📡 CMCSA Massive $6.7M Long Call Bet - Cable Giant Gets Post-Spinoff Bull Vote! 🚀

📅 December 17, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just loaded up $6.7 MILLION in Comcast long calls expiring January 16th, 2026! First a $4.3M buy at 10:51am, then another $2.4M at 2:20pm - total 51,000 contracts at the $35 strike. With CMCSA trading at $30.34, this is a bold bet on a 15.4% rally in just 30 days, right after the January 2nd cable network spinoff completes. Translation: Smart money thinks the Versant separation is going to UNLOCK major value!

📊 Company Overview

Comcast Corporation (CMCSA) is a telecommunications and media powerhouse undergoing massive transformation:

- Market Cap: $108.3 Billion (one of the world's largest media companies)

- Industry: Cable & Pay Television Services

- Current Price: $30.34 (down from 52-week high of $40.20)

- Primary Business:

- Cable: TV, internet, and phone services to 65M U.S. homes/businesses (~29.4M broadband subs)

- NBCUniversal: NBC broadcast, Peacock streaming, Universal Studios, theme parks

- Sky: Major TV provider in UK and Italy

- Upcoming: Spinning off most cable networks into Versant Media Group (January 2, 2026)

💰 The Option Flow Breakdown

The Tape (December 17, 2025):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:51:34 | CMCSA | ASK | BUY | CALL $35 | 2027-01-15 | $4.3M | $35 | 20K | - | 20,000 | - | - | CMCSA270115C00035000 |

| 14:20:07 | CMCSA | ASK | BUY | CALL $35 | 2027-01-15 | $2.4M | $35 | 31K | - | 31,000 | - | - | CMCSA270115C00035000 |

🤓 What This Actually Means

This is pure bullish speculation on CMCSA's post-spinoff future! Here's what's happening:

- 💸 Total capital deployed: $6.7M across 51,000 contracts (two separate buys, same strike/expiration)

- 🎯 Target price: $35 represents 15.4% upside from current $30.34 price

- ⏰ Strategic timing: January 15, 2027 expiration gives 394 days - captures Versant spinoff completion, NBA deal launch, Epic Universe ramp

- 📊 Out-of-the-money bet: Needs $35+ by Jan 2027 to profit (currently $4.66 out of the money)

- 🏦 Conviction play: Coming back for MORE at 2:20pm (31K contracts) after initial 20K buy shows strong conviction

What's really happening here: This trader believes the January 2, 2026 Versant spinoff will be a MASSIVE catalyst that re-rates CMCSA higher. By spinning off declining cable networks (MSNBC, CNBC, USA), Comcast gets to focus on growth businesses: broadband, wireless (7.8M lines), Peacock streaming, theme parks, and the huge NBA deal starting 2025-26 season. The $35 strike aligns with analyst consensus price target of $37.79 - essentially betting CMCSA gets to "fair value" once the market recognizes the cleaner story.

Second tranche at 2:20pm (31K more contracts) suggests either: (1) Same trader adding to position, or (2) Separate institution following similar thesis. Either way, the conviction is clear - big money wants exposure to post-spinoff CMCSA.

Unusual Score: 🔥🔥 VERY HIGH - This represents massive accumulation in a single day at identical strikes. The Z-scores of 52.1 and 80.95 indicate this is EXTREMELY unusual activity - happening only a few times per year for CMCSA. Total volume of 51,000 contracts is 1.348x higher than typical activity, making this stand out significantly.

📈 Technical Setup / Chart Check-Up

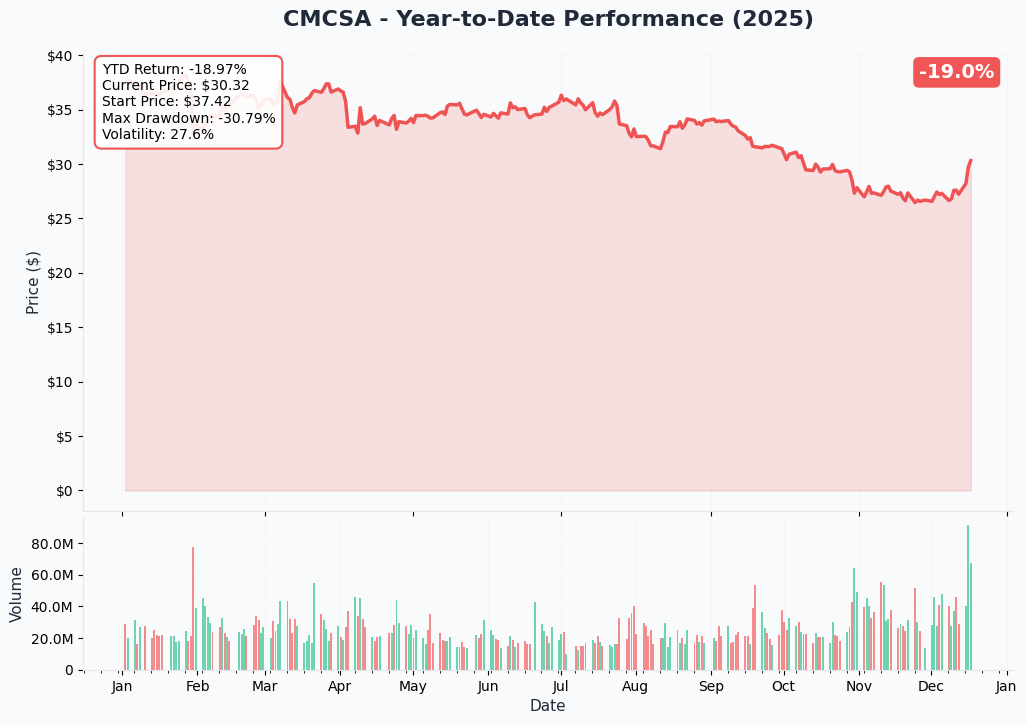

YTD Performance Chart

CMCSA has been PUNISHED in 2025 - currently trading at $30.34, the stock is down significantly from its 52-week high of $40.20 (a -24.5% decline). The chart tells a painful story of secular headwinds and transformation challenges.

