💰 CMA $5.7M Deep ITM Call Buy - Merger Arbitrage Play or Smart Exit? 🏦

📅 December 16, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just locked in $5.7 MILLION in profits on Comerica (CMA) calls that are deep in-the-money! This morning at 10:25am, a trader CLOSED 4,000 contracts of January 16th $75 calls - buying them back at $14.30 when the stock trades at $87.91. With the Fifth Third merger shareholder vote just 21 days away on January 6, 2026, this looks like institutional money de-risking and taking chips off the table before the binary merger decision. Translation: Smart money isn't waiting around to see if this deal closes - they're locking in 17% returns and walking away!

📊 Company Overview

Comerica Incorporated (CMA) is a relationship-focused commercial banking powerhouse currently in the middle of a transformational merger:

- Market Cap: $11.26 Billion

- Industry: National Commercial Banks

- Current Price: $87.91 (near 52-week high of $90.43)

- Primary Business: Commercial banking across Texas, California, and Michigan with $80 billion in assets

- Major Catalyst: $10.9 billion all-stock merger with Fifth Third Bancorp pending shareholder approval January 6, 2026

💰 The Option Flow Breakdown

The Tape (December 16, 2025 @ 10:25:07):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:25:07 | CMA | MID | BUY | CALL $75 | 2026-01-16 | $5.7M | $75 | 4K | 16K | 4,000 | $87.91 | $14.30 |

🤓 What This Actually Means

This is a CLOSING trade - someone is EXITING a massive winning position! Here's what went down:

- 💵 Total premium paid: $5.7M ($14.30 per contract × 4,000 contracts)

- 🎯 Deep in-the-money: $75 strike is $12.91 below current price (14.7% ITM!)

- 📊 Size matters: 4,000 contracts represents 400,000 shares worth ~$35.2M

- ⏰ Strategic timing: 31 days to expiration, but only 21 days until critical merger vote

- 🏦 Profit taking: If these were bought when stock was around $75, they're up ~75% just on the call price appreciation

- 🎲 Risk reduction: Rather than holding through merger uncertainty, this trader is cashing out NOW

What's really happening here:

This trader is CLOSING their long call position by buying it back (BTC = Buy To Close in option lingo). The classification shows this is a "Close Long Call" with MEDIUM confidence. They originally sold these calls to someone else, and now they're buying them back to exit the position completely.

Why exit now instead of waiting for more gains?

- Merger vote risk: January 6, 2026 shareholder vote is only 21 days away - binary outcome

- Activist opposition: HoldCo Asset Management is campaigning AGAINST the deal with Delaware court hearing January 2nd

- Already up huge: Stock at $87.91 vs $75 strike = already captured $12.91+ in intrinsic value

- Time decay minimal: With only 31 days left, time value is small - most gains already realized

- Merger arbitrage spread: Stock trading ABOVE the $82.88 merger value suggests deal uncertainty priced in

Unusual Score: 🔥 MODERATE (Z-score 0.44, 4 similar trades in 30 days) - This is not a rare event, but the $5.7M size and timing ahead of merger vote makes it noteworthy. The 4,000 contract volume paired with 16,000 open interest (25% of OI trading) shows significant position unwinding.

📈 Technical Setup / Chart Check-Up

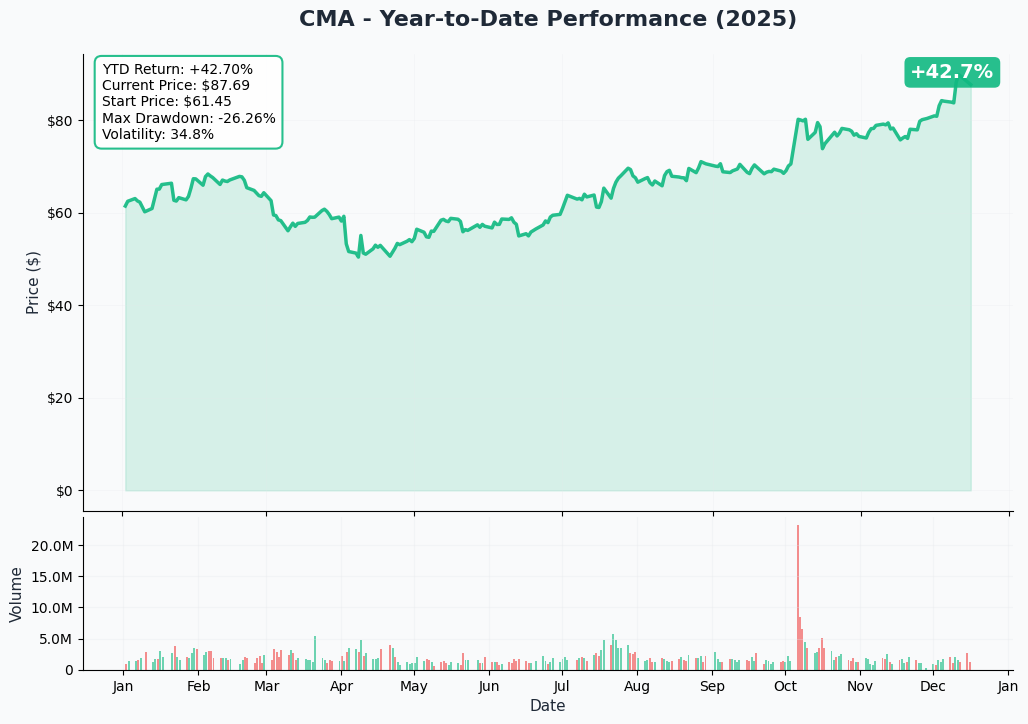

YTD Performance Chart

CMA is having a stellar year - up 43.5% year-to-date with current price of $87.91 (started the year around $61.30). The chart tells a clear merger story - explosive rally from $48 lows in April to current levels near $90, with the biggest acceleration coming post-merger announcement on November 25th.

