🔥 CRWV Mega $83M Options Spread - Smart Money Hedging AI Cloud Giant! 🛡️

📅 December 8, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just deployed a MASSIVE $83 MILLION options spread on CoreWeave this morning at 10:55:52! This sophisticated institutional trade involves selling 25,000 deep-in-the-money $150 calls expiring January 2028 for $67M premium while simultaneously buying 10,000 $80 calls expiring March 2026 for $16M. With CRWV down -55% from peak at $84.99 after the brutal November "neocloud crash," smart money is restructuring positions around the stock's recovery trajectory. Translation: Big players are locking in gains on covered positions while maintaining upside exposure through mid-2026!

📊 Company Overview

CoreWeave (CRWV) is the AI infrastructure pure-play that went public in March 2025, specializing in GPU cloud services for AI model training and deployment:

- Market Cap: $44.0 Billion (valued at peak innovation potential)

- Industry: Services - Prepackaged Software / Cloud Infrastructure

- Current Price: $84.99 (down from $187 all-time high, up from $40 IPO price)

- Primary Business: AI hyperscaler operating 32 data centers with 250,000+ NVIDIA GPUs, providing specialized compute infrastructure for OpenAI ($22.4B contract), Meta ($14.2B contract), and other AI leaders

💰 The Option Flow Breakdown

The Tape (December 8, 2025 @ 10:55:52):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order_Type | Z_Score | Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2025-12-08 | 10:55:52 | CRWV | SELL | CALL $150 | 2028-01-21 | $150 | 25,000 | $67M | STO | 633.24 | EXTREMELY_UNUSUAL |

| 2025-12-08 | 10:55:52 | CRWV | BUY | CALL $80 | 2026-03-20 | $80 | 10,000 | $16M | BTO | 51.62 | EXTREMELY_UNUSUAL |

🤓 What This Actually Means

This is a sophisticated diagonal call spread - a complex institutional restructuring play! Here's the breakdown:

Leg 1 - The Cash Generator (SELL $150 calls):

- 💸 Premium collected: $67M ($2,680 per contract × 25,000 contracts)

- 🎯 Strike chosen: $150 represents 76% upside from current $84.99 - this is DEEP in-the-money

- ⏰ Time horizon: 3+ years to January 2028 expiration

- 📊 Covered position: Almost certainly covered calls on existing 2.5M share long position (25,000 × 100 = 2,500,000 shares worth ~$212M at current price)

- 🏦 Income strategy: Collecting massive premium while capping upside at $150 over the next 3 years

Leg 2 - The Upside Bet (BUY $80 calls):

- 💰 Premium paid: $16M ($1,600 per contract × 10,000 contracts)

- 🛡️ Protection strike: $80 provides 5.9% downside buffer below current price

- ⏰ Strategic timing: 15 months to March 2026 expiration - captures Q4 2025 earnings (Feb 18), full 2025 results, GB300 scaling, and federal market entry progress

- 📈 Breakeven logic: Stock only needs to stay above $80 for these to retain value; any move back to $100+ delivers solid profits

- 🎢 Participation: Maintains 40% of original position size exposure (10,000 vs 25,000) to potential 2026 recovery

The Net Effect - What's Really Happening: This trader is playing a MASTERFUL game of risk management. They likely accumulated a massive CRWV position during the IPO or early rally from $40 to $140+. Now, sitting on unrealized losses after the stock crashed from $187 to $85 (-55%), they're:

- Locking in $67M cash TODAY by selling covered calls at $150 (which caps their upside but generates immediate income)

- Reducing their long exposure by 60% (from 25,000 to effectively 10,000 call equivalents)

- Maintaining strategic upside through the $80 March 2026 calls that profit if stock recovers to $100-120 range

- Hedging against further downside below $80 while keeping skin in the game above that level

Net premium: $67M collected - $16M paid = $51M NET CREDIT (incredible cash generation!)

Think of it like this: They're selling their penthouse apartment at $150 (with a 3-year lease-back option), using $16M of the proceeds to buy a condo at $80, and pocketing $51M in cash. If CRWV recovers modestly to $100-120 by March 2026, the $80 calls print money. If it goes parabolic to $200+, they miss upside above $150 but still made $51M today plus stock gains from $85→$150 (+76%).

Unusual Score: 🔥 EXTREME (633.24 Z-score on the short call leg, 51.62 on the long call leg) - This is literally one of the largest CRWV trades ever recorded. The combined $83M notional value represents more capital than most hedge funds manage. This is happening maybe a few times per year across ALL stocks.

