🐻 CRWV: $4.9M Bearish Bet Braces for AI Infrastructure Meltdown!

📅 December 19, 2025 | 🔥 Extremely Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $4.9 million on deep out-of-the-money CRWV puts with a 552x unusualness score - positioning for a catastrophic 32% crash from $81.64 to $55 by May 2026. This isn't a hedge, it's a declaration: a sophisticated trader thinks CoreWeave's AI infrastructure house of cards is about to collapse under $14+ billion in debt and execution risks. With the stock already down 65% from its $187 peak and the May 2026 implied move pricing exactly this downside range, someone knows something the market hasn't fully priced in yet.

💰 The Option Flow Breakdown

📊 What Just Happened

| Time | Symbol | Side | Type | Expiration | Strike | Premium | Volume | Z-Score | Option Chart |

|---|---|---|---|---|---|---|---|---|---|

| 11:14:23 | CRWV | 🔴 BUY | PUT | 2026-05-15 | $55 | $4.9M | 7,100 | 552.32 | View Chart |

📈 Volume/OI Ratio: 70.3 (HIGH_ACTIVITY - 70x more volume than existing open interest)

⏰ Time to Expiration: 147 days (nearly 5 months to thesis)

💸 Strategy: Long Put (STANDALONE) - Pure directional bearish bet, no spread or hedge

🎯 Signal: OPEN - Initiating new bearish position

🤓 What This Actually Means

Real talk: Someone paid $4.9 million for the right to sell 710,000 shares of CRWV at $55 when it's trading at $81.64 - that's a 32% drop they're betting on. The volume/OI ratio of 70.3 means today's volume is 70 times higher than the total existing positions at this strike, signaling fresh conviction, not closing out old positions.

The 552x unusualness score puts this in rarified air - we're talking a few-times-a-year type event for a stock that only IPO'd in March 2025 at $40. This trader structured it as a standalone long put instead of a put spread, meaning they're willing to pay full premium for unlimited downside exposure rather than capping profits to reduce cost. That's aggressive.

Translation for us regular folks: Big money thinks CoreWeave is heading to $55 or lower within the next 5 months, and they're betting nearly $5 million on it. They're not hedging - they're hunting.

🏢 Company Overview: CoreWeave

What They Do: CoreWeave (NASDAQ: CRWV) is a modern cloud infrastructure technology company offering the CoreWeave Cloud Platform - proprietary software and cloud services designed to manage AI infrastructure at scale. Think of them as the pickaxe seller in the AI gold rush, providing the raw computing horsepower (NVIDIA GPUs) that companies like OpenAI and Meta need to train AI models.

The Numbers:

- Market Cap: $33.7 billion

- Industry: SERVICES-PREPACKAGED SOFTWARE

- Current Price: $81.64 (down 65% from $187 peak in June 2025)

- IPO: March 28, 2025 at $40/share (+104% from IPO, -56% from all-time high)

- Q3 Revenue: $1.36 billion (+134% YoY)

- Revenue Backlog: $55.6 billion (nearly doubled in Q3)

The CoreWeave Story: CoreWeave is NVIDIA's preferred cloud partner (NVIDIA owns 5.1% of the company) and offers 80% lower pricing than AWS/Azure for AI workloads. They've signed massive deals: $14.2B with Meta, $22.4B with OpenAI, providing access to cutting-edge GB200/GB300 GPU clusters. They completed the $1.7B acquisition of Weights & Biases in May 2025, creating an end-to-end AI platform.

The Plot Twist: But here's where it gets dicey. CoreWeave carries $14+ billion in debt with a debt-to-equity ratio of 4.85 and an interest coverage ratio of just 0.16 - meaning they're struggling to cover interest expenses. Q3 interest expenses were $310.6 million, dwarfing operating income. Their Altman Z-Score of 0.79 puts them in the "distress zone," and credit default swap spreads have exploded from 250-300 bps to 600-700 bps in recent weeks.

Add in data center construction delays that forced them to cut 2025 revenue guidance to $5.05-5.15B (below $5.29B consensus), a failed $9 billion Core Scientific merger, and Microsoft representing 67-71% of revenue - and you start to see why someone would make this bearish bet.