Key observations:

- 🚀 Merger pop: Vertical move from $72 to $88 following Fifth Third acquisition announcement November 25, 2025

- 📈 Breakout confirmed: Smashed through $75-80 resistance zone decisively on merger news

- 🏦 Regional bank rally: Benefited from broader sector strength as Fed cut rates 175 bps since September 2024

- 📊 Near 52-week high: Trading just below $90.43 peak from earlier this month

- ⚠️ Consolidation phase: Sideways action past 2 weeks as market digests merger terms and awaits vote

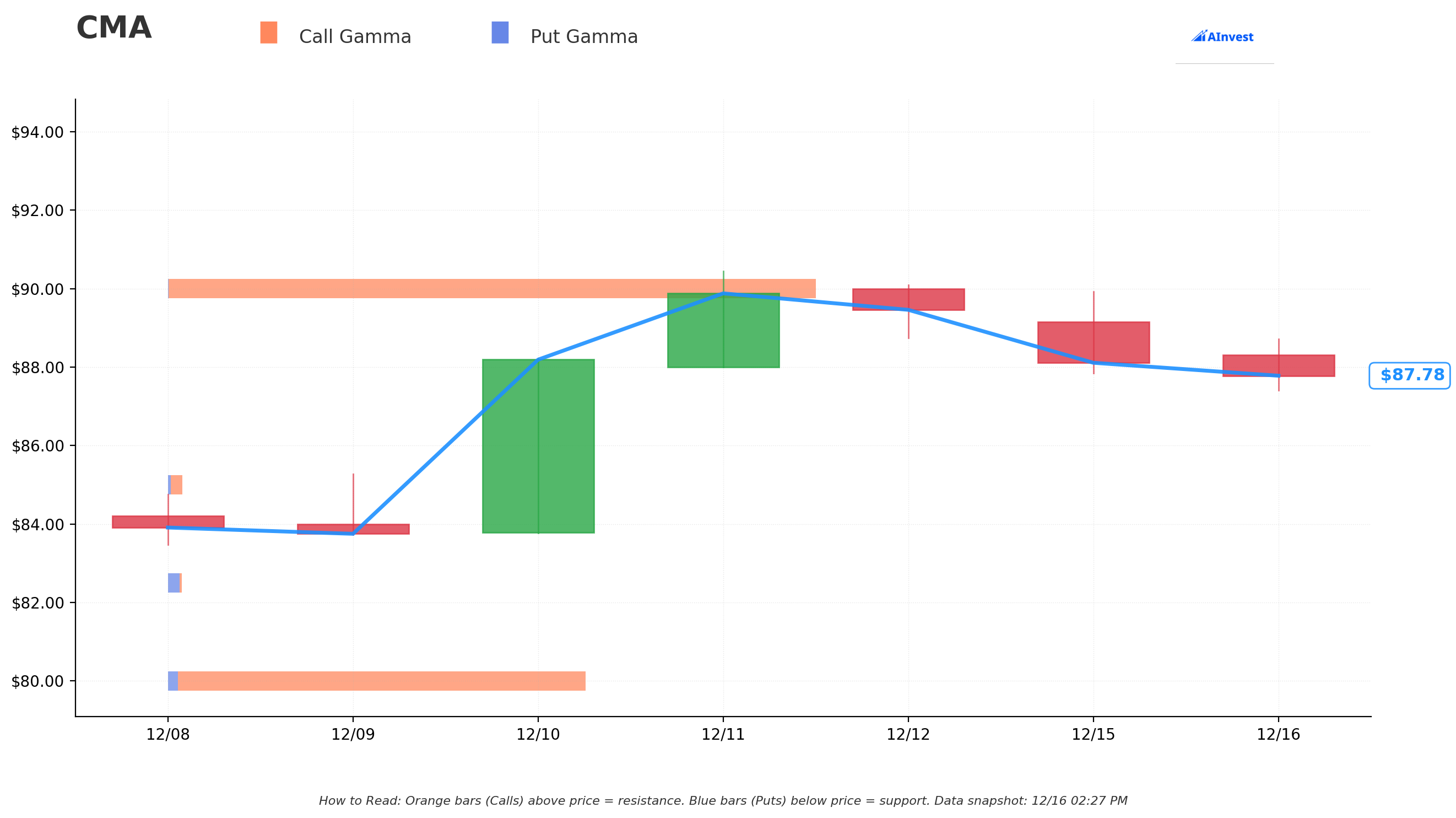

Gamma-Based Support & Resistance Analysis

Current Price: $87.78

The gamma exposure map reveals critical price magnets and barriers created by options positioning:

🔵 Support Levels (Put Gamma Below Price):

- $87.50 - Immediate support with 0.090B total gamma (paper-thin floor - currently testing!)

