CX Options Flow Analysis - January 16, 2026

Trade Summary

A $4.7 million call position just hit the tape on CEMEX (CX), targeting the March 20, 2026 expiration at the $13 strike. With the stock trading at $12.40, someone is betting big that CX breaks above its recent 52-week high and keeps running.

Trade Tape

| Field | Value |

|---|---|

| Time | 13:57:08 |

| Ticker | CX |

| Direction | BUY |

| Option Type | CALL |

| Strike | $13.00 |

| Expiration | 2026-03-20 |

| Option Symbol | CX20260320C13 |

| Spot Price | $12.40 |

| Option Price | $0.65 |

| Size | 72,500 contracts |

| Volume | 73,000 |

| Open Interest | 0 |

| Premium | $4,712,500 |

| Strategy | Single Leg Call Buy (BTO) |

Unusual Score

Score: 8.5/10 - Highly Unusual Activity

[=========------] 8.5/10

Why This Stands Out:

- Premium Size: $4.7M is a substantial single-ticket bet for a $18B market cap company

- Volume vs OI: 72,500 contracts traded against 0 open interest - this is brand new positioning

- Moneyness: Strike is 4.8% out-of-the-money, requiring a move to new highs

- Timing: 63 days to March quarterly expiration (triple witch)

- Contract Control: This position controls $94.25M in notional stock exposure

This is large fund-level positioning. A $4.7M premium on a single strike with zero prior open interest suggests a new institutional thesis being established, not a hedge or roll.

Company Overview

CEMEX, S.A.B. de C.V. is a global building materials company headquartered in Monterrey, Mexico. The company produces, markets, and distributes cement, ready-mix concrete, aggregates, and related building materials across 60+ countries.

| Metric | Value |

|---|---|

| Market Cap | $17.92 billion |

| Sector | Basic Materials |

| Industry | Building Materials |

| Employees | 40,244 |

| Exchange | NYSE (ADR) |

| P/E Ratio | 13.44 |

| Beta | 1.59 |

| Dividend Yield | 0.76% |

CEMEX is one of the largest cement producers globally, competing with Holcim, CRH, and Heidelberg Materials. The company has been undergoing a strategic transformation under new CEO Jaime Muguiro, who took the helm in April 2025 after 35 years at the company1.

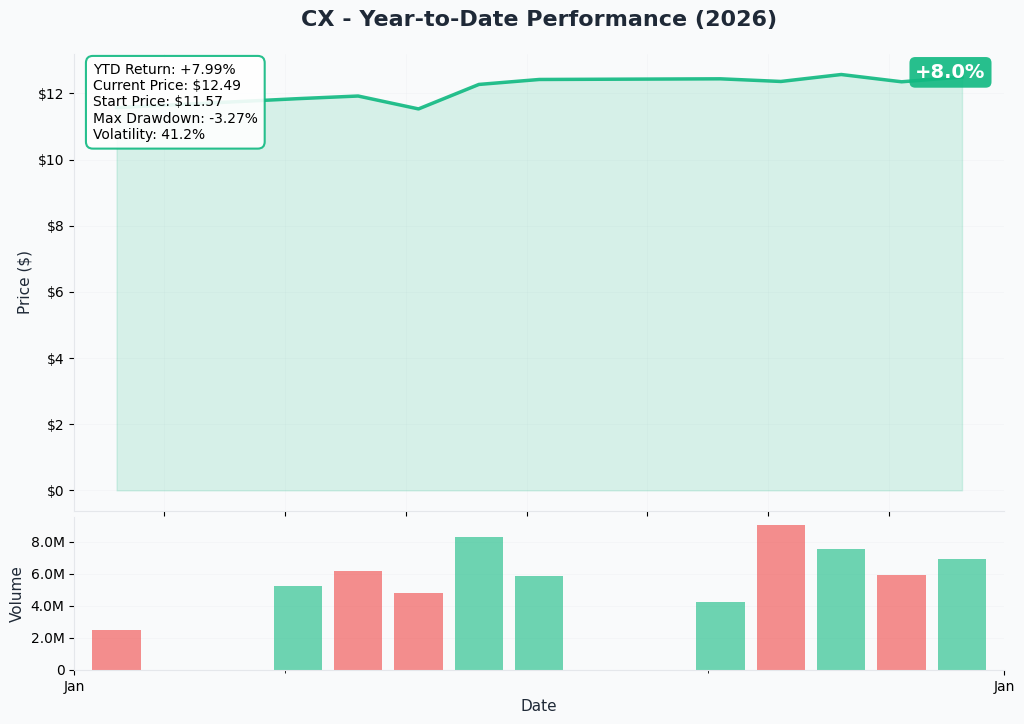

YTD Performance

CX has been on a tear, up 6.8% YTD and outperforming the Construction sector average of 4.7%2. The stock recently hit a new 52-week high of $12.50, having climbed from a 52-week low of $4.89 - a remarkable recovery of over 155%3.

