🛡️ CRWV $8.7M Risk Reversal - Big Money Betting Against AI Cloud Hype! 🐻

📅 December 16, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just executed an $8.7 MILLION risk reversal on CoreWeave this morning at 10:09:53! This sophisticated two-leg trade bought 5,000 puts at $45 strike for $4.8M protection while simultaneously selling 5,000 calls at $165 strike for $3.9M - netting a $900K debit for bearish positioning on January 15, 2027 expiration. With CRWV at $69.55 and down 61% from all-time highs, smart money is betting on further downside while capping any potential recovery above $165. Translation: Institutional investors are structuring a bearish bet on the AI infrastructure poster child, expecting weakness over the next 13 months!

📊 Company Overview

CoreWeave (CRWV) is a modern AI cloud infrastructure company competing in the exploding GPU-as-a-service market:

- Market Cap: $36.05 Billion

- Industry: Prepackaged Software Services / AI Cloud Infrastructure

- Current Price: $69.55 (down from $187 peak in June 2025)

- Primary Business: AI cloud platform, GPU infrastructure, data center services for AI model training and inference

- IPO: March 28, 2025 at $40/share (currently up 74% from IPO but down 63% from peak)

💰 The Option Flow Breakdown

The Tape (December 16, 2025 @ 10:09:53):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:09:53 | CRWV | MID | BUY | PUT $45 | 2027-01-15 | $4.8M | $45 | 5,000 | 257 | 5,000 | $69.55 | $9.52 |

| 10:09:53 | CRWV | MID | SELL | CALL $165 | 2027-01-15 | $3.9M | $165 | 5,000 | 265 | 5,000 | $69.55 | $7.87 |

Net Position: Risk Reversal (Bearish Collar) with $900K net debit paid

🤓 What This Actually Means

This is a risk reversal - one of the most sophisticated bearish strategies in the options playbook! Here's what went down:

- 🛡️ Bought downside protection: $4.8M for $45 strike puts - pays off dollar-for-dollar below $45 (35% below current price)

- 💸 Sold upside participation: $3.9M premium collected from $165 calls - caps gains if CRWV rallies above $165 (137% above current)

- 💰 Net cost: $900K total debit ($1.80/share on 500K shares notional)

- ⏰ Time horizon: 395 days to expiration (January 15, 2027) - catching Q4 2025 earnings (Feb 18), full year 2026 results, and product launches

- 📊 Notional exposure: Controls 500,000 shares worth $34.8M at current price

- 🎯 Breakeven: Needs CRWV below $66.55 by expiration to profit (4.3% downside from entry)

What's really happening here:

This trader is making a DIRECTIONAL bearish bet with asymmetric risk/reward. The structure says: "I think CRWV is going lower over the next 13 months, but I'm willing to give up upside above $165 to reduce the cost of my bearish position." This isn't a hedge - this is a VIEW.

The trade makes money if CRWV falls below the $66.55 breakeven (current $69.55 minus $3 net credit after accounting for the collar structure). Maximum profit occurs anywhere below $45, where the $45 puts reach full value while the $165 calls expire worthless. That's a potential $21.55/share profit ($10.8M total) on the $900K investment - a 12:1 return if the bearish thesis plays out.

Risk profile:

- ✅ Max Profit: $10.8M if CRWV closes below $45 (1,100% return)

- ⚠️ Max Loss: $900K net debit if CRWV stays between $66.55-$165 at expiration

- ❌ Unlimited Loss Above $165: If CRWV rallies above $165, the short calls create losses dollar-for-dollar (though offset by long puts)

Unusual Score: 🔥 EXTREMELY UNUSUAL - Both legs scored extraordinarily high:

- $45 Put leg: Z-score 426.72 (happens 19.5x larger than average volume)

- $165 Call leg: Z-score 194.28 (happens 18.9x larger than average volume)

This level of unusual activity in BOTH legs executed simultaneously screams institutional positioning. The volume-to-open-interest ratios are extreme (19.5 and 18.9 respectively), meaning this trade represents entirely new positioning, not an unwind.