📈 Technical Setup / Chart Check-Up

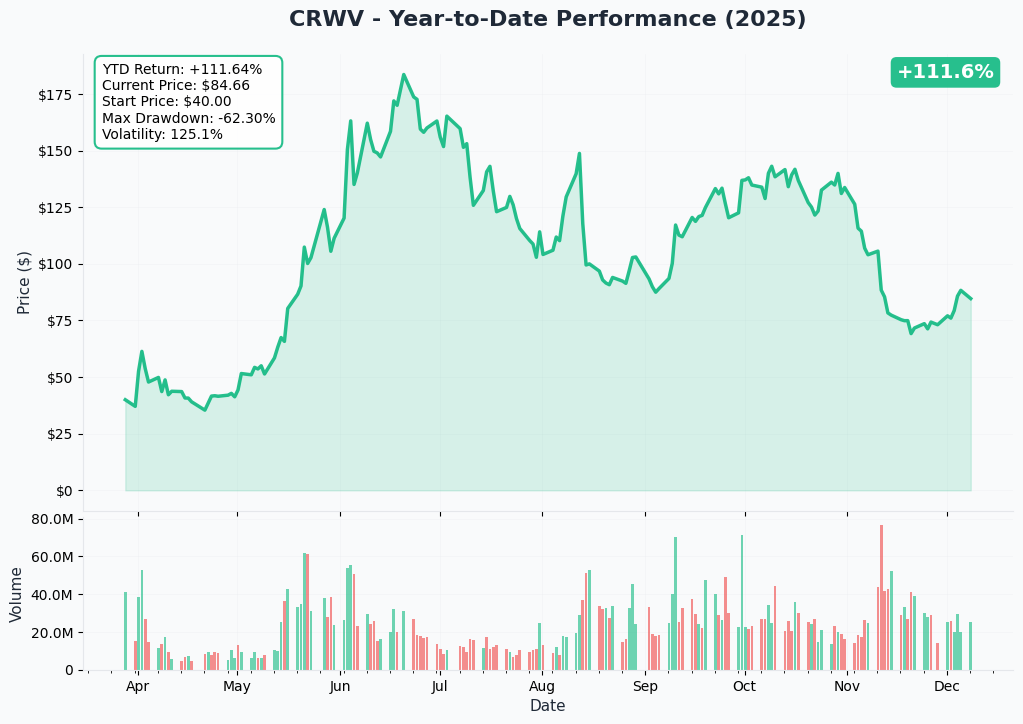

YTD Performance Chart

CRWV has been on an absolute ROLLERCOASTER - up +112% from $40 IPO price but down -55% from $187 peak. The chart tells a brutal boom-bust story in AI infrastructure:

Key observations:

- 🚀 IPO at $40 (March 28, 2025): Priced below expected $47-55 range but stock immediately found support

- 📈 Parabolic rally May-Sept: Surged 250% to $140 by June on AI infrastructure hype, hit $187 peak after OpenAI $22.4B deal announcement

- 💥 "Neocloud crash" November: Plummeted 45% in single month after Q3 earnings guidance cut due to data center construction delays

- 📊 Current consolidation: Trading $85-90 range, trying to establish base after brutal selloff

- ⚠️ High volatility environment: Stock moves 5-10% on no news regularly - not for the faint of heart

- 🎢 Finding support: $80 level has held on multiple tests - critical psychological and gamma support zone

The $150 strike where calls were sold represents the stock's previous peak area from late summer before the crash. The $80 strike where calls were bought sits right at the emerging support base.

