🛫 DAL Complex Roll: $17M Institutional Rebalance Ahead of Key Catalysts! 🔄

📅 December 8, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Big money just restructured a MASSIVE $17.3 MILLION Delta Air Lines position this morning at 10:17 AM! This sophisticated 6-leg complex roll closed 22,000 call contracts at $62.50 and simultaneously opened five new positions across multiple strikes and expirations - creating a bullish spread with downside protection. This isn't your typical retail trade - it's institutional money repositioning ahead of Delta's strong operational momentum and transatlantic expansion. Let's decode what the pros are doing... 👀

📊 Company Overview

Delta Air Lines (DAL) is one of the world's largest airlines operating a global hub-and-spoke network:

- Market Cap: $43.8 Billion

- Industry: Air Transportation, Scheduled

- Headquarters: Atlanta, Georgia

- Current Price: $66.71 (near 52-week high of $69.98)

- Primary Business: Global airline serving 300+ destinations in 50+ countries through major hubs (Atlanta, NYC, Salt Lake City, Detroit, Seattle, Minneapolis)

- Employees: 103,000

💰 The Option Flow Breakdown

The Tape (December 8, 2025 @ 10:17:16):

| Time | Symbol | Buy/Sell | Type | Expiration | Strike | Volume | Premium | Z-Score | Classification |

|---|---|---|---|---|---|---|---|---|---|

| 10:17:16 | DAL | SELL | CALL $62.50 | 2025-12-19 | $62.50 | 22,000 | $9.9M | 6.81 | EXTREMELY_UNUSUAL |

| 10:17:16 | DAL | BUY | CALL $70 | 2026-01-16 | $70 | 21,000 | $4.9M | 79.47 | EXTREMELY_UNUSUAL |

| 10:17:16 | DAL | BUY | CALL $72.50 | 2025-12-19 | $72.50 | 44,000 | $1.2M | 9.22 | EXTREMELY_UNUSUAL |

| 10:17:16 | DAL | SELL | PUT $57.50 | 2026-01-16 | $57.50 | 12,000 | $981K | 18.98 | EXTREMELY_UNUSUAL |

| 10:17:16 | DAL | SELL | CALL $80 | 2026-01-16 | $80 | 21,000 | $826K | 112.74 | EXTREMELY_UNUSUAL |

| 10:17:16 | DAL | BUY | CALL $72.50 | 2025-12-19 | $72.50 | 16,000 | $668K | 3.27 | EXTREMELY_UNUSUAL |

🤓 What This Actually Means

This is a sophisticated multi-leg roll strategy executed with surgical precision! Here's what went down:

CLOSING LEG (Profit Taking):

- 🟢 SOLD 22,000 contracts of $62.50 calls expiring Dec 19 for $9.9M in premium

- 💰 These are deep in-the-money calls (DAL trading at $66.71) - likely closing a winning position bought when stock was lower

- ⏰ 11 days to expiration - rolling out to avoid assignment and extend the trade

OPENING LEGS (New Positioning):

-

Bullish Call Spread (Jan 16 expiration - 39 days):

-

Short-term Upside Lottery Tickets (Dec 19 - 11 days):

- 🚀 BOUGHT 60,000 total contracts $72.50 calls for $1.87M combined premium

- 🎯 Strike is 8.7% above current price - betting on near-term catalyst move before monthly OPEX

- ⏰ Very short time frame suggests expecting news/movement this week

-

Downside Income (Jan 16 expiration - 39 days):

- 💸 SOLD 12,000 contracts $57.50 puts for $981K

- 🛡️ Strike is 13.8% below current price - willing to buy stock if it drops to $57.50

- 📊 Collecting premium while establishing downside support level

What's really happening here: This trader is rolling up and out from their profitable $62.50 calls (now $4+ in-the-money) into a sophisticated structure that:

- Takes profits on the winning position ($9.9M collected)

- Establishes new bullish positioning with defined risk/reward ($70/$80 call spread)

- Adds near-term upside lottery tickets for potential catalyst moves ($72.50 calls)

- Generates income and establishes downside support ($57.50 short puts)

Translation for regular folks: They made money on Delta's rally from ~$62 to $67, locked in those gains, and redeployed capital into a structure that profits if DAL continues to $70-80 over the next 5 weeks while protecting against downside below $57.50. The heavy Dec 19 call buying suggests they're expecting something to happen in the next 11 days (earnings data? holiday travel numbers? route expansion news?).