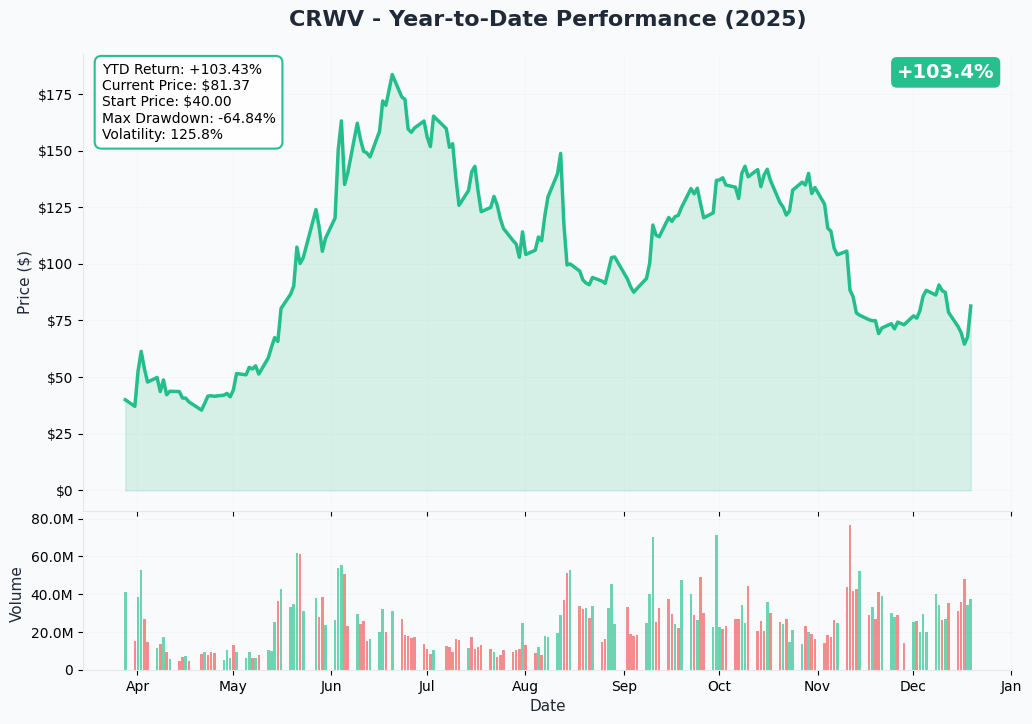

📈 Technical Setup / Chart Check-Up

Year-to-Date Performance

CoreWeave's chart tells a story of euphoria, disappointment, and renewed uncertainty. The stock exploded from its $40 IPO price to $187 by June 2025 (+368% in 3 months) as AI infrastructure mania hit peak frenzy. Then reality set in: the stock has collapsed 65% from that peak to today's $81.64, giving back more than half its gains.

Key technical observations:

- Volatility: Massive 120-point range ($67 low to $187 high) in just 9 months since IPO

- Trend: Clearly in a downtrend since June peak, lower highs and lower lows

- Recent Action: Stock down 27% in the week ending December 18 on AI infrastructure bubble concerns following Oracle's earnings

- Support Test: Currently trading just above the March-April consolidation zone around $70-80

The chart pattern suggests exhaustion after the post-IPO hype cycle. Bears are clearly in control, and this massive put position is betting the breakdown continues.

Gamma-Based Support & Resistance Analysis

Current Price: $81.64

Gamma-Based Levels:

🔵 Support at $80 (Net GEX: 7.27B) - Very Strong

- This is the critical line in the sand right now

- Massive put gamma accumulation creates a magnet effect

- Market makers hedging these puts will need to buy stock as price approaches $80

- Break below $80 could trigger accelerated selling as delta hedges get adjusted

🟠 Resistance at $85 (Net GEX: 5.09B) - Very Strong

- Call gamma wall just above current price creates a ceiling

- Market makers are net short calls here, will sell stock into rallies

- Need significant buying pressure to break through

What This Means: CRWV is currently trapped in a tight $80-$85 gamma sandwich. The stock is pinned between these levels as options market makers manage their hedges. For bulls to regain control, we need a decisive break above $85 with volume. For bears, a breakdown below $80 opens the door to much lower levels with limited gamma support until the $60s.

