🚀 CYTK $15.4M Bullish Bet - Massive FDA Approval Play Ahead of December 26th! 💊

📅 December 3, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Institutional money just deployed $15.4 MILLION across two massive bullish call positions on Cytokinetics ahead of the critical December 26, 2025 FDA PDUFA decision! Smart money bought $10M in $55 calls (Jan 16) PLUS $5.4M in $75 calls (Apr 17) - a sophisticated two-tranche structure positioning for BOTH near-term FDA approval AND post-launch commercial momentum. With CYTK at $64.89 and 85-90% analyst approval odds, this is a HIGH-CONVICTION bet that aficamten becomes the next blockbuster HCM drug! Translation: Big money believes the FDA says YES on December 26th!

📊 Company Overview

Cytokinetics, Incorporated (CYTK) is a late-stage specialty cardiovascular biopharmaceutical company focused on discovering, developing, and commercializing muscle biology-directed drug candidates as potential treatments for debilitating diseases in which cardiac muscle performance is compromised. Founded in 1997 and headquartered in South San Francisco, California, the company is pioneering muscle activators and inhibitors as treatments for conditions including heart failure, hypertrophic cardiomyopathy (HCM), and other cardiac diseases.

Key Business Highlights:

- 💊 Lead Asset: Aficamten, a cardiac myosin inhibitor for hypertrophic cardiomyopathy awaiting FDA approval

- 📅 FDA PDUFA Date: December 26, 2025 - critical binary catalyst

- 💰 Financial Position: $1.3 billion in cash providing runway into 2027

- 🤝 Strategic Partnerships: Collaborations with Ji Xing Pharmaceuticals (Greater China), Sanofi (recent rights acquisition)

- 🔬 Pipeline: Multiple Phase 3 trials ongoing including omecamtiv mecarbil (heart failure), CK-586 (HFpEF)

- 📈 Recent Performance: +69% over past 3 months, driven by FDA decision anticipation

💰 The Option Flow Breakdown

💸 Total Premium Deployed: $15.4M

On December 3, 2025, institutional traders deployed $15.4 million across two large bullish call positions ahead of the critical FDA PDUFA decision on December 26, 2025. This represents an extremely high-conviction bet on positive regulatory outcome and subsequent stock appreciation.

The Tape (December 3, 2025 @ 11:31:55):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:31:55 | CYTK | MID | BUY | CALL $55 | 2026-01-16 | $10M | $55 | 7,500 | 8,400 | 7,500 | $64.89 | $13.80 | CYTK 55C 01/16 |

| 11:31:55 | CYTK | MID | BUY | CALL $75 | 2026-04-17 | $5.4M | $75 | 5,000 | 92 | 5,000 | $64.89 | $10.70 | CYTK 75C 04/17 |

🤓 What This Actually Means

This is sophisticated bullish positioning with serious institutional conviction! Here's the breakdown:

Trade #1: Near-Term FDA Play ($55 CALL Jan 16) 💊

- 💸 Premium paid: $10,000,000 ($13.80 per contract × 7,500 contracts)

- 🎯 Moneyness: In-the-money (strike $9.89 below spot price)

- ⏰ Time to Expiry: 44 days (expires 21 days BEFORE FDA decision!)

- 📊 Vol/OI ratio: 0.89 - HIGH ACTIVITY indicating major position opening

- 🔥 Z-Score: 7.67 (EXTREMELY UNUSUAL activity)

- 💪 Breakeven: $68.80 (6% above current price)

- 🎪 The Play: Capture immediate FDA approval momentum - positioned to benefit from pre-PDUFA positioning and early approval speculation

Trade #2: Post-Approval Expansion ($75 CALL Apr 17) 🚀

- 💰 Premium paid: $5,400,000 ($10.70 per contract × 5,000 contracts)

- 🎯 Moneyness: Out-of-the-money (strike $10.11 above spot)

- ⏰ Time to Expiry: 135 days (expires 112 days AFTER FDA decision!)

- 📊 Vol/OI ratio: 54.35 - EXTREME ACTIVITY (volume 54x open interest!)

- 🔥 Z-Score: 432.57 (EXTREMELY UNUSUAL - unprecedented level!)

