💊 CYTK $2.7M Call Close - Big Money Cashes Out Before Major Clinical Trial Readout!

📅 March 3, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just closed a $2.7 MILLION long call position in Cytokinetics at the $70 strike expiring May 15th - buying to close 3,000 contracts while the stock trades at ~$61. This is a highly unusual trade (Z-Score: 2.4) that suggests a large player is locking in profits or cutting bait ahead of the make-or-break ACACIA-HCM Phase 3 readout expected in Q2 2026. With the stock down ~12% from its December highs after a post-earnings slide, this exit is worth paying attention to.

📊 Company Overview

Cytokinetics, Inc. (CYTK) is a late-stage biopharmaceutical company focused on muscle-directed therapies for cardiovascular and neuromuscular diseases:

- Market Cap: $7.5B

- Industry: Pharmaceutical Preparations (SIC: 2834)

- Exchange: NASDAQ

- Current Price: ~$61 (down ~14% from 52-week high of $70.98)

- Employees: 498

- HQ: South San Francisco, CA

- Primary Product: MYQORZO (aficamten) - FDA-approved December 2025 for obstructive hypertrophic cardiomyopathy (oHCM), a cardiac myosin inhibitor competing against Bristol Myers Squibb's CAMZYOS

💰 The Option Flow Breakdown

The Tape (March 3, 2026 @ 11:16:39):

| Time | Symbol | Side | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|

| 11:16:39 | CYTK | -- | BUY | CALL | 2026-05-15 | $2.7M | $70 | 3,000 | CYTK20260515C70 |

🤓 What This Actually Means

This is a buy-to-close (BTC) trade - someone who was already long these $70 calls is closing out the position. Here's the breakdown:

- 💸 Total cost to close: $2.7M ($9.00 per contract x 3,000 contracts)

- 🎯 Out-of-the-money: The $70 strike is ~$9 above the current stock price of ~$61, meaning these calls have no intrinsic value - it's all time value and hope

- ⏰ 73 days to expiration: May 15 lines up perfectly with the expected Q2 ACACIA-HCM Phase 3 data readout

- 📊 Position size: 3,000 contracts = 300,000 shares worth ~$18.3M notional

- 🏦 Vol/OI ratio: 0.326 (moderate activity level)

What's really happening here:

This trader originally bet big on $CYTK reaching $70+ by mid-May - likely positioning for the ACACIA-HCM catalyst or the commercial launch momentum. Now they're closing that bet. Why? A few possibilities:

- 📈 Profit-taking: They may have entered when the stock was lower (it traded near $30 a year ago) and are locking in gains even though the calls are currently out of the money

- 🔄 Repositioning: They might be rolling into a different strike or expiration to better align with the catalyst timeline

- 😰 Reducing risk: After the 10% post-earnings drop in late February, they may be cutting exposure before the binary ACACIA-HCM event

Unusual Score: 🔥 HIGHLY UNUSUAL (Z-Score: 2.4) - A trade like this shows up only a handful of times per quarter. The $2.7M clip and BTC classification confirm this is an institutional-level position unwind, not retail noise.

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

$CYTK has had a volatile ride in 2026. After peaking near $70 in late December following the FDA approval of MYQORZO, the stock pulled back sharply. The Q4 earnings miss in late February triggered another 10% slide, dragging the stock into the low $60s.

Key observations:

- 📉 Trading below the 50-day SMA ($64.12): Short-term momentum is bearish

- 📈 Holding above the 200-day SMA ($59.07): Longer-term trend still intact

- 🎢 52-week range: $29.31 - $70.98: Stock is sitting right in the middle of its range

