CRWV $12M Bearish Options Structure - Institutional Risk-Off on AI Infrastructure Play

January 12, 2026 | Unusual Activity Detected

The Quick Take

Institutional traders built a $12 million bearish options structure on CoreWeave today using a risk reversal strategy: buying 20,500 long-dated $40 puts ($4.7M) while selling 10,000 $150 calls ($5.7M). This positions for significant downside over the next 12 months on a stock trading at $89.88 - implying a potential 55% decline to the put strike. With CRWV carrying $18.5 billion in debt, an Altman Z-Score in distress territory (0.69), and Q4 earnings approaching February 18th, this trade signals sophisticated money is hedging against execution risk in the AI infrastructure buildout. Translation: Smart money is buying insurance against the possibility that CoreWeave's growth story hits a wall.

Company Overview

CoreWeave (CRWV) is an AI-focused cloud computing company providing GPU infrastructure to leading AI companies:

- Market Cap: $40.0 Billion

- Industry: AI Cloud Infrastructure / Data Centers

- Current Price: $89.88 (down 52% from 52-week high of $187)

- Primary Business: NVIDIA-powered cloud computing for AI training and inference, serving OpenAI, Microsoft, and Meta

- Revenue Backlog: $55.6 billion in contracted future revenue

The Option Flow Breakdown

The Tape (January 12, 2026):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:03:54 | CRWV | ASK | BUY | PUT $40 | 2027-01-15 | $2,100,000 | $40 | 11,000 | - | 11,000 | $89.88 | $1.91 |

| 11:00:16 | CRWV | ASK | BUY | PUT $40 | 2027-01-15 | $1,300,000 | $40 | 6,000 | - | 6,000 | $89.88 | $2.17 |

| 10:59:06 | CRWV | ASK | BUY | PUT $40 | 2027-01-15 | $1,300,000 | $40 | 3,500 | - | 3,500 | $89.88 | $3.71 |

| 11:03:54 | CRWV | BID | SELL | CALL $150 | 2027-01-15 | $2,500,000 | $150 | 5,000 | - | 5,000 | $89.88 | $5.00 |

| 11:00:16 | CRWV | BID | SELL | CALL $150 | 2027-01-15 | $1,600,000 | $150 | 3,000 | - | 3,000 | $89.88 | $5.33 |

| 10:59:06 | CRWV | BID | SELL | CALL $150 | 2027-01-15 | $1,600,000 | $150 | 2,000 | - | 2,000 | $89.88 | $8.00 |

Aggregated Position:

- Long Puts: 20,500 contracts @ $40 strike, ~$4.7M total premium (Long Put strategy)

- Short Calls: 10,000 contracts @ $150 strike, ~$5.7M total premium (Short Call strategy)

Option Symbols:

- Put: CRWV270117P00040000

- Call: CRWV270117C00150000

What This Actually Means

This is a risk reversal structure - a sophisticated bearish positioning strategy. Here's the breakdown:

- Long $40 Puts (20,500 contracts): Paying ~$4.7M for the right to sell CRWV at $40 through January 2027 - a 55% discount to current levels

- Short $150 Calls (10,000 contracts): Collecting ~$5.7M premium by selling upside above $150 (67% above current price)

- Net Credit: Structure generates ~$1M net premium received, making it a partially funded hedge

- Break-even Analysis: Maximum pain below $40, unlimited risk above $150

- Time Horizon: 12 months to expiration captures multiple earnings cycles, data center buildout milestones, and potential macro stress

What's really happening here:

This trader (likely a fund with existing CRWV exposure or a directional speculator) is expressing a view that CRWV has limited upside above $150 while protecting against catastrophic downside to $40. The structure makes sense for someone who believes:

- The $55B revenue backlog won't convert as efficiently as bulls expect

- The $18.5B debt burden creates refinancing/liquidity risk

- Hyperscaler competition (Microsoft expanding AI capacity 80%+) will compress margins

- The Altman Z-Score of 0.69 signals genuine bankruptcy risk within 2 years

The January 2027 expiration captures Q4 2025 earnings (Feb 18), Q1-Q3 2026 earnings, and the critical NVIDIA Rubin deployment in H2 2026.

Unusual Score: HIGH - $12M notional on a recently-IPO'd stock with concentrated customer risk and significant leverage. This is institutional-grade positioning, not retail speculation.