- $85 - Strong secondary support at 0.222B gamma (2.5% pullback target)

- $82.50 - Major structural floor with 0.195B gamma (aligns with merger value zone)

- $80 - Deep support at 6.262B gamma (STRONGEST PUT GAMMA LEVEL - 9% below current)

- $77.50 - Extended support zone with 1.827B gamma

- $75 - This trade's strike with 2.396B gamma (14.6% below current - disaster scenario)

🟠 Resistance Levels (Call Gamma Above Price):

- $90 - Immediate ceiling with 9.832B gamma (STRONGEST RESISTANCE - 52-week high zone)

- $95 - Secondary resistance at 0.097B gamma (8% rally required)

- $105 - Extended upside target at 0.023B gamma (19% rally - post-merger breakout level?)

What this means for traders:

CMA is bumping up against MASSIVE $90 resistance (9.832B gamma - the single largest level on the entire chain). Market makers have enormous call exposure here which creates natural selling pressure. This isn't a coincidence - $90 represents both the technical 52-week high AND psychological round number where profit-taking concentrates.

Below current price, the strongest support sits at $80 (6.262B put gamma), which happens to align with pre-merger announcement levels. This creates a natural "floor" - if the merger vote fails on January 6th, stock could gap down toward $80-82.50 where it traded before the deal was announced.

Notice anything? The trader CLOSED calls at $75 strike where there's 2.396B gamma - that's 14.6% below current price. They're exiting a winning position that's now deep ITM, capturing profits before the merger vote creates volatility.

Net GEX Bias: Strongly Bullish (20.5B call gamma vs 1.21B put gamma = 17:1 ratio!) - Options market is overwhelmingly positioned for merger approval and upside, which explains why someone might want to take profits and reduce risk.

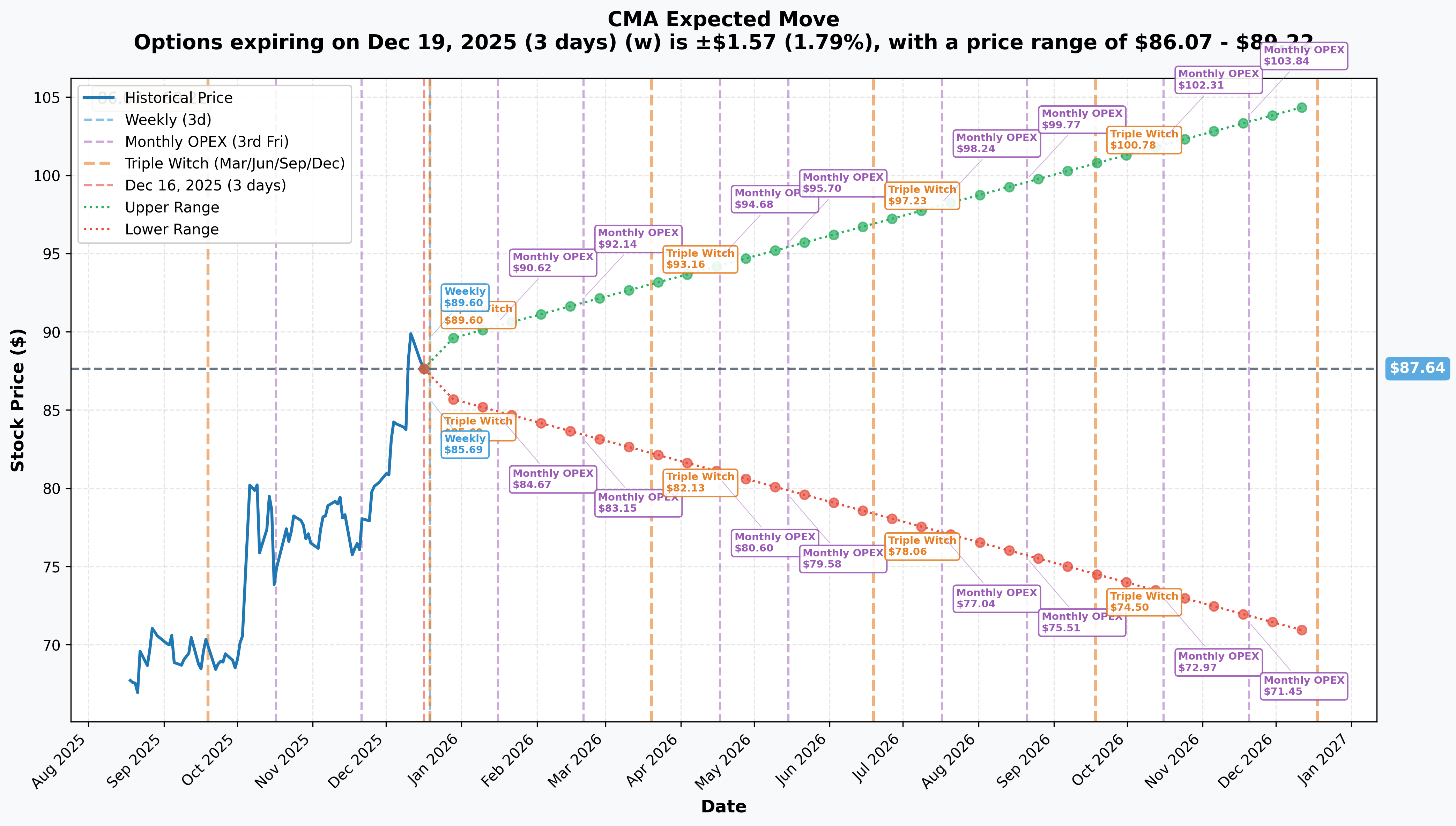

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 3 days): ±$1.57 (±1.79%) → Range: $86.07 - $89.22