📈 Technical Setup / Chart Check-Up

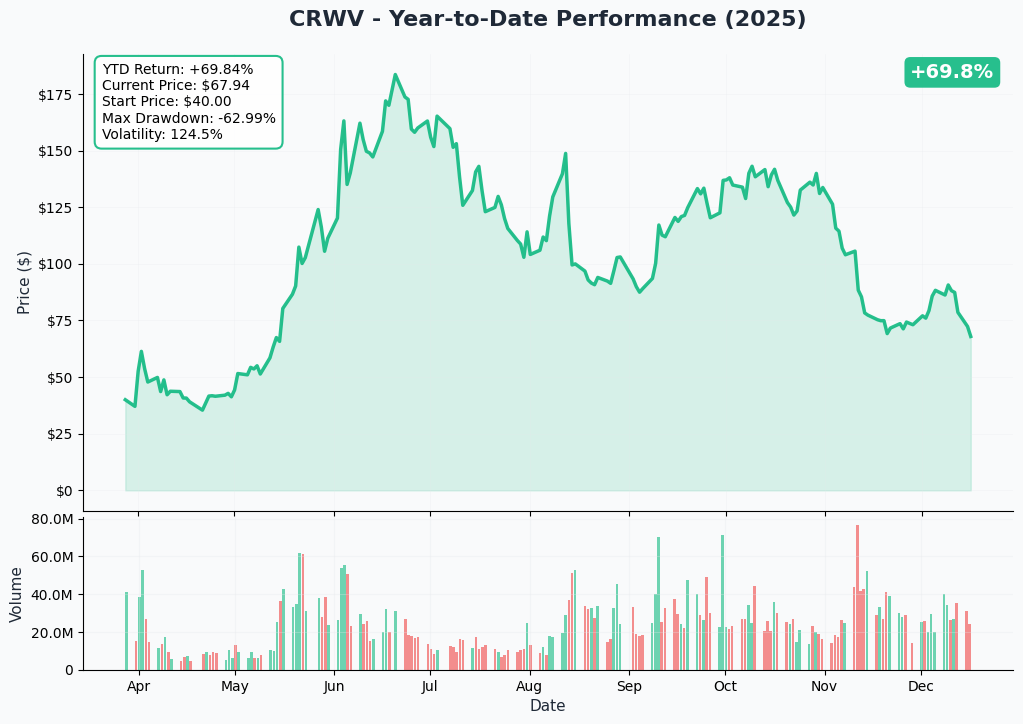

YTD Performance Chart

CRWV has had a BRUTAL year since its euphoric June peak. After IPO-ing at $40 in March 2025, the stock exploded to $187 by June on AI infrastructure hype - only to collapse 63% to current levels around $69. The chart screams "growth stock reality check":

Key observations:

- 🚀 Post-IPO euphoria: Rocketship from $40 to $187 (367% gain) in just 3 months on AI cloud narrative

- 📉 Peak destruction: Down 61% from $187 all-time high - one of the worst performing tech IPOs of 2025

- ⚠️ Failed bounce attempts: Multiple rallies above $90 have failed, creating a series of lower highs

- 📊 Volume spike on selloffs: Distribution pattern as early investors and insiders take profits

- 💔 Below key support: Currently trading below most institutional cost bases from summer 2025

- 🎢 Extreme volatility: 20% intraweek swings common - stock fell from $90 to $72 in just one week (Dec 9-15)

The technical picture aligns perfectly with the bearish risk reversal: CRWV is in a confirmed downtrend with no clear support until much lower levels. The options trader is betting this technical breakdown continues.

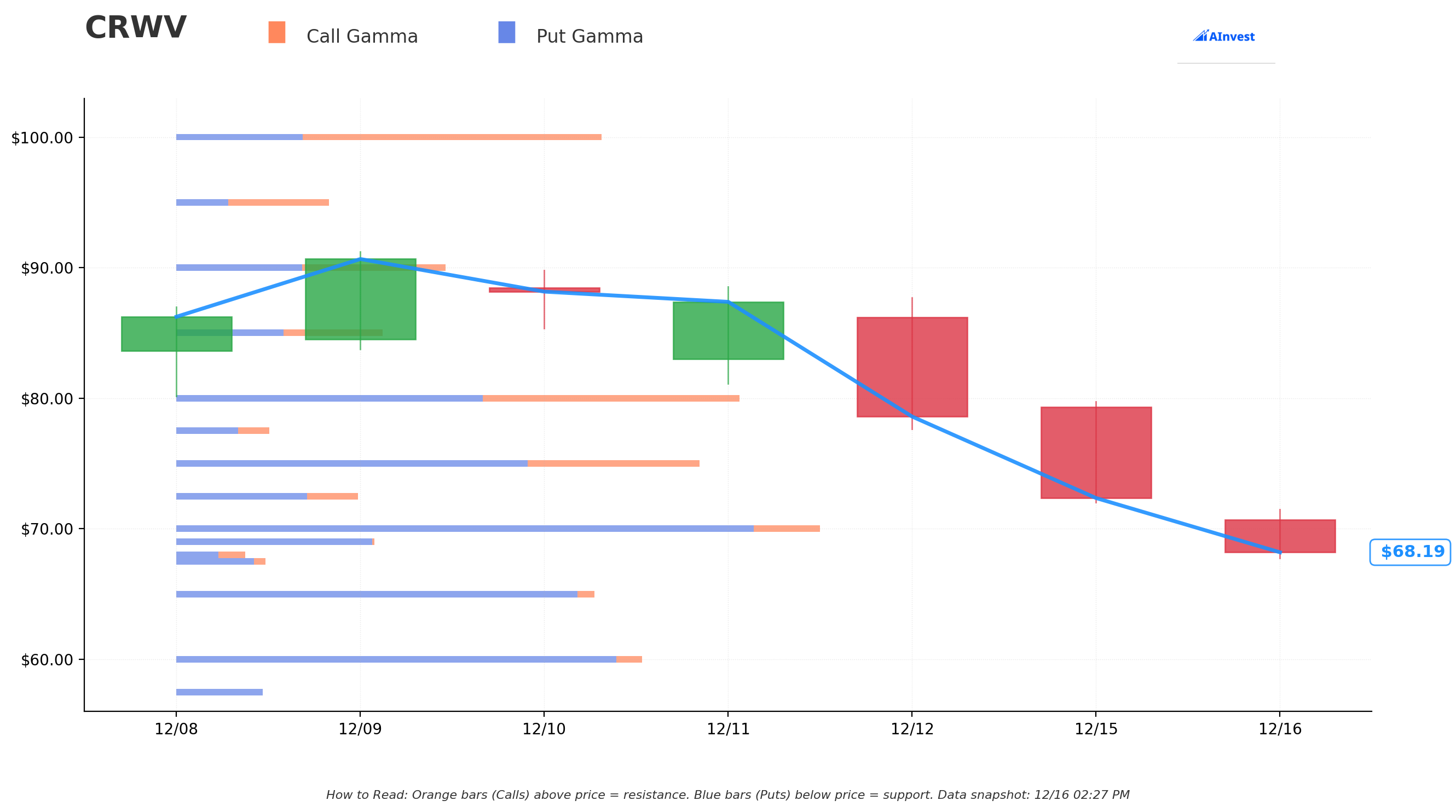

Gamma-Based Support & Resistance Analysis

Current Price: $68.42

The gamma exposure map reveals a bearish technical setup with limited near-term support and massive overhead resistance:

🔵 Support Levels (Put Gamma Below Price):

- $67.50 - Immediate support with 1.39B total gamma (WEAK - only 1.34% below current)

- $65 - Secondary support at 6.46B gamma (4.99% below current, first meaningful floor)

- $60 - Major structural floor with 7.06B gamma (12.3% below - THIS IS THE LINE IN THE SAND)

- $55 - Deep support at 1.85B gamma (19.6% below - potential capitulation zone)

🟠 Resistance Levels (Call Gamma Above Price):

- $69 - Immediate ceiling with 3.09B gamma (0.85% overhead)

- $70 - Strong resistance at 10.07B gamma (2.3% above - MASSIVE CEILING HERE!)

- $72.50 - Secondary resistance at 2.87B gamma (5.96% above)

- $75 - Major ceiling zone with 8.38B gamma (9.6% rally required)

- $77.50 - Extended resistance at 1.48B gamma (13.3% above)

- $80 - Psychological barrier with 9.05B gamma (16.9% rally needed)

What this means for traders:

CRWV is trapped in a BEARISH gamma profile! The lack of strong support nearby ($67.50 is paper-thin at 1.39B gamma) means any selling pressure could accelerate quickly toward $65 or even $60. Meanwhile, massive overhead resistance at $70 (10.07B gamma) acts like a brick wall preventing rallies.

Notice the setup? The risk reversal buyer structured protection at $45 strike, which is 34% below current price but captures potential capitulation if CRWV breaks the critical $60 level (which holds 7.06B gamma support). They're positioning for a potential flush through all support levels.

The $165 call sold is 141% above current price - essentially saying "I don't believe CRWV can more than double from here even with 13 months to work with."

Net GEX Bias: BEARISH - Net gamma of -27B (69.9B put gamma vs 42.7B call gamma). This negative gamma positioning means market makers will AMPLIFY moves - they'll sell into rallies and buy into dips, creating choppy volatile action that favors the downside.

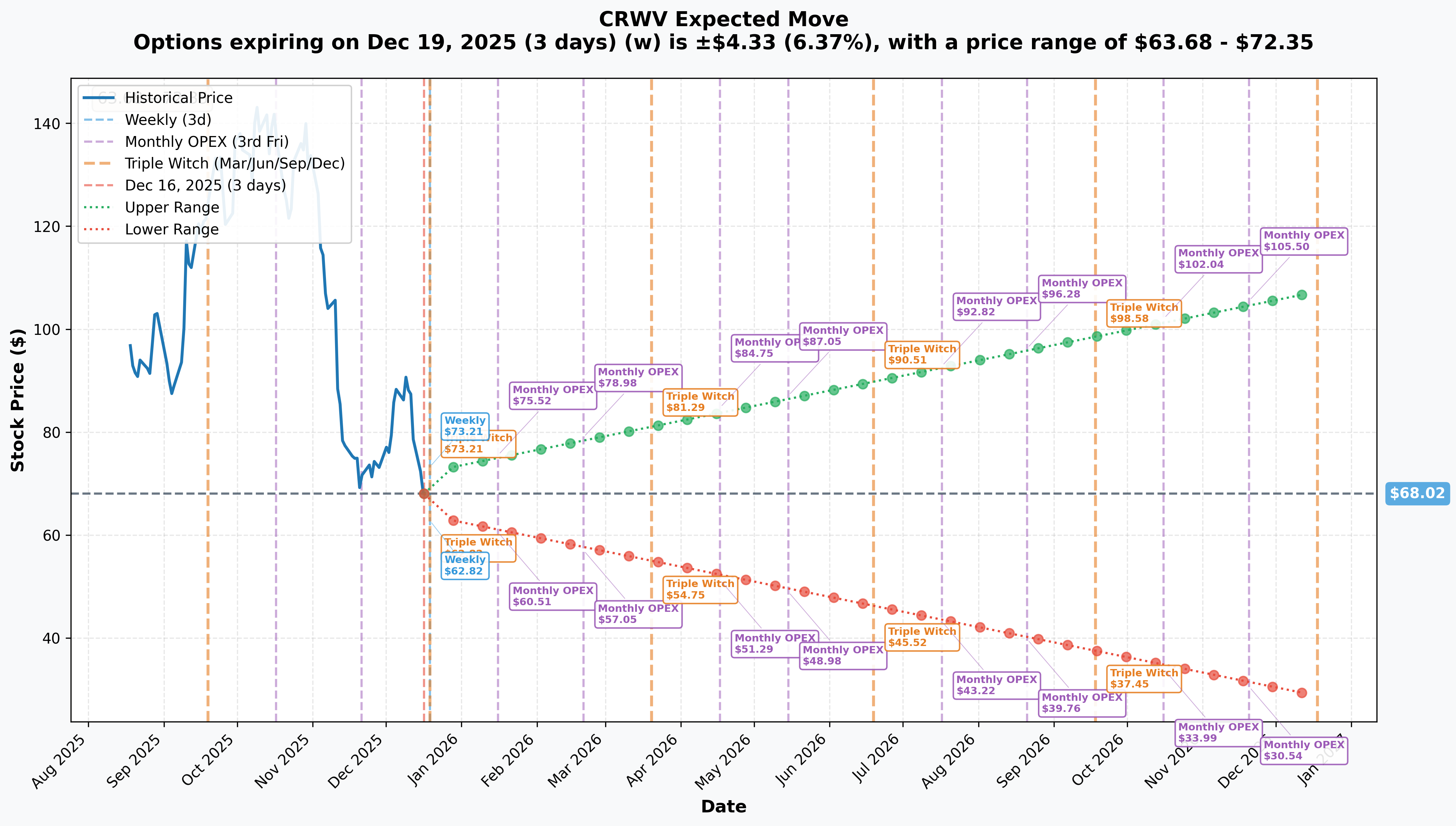

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 3 days): ±$4.33 (±6.37%) → Range: $63.68 - $72.35