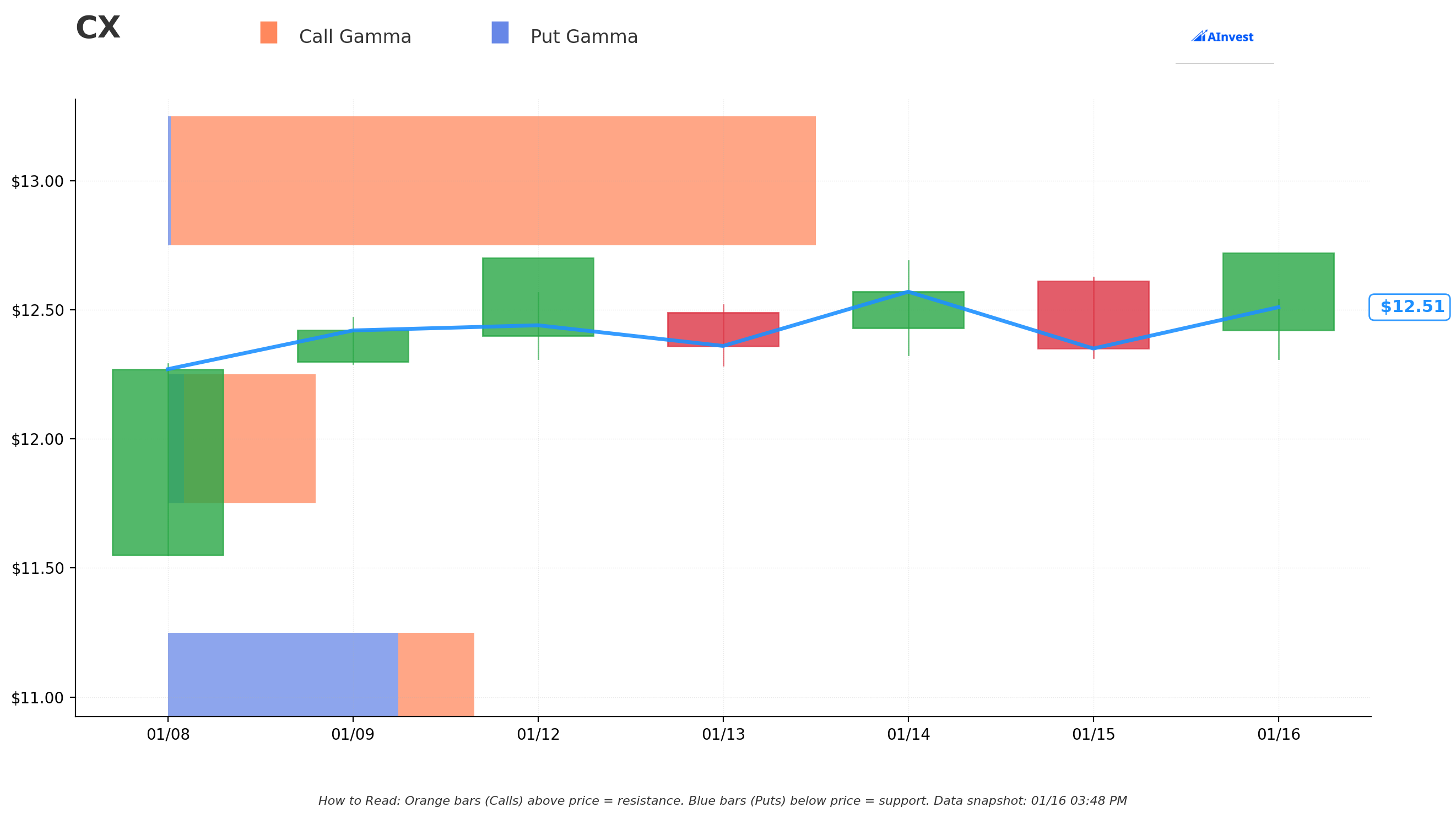

Gamma Support/Resistance Levels

Key gamma levels to watch:

| Level | Price | Significance |

|---|---|---|

| Gamma Resistance | $13.00 | Heavy call OI at strike target |

| Current Price | $12.40 | Trading near recent highs |

| Gamma Support | $11.50 | Put wall providing floor |

| Secondary Support | $11.00 | 50-day moving average3 |

The $13 strike represents both the trade target and a potential gamma wall. If CX pushes through this level, dealer hedging could accelerate the move higher.