Technical Setup

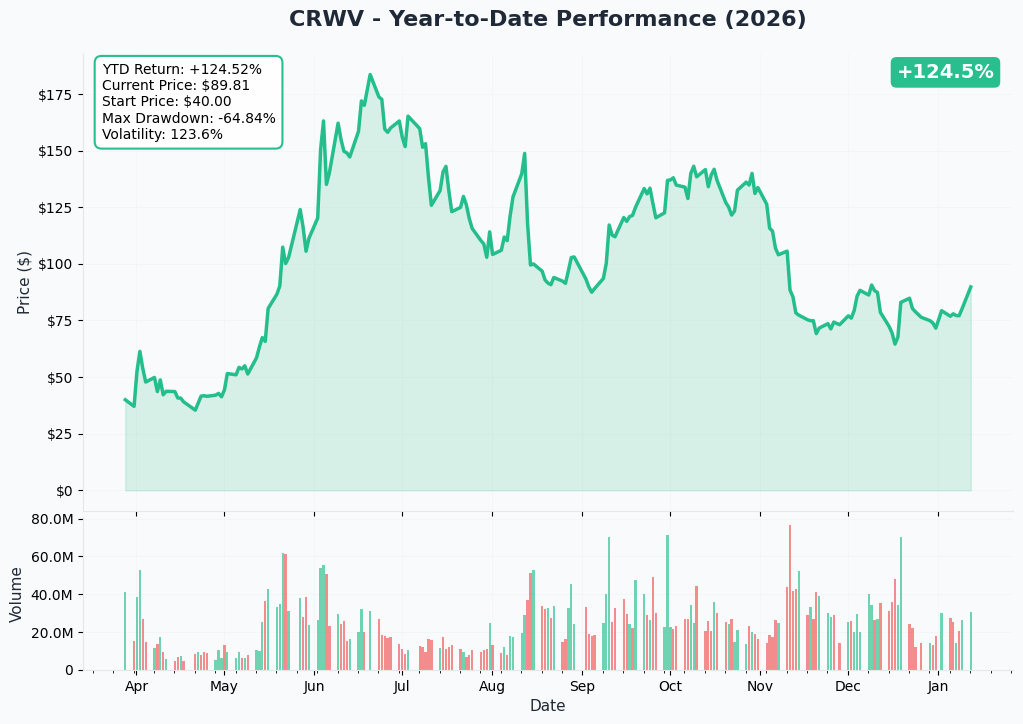

YTD Performance Chart

CoreWeave IPO'd in March 2025 at $40 and has been on a volatile journey since:

- IPO Price (March 2025): $40

- 52-Week High: $187 (June 20, 2025) - representing 367% gain from IPO

- 52-Week Low: $33.52 (April 21, 2025) - a 16% decline from IPO price shortly after listing

- Current Price: $89.88 - up 125% from IPO but down 52% from highs

- YTD 2026 Performance: +24%

Key observations:

- Stock exhibits extreme volatility typical of high-growth, high-leverage infrastructure plays

- The $40 put strike matches the IPO price - institutional investors may be hedging back to "ground zero"

- The $150 call strike represents a level not seen since the post-IPO euphoria period

- Price action suggests market still digesting the risk/reward of the leveraged growth model