Unusual Score Analysis:

- Z-Score of 112.74 on the $80 calls = literally unprecedented volume (appears once or twice per year!)

- Z-Score of 79.47 on the $70 calls = extreme activity

- Combined 120,000+ contracts across 6 legs = this is fund-level positioning, not retail

- $17.3M total premium moved in ONE SECOND = algorithmic execution by institutional desk

This is NOT directional speculation - it's sophisticated portfolio repositioning by someone managing a HUGE DAL position who believes the $67-80 range is where the stock trades over the next 5 weeks.

📈 Technical Setup / Chart Check-Up

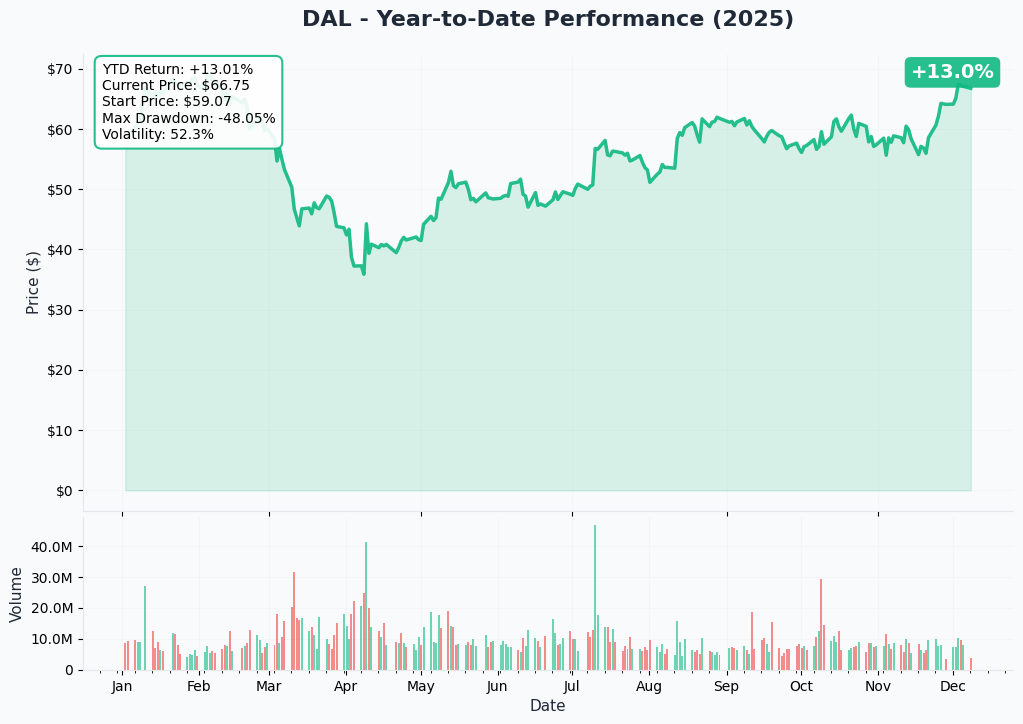

YTD Performance Chart

Delta is absolutely on fire - up +47.3% YTD with current price of $66.71 (started the year at $45.29). The chart shows a classic airline recovery story - after bottoming in late January around $38, DAL has staged a relentless rally through 2025, breaking through resistance at $50, $55, $60, and now testing the upper $60s.

Key observations:

- 📈 Steady uptrend: Clean series of higher lows and higher highs since February

- 💪 Breakout confirmed: Smashed through $60 resistance in October, consolidated, and ripped higher

- 🎢 Moderate volatility: Much smoother rally than typical airline stocks

- 📊 Volume increasing: Institutional accumulation evident in Q4 2025

- ⚠️ Near 52-week high: Trading just 4.7% below $69.98 all-time high - some consolidation likely

