30% (most OTM calls expire worthless, need multiple catalysts to align)

Better alternative for aggressive traders: Consider buying June $320 calls instead - only 11% OTM vs 24%, much higher probability of profit, still captures upside to $360-380.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q4 earnings in 30 days: Results February 4th before market open create MASSIVE volatility risk. Stock could gap 10-20% either direction based on revenue ($3.45B vs $3.33B low-end makes huge difference), CCS segment growth (need 43%+ to maintain momentum), and 2026 guidance (any cut to $16B target would be devastating). Recent analyst downgrades suggest some expect disappointment.

-

💸 Valuation at 48x trailing P/E, 35x forward P/E: This is EXTREMELY stretched - stock priced for PERFECT execution. Requires 40% CCS growth and $16B revenue in 2026 to justify current multiple. Zero margin of safety. Any stumble magnified 3-4x. Compare to peer Jabil at 20x forward P/E - CLS trading at 75% premium.

-

👥 Customer concentration is HUGE risk: 59% of revenue from 3 hyperscalers, with top customer at 30%. ANY single customer spending reduction, program delay, or shift to competitor could crater stock 20-30% overnight. Hyperscaler capex is lumpy and unpredictable.

-

🌐 1.6T program execution risk: New technology ramps ALWAYS have issues. Delays, customer acceptance problems, competitive solutions, or technical bugs could push revenue contribution to 2027. DS6000/DS6001 availability "later in 2026" is vague - could slip to Q4 2026 or beyond.

-

🇨🇳 Tariff and geopolitical wildcard: Company guidance assumes no changes from October 2025 tariff environment. New administration could impose tariffs on Mexico/Thailand production. China exposure creates ongoing uncertainty. Any new restrictions hit margins.

-

💰 Margin pressure from competition: Operating margin of 8.18% vs EMS sector average 18.23% shows CLS operates on thin margins. Price competition from Jabil, Flex, Foxconn could force aggressive pricing, compressing already-low margins below 7% target.

-

📊 Recent analyst downgrades signal caution: Zacks and Wall Street Zen both downgraded from Buy to Hold in late December citing valuation concerns. When analysts who rode the rally take chips off table, it's a warning sign smart money is derisking.

-

🎢 Extreme momentum creates whipsaw risk: Stock up 360% in 12 months, then down 20% from November peak. This isn't stable blue chip - CLS can move 5-10% on NO NEWS. Max drawdown potential is real if AI infrastructure narrative shifts.

-

🔮 AI infrastructure spending could slow: If hyperscalers decide they've overbuilt capacity or AI monetization disappoints, data center spending could pause rapidly. CLS has zero diversification - 77% of revenue from hyperscalers. One bad quarter of capex cuts = disaster.

-

⚖️ Competitive moat is EXECUTION, not IP: Unlike Nvidia/Broadcom who own chip designs, CLS is a contract manufacturer. Customers can shift production to competitors (Jabil, Flex) if CLS stumbles on quality, delivery, or price. Market share gains are NOT sticky.

🎯 The Bottom Line

Real talk: Someone with serious conviction just bet $2.4 MILLION that CLS rallies to $360+ by June. This isn't a hedge or defensive play - this is a pure bullish bet on the AI infrastructure story accelerating through 2026.

What this trade tells us:

- 🎯 Institutional player expects CLS to deliver on aggressive 2026 guidance ($16B revenue, $8.20 EPS)

- 💰 They're willing to risk $2.4M betting on Q4 earnings beat + guidance raise in 30 days

- ⚖️ The timing (pre-earnings) shows HIGH conviction - they're not waiting for confirmation

- 📊 $360 strike matches Wall Street consensus targets ($336-$372 average) - betting on high-end case

- ⏰ June expiration captures multiple catalysts: Q4 earnings, Q1 earnings, 1.6T program ramps, Google TPU updates

This IS a bullish signal - but context matters:

The bull case is REAL:

- ✅ CLS has 41% market share in 800G/1.6T networking - dominant player

- ✅ Proven execution with consistent beat-and-raise pattern

- ✅ Multiple 1.6T programs ramping in 2026 = visible revenue catalyst

- ✅ Google TPU rack solution leader with 3M-5M units projected 2026-2027

- ✅ Stock already PROVED it can reach $360+ (hit $363 in November)

- ✅ Wall Street consensus targets $336-$440 support upside case

But the risks are REAL too:

- ⚠️ Valuation stretched at 35x forward P/E - requires flawless execution

- ⚠️ Customer concentration (59% from 3 hyperscalers) = binary risk

- ⚠️ Recent analyst downgrades signal profit-taking by smart money

- ⚠️ Earnings in 30 days = massive volatility (could gap down 15-20% on miss)

- ⚠️ Up 360% already - easy gains captured, harder gains ahead

If you own CLS stock:

- ✅ HOLD through earnings if long-term believer - AI infrastructure story intact

- 📊 Set mental stop at $280 (gamma support) to protect against catastrophic earnings miss

- 🎯 Consider taking 10-20% profits at $300-310 to derisk before earnings

- ⏰ If holding, you're betting on earnings beat + 2026 guidance confirmation

- 💪 Long-term (12-24 months), CLS could absolutely reach $400-440 if execution delivers

If you're watching from sidelines:

- ⏰ DO NOT chase before February 4th earnings - too much binary risk at $289

- 🎯 Best entry is post-earnings pullback to $270-280 gamma support (if it happens)

- 📈 If earnings CRUSH and stock gaps to $320-330, accept you missed the move

- 🚀 Better to pay $275 with earnings clarity than $289 with uncertainty

- 💡 Consider small starter position at $285-290, add MUCH more at $270-280 on any dip

If you want options exposure:

- 🛡️ Conservative: Sell March bull put spreads AFTER earnings ($280/$270) - collect premium, defined risk

- ⚖️ Balanced: Buy June $320 calls (less aggressive than $360 strike, higher probability)

- 🚀 Aggressive: Copy the $360 calls BUT size appropriately (1-3% portfolio max!)

Mark your calendar - Key dates:

- 📅 February 4, 2026 (Tuesday) before market open - Q4 FY2025 earnings report (30 DAYS!)

- 📅 February 5 - Post-earnings price action and analyst reactions

- 📅 March 20 - Quarterly triple witch (±23% implied move window)

- 📅 April 2026 - Q1 FY2026 earnings (proof 2026 guidance is tracking)

- 📅 June 18, 2026 - Expiration of this $2.4M call trade

- 📅 Late 2026 - DS6000/DS6001 1.6TbE switch commercial availability

Final verdict: The $2.4M institutional call buy is a HIGH-CONVICTION bet on CLS's AI infrastructure story. The fundamentals support the bull case - market share leadership, hyperscaler partnerships, 31% projected 2026 growth. BUT at 35x forward P/E after 360% YTD gain, the risk/reward for NEW aggressive positioning is balanced at best.

If you believe in the AI infrastructure buildout and CLS's ability to execute, this is a compelling story. Just don't bet more than you can afford to lose, and recognize that Q4 earnings on February 4th will likely determine whether this $360 call bet looks brilliant or foolish.

The AI revolution is real. CLS is positioned to benefit. But timing and price matter. Choose your spots wisely. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 94.6 Z-score reflects this specific trade's size relative to recent CLS history - it does not imply the trade will be profitable or that you should copy it. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for 15-20% gaps either direction. The institutional call buyer may have complex portfolio strategies not applicable to retail traders.

About Celestica Inc.: Celestica operates as a supply chain solutions provider serving aerospace, defense, industrial, healthtech, communications, and enterprise markets. The company generates majority revenue from its Connectivity & Cloud Solutions segment, manufacturing servers, storage, and networking equipment for hyperscaler data centers, with a market cap of $34.79 billion in the Electronics Manufacturing Services industry.