- 💹 $60 psychological support: The round number has been holding so far

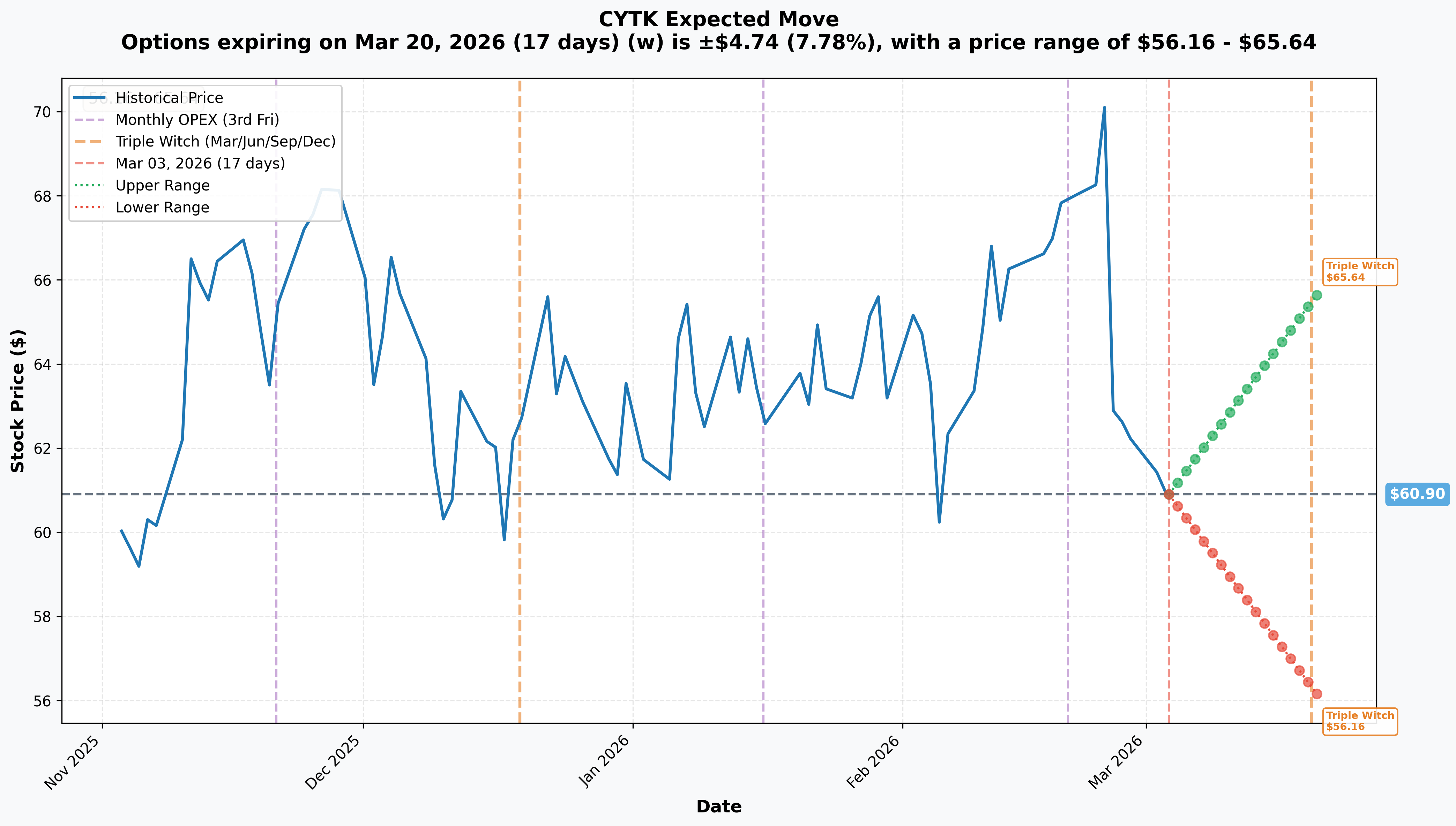

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Monthly OPEX / Triple Witch (March 20 - 17 days): +/-$4.74 (+/-7.78%) --> Range: $56.16 - $65.64

Translation for regular folks:

Options traders are pricing in a 7.78% move (~$4.74) through March expiration. That's pretty spicy for a $7.5B biotech - the market expects $CYTK to trade roughly between $56 and $66 over the next two and a half weeks. For context, that 7.78% implied move is well above what you'd see for a typical large-cap stock, reflecting the elevated uncertainty around the commercial launch ramp and upcoming clinical catalysts.