Key observations:

- 📉 Brutal selloff: Down from $40+ in early 2025 to current $30 levels

- 🔴 52-week range: $25.75 - $40.20 (currently near the MIDDLE, not the bottom)

- 😰 Catalyst overhang: Market pricing in risk from broadband losses (411K in 2024) and cable network decline

- 📊 Spinoff discount: Typical pre-spinoff weakness as investors await clarity on structure

- 💔 Sentiment shift: From growth story to value/turnaround narrative

- ⚠️ Support test: Recent bounce from $27-28 levels suggests some institutional buying

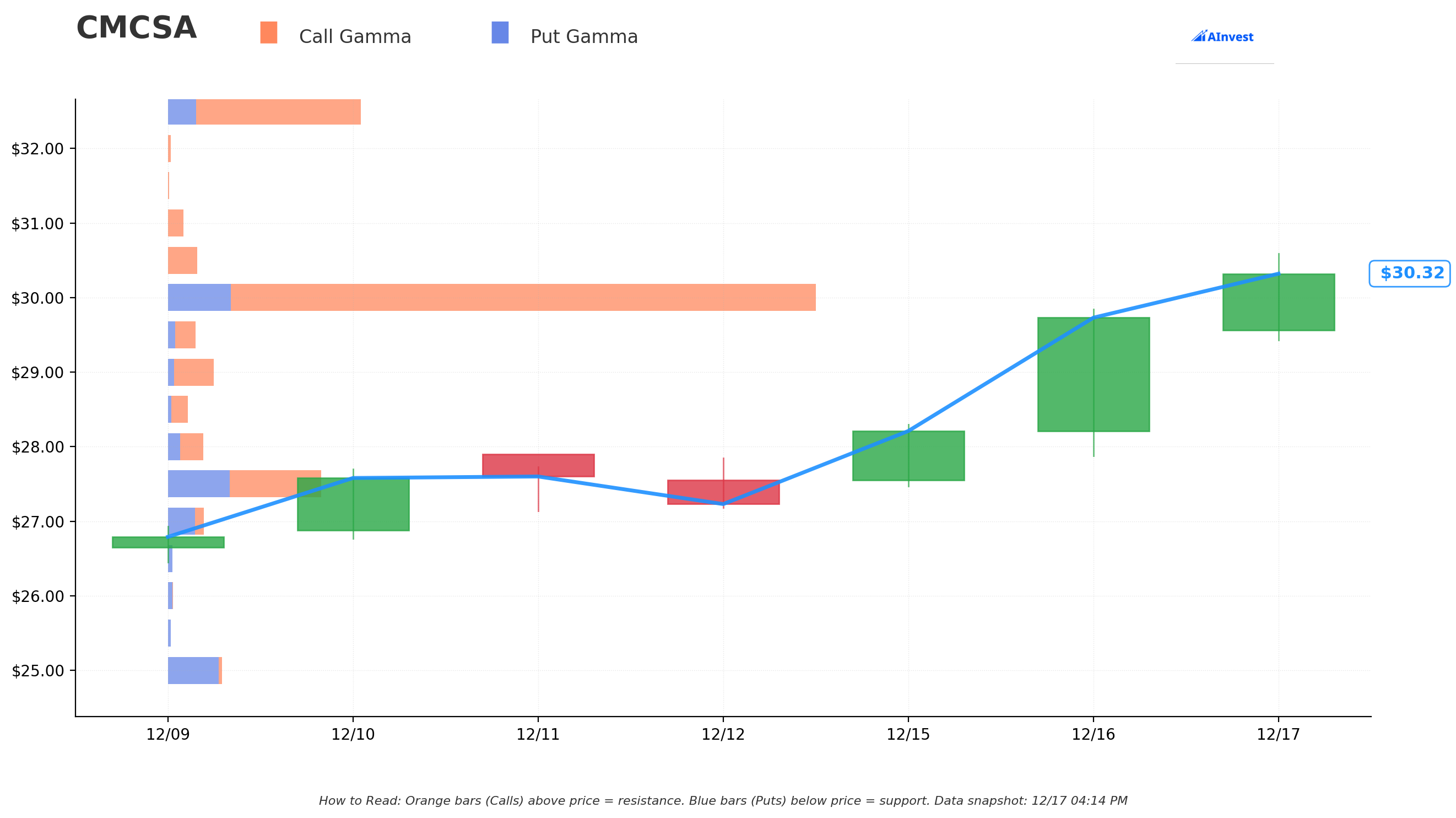

Gamma-Based Support & Resistance Analysis

Current Price: $30.34

The gamma exposure map reveals critical price magnets where options activity is concentrated:

🔵 Support Levels (Put Gamma Below Price):

- $30.00 - MASSIVE support with 83.5B total gamma exposure (STRONGEST LEVEL - the line in the sand!)

- $29.50 - Secondary support at 3.5B gamma (1.1% below current)

- $29.00 - Deeper floor at 5.2B gamma (4.4% below)

- $28.00 - Major structural support with 4.1B gamma (7.7% below)

- $27.50 - Critical zone at 19.0B gamma (9.4% below - recent test held here)

- $27.00 - Deep support at 4.5B gamma (11% below)

- $25.00 - Disaster floor at 6.8B gamma (17.6% below - 52-week low area)

🟠 Resistance Levels (Call Gamma Above Price):

- $30.50 - Immediate ceiling with 3.8B gamma (just 0.5% overhead - very close!)

- $32.50 - Major resistance zone with 24.7B gamma (HUGE WALL at 7.1% above current)

- $35.00 - Extended target at 18.1B gamma (15.4% rally needed - THIS IS THE CALL STRIKE!)