The massive $4.9M put position at $55 sits well below the current gamma structure, suggesting the trader expects a complete gamma collapse - meaning they think we'll blow through all technical levels on the way down.

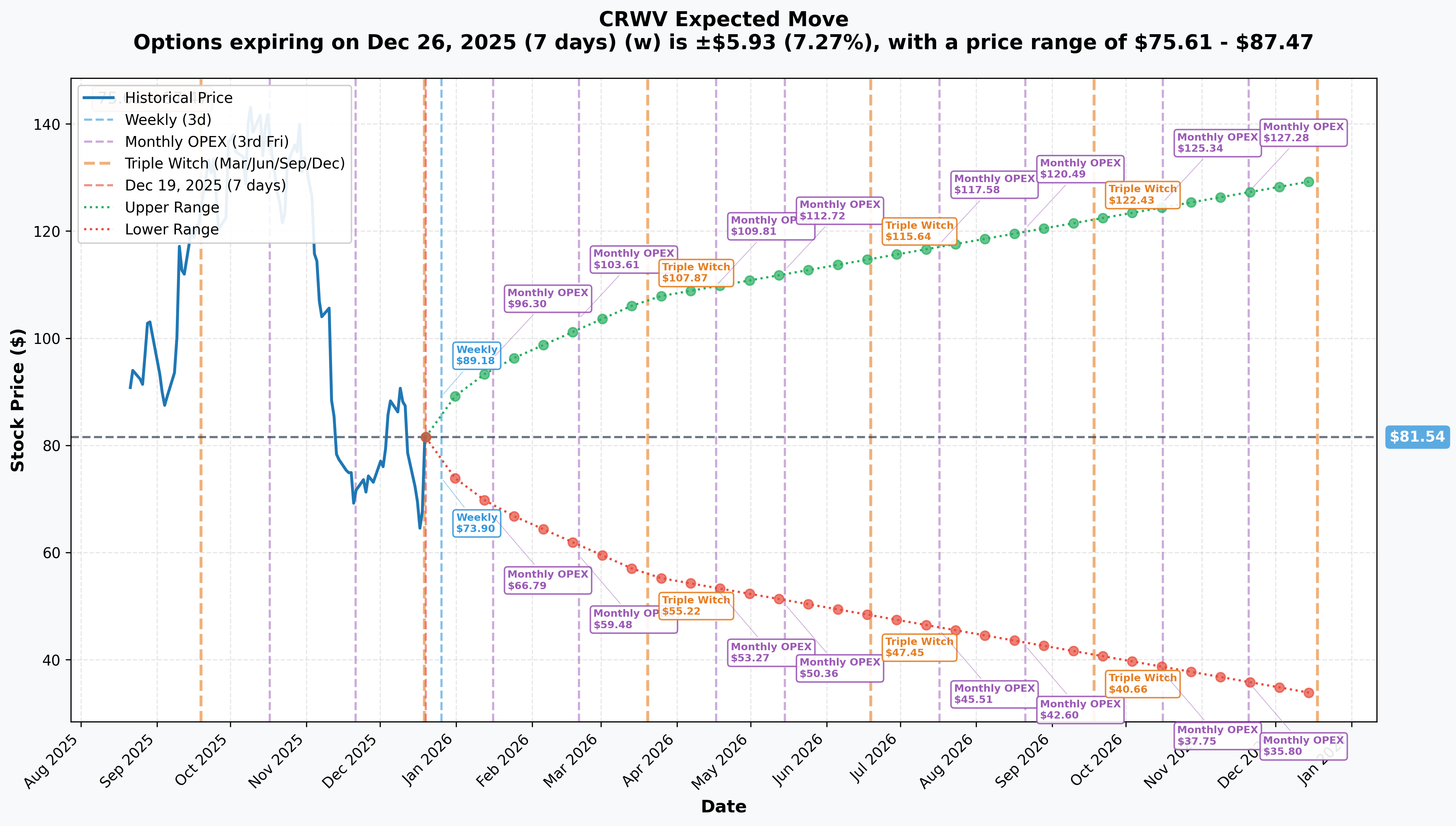

Implied Move-Based Price Ranges

The options market is pricing in serious volatility ahead. Here's what the implied moves tell us:

📊 Weekly (Dec 26): ±7.27% ($75.61 - $87.47)

- Market expects $81.64 +/- $5.93 move by next week

- That's a $12 range - wild for a $34B market cap company

- Reflects continued post-earnings/news uncertainty

📊 Monthly OPEX (Jan 16): ±16.11% ($68.41 - $94.67)

- $26 range in 28 days - that's $930M/day in market cap swings

- Lower bound at $68.41 would be -16% from here

- This is where first major test of conviction happens

📊 Quarterly Triple Witch (March 20): ±31.79% ($55.62 - $107.47)

- Plot twist: The lower bound of $55.62 is almost exactly the $55 strike!

- Market is literally pricing the possibility of the put bet paying off

- Upper bound at $107 would require complete reversal of current trend

📊 May 15 OPEX (This Trade's Expiration): $50.36 - $112.72

- Lower range: $50.36 - even below the $55 strike

- The options market is saying there's a real probability this put finishes in-the-money

- That's not a tail risk - that's a legitimate scenario being priced

Critical Insight: The May 2026 implied move has a lower bound of $50.36, which means the market is already pricing a realistic path to the $55 strike. This isn't some crazy lottery ticket - it's a bet that aligns with what volatility is telling us.

🎪 Catalysts

🔥 Recent Events (Already Happened)

Q3 2025 Earnings - November 10, 2025 CoreWeave reported strong Q3 results with $1.36B revenue (+134% YoY) and $217M adjusted operating income. However, they cut full-year 2025 revenue guidance to $5.05-5.15B from $5.29B consensus due to data center delays in Texas. Stock dropped 16% the next day despite beating estimates. Backlog nearly doubled to $55.6B, but execution concerns overshadowed growth.

Failed Core Scientific Merger - October 30, 2025 Core Scientific shareholders voted down CoreWeave's $9B all-stock acquisition, marking the second failed attempt. Major shareholder Two Seas Capital argued Core Scientific could trade at twice the merger value. This strategic setback highlighted valuation concerns and integration risks.

Weights & Biases Acquisition Completed - May 5, 2025 CoreWeave completed the $1.7B acquisition of the leading MLOps platform, creating an end-to-end AI platform. This was a major strategic win, but added to the already massive debt load.

Genesis Mission Partnership - December 18, 2025 CoreWeave joined the DOE's Genesis Mission, bringing its AI cloud platform to government scientific workloads. Stock surged 9.8% on the announcement. Citigroup initiated coverage with Buy rating and $135 target same day. However, the rally faded quickly, suggesting skepticism about near-term revenue impact.

$2.25 Billion Convertible Notes Offering - December 2025 CoreWeave priced $2.25B in convertible notes at 1.75% due 2031, with $107.80 conversion price (59% premium). While this provided capital for expansion, it added to the $14+ billion debt burden and raised concerns about financing costs and potential dilution.

📅 Upcoming Catalysts (Next 5 Months)

Q4 2025 Earnings - February 18, 2026 (After Market Close) ⭐⭐⭐⭐⭐ This is the most critical catalyst for the May put position. Consensus expects $1.3-1.4B revenue to meet full-year $5.05-5.15B guidance. Key metrics to watch:

- Data center delivery progress: Did the Texas/Oklahoma/North Carolina delays get resolved in Q1 as CEO promised?

- Customer concentration: Is Microsoft still 67-71% of revenue or has diversification started?

- 2026 revenue guidance: Consensus expects $11.6B (+127% YoY), but bears are looking for $8-10B range

- Profitability path: Can they show sustainable path to GAAP profitability amid massive interest expenses?