For the $70 strike on the closed trade, the stock would need to rally ~15% from current levels by May 15 to reach the strike. That's a tall order in the near term, but the ACACIA-HCM readout could absolutely move the stock that much - in either direction.

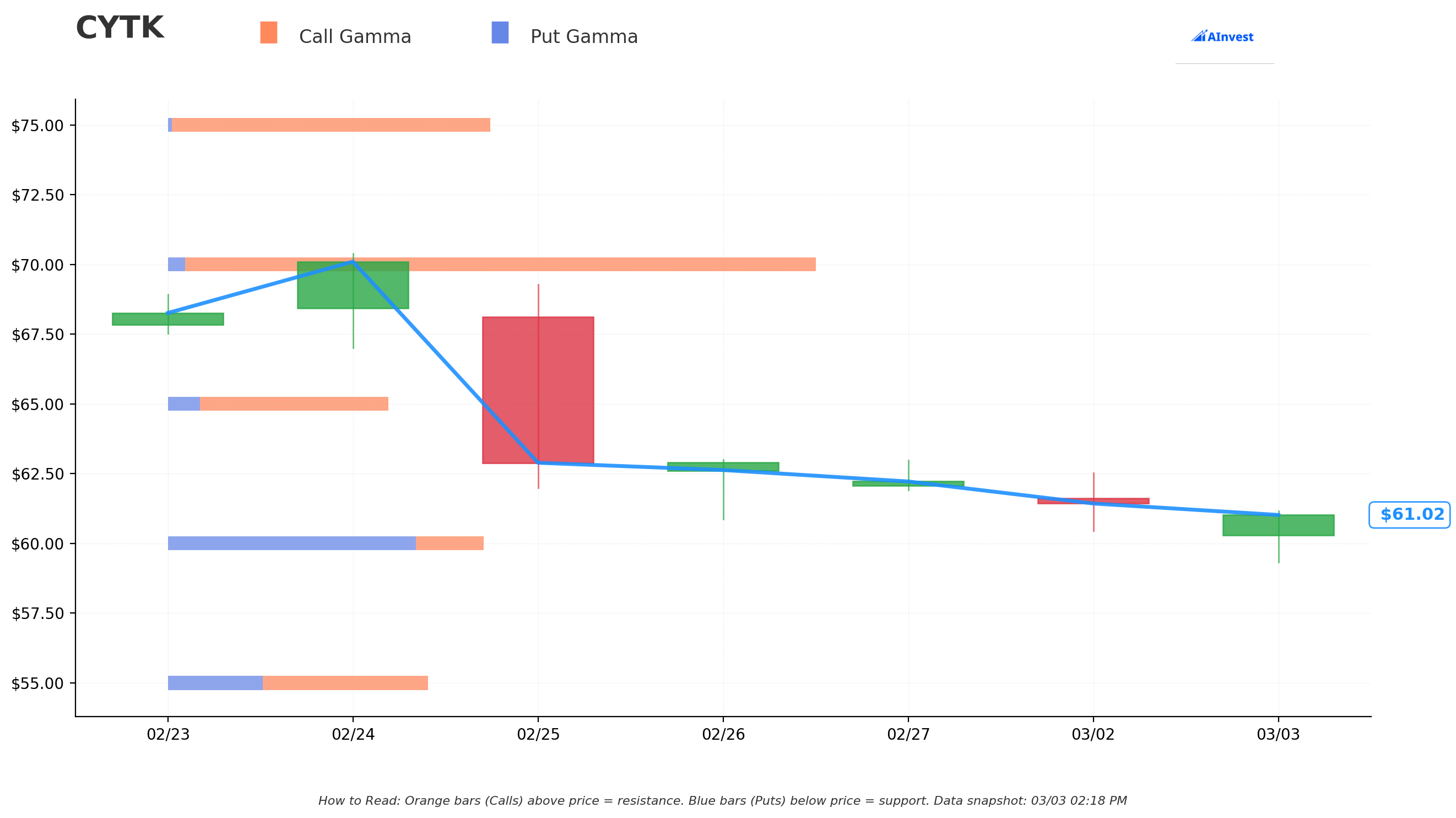

Gamma-Based Support & Resistance Analysis

Key gamma levels from options positioning:

The gamma exposure data shows elevated open interest clustering at several key strikes. While net GEX values are neutral (common in biotech names where positioning is heavily skewed by event-driven trading), the strike clustering tells us where the action is concentrated:

🔵 Support Levels:

- $55 - Significant gamma concentration; this level would represent a ~10% decline and lines up with a major selloff scenario

- $50 - Heavy gamma level below; worst-case floor where put protection is concentrated

- $56.16 - Implied move lower bound for March OPEX

🟠 Resistance Levels:

- $65.64 - Implied move upper bound for March OPEX

- $70 - The strike on today's big trade; also near the 52-week high ($70.98) and a massive psychological barrier

- $75-$80 - Higher gamma levels where call OI starts to cluster; would require a major catalyst to reach

- $90 - Maximum gamma strike; the bull-case dream target if ACACIA-HCM data is a home run

What this means for traders: The $55-$70 range captures the vast majority of near-term options positioning. The $70 strike is a clear ceiling from both a technical standpoint (52-week high) and an options standpoint (heavy OI). A breakout above $70 would likely trigger significant dealer hedging flows and short covering. On the downside, $55-$56 represents a strong floor backed by both put gamma and the implied move lower bound.

🎪 Catalysts

🔥 Upcoming Catalysts

March 9-11 - Investor Conference Blitz 📊

Cytokinetics is hitting four investor conferences in Miami Beach in a single week:

- 📅 March 9: Leerink 2026 Global Healthcare Conference

- 📅 March 10: Citizens 2026 Life Sciences Conference

- 📅 March 11: Jefferies Biotech on the Beach Summit

- 📅 March 11: Barclays 28th Annual Global Healthcare Conference

These could be the first public updates on MYQORZO prescription trends and launch trajectory. Watch for any hints about early sales momentum.

May 6 - Q1 2026 Earnings (Expected) 💰

This will be the first quarter with meaningful MYQORZO product sales data since the drug launched January 27. Key metrics to watch:

- 📊 Number of prescriptions filled

- 🏥 Unique prescribers

- 💸 Payer coverage rates

- 📈 Revenue trajectory vs. CAMZYOS's ~$53M in its first four full quarters

Q2 2026 - ACACIA-HCM Phase 3 Topline Results 🧬

This is the big one. The ACACIA-HCM trial is testing aficamten in non-obstructive HCM (nHCM), which has roughly twice as many patients as the obstructive form. With 500+ patients enrolled, this trial has dual primary endpoints: change in KCCQ Clinical Summary Score AND change in peak VO2.

- ✅ If positive: Could double the addressable market for MYQORZO - a potential multi-billion-dollar expansion

- ❌ If negative/mixed: Would limit aficamten to oHCM only and remove a huge chunk of the bull case

Q2 2026 - Germany/EU Commercial Launch 🌍

The European Commission approved MYQORZO on February 17, with Germany launch planned for Q2 2026. This opens up the world's second-largest pharma market.

⏪ Recent Catalysts (Already Happened)

December 19, 2025 - FDA Approval of MYQORZO 🎉

The FDA approved MYQORZO for adults with symptomatic oHCM - Cytokinetics' first ever commercial product. Stock rallied to near $71.

January 27, 2026 - U.S. Commercial Launch 💊

MYQORZO became available for prescription in the U.S. First scripts were dispensed within days.

December 17, 2025 - China Approval 🇨🇳

China's NMPA approved MYQORZO for oHCM, triggering a $7.5M milestone from Sanofi.

February 17, 2026 - EU Approval 🇪🇺

European Commission approval completed the global regulatory "triple crown" across U.S., China, and Europe.

