🔥 CLX: $1.4M LEAPS Put Sale Bets on Multi-Year Recovery from 52-Week Lows!

📅 December 24, 2024 | 🐋 Whale Activity Detected

🎯 The Quick Take

Someone just collected $1.4 MILLION in premium selling 2-year puts on Clorox at $135 - a strike that's 37.8% ABOVE the current stock price of $97.94! This isn't panic selling, it's a massive bullish bet that CLX will recover from its brutal 39.72% yearly decline by January 2027. Real talk: This is institutional-grade optimism on a deeply beaten-down consumer staples name.

💰 Company Overview

The Clorox Company (NYSE: CLX) - Since its inception over 100 years ago, Clorox has expanded to operate in a variety of consumer product categories, including cleaning supplies, laundry care, trash bags, cat litter, charcoal, food dressings, water filtration products, and natural personal care products. The firm maintains a diverse portfolio spanning household brands like Glad, Brita, Hidden Valley, and Burt's Bees, with over 80% of revenues generated domestically.

- Market Cap: $11.88 billion

- Industry: Specialty Cleaning, Polishing and Sanitation Preparations

- Current Price: $97.94 (near 52-week low of $97.39)

- 52-Week Range: $97.39 - $164.41

- Year Performance: Down 39.72% (brutal decline from highs)

💰 The Option Flow Breakdown

📊 What Just Happened

| Field | Details |

|---|---|

| Symbol | CLX |

| Option Symbol | CLX20270115P135 |

| Trade Type | SELL TO OPEN (Cash-Secured Put) |

| Strike Price | $135.00 |

| Expiration | 2027-01-15 (754 days out - LEAPS!) |

| Premium Collected | $39.50 per contract |

| Contracts | 350 |

| Total Premium | $1,382,500 |

| Open Interest | 361 contracts |

| Vol/OI Ratio | 0.97 (HIGH_ACTIVITY) |

| Z-Score | 235.99 (EXTREMELY_UNUSUAL) |

| Current Stock Price | $97.94 |

| Side | BID (seller hitting the bid for immediate execution) |

🤓 What This Actually Means

Translation for us regular folks: A big player just said "I'm willing to buy CLX at $135 two years from now, and I'll get paid $39.50 per share TODAY for making that promise."

Here's the kicker - the stock is currently at $97.94. That means they're agreeing to buy the stock at a price 37.8% HIGHER than where it trades now!

The real play here:

- They keep the $1.4M premium no matter what happens

- Breakeven: $135 - $39.50 = $95.50

- If CLX stays above $95.50 by January 2027, they profit

- If CLX recovers anywhere close to $135, they win big

- This is a MASSIVELY BULLISH 2-year bet on CLX recovery

The Z-Score of 235.99 means this trade is extremely unusual - we're talking about activity that's 235 times larger than average for CLX. This definitely isn't your neighbor Bob trading on Robinhood! 🐋