A miss here or cautious guidance could trigger the breakdown to $55 this trade is betting on.

Data Center Capacity Deliveries - Q1 2026 ⭐⭐⭐⭐ Multiple third-party developer projects coming online including the delayed 260MW Denton, Texas facility for OpenAI. CEO stated "overwhelming majority of delay should be taken care of within Q1" - execution on this timeline is make-or-break for the bull case. Any further delays would validate bearish thesis.

2026 CapEx Ramp - Ongoing ⭐⭐⭐ CFO guided to $24-28+ billion in 2026 CapEx (vs. $12-14B in 2025). With $14+ billion existing debt and rising rates, funding this expansion could require additional dilutive financing or force slower growth. Credit markets are already spooked - CDS spreads at 600-700 bps.

Hyperscaler Competition Intensifies - Q1 2026 ⭐⭐⭐ AWS, Azure, and Google Cloud continue rolling out custom AI chips and purpose-built infrastructure to compete with GPU-centric providers like CoreWeave. Any major announcements from hyperscalers could pressure pricing and margins.

Potential Credit Rating Action - Q1-Q2 2026 ⭐⭐⭐ With Fitch at BB- and S&P at B (both below investment grade), and deteriorating credit metrics, any downgrade could spike borrowing costs and trigger covenant concerns.

🎲 Price Targets & Probabilities

📊 The Three Scenarios

🐻 Bear Case: $45-55 (May 2026) - 35% Probability

Path to $55:

- Q4 earnings miss with weak 2026 guidance ($8-10B revenue vs. $11.6B consensus)

- Data center delays extend into Q2, forcing another guidance cut

- Microsoft reduces commitment or renegotiates pricing (they're 67-71% of revenue)

- Credit rating downgrade forces refinancing at higher rates

- Broader AI infrastructure sector correction accelerates (Oracle concerns spread)

- Technical breakdown below $80 gamma support triggers cascade to $60s, then $55

What Needs to Happen: This scenario requires a fundamental re-rating of the AI infrastructure opportunity or CoreWeave-specific execution failure. The $55 strike sits right at the May implied move lower bound ($50.36), so it's already being priced as a realistic outcome. With debt-to-equity at 4.85x and Altman Z-score in distress territory, a liquidity crisis or forced equity raise at depressed prices could crater the stock.

The massive put buyer is clearly betting on this scenario - and with 147 days to expiration, they have plenty of time for the thesis to play out.

⚖️ Base Case: $70-85 Range (May 2026) - 45% Probability

Sideways Grinding:

- Q4 meets lowered expectations, 2026 guidance comes in-line around $10-11B

- Data centers come online in Q1 but with minimal fanfare

- Customer concentration slowly improves but Microsoft remains 50%+ of revenue

- Stock remains trapped between $80 gamma support and $85 resistance

- Debt concerns persist but no imminent crisis

- Multiple compression continues as AI infrastructure hype cools

What This Looks Like: CoreWeave muddles through, neither collapsing nor breaking out. The stock trades in a choppy range as bulls and bears battle over whether the growth story justifies the leverage. In this scenario, the $55 puts expire worthless but the stock doesn't exactly thrive either. Volatility remains elevated but directional conviction is low.

🚀 Bull Case: $95-110 (May 2026) - 20% Probability

Back from the Brink:

- Q4 blowout earnings, 2026 guidance raises to $12-13B

- Data centers deliver ahead of schedule, major new customer contracts announced

- Customer diversification accelerates (Microsoft drops below 50% of revenue)

- Successful refinancing of debt at lower rates

- NVIDIA Blackwell ramp drives margin expansion

- Genesis Mission converts to material government revenue

- Hyperscaler AI chip initiatives stumble, validating GPU-centric approach

- Technical breakout above $85 gamma resistance opens path to $95-110

What Needs to Happen: This requires near-perfect execution plus sector tailwinds. The May implied move upper bound is $112.72, so there's volatility pricing for this scenario. However, with 10% short interest, any sustained rally could trigger a squeeze. Analyst consensus price target of $127 suggests significant upside if fundamentals cooperate.