- 💪 Breakeven: $85.70 (32% above current price)

- 🎪 The Play: Capitalize on commercial launch momentum and label strength - positioned for post-PDUFA label analysis, launch execution, and market share capture

What's really happening here: This trader constructed a staggered bullish call spread with distinct risk/reward profiles targeting different phases of the FDA catalyst cycle:

- The ITM $55 Jan calls provide maximum exposure to FDA approval anticipation rally with defined time boundary

- The OTM $75 Apr calls bet on asymmetric upside from blockbuster label and competitive differentiation vs. Bristol Myers' Camzyos

Capital allocation: $10M ITM vs. $5.4M OTM shows confidence-weighted exposure favoring near-term catalyst

No hedging: Pure directional bullish bet with no protective puts detected - this is HIGH CONVICTION

📈 Technical Setup / Chart Check-Up

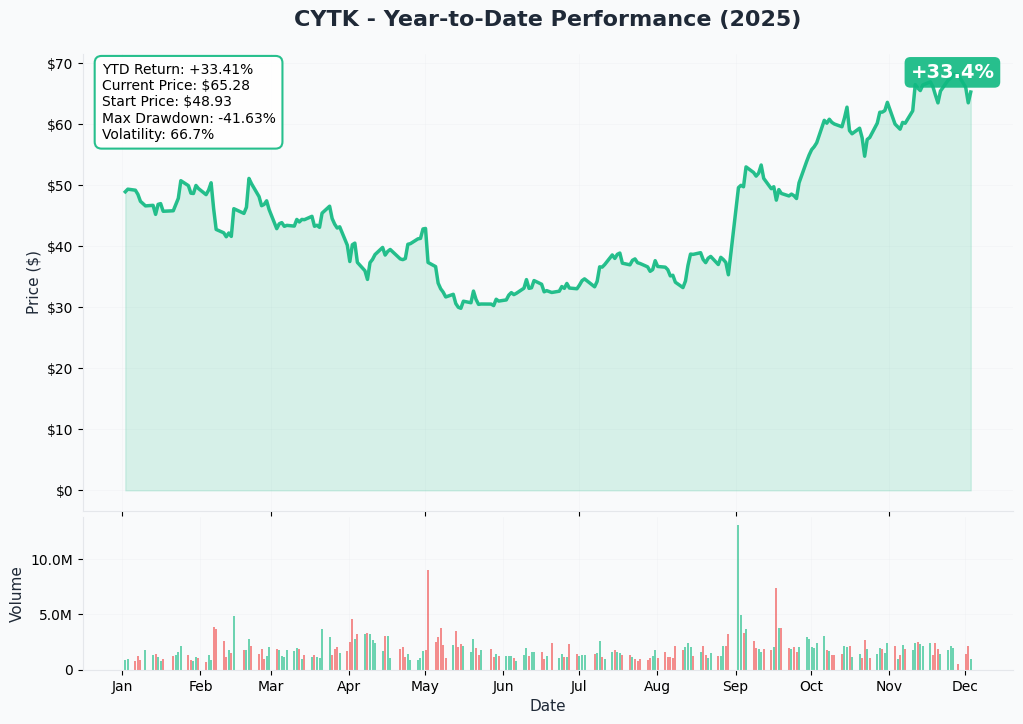

YTD Performance Chart

Current Price: $64.89 52-Week Range: $29.31 - $69.33 Recent Momentum: +69% over 3 months YTD Performance: +31%

CYTK is in a powerful uptrend driven entirely by FDA approval anticipation! The chart shows:

Key observations:

- 🚀 Strong uptrend since September 2024 as FDA date approached

- 📈 Currently trading near 52-week highs - market pricing in high approval odds

- 🛡️ Significant support established at $55-60 range (aligns with $55 call strike!)