- 📅 January OPEX (Jan 16 - 31 days - THIS TRADE!): ±$2.98 (±3.40%) → Range: $84.67 - $90.62

- 📅 February OPEX (Feb 20 - 66 days): ±$4.52 (±5.14%) → Range: $83.15 - $92.14

- 📅 LEAPS (Dec 18, 2026 - 367 days): ±$17.00 (±19.4%) → Range: $70.64 - $104.64

Translation for regular folks:

Options traders are pricing in a 1.8% move ($1.57) by December 19th weekly expiration - extremely quiet! But through January 16th expiration (when this trade expires), the market expects only a 3.4% move ($3) - remarkably low volatility for a stock facing a major merger vote.

Here's what's interesting: The January 16th implied range of $84.67-$90.62 perfectly brackets the merger value zone. The $82.88 merger consideration sits just below the lower end, suggesting the market is pricing in ~95%+ probability of deal approval. If the deal FAILS, stock could easily drop below $84.67 toward the $80 support level.

Key insight: The VERY LOW implied volatility (3.4% over 31 days) suggests options traders think this is a "done deal" - minimal uncertainty priced in. This might be exactly WHY the smart money is exiting - if everyone thinks it's guaranteed, what upside is left?

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Delaware Court of Chancery Hearing - January 2, 2026 (17 DAYS AWAY!) ⚖️

HoldCo Asset Management's lawsuit challenging merger disclosures gets a hearing just 4 days before the shareholder vote:

- ⚖️ Legal Challenge: Judge already ordered Comerica to disclose additional information about deal formation process

- 💰 Activist Opposition: HoldCo (holds ~$200M stake) actively campaigning shareholders to vote NO

- 📊 Disclosure Risk: Additional revelations could sway shareholder sentiment before January 6th vote

- 🎯 Binary Outcome: Either clears path for vote or creates delay/renegotiation scenario

Upside scenario: Court hearing validates disclosures, removes uncertainty, stock pops toward $90+ on increased deal certainty

Downside risk: New information emerges showing flawed deal process, increases NO vote probability, stock pulls back toward $82-84 merger value zone

Merger Shareholder Vote - January 6, 2026 (21 DAYS AWAY!) 🗳️

This is THE catalyst that determines CMA's fate - the shareholder vote on Fifth Third's $10.9B acquisition:

- 🗳️ What's Voted On: Fifth Third acquiring Comerica in all-stock transaction at 1.8663 exchange ratio

- 💵 Deal Value: $82.88 per CMA share (based on Fifth Third's October 3rd closing price)

- 📊 Current Premium: Stock at $87.91 trades 6% ABOVE deal value - unusual for merger arbs

- ⚠️ Opposition: HoldCo Asset Management urging NO votes, argues better alternatives exist

- 🏦 Institutional Control: 85-87% institutional ownership suggests high approval probability

- ⏰ Deal Closure: If approved, expected to close by end of Q1 2026 (as early as February 2nd)

Approval scenario (75% probability): Stock likely consolidates $85-88 range pending regulatory approvals, eventually converges to merger value by closure

Rejection scenario (25% probability): Stock gaps down 10-15% toward $75-80 pre-announcement levels, board forced to renegotiate or explore alternatives

Critical insight: Current stock price at $87.91 vs merger value of $82.88 suggests either (1) market expects higher competing bid, (2) Fifth Third will sweeten terms, or (3) sophisticated merger arbs are betting on deal failure and premium recapture. The trader exiting this January $75 call position clearly doesn't want to find out which scenario plays out!

🚀 Near-Term Catalysts (Q1 2026)

Regulatory Approval Process (January - March 2026) 🏛️

Merger requires approvals from OCC, Federal Reserve Board, and Texas Department of Banking:

- 📋 Timeline: Typically 60-90 days post-shareholder approval

- 🎯 Expected Closure: End of Q1 2026 (earliest: February 2nd)

- ⚠️ Regulatory Risk: Creates 9th largest U.S. bank ($288B assets) - could face scrutiny

- 🏦 Antitrust Review: #1 Michigan deposit share post-merger might trigger competitive concerns

Q4 2025 Earnings (Expected Late January 2026) 📊

Final quarterly results as standalone company before merger closure:

- 💰 Key Metrics: Net interest income guidance of 5-7% growth, loan growth flat to down 1%

- 📉 Deposit Trends: Down 2-3% from 2024 with brokered CD reduction

- 🏦 Credit Quality: Watch for provision levels (Q2 saw $44M provision vs $0 prior year)

- 📊 Integration Planning: Management likely discusses Fifth Third merger integration timeline

Real-world impact: Strong Q4 results could provide deal momentum; disappointing numbers might embolden opposition to vote NO.