What this means for traders: CMCSA is trading RIGHT ON TOP of massive $30.00 support (83.5B gamma - by far the largest level). This creates a natural floor where market makers will aggressively defend. However, there's a MASSIVE resistance wall at $32.50 (24.7B gamma) that will require significant buying pressure to overcome.

Notice anything? The call buyer struck at $35.00 where there's 18.1B gamma and significant call open interest. This is a KEY psychological and technical level - breaking through $32.50 resistance would likely trigger momentum push toward $35. They're betting on a breakout scenario.

Net GEX Bias: Bullish (168.9B call gamma vs 42.5B put gamma = 126.4B net bullish) - Overall positioning strongly favors upside, suggesting market makers are positioned for higher prices.

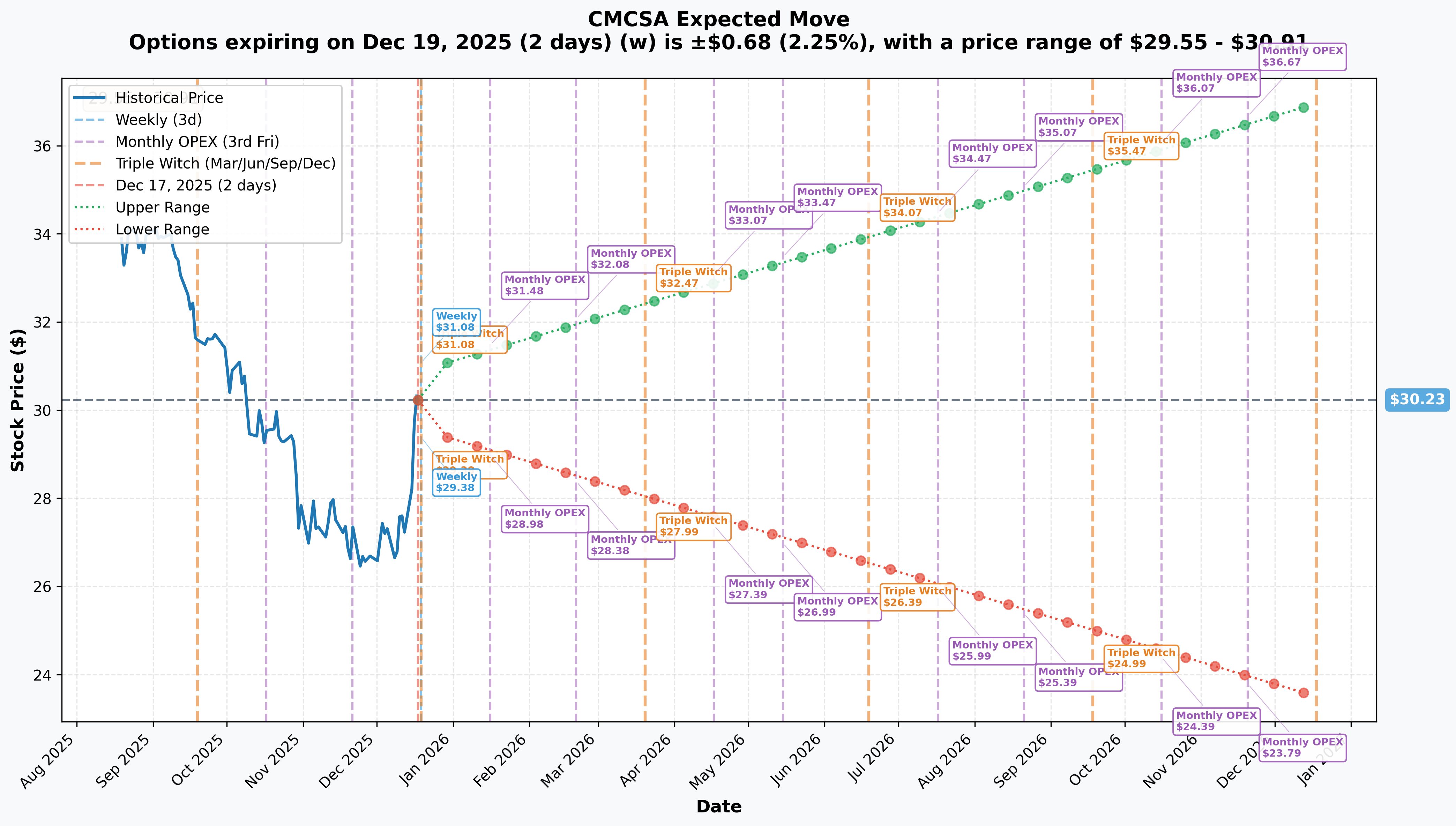

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly/Triple Witch (Dec 19 - 2 days): ±$0.68 (±2.25%) → Range: $29.55 - $30.91

- 📅 January OPEX (Jan 16 - 30 days): ±$1.25 (±4.14%) → Range: $28.98 - $31.48

- 📅 Yearly LEAPs (Dec 18, 2026 - 366 days): ±$6.74 (±22.28%) → Range: $23.49 - $36.97

Translation for regular folks: Options traders are pricing in a 2.25% move ($0.68) through this week's triple witch expiration on Friday. That's relatively calm for a media stock. Looking out to January (30 days), the market expects a 4.1% move - pretty subdued, suggesting expectations for range-bound trading through year-end and the Versant spinoff completion.

BUT - the yearly LEAP implied move is HUGE at 22.3% ($6.74), with an upper range of $36.97. This aligns PERFECTLY with the call buyer's $35 target! The market is saying: "We don't expect much volatility near-term, but over the next 12 months, this stock could be ANYWHERE from $23 to $37."

Key insight: Low near-term implied volatility (2-4%) combined with high long-term volatility (22%) creates an attractive setup for long-dated call buyers. You're not paying up for short-term event risk, but getting exposure to the bigger structural story (spinoff execution, NBA deal, wireless growth).