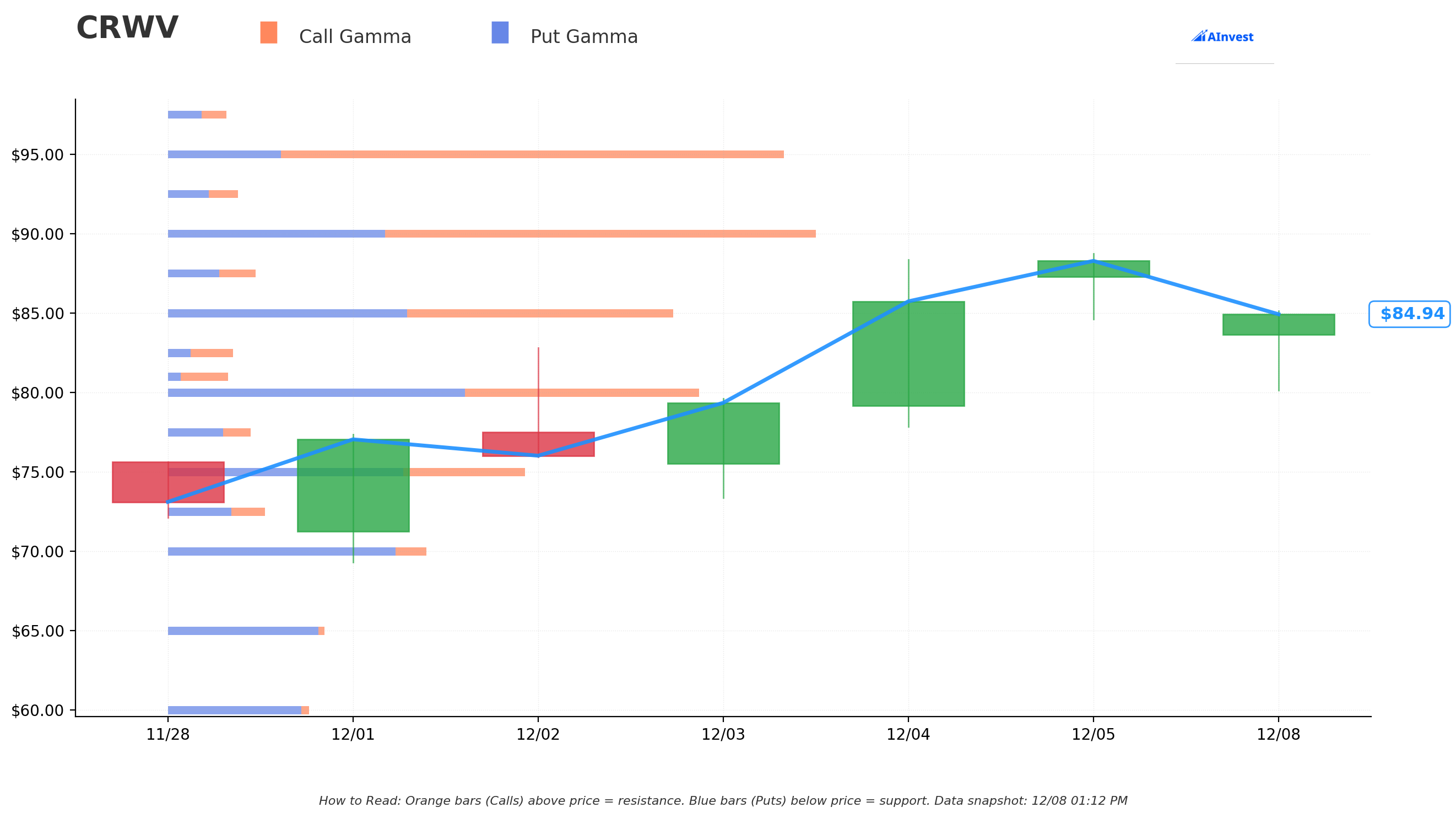

Gamma-Based Support & Resistance Analysis

Current Price: $84.99

The gamma exposure map reveals the battlefield where options dealers and institutions are positioning:

🔵 Support Levels (Put Gamma Below Price):

- $80 - STRONGEST SUPPORT with 7.8B total gamma exposure (this is THE LINE IN THE SAND - notice the call buyer struck here!)

- $77.50 - Secondary support at 1.2B gamma (minor buffer)

- $75 - Major structural floor with 5.2B gamma (deep safety net)

- $72.50 - Extended support at 1.4B gamma

- $70 - Disaster floor at 3.8B gamma (would represent 18% decline from current)

🟠 Resistance Levels (Call Gamma Above Price):

- $85 - Immediate ceiling with 7.4B gamma (stock fighting this level NOW - just 0.01% above current)

- $87.50 - Minor resistance at 1.3B gamma (short-term hurdle)

- $90 - Major resistance zone with 9.6B gamma (STRONGEST OVERHEAD BARRIER - 6% rally needed)

- $95 - Secondary ceiling at 9.1B gamma (psychological round number)

- $100 - Extended upside target at 12.4B gamma (critical recovery milestone - 18% rally)

What this means for traders: CRWV is sitting RIGHT ON TOP of the $85 resistance level (7.4B gamma) while also just above the massive $80 support (7.8B gamma). This creates a narrow 5.9% trading range where dealers have ENORMOUS positioning. The stock is essentially trapped between these two gamma walls.

Notice the strategic strikes:

- The $150 call seller is banking on stock NOT doubling from current levels over 3 years (ambitious but possible given debt concerns)

- The $80 call buyer positioned EXACTLY at the strongest support level - they're betting this floor HOLDS and stock recovers to $100+ by March 2026

Net GEX Bias: Bullish (71.0B call gamma vs 45.2B put gamma) - Despite the crash, overall positioning remains tilted toward recovery. Options market expects eventual bounce.