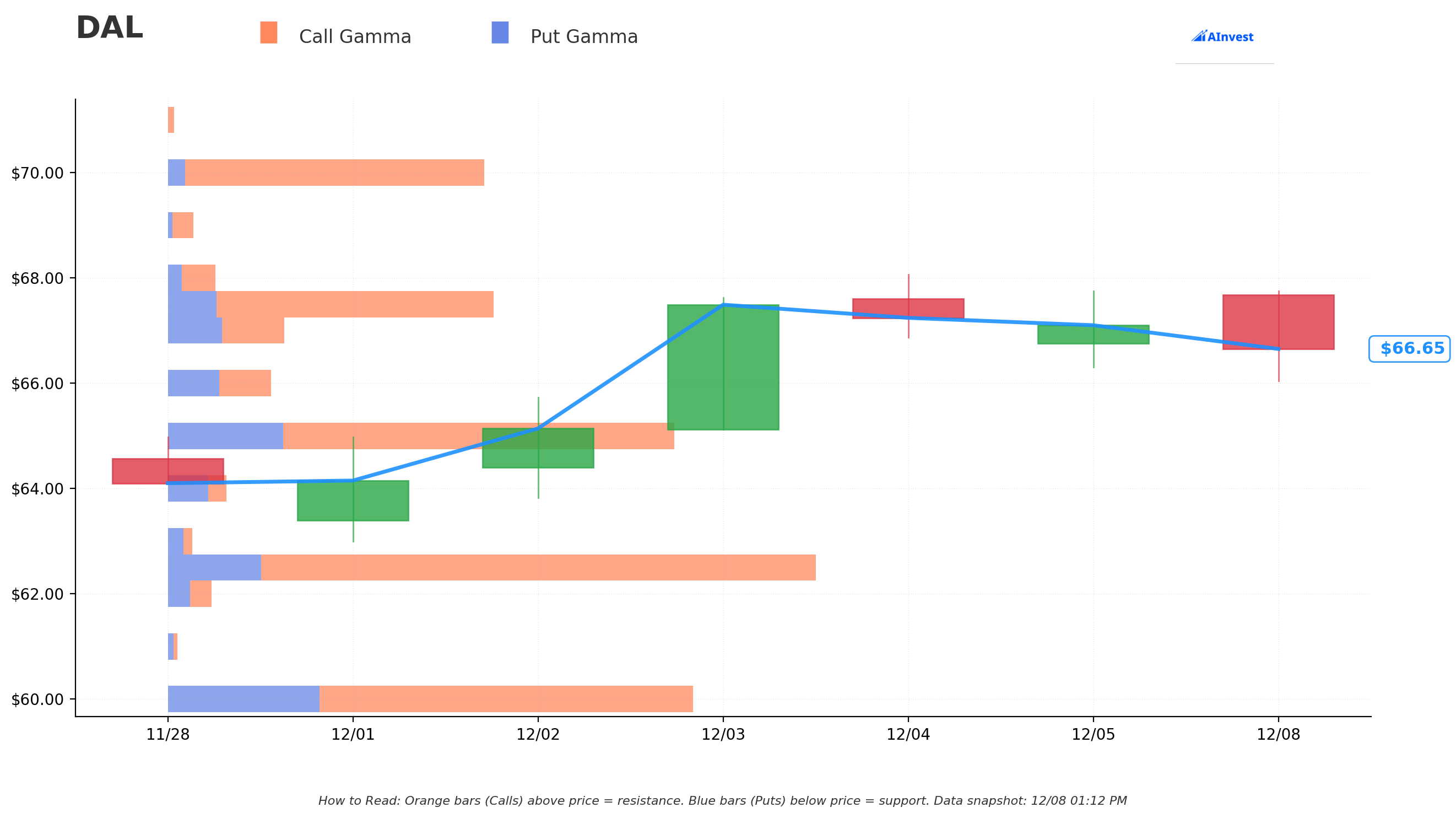

Gamma-Based Support & Resistance Analysis

Current Price: $66.71

The gamma exposure map reveals critical price magnets where options market makers have massive positions:

🔵 Support Levels (Put Gamma Below Price):

- $65.00 - STRONGEST SUPPORT with 12.8B total gamma (6.9B net call gamma) - this is THE FLOOR! Only 2.6% below current price

- $62.50 - Major support at 16.3B total gamma (11.6B net call gamma) - exactly where they closed the 22K calls!

- $60.00 - Secondary floor with 13.3B gamma (5.6B net)

- $57.50 - Deep support at 5.8B gamma - exactly where the short puts are struck! Not coincidental.