- 🚧 Resistance at $70 psychological level and $75 options strike

- 💪 Volume explosion as institutional money flows in ahead of binary catalyst

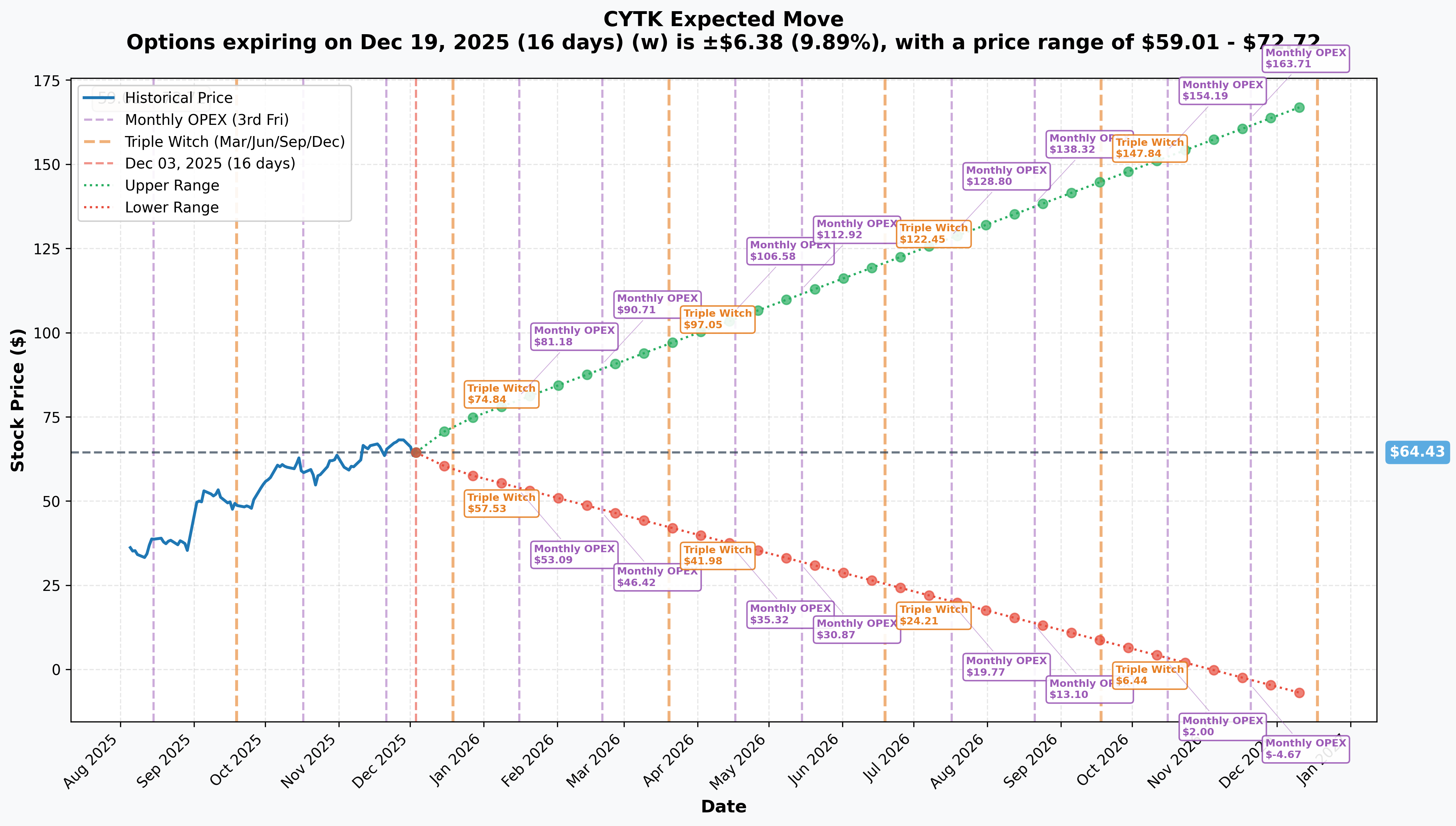

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 December 19, 2025 Monthly OPEX (Triple Witch): ±9.89% ($6.38) → Range: $59.01 - $72.72 (16 days)

- 📅 January 16, 2026 OPEX ($55 CALL expiry): ~15-18% estimated → Range: $53.09 - $81.18

- 📅 April 17, 2026 OPEX ($75 CALL expiry): ~40-45% estimated → Range: $35.32 - $106.58

Translation for regular folks: The market is pricing MASSIVE volatility around the December 26th FDA decision! The January expiry occurs 21 days BEFORE FDA decision, suggesting trader expects FDA anticipation rally to drive ITM position deep into profitability. The April wide range accounts for binary FDA outcome plus 3-4 months of commercial launch execution data.