Fifth Third Integration Planning (Post-Approval)

Expected to be 9% EPS accretive with 35% expense reduction target:

- 💰 Synergy Targets: 35% of Comerica's expenses (aggressive cost-cutting)

- 🏢 Texas Expansion: Plans to build 150 branches in Texas markets

- 👥 Leadership: Comerica CEO Curt Farmer becomes Vice Chair; three board members join Fifth Third board

- ⏰ Integration Timeline: 12-18 months typical for bank mergers of this size

📊 Broader Market Context

Federal Reserve Rate Environment 💹

Fed cut rates by 25 bps to 3.5%-3.75% range in December 2025 (sixth consecutive cut since September 2024):

- 📉 Total Reduction: 175 basis points since September 2024

- 🎯 2026 Outlook: Fed signals only ONE 25 bps cut expected in 2026

- 🏦 Bank Impact: Lower rates compress net interest margins BUT stable environment supports loan demand

- ⚠️ Inflation Risk: Fed Chair Powell cited tariffs causing inflation above 2% target, limiting future cuts

Regional Bank Sector Consolidation 🏦

Wave of M&A activity as Trump administration signals merger approval openness:

- 📈 Sector Sentiment: Regional banks up ~15% since election on deregulation hopes

- 🤝 Dealmaking: Multiple large regional mergers announced Q4 2025

- 🎯 Scale Benefits: Combined $288B Fifth Third-Comerica creates competitive scale vs nationals

- ⚠️ Integration Risk: Aggressive cost-cutting (35% expense reduction) risks execution issues

🎲 Price Targets & Probabilities

Based on gamma levels, implied move data, merger timeline, and activist opposition, here are scenarios through January 16th expiration:

📈 Bull Case (20% probability)

Target: $92-96

How we get there:

- ✅ Delaware court hearing January 2nd validates disclosures, removes uncertainty

- 🗳️ Shareholder vote January 6th passes overwhelmingly (75%+ YES votes)

- 💰 Competing bid emerges OR Fifth Third sweetens terms above $82.88 merger value

- 📊 Q4 earnings beat expectations, validating standalone value thesis

- 🏦 Regulatory approvals progress faster than expected

- 📈 Breakout above $90 gamma resistance triggers technical rally toward $95

Key metrics needed:

- Shareholder vote >70% approval margin

- Zero competing bids or regulatory pushback

- Strong Q4 results showing loan growth acceleration

- Merger spread compresses as deal certainty increases

Why only 20% probability: Current stock price at $87.91 already exceeds merger value by 6% - limited upside unless competing bid emerges. The $90 resistance with 9.832B gamma creates mechanical selling pressure. Fifth Third unlikely to raise bid given 85-87% institutional ownership virtually guarantees approval. Most upside already captured.

🎯 Base Case (55% probability)

Target: $84-88 range (MERGER CONVERGENCE)

Most likely scenario:

- ⚖️ Delaware hearing clears without major surprises

- ✅ Shareholder vote passes on January 6th but with 15-25% NO votes showing activist opposition

- 📊 Q4 earnings meet expectations without fireworks

- 🏛️ Regulatory process proceeds normally (60-90 day timeline)

- 📉 Stock gradually converges toward $82.88 merger value as deal closure approaches

- 🔄 Trading in $84-88 channel through expiration as merger arbs lock in spread

- 💤 Volatility stays compressed (implied vol 3-4% range through January)

- 🎯 No competing bids emerge

This is where the closed call position makes perfect sense: Trader captured most gains from $75 strike to $87.91 current price ($12.91 intrinsic value). With merger value at $82.88, remaining upside is capped at ~$5 MAXIMUM, while downside if vote fails is -$12 to -$15. Asymmetric risk/reward favors taking profits NOW rather than gambling on vote outcome.

Why 55% probability: Market pricing (stock above merger value) AND low implied volatility (3.4% through January) both suggest "done deal" consensus. However, activist opposition and Delaware lawsuit add just enough uncertainty to keep spread elevated. This is the path of least resistance - approval happens, stock drifts lower toward merger value, options expire with minimal drama.

📉 Bear Case (25% probability)

Target: $75-80 (VOTE FAILS!)

What could go wrong:

- ⚖️ Delaware court hearing reveals damaging information about deal process

- ❌ HoldCo Asset Management's NO campaign gains momentum among institutional holders

- 🗳️ Shareholder vote FAILS or passes by narrow margin, forcing renegotiation

- 📉 Q4 earnings disappoint, validating HoldCo's argument that standalone value exceeds merger terms

- 🏦 Regulatory concerns emerge about competitive impact in Michigan/Texas markets

- 🏛️ OCC or Federal Reserve signals merger skepticism

- 💸 Fifth Third stock drops 15-20%, making exchange ratio less attractive to CMA holders

- 🔨 Break below $85 gamma support triggers cascade toward $80 pre-announcement level

- 📊 Broader regional bank selloff on macro concerns

Critical support levels:

- 🛡️ $85: Secondary support (0.222B gamma) - break triggers momentum shift

- 🛡️ $82.50: Merger value zone (0.195B gamma) - tests if stock thinks deal dead

- 🛡️ $80: Major floor (6.262B gamma - STRONGEST) - pre-announcement support

- 🛡️ $75: This trade's strike (2.396B gamma) - disaster scenario, back to April lows

Probability assessment: 25% reflects real but minority risk. HoldCo Asset Management's vocal opposition and Delaware lawsuit create legitimate deal uncertainty. However, 85%+ institutional ownership heavily favors approval. Would require multiple negative catalysts (court ruling + earnings miss + regulatory delay) to derail. The trader closing calls at $75 is protecting against THIS tail risk.