But here's the problem: this scenario requires the company to defy gravity on multiple fronts simultaneously while carrying massive debt. Possible? Yes. Probable given current setup? That's why it's only 20% odds.

🎯 Put Position Analysis

Breakeven: $48.10 ($55 strike - $6.90 premium paid)

- Stock needs to drop 41% from current $81.64 for breakeven

- That would be a $33.5 billion market cap destruction

Max Profit: Unlimited below $48.10 (but realistically capped at zero since stocks don't go negative)

- At $40 (IPO price): $15 profit per share = $10.7M total (+118% return)

- At $48.10 (breakeven): $6.90 profit per share = $4.9M total (+100% return)

- At $55 (strike): $0.10 profit per share = $71K total (+1.4% return)

Max Loss: $4.9M if stock above $55 at expiration (-100%)

Risk/Reward: At current $81.64 price, this put is trading for $6.90 with $26.64 of distance to strike ($81.64 - $55.00). The implied volatility is pricing about 35% chance of stock being below $55 at May expiration based on the lower bound of implied move. That's not crazy - it's what the market is telling us.

Time Decay: With 147 days to expiration, theta decay is relatively slow for the first 90 days. But the last 60 days (March-May) will see accelerating decay. The trader needs meaningful downside movement by Q4 earnings (Feb 18) to avoid the theta crush zone.

💡 Trading Ideas

🛡️ Conservative: Sell Call Spreads into Strength

Setup: If CRWV rallies to $85-90 on any positive news, sell the $90/$95 call spread expiring March 2026

- Collect $2.00-2.50 premium

- Max loss: $5.00 - $2.50 = $2.50

- Return on risk: 100% if stock stays below $90

Why This Works: The gamma resistance at $85 and bearish sentiment make rallies a selling opportunity. With customer concentration, debt concerns, and execution risks, any bounce to $90+ faces strong headwinds. You're betting the stock can't sustain above $90 by March - which aligns with the broader bearish setup without requiring a catastrophic decline.

Risk: Bull case plays out, stock squeezes to $100+ on major positive catalyst. Your loss is capped at $2.50 per spread, so 10 contracts = $2,500 max risk.

⚖️ Balanced: March 2026 $75/$70 Put Spread

Setup: Buy the March 20, 2026 $75 put, sell the $70 put

- Cost: ~$2.50-3.00 debit

- Max profit: $5.00 - $3.00 = $2.00 (67% return)

- Breakeven: $72.00

Why This Works: You're playing for the base-to-bearish case without betting the farm on a crash to $55. The March triple witch implied move has a lower bound of $55.62, so a move to $70-75 by March is well within expected range. This gives you defined risk ($3.00 max loss) while positioning for the breakdown below $80 gamma support.

If Q4 earnings disappoint in mid-February, this spread could be worth $4-5 by March expiration. You're risking $3 to make $2 - not sexy, but aligned with the unusual activity without the extreme tail risk.

Risk: Stock holds $80 support, consolidates, or rallies. You lose the $3.00 premium. But compared to the standalone $55 put which needs a 32% crash, you only need a 8-13% decline.

🚀 Aggressive: Replicate the Whale - Buy May 2026 $60 or $65 Puts

Setup: Buy May 15, 2026 $60 or $65 puts (closer to current price than $55)

- $65 puts: ~$8-9 cost, breakeven around $56-57

- $60 puts: ~$6-7 cost, breakeven around $53-54

- You need 23-27% decline vs. 32% for the $55 strike

Why This Works: You're following the smart money's bearish thesis but giving yourself better odds with strikes closer to the May implied move lower bound. The $65 strike sits right in the middle of the $50.36-$68.41 range that the January implied move is pricing. You get 147 days for the thesis to play out - Q4 earnings, Q1 data center deliveries, potential credit issues, sector rotation away from AI infrastructure.

If the bear case accelerates, these puts could double or triple. The $65 put at $9 would be worth $19+ if stock hits $55 by May (111% return).

Risk: This is a pure directional bet requiring significant downside. If CoreWeave stabilizes at $75-80, you're staring at 60-80% losses as time decay accelerates in final 60 days. Only allocate capital you can afford to lose entirely.