February 24, 2026 - Q4 Earnings Miss 📉

Q4 revenue of $17.8M beat estimates ($6.9M expected), but EPS of -$1.50 missed by $0.02. The widening loss and lack of MYQORZO sales guidance caused a ~10% selloff.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, analyst targets, and the catalyst calendar:

📈 Bull Case (25% probability)

Target: $80-$100

How we get there:

- 🧬 ACACIA-HCM Phase 3 hits both primary endpoints - market re-rates $CYTK for the doubled addressable market opportunity

- 💊 March investor conferences reveal strong early MYQORZO prescription trends that exceed CAMZYOS's launch trajectory

- 📊 Q1 earnings show first meaningful product revenue, beating even the most optimistic estimates

- 🌍 Germany launch gains early traction, proving European demand

- 📈 Average analyst target of ~$89-$91 gets pulled higher as the ACACIA bull case gets priced in; B. Riley's $108 target becomes consensus

- 💪 Stock breaks above the $70 resistance / 52-week high, triggering momentum buying through the $75-$90 gamma levels

Key risk to bulls: ACACIA-HCM uses dual primary endpoints (KCCQ + peak VO2), which raises the bar for a clean win. Mixed results could leave the stock stuck.

🎯 Base Case (50% probability)

Target: $56-$70 range-bound

Most likely scenario:

- ✅ March conferences provide encouraging but not game-changing MYQORZO updates

- 📊 Q1 earnings show modest but growing prescription volumes, in line with typical specialty drug ramp

- 🔬 ACACIA-HCM readout hasn't dropped yet, keeping the stock in "wait and see" mode

- ⚖️ Stock oscillates between the implied move bounds ($56-$66 near-term) with occasional forays toward $70

- 📉 The 50-day SMA at $64 acts as overhead resistance until the catalyst resolves

What this means: The $70 call position that was just closed would expire worthless in this scenario, validating the decision to take the exit now rather than wait for the binary event.

📉 Bear Case (25% probability)

Target: $40-$55

What could go wrong:

- 😰 ACACIA-HCM fails to meet one or both primary endpoints - the non-obstructive HCM expansion is dead, removing a huge pillar of the valuation

- 💸 MYQORZO launch underwhelms - CAMZYOS has a 3+ year head start with $1B+ annual revenue and entrenched payer relationships

- 📉 Cash burn continues at >$500M/year with only ~$1.22B in reserves - financing concerns emerge

- ⚖️ The pending securities fraud class action creates settlement risk

- 🏦 Insider selling accelerates - recent sales of 121K shares worth $7.8M in the last 90 days is worth noting

- 📉 Stock drops through the $55 gamma support and $50 level, revisiting the $40-$45 zone seen in mid-2025

Impact on today's trade: The trader who closed the $70 calls would be vindicated - exiting before a potential wipeout on the binary event saved them from a total loss on the position.

💡 Trading Ideas

🛡️ Conservative: The "Wait for the Data" Bull Put Spread

Play: Sell a put spread below the implied move floor to collect premium while waiting for the ACACIA-HCM catalyst

Structure: Sell May 15 $55 puts / Buy May 15 $50 puts

Why this works:

- 💰 Collect ~$0.80-$1.20 per spread (~16-24% of width)

- 📊 $55 support is backed by gamma levels and is ~10% below current price

- 🛡️ Defined risk: Max loss $5 per spread minus premium collected

- ⏰ If ACACIA-HCM is positive (or even just neutral), the stock stays well above $55

- 📉 You'd need the stock to drop 10%+ AND the data to fail for this to lose

- 🏦 17 of 21 analysts have Buy ratings with an average target ~45% above current price

Estimated P&L:

- 💰 Max profit: ~$80-$120 per spread if $CYTK stays above $55

- 📉 Max loss: ~$380-$420 per spread if $CYTK below $50 at expiration

- 🎯 Breakeven: ~$53.80-$54.20

Risk level: Low-Moderate (defined risk, cushion to downside) | Skill level: Beginner-friendly

⚖️ Balanced: The "Catalyst Straddle" Long Volatility Play

Play: Buy a straddle to profit from a big move in either direction around the ACACIA-HCM readout

Structure: Buy May 15 $60 calls + Buy May 15 $60 puts

Why this works:

- 🧬 ACACIA-HCM is a genuine binary event - positive results could send $CYTK to $80+, while failure could tank it to $45

- 📊 The current implied move of 7.78% for March OPEX understates the potential move from the clinical readout