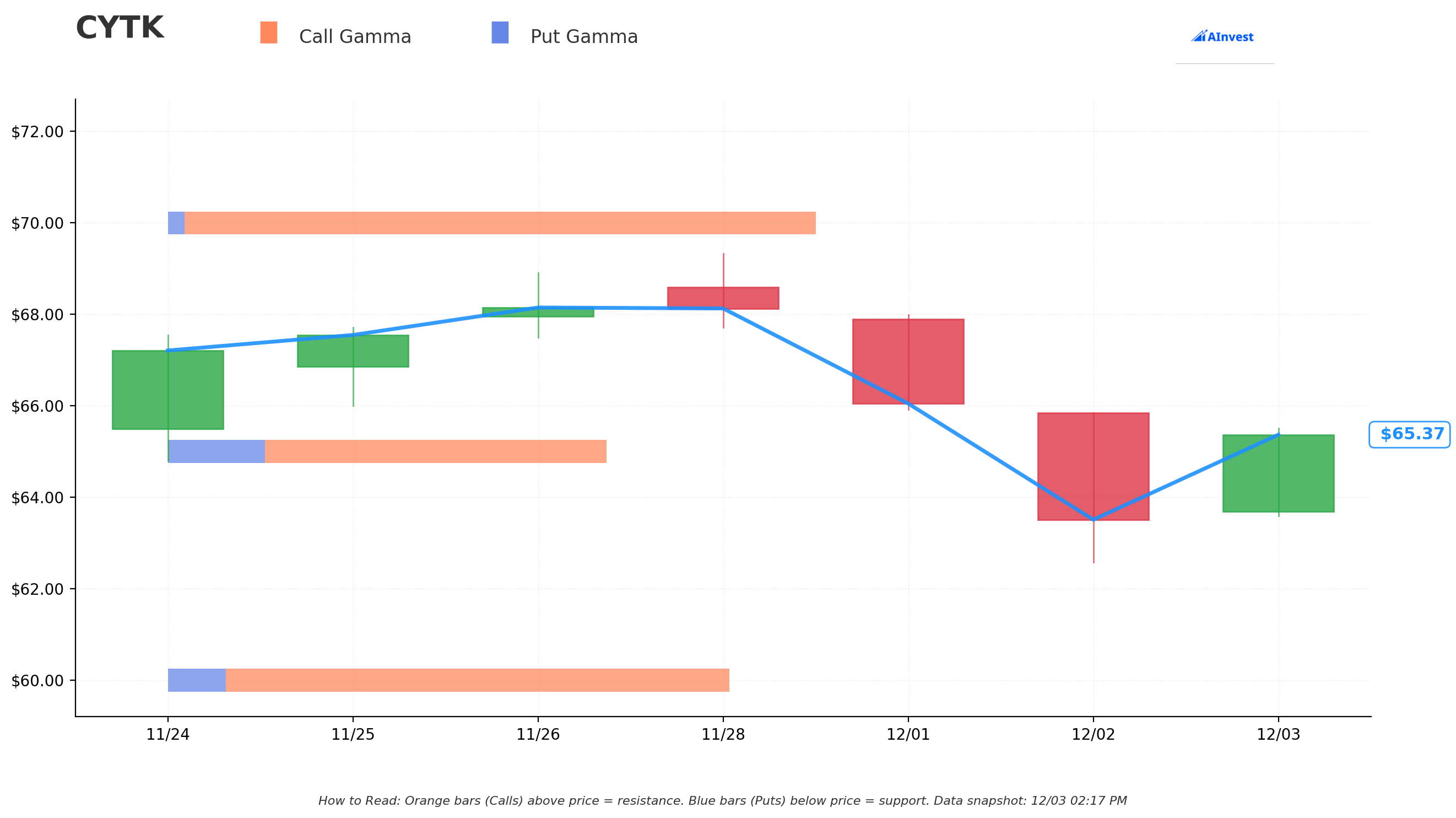

Gamma Exposure Analysis

Key GEX Levels:

- 🔵 Support Zones: $55, $60, $65 (heavy put gamma concentration)

- 🟠 Resistance Zones: $70, $75 (call gamma walls)

- ✅ Current Regime: Positive gamma environment (dealers long gamma)

Interpretation:

- Dealers will act as stabilizers, buying dips and selling rallies

- Breakout above $70 could trigger short gamma flip, accelerating upward momentum

- $75 strike represents major call gamma wall - breakthrough would be EXPLOSIVE

- Today's $15.4M call buying adds to positive gamma profile

🎪 Catalysts

🔥 Confirmed Near-Term Catalysts

1. FDA PDUFA Decision - December 26, 2025 ⭐⭐⭐⭐⭐

- 📅 Event: FDA action date for aficamten NDA for obstructive hypertrophic cardiomyopathy (oHCM)

- 📊 Probability of Approval: 85-90% (analyst consensus)

- 💥 Expected Impact: Binary event with 20-40% stock movement potential

- ✅ Key Factors:

- No additional clinical data requested by FDA (highly positive signal!)

- SEQUOIA-HCM data published in New England Journal of Medicine validates efficacy

- REMS extension suggests regulatory focus on monitoring protocols, not efficacy concerns

- Successful approval unlocks $1.5-3.0 billion peak sales opportunity

Label Quality Considerations:

- Approved dosing regimen and titration protocol

- REMS requirements (frequency of LVEF monitoring - critical for adoption)

- Language on efficacy endpoints vs. Bristol Myers' Camzyos

- Any restrictions on patient population or comorbidities

2. Q4 2024 Earnings Report - February 27, 2025 📊

- 📈 Expected Focus: Cash burn rate, commercial infrastructure investment, manufacturing scale-up

- ⏰ Impact on Options: May provide additional confidence in Q1 2026 launch readiness

- 📊 Timing: Falls within both options' life cycles, could drive volatility

3. MAPLE-HCM Full Results Publication - Q1-Q2 2025 📑

- 🔬 Event: Detailed head-to-head data: aficamten vs. metoprolol monotherapy

- 💪 Commercial Significance: Demonstrates superiority vs. standard-of-care beta-blocker

- 📅 Expected Presentation: European Society of Cardiology Congress 2025 + NEJM publication

🚀 Medium-Term Catalysts (Relevant for Apr 17 Position)

4. European Medicines Agency (EMA) Decision - Mid-2025 🇪🇺

- ⏰ Timeline: Q2-Q3 2025

- 🌍 Market Expansion: Additional $800M-$1.2B peak sales opportunity in Europe

- 📈 Impact: Validates global commercial potential, supports higher valuation multiples

5. ACACIA-HCM Non-Obstructive HCM Data Updates 🔬

- 📊 Market Expansion Potential: Could double addressable patient population to 240,000

- 🎯 Competitive Advantage: Bristol Myers' Camzyos failed in nHCM indication

- 💰 Revenue Impact: Additional $1.5B in peak sales if successful

6. Commercial Launch Execution Updates - Q1-Q2 2026 🚀

- 📈 Early Prescribing Data: TRx (prescription) tracking

- 💊 Payer Coverage Decisions: Critical for market penetration

- 📊 Market Share Capture: Evidence of penetration vs. entrenched Camzyos

- 👨⚕️ Physician Adoption Metrics: Sales force effectiveness indicators

⚠️ Risk Factors That Could Impact Options

Downside Catalysts:

- ❌ FDA Rejection or Complete Response Letter (CRL): 10-15% probability - would result in 30-50% stock decline

- 🚨 Restrictive REMS Requirements: Could burden adoption and slow commercial uptake

- 📉 Weak Label vs. Camzyos: Failure to differentiate could limit market share capture

- ⏰ Commercial Launch Delays: Manufacturing, supply chain, or regulatory distribution issues

- 🏥 Adverse Safety Signal: Any post-marketing surveillance concerns

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through January 16th and April 17th expirations:

📈 Bull Case (60% probability)

Target: $80-95 by Q1 2026

Scenario 1: Clean FDA Approval + Strong Label

How we get there:

- ✅ FDA approves aficamten December 26 with clean label

- 💪 Strong differentiation vs. Camzyos (shorter half-life, favorable safety profile)