Position Sizing:

- Conservative: 5-10 contracts ($4,500-9,000) for $80K-100K portfolio

- Balanced: 15-20 contracts ($12,000-16,000) for $100K-150K portfolio

- Aggressive: 25-30 contracts ($20,000-27,000) for $200K+ portfolio

⚠️ Risk Factors

What Could Make This Put Position Worthless

🎯 Execution Excellence: If CoreWeave delivers flawless Q4 earnings with strong 2026 guidance, gets all delayed data centers online in Q1, and announces major new customer wins (reducing Microsoft concentration below 50%), the stock could re-rate higher. The Genesis Mission partnership could convert to material government revenue faster than expected. Stock back to $95-100+ makes the $55 put a wipeout.

💰 Debt Refinancing Success: If CoreWeave successfully refinances its $14+ billion debt at lower rates or secures strategic equity investment from NVIDIA/Microsoft/Meta, the solvency concerns evaporate. Credit spreads tightening from 600-700 bps back to 250-300 bps would signal major de-risking.

🚀 AI Infrastructure Boom 2.0: If the AI infrastructure arms race accelerates (new frontier models, enterprise AI adoption, government AI initiatives), demand for GPU compute could exceed even bullish expectations. CoreWeave's $55.6B backlog could prove conservative, and hyperscaler custom chip initiatives could fail to compete with NVIDIA GPUs.

📊 Technical Support Holds: If the $80 gamma support proves impenetrable and stock consolidates in a $78-85 range through May, theta decay will destroy the put value even if the stock doesn't rally. Need directional movement, not sideways grinding.

🎪 Surprise M&A: If CoreWeave becomes a takeout target - perhaps NVIDIA or a hyperscaler decides to acquire them - any deal above $90/share would make puts worthless. With $14B debt, financing such a deal is complex, but not impossible if strategic value is high enough.

What Makes This Bearish Bet MORE Likely to Pay Off

💣 Q4 Earnings Miss: Revenue guidance already cut once. Another disappointment in February would shatter credibility. If 2026 guidance comes in at $8-10B vs. $11.6B consensus, stock could gap down 20-30% overnight, putting the $55 strike in play immediately.

🏗️ Data Center Delays Continue: CEO promised Q1 resolution, but third-party developers have already missed multiple deadlines. Weather, permitting, design revisions - these are real-world construction risks. Another delay announcement would validate bear case.

💸 Debt Crisis: With interest coverage ratio of 0.16 and $310M quarterly interest expense, CoreWeave is one bad quarter away from liquidity concerns. If 2026 CapEx requirements ($24-28B) clash with tighter credit markets, forced equity dilution at depressed prices could spiral the stock lower.

🔥 Microsoft Concentration Blows Up: 67-71% of revenue from one customer is Russian roulette. If Microsoft builds out internal GPU capacity, renegotiates pricing, or reduces commitment, CoreWeave's revenue model collapses. The $14.2B Meta deal and OpenAI expansion help, but Microsoft remains the Sword of Damocles.

📉 AI Infrastructure Sector Correction: Oracle's earnings showing negative free cash flow already sparked sector-wide concerns about overbuilding. If more AI infrastructure providers report disappointing results or major customers (OpenAI, Anthropic, etc.) slow spending, the entire neocloud thesis gets questioned. CRWV down 27% in one week shows how fast sentiment can shift.

🎰 Hyperscaler Competition Succeeds: If AWS Trainium, Azure Maia, or Google TPUs prove competitive with NVIDIA GPUs for AI workloads, CoreWeave's cost advantage and strategic positioning erode. The "NVIDIA's preferred partner" moat crumbles if customers can get equivalent performance from integrated hyperscaler offerings at lower total cost.

📊 Technical Breakdown: Break below $80 gamma support with volume opens air pocket to $60s. With 10% short interest already positioned and put/call ratios elevated, a breakdown could become self-reinforcing as stops trigger and weak hands panic.