🎪 Catalysts

🔥 Upcoming Catalysts (Next 6 Months) - THESE COULD MOVE THE STOCK!

Versant Media Group Spinoff Completion - January 2, 2026 (16 DAYS!) 🎬

The BIGGEST catalyst is just weeks away! Comcast's Board approved the separation in December 2025, with completion set for January 2, 2026:

- 📊 Record Date: December 16, 2025 (ALREADY HAPPENED - you had to own CMCSA yesterday to get Versant shares)

- 💰 Distribution: 1 Versant share for every 25 CMCSA shares held

- 🆓 Tax-free spin to existing shareholders

- 📺 What's being spun off: USA Network, CNBC, MSNBC, Oxygen, E!, SYFY, Golf Channel, Fandango, Rotten Tomatoes

- 🎯 What stays with CMCSA: NBC broadcast, NBC News/Sports, Peacock, Bravo, theme parks, broadband/wireless

- 💵 Versant 2025 revenue guidance: $6.61B (-6% decline), but with $2.15B EBITDA and $1.37B free cash flow

- 📈 Valuation: Versant estimated at ~$10B (6-7x EV/EBITDA, 10%+ FCF yield)

Why this matters for the call trade: This is THE catalyst that could unlock 15-20% upside. Currently, CMCSA trades at a "sum-of-parts discount" because investors lump together growing businesses (broadband, wireless, streaming, parks) with declining cable networks. Post-spinoff, CMCSA becomes a PURE PLAY on:

- 💻 Connectivity (29.4M broadband subs, 7.8M wireless lines)

- 🎬 Entertainment (Peacock with NBA coming, theme parks with Epic Universe, Universal Studios)

- 📈 High-margin businesses (wireless approaching $10B at 57% margins)

The $35 strike call buyer is betting that once Wall Street can model CMCSA WITHOUT the cable network drag, the multiple expands from current depressed levels toward fair value. Analyst consensus of $37.79 supports this thesis.

Historical precedent: Successful spinoffs often result in BOTH companies outperforming - parent gets cleaner story, spinco gets focused management. Fox/News Corp, Time Warner/Time Inc, Viacom/CBS separations all saw initial pops.

NBA Media Rights Deal - Starts 2025-26 Season (6 MONTHS!) 🏀

In July 2024, Comcast/NBCUniversal secured an 11-year NBA media rights deal worth approximately $2.5 billion per year as part of a combined $77 billion deal. Coverage begins 2025-26 season (October 2026):

- 📺 Coverage: 100 NBA games annually across NBC and Peacock

- 🏆 Playoffs: 28 first/second-round games, one Conference Finals series in 6 of 11 years

- ⭐ All-Star Weekend: NBC becomes home of NBA All-Star events

- 🎯 Strategic significance: NBA returns to NBC after 22-year absence - nostalgia factor HUGE

- 📈 Peacock boost: Expected to be "launch pad" for subscriber growth from current 36M

- 💰 Revenue impact: Advertising + subscription revenue could add $3-4B annually

Why this matters: Peacock lost $1.58B in 2024 despite 36M subscribers. The path to profitability REQUIRES a killer content exclusive that drives subscriptions. NBA is that catalyst - proven to drive streaming adoption (see ESPN+, League Pass success). If Peacock adds 10-15M subs over 2-3 years from NBA (very achievable), losses flip to profits by 2027-28, dramatically improving CMCSA's earnings profile.

The call buyer's January 2027 expiration captures the FULL FIRST SEASON of NBA coverage - by expiration, Wall Street will have concrete data on subscriber growth, advertising rates, and profitability trajectory.

Epic Universe Theme Park Ramp - Opened May 22, 2025 (ALREADY OPEN!) 🎢

Epic Universe opened in May 2025 - Comcast's largest single investment in theme parks (~$7B estimated):

- 🎪 Size: 750-acre development, first new Orlando theme park in 25 years

- 💪 Early performance (Q2 2025): Theme parks revenue jumped to $2.349B (+18.7% YoY) in Q2 2025

- 📊 Technology: Billed as "most technologically-advanced theme park ever"

- 🎯 Market impact: Challenges Disney's Orlando dominance with cutting-edge attractions

- 💰 Revenue potential: Parks generated $8.6B revenue in 2024 - Epic Universe could add $1-2B annually at maturity

Why this matters: Theme parks represent ~20% of revenue but 44% of adjusted EBITDA - incredibly high-margin business. Epic Universe is ALREADY driving results (Q2 +18.7% growth), but the ramp continues through 2026-2027 as word-of-mouth builds and new attractions open. By January 2027 call expiration, Epic Universe will be hitting its stride with full-year comparable data showing the massive revenue/profit contribution.

This is a physical, tangible growth driver that's NOT dependent on fickle consumer streaming adoption - families will keep visiting theme parks in any macro environment.

Xfinity Mobile Wireless Growth - 2026 Target 🚀

Wireless is Comcast's fastest-growing segment:

- 📱 Current scale: 7.8 million wireless lines (ended 2024)

- 📈 Growth: +1.2 million net adds in 2024 (+18.2% YoY)

- 💡 Penetration: Only 12% of broadband customer base - HUGE upside runway

- 💰 Economics: Capital-light MVNO model (uses Verizon network + Xfinity WiFi)

- 🎯 Management priority: "We will lean into wireless more than ever before" - Mike Cavanagh, President

- 📊 TAM: Wireless market is 2.5x size of broadband market

Why this matters: If CMCSA reaches 20% wireless penetration of broadband base by 2026-27 (very achievable given current growth trajectory), that's 13M total wireless lines - nearly DOUBLING the business. At $30-40/month ARPU, that's $5-6B in annual wireless revenue at high margins. This growth offsets broadband subscriber losses (411K lost in 2024) and provides a compelling "new growth vector" narrative for Wall Street.