- 📅 Monthly OPEX (Dec 19 - 3 days - TRIPLE WITCH!): ±$4.33 (±6.37%) → Range: $63.68 - $72.35

- 📅 Quarterly Triple Witch (Dec 19 - 3 days): ±$4.33 (±6.37%) → Range: $63.68 - $72.35

- 📅 Yearly LEAPS (Dec 18, 2026 - 367 days): ±$39.31 (±57.8%) → Range: $28.71 - $107.33

Translation for regular folks:

The options market is pricing 6.4% volatility through this Friday's Triple Witch expiration - that's massive! This week could see CRWV swing between $63.68 and $72.35, which conveniently brackets the current gamma support/resistance levels.

The yearly LEAPS (similar timeframe to our risk reversal trade) shows even MORE dramatic expectations: ±57.8% implied move with a lower bound of $28.71 and upper bound of $107.33. This tells us the options market sees HUGE uncertainty in CRWV's future.

Key insight: The risk reversal structure ($45 put / $165 call) sits OUTSIDE the yearly implied move range on the call side, but the $45 put is well within the bearish scenario (lower bound $28.71). The trader is betting CRWV trends toward the bearish end of expectations rather than the bullish scenario.

🎪 Catalysts

🔥 Upcoming Catalysts (What's Ahead)

Q4 2025 Earnings - February 18, 2026 (64 DAYS AWAY!) 📊

CRWV reports Q4 2025 results on February 18, 2026 after market close per Nasdaq's earnings calendar and MarketBeat's schedule. This is THE catalyst that could validate or destroy the recent selloff narrative:

What Wall Street is watching:

- 📊 Full Year 2025 Revenue: Guidance of $5.05-$5.15B total (Q4 implied $1.33-$1.43B)

- 💰 Adjusted EBITDA: Q3 hit $838M (doubled YoY) - can they maintain momentum?

- 🏗️ Data Center Delays Impact: Q4 guidance was CUT by $100-200M due to third-party construction delays

- 💸 Debt Service Coverage: $311M quarterly interest expense on $14.03B debt - GAAP margins only 4%

- 📈 2026 Guidance: Expected CapEx of $26-30B (more than 2x 2025's $12-14B)

- 🤝 Customer Concentration: Reducing 62% Microsoft revenue dependency with Meta and OpenAI ramps

Bear case risks: Any further delay announcements, customer concentration concerns, margin compression, or conservative 2026 guidance could trigger another leg down. The stock already fell 20% in one week (Dec 9-15) on convertible debt announcement - fragile sentiment.

Bull case scenario: Strong Q4 execution, raised 2026 guidance, customer diversification progress, or profitability pathway could spark relief rally toward $85-90 resistance.

$14.2 Billion Meta Partnership Ramp (2026-2031) 🤝

CoreWeave's landmark agreement with Meta announced September 30, 2025 to provide computing capacity through December 2031:

- 💰 Contract Value: $14.2 billion commitment with option to extend through 2032

- 🚀 Revenue Impact: Stock surged 12-14% on announcement

- 🎯 Strategic Importance: Reduces reliance on Microsoft (71% of Q2 revenue)

- 🏭 Technology: Meta gains access to NVIDIA GB300 systems operated by CoreWeave

- 📊 Quarterly Revenue: Expected $500M-$1B contribution begins ramping through 2026

Why this matters for the risk reversal: If Meta deployment encounters delays, performance issues, or scope reductions, the bull case for CRWV valuation collapses. The trade expires January 2027 - perfectly positioned to capture any Meta ramp execution risks through 2026.

$22.4 Billion OpenAI Commitments (Cumulative) 🤖

CoreWeave has become OpenAI's infrastructure partner with escalating commitments:

- 💰 Initial Contract: $11.9 billion signed March 2025

- 📈 May Addition: $4 billion expansion

- 🎯 September Extension: Additional $6.5 billion bringing total to $22.4B

- 🚀 Stargate Project: OpenAI's initiative aims for 10 GW capacity with potential $500B investment

- 🏗️ Deployment: Supports training of OpenAI's most advanced next-generation models

Risk factor: Microsoft owns 46% of OpenAI and operates Azure as OpenAI's primary infrastructure. If Microsoft-OpenAI dynamics shift or if OpenAI's Stargate ambitions prove unrealistic, CoreWeave's largest contracts evaporate.

NVIDIA GB300 NVL72 First Deployment Advantage 🎮

CoreWeave announced on July 3, 2025 becoming first cloud provider to deploy NVIDIA GB300 NVL72 platform:

- 🏆 First-to-Market: Consistent pattern across H100, H200, GB200, and now GB300 generations

- 💾 Specs: Each GB300 NVL72 rack features 21 TB total GPU memory

- 🚀 Performance: Up to 10x boost in user responsiveness vs prior generation

- 🤝 NVIDIA Partnership: NVIDIA holds equity stake ($100M invested April 2023)

Timeline Risk: Deployment scaling through 2026 will determine if CoreWeave can maintain technology leadership edge versus hyperscalers.