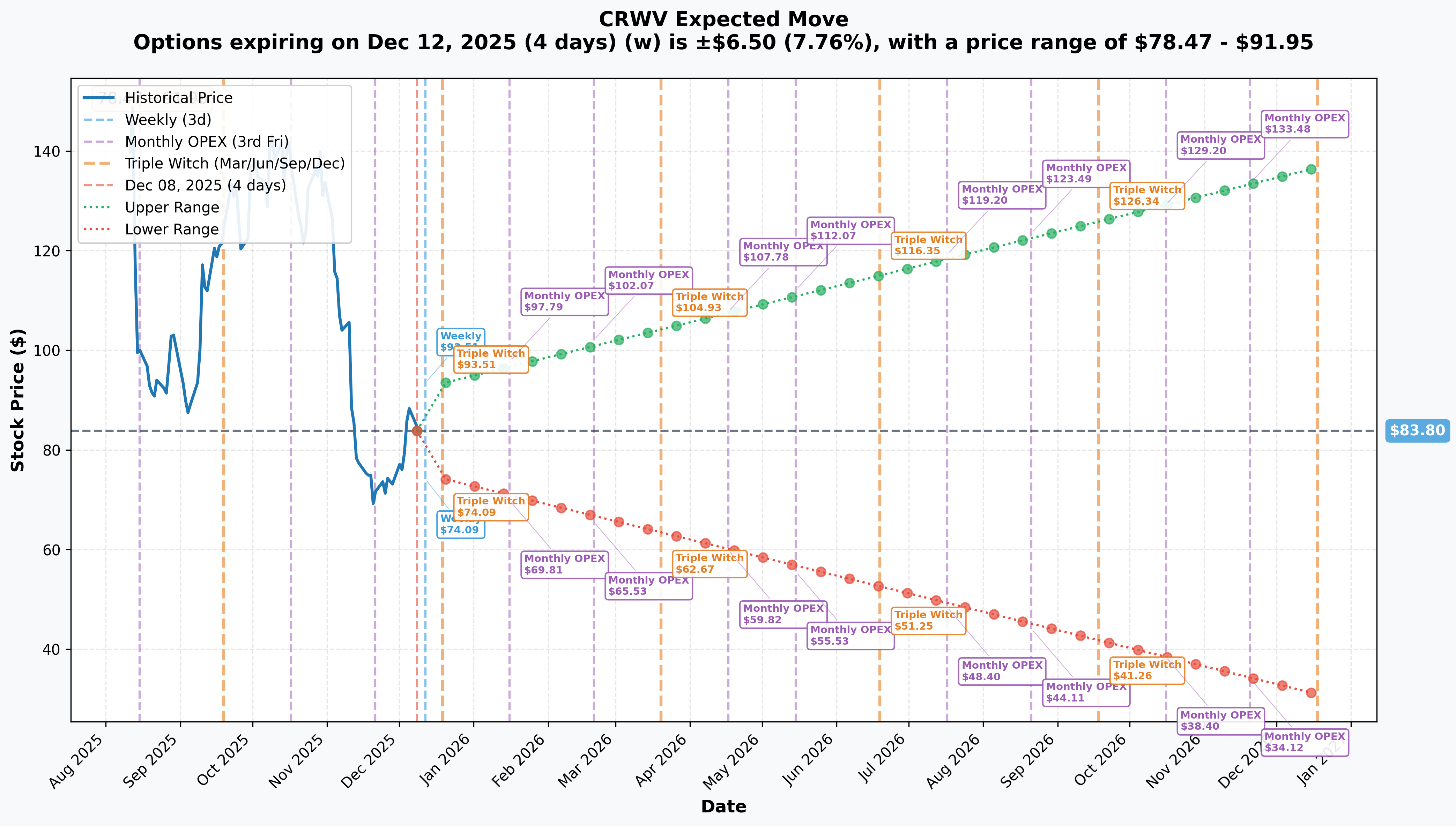

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 12 - 4 days): ±$6.50 (±7.76%) → Range: $78.47 - $91.95

- 📅 Monthly OPEX (Dec 19 - 11 days): ±$9.58 (±11.44%) → Range: $74.21 - $93.39

- 📅 Quarterly Triple Witch (Dec 19 - same): ±$9.58 (±11.44%) → Range: $74.21 - $93.39

- 📅 Yearly LEAPS (Dec 18, 2026 - 375 days): ±$49.96 (±59.62%) → Range: $30.91 - $136.69

Translation for regular folks: Options traders are pricing in a 7.8% move ($6.50) by this Friday for weekly expiration - that's MASSIVE for a 4-day window! The market expects continued VOLATILITY with potential for wild swings.

The December 19th monthly OPEX has an 11.4% implied move - the market is pricing real possibility of CRWV trading anywhere from $74 to $93 over the next 11 days. This reflects:

- Uncertainty around data center delay resolution

- Q4 2025 earnings preview expectations (Feb 18 report)

- Broader "neocloud" sentiment recovery or further deterioration

Key insight for the spread trade: The 1-year LEAPS show a MASSIVE 59.62% implied volatility with range from $30.91 to $136.69. This validates the spread structure:

- The $150 call sale sits ABOVE even the optimistic 1-year upper range ($136.69) - low probability of being exercised

- The $80 call purchase sits right in the middle of expected 1-year range - high probability of finishing in-the-money if stock stabilizes

This is brilliant positioning: selling low-probability far out-of-the-money calls for huge premium while buying high-probability in-the-money calls for reasonable cost.

🎪 Catalysts

🔥 Recent Catalysts (Already Happened - Past 3 Months)

Q3 2025 Earnings Disaster - November 10, 2025 💥

CRWV reported Q3 results that beat on revenue ($1.36B vs $1.29B consensus) and EPS (-$0.22 vs -$0.57 expected), BUT the stock CRASHED 16% immediately due to slashed guidance:

- 📊 Revenue backlog doubled to $55.6B (+$25B added in single quarter!) from OpenAI and Meta contracts

- 💰 Adjusted EBITDA: $838M (doubled from Q3 2024)

- 🚨 Guidance CUT: FY2025 revenue lowered to $5.05-5.15B from $5.15-5.35B

- 🏗️ Capex slashed 40%: From $21.5B to $13B due to "temporary delays related to third-party data-center developer"

- 📉 Stock reaction: Down 16% day-of, extended to -45% decline through November in the "neocloud crash"

Why this matters for the options trade: The stock crashed from $150+ in October to $85 by December. The call seller may have been underwater on a long position and is now monetizing the position at $150 strike while maintaining downside exposure through the $80 long calls.

OpenAI $22.4 Billion Partnership Expansion - September 25, 2025 🤝

- 🏭 Massive multi-year compute infrastructure commitment

- 💎 OpenAI invested $350M in CRWV stock as part of partnership

- 📈 Represents average annual revenue of ~$3.2B from single customer

- 🎯 Validates CRWV's technical capabilities at highest level (competing with their existing Nvidia partnership)

Meta $14.2 Billion Deal 🏢

Six-year contract with Meta Platforms worth $14.2B to supply AI compute workloads through 2031:

- 🖥️ Provides access to NVIDIA's advanced GB300 systems

- 💰 Average annual revenue of $2.3B

- 📊 Combined with OpenAI, these two customers alone represent $5.5B annual revenue - more than CRWV's entire 2025 revenue!

Failed Core Scientific Acquisition - October 30, 2025 ❌

CRWV's $9B all-stock acquisition of Core Scientific (NASDAQ: CORZ) was terminated after failing shareholder approval:

- 🏢 Would have provided 1.3 GW of gross power capacity

- 💸 Eliminated $10B+ in future lease obligations

- ⚠️ Failure highlighted CRWV's infrastructure dependency on third-parties (which came back to haunt them in Q3 delays)

🚀 Upcoming Catalysts (Next 6 Months)

Q4 2025 Earnings Report - February 18, 2026 (72 DAYS!) 📊

This is THE catalyst that could make or break the recovery thesis:

- 📅 Date: After market close on February 18, 2026

- 💰 Full-Year 2025 Guidance: Revenue $5.05-5.15B, adjusted operating income $690-720M

- 🎯 Key Metrics to Watch:

- Resolution of third-party data center construction delays (Texas, Oklahoma, North Carolina sites)

- Data center capacity additions and MW deployment progress

- Customer concentration trends (Microsoft was 71% of Q2 revenue - hopefully diversifying)

- Debt service and interest expense trajectory ($1.2B annual interest burden)

- Capital expenditure execution vs. revised $12-14B guidance

- GB300 deployment scaling updates

Critical questions:

- Have the construction delays been resolved as CEO Michael Intrator promised "rapidly"?