By January 2027, wireless could be approaching 10M lines with clear path to enterprise scale - a massive rerating catalyst.

Q1 2025 Earnings - Expected Late April 2026 📊

Comcast reports Q1 results typically late April. For context, Q4 2024 results (reported Jan 30, 2025) were strong:

- ✅ Q4 Revenue: $31.92B, beating forecast by 2% (+2% YoY)

- ✅ EPS: $0.96, beating consensus by 11.6%

- ✅ Full-year 2024: Record revenue of $124B, adjusted EBITDA of $38B, FCF $12.5B

- ⚠️ Video subs: Lost 311K in Q4 (improved from -389K year ago)

- ⚠️ Broadband: Lost 139K in Q4 (worse than expected -100K)

- ✅ Wireless: Reached 7.8M lines (+1.2M net adds for year)

What to watch in Q1 2025 (April 2026 report):

- 🎯 Broadband losses stabilizing? (Target: Better than Q4's -139K)

- 📈 Wireless growth continuing? (Target: +300K+ net adds)

- 🎬 Peacock subscribers + NBA anticipation building? (Target: 38-40M)

- 🎢 Epic Universe contribution showing in margins? (Target: Parks revenue +15%+)

- 💰 Post-spinoff guidance and strategic priorities clear?

📊 Past Catalysts (Already Happened) - Context for the Story

Q4 2024 Earnings Results - January 30, 2025

Strong quarter with record annual revenue of $124B - validated operational excellence even as stock declined due to structural concerns.

Cable Network Spinoff Announcement - November 20, 2024

Transformational strategic move to separate declining cable networks into Versant, allowing NBCUniversal to focus on higher-growth opportunities. Market initially uncertain on structure, but now clarity emerging as January 2 completion approaches.

Peacock Streaming Performance - 2024

- Subscribers: 36 million (flat Q3 to Q4 2024 after Olympics boost)

- Revenue: $4.9B for full-year 2024 (+46% from 2023)

- Loss: $1.58B for year (narrowing but still unprofitable)

- NBA deal announcement provides clear path to profitability by 2027-28

Broadband Subscriber Challenges - "Cord Cutting 2.0"

Full-year 2024: Lost 411,000 total internet customers due to fixed wireless competition (T-Mobile, Verizon 5G home internet) and Starlink satellite. This is the PRIMARY bear case against CMCSA - the core broadband business is declining.

Analyst Activity - Mixed Views

Recent price target changes show divergent views:

- ✅ December 12, 2024: Seaport Global raised target to $46 (bullish on spinoff)

- ⚠️ Others: Oppenheimer downgraded to Perform, Citi lowered to $35, JPMorgan to $33

- 📊 Consensus: 23 analysts average "Buy" rating with $37.79 target (+24.5% upside)

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timeline through January 2027 expiration:

📈 Bull Case (30% probability)

Target: $35-40 (Call Strike to Upper Implied Range)

How we get there:

- 🎯 Versant spinoff executes perfectly - Both CMCSA and Versant trade UP 10-15% post-separation as sum-of-parts discount closes

- 🏀 NBA deal drives Peacock surge - Subscriber count jumps from 36M to 45-50M through 2026 on NBA hype and strong content

- 📱 Wireless keeps crushing - Reaches 9-10M lines by end 2026 (20%+ penetration of broadband base)

- 🎢 Epic Universe becomes cash machine - Parks segment shows +20%+ revenue growth with expanding margins

- 💰 Broadband losses stabilize - Q1-Q2 2026 show better-than-expected net losses improving to -50-75K per quarter

- 📊 Peacock profitability path clear - Management guides to breakeven by Q4 2026, profits starting 2027

- 🇨🇳 No new regulatory/export issues - Clean execution environment

- 📈 Break through $32.50 gamma resistance triggers technical buying to $35, then momentum to $37-40

Key metrics needed:

- Wireless net adds >1.5M for 2026

- Peacock sub growth >5M net adds in 2026

- Parks EBITDA margins expanding 200-300 bps

- FCF staying strong at $12-13B despite investments

Probability assessment: 30% because it requires MULTIPLE things going right simultaneously. The setup is there (spinoff, NBA, Epic, wireless), but execution is hard. Getting to $35 by Jan 2027 is achievable; beyond that requires perfect storm.

🎯 Base Case (50% probability)

Target: $28-34 Range (Choppy Consolidation Around Current)

Most likely scenario:

- ✅ Versant spinoff completes smoothly but no major re-rating - market waits to see sustained performance

- 📺 NBA deal anticipation builds but subscriber impact won't show until Fall 2026 - too early to call

- 📉 Broadband keeps bleeding but not accelerating - losses of 300-400K for 2026, in-line with 2024

- 📱 Wireless growth solid but not spectacular - adds 1.0-1.2M lines (similar to 2024)

- 🎢 Epic Universe performing well but already priced in after Q2 2025 results showed strong start

- 💔 Peacock still losing money through most of 2026 - profitability delayed to 2027-28

- ⚖️ Macro uncertainty keeps valuation multiple compressed despite improving story

- 🔄 Trading between $28-34 gamma support/resistance as market digests transformation

- 💤 Volatility remains low - stock just grinds sideways for 6-9 months

What happens to the calls:

- Stock at $32-33 by Jan 2027: Calls expire worthless or minimal value (bought at ~$0.13, expire $0-1)

- Need $35.13 just to breakeven on the trade

- Theta decay erodes value steadily if stock stays range-bound

- This is a LOSS scenario for the call buyer unless stock makes a late push

Why 50% probability: CMCSA has A LOT going on, but market sentiment remains skeptical after years of cord-cutting narrative. The positive catalysts are real but will take TIME to show in numbers. Most institutions will "wait and see" rather than aggressively buy at current levels. Stock needs to PROVE the turnaround story before multiple expansion happens.