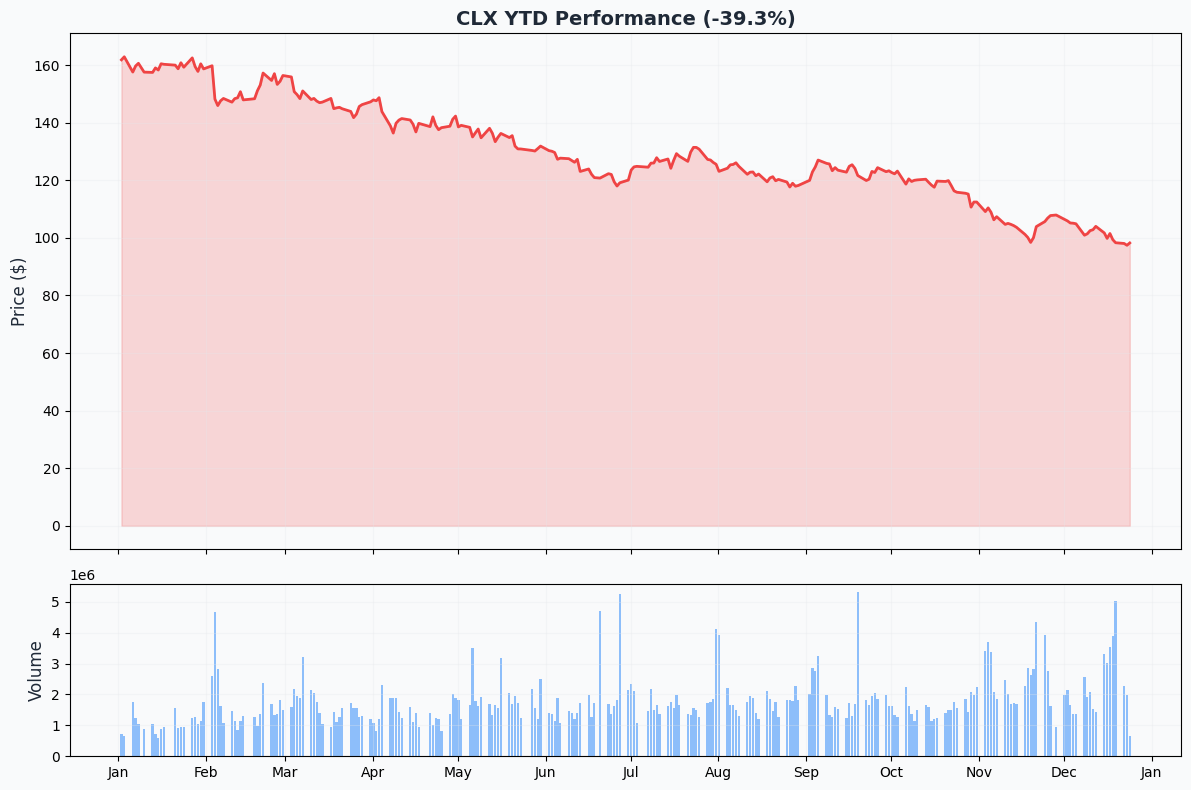

📈 Chart Check-Up

📉 YTD Performance: The Brutal Decline

CLX has been absolutely crushed this year, down nearly 40% from its highs near $164. The stock recently tested 52-week lows at $97.39, creating what could be a generational value opportunity - or a value trap. The YTD chart shows a relentless downtrend with multiple failed rallies, but the recent stabilization near $98 could signal capitulation selling is complete.

Key observations:

- Stock fell from $164 to $98 - a brutal $66 decline

- Recent stabilization near 52-week lows

- Cyberattack recovery period lapping comparisons

- ERP transition creating near-term headwinds

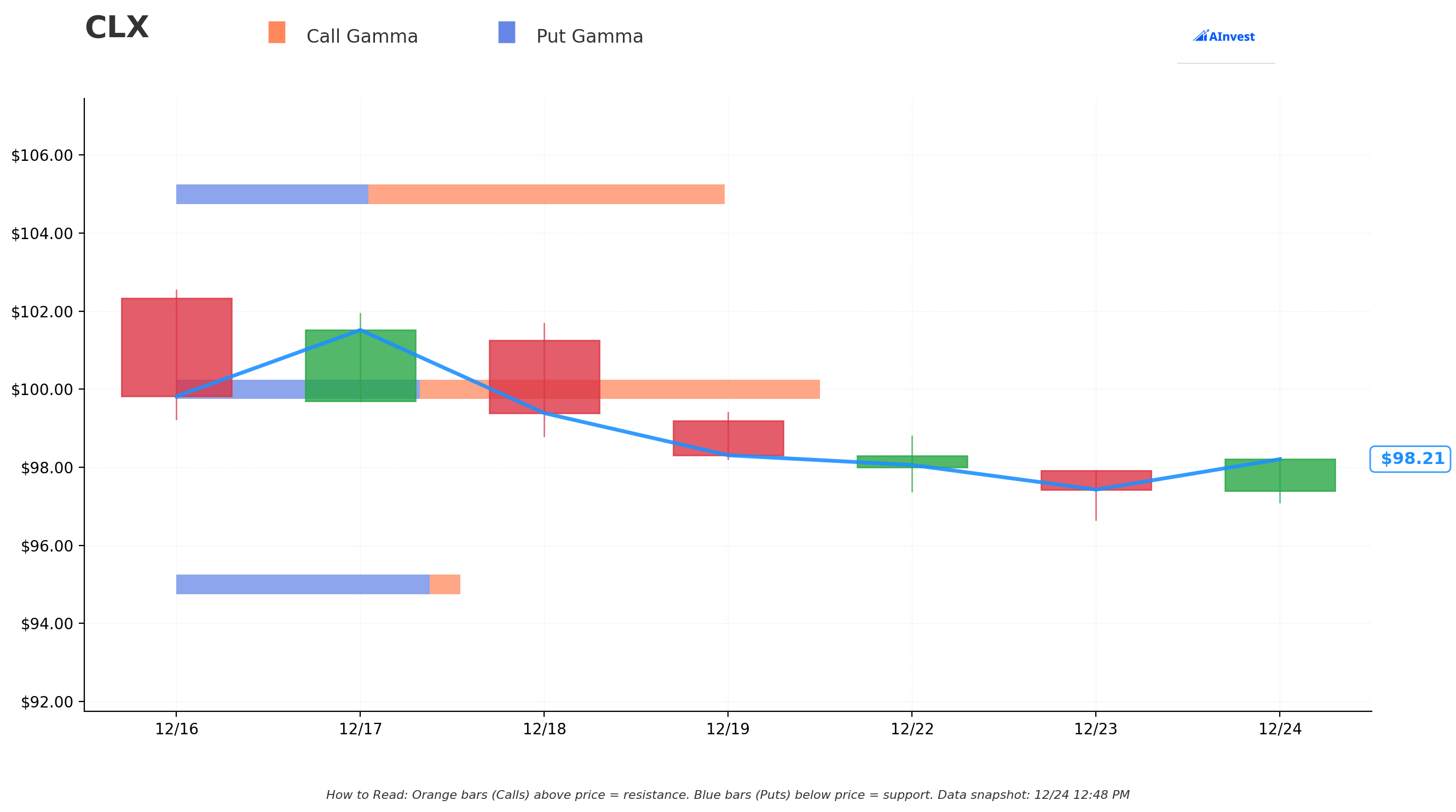

🔵 Gamma-Based Support & Resistance Analysis

Current Price: $98.25 (nearly perfect alignment with entry)

Major Resistance Levels (Call Gamma Above):

- 🟠 $100.00 - Strongest resistance (1.78% away) with 3.45M total GEX and net call gamma of +0.86M. This psychological level is heavily defended with 2.15M call GEX vs. 1.29M put GEX.

- 🟠 $105.00 - Second major resistance (6.87% away) with 2.94M total GEX and net call gamma of +0.89M. Break above $100 could trigger momentum toward this level.

- 🟠 $110.00 - Key resistance (11.96% away) with 0.97M total GEX. This represents the beginning of recovery territory.

- 🟠 $115.00 - Long-term target (17.05% away) with 0.45M total GEX.

Major Support Levels (Put Gamma Below):

- 🔵 $95.00 - Strongest support (3.31% below) with 1.52M total GEX and net put gamma of -1.19M. This is where the put seller's breakeven ($95.50) aligns perfectly with heavy put gamma!

- 🔵 $90.00 - Secondary support (8.40% below) with 0.53M total GEX. Downside floor if recovery thesis breaks.

- 🔵 $85.00 - Deep support (13.49% below) with 0.12M total GEX.

Net GEX Bias: Bullish (+1.40M call gamma vs. -5.00M put gamma total)

The gamma landscape shows CLX trapped in a tight range between massive $95 support and formidable $100 resistance. The put seller's breakeven at $95.50 sits perfectly on top of the strongest gamma support level - smart positioning! If CLX can reclaim $100, there's clear runway to $105-$110 based on gamma positioning.