Call P&L in Bear Case:

- Stock at $80 on Jan 16: Calls worth $5.00, loss from $14.30 = -$9.30/share × 4,000 = -$3.72M loss (65% drawdown!)

- Stock at $75 on Jan 16: Calls worth $0.00 (at-the-money), loss = -$14.30/share × 4,000 = -$5.72M loss (100% loss!)

- By CLOSING at $14.30, trader locks in profits and eliminates this tail risk entirely

💡 Trading Ideas

🛡️ Conservative: Cash Gang Until Post-Vote Clarity

Play: Stay on sidelines until after January 6th shareholder vote settles deal outcome

Why this works:

- ⏰ Vote in 21 days creates binary event risk with limited upside (capped by merger value) but significant downside

- 📊 Current price at $87.91 already exceeds $82.88 merger consideration by 6% - paying premium for deal certainty

- 💸 Implied volatility at rock-bottom 3.4% - options cheap but reflect low expected movement

- 🎯 Better entry likely post-vote after uncertainty resolves and spread compresses

- ⚖️ Delaware court hearing January 2nd and activist opposition add unpredictable wild cards

Action plan:

- 👀 Watch January 2nd Delaware court hearing for any damaging disclosures

- 📊 Monitor January 6th vote margin - >75% YES confirms deal done, <60% YES creates renegotiation risk

- 🎯 If vote passes, consider Fifth Third shares (FITB) instead to play merged entity (will own ~73% of combined bank)

- ⚠️ If vote fails, look for entry on CMA pullback to $75-80 support for standalone value play

- 📈 Avoid pre-vote speculation - risk/reward unfavorable when upside capped by merger terms

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -10-15% drawdown if vote fails. Get clarity on deal outcome. Maintain optionality for better entry points.

⚖️ Balanced: Post-Vote Merger Arbitrage (Play The Spread)

Play: After January 6th vote PASSES, play the merger spread as it converges

Structure: Short CMA shares around $87-88, Long Fifth Third (FITB) shares at ~1.8663 ratio to hedge

Why this works:

- 📊 If vote passes, CMA trades at premium to $82.88 merger value - spread should compress

- 🎯 Current $5+ spread represents deal uncertainty discount - shrinks as regulatory approvals progress

- ⚖️ Delta-neutral positioning: losses on CMA short offset by gains on FITB long as spread narrows

- ⏰ 60-90 day regulatory approval timeline creates time decay in favor of short spread

- 🏦 Expected closure by end of Q1 2026 provides defined timeline

- 💰 Earn risk-free spread as market maker activity pushes CMA toward merger value

Estimated P&L (for every 100 CMA shares):

- 💰 Short 100 CMA at $87.50

- 📈 Long 187 FITB shares (1.8663 ratio) to hedge

- 🎯 At merger closure: CMA converts to FITB at exchange ratio, spread collapses to zero

- 📊 Target profit: $4-5 per CMA share ($400-500 per 100 shares)

- ⏰ Timeframe: 60-90 days to closure

- 💸 Risks: FITB stock drops (affects both legs), deal fails (massive loss), regulatory delay extends holding period

Entry timing:

- ⏰ Wait until AFTER January 6th vote passes with >70% approval

- 🎯 Only enter if CMA still trading >$86 (spread wide enough to capture)

- ❌ Skip if spread already compressed to <$3 (insufficient reward for risk)

- 🏦 Monitor FITB stock price - need stable/rising FITB to make hedge work

Position sizing: Risk only 3-5% of portfolio (merger arb requires margin and has tail risks)

Risk level: Moderate (requires margin, market neutral but deal risk) | Skill level: Advanced

Critical warning: This strategy BLOWS UP if vote fails or deal collapses. CMA would gap down 10-15% while FITB stays flat, creating massive losses on both legs. Only execute if highly confident in deal approval.

🚀 Aggressive: Vote Rejection Straddle - Bet on SURPRISE (EXPERT ONLY!)