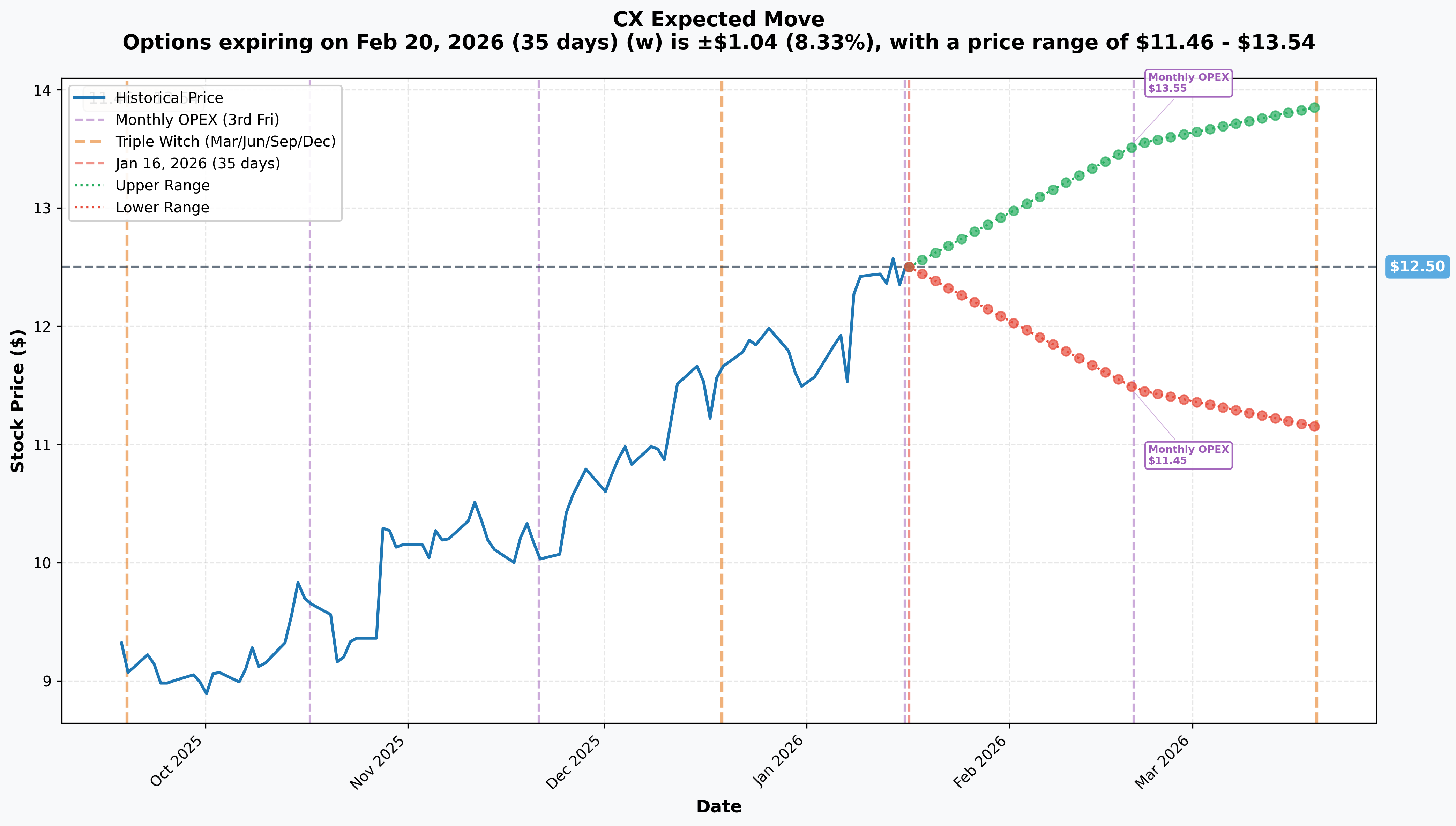

Implied Move Analysis

| Timeframe | Expiry | Days | Implied Move | Range |

|---|---|---|---|---|

| Monthly OPEX | 2026-02-20 | 35 | +/- 8.33% | $11.46 - $13.54 |

| Quarterly (Mar) | 2026-03-20 | 63 | +/- 10.88% | $11.14 - $13.86 |

The options market is pricing in a potential move to $13.86 by March expiration, which would put the $13 strike comfortably in-the-money. The current implied volatility suggests the market sees meaningful event risk ahead.