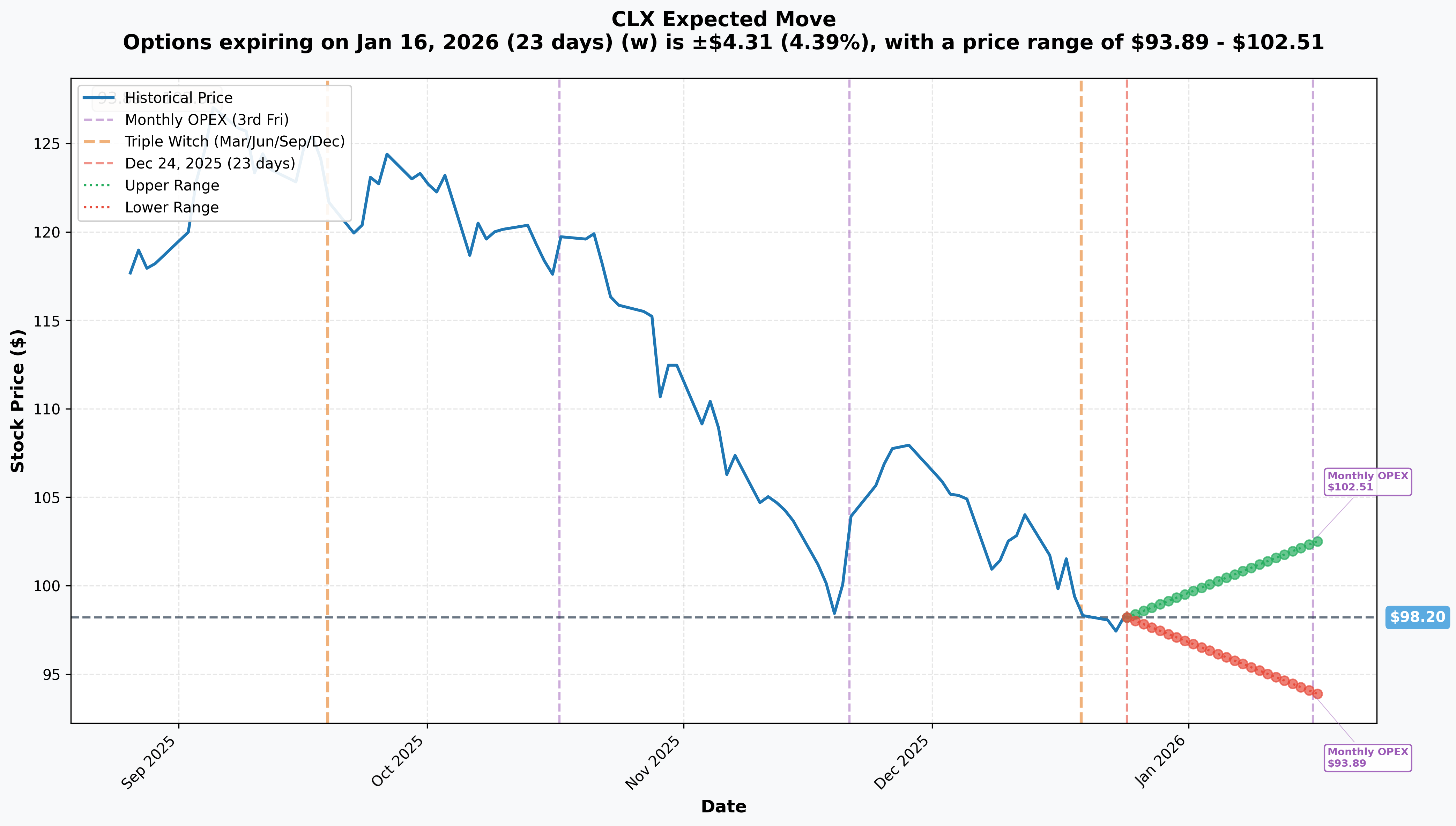

📊 Implied Move Analysis

Monthly OPEX (2026-01-16) - 23 Days Out:

- Implied Move: 4.39% ($4.31)

- Upper Range: $102.51 (above $100 resistance!)

- Lower Range: $93.89 (below $95 support)

- Reliability: High (based on monthly option volume)

The market is pricing a 4.39% move into January monthly OPEX, with the upper range at $102.51 suggesting the market expects CLX to break through $100 resistance in the next 23 days. The lower range at $93.89 sits just below the critical $95 gamma support, indicating limited downside risk is priced in.

Key Insight: The implied move suggests CLX could test $102+ by mid-January, which would validate the bullish thesis of the LEAPS put seller. The narrow range ($93.89-$102.51) indicates the market expects resolution of the current consolidation pattern soon.