🎯 The Bottom Line

Real talk: This is one of the most conflicted setups I've seen in 2025. On one hand, you've got a company at the epicenter of the AI boom - NVIDIA's favorite cloud partner, $55.6B backlog nearly doubling, customers like OpenAI and Meta signing multi-billion dollar deals, and analysts with $127 average price target suggesting 56% upside.

On the other hand, you've got $14+ billion in debt, a debt-to-equity ratio of 4.85x, interest coverage of 0.16x, Altman Z-Score in the distress zone, CDS spreads that have doubled to 600-700 bps, 67-71% customer concentration in Microsoft, construction delays forcing guidance cuts, and a stock that's down 65% from its peak despite the AI infrastructure narrative getting stronger.

Someone just put $4.9 million on the table betting the house of cards collapses to $55 within 5 months. The 552x unusualness score and standalone put structure (not a spread) signals serious conviction. They're not hedging existing long positions - they're hunting.

📋 Action Plan for Different Investors

If You Own CRWV Stock:

- ⚠️ Major Red Flag: This trade is a warning shot. Consider trimming exposure or hedging with March $75-80 puts

- 📅 Mark Your Calendar: Q4 earnings on February 18 is make-or-break. If they miss or guide weak, get out before the flush

- 🎯 Set Stop Loss: Below $78 breaks gamma support and opens door to cascade lower

- ✅ Why Hold: If you believe in the long-term AI infrastructure thesis and can stomach 30-40% drawdowns, $55.6B backlog and NVIDIA partnership still have legs. Just don't use leverage.

If You're Watching CRWV:

- 👀 Wait for Confirmation: Don't chase either direction here. Let Q4 earnings provide clarity

- 📊 Technical Entry: Below $78 or above $87 provides better risk/reward than current $81 no-man's land

- 🎰 High Risk Play: If you believe in the bearish thesis, consider the Balanced strategy (March $75/$70 put spread) for defined risk exposure

- ⏰ Key Dates:

- February 18: Q4 earnings

- March 20: Triple witch expiration (first gamma test)

- April-May: Data center delivery updates

If You're Bearish on CRWV:

- 🐻 Thesis Validation: The $4.9M put buyer shares your view. But you need catalysts to play out by May

- 💰 Cheaper Entry: Consider $60 or $65 puts instead of $55 for better odds while maintaining bearish exposure

- 📉 Spread It Out: March $75/$70 put spread gives you more probability of success than lottery ticket $55 strike

- ⚠️ Risk Management: Position size like this could go to zero. The May implied move says there's a path to $55, but it's not the base case

🎲 My Take

The debt burden is real, the customer concentration is scary, and the execution risks are mounting. But CoreWeave is also legitimately well-positioned in a massive growth market with tier-one customers and NVIDIA backing.

The problem is the financing structure. They're trying to fund $24-28 billion in 2026 CapEx while carrying $14+ billion in debt and burning cash on $310M quarterly interest. That's a tightrope walk, and credit markets are pricing serious distress.

This $4.9M bet isn't crazy - the May implied move lower bound is literally $50.36, almost exactly the $55 strike. The trader is betting on what volatility is already pricing as possible. That's sophisticated positioning.

For most retail traders, I'd say stay on the sidelines until Q4 earnings clarifies the picture. If you must play it:

- Bearish tilt: March $75/$70 put spread (defined risk, better probability)

- Bullish tilt: Wait for break above $87, then buy stock with tight stop at $83

- Neutral: Sell premium in the $80-85 range where gamma is highest

But whatever you do, respect the 552x unusual activity score. Someone with $4.9 million knows something or sees something most of us don't. Maybe they're wrong. But they're definitely not stupid.

Trade carefully, size appropriately, and remember: options can go to zero. 💸

⚠️ Disclaimer: Options trading involves substantial risk and is not suitable for all investors. The analysis provided is for educational purposes only and should not be construed as financial advice. Past performance does not guarantee future results. Always consult with a qualified financial advisor before making investment decisions. The author may hold positions in CRWV or related securities.

📊 Want to see the live option flow as it happens? Check out the CRWV ticker page for real-time data and the May 2026 $55 Put option chain for current pricing.