- Is 2026 capex guidance still "well in excess of double 2025" (implying $26-30B)?

- Any updates on customer diversification to reduce Microsoft concentration?

Upside scenario: Clean resolution of delays, strong 2026 guidance, customer wins → stock recovers to $120-140 range.

Downside scenario: Continued delays, conservative 2026 outlook, debt concerns → stock tests $70-75 support.

GB300 Production Scaling (Q4 2025 - Q2 2026) 🏭

CoreWeave became first cloud provider to deploy NVIDIA's GB300 NVL72 systems on July 3, 2025:

- 💪 10x boost in user responsiveness, 5x improvement in throughput per watt vs. Hopper

- 🚀 Plans to significantly scale deployments worldwide throughout 2025-2026

- 🎯 This is the technology edge that justifies premium pricing vs. hyperscalers

- ⚠️ Deployment success critical for maintaining competitive moat

The $80 March 2026 calls expire right as GB300 scaling results become visible - strategic timing!

Federal Market Entry & FedRAMP Authorization (2026) 🇺🇸

CRWV announced intent to enter U.S. federal government market on October 28, 2025:

- 🏛️ Targeting Defense Industrial Base and government agencies

- 📜 Pursuing FedRAMP authorization (12-24 month process)

- 🌍 Working on 40+ sovereign AI projects worldwide

- 💰 Could diversify revenue away from Microsoft concentration risk

- 🎯 Positions CRWV as strategic national security asset

European Data Center Launches (Q4 2025 - Q1 2026) 🌍

$3.5B investment in European expansion:

- 🇬🇧 UK: Two data centers in Crawley (October) and London Docklands (December) backed by £1B investment

- 🇳🇴 Norway: Completion by end of 2025

- 🇸🇪 Sweden: Partnership with EcoDataCenter for NVIDIA Blackwell clusters by end 2025

- 🇪🇸 Spain: Completion by end of 2025

- ♻️ All powered by 100% renewable energy

Geographic diversification reduces regulatory/geopolitical risk and taps growing European AI demand.

Third-Party Data Center Delay Resolution (Q1 2026) 🛠️

Management indicated delays at facilities in Texas, Oklahoma, and North Carolina tied to major third-party developer:

- ⏰ CEO stated delays "are going to be cleaned up rapidly" with CRWV "boots on the ground"

- 🏦 Bank of America analyst expects resolution by Q1 2026

- 📊 Successful resolution removes major overhang and could spark 20-30% relief rally

- ⚠️ Further delays would confirm structural execution problems and crater stock

This is THE near-term catalyst for the March 2026 calls - if delays resolve, $80 calls will be deep in-the-money!

📊 Analyst Activity & Price Targets

Recent Downgrades (Post-Crash):

- JPMorgan: Downgraded from Overweight to Neutral, price target cut to $110 from $135

- Loop Capital: Lowered to $120 from $165

- Evercore ISI: Cut to $160 from $175

Recent Upgrades:

- Roth MKM (Dec 5): Initiated with Buy rating and $110 price target (25-30% upside from current)

Current Consensus:

- Average Rating: "Buy" from 23-28 analysts

- Average Price Target: $127.84-$146.65 (44.78%-71.02% upside)

- Price Target Range: $32 (bearish extreme) to $430 (bull extreme)

The spread trade aligns with consensus: $150 short strike sits just above average price target, $80 long strike provides downside protection if bearish case materializes.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through the option expirations:

📈 Bull Case (30% probability)

Target: $120-150 by March 2026

How we get there:

- ✅ Q4 2025 earnings (Feb 18) meet/beat with clean resolution of data center delays

- 🏗️ Third-party construction issues fully resolved by Q1 2026 as promised

- 🚀 GB300 deployment scaling ahead of schedule with major customer wins announced

- 📊 2026 guidance strong: Revenue $7-8B, maintaining path to profitability

- 💰 Debt refinancing at lower rates, reducing $1.2B annual interest burden

- 🌍 European data centers operational and generating revenue

- 🇺🇸 Federal market progress (FedRAMP in process, early government contracts)

- 📈 Microsoft concentration decreases to <50% as OpenAI/Meta revenue ramps

- 🎯 Market sentiment on "neoclouds" recovers as AI infrastructure demand proven durable

Key metrics needed:

- Data center capacity reaching 700+ MW (from 590MW in Q3)

- Gross margins stable/improving (proving pricing power)

- Operating cash flow turning positive

- Backlog conversion accelerating ($55.6B contracted → revenue)

Probability assessment: 30% because it requires smooth execution across multiple fronts after recent stumbles. However, fundamentals remain strong (massive backlog, blue-chip customers, technical leadership) and stock is down 55% from peak - recovery thesis has merit.

Options trade P&L in Bull Case:

- $80 March 2026 calls at $120 stock: Worth $40.00, profit = $38.40/share × 10,000 = $38.4M gain (240% ROI!)