🎪 Catalysts

📅 Upcoming Events (Why This Could Work)

Immediate Term:

- January 29, 2026 - Q1 FY2026 Earnings (before market open). Key metrics: ERP transition impact normalization, organic sales growth, margin expansion continuation.

- January 31, 2026 - Glad Joint Venture Acquisition Completion. Clorox acquires P&G's 20% stake at fair market value, gaining full operational control of Glad bags and wraps business. This could enhance margins and strategic flexibility.

FY2025 Guidance (Confidence Building):

- Adjusted EPS Target: $6.95-$7.35 (13-19% YoY growth) - Management raised guidance despite headwinds

- Organic Sales Target: 4-7% growth

- Gross Margin Expansion: 125-150 basis points (ninth consecutive quarter of expansion!)

Long-Term Recovery Drivers:

- ERP System Stabilization: Full stabilization expected by mid-FY2026. Once headwinds reverse, could unlock organic growth.

- Cyberattack Recovery Complete: Market share restored in 7 of 8 categories, distribution and supply fully restored per CEO Linda Rendle.

- Sustainability Initiatives: M2030 partnership for net-zero emissions by 2050, EcoClean product line winning industry awards.

Analyst Support:

- Average Price Target: $131.82 (35% upside from current levels)

- Bull Case PT: $170 from TD Cowen (73% upside!)

- Consensus: Hold with 1 Buy, 9 Hold, 2 Sell

📜 Recent Events (What Led Us Here)

Q2 FY2025 Results (Reported February 3, 2025):

- Revenue: $1.69B, down 15% YoY - Tough comps from cyberattack recovery

- Adjusted EPS: $1.55, down 28% YoY but beat expectations

- Gross Margin: 43.8%, up 30bps YoY - ninth consecutive quarter of expansion!

Q1 FY2026 Results (November 2024):

- Revenue: $1.43B (beat $1.39B consensus)

- EPS: $0.85 (beat $0.82 forecast)

- Stock Reaction: Declined 2.95% despite beat - market focused on ERP headwinds

The Pain Points:

- Cyberattack (August 2023): 47 days to restore operations, lost 1/3 of distribution and market share. $57M total costs through March 2024.

- ERP Transition Disruptions: Organic sales declined 3% in Q1 FY2026 due to implementation challenges (underlying: only 1% decline).

- Category Growth Stagnation: Overall categories growing only 0-1% per management.

Why The Stock Tanked:

- Lapping difficult cyberattack recovery comparisons

- ERP system causing temporary shipment timing issues

- Sluggish category growth (0-1%) limiting organic expansion

- Analyst downgrades: Deutsche Bank ($135→$128), BofA ($135→$125), Morgan Stanley ($137→$125)

🎲 Price Targets & Probabilities

Using gamma levels, implied moves, and fundamental catalysts, here's the roadmap:

🚀 Bull Case (40% Probability): $105-$115 by January 2027

Path to Victory:

- January 2026 earnings show ERP headwinds reversing ✅

- Glad JV acquisition completed, margin expansion accelerates ✅

- Q1 FY2026 guidance demonstrates sustained 4-7% organic growth ✅

- Analyst price targets ($131 average) start getting hit ✅

- Stock reclaims $100, momentum carries to $105 gamma resistance ✅

Price Targets:

- Near-Term (Q1 2025): $102-$105 (breaking above implied move upper range)

- Mid-Term (Mid-2025): $110-$115 (recovery trajectory confirmed)

- Long-Term (January 2027): $125-$135 (approaching put seller's strike)

Why This Works:

- Gross margin expansion continuing for 9 quarters straight shows operational excellence

- Cyberattack recovery complete - no more tough comps dragging results

- ERP stabilization by mid-2026 unlocks true organic growth potential

- 81% institutional ownership with Vanguard (12%) and BlackRock (5.76%) supporting

- Consumer staples sector rotation as economy stabilizes

⚖️ Base Case (40% Probability): $95-$105 Range-Bound

The Reality:

- Stock consolidates between $95 gamma support and $100 resistance for several quarters

- Earnings beat expectations but stock trades sideways on skepticism

- ERP headwinds take longer than expected to fully resolve

- Category growth remains tepid at 0-1%, limiting upside

- Put seller still wins (collects premium, stock stays above $95.50 breakeven)

Price Targets:

- 2025: $95-$105 range (consolidation mode)

- January 2027: $100-$110 (modest recovery)

Why This Happens:

- Market remains skeptical despite execution improvements

- Customer concentration risk (Walmart 25%, Top 5 = 50%) caps valuation

- Private label competition intensifies in stagnant categories

- Economic uncertainty delays consumer staples multiple expansion

😰 Bear Case (20% Probability): Below $95 - Put Seller Assigned

Nightmare Scenario:

- ERP transition costs spiral higher, margins compress instead of expanding

- Major customer (Walmart) renegotiates terms, pressuring revenue

- Private label competition accelerates in key categories

- Economic recession drives consumer trade-down

- Stock breaks below $95 gamma support, put seller gets assigned at $135

Price Targets:

- Downside: $85-$90 (deep support levels)

- Put Seller Loss: If assigned at $135 with stock at $85, effective cost = $135 - $39.50 premium = $95.50. Still only -10% loss.

Why This Happens:

- Category growth remains at 0-1% indefinitely

- Consumer shift to private label accelerates permanently

- ERP system never fully stabilizes

- Another cyberattack or operational disruption

- Tariff uncertainty materializes into margin pressure

Real Talk: Even in this scenario, the put seller's downside is limited to $95.50 effective cost on a $97.94 stock - only -2.5% risk! That's the beauty of collecting $39.50 in premium.

💡 Trading Ideas

🛡️ Conservative: The "Show Me" Approach

Strategy: Wait and watch, but prepare for entry

- Action: Set price alerts at $95 (support test) and $102 (breakeven above resistance)

- Entry Point: Buy shares if stock tests $95 support with volume

- Stop Loss: $92 (below deep support)

- Target: $110-$115 (recovery play)

- Timeline: 6-12 months

- Why This Works: You get better risk/reward than the put seller by buying actual stock at support rather than selling puts. If the bull thesis is right, you participate fully in the recovery with limited downside at $95 support.

Who This Is For: Risk-averse investors who want Clorox exposure but need evidence of stabilization first.

⚖️ Balanced: The "Mini Whale" Strategy

Strategy: Sell shorter-dated puts to collect premium while building position

- Action: Sell 1-2 CLX April 2025 $95 Puts (collect ~$3-4 premium)

- Max Profit: $3-4 per contract ($300-400 total)

- Max Risk: Assigned at $95, effective cost ~$91-92 (stock currently $97.94)

- Breakeven: $91-92

- Probability of Profit: ~65-70% (stock needs to stay above $95 into April)

- Why This Works: You mimic the whale's strategy but with shorter duration and less capital. If assigned, you own CLX at $91-92, a 6-7% discount to current price and right at gamma support. If not assigned, you collect premium and repeat.

Who This Is For: Experienced option traders comfortable with assignment who are bullish medium-term but want to get paid to wait.

🚀 Aggressive: The "LEAPS Call Lottery Ticket"

Strategy: Buy deep out-of-the-money LEAPS calls for leveraged upside

- Action: Buy CLX January 2027 $120 Calls (likely ~$8-10 per contract)

- Cost: $800-1,000 per contract

- Breakeven: $128-130 (needs 30%+ gain from current price)

- Max Profit: Unlimited above $128-130

- Max Loss: $800-1,000 (premium paid)

- Why This Works: If the put seller is right and CLX recovers to $135 by January 2027, your $120 calls would be worth $15+ ($1,500 value on $800-1,000 cost = 50-88% gain). If CLX mean-reverts to analyst PT of $131, you're profitable. You're essentially buying the same bet as the whale but with defined risk and asymmetric upside.

Who This Is For: YOLO traders with high risk tolerance who believe CLX is a coiled spring at 52-week lows and analysts' $131 average PT is achievable.

Risk Warning: You can lose 100% of premium paid if CLX stays below $120 by January 2027. Only risk money you can afford to lose completely.