📉 Bear Case (20% probability)

Target: $24-28 (Test 52-Week Lows)

What could go wrong:

- 😰 Broadband losses ACCELERATE - Q1-Q2 2026 show -200K+ per quarter as 5G fixed wireless gains traction

- 🚨 Versant spinoff disappoints - Both stocks decline 5-10% post-separation as investors realize limited upside in either

- 📉 Wireless growth stalls - Competition from carriers intensifies, CMCSA adds only 500-700K in 2026

- 💸 Peacock losses WIDEN - NBA rights costs hit before revenue benefits, losses expand to $2B+ in 2026

- 🎢 Epic Universe demand softens - Macro recession hits consumer discretionary spending, park visits decline

- 🇨🇳 Regulatory issues - FCC data caps investigation leads to restrictions on pricing power

- 📊 Macro recession - Advertising market collapses, dragging NBCUniversal revenue down 15-20%

- 💰 Dividend cut speculation - FCF pressures force dividend reduction, killing income investor appeal

- 🔨 Break below $30.00 gamma floor triggers cascade to $27.50, then $25 (52-week lows)

Critical support levels to watch:

- 🛡️ $30.00: MASSIVE 83.5B gamma support - if this breaks, lookout below

- 🛡️ $27.50: Secondary floor at 19.0B gamma - tested in 2024, held

- 🛡️ $25.00: Disaster scenario at 52-week lows (6.8B gamma)

Probability assessment: Only 20% because it requires multiple negative catalysts AND ignores that CMCSA is generating $12.5B annual FCF, has fortress balance sheet, and is executing on strategic transformation. The bear case exists (broadband secular decline is real), but the company has enough growth vectors to offset. Still, if macro turns or execution stumbles, downside exists.

Call P&L in Bear Case:

- Stock at $28 on Jan 2027: Calls expire worthless, loss = -$0.13/share × 51,000 = -$663K (100% loss of premium)

- Stock at $25 on Jan 2027: Same result - calls worthless below $35 strike

💡 Trading Ideas

🛡️ Conservative: Wait for Post-Spinoff Clarity

Play: Stay on sidelines until January 2nd spinoff completes and dust settles (1-2 weeks after)

Why this works:

- ⏰ Spinoff in 16 days creates binary event risk - stock could gap 5-10% either direction

- 📊 Tax-loss selling pressure into year-end - wait until January for fresh capital to flow in

- 🎯 Better visibility post-separation - Will know exact Versant valuation, CMCSA standalone guidance, strategic priorities

- 💸 Avoid "spin arbitrage" games - Hedge funds often create weird price action around record dates and distribution dates

- 📈 Entry clarity - If stock trades down to $28-29 post-spin, that's excellent risk/reward. If it rips to $33-34, can reassess

- 🤔 Smart money bought calls, not stock - They structured for leverage/time, not immediate conviction

Action plan:

- 👀 Watch January 2nd separation closely - See how both CMCSA and Versant trade in first week

- 🎯 Target entry $27-29 if weakness post-spin (that's 10% off current price with massive $27.50 gamma support)

- ✅ Need to see: Wireless net adds continuing, broadband losses not accelerating, Peacock sub growth ahead of NBA

- 📊 Monitor analyst updates post-spinoff - Wall Street will refresh models with new sum-of-parts valuations

- ⏰ Re-evaluate in Q1 2026 after dust settles and strategic vision is clear

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 5-10% spinoff volatility. Get better entry if market doesn't immediately re-rate the stock. Maintain optionality to deploy capital at better levels.

⚖️ Balanced: Slow Accumulation of Stock + Short Puts

Play: Buy small CMCSA stock position here, sell cash-secured puts at support to accumulate more

Structure:

- 💰 Buy 100-300 shares at current $30-31 levels (starter position)

- 📉 Sell $28 puts or Sell $27.50 puts (February or March expiration)

- 💵 Collect premium while waiting for lower entry on additional shares

Why this works:

- 📊 Valuation is reasonable - Trading at 13-15x forward earnings with 3.3% dividend yield

- 🎯 Strong $27.50-30.00 gamma support provides downside cushion (19.0B + 83.5B gamma)

- 💰 Generate income while waiting - short puts collect premium, funded by dividends on stock position

- ⏰ Time horizon advantage - You're not gambling on near-term spinoff pop; building position for 2026-27 catalysts

- 🤝 Combine income + capital appreciation - Dividends ($1.24/year = 3.3% yield) + potential upside to $35-37

- 🛡️ Defined entry points - If puts get assigned, you buy at $27.50-28 (better than current $30)

Estimated P&L:

- 💰 Stock dividends: $1.24/share annually (paid quarterly)

- 💵 Put premium: $0.50-1.00 per put (depends on strike/expiration) - annualized 15-20% return on cash securing puts

- 📈 Upside: If stock reaches $35 by Jan 2027, gain $4-5/share (13-17% capital appreciation) + dividends

- 📉 Downside: If stock drops to $27, lose $3-4/share but cushioned by dividends + put premiums collected

Position sizing:

- Allocate 3-5% of portfolio to CMCSA stock

- Set aside another 3-5% cash to secure short puts

Risk level: Moderate (stock can still decline) | Skill level: Intermediate

Expected outcome: Build CMCSA position over 3-6 months at average cost $28-30. By mid-2026, have meaningful position to benefit from NBA launch, wireless growth, and improved sentiment. Income generation (3.3% dividend + put premiums) provides 5-6% annual yield while waiting for catalysts.

🚀 Aggressive: Copy the Call Trade (ADVANCED ONLY!)