- 📊 MAPLE-HCM data impresses showing head-to-head superiority vs. metoprolol

- 🎯 Analyst upgrades flood in with $80-95 price targets

- 💰 Commercial readiness confirmed in Q4 earnings (Feb 27)

- 🚀 Market share projections exceed 50% within 5 years

Key metrics needed:

- FDA approval with minimal REMS restrictions

- Dosing flexibility advantages confirmed vs. Camzyos

- Physician survey data showing 75%+ confidence in aficamten

- Manufacturing scale-up on track

Call P&L in Bull Case:

- $55 CALL (Jan 16) at $85 stock: Profit = $16.20/share × 7,500 = $12.2M gain (122% ROI)

- $75 CALL (Apr 17) at $95 stock: Profit = $9.30/share × 5,000 = $4.7M gain (87% ROI)

- Combined: $16.9M profit on $15.4M invested = 110% return!

Probability assessment: 60% because fundamentals are STRONG (85-90% approval odds, differentiated profile, massive market opportunity) and no additional FDA data requests is highly positive signal.

🎯 Base Case (20% probability)

Target: $70-75 (MODEST GAINS)

Scenario 2: Approval with Restrictive REMS

Most likely scenario:

- ✅ FDA approves but with burdensome REMS requirements

- ⚖️ Monitoring protocols more intensive than expected

- 📊 Stock rallies to $70-75 but not explosive breakout

- 💤 Market concerned about adoption headwinds

- 🔄 Commercial launch timeline extends slightly

- 📈 Analyst targets remain conservative $70-80 range

Call P&L in Base Case:

- $55 CALL (Jan 16) at $72 stock: Profit = $3.20/share × 7,500 = $2.4M gain (24% ROI)

- $75 CALL (Apr 17) at $75 stock: Breakeven to small loss

- Combined: +$2M to +$3M gain (13-19% return)

Why 20% probability: Requires approval with significant restrictions - possible but less likely given clean review process.

📉 Bear Case (15% probability)

Target: $40-50 (REJECTION SCENARIO)

Scenario 3: FDA Rejection or CRL

What could go wrong:

- ❌ FDA issues Complete Response Letter requiring additional data

- 😰 Unexpected safety concerns raised

- 💔 Manufacturing issues identified

- 📉 Stock crashes 30-50% to $40-50 range

- 🔨 Analyst downgrades cascade

- ⏰ Timeline pushed out 12-18 months

Call P&L in Bear Case:

- Both positions: -80% to -100% loss ($12M to $15.4M loss)

Probability assessment: Only 15% because approval odds are high (85-90%), clean review process, published NEJM data, and no additional FDA requests.

⏰ Delay Scenario (5% probability)

Target: $55-60 (UNEXPECTED DELAY)

Scenario 4: Unexpected Delay Beyond Dec 26

- 🚨 FDA announces PDUFA delay without explanation

- 📊 Stock volatile, likely drifts lower to $55-60

- $55 CALL (Jan 16): -50% to -80% loss (expires before resolution)

- $75 CALL (Apr 17): -40% to -60% loss

- Combined: -$7M to -$11M loss (45-70% loss)

Probability-Weighted Expected Return: (0.60 × +110%) + (0.20 × +16%) + (0.15 × -90%) + (0.05 × -57.5%) = +76% expected return

💡 Trading Ideas

🛡️ Conservative: Wait for Post-FDA Reaction

Play: Stay on sidelines until AFTER December 26th FDA decision settles

Why this works:

- ⏰ Binary event risk with unpredictable short-term price action

- 📊 If approved with strong label: Buy $75-80 CALL (Mar-Apr) for commercial momentum play

- 💸 If rejected: Wait for stabilization, potentially sell puts at support

- 🎯 Deploy capital with perfect information vs. gambling on binary outcome

Action plan:

- 👀 Watch December 26th FDA announcement closely

- 📈 If approval: Enter within 48 hours targeting commercial execution phase

- 📉 If rejection: Wait 1-2 weeks for dust to settle, reassess thesis

- 💰 Preserve capital, avoid 100% loss risk

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

⚖️ Balanced: Risk-Defined Call Spread

Play: Buy call spread to capture upside to analyst price targets while limiting risk