⚠️ Risk Factors (Real Talk Time)

What Could Torpedo This Trade:

🏢 Company-Specific Risks:

- ERP System Failure: If the $560-580M technology investment doesn't pay off and organic sales keep declining

- Customer Concentration: Walmart = 25% of revenue. One bad renegotiation could crush margins

- Private Label Onslaught: Increasing competition from store brands in cat litter and trash bags

- Cyberattack 2.0: Another security breach could devastate already-fragile investor confidence

📊 Market/Macro Risks:

- Category Stagnation: 0-1% category growth continues indefinitely - no rising tide to lift CLX boat

- Economic Recession: Consumer trade-down accelerates, premium products suffer

- Tariff Uncertainty: FY2025 outlook excludes tariff impacts - trade policy changes could pressure margins

- Interest Rates: Higher-for-longer rates keep money in bonds instead of beaten-down stocks

💸 Option-Specific Risks:

- Time Decay for Call Buyers: LEAPS calls lose value every day if stock doesn't move

- Assignment Risk for Put Sellers: You WILL get assigned if stock drops below strike by expiration

- Liquidity Risk: CLX options aren't as liquid as mega-caps - wider bid/ask spreads

- Implied Volatility Crush: If uncertainty resolves positively, IV collapses and option values drop

🔴 Red Flags to Monitor:

- Insider sales accelerating (currently 7 sales, 0 purchases in 6 months)

- Analyst downgrades continuing (recent cuts from Deutsche Bank, BofA, Morgan Stanley)

- Quarterly earnings misses or guidance reductions

- Market share losses in core categories

- Margin compression instead of expansion

Bottom Line: The put seller has 2+ years and $39.50/share of cushion. Call buyers and put sellers with shorter expirations have much less room for error.

🎯 The Bottom Line

Here's the deal: A sophisticated player just made a $1.4M bet that Clorox's nightmare is over. They're collecting huge premium selling $135 puts on a $98 stock - that's 37.8% of upside cushion before they even start losing money.

The Bull Case is Compelling:

- Stock at 52-week lows with 35% upside to analyst average PT

- Nine consecutive quarters of gross margin expansion proves operational excellence

- Cyberattack recovery complete, ERP headwinds temporary

- Glad JV acquisition provides strategic flexibility

- Institutional ownership at 81% with smart money (Vanguard, BlackRock) holding

But The Risks Are Real:

- Revenue down 15% YoY, categories growing 0-1%

- Customer concentration creates binary risk

- Insiders selling (7 sales, 0 buys in 6 months)

- Multiple analyst downgrades in recent months

- Private label competition intensifying

My Take: This isn't a trade - it's a 2-year investment thesis. The put seller believes CLX at $98 represents deep value in a quality consumer staples name that's been unfairly punished. The $39.50 premium provides a massive margin of safety (breakeven at $95.50 vs. $98 current price).

Action Plan:

📊 If You Own It: Hold through the recovery. January 2026 earnings and Glad acquisition are key inflection points. Stop loss at $92 if you need one.

👀 If You're Watching: Set alerts at $95 (support test = buy opportunity) and $102 (breakout = momentum confirmed). January 29 earnings will be critical.

😰 If You're Bearish: The put seller might be early but has 754 days and $39.50/share cushion. Even bears should respect that risk management. If you're short, watch the $95 support like a hawk.

Mark Your Calendar:

- January 29, 2026 - Q1 FY2026 Earnings (before market open)

- January 31, 2026 - Glad JV acquisition closes

- Mid-2026 - ERP stabilization expected

Final Word: This is a bet on mean reversion in a quality business at historically cheap valuations. The put seller is getting paid $1.4M to wait 2 years for CLX to recover from temporary headwinds. That's not crazy - that's patient capital at work. The question is whether temporary becomes permanent. 🤔

⚠️ Disclaimer

This analysis is for educational and informational purposes only and should not be considered financial advice. Options trading involves substantial risk of loss and is not suitable for all investors. Past performance does not guarantee future results. The author may or may not hold positions in the securities discussed. Always consult with a qualified financial advisor before making investment decisions and only trade with capital you can afford to lose entirely.

Options can expire worthless, and you can lose 100% of your investment. The specific trades mentioned are examples only and may not be suitable for your investment objectives, financial situation, or risk tolerance. The catalysts, price targets, and probabilities discussed are the author's opinions and may not materialize.

Analysis generated December 24, 2024. Data sources: ThetaData (option flow), Polygon.io (company data), Clorox Investor Relations, TipRanks, Investing.com, and company filings.