Runway AI Partnership (Announced December 11, 2025) 🎬

Brand new multi-year contract announced December 11, 2025 to power Runway's AI video models:

- 🎥 Workload: Runway will utilize GB300 NVL72 systems for training/inference

- 🏭 Integration: W&B Models for observability and W&B Inference powered by CoreWeave

- 🎬 Runway Profile: Leader in video generation used by major film studios, gaming companies, robotics developers

- 💰 Revenue Impact: Contract size undisclosed but adds to customer diversification narrative

2026 Capital Expenditure Guidance ($26-30 Billion Projected) 💸

Company expects CapEx "well in excess of double" 2025's $12-14B:

- 📊 2025 CapEx: $12-14 billion guidance for current year

- 🎯 2026 Estimate: $26-30 billion projected for data center expansion and GPU procurement

- ⚠️ Debt Implications: With $14.03B existing debt and $2.587B new convertibles, massive CapEx needs could force additional dilutive capital raises

Critical question: Can CoreWeave fund $26-30B CapEx without destroying shareholder value through equity dilution? The risk reversal trader is betting NO.

💔 Past Catalysts (What Already Happened)

Failed Core Scientific Acquisition (Terminated October 30, 2025) ❌

CoreWeave announced $9B all-stock acquisition of Core Scientific on July 7, 2025:

- 💰 Deal Terms: $9 billion all-stock at 0.1235 CRWV shares per CORZ share, implying $20.40/share

- 🏭 Strategic Rationale: Would have provided 1.3 GW of power across national data center footprint

- ❌ Shareholder Rejection: Voted down October 30, 2025 following negative recommendation from largest shareholder Two Seas Capital

- 📉 Impact: Eliminated planned $10+ billion reduction in cumulative future lease overhead

- 💔 Market Reaction: Core Scientific stock rose post-rejection, trading at $6.6B market cap

Takeaway: Failed M&A signals potential strategic execution risk and difficulty securing power capacity through acquisitions. CoreWeave must now contract capacity at market rates versus owning infrastructure.

$2.587 Billion Convertible Debt Offering (December 2025) 💸

Announced $2B convertible senior notes December 8, 2025, upsized to $2.25B, ultimately $2.587B including full exercise:

- 📊 Terms: 1.75% coupon, due 2031, conversion price approximately $107.80

- 📉 Market Reaction: Stock fell 7% in premarket trading on announcement

- 💰 Purpose: Fund continued data center expansion amid massive CapEx needs

- 🛡️ Dilution Protection: Includes capped call transactions to reduce potential dilution

- ⚠️ Debt Load: Adds to already $14.03B total debt burden

Why this matters: The convertible debt at $107.80 conversion price (55% above current $69.55 price) shows underwriters are skeptical CRWV reaches those levels. The 7% selloff signals market exhaustion with constant capital raises.

CEO & CFO Insider Selling (December 2025) 📉

Significant executive sales raised red flags:

- 👔 CEO Michael Intrator: Sold 54,771 shares December 3 for ~$6.3M at $74.17-$79.53/share

- 👔 Additional CEO Sales: 82,455 shares around $76.88 totaling $6.3M

- 💼 CFO Nitin Agrawal: Sold 66,467 shares December 11 at $82.58 for $5.49M

- 📋 Context: Sales pursuant to Rule 10b5-1 trading plans, but timing after 61% decline raises questions

- 💸 Total: ~$12M sold by top two executives in December alone

Market interpretation: While some sales attributed to tax withholding obligations from RSU vesting, the optics are terrible given stock's collapse and CEO interview saying company is "misunderstood".

Q3 2025 Earnings Beat (November 10, 2025) 📊

CRWV reported Q3 results November 10, 2025:

- 💰 Revenue: $1.36B vs $1.29B consensus (5.43% beat), up 134% YoY

- 📉 EPS: -$0.22 vs -$0.57 expected (61.4% beat)

- 💸 Net Loss: $110M improved from $360M in Q3 2024

- 📈 Adjusted EBITDA: $838M (doubled from prior year)

- 📊 Operating Income: $51.9M (down 56% YoY due to increased expenses)

- 🎯 Backlog: Added $25B+ in Q3, bringing total to $55+ billion (nearly doubled from Q2)

- ⚠️ Guidance Cut: Full year revenue lowered to $5.05-$5.15B from $5.15-$5.35B due to data center delays

Market reaction: Despite beat, stock continued declining on guidance cut and debt/profitability concerns. The $55B backlog sounds impressive but conversion to actual revenue remains uncertain.

🎲 Price Targets & Probabilities

Using Gamma Levels and Implied Move for Price Targets:

Based on gamma exposure data and implied volatility through January 2027 (when the risk reversal expires), here are the realistic scenarios:

🐻 Bear Case: $45-55 (Target of Risk Reversal)

Probability: 25-30%

Thesis: Customer concentration risks materialize, Microsoft reduces commitments, Meta/OpenAI deployments encounter delays, or $26-30B 2026 CapEx requires massive dilutive equity raise. The January 2027 $45 put becomes profitable.

Catalysts supporting bear case:

- ❌ Failed Core Scientific acquisition shows execution challenges in securing 1.3 GW power capacity

- 💸 $14B+ debt with only 4% GAAP operating margins can't cover $311M quarterly interest expense

- ⚠️ Data center construction delays already cut Q4 2025 guidance by $100-200M

- 🔴 D.A. Davidson analyst price target: $36 (50% downside), calling it "one of the ugliest balance sheets in technology"

- 📉 Technical breakdown: No major gamma support until $60 level (7.06B), then $55 (1.85B)

- 🏦 Hyperscalers (AWS, Azure, Google Cloud) building massive competing GPU capacity

- 👔 CEO and CFO sold $12M+ combined in December despite stock already down 61%

Price targets: $55 (gamma support) → $45 (max profit zone for risk reversal) → $32 (HSBC target)

📊 Base Case: $60-75 (Sideways Churn)

Probability: 40-45%

Thesis: CRWV muddles through with mixed execution - some customer wins offset by continued cash burn and dilution. Stock remains range-bound between $60 support and $75 resistance as market waits for proof of profitable scale.