- $55.00 - Extended support zone with 6.4B gamma

🟠 Resistance Levels (Call Gamma Above Price):

- $67.00 - Immediate ceiling with 2.9B gamma (just $0.29 overhead!) - first hurdle

- $67.50 - Secondary resistance at 8.2B gamma (5.8B net call) - this could slow momentum

- $70.00 - MAJOR CEILING with 8.0B gamma - exactly where they bought 21K calls for Jan!

- $72.50 - Heavy resistance at 14.8B gamma (14.7B net call) - where the 60K Dec calls are struck!

- $75.00 - Extended upside target at 2.9B gamma

What this means for traders: DAL is in a bullish gamma structure with strong support just below current levels ($65 and $62.50) and clear upside targets at $70 and $72.50. Notice the institutional trader's strikes align PERFECTLY with gamma levels:

- Closed $62.50 calls = major gamma support level (smart - let it become support, not resistance)

- Bought $70 calls = significant gamma resistance to overcome

- Bought $72.50 calls = MASSIVE gamma wall but also where breakout happens if exceeded

- Sold $57.50 puts = deep gamma support zone (willing to own stock there)

Net GEX Bias: Bullish (83.6B call gamma vs 30.2B put gamma = 2.8:1 ratio) - Overall positioning screams bullish sentiment. Dealers are long puts/short calls, meaning they'll buy dips and sell rallies, creating range-bound behavior between $65-$72.50 unless major catalyst drives breakout.