- 🎢 You're paying for volatility, but this is a name where the volatility is real and imminent

- 💡 You don't need to pick a direction - just need a big move

Why this could go wrong:

- ⏰ If the ACACIA-HCM readout is delayed past May 15, time decay eats both legs alive

- 💸 Straddles are expensive - you need the stock to move beyond the breakeven range to profit

- 📉 If the stock drifts sideways through Q1 earnings without a readout, both legs decay

Estimated P&L:

- 💰 Cost:

$8-$10 per straddle ($800-$1,000 per position) - 📈 Upside breakeven: ~$68-$70 (where the closed calls were struck!)

- 📉 Downside breakeven: ~$50-$52

- 🎯 Sweet spot: Stock moves violently in either direction on ACACIA data

Risk level: Moderate (defined risk, high premium cost) | Skill level: Intermediate

🚀 Aggressive: The "Double Down on ACACIA" Call Spread

Play: Buy a call spread targeting the analyst consensus price zone if ACACIA-HCM delivers positive results

Structure: Buy May 15 $65 calls / Sell May 15 $80 calls

Why this works:

- 🧬 If ACACIA-HCM hits, the stock likely gaps above $70 and runs toward analyst targets of $84-$108

- 📊 The $80 short call captures the first major gamma resistance level above

- 💰 Net debit ~$2.50-$3.50 per spread for a $15 wide spread - risk/reward up to 3:1 to 5:1

- 📈 The trader who just closed their $70 calls essentially handed you the baton - you're picking up where they left off but with a defined-risk structure

- 🌍 Q1 earnings + EU launch provide additional upside catalysts before expiration

Why this could go wrong:

- 💥 ACACIA-HCM fails - the calls go to zero and you lose the full debit

- ⏰ Readout comes after May 15 expiration, leaving you with time-decayed out-of-the-money calls

- 📉 Stock continues drifting lower post-earnings, never reaching the $65 strike

Estimated P&L:

- 💰 Max risk: ~$250-$350 per spread (net debit paid)

- 📈 Max profit: ~$1,150-$1,250 per spread if $CYTK at or above $80 at expiration

- 🎯 Breakeven: ~$67.50-$68.50

- 💪 If the stock hits the average analyst target of $89, you capture the full $15 spread width

Risk level: High (binary event dependent) | Skill level: Intermediate-Advanced

⚠️ Risk Factors

Don't sleep on these potential landmines:

-

🧬 ACACIA-HCM trial failure: This is the elephant in the room. The trial uses dual primary endpoints (KCCQ Clinical Summary Score AND peak VO2), which raises the bar for a clean win. If either endpoint misses, the non-obstructive HCM market expansion evaporates, and the stock could easily give back 30-40%.

-

💸 Cash burn is real: Cytokinetics burned $510M in operating cash outflows in 2025 with guided expenses of $830M-$870M for 2026. At $1.22B in cash, the company has roughly 18-24 months of runway. If MYQORZO sales ramp slowly, financing concerns could weigh on the stock.

-

🏥 CAMZYOS is a formidable competitor: Bristol Myers Squibb's CAMZYOS generated over $1B in full-year 2025 revenue with a 3+ year head start. Entrenched payer contracts, physician familiarity, and real-world outcomes data create significant switching barriers. BMS also recently won a pediatric indication, adding competitive pressure.

-

🏦 Insider selling pattern: Directors and executives have sold 121,171 shares worth $7.8M in the last 90 days, including sales by a director just yesterday. While this could be routine diversification, the timing around the commercial launch is worth watching.

-

⚖️ Securities fraud class action: A class action lawsuit alleging misleading statements about the aficamten NDA timeline is pending. While outcomes are uncertain, settlement or adverse rulings could create unexpected headwinds.

-

📊 No revenue guidance = uncertainty: Management declined to provide MYQORZO revenue guidance for 2026. Without a revenue target, the street is flying blind on launch trajectory expectations, which creates conditions for disappointment in either direction.

-

🌍 Biotech sector headwinds: The broader biotech sector faces FDA policy uncertainty and risk-off sentiment in early 2026. Pre-profitability biotechs like CYTK are particularly sensitive to macro shifts and interest rate expectations.