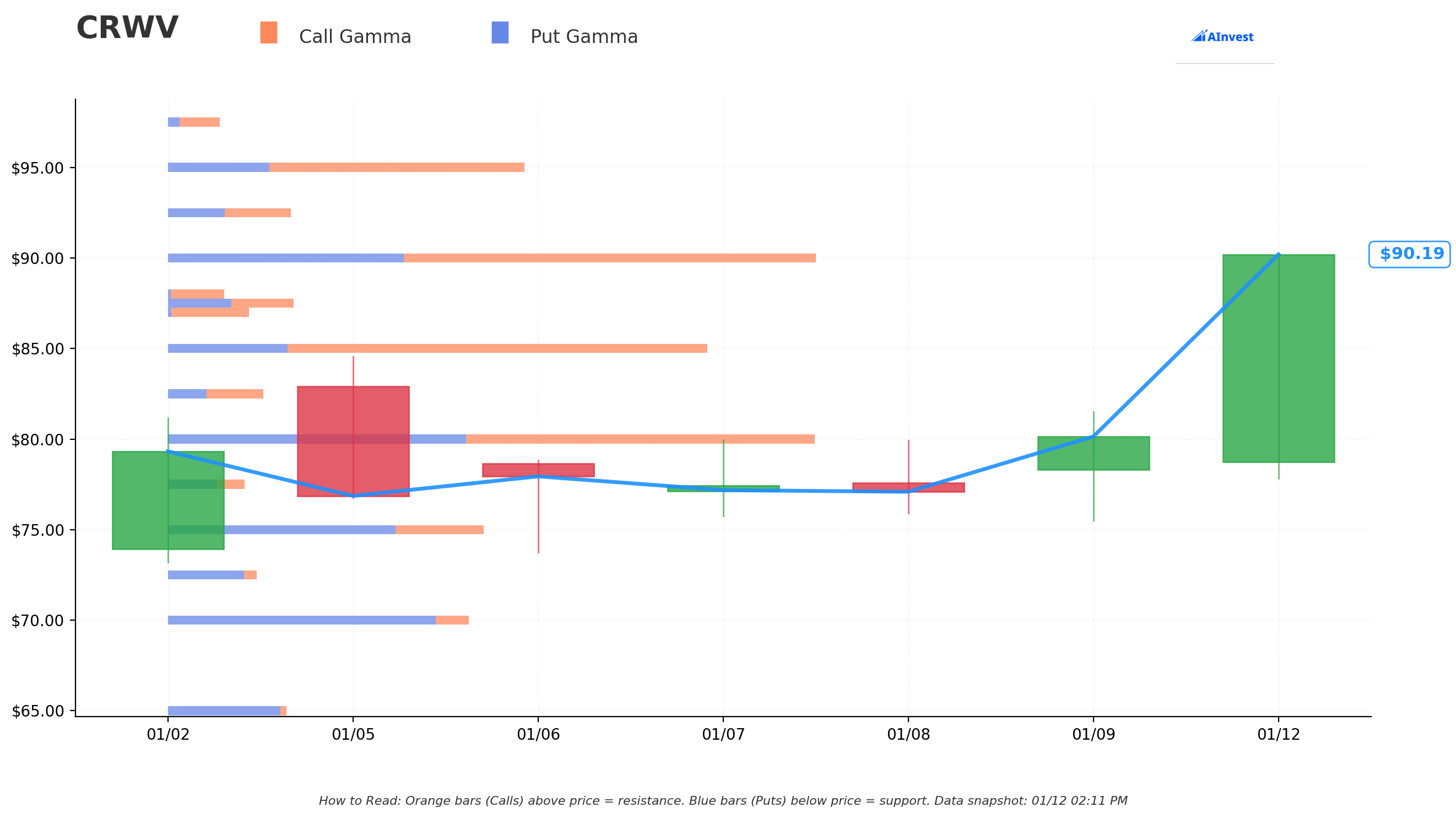

Gamma-Based Support & Resistance Analysis

Current Price: $89.88

Support Levels (Put Gamma Below Price):

- $87.50 - Immediate support with strongest nearby gamma concentration

- $80 - Secondary psychological support (round number)

- $65 - Extended support zone

- $40 - Put strike level / IPO price (deep structural floor)

Resistance Levels (Call Gamma Above Price):

- $90 - Immediate ceiling (current price testing this level)

- $100 - Major psychological resistance

- $125 - Analyst average target zone

- $150 - Call strike level / extended upside barrier

Net GEX Bias: Bullish - Gamma positioning suggests near-term support, but the bearish options structure indicates smart money sees risks that gamma analysis doesn't capture (fundamental/credit risk).