- $150 Jan 2028 calls at $120 stock: Worth ~$10-15 (time value), loss = ~$253.80/share × 25,000 = -$63.5M loss

- Net position: +$38.4M - $63.5M + $51M premium collected = +$25.9M profit on spread

🎯 Base Case (50% probability)

Target: $75-100 range (CONSOLIDATION)

Most likely scenario:

- 📊 Q4 earnings solid but unspectacular - meet lowered guidance

- ⚖️ Data center delays partially resolved but some issues persist into Q2 2026

- 🤖 GB300 deployment progressing steadily but not explosively

- 💸 2026 guidance conservative due to macro uncertainty and execution caution

- 🏦 Debt burden remains concern - interest expense stays elevated

- 📉 Stock trades in $75-100 range for months as market waits for proof points

- 💤 Volatility remains high but directional conviction low

- 🔄 Investors demand evidence of execution before re-rating multiple higher

This is likely what the spread trader expects: Stock consolidates in $80-100 range through 2026. The $80 March 2026 calls retain value or show modest profit, while $150 short calls decay over time. They've monetized $51M cash TODAY and maintain exposure to gradual recovery.

Why 50% probability: This is the "muddle through" scenario - neither disaster nor triumph. CRWV's fundamental story (massive backlog, customer quality) supports floor at $80, but execution concerns and debt burden prevent breakout above $100 near-term. Most institutions will hold and wait.

Options trade P&L in Base Case:

- $80 calls at $90 stock: Worth $10.00, profit = $8.40/share × 10,000 = $8.4M gain (53% ROI)

- $150 calls at $90 stock: Worth ~$5-8 (time value decays from $268), loss = ~$260/share × 25,000 = -$65M loss

- Net position: +$8.4M - $65M + $51M premium = -$5.6M small loss (but protected $212M stock position!)

📉 Bear Case (20% probability)

Target: $50-75 (TEST THE LONG STRIKE!)

What could go wrong:

- 😰 Q4 earnings miss with further guidance cuts - execution concerns compound

- 🚨 Data center delays extend beyond Q1 2026 - structural problems confirmed

- 💸 Major customer (Microsoft/OpenAI/Meta) reduces commitment or demands pricing concessions

- 📊 Debt burden becomes unsustainable - credit rating downgrade, liquidity concerns

- 🏦 Unable to refinance $14.6B debt at reasonable rates - interest expense rises

- ⚠️ Competitive pressure intensifies - AWS/Azure/Google offer competing AI infrastructure at lower prices

- 🌊 Broader "neocloud" selloff continues - contagion from other AI infrastructure stocks

- 💔 Break below $80 gamma support triggers cascade to $70, then $60

Critical support levels:

- 🛡️ $80: MUST HOLD (7.8B gamma) - this is where long calls struck!

- 🛡️ $75: Secondary floor (5.2B gamma)

- 🛡️ $70: Disaster scenario (3.8B gamma) - would imply serious fundamental concerns

Probability assessment: Only 20% because CRWV has $55.6B revenue backlog, $22.4B OpenAI contract, $14.2B Meta contract, and technical leadership. Fundamentals support current valuation even with execution hiccups. However, debt burden ($14.6B), customer concentration (71% Microsoft), and third-party infrastructure dependency create real tail risks.

Options trade P&L in Bear Case:

- $80 calls at $65 stock: Worth $0 (out-of-the-money), loss = -$16M (100% loss)

- $150 calls at $65 stock: Worth $0-1 (time value only), loss = ~$267/share × 25,000 = -$66.75M

- Net position: -$16M - $66.75M + $51M premium = -$31.75M loss (but underlying stock lost much more!)

The beauty of this structure: Even in bear case, the $51M premium collected partially offsets losses. If they held naked stock, losses would be catastrophic ($212M → $163M = -$49M loss). This spread limits damage.

💡 Trading Ideas

🛡️ Conservative: Wait for Earnings Clarity (Cash Gang)

Play: Stay on sidelines until after February 18th Q4 earnings

Why this works:

- ⏰ Earnings in 72 days creates binary event risk - too much uncertainty pre-results

- 💸 Volatility elevated (11.4% implied move for Dec OPEX) - options expensive

- 📊 Stock at inflection point - could break either direction based on delay resolution

- 🎯 Better entry likely post-earnings after picture clarifies

- 🤔 The $83M institutional spread signals even smart money is UNCERTAIN about direction

Action plan:

- 👀 Monitor Q4 earnings closely for:

- Data center delay resolution status

- 2026 capex guidance (confirms/reduces $26-30B estimate)

- Customer concentration metrics

- GB300 deployment progress

- Debt refinancing opportunities

- 🎯 Look for pullback to $70-75 gamma support for stock entry if bear case, OR

- 📈 Wait for breakout above $100 with volume if bull case confirms

- ✅ Need concrete proof delays resolved before committing capital

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -15-20% drawdown if earnings disappoint. Get clarity on execution before risking capital. Maintain optionality.

⚖️ Balanced: Copy the Pro Spread (Scaled Down)

Play: Replicate the institutional diagonal call spread structure at retail scale

Structure (Post-Earnings):

- Sell 10 Jan 2028 $150 calls

- Buy 5 March 2026 $80 calls

Why this works:

- 🎢 Mimics exact institutional positioning - "copy the smart money"

- 💰 Generates immediate net credit (collect more premium than you pay)

- 📊 Defined risk spread with capped upside at $150 but protection below $80

- 🎯 Targets same price zones where institutions positioned ($80 support, $150 resistance)

- ⏰ Different time horizons create income from time decay on short calls

- 🛡️ If you own CRWV stock, short calls provide covered call income

Estimated P&L (retail scale - 10:5 ratio):

- 💰 Collect ~$26,800 from selling 10 Jan 2028 $150 calls

- 💸 Pay ~$16,000 for buying 5 March 2026 $80 calls

- 💵 Net credit: $10,800 collected upfront

Profit/Loss scenarios:

- 📈 Stock at $120 by March 2026: Long $80 calls worth $40 = +$20,000; Short $150 calls worth $10 = -$10,000; Net = +$20,800 profit

- 🎯 Stock at $90 by March 2026: Long calls worth $10 = +$5,000; Short calls worth $5 = -$5,000; Net = +$10,800 (keep premium)

- 📉 Stock at $70 by March 2026: Long calls expire worthless = -$16,000; Short calls worth $2 = -$2,000; Net = -$7,200 loss (but collected $10,800, so still +$3,600!)