🎯 The Bottom Line

Real talk: A large institutional player just closed out $2.7M in $CYTK $70 calls, and this trade speaks volumes about how big money is thinking about the risk/reward heading into the ACACIA-HCM readout. This isn't someone panicking - the BTC on a HIGHLY UNUSUAL z-score of 2.4 suggests deliberate, calculated profit-taking or risk reduction by a sophisticated player who's been in this name.

What this trade tells us:

- 🎯 An institutional player doesn't think $CYTK reaches $70 by mid-May - or at least isn't willing to hold through the binary catalyst to find out

- 💰 The $70 strike aligns perfectly with the 52-week high ($70.98) and represents a major psychological and technical resistance level

- ⚖️ Closing before the ACACIA-HCM readout suggests this trader may be recycling into a different position with a better risk profile for the binary event

- 📊 The timing matters: the stock is ~14% below its recent highs, and someone chose to take whatever value remained rather than gamble on the trial

If you own CYTK:

- ✅ The fundamental story is intact - 17 out of 21 analysts rate it Buy with a consensus target of ~$89-$91, implying 45%+ upside

- 📊 Watch the March conferences (March 9-11) for early MYQORZO prescription color - this could move the stock before earnings

- 🛡️ Consider protective puts or collars to manage risk through the ACACIA-HCM binary event

- ⏰ Q1 earnings (~May 6) will be the first real report card on MYQORZO sales - set your expectations carefully

If you're watching from the sidelines:

- 🎯 A pullback to $56 (implied move lower bound) or $55 (gamma support) would be an attractive entry ahead of the ACACIA catalyst

- 📊 Wait for March conference updates on prescriptions before initiating a large position

- 💡 The global "triple crown" of approvals in the U.S., China, and EU gives MYQORZO a global launchpad that CAMZYOS took years to build

If you're bearish:

- 📉 The $785M annual net loss and no revenue guidance are legitimate concerns

- 🏦 The insider selling pattern and today's institutional call exit are potential warning signs

- ⚠️ Bear put spreads ($60/$50) offer defined-risk downside plays if ACACIA disappoints

- ⏰ Shorting into a binary clinical readout is dangerous - use defined-risk options strategies instead

Mark your calendar - Key dates:

- 📅 March 9-11 - Four investor conferences in Miami Beach (early MYQORZO launch data)

- 📅 March 20 - Triple Witch OPEX (implied range: $56.16-$65.64)

- 📅 ~May 6 - Q1 2026 earnings (first quarter with MYQORZO product sales)

- 📅 May 15 - Expiration of today's closed $70 call trade

- 📅 Q2 2026 - ACACIA-HCM Phase 3 topline results (THE catalyst)

- 📅 Q2 2026 - Germany/EU commercial launch of MYQORZO

Final verdict: The $2.7M call close tells us one thing clearly - even big believers in $CYTK are de-risking ahead of the ACACIA-HCM binary event. The stock is caught between a powerful bull case (global drug launch + potential market-doubling trial data + 45% analyst upside) and a real bear case (massive cash burn + no revenue guidance + entrenched competitor). If you're trading this name, use defined-risk options strategies that account for both outcomes. The ACACIA readout will resolve the debate one way or another - just make sure you're positioned to survive whichever way it breaks.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-Score of 2.4 reflects this specific trade's unusualness relative to recent activity - it does not imply the trade will be profitable or that you should follow it. CYTK is a pre-profitability biotech company with elevated binary risk from clinical trial outcomes. Always do your own research and consider consulting a licensed financial advisor before trading.

About Cytokinetics, Inc.: Cytokinetics is a $7.5B late-stage biopharmaceutical company focused on muscle-directed therapies. Its first commercial product, MYQORZO (aficamten), was FDA-approved in December 2025 for obstructive hypertrophic cardiomyopathy (oHCM), with additional approvals in China and Europe. The company is also advancing pipeline programs in non-obstructive HCM (ACACIA-HCM trial) and heart failure (omecamtiv mecarbil, COMET-HF trial).