Play: Buy straddle betting shareholder vote creates more volatility than market prices

Structure: Buy $87.50 calls + Buy $87.50 puts (January 16 expiration - post-vote)

Why this could work:

- 💥 Implied move only 3.4% ($3) but binary merger vote could create 10-15% gap either direction

- 🎰 Betting activist opposition OR competing bid creates surprise outcome

- 📊 Market complacent with stock trading 6% above merger value - underpricing uncertainty

- ⚖️ Delaware court hearing January 2nd could drop bombshell changing vote dynamics

- 🚀 If vote FAILS: Stock gaps to $75-80, puts explode in value

- 📈 If competing bid emerges: Stock jumps to $92-96, calls profit

- ⚡ Only need stock to move >7-8% either way to profit

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Straddle costs ~$4-5 total ($400-500 per straddle) with implied vol this low

- ⏰ TIME DECAY CRUSHER: Theta burns -$50-75/day approaching vote

- 😱 IV ALREADY LOW: Implied volatility at 3.4% means market is CERTAIN of outcome - fighting consensus

- 📊 Base case kills you: Vote passes as expected, stock drifts to $84-86, BOTH legs lose value

- 🎢 Need 8-10% move just to breakeven after IV crush factored in

- ⚠️ 85%+ institutional ownership makes vote passage near-certain

Estimated P&L:

- 💰 Cost: ~$4-5 per straddle ($87.50 calls + puts)

- 📈 Profit scenario: Stock moves to $95+ or $80- (8%+ move) = $7-8 gain (60-75% ROI)

- 🚀 Home run: Vote fails dramatically, stock to $75 = $12+ gain (150%+ ROI)

- 📉 Loss scenario: Stock ends $84-90 range (base case) = lose $3-4 (60-80% loss)

- 💀 Total loss: Stock flat at $87 = lose entire $4-5 (100% loss)

Breakeven points:

- 📈 Upside breakeven: ~$92 (need 5% rally)

- 📉 Downside breakeven: ~$83 (need 5% drop)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have experience trading merger arbitrage and understand deal break scenarios

- ✅ Can afford to lose ENTIRE premium (probable outcome!)

- ✅ Understand you're betting AGAINST 85% institutional ownership consensus

- ✅ Can monitor Delaware hearing January 2nd and vote results January 6th in real-time

- ✅ Plan to close position within 24 hours of vote (don't hold through convergence period)

- ⏰ Accept that implied vol is LOW because market is RIGHT about high probability outcome

Risk level: EXTREME (can lose 100% of premium easily) | Skill level: Expert only

Probability of profit: ~30% (lower than implied 50% because fighting institutional vote approval)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Shareholder vote binary event in 21 days: January 6, 2026 vote creates MASSIVE uncertainty despite market complacency. While 85%+ institutional ownership suggests approval likely, even narrow passage (60-65% YES) could trigger renegotiation demands. Stock could gap 10-15% either direction based on vote margin and any surprise announcements.

-

⚖️ Delaware lawsuit adds unpredictable wild card: HoldCo Asset Management's legal challenge with court hearing January 2nd (4 days before vote) could drop last-minute bombshell revelations about deal process. Judge already ordered additional disclosures - suggests something wasn't transparent initially. Even if vote passes, legal challenges could delay closure or force Fifth Third to renegotiate terms.

-

💰 Stock trading 6% ABOVE merger value is unusual: Current price at $87.91 vs $82.88 merger consideration represents significant premium that typically compresses as deal closure approaches. This spread exists because either (1) market expects competing bid (unlikely), (2) Fifth Third will sweeten terms (possible), or (3) meaningful deal break probability (HoldCo's thesis). If none materialize, natural path is DOWN toward $82.88 regardless of vote outcome.

-

🏦 Regulatory approval NOT guaranteed despite vote passing: Requires approvals from OCC, Federal Reserve Board, and Texas Department of Banking. Combined entity creates 9th largest U.S. bank with #1 Michigan deposit share - potential antitrust concerns. Timeline of 60-90 days is optimistic; delays common. Any regulatory pushback extends uncertainty and compresses stock toward merger value.

-

💸 Fifth Third stock performance affects effective merger value: Exchange ratio of 1.8663 FITB shares means CMA value fluctuates with FITB stock price. Current $82.88 valuation based on FITB's October 3rd price. If FITB drops 10% before closure, effective CMA value drops to ~$75. Regional bank sector weakness (CRE concerns, macro deterioration) would hit both stocks but hurt merger arbitrage.

-

🏗️ Integration execution risk with aggressive 35% cost cuts: Fifth Third targets 35% expense reduction from Comerica - extremely aggressive. Integration of $288B combined platform requires flawless execution. Customer attrition, technology issues, or cultural clashes could derail 9% EPS accretion and 22% IRR targets. Post-merger disappointments would hurt FITB stock and effective CMA value.

-

📉 Commercial real estate exposure across regional bank sector: CMA's commercial banking focus (85% of loans) creates CRE concentration risk. Small banks under $20B assets hold 56.1% of all U.S. commercial property loans. Q2 2025 saw $44M provision for credit losses vs $0 prior year and criticized loans at 5.4%. Broader CRE crisis would impact both standalone value AND merger completion likelihood.

-

🎯 Options market pricing extreme certainty - dangerous complacency: Implied volatility at 3.4% through January expiration is REMARKABLY low for stock facing binary merger vote. Gamma positioning overwhelmingly bullish (17:1 call/put ratio) shows consensus is "done deal approved." When everyone leans same direction, surprises hurt. The trader closing $5.7M in calls suggests smart money isn't as confident as implied vol indicates.

-

⏰ Q4 earnings late January could shift narrative: Final standalone results before merger closure. Q2 2025 showed deposit decline, increased provisions. Disappointing Q4 would validate HoldCo's argument that standalone value deteriorating and merger terms too low. Could trigger post-vote renegotiation demands even if initially approved.