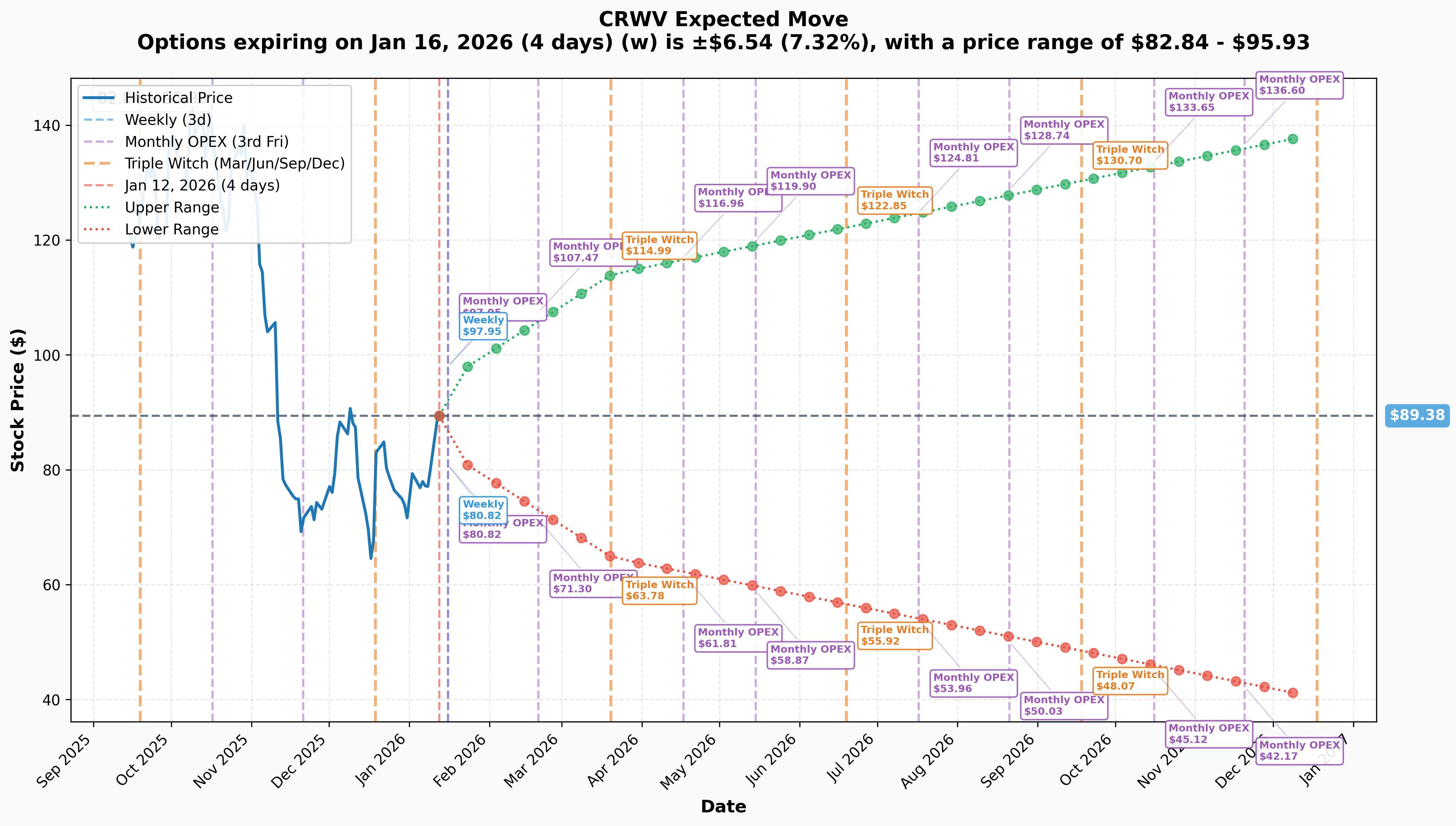

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (7 days): +/-7.08% ($83.52 - $96.25)

- Quarterly: +/-25.36% ($67.08 - $112.69)

- Yearly: +/-70.64%

Translation:

The options market is pricing CRWV as an extremely volatile stock - a 70% annualized implied move reflects the binary nature of the AI infrastructure thesis. The quarterly range of $67-$113 encompasses both the bull case (backlog conversion, capacity expansion) and bear case (debt stress, competitive pressure).

The $40 put strike sits well outside even the quarterly implied range - this is deep out-of-the-money protection against tail risk scenarios like:

- Failed debt refinancing

- Major customer loss (Microsoft, OpenAI, or Meta)

- Data center execution delays extending multiple quarters

- Hyperscaler pricing pressure destroying unit economics

Catalysts

Immediate Catalysts (Next 30-60 Days)

Q4 2025 Earnings - February 18, 2026 (After Market Close)

CoreWeave reports fiscal Q4 results on February 18th - the first major catalyst within the options expiration window. Based on Q3 2025 results where the company beat revenue estimates by 5.4%:

- Revenue Estimate: ~$1.5-1.6B (implied from FY guidance of $5.05-5.15B)

- Adjusted EBITDA Margin: Targeting 61%+ continuation (Q3 achieved 61% margin)