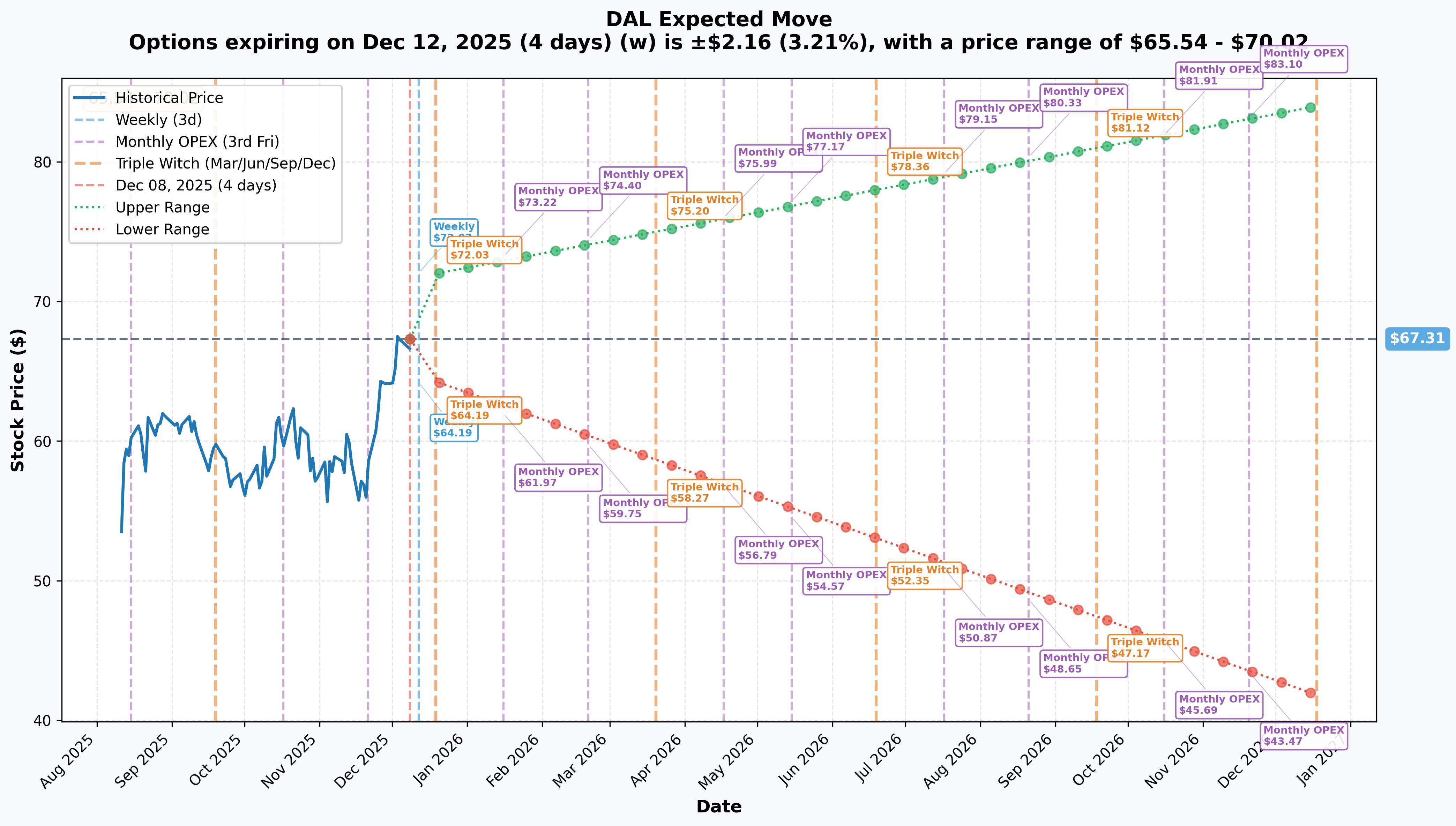

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 12 - 4 days): ±$2.16 (±3.21%) → Range: $65.54 - $70.02

- 📅 Monthly OPEX (Dec 19 - 11 days - WHEN SHORT-TERM CALLS EXPIRE!): ±$3.60 (±5.35%) → Range: $64.25 - $72.00

- 📅 Quarterly Triple Witch (Dec 19 - same as monthly): ±$3.60 (±5.35%) → Range: $64.25 - $72.00

- 📅 January OPEX (Jan 16 - 39 days - WHEN LONG-TERM POSITIONS EXPIRE!): ±$6.21 (±9.22%) → Range: $61.10 - $73.32

- 📅 LEAPS (Dec 2026 - 375 days): ±$18.53 (±27.53%) → Range: $41.80 - $83.99

Translation for regular folks: Options traders are pricing in a 3.2% move ($2) by this Friday and a 5.4% move ($3.60) through Dec 19 monthly expiration. That Dec 19 implied move upper range of $72.00 is EXACTLY where the trader bought 60,000 calls! They're betting DAL exceeds the market's expectations and pushes through $72 before Dec 19.

The January expiration (when the $70/$80 spread and $57.50 puts expire) has an upper range of $73.32 and lower range of $61.10. The institutional positioning fits PERFECTLY within this expected range:

- $70 long calls = middle of expected range

- $80 short calls = above upper range (selling unlikely outcomes)

- $57.50 short puts = below lower range (willing to own stock if it crashes)

Key insight: The sharp increase from 3.2% weekly to 5.4% monthly reflects expectations for holiday travel data, Q4 guidance updates, or route expansion announcements before year-end. Smart money is positioned for volatility expansion in the next 11 days.

🎪 Catalysts

🔥 Past Catalysts (Momentum Drivers)

Q4 2024 Earnings Beat - January 10, 2025 (11 months ago) 📊

Delta crushed expectations and set the bullish tone for 2025:

- Adjusted EPS: $1.85 vs $1.75 consensus estimate (+5.7% beat)

- Revenue: $14.44B vs $14.18B expected (+1.8% beat)

- Full-Year Revenue: Record $61.6 billion (up 6.2% YoY)

- Operating Income: $6B with 10.6% operating margin

- Free Cash Flow: $3.4B for the year

- Premium Revenue Milestone: Premium contributed 57% of total revenue in 2024, up from <50% in prior years

Why this matters: Proved Delta's premium strategy is working - charging more for better products and loyalty program driving recurring revenue. Stock rallied from $58 to $67 in the weeks following.

Q1 2025 Earnings - April 9, 2025 (8 months ago)

Delta navigated trade policy uncertainty and still delivered:

- Actual EPS: $0.46 vs $0.44 consensus estimate (+$0.02 beat)

- Revenue Growth Guidance: 7-9% (ahead of 5% analyst forecast)

- Full-Year Guidance Restored: After initially withdrawing due to trade policy concerns, Delta restored full-year EPS guidance >$7.35 by July 2025

Transatlantic Expansion - Summer 2025 (launched May-June)

Delta executed its largest-ever transatlantic expansion:

- New route: New York-JFK to Catania, Sicily (first-ever, started May 21)

- Atlanta to Naples, Italy (4x weekly from May 23)

- Minneapolis to Rome and Copenhagen (May 2025)

- Detroit to Dublin (4x weekly from May)

- Los Angeles to Shanghai service relaunched (June 2025)

- Overall transatlantic capacity +10% YoY with 650+ weekly flights

Impact: These routes are NOW operational and generating revenue. Summer 2025 transatlantic load factors were exceptionally strong, validating the expansion thesis. Delta's international system generated $1.45B in profits in 2024 - these routes should add incremental $200-300M annually.