Entry timing:

- ⏰ Wait until after Feb 18 Q4 earnings for volatility to settle

- 🎯 Only enter if stock trading $80-95 range (gives spread room to work)

- ❌ Skip if stock already above $110 (spread too narrow) or below $70 (too risky)

Position sizing: Use only 5-10% of portfolio for this speculative spread

Risk level: Moderate (net credit but capped upside) | Skill level: Intermediate (requires understanding diagonal spreads)

🚀 Aggressive: Volatility Play - Long Straddle into Earnings (ADVANCED!)

Play: Bet on massive post-earnings move exceeding implied 11.4%

Structure:

- Buy Dec 2025 $85 calls

- Buy Dec 2025 $85 puts

Why this could work:

- 💥 Implied move only 11.4% but CRWV moved 45% in November alone

- 🎰 Betting market UNDERPRICES earnings volatility given execution uncertainty

- 📊 Stock could EXPLODE either direction based on delay resolution news

- 🚀 Clean resolution + strong guidance = gap to $110+

- 😱 Continued delays + weak outlook = crash to $65-70

- ⚡ Only need 15%+ move either way to profit after IV crush

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Straddle costs

$12-15 per contract ($1,200-1,500) - ⏰ TIME DECAY KILLER: Theta burns premium daily approaching earnings

- 😱 IV CRUSH: Even if stock moves 8-10%, volatility collapse could cause LOSS

- 📊 Two-way risk: Stock stays $80-90 and you lose entire premium

- ⚠️ Earnings could be "fine but not exciting" - stock gaps to $88-92 (only 5% move) and straddle loses 50%

Estimated P&L:

- 💰 Cost: ~$12-15 per straddle

- 📈 Profit scenario: Stock moves to $110 or $65 (20%+ move) = $25+ gain (166%+ ROI)

- 🚀 Home run: Stock moves to $120 or $55 (30%+ move) = $35+ gain (233%+ ROI)

- 📉 Loss scenario: Stock ends $80-90 range = lose $8-12 (60-80% loss)

- 💀 Total loss: Stock flat at $85 = lose entire $12-15 (100% loss)

Breakeven points:

- 📈 Upside breakeven: ~$98-100

- 📉 Downside breakeven: ~$70-72

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand IV crush mechanics and have traded earnings straddles before

- ✅ Can afford to lose ENTIRE premium (high probability!)

- ✅ Accept you're betting AGAINST options market pricing

- ✅ Can monitor position closely on Feb 18-19 and take profits quickly

- ⏰ Plan to close within 24-48 hours post-earnings (don't hold to expiration)

Risk level: EXTREME (100% loss possible) | Skill level: Advanced only

Probability of profit: ~35% (lower than implied due to IV crush)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q4 Earnings binary event (Feb 18): Results could determine whether stock breaks to $120 or crashes to $65. Data center delay resolution is EVERYTHING - CEO promised "cleaned up rapidly" but if delays extend, credibility shattered. Historical precedent shows CRWV gapped -16% on Q3 earnings despite beating estimates.

-

💸 Debt service burden crushing cash flow: $14.6B total debt generating $1.2B annual interest at ~11% average cost. Monthly obligations approaching $350-420M against negative operating cash flow. Current ratio of 0.44 with $7.6B current liabilities creates liquidity risk. Credit ratings speculative-grade (B1/BB-). If refinancing fails or rates rise, stock could collapse.

-

🇨🇳 Customer concentration catastrophic if Microsoft/OpenAI reduce spend: Microsoft alone represented 71% of Q2 2025 revenue, down slightly from 77% of 2024 revenue from top 2 customers. Any reduction in Microsoft commitment, OpenAI deployment delays, or Meta scaling back would crater revenue. 96% of revenue from take-or-pay contracts provides near-term visibility but faces renewal risk if AI investment cycle slows.

-

🏗️ Third-party infrastructure dependency is structural weakness: CRWV owns almost NONE of its data center infrastructure, leasing from third-parties. Recent construction delays at Texas, Oklahoma, North Carolina sites forced 40% capex cut and $200M revenue reduction. $34B in off-balance-sheet lease payments starting between now and 2028. Failed Core Scientific acquisition highlighted this vulnerability.

-

⚖️ Hyperscaler competition intensifying: AWS, Azure, Google collectively spending hundreds of billions on AI infrastructure. Google alone allocated $85B capex for 2025. CRWV can't match hyperscaler resources long-term. While 30-80% pricing advantage exists today, hyperscalers could close gap with scale economics. CRWV lacks ecosystem moat - no managed databases, integrated analytics, or prebuilt AI platforms like SageMaker/Vertex AI.

-

🚀 Massive 2026 capex ($26-30B) requires continuous capital access: Management expects capex "well in excess of double" 2025's $13B, implying $26-30B+ in 2026. Total capex guidance over 18 months: $37-44B. This requires continuous access to capital markets potentially in unfavorable conditions. At speculative credit ratings, cost of capital could spike.

-

💔 "Neocloud crash" contagion risk: CRWV suffered 45% plunge in November 2025 as part of broader selloff affecting high-flying AI infrastructure stocks. Valuation multiple compression could persist if AI infrastructure spending concerns mount. Short seller Kerrisdale Capital calls CRWV "debt-fueled GPU rental business with no moat, dressed up as innovation" with 90% downside potential.