Structure: Buy $65 CALL / Sell $85 CALL (February expiry)

Why this works:

- 📊 Max risk: ~$5-7 per spread ($500-700 per contract)

- 🎯 Max reward: ~$13-15 per spread (100-150% return if stock reaches $85)

- ✅ Captures upside to analyst consensus price targets ($78-83)

- 🛡️ Defined risk structure protects against binary downside

- ⏰ February expiry captures FDA decision plus initial reaction

Estimated P&L:

- 💰 Max profit: $1,300-1,500 if CYTK above $85 at expiration

- 📉 Max loss: $500-700 (limited to premium paid)

- 🎯 Breakeven: ~$70-72

Position sizing: Risk only 2-5% of portfolio

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

🚀 Aggressive: Copy The Institutional Play (SPECULATIVE!)

Play: Replicate the January $55 ITM calls for high-probability pre-FDA play

Structure: Buy $55 calls expiring January 16

Why this could work:

- 🐋 "Following smart money" - someone with $15.4M sees value here

- 💥 FDA approval odds are REAL (85-90% analyst consensus)

- 📊 ITM positioning provides high delta exposure with lower risk than OTM

- 🎯 Expires 21 days before FDA, capturing anticipation rally

- ⏰ 44 days provides cushion for position to work

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Calls cost ~$13.80 ($1,380 per contract)

- ⏰ Timing risk: Expires BEFORE FDA decision - need strong pre-PDUFA rally

- 😱 Theta decay: Burns ~$30-40 per contract per day

- 💀 Total loss risk: If stock consolidates or drifts lower, lose entire premium

- 🎰 Exit timing critical: Must close by early January or risk missing FDA decision

Estimated P&L:

- 💰 Cost: ~$13.80 per call ($1,380 per contract)

- 📈 Profit scenario: Stock at $75 by Jan 16 = $6.20 profit (45% ROI)

- 🚀 Home run: Stock at $85 by Jan 16 = $16.20 profit (117% ROI)

- 📉 Loss scenario: Stock at $65 by Jan 16 = -$3.80 loss (28% loss)

- 💀 Total loss: Stock below $55 by Jan 16 = -$13.80 loss (100% wipeout)

Breakeven point: $68.80 (6% rally from current $65)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand binary biotech event risk and can afford total loss

- ✅ Have clear exit plan (e.g., sell 50% at 50% gain, let rest run)

- ✅ Can monitor daily and make quick decisions on exit timing

- ⏰ Accept that position expires BEFORE FDA decision

- 💰 Size at 2-5% of portfolio MAX

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~60% (if FDA approval odds hold and anticipation rally materializes)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🎰 Binary Event Risk is EVERYTHING: This is an all-or-nothing FDA approval play. 10-15% rejection probability means REAL chance of 30-50% stock decline and 70-100% options loss. The $15.4M institutional bet signals confidence, but even sophisticated players get FDA binary events wrong. Only risk capital you can afford to lose entirely.

-

📅 January Calls Expire BEFORE FDA Decision: The $55 Jan 16 calls expire 21 days before December 26th PDUFA date! This requires STRONG anticipation rally in late December/early January to profit. If stock consolidates around $65-70 through January expiration, these ITM calls could still lose money despite being "right" on FDA approval thesis.

-

💸 Already-Elevated Valuation: Stock up 69% in 3 months - significant approval expectation already priced in. $7.77B market cap vs. zero revenue (pre-commercial). If approval comes with in-line label (not superior vs. Camzyos), limited upside. Market may have front-run too much of the good news.

-

🏛️ Camzyos Entrenchment Risk: Bristol Myers has 2+ year first-mover advantage with established physician relationships and payer coverage. Switching inertia may limit market share capture below 50% expectations. BMS's massive sales/marketing budget advantage could slow CYTK's penetration.

-

📊 Commercial Execution Risk: Cytokinetics building infrastructure from scratch vs. established BMS capabilities. Payer coverage decisions uncertain despite Camzyos precedent. Manufacturing scale-up issues could cede early market share to entrenched competitor.