Play: Buy out-of-the-money calls betting on post-spinoff re-rating (SAME thesis as $6.7M trade)

Structure: Buy $35 calls expiring June 2026 or later (NOT January 2027 like the big trade - too expensive, too much time decay)

Why this could work:

- 🎯 Following smart money - Institutions deployed $6.7M with this exact thesis

- 📊 Asymmetric payoff - Calls cost $0.50-1.00 but worth $5-8 if stock hits $40-43 (5-10x return)

- 🚀 Multiple catalysts in 6-month window: Versant spin, Q1 earnings, NBA hype building, wireless hitting 8.5-9M lines

- 💰 Defined risk - Can only lose premium paid (unlike shorting or margin)

- ⚡ Gamma exposure at $35 means if stock breaks $33-34, could accelerate quickly to $35-36

- 📈 Analyst target of $37.79 validates thesis - you're betting on "fair value" realization

Why this could blow up (SERIOUS RISKS):

- 💸 Out-of-the-money = HIGH probability of worthless expiration - Stock needs to gain 15%+ in 6 months

- ⏰ Time decay kills - Theta burns value every day; if stock stays at $30-32, you lose 100%

- 😱 Stock could easily stay range-bound - Base case (50% probability) is $28-34, which means ZERO value at $35 strike

- 📊 Volatility already pricing transformation - IV not cheap; you're paying for the story

- 🎢 Spinoff could be "sell the news" - Market may already be pricing in best-case scenario

- ⚠️ Broadband losses could accelerate - One bad quarter of -200K+ subs and stock drops to $26-27

Estimated P&L:

- 💰 Cost: ~$0.75-1.25 per contract (June 2026 expiration) = $75-125 per contract

- 📈 Profit scenario: Stock at $38-40 by June 2026 = calls worth $3-5 = 200-400% gain

- 🚀 Home run: Stock at $42-45 by June 2026 = calls worth $7-10 = 600-900% gain

- 📉 Loss scenario: Stock below $35 at expiration = lose 50-100% of premium

- 💀 Total loss: Stock at $30-33 = calls expire worthless = -100% loss

Breakeven point:

- 📈 Need stock at ~$36.00-36.50 by June 2026 just to breakeven after premium paid

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand this is PURE SPECULATION with high probability of total loss

- ✅ Can afford to lose 100% of premium (very real possibility!)

- ✅ Have experience trading options and understand time decay/implied volatility

- ✅ Accept that even if thesis is RIGHT, timing might be wrong (stock hits $37 in August, not June)

- ✅ Plan to take profits at 100-200% gains rather than holding for expiration

- ⏰ Are willing to roll forward to later expirations if thesis intact but timing off

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~25-30% (need 15%+ move in 6 months on stock that's rangebound for 9 months)

Position sizing: Risk NO MORE than 1-2% of portfolio on this speculative trade. This is a "lottery ticket" not a core position.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Versant spinoff execution in 16 days: January 2, 2026 separation creates MASSIVE uncertainty. Structural separation involves IT systems, shared services, content agreements - any hiccups could tank both stocks. Versant guidance shows 6% revenue decline in 2025, 3-7% decline in 2026 - if deterioration accelerates faster, drags down CMCSA sentiment. Risk that market doesn't immediately re-rate CMCSA - could take 2-3 quarters to prove cleaner story.

-

📉 Broadband secular decline accelerating: Lost 411,000 internet customers in 2024 due to 5G fixed wireless (T-Mobile, Verizon, AT&T) and Starlink competition. This is the CORE cash flow engine - 29.4M broadband subs drive majority of revenue/profit. If losses accelerate to 500K-600K in 2025-26, thesis breaks. Wireless growth (1.2M adds) only partially offsets broadband losses. ARPU growth of 3.6% helps but may not sustain if competition intensifies. Risk of "death spiral" - lose subs → raise prices → lose more subs.

-

💸 Peacock profitability path uncertain: Despite narrowing losses, Peacock still lost $1.58B in 2024 with subscriber growth stalled at 36M (flat Q3-Q4). The $2.5B annual NBA rights deal starting 2025-26 adds MASSIVE costs before generating revenue benefits. Competition from Netflix (~260M subs), Disney+ (~150M), Max (~100M) intensifying. Risk: NBA deal fails to drive expected subscriber growth (target 10-15M net adds), deepening losses through 2026-27. Profitability delayed to 2028-29, forcing management to reconsider streaming strategy or cut costs aggressively.

-

🇨🇳 Regulatory scrutiny intensifying: FCC launched inquiry into broadband data caps in October 2024 - Comcast charges $25-30 monthly to remove caps (significant revenue source). Risk of regulatory action limiting pricing power. Net neutrality uncertainty continues after court rulings. DEI policies investigation by FCC adds political/regulatory risk. Could face additional fines or operational restrictions.

-

📊 Valuation still not "cheap" despite decline: Trading at 13-15x forward earnings after 24% decline from highs. This is FAIR value, not deep value. Stock needs to GROW to justify current multiple. If broadband losses continue and Peacock doesn't reach profitability, earnings decline and multiple contracts - double whammy sends stock to $24-26. Limited margin of safety at current $30 price.

-

🎰 Wireless competition from carriers: Comcast operates as MVNO on Verizon network - lacks network ownership, vulnerable to Verizon raising wholesale rates. Direct competition from T-Mobile, Verizon, AT&T with bundled home internet + mobile offerings. Penetration still only 12% of broadband base after years of effort - suggests difficulty converting customers. If growth slows to <1M net adds in 2026, narrative breaks.

-

💰 Epic Universe success dependent on consumer spending: $7B investment in theme park requires sustained consumer discretionary spending. If recession hits in 2026, theme park visits decline sharply (highly cyclical business). Q2 2025 showed strong start (+18.7% revenue growth), but that's honeymoon period. By 2026-27, need to prove sustained attendance and spending. Disney's scale advantages (larger IP portfolio, global footprint, $32B+ parks revenue vs $8.6B) remain significant.

-

🚨 M&A distraction risk: Persistent rumors of Comcast-Charter merger face significant regulatory hurdles. Any blocked merger attempt costly and distracting. Alternative scenario: Charter pursued by T-Mobile could leave Comcast at competitive disadvantage. Activist investor speculation (December 16 volume spike) adds uncertainty - activists could push for aggressive actions that backfire.