Catalysts supporting base case:

- ✅ $55B revenue backlog provides revenue visibility but conversion uncertain

- 🤝 $14.2B Meta contract and $22.4B OpenAI commitments reduce Microsoft concentration

- 📈 134% YoY revenue growth and doubled adjusted EBITDA show operational progress

- ⚖️ First-to-market GB300 deployment maintains competitive edge

- 🎯 European expansion ($2.2B across Norway, Sweden, Spain) diversifies geography

But constrained by:

- ⚠️ Continued capital raises needed for $26-30B 2026 CapEx = shareholder dilution

- 💸 Debt service coverage remains challenged at 4% margins

- 🏗️ Execution risks on 41-data-center portfolio coordination

- 📊 Analyst consensus $127.84 target seems disconnected from technical reality

Price targets: Gamma resistance at $70-75 caps upside, gamma support at $60-65 provides floor

🚀 Bull Case: $90-120 (Unlikely Rally)

Probability: 25-30%

Thesis: Customer diversification succeeds, profitability timeline accelerates, hyperscale validation drives multiple expansion. Stock recovers toward consensus analyst targets but remains capped by the $165 short call in the risk reversal.

Catalysts supporting bull case:

- 🚀 Meta and OpenAI ramps ahead of schedule, reducing Microsoft to <40% of revenue by Q4 2026

- 💰 Path to positive cash flow demonstrated with margin expansion and controlled CapEx

- 🏆 GB300 competitive advantage drives premium pricing and customer wins

- 🤝 New tier-1 customer announcements (Runway AI partnership as template)

- 📈 AI cloud market projections ($589B by 2032 at 28.5% CAGR) materialize faster than expected

- ✅ Data center construction delays resolved, capacity comes online on schedule

Resistance levels:

- $75-80: Heavy gamma resistance (8.38B + 9.05B)

- $90-100: Psychological resistance and volume profile

- $107.80: Convertible debt conversion price acts as ceiling

- $120-130: Analyst consensus range

- $165: SHORT CALL STRIKE - max pain for risk reversal trader

Reality check: For CRWV to reach $165 (137% above current $69.55), it would need to:

- Achieve sustained profitability with >10% GAAP margins

- Reduce debt load by 50%+

- Prove customer diversification eliminates concentration risk

- Deliver on $55B backlog without execution hiccups

- Maintain technology lead as hyperscalers scale GPU capacity

The risk reversal trader selling the $165 call is saying: "Even in a bull scenario, CRWV doesn't more than double from here in 13 months."

💡 Trading Ideas

🛡️ Conservative: Cash-Secured Put Selling

Strategy: Sell Jan 2026 $55 puts, collect premium while waiting for better entry

The setup:

- Sell 1x Jan 16, 2026 $55 PUT @ ~$4.50 premium

- Collateral required: $5,500 cash per contract

- Breakeven: $50.50 (27% below current $69.55)

- Max profit: $450 premium (8.2% return on $5,500 collateral in 31 days)

Why this works:

- ✅ Get paid to wait at $55 support level (19.6% below current)

- ✅ $55 strike has 1.85B gamma support - meaningful floor

- ✅ If assigned, cost basis $50.50 is near analyst bear case ($36-45 range)

- ✅ Premium collection softens downside risk

- ✅ Aligned with risk reversal thesis that CRWV could test $55 level

Risk management:

- Max loss if CRWV goes to zero: $5,050 per contract

- Set stop loss if stock breaks $60 decisively (next support level)

- Consider rolling down and out if stock approaches $55 in mid-December

Best for: Investors who want CRWV exposure but only at deeply discounted prices 20%+ below current

⚖️ Balanced: Bear Put Spread

Strategy: Buy near-money put, sell lower put = defined risk bearish play

The setup:

- Buy 1x Jan 16, 2026 $67.50 PUT @ $6.50

- Sell 1x Jan 16, 2026 $60 PUT @ $3.80

- Net debit: $2.70 per spread

- Max profit: $4.30 ($750 - $270 = $480, or 178% return)

- Breakeven: $64.80 (6.8% below current $69.55)

- Max loss: $270 premium paid

Why this works:

- ✅ Defined risk - can't lose more than $270 per spread

- ✅ Mimics the risk reversal bearish thesis without short call risk

- ✅ Breakeven at $64.80 is just below weak $65 support (6.46B gamma)

- ✅ Max profit zone $60-$45 aligns with gamma support levels

- ✅ 178% return if CRWV breaks $60 by January

- ✅ 31-day timeframe captures Christmas/New Year volatility and Q4 prelim data

Risk management:

- Max loss: $270 per spread (59% of potential profit)

- Exit at 50% profit ($135) if stock quickly drops to $62

- Add to position if CRWV rallies to $72-75 resistance

- Can roll to February expiration if thesis needs more time

Best for: Traders who believe in the bearish thesis but want to risk less than $900K! Offers 2:1 reward-risk ratio with defined downside.

🚀 Aggressive: Replicate the Risk Reversal (Smaller Size!)

Strategy: Copy the whale trade but scale it to retail size

The setup:

- Buy 2x Jan 15, 2027 $45 PUT @ $9.52 = $1,904 debit

- Sell 2x Jan 15, 2027 $165 CALL @ $7.87 = $1,574 credit

- Net debit: $330 total for the combo

- Max profit: $4,010 if CRWV below $45 (1,115% return!)