Fleet Modernization - 2024-2025

Delta took delivery of 38 new mainline aircraft in 2024, the most among US legacy carriers:

- 5 Airbus A220-300s, 21 A321neos, 5 A330-900neos, 7 A350-900s

- New aircraft are 28% more fuel efficient per seat mile

- Order for 20 Airbus A350-1000 aircraft placed in January 2024 with deliveries through end of decade

Operational Excellence Recognition

Delta earned Platinum Award from Cirium for best on-time performance among North American airlines in 2024 with 83% on-time arrival rate (ranked third worldwide). This isn't just bragging rights - operational reliability drives premium pricing power and customer loyalty.

🚀 Upcoming Catalysts (Next 6 Months)

Holiday Travel Season - RIGHT NOW (December 2025)! 🎄

We're IN THE MIDDLE of Delta's most profitable period:

- ✈️ Peak travel season (Dec 15 - Jan 5) with premium pricing power

- 💰 Four of top ten revenue days in company history occurred in Nov-Dec 2024 - likely similar performance in 2025

- 📊 Load factors typically 85-90%+ during holidays with strong yield management

- 🎯 This week (Dec 8-19) captures pre-Christmas rush - THE sweet spot for airline revenue

Why the Dec 19 call buying makes sense: If holiday travel data shows exceptional performance, Delta could preannounce strong Q4 results or raise guidance, driving stock from $67 to $72+ before monthly OPEX. Smart money positioning for this catalyst.

Q4 2025 Earnings Preview - Expected January 2026 📊

While formal date not announced yet, next earnings expected January 9, 2026 based on historical patterns:

What to watch:

- 💰 Premium revenue growth vs main cabin (Q4 2024 premium grew 6 percentage points faster)

- 🤖 SkyMiles & AmEx partnership revenue - targeting $10B annually by 2028 vs $7.6B in 2024

- ✈️ Transatlantic expansion revenue contribution (first full quarter with all new routes operational)

- 📈 Full-year 2026 guidance - critical for sustaining momentum

- 🛢️ Fuel cost outlook (major expense line, highly volatile)

Potential surprise factor: If holiday travel exceeds expectations AND new international routes outperform, Delta could guide materially above Street estimates for 2026, triggering another leg higher toward $75-80.

Fuel Cost Tailwinds - 2026 Outlook 🛢️

Industry forecasts suggest significant fuel savings ahead:

- IATA forecast: Average jet fuel $86/barrel in 2025 vs $99 in 2024 (-13% reduction)

- Alternative estimate: $87/barrel ($2.07/gallon), nearly 5% reduction in fuel expenditure

- Delta spent $10.5B on fuel in 2024 consuming 4.1B gallons

Do the math: With 4.1B gallons annual consumption, a $13/barrel ($0.31/gallon) reduction saves $1.27 BILLION annually, potentially adding $1.50-2.00 per share to earnings. If this materializes in 2026 guidance, it's a massive positive catalyst.

Premium Revenue Overtaking Main Cabin - 2027 Target 🎯

Delta projects premium ticket revenue will exceed main cabin revenue by 2027:

- Q4 2024 gap: Premium at $5.2B vs Main cabin at $6.0B (premium is 87% of main cabin)

- Premium growing 6 percentage points faster than main cabin

- Premium cabins deliver 15% higher margins

Why this matters NOW: Every quarter that passes showing premium growth acceleration validates the 2027 thesis and supports premium valuation multiple. The Jan earnings will be critical data point - if premium revenue grows 8-10%+ vs main cabin 2-3%, it reinforces the trajectory.