- 2026 Guidance: Street expects ~$12B revenue (133% growth)

- CapEx Plans: "Well in excess of double" 2025 levels ($12-14B spent in 2025)

Critical metrics to watch:

- Progress converting $55.6B revenue backlog to recognized revenue (nearly doubled in Q3)

- Customer concentration update (no single customer >35% of backlog per Q3 investor update)

- Data center capacity expansion (currently 590 megawatts active vs. 2.9 gigawatts contracted)

- Debt covenant compliance and liquidity position

Why this matters for the trade: If earnings disappoint or 2026 guidance underwhelms, CRWV could gap down 15-25% given current valuation. The long puts provide protection against this scenario.

Near-Term Catalysts (Q1-Q2 2026)

NVIDIA Rubin Platform Deployment - H2 2026

CoreWeave announced January 5, 2026 that it will be among the first cloud providers to deploy NVIDIA Rubin. This is critical for maintaining competitive advantage:

- Rubin deployment validates NVIDIA's continued preference for CoreWeave as a launch partner (track record as first to offer GB200 NVL72)

- Enables expansion into agentic AI, reasoning, and large-scale inference workloads

- Supports Poolside partnership with 40,000+ GPU cluster

- However, execution delays would damage the growth narrative

Applied Digital Data Center Delivery

The 250MW capacity lease worth $7 billion over 15 years depends on third-party data center completion. Management acknowledged delays in Q3 earnings call - any further slippage could:

- Delay revenue recognition

- Strain customer relationships

- Pressure already-tight liquidity

Recent Strategic Wins:

- Runway AI multi-year agreement (December 11, 2025) for next-gen video AI models

- DOE Genesis Mission partnership (December 18, 2025) alongside AWS, Google, Microsoft, NVIDIA, OpenAI, Oracle, Anthropic

Risk Catalysts (Negative)

$18.5B Debt Burden and Distress Indicators

CoreWeave's balance sheet represents the primary bear case per Yahoo Finance analysis and Baptista Research:

- Total Debt: $18.5 billion

- Quarterly Interest Payments: ~$310 million

- Debt-to-Equity Ratio: 363% (4.85x)

- Net Debt to EBITDA: 5.5x

- Altman Z-Score: 0.69 (distress zone - scores below 1.8 indicate bankruptcy risk)

- Projected 2025 Net Loss: ~$1.09 billion

The recent $2.59B convertible notes offering (December 2025) adds potential dilution at $107.80 conversion price. Stock fell 10% on announcement. If stock falls significantly, the company may need additional equity raises at depressed prices.

Hyperscaler Competition Intensifying

Microsoft plans to boost AI capacity 80%+ in FY2026 while doubling data center footprint. AWS, Google, and Oracle are similarly expanding GPU infrastructure. Per Motley Fool analysis, this threatens CoreWeave's scarcity premium:

- Hyperscalers can price aggressively given lower cost of capital

- Custom AI chips (Google TPUs, Amazon Trainium) reduce NVIDIA dependence

- CoreWeave has "no economic moat" as hyperscalers offer similar services

- CoreWeave's NVIDIA-centric model could become a disadvantage if supply normalizes

Customer Concentration Risk

Despite improvement from 85% to 35% for top customer (Q3 investor update), the top 3 customers (Microsoft, OpenAI, Meta) represent ~75% of revenue:

- Loss of any major customer would be devastating

- OpenAI is both a customer AND an investor ($350M stock issuance) - creating potential conflicts

- Meta deal worth $14.2B but stock still declined 30% after announcement

Legal/Regulatory Overhang

Kaplan Fox is investigating CoreWeave for potential securities law violations as of January 10, 2026. No specific allegations disclosed, but securities investigations can pressure stock prices regardless of outcome.

Price Targets & Probabilities

Analyst Consensus: Per TipRanks and Stock Analysis, 16 Buy / 8 Hold / 1 Sell ratings with average target $124.12 (range: $44-$208).

Using gamma levels, implied move data, and fundamental analysis, here are scenarios through January 2027 expiration:

Bull Case (20% probability)

Target: $140-$180

How we get there:

- Revenue backlog converts ahead of schedule with 2026 revenue exceeding $14B

- Data center capacity reaches 1.5+ gigawatts active (from current 590MW)

- Customer diversification accelerates - no customer >25% of revenue

- Debt refinanced at favorable terms, extending maturities

- NVIDIA Rubin deployment generates incremental large customer wins

- AI infrastructure spending accelerates despite broader macro concerns

Risk to the trade: The short $150 calls become at-risk if stock rallies above $140. Position would need to be managed or closed.