Catalyst Timeline

Near-Term (0-30 Days)

Q4 2025 Earnings (Expected early February 2026)

- Consensus EPS estimate: ~$0.18 per share4

- Full-year EBITDA guidance: Flat vs 2024 with potential upside5

- Key metrics: Project Cutting Edge savings realization, U.S. infrastructure demand6

Medium-Term (30-90 Days)

2026 FIFA World Cup Infrastructure Push

- Over $1 billion in Mexico City investment alone7

- Monterrey: 34 strategic projects including Metro expansion8

- CEO Muguiro confirmed "extensive number of projects in the pipeline"9

Dividend Payment (March 2026)

- Fourth installment of $32.5M expected starting March 12, 202610

- Ex-dividend date: March 11, 2026

European CBAM Implementation (January 1, 2026)

- EU carbon border adjustment could allow EUR 5-10/ton price increases11

- CEMEX Europe saw high-single-digit cement volume growth in Q39

Structural Tailwinds

Project Cutting Edge

- $200M EBITDA savings achieved in 20255

- $400M annual run-rate target by 20275

- Corporate headcount reduction contributing ~$200M5

U.S. Infrastructure Act (IIJA)

- $363 billion in infrastructure spending ongoing12

- U.S. operations posted record Q3 margins9

- CEMEX allocated $104M to U.S. in Q1 2025 alone12

Investment Grade Status

- S&P upgraded to BBB- (March 2024)13

- Fitch upgraded to BBB- (April 2024)14

- Optimized cost of capital and improved debt profile14

Price Targets & Probabilities

Based on the implied move data, gamma levels, and catalyst timeline:

| Target | Price | Probability | Rationale |

|---|---|---|---|

| Conservative | $13.00 | 55% | At-strike target, aligns with gamma resistance |

| Base Case | $13.50 | 40% | Within implied move upper range ($13.54 Feb, $13.86 Mar) |

| Bullish | $14.50 | 20% | Requires earnings beat + World Cup infrastructure momentum |

Breakeven Analysis for the Trade:

- Breakeven at expiration: $13.65 ($13.00 strike + $0.65 premium)

- Current distance to breakeven: 10.1%

- Implied probability of profit: ~35-40% based on current IV

Trading Strategies

Conservative Approach

Strategy: Sell cash-secured puts below support

- Trade: Sell CX March 20 $11 Puts

- Rationale: Collect premium while getting paid to buy at a 11% discount

- Max Profit: Premium received (approximately $0.35-0.45)

- Max Risk: Assignment at $11 (your cost basis minus premium)

- Best For: Investors who want exposure but prefer better entry

Balanced Approach

Strategy: Call spread to reduce cost

- Trade: Buy CX March 20 $13 Calls / Sell CX March 20 $15 Calls

- Cost: ~$0.35-0.40 per spread (vs $0.65 for naked call)

- Max Profit: $1.60-1.65 per spread if CX above $15 at expiration

- Risk/Reward: 4:1 potential return with capped risk

- Best For: Bullish bias with defined risk tolerance

Aggressive Approach

Strategy: Follow the flow with smaller position

- Trade: Buy CX March 20 $13 Calls (same as institutional flow)

- Position Size: Risk no more than 2-3% of portfolio

- Stop Loss: Exit if premium declines 50% ($0.325)

- Target: Take profits at $1.00-1.30 (50-100% gain)

- Best For: Traders comfortable with binary outcomes around catalysts

Risk Factors

Tariff Exposure (High Risk)

The Trump administration's proposed 25% tariffs on Mexico and Canada pose significant risk to CEMEX operations. Canada and Mexico account for 27% of U.S. cement imports15. CEO Muguiro stated CEMEX would "immediately" pass costs to customers, but demand destruction is a concern16.

Mexico Volume Headwinds (Medium Risk)

Difficult comparison base from pre-election infrastructure spending in 2024. CEMEX expects a "story of two halves" in Mexico similar to 202417. Peso weakness also impacts dollar-reported results.

U.S. Residential Softness (Medium Risk)

Q3 2025 volumes for core products declined 1% year-over-year. Infrastructure strength is offsetting residential weakness, but a broader slowdown could pressure results9.

Valuation After Rally (Medium Risk)

Stock has rallied 155% from 52-week lows. Several analysts have set price targets below current levels - Itau BBA and Bradesco BBI both at $7.5018. Some profit-taking expected at current levels.

Execution Risk (Low-Medium Risk)

Project Cutting Edge savings must materialize on schedule. World Cup infrastructure spending depends on government execution and timelines7.