-

💹 Fed rate policy uncertainty impacts bank valuations: While Fed cut 175 bps since September 2024, signaling only ONE more 25 bps cut in 2026 creates net interest margin compression risk. Inflation above 2% target from tariffs limits further cuts. Regional banks highly rate-sensitive - macro policy shift would impact both CMA standalone value AND FITB stock.

🎯 The Bottom Line

Real talk: Someone just walked away with $5.7 MILLION by closing deep ITM calls on Comerica 21 days before the most important shareholder vote in the company's history. This isn't a bearish bet on the Fifth Third merger - it's smart profit-taking by institutions who don't want to gamble their gains on a binary vote outcome.

What this trade tells us:

- 🎯 Sophisticated player captured big gains ($75 strike → $87.91 current price = $12.91 intrinsic value) and locked them in BEFORE vote

- 💰 They're walking away from potential $5+ upside (stock to $95 if competing bid) to AVOID -$12-15 downside risk if vote fails January 6th

- ⚖️ Timing (21 days pre-vote, 4 days after Delaware court hearing) shows concern about activist opposition derailing "sure thing"

- 📊 Despite 85%+ institutional ownership suggesting easy approval, smart money isn't taking chances

- ⏰ Options implied vol at rock-bottom 3.4% suggests market complacency - this trader disagrees

This is NOT a "sell everything" signal - it's a "take profits and reduce risk into uncertainty" signal.

If you own CMA shares:

- ✅ Consider trimming 30-50% at $87-88 levels to lock in 43% YTD gains

- 📊 If holding through vote, set MENTAL STOP at $82.50 (merger value zone) to protect remaining position

- ⏰ Don't get greedy - you've already captured most merger premium! Stock at $87.91 vs $82.88 merger value leaves limited upside

- 🎯 If vote passes, stock naturally drifts DOWN toward $82.88 as spread compresses through regulatory approval period

- 🛡️ If concerned about downside, consider buying protective puts at $85 or $82.50 strikes

If you're watching from sidelines:

- ⏰ January 2nd Delaware court hearing and January 6th shareholder vote are the moments of truth - DO NOT enter before these events!

- 🎯 Post-vote pullback to $82-84 merger value zone would be entry point to play spread compression (if vote passes with >70%)

- 📈 Better opportunity might be Fifth Third (FITB) shares AFTER merger closes - gets Comerica's Texas/California franchise at 35% expense discount

- ⚠️ If vote FAILS, wait for dust to settle toward $75-80 support before considering standalone CMA position

- 🚀 Current risk/reward UNFAVORABLE: upside capped by merger terms, downside open if deal breaks

If you're considering options:

- 🎯 Implied volatility at 3.4% is TOO LOW for binary vote event - BUT fighting consensus is dangerous

- ⏰ Options strategies should focus on POST-vote period, not pre-vote speculation

- 📊 Straddles/strangles only make sense if you believe vote outcome will SURPRISE (fail or dramatic competing bid)

- ⚠️ Call buying has limited upside (capped by merger value); put buying fights 85% institutional approval odds

- 🛡️ Best use of options: protective puts if holding large share position through vote

Mark your calendar - Key dates:

- 📅 December 19 (Thursday) - Weekly/Monthly/Triple Witch OPEX

- 📅 January 2, 2026 (Friday) - Delaware Court of Chancery hearing on HoldCo lawsuit (17 days!)

- 📅 January 6, 2026 (Tuesday) - Shareholder vote on Fifth Third merger (21 DAYS!)

- 📅 January 16, 2026 (Friday) - Monthly OPEX, expiration of this $5.7M closed call trade

- 📅 Late January 2026 - Q4 2025 earnings (final standalone results)

- 📅 Q1 2026 (Feb-Mar) - Regulatory approval process (OCC, Federal Reserve, Texas Banking)

- 📅 End of Q1 2026 (March 31) - Expected merger closure (earliest: February 2nd)

Final verdict: The Fifth Third merger will PROBABLY pass given overwhelming institutional support, but the current stock price at $87.91 offers poor risk/reward. You're paying 6% premium above $82.88 merger value for "certainty" that isn't truly certain. The $5.7M call closing trade shows sophisticated money agrees: gains already captured, remaining upside capped, downside tail risk not worth taking.

Be smart like this trader: take profits, reduce risk, wait for post-vote clarity. If you missed the 43% YTD rally, the next opportunity is AFTER the vote resolves uncertainty - either playing spread compression post-approval or buying the $75-80 dip post-failure. The time to speculate was November 25th at $72. At $88, it's time to be DEFENSIVE.

Protect your capital. Wait for better setups. The market will give you another chance. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Merger arbitrage carries significant risks including deal failure, regulatory denial, and market value deterioration. The Z-score of 0.44 indicates this is a typical trade size for CMA - it does not imply the trade will be profitable or that you should follow it. Shareholder votes create binary event risk with potential for 10-15% gaps either direction. The trader may have complex hedging strategies or portfolio needs not applicable to retail traders. Always do your own research and consider consulting a licensed financial advisor before trading.

About Comerica Incorporated: Comerica is a relationship-focused commercial bank with approximately $80 billion in assets, operating across Texas, California, and Michigan markets, with a market cap of $11.26 billion in the National Commercial Banks industry.