- Breakeven: ~$67 (similar to institutional trade at $66.55)

- Max loss: UNLIMITED above $165 (naked short calls!)

Why this works (and why it's risky):

- ✅ Exact same structure as $8.7M institutional trade

- ✅ 13-month timeframe captures all 2026 catalysts

- ✅ Breakeven only 3.6% below current price

- ✅ 11:1 return if CRWV drops to $45 or below

- ✅ Cheap cost basis - only $330 total risk IF stock stays below $165

But watch out:

- ❌ NAKED SHORT CALLS = unlimited loss if CRWV rockets above $165

- ❌ If CRWV rallies to $200, you lose $7,000 per combo (minus the $330 credit)

- ❌ No upside participation if AI narrative reverses

- ❌ Requires Level 3 options approval (short uncovered options)

- ❌ Margin requirements could be $30,000+ depending on broker

Risk management (CRITICAL!):

- Set mental stop at $85-90 to buy back short calls if bearish thesis breaks

- Consider buying back $165 calls for 50% profit if CRWV drops to $55-60

- Never let short calls go into earnings unhedged

- Be prepared to roll short calls higher if stock sustains above $85

Best for: Experienced options traders with Level 3 approval who fully understand naked call risk and believe CRWV is heading significantly lower over next 13 months. NOT for beginners!

Alternative (safer): Replace naked calls with a put debit spread ($65/$55 puts) to eliminate unlimited risk.

⚠️ Risk Factors

Let's be brutally honest about what could go WRONG with this bearish thesis:

💥 Balance Sheet Time Bomb

- $14.03B total debt generating $311M quarterly interest expense

- GAAP operating margins only 4% - can't cover debt service from operations

- D.A. Davidson calls it "one of the ugliest balance sheets in technology sector"

- Despite 62% adjusted EBITDA margin, actual cash generation is negative

- $2.587B new convertible debt adds to leverage pile

- If growth slows or margins compress, debt spiral could force distressed financing

What this means: The risk reversal could be betting on a balance sheet crisis forcing CRWV toward $45 or lower if they can't service debt obligations. This is a REAL risk.

🎯 Customer Concentration - Existential Dependency

- 62% of 2024 revenue from Microsoft alone (down from 77% including #2 customer)

- Microsoft chose NOT to exercise $12B option for additional capacity in March 2025

- Market interpreted this as signal of slowing AI computing demand

- What if Microsoft reduces existing commitments or doesn't renew in 2026?

- Meta ($14.2B) and OpenAI ($22.4B) contracts won't fully ramp until 2026-2027

- Single customer loss could crater revenue by 50%+

Counter-risk: If Microsoft actually INCREASES commitments or Meta ramps ahead of schedule, the bearish thesis breaks and CRWV could rally sharply. The risk reversal would lose money between $67-$165.

🏗️ Execution Nightmare - 41 Data Centers to Coordinate

- Data center construction delays already cut Q4 2025 guidance by $100-200M

- Third-party developer dependencies create supply chain vulnerability

- CEO acknowledged "unprecedented pressure across supply chains"

- $26-30B CapEx planned for 2026 - can they execute without delays?

- Failed Core Scientific acquisition showed challenges securing power capacity

- Operating 33 data centers, scaling to 41+ in 2026 = coordination complexity explodes

Counter-risk: If CoreWeave OVER-DELIVERS on data center deployments and brings capacity online ahead of schedule, revenue could significantly exceed guidance. This would invalidate the bearish thesis.

💸 Dilution Death Spiral - Constant Capital Raises

- $2.587B convertible debt in December at $107.80 conversion (55% above current)

- Stock fell 7% on convertible announcement - market exhausted with capital raises

- $26-30B 2026 CapEx will require more debt or equity financing

- Each capital raise dilutes existing shareholders and pressures stock

- Negative cash flow despite revenue growth means continuous funding needs

- If capital markets freeze or risk appetite declines, funding could dry up

Counter-risk: If CoreWeave achieves positive cash flow sooner than expected or CapEx needs prove lower than guided, they could avoid dilution and stock could re-rate higher.

🏦 Hyperscaler Competition - The 800lb Gorillas

- AWS, Azure, Google Cloud aggressively building massive GPU capacity

- Microsoft Azure's direct relationship with OpenAI (46% ownership) creates strategic conflict

- Hyperscalers have 10x+ larger balance sheets and can sustain losses longer

- Oracle reported 70% cloud infrastructure growth fueled by AI demand

- Customers building custom AI accelerators (Google TPU, AWS Trainium) reduce addressable market

- As GPU supply increases industry-wide, pricing power may erode

The brutal question: Why would customers pay CoreWeave when they can use AWS/Azure/GCP with broader service portfolios, better integration, and enterprise relationships?

Counter-risk: CoreWeave's specialized focus and first-to-market GB300 deployments could maintain premium positioning. Purpose-built AI infrastructure may outperform retrofitted hyperscaler data centers.

🎭 AI Bubble Concerns - Hype Cycle Peak?

- Microsoft's decision not to exercise $12B option raises demand durability questions

- What if AI investment slows because returns on AI deployments disappoint?

- Current valuations assume sustained hypergrowth - any demand normalization could be catastrophic

- CRWV down 61% from peak already reflects SOME bubble concerns

- If broader AI infrastructure spending contracts in 2026, CRWV has nowhere to hide

Counter-risk: AI adoption could actually ACCELERATE as models improve and use cases expand. The $589B by 2032 market projection at 28.5% CAGR might prove CONSERVATIVE.

👔 Insider Selling Red Flag

- CEO sold $6.3M in December, CFO sold $5.49M

- $12M+ combined sales by top two executives in December alone

- While some attributed to tax obligations and 10b5-1 plans, optics are terrible

- If insiders don't believe in $165+ upside, why should we?