CrowdStrike Lawsuit Resolution - Potential Wildcard 💼

Delta's $500M lawsuit against CrowdStrike is proceeding:

- 📋 Claim: Over $500M in losses from July 2024 outage causing 7,000 flight cancellations

- ⚖️ Georgia judge ruled Delta can proceed with negligence and computer trespass claims (May 2025)

- 💰 If Delta prevails, $500M recovery = $0.75-0.80/share earnings boost

Timeline unclear but any settlement announcement would be immediate positive catalyst.

⚠️ Risk Catalysts (Negative)

Macro Recession Risk 📉

Economic slowdown in 2026 could impact:

- 💼 Corporate travel demand (though currently strong)

- ✈️ Premium cabin load factors (high-margin business/first class most vulnerable)

- 💰 Pricing power in competitive leisure markets

Competitive Pressure from United 🥊

United Airlines posted strong Q4 2024 results:

- Q4 profit: $985M (up 64% YoY) on $14.70B revenue (+8% YoY)

- Adjusted EPS: $3.26 (beat expectations)

- Focus: Ramping up competition for high-spending travelers

United is investing heavily in premium products to compete directly with Delta's strength. Market share battle intensifying.

Labor Cost Inflation 💸

Rising labor costs pressuring margins:

- Industry-wide unit costs (excluding fuel) increased 28% since pandemic, adding $37B in operating expenses

- Ongoing pilot contract amendments and flight attendant negotiations

- Higher wages necessary to retain talent but compress margins if not offset by revenue growth

Geopolitical & Currency Risks 🌍

International expansion exposes Delta to:

- Political instability in Europe/Middle East impacting travel demand

- USD strength making international travel more expensive for Americans

- Regulatory changes in foreign markets

- Trade policy uncertainty (lessons from Q1 2025 guidance withdrawal)

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through January 16th expiration:

📈 Bull Case (40% probability)

Target: $72-$77

How we get there:

- 🎄 Holiday travel data shows record-breaking performance with 88%+ load factors and premium pricing

- 💰 Delta preannounces strong Q4 results or raises full-year guidance in late December

- ✈️ Transatlantic expansion routes performing ahead of expectations (95%+ load factors on new Italy routes)

- 🛢️ Oil prices decline further (Brent to $70-75/barrel) improving Q1 2026 fuel outlook

- 📊 SkyMiles/AmEx revenue accelerating toward $10B annual target

- 🚀 Analyst upgrades on premium revenue momentum and margin expansion visibility

- 📈 Breakout above $70 gamma resistance triggers technical rally through $72.50 to $75+

This scenario validates the institutional positioning:

- ✅ Dec 19 $72.50 calls go in-the-money (60K contracts profitable!)

- ✅ Jan 16 $70/$80 call spread captures $70-77 move for max profit

- ✅ $57.50 short puts expire worthless, keep premium

Key metrics needed:

- Holiday RASM (revenue per available seat mile) up 8-10% YoY

- Premium revenue growth >10% in Q4

- Load factors 85%+ system-wide during peak travel period

- International revenue up 15%+ driven by transatlantic expansion

Probability assessment: 40% because it requires strong execution on multiple fronts PLUS favorable macro (oil prices, consumer spending, no recession fears). However, Delta has consistently delivered, operational excellence is proven, and institutional money is clearly betting on upside with massive call buying.

🎯 Base Case (45% probability)

Target: $65-$70 (CONSOLIDATION)

Most likely scenario:

- ✅ Solid holiday travel season meeting (not exceeding) expectations

- 📱 Q4 results in-line with consensus when reported in January

- ⚖️ Transatlantic routes performing as planned, no major surprises either way

- 💼 Corporate travel demand steady but not accelerating

- 🛢️ Oil prices range-bound $75-85/barrel (neutral impact)

- 📊 Trading within gamma support ($65) and resistance ($67.50-$70) for weeks

- 🤝 Market digests YTD gains (+47%), waits for January earnings for next catalyst

- 💤 Volatility relatively muted vs implied move expectations

This is the "chop zone" outcome:

- ❌ Dec 19 $72.50 calls expire worthless (-$1.87M loss on those)

- ⚖️ Jan 16 $70/$80 spread captures modest gains if stock at $68-69 (breakeven to small profit)

- ✅ $57.50 short puts expire worthless, keep $981K premium

Why 45% probability: Stock at technical crossroads after strong rally - neither breaking out nor breaking down. Fundamentals solid but much good news already priced in at $67. Most institutional players will hold existing positions and wait for Q4 earnings data before adding aggressively.