-

💰 Cash Burn Pressure: $130-140M quarterly burn rate accelerates with commercial launch. If launch disappoints, may need dilutive financing by 2026-2027. Operating expenses guided to $680-700M for 2025 - runway depends on execution.

-

🚨 Insider Selling Signal: 53 insider sales with 0 purchases over past year raises questions. Could indicate executives securing liquidity ahead of binary risk rather than confidence in approval.

-

🎢 Extreme Volatility: $13.80 premium on $65 stock = 21% of stock price! This reflects market's expectation of MASSIVE volatility. Theta decay burns approximately $30-40/day on these calls.

🎯 The Bottom Line

Real talk: Institutional money just bet $15.4 MILLION that Cytokinetics gets FDA approval on December 26th and becomes the next blockbuster cardiovascular drug. This sophisticated two-tranche structure ($10M ITM Jan calls + $5.4M OTM Apr calls) demonstrates institutional-grade risk management.

What this trade tells us:

- 🎯 Z-scores of 7.67 and 432.57 signal EXTREME institutional conviction - this is not retail speculation

- ✅ Staggered expirations de-risk timing uncertainty while maintaining asymmetric upside

- 💪 85-90% FDA approval probability + differentiated product profile + $1.5-3.0B peak sales opportunity

- ⚠️ BUT 10-15% rejection risk means real chance of 70-100% loss on positions

- 📊 Probability-weighted expected return: +76% based on scenario analysis

This trade warrants SERIOUS ATTENTION from options traders with appropriate risk tolerance for binary biotech catalysts.

If you're considering playing this:

- 🎯 The Jan $55 ITM calls are high-probability positioning BUT expire BEFORE FDA decision

- 💰 The Apr $75 OTM calls capture full commercial momentum IF approval is strong

- ⚠️ Only allocate 2-5% of portfolio maximum - this is SPECULATION, not investment

- 📊 Have exit plan BEFORE entering: Take profits at 50-100% gain rather than holding for max

- ⏰ Monitor December 20-23 for "whisper number" sentiment on trading desks

If you're on the sidelines:

- ⏰ December 26th FDA decision is THE catalyst - wait for reaction before committing

- 📈 If approval with strong label: Enter within 48 hours targeting $80-95 move

- 📉 If rejection: Wait for stabilization around $40-45 before reassessing

- 🛡️ Consider risk-defined call spreads vs. naked long calls

Mark your calendar - Key dates:

- 📅 December 19 (Thursday) - Monthly OPEX (implied range $59-$73)

- 📅 December 20-23 - Pre-PDUFA "whisper number" sentiment period

- 📅 December 26 (Thursday) - FDA PDUFA DECISION (THE BIG DAY!)

- 📅 December 27-30 - Initial analyst label analysis and price target revisions

- 📅 January 16, 2026 (Friday) - Monthly OPEX, $10M call expiration

- 📅 February 27, 2025 - Q4 earnings report and management commentary

- 📅 April 17, 2026 (Friday) - $5.4M call expiration

Final verdict: The institutional scale, timing sophistication, and extreme statistical anomalies (Z-scores 7.67 and 432.57) suggest access to positive signals not yet public. However, all-or-nothing binary risk makes this suitable ONLY for experienced traders with strong conviction in FDA approval.

For retail investors: Consider risk-defined alternatives like call spreads or waiting for post-PDUFA reactive strategies rather than replicating the naked long call structure.

Be smart. Size appropriately. Use defined risk. This is biotech binary event trading at its purest form - high conviction, high risk, high potential reward. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational and informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Past performance does not guarantee future results. Binary event options (like FDA approvals) can result in total loss of invested capital. Cytokinetics is a pre-revenue biotech company with concentrated risk in a single FDA approval decision. The options analyzed in this report carry high risk of total loss if FDA rejects aficamten's New Drug Application. Always conduct your own due diligence and consult with a licensed financial advisor before making investment decisions.

About Cytokinetics, Incorporated: Cytokinetics is a late-stage specialty cardiovascular biopharmaceutical company focused on discovering, developing, and commercializing muscle biology-directed drug candidates as potential treatments for debilitating diseases in which cardiac muscle performance is compromised, with a market cap of $7.77 billion in the Biotechnology industry.