- CEO said company is "misunderstood" - but selling $6M doesn't help that narrative

Counter-risk: Insider sales could be purely for diversification/liquidity after lockup expiration. CEO still retains over 5.9M shares, showing continued alignment.

📉 Technical Breakdown - Momentum Crushed

- Down 61% from $187 June peak

- Stock fell 20% in ONE WEEK (Dec 9-15 from $90.66 to $72.35)

- Series of lower highs establishes confirmed downtrend

- Trading below most institutional cost bases from summer 2025

- Bearish gamma profile (-27B net GEX) amplifies downside moves

- No clear support until $60 (12.3% below current)

Counter-risk: Extreme oversold conditions could trigger violent short squeeze if ANY positive catalyst emerges. 61% decline has likely shaken out weak hands.

⚠️ What Could Make Me WRONG on the Bearish Thesis?

Bull case scenarios that would hurt the risk reversal:

- Profitability Breakthrough: CRWV announces path to positive cash flow in 2026 with 15%+ GAAP margins

- Microsoft Renewal: Surprise announcement that MSFT exercises expansion options or extends contracts

- Strategic Acquisition: Tech giant (Amazon, Google, Oracle) acquires CRWV at premium valuation

- Customer Wins: Multiple new tier-1 customer announcements diversifying revenue beyond MSFT/Meta/OpenAI

- Margin Expansion: GPU pricing power sustains as supply remains constrained, driving 25%+ GAAP margins

- Debt Refinancing: Successful refinancing at lower rates reducing interest burden by 50%+

If ANY of these scenarios materialize, CRWV could easily rally to $90-120 range, causing the risk reversal to lose money. The $165 short call caps upside but doesn't eliminate losses between breakeven $67 and the call strike.

🎯 The Bottom Line

Real talk: This $8.7M risk reversal is one of the most SOPHISTICATED bearish bets we've seen all year. An institutional trader just paid $900K to position for significant downside in CoreWeave over the next 13 months while capping their upside participation at $165 - essentially saying "I think this goes lower, and even if it goes higher, it's not reaching $165."

Here's the deal:

If you OWN CRWV:

- 🚨 This trade is a WARNING SIGN from smart money

- 📊 Mark your calendar for Feb 18 earnings - that's the next make-or-break event

- 🛡️ Consider protective puts at $65 or $60 to hedge through Q4 results

- ⚖️ Reassess your position if stock breaks $60 decisively (major gamma support level)

- 💎 Diamond hands if you believe in the $55B backlog and customer diversification story

If you're WATCHING CRWV:

- 👀 Wait for confirmation of trend reversal before buying - no rush to catch falling knives

- 🎯 Better entry points: $60 (major gamma support), $55 (deeper value), or $45 (extreme value matching risk reversal put strike)

- 📈 Bull case needs PROOF of customer diversification and path to profitability

- ⏰ Best opportunities after Feb 18 earnings or if any Meta/OpenAI deployment issues emerge

- 💡 Consider selling cash-secured puts at $55 to get paid while waiting for better entry

If you're BEARISH like the risk reversal trader:

- 🐻 The technical setup confirms your thesis - weak support, strong overhead resistance

- 📉 Key level to break: $67.50 (immediate support), then $65, then the critical $60 floor

- ⚠️ Bear put spreads offer similar exposure with DEFINED risk (way better than naked calls!)

- 🎯 Price targets: $60 → $55 → $45 progression if support levels break

- 🛡️ Risk management: Set stops if stock reclaims $75 or if Feb 18 earnings are VERY bullish

Key dates to watch:

- 📅 December 19 - Triple Witch expiration (implied move ±6.4% this week!)

- 📅 February 18, 2026 - Q4 2025 earnings (THE catalyst for next major move)

- 📅 Mid-2026 - Meta contract ramp begins, OpenAI MI450 deployment scheduled

- 📅 January 15, 2027 - Risk reversal expiration (13 months of catalysts and execution risk)

The verdict:

This risk reversal tells us someone with $8.7M to deploy believes CoreWeave's troubles are FAR from over. The choice of $45 downside protection (35% below current) paired with $165 upside cap (137% above current) creates a massively asymmetric bet on further weakness.

Between the $14B debt load that can't be serviced at 4% margins, 62% Microsoft customer concentration, data center construction delays, $26-30B 2026 CapEx needs, and CEO/CFO insider selling $12M+ in December - there's a LOT of smoke here.

But remember: CRWV also has $55B in backlog, $14.2B Meta contract, $22.4B OpenAI commitments, and first-to-market NVIDIA GB300 advantage. If they execute flawlessly through 2026, this bearish bet could be dead wrong.

Most importantly: Options are risky! The risk reversal structure involves NAKED SHORT CALLS which carry unlimited loss potential if CRWV rockets above $165. Don't blindly copy whale trades without understanding the risks and having the capital to manage them. Trade smart, stay safe, and never risk more than you can afford to lose! 💪

Disclaimer: This analysis is for educational and informational purposes only and should not be considered financial advice. Options trading involves substantial risk and is not suitable for all investors. The risk of loss in trading options can be substantial and may result in the loss of your entire investment. Past performance is not indicative of future results. Always conduct your own research and consider consulting with a qualified financial advisor before making investment decisions. The unusual options activity described may represent hedging, speculation, or other strategies that cannot be determined with certainty.

The risk reversal strategy discussed involves selling uncovered call options, which carry unlimited loss potential if the underlying stock rises significantly. This strategy is suitable only for experienced investors with substantial capital and risk tolerance. All strike prices, premiums, and dates are based on market data as of December 16, 2025, and are subject to change.