Institutional Context

Ownership Structure:

- Institutional ownership: ~83% of NYSE-listed shares19

- Largest holder: BlackRock, Inc. at 9.1%19

- Other major holders: Dodge & Cox, FMR LLC, UBS Asset Management19

Recent Analyst Activity:

| Firm | Rating | Target | Date |

|---|---|---|---|

| Barclays | Overweight | $12.00 | Oct 29, 202520 |

| Goldman Sachs | Buy | $11.00 | Oct 202520 |

| JPMorgan | Overweight | - | Recent18 |

| RBC Capital | Sector Perform | $11.25 | Dec 8, 202518 |

| Citigroup | Neutral | $10.00 | Oct 13, 202518 |

Consensus: 4 Buy, 2 Hold, 0 Sell with average target of $10.5718 - notably below current price.

The Bottom Line

What's Happening: A large institution just established a $4.7 million bullish position in CEMEX, betting the stock breaks above $13 by March expiration. The zero prior open interest confirms this is new directional positioning, not hedging activity.

Why It Matters: CEMEX has multiple catalysts converging - Q4 earnings in early February, 2026 World Cup infrastructure spending ramping in Mexico, and ongoing benefits from U.S. infrastructure legislation. The company's Project Cutting Edge program is ahead of schedule, and investment-grade credit status provides financial flexibility.

The Catch: The stock has already rallied significantly from its 52-week low, and analyst price targets average below current levels. Tariff risk remains a wildcard that could disrupt the thesis. The trade needs CX to reach $13.65 (10% higher) just to break even.

Action Plan:

- If Bullish: Consider the call spread strategy (buy $13/sell $15) to participate with defined risk and better cost basis than the outright call

- If Cautious: Wait for Q4 earnings to validate the thesis before establishing a position

- If Bearish: The high IV environment makes put selling attractive if you believe support holds

Key Dates to Watch:

- Early February: Q4 2025 earnings release

- March 11, 2026: Ex-dividend date

- March 20, 2026: Option expiration (quarterly triple witch)

- June 2026: FIFA World Cup kicks off

The institutional flow here is notable, but remember - big money isn't always right money. Position size appropriately and don't chase premium in a stock that's already near 52-week highs.

References

Analysis generated January 16, 2026. Options trading involves significant risk. Past performance does not guarantee future results.

Footnotes

-

CEMEX, "Jaime Muguiro begins tenure as CEO of Cemex", April 1, 2025 ↩

-

Yahoo Finance, "Is Cemex (CX) Stock Outpacing Its Construction Peers This Year?", January 2026 ↩

-

The Markets Daily, "Cemex (NYSE:CX) Hits New 12-Month High", January 12, 2026 ↩ ↩2

-

Seeking Alpha, "Cemex Q3 Earnings Preview", October 2025 ↩

-

CEMEX, "Cemex accelerates strategic transformation", H1 2025 ↩ ↩2 ↩3 ↩4

-

MarketBeat, "Cemex (CX) Earnings Date and Reports 2025", January 2026 ↩

-

Washington Post, "Sheinbaum: Mexico will finish 2026 World Cup infrastructure projects in time", November 10, 2025 ↩ ↩2

-

Mexico Business News, "Mexico's World Cup 2026: Infrastructure Race", 2025 ↩

-

Argus Media, "Stronger 3Q helps Cemex offset weaker 1H", October 2025 ↩ ↩2 ↩3 ↩4

-

Stock Analysis, "CEMEX (CX) Dividend History, Dates & Yield", January 2026 ↩

-

CemNet, "Outlook: challenges remain in 2026", January 2026 ↩

-

AInvest, "Cemex's Strategic Turnaround and EBITDA Growth Catalysts", 2025 ↩ ↩2

-

CEMEX, "Standard & Poor's Upgrades Cemex to Investment Grade", March 2024 ↩

-

CEMEX, "Fitch Ratings Upgrades Cemex to Investment Grade", April 30, 2024 ↩ ↩2

-

S&P Global, "Replacement of Canadian, Mexican cement imports to US 'difficult'", February 13, 2025 ↩

-

Argus Media, "Cemex may increase cement prices on tariffs", February 2025 ↩

-

CEMEX, "Q4 2024 Report", February 2025 ↩

-

Stock Analysis, "CEMEX, SAB de CV (CX) Analyst Ratings", January 2026 ↩ ↩2 ↩3 ↩4 ↩5

-

MarketBeat, "Cemex (CX) Institutional Ownership 2025", January 2026 ↩ ↩2 ↩3

-

TipRanks, "Cemex SAB (CX) Stock Forecast", January 2026 ↩ ↩2