Base Case (50% probability)

Target: $70-$110 range (Volatile Consolidation)

Most likely scenario:

- Q4 earnings meet expectations but 2026 guidance creates concern

- Backlog conversion progresses but at slower-than-expected pace

- Data center delays remain manageable but persistent

- Debt burden weighs on stock but no liquidity crisis materializes

- Stock trades between gamma support ($87.50) and resistance ($100-$110)

- Options structure generates modest profit from time decay on both legs

This is the put buyer's acceptable scenario: The risk reversal generates income from premium decay while providing tail risk protection. The stock neither crashes nor rallies meaningfully.

Bear Case (30% probability)

Target: $35-$55 (Distress Scenario)

What could go wrong:

- Q4 miss or weak 2026 guidance triggers -20%+ gap down

- Data center delays extend 6+ months, straining customer relationships

- Major customer (Microsoft or OpenAI) reduces allocation

- Debt covenant violation triggers accelerated repayment requirements

- Hyperscaler pricing pressure compresses margins below viability

- Securities investigation expands or results in negative findings

- Broader AI spending slowdown reduces demand for GPU infrastructure

- Convertible notes trigger dilutive share issuance

- Stock approaches IPO price of $40 - the put strike

Put P&L in Bear Case:

- Stock at $50 by Jan 2027: Puts expire worthless, call premium retained (~$5.7M profit)

- Stock at $40 by Jan 2027: Puts at-the-money, minimal value, call premium retained (~$5.5M profit)

- Stock at $30 by Jan 2027: Puts worth ~$10, profit = ($10 - $2.29) x 20,500 = $15.8M + $5.7M call premium = $21.5M total profit

Trading Ideas

Conservative: Avoid Until Clarity

Play: Stay on sidelines until Q4 earnings (Feb 18) provides visibility on 2026 trajectory

Why this works:

- Debt-heavy balance sheet creates binary risk profile

- 70% implied volatility means options are expensive for directional bets

- February earnings will clarify revenue conversion trajectory and 2026 guidance

- Legal investigation overhang adds uncertainty

- Better entry points likely at support levels ($80, $65) if they're tested

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Balanced: Post-Earnings Put Spread

Play: After February 18 earnings, consider bear put spread if guidance disappoints

Structure: Buy $80 puts, Sell $60 puts (April 2026 expiration)

Why this works:

- Defined risk ($20 wide spread = $2,000 max risk per spread)

- Capitalizes on IV crush after earnings volatility

- Targets realistic downside zone based on gamma support levels

- Lower premium than outright puts due to short leg

Entry timing:

- Wait 2-3 days post-earnings for IV collapse

- Only enter if stock shows weakness on earnings reaction

- Skip if stock holds $85+ support convincingly

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

Aggressive: Synthetic Short via Risk Reversal

Play: Replicate institutional positioning with smaller risk reversal

Structure: Buy $70 put, Sell $120 call (July 2026 expiration)

Why this could work:

- Mimics the institutional trade thesis at reduced size

- Generates premium from short call to partially fund put

- 6-month timeframe captures Q4 and Q1 earnings

- Defined max gain on downside, capped upside above $120

Serious risks:

- Unlimited risk if stock rallies above $120

- Requires margin for naked short call

- Early assignment risk on call leg

- Position sizing critical - small allocation only

Risk level: HIGH (unlimited upside risk) | Skill level: Advanced only

Risk Factors

Critical risks to monitor:

-

Debt Distress: The $18.5B debt load with $310M quarterly interest payments creates genuine liquidity risk. The Altman Z-Score of 0.69 places CoreWeave in bankruptcy risk territory. Any covenant violation or failed refinancing could trigger rapid share price decline. The company recently amended its credit agreement to improve liquidity.

-

Customer Concentration: Top 3 customers represent 75% of revenue. Microsoft's own AI capacity expansion (80%+ increase in FY2026) could reduce their CoreWeave allocation over time. Customer concentration has improved from 85% to 35% for the largest customer in 2025.

-

Data Center Execution: Management acknowledged third-party developer delays in Q3. Completing data centers is the "largest single risk" per management - capacity delays mean revenue delays. Currently at 590MW active vs. 2.9GW contracted.