-

🐋 Insider selling signal ($763M over 24 months): Major shareholder Magnetar sold $372M in September, CEO sold $50M, CFO sold $85M. This massive insider selling right before stock crashed raises questions about management confidence vs. public guidance. Why sell if they believed in $150+ targets?

-

📊 Valuation still rich despite crash: At $44B market cap on $5.1B FY2025 revenue (8.6x sales), CRWV trades at premium multiples. While down from peak, valuation assumes flawless execution on $55.6B backlog conversion, zero customer churn, successful GB300 scaling, and debt burden manageability. Limited margin of safety at current prices.

-

🎢 Extreme volatility creates whipsaw risk: Stock moves 5-10% on no news regularly. 62.7% annualized volatility means CRWV can gap $8-10 overnight. This isn't blue-chip infrastructure - this is speculative growth with execution risk. November crash from $150 to $85 (-43%) in weeks shows how fast sentiment shifts.

🎯 The Bottom Line

Real talk: Someone just deployed an $83 MILLION options spread that perfectly captures the CRWV dilemma - massive long-term potential tempered by near-term execution risk and debt burden concerns.

What this trade tells us:

- 🎯 Sophisticated institution expects stock to stabilize in $80-100 range through 2026, NOT crash to $50 but also NOT rocket back to $150+ anytime soon

- 💰 They're monetizing $67M from covered calls while maintaining $16M exposure to recovery through March 2026

- ⚖️ The structure shows they're 50-60% less bullish than before (reduced from 25,000 to 10,000 call equivalents) but NOT abandoning position entirely

- 📊 Striking at $150 for short calls suggests they think stock needs 2-3 YEARS to reach those levels, not months

- ⏰ Buying $80 March 2026 calls signals confidence in data center delays resolving and GB300 deployments progressing - they just want downside protection during uncertainty

This is NOT a "sell everything" signal - it's a "take profits on portion, maintain exposure to upside, protect downside" trade.

If you own CRWV:

- ✅ Consider trimming 30-50% at $85-90 levels (lock in gains from IPO $40, reduce risk exposure)

- 📊 Set MENTAL STOP at $75-80 (major gamma support) if holding through earnings

- 🛡️ Consider selling covered calls at $100-110 strikes (generate income while capped upside acceptable)

- ⏰ Don't fight the tape - stock has serious execution challenges to work through before returning to $150

- 🎯 If Q4 earnings clean and delays resolve, could re-add trimmed shares on breakout above $100

If you're watching from sidelines:

- ⏰ February 18 Q4 earnings is the moment of truth - DO NOT enter before clarity!

- 🎯 Post-earnings dip to $70-75 would be EXCELLENT entry for long-term hold (gamma support + 50% off peak)

- 📈 Looking for confirmation: Delay resolution, 2026 capex guidance manageable, customer diversification progress, debt refinancing at lower rates

- 🚀 Longer-term (12-24 months), OpenAI/Meta contract execution and federal market entry are legitimate catalysts for $120-150 if execution delivers

- ⚠️ Current valuation requires FLAWLESS execution - one more stumble and it's back to $60-70

If you're bearish:

- 🎯 First major support at $80 (7.8B gamma - THE LINE), deeper support at $75 (5.2B gamma)

- 📊 Break below $80 would be catastrophic - triggers cascade to $70, potentially $60

- ⚠️ Post-earnings put spreads ($90/$80 or $85/$75) offer defined-risk way to play downside

- ⏰ Wait for earnings - if delays persist and guidance weak, bearish thesis confirmed

Mark your calendar - Key dates:

- 📅 December 19 - Monthly/Quarterly OPEX (±11.4% implied move window)

- 📅 End December 2025 - European data centers (Norway, Sweden, Spain) scheduled completion

- 📅 Q1 2026 - Third-party data center delays expected resolution

- 📅 February 18, 2026 - Q4 2025 earnings report (THE BIG ONE!)

- 📅 March 20, 2026 - Expiration of the $16M long $80 call position

- 📅 January 21, 2028 - Expiration of the $67M short $150 call position

Final verdict: CRWV's AI infrastructure story remains INCREDIBLY compelling long-term - $55.6B backlog, OpenAI $22.4B + Meta $14.2B contracts, GB300 technical leadership, federal market entry. BUT, at $44B market cap with $14.6B debt, third-party infrastructure dependency, and customer concentration, the risk/reward is UNCERTAIN short-term. The $83M institutional spread is a CLEAR signal: smart money is derisking but not abandoning the position.

Be patient. Let Q4 earnings (Feb 18) provide clarity. The AI revolution will still be here in 3 months, and you'll sleep better entering at $75 after confirmation rather than $85 with fingers crossed.

This is infrastructure buildout - measured in years, not quarters. Protect your capital. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual scores (633.24 and 51.62 Z-scores) reflect trade size relative to recent CRWV history - they do not imply trades will be profitable or that you should follow them. Diagonal call spreads are complex strategies requiring advanced understanding of time decay, volatility, and multi-leg risk management. Q4 earnings create binary event risk with potential for 15-20% gaps either direction. The spread trader may have complex portfolio hedging needs not applicable to retail traders. Always do your own research and consider consulting a licensed financial advisor before trading.

About CoreWeave: CoreWeave offers the CoreWeave Cloud Platform which consists of proprietary software and cloud services that deliver the automation and efficiency needed to manage complex AI infrastructure at scale, with a market cap of $44.0 billion in the Services-Prepackaged Software industry.