-

🎢 Macro recession could crush multiple fronts: At current valuation, CMCSA vulnerable to economic downturn hitting: (1) Advertising revenue at NBCUniversal, (2) Theme park attendance, (3) Broadband/wireless upgrades delayed, (4) Peacock subscription cancellations. No recession protection at current multiple.

-

📉 Sky Europe losing money: Sky Group reported £224M operating loss in 2024, doubled from £111M in 2023. Traditional satellite TV subscriber erosion offsetting Sky Glass smart TV growth. Recent sale of Sky Deutschland to RTL Group suggests Comcast rethinking international strategy. Could face more writedowns or forced asset sales.

🎯 The Bottom Line

Real talk: Someone just put $6.7 MILLION to work betting on Comcast's transformation story - and did it TWICE in one day (10:51am and 2:20pm)! This isn't a hedge, this is pure bullish conviction on the post-spinoff future.

What this trade tells us:

- 🎯 Smart money believes January 2 Versant spinoff will unlock 15-20% upside as sum-of-parts discount closes

- 📅 They structured for January 2027 expiration (394 days) to capture FULL transformation cycle: Versant separation, Q1-Q4 2026 earnings, NBA season launch, Epic Universe ramp, wireless hitting 9-10M lines

- 💰 $35 strike target aligns EXACTLY with Wall Street consensus $37.79 - betting on re-rating to "fair value"

- 📊 Coming back for MORE at 2:20pm shows conviction didn't waiver - either same buyer doubling down or separate fund with identical thesis

- 🎰 This is SPECULATION, not hedging - $6.7M bet that CMCSA becomes growth story once cable network drag removed

This is NOT a "buy everything now" signal - it's a "transformation thesis has legs" signal.

If you own CMCSA:

- ✅ HOLD through spinoff - Don't sell before January 2 or you forfeit Versant shares (already past record date if you owned Dec 16)

- 📊 Watch January 2-10 for post-spin trading - Both CMCSA and Versant should trade independently by Jan 5-10

- 🎯 If CMCSA gaps DOWN to $28-29 post-spin, that's OPPORTUNITY to add (market confused, not rational)

- 🚀 If CMCSA gaps UP to $33-35, consider trimming 20-30% to lock in gains and reduce risk

- 💰 Collect $1.24/year dividend (3.3% yield) while waiting for catalysts - you're getting paid to be patient

- ⏰ Key checkpoints: Q1 2026 earnings (late April), NBA season launch (October 2026), wireless hitting 9M lines (Q4 2026)

If you're watching from sidelines:

- ⏰ DO NOT chase into spinoff - Wait 1-2 weeks after January 2 for dust to settle

- 🎯 Target entry $27-29 if post-spinoff weakness (that's 10-13% discount with strong gamma support)

- 📈 Looking for confirmation: Wireless net adds >300K per quarter, broadband losses stabilizing <100K per quarter, Peacock subs growing toward NBA launch

- 💡 Consider starter position at $30-31 if you believe in 12-24 month thesis - but size small (3-5% of portfolio max)

- 🚀 Longer-term (6-12 months), NBA partnership, Epic Universe maturation, and wireless scaling are legitimate catalysts for $35-38

- ⚠️ Current valuation requires EXECUTION - one stumble on broadband (losses accelerate) or Peacock (NBA flops) and it's back to $26-28

If you're bearish:

- 🎯 The bear case is legitimate - broadband secular decline is REAL and accelerating

- 📊 Wait for post-spinoff to short - Better risk/reward after event clarity

- 🛡️ Watch $30.00 support (83.5B gamma) - if this breaks, cascade to $27.50 likely

- ⚠️ Put spreads offer better risk/reward than naked shorts (defined risk, lower capital requirements)

- ⏰ Q1 2026 earnings (April) will be KEY test - need to see broadband losses improving or thesis breaks

Mark your calendar - Critical dates:

- 📅 December 19 (Friday) - Triple witch OPEX (2 days away!)

- 📅 January 2, 2026 (Thursday) - Versant spinoff completion (16 DAYS!)

- 📅 January 5-10 - First week of separate CMCSA/Versant trading

- 📅 Late April 2026 - Q1 2026 earnings report

- 📅 October 2026 - NBA season launch on NBC/Peacock

- 📅 January 15, 2027 - Expiration of this $6.7M call trade

Final verdict: Comcast's transformation story is REAL and CREDIBLE - Versant spinoff, NBA rights, Epic Universe, and wireless scaling provide multiple growth vectors to offset broadband decline. BUT execution is HARD and timeline is LONG (12-18 months for thesis to play out).

The $6.7M institutional call buy signals belief in the long-term story, but doesn't mean "buy today at any price."

Be patient. Wait for better entry points $27-30. The transformation will take time, but if executed well, $35-38 by 2027 is achievable. You don't need to be a hero - let the setup come to you. 💪

This is a marathon, not a sprint. Build positions slowly. Collect dividends. Let catalysts unfold.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual activity described reflects specific trades by institutional investors who may have complex portfolio needs, risk management strategies, or information not available to retail traders. The Z-scores and unusualness metrics measure statistical deviation from normal trading patterns - they do NOT imply the trades will be profitable or that you should follow them. Always do your own research, understand the risks, and consider consulting a licensed financial advisor before trading. Spinoff events create additional complexity and risk. Out-of-the-money call options have a high probability of expiring worthless.

About Comcast Corporation: Comcast operates through three main divisions - Cable (TV, internet, phone to 65M U.S. homes/businesses), NBCUniversal (NBC broadcast, Peacock streaming, Universal Studios, theme parks), and Sky (UK/Italy TV provider). The company is spinning off most cable networks into Versant Media Group on January 2, 2026 to focus on growth businesses. Market cap of $108.3 billion in the Cable & Pay Television Services industry.