-

Hyperscaler Competition: AWS, Google, Microsoft, and Oracle are building massive GPU infrastructure. Per Seeking Alpha analysis, CoreWeave's scarcity premium from 2023-2025 may evaporate as supply normalizes. The company has no economic moat and cannot match hyperscaler cost of capital for aggressive pricing.

-

Securities Investigation: Kaplan Fox announced investigation for potential securities violations on January 10, 2026. While no specific allegations disclosed, legal overhang creates uncertainty.

-

Convertible Notes Dilution: The $2.59B convertible notes convert at $107.80 per share with capped calls at $215.60. If stock trades above conversion price, dilution occurs. If stock falls significantly, additional equity raises at depressed prices become likely.

-

AI Spending Cyclicality: If broader AI investment decelerates due to ROI concerns or economic weakness, CoreWeave's highly leveraged model faces severe stress. The infrastructure buildout assumes continued exponential demand growth.

The Bottom Line

Real talk: A sophisticated institution just positioned $12 million in bearish options structure on CoreWeave - buying deep out-of-the-money puts while selling upside calls. This is not a bet that CRWV goes to zero tomorrow; it's a calculated hedge that the current valuation doesn't adequately price in:

- Balance sheet risk from $18.5B debt with Altman Z-Score in distress zone

- Execution risk on data center buildout that management calls their "largest single risk"

- Competitive risk as hyperscalers expand AI capacity at a pace CoreWeave cannot match

- Concentration risk with 75% of revenue from 3 customers

What this trade tells us:

- Institutional investors see meaningful probability of retest toward IPO price ($40) within 12 months

- They're willing to cap upside at $150 to fund downside protection - implying limited confidence in further multiple expansion

- The January 2027 expiration captures multiple earnings cycles and the critical H2 2026 NVIDIA Rubin deployment

- This is sophisticated portfolio risk management, not speculative gambling

If you own CRWV:

- Consider trimming 25-40% at current levels to reduce concentration

- Set mental stop at $80 (immediate gamma support)

- Monitor Q4 earnings (Feb 18) for guidance quality and debt covenant commentary

- The 24% YTD gain in 2026 provides an opportunity to lock in profits

If you're watching from sidelines:

- February 18th Q4 earnings is the next major catalyst

- Wait for clarity on 2026 guidance and debt trajectory before initiating positions

- Entry at $65-70 (extended support zone) offers better risk/reward if tested

- The $55.6B backlog is real, but conversion timing and margin quality remain uncertain

If you're bearish:

- Post-earnings put spreads offer defined-risk exposure if guidance disappoints

- Watch for break below $80 gamma support as confirmation signal

- Risk reversals require advanced knowledge and margin capability

Key dates:

- February 18, 2026 - Q4 2025 earnings report (after market close)

- May 2026 (estimated) - Q1 2026 earnings

- H2 2026 - NVIDIA Rubin platform deployment begins

- January 17, 2027 - Options expiration for this $12M trade

Final verdict: CoreWeave's growth story remains compelling - $55.6B backlog, first-mover on NVIDIA hardware, validated by OpenAI/Microsoft/Meta partnerships. However, the $18.5B debt load, Altman Z-Score in distress territory, and hyperscaler competitive pressure create genuine downside risk that the $12M bearish options structure is designed to capture. This is not a "sell everything" signal - it's a "the risk/reward is not as favorable as it appears" signal. Smart money is positioning for the possibility that execution stumbles, debt becomes problematic, or competitive dynamics shift against CoreWeave's specialized model.

The institutional thesis: CoreWeave faces a "prove it" period over the next 12-18 months where backlog must convert to revenue while managing leverage in an increasingly competitive market. The options structure reflects measured skepticism, not panic.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. CoreWeave is a recently-IPO'd company with limited trading history and elevated volatility. The debt-heavy balance sheet creates additional risk not present in more established companies. Always do your own research and consider consulting a licensed financial advisor before trading.

About CoreWeave: CoreWeave is an AI-focused cloud computing company that operates NVIDIA-powered data centers providing GPU infrastructure to leading AI companies including OpenAI, Microsoft, and Meta. Founded in 2017 and headquartered in Roseland, New Jersey, CoreWeave IPO'd in March 2025 at $40 per share and has grown to a market capitalization of approximately $40 billion.