The gamma structure ($65 support, $70 resistance) creates natural range for consolidation. Without major catalyst, stock likely grinds in this zone.

📉 Bear Case (15% probability)

Target: $57-$62 (CORRECTION)

What could go wrong:

- 😰 Holiday travel disappoints - weather disruptions, capacity issues, or weaker-than-expected demand

- 🚨 Recession fears intensify in December/January with weak economic data

- 💸 Oil prices spike to $95-100/barrel on geopolitical events (Middle East, Russia)

- ⚖️ Competitive pressure intensifies - United/American match premium offerings, compressing yields

- 📉 Broader market selloff drags airlines lower (sector rotation out of cyclicals)

- 🇨🇳 China tensions impact Pacific routes or broader sentiment

- 💰 Labor negotiations turn contentious, raising cost concerns

- 🔨 Break below $65 gamma support triggers technical cascade to $62.50, then $60

Critical support levels:

- 🛡️ $65: Major gamma floor - MUST HOLD or momentum shifts bearish

- 🛡️ $62.50: Deep support (where they closed the 22K calls) - likely institutional buying

- 🛡️ $60: Extended floor - disaster scenario

- 🛡️ $57.50: Ultimate support (where short puts are struck) - major accumulation zone

Why only 15% probability: Delta's fundamentals are STRONG. The company is executing flawlessly - 83% on-time performance, premium strategy working, international expansion launched successfully, balance sheet solid. Bear case requires multiple external shocks (recession, oil spike, macro selloff) rather than Delta-specific issues.

The institutional positioning (selling $57.50 puts) shows smart money is WILLING to own Delta at $57.50 - they view that as compelling value. This creates floor.

Put P&L in Bear Case:

- Stock at $60 on Jan 16: $70/$80 spread worthless, $57.50 puts OTM = total loss ~$4-5M on net structure

- Stock at $57 on Jan 16: $70/$80 spread worthless, $57.50 puts ITM = assigned stock, total loss ~$6-8M

- Stock at $65 on Jan 16: $70 calls worthless, $80 calls worthless, $57.50 puts worthless = loss on Dec calls, keep put premium

💡 Trading Ideas

🛡️ Conservative: Ride the Holiday Wave with Stock

Play: Buy Delta shares at current levels ($66-67) with tight stop

Why this works:

- ⏰ We're IN peak holiday travel season RIGHT NOW - highest revenue period of year

- 💰 Institutional money just deployed $17.3M repositioning - following smart money

- 📊 83% on-time performance and operational excellence driving brand premium

- 🎯 Strong gamma support at $65 (just 2.6% below) limits downside

- ✈️ Transatlantic expansion adding $200-300M incremental revenue

- 💪 Premium revenue strategy working - 57% of total revenue

- 🛢️ Potential fuel tailwinds in 2026 ($1.27B savings if oil drops)

Action plan:

- 🎯 Entry: $66-67 (current levels)

- 🛡️ Stop loss: $64.50 (below $65 gamma support)

- 📈 Target 1: $70 by mid-January (+4.5% gain)

- 🚀 Target 2: $72-75 if holiday data exceptional (+8-12% gain)

- 📊 Position size: 5-10% of portfolio (core airline holding)

- ⏰ Hold through Q4 earnings in January unless stop hit

Dividend bonus: Delta increased dividend 25% in September 2025, provides income while waiting

Risk management:

- Hard stop at $64.50 limits loss to 3.4%

- If stopped out, reassess at $62.50 support

- Trail stop to $66 if stock reaches $70 (lock in gains)

Risk level: Low-moderate (stock position with defined stop) | Skill level: Beginner-friendly

Expected outcome: Capture 5-10% upside through January with limited downside risk. Worst case: small 3% loss if stop hit. Best case: 12%+ if premium strategy accelerates and fuel tailwinds materialize.

⚖️ Balanced: Copy the Pros with Call Spread

Play: Replicate the institutional $70/$80 call spread for January

Structure: Buy $70 calls, Sell $80 calls (January 16 expiration - SAME as the $17M trade)

Why this works:

- 🤝 Literally copying the institutional positioning from this morning's trade

- 📊 Defined risk spread ($10 wide = $1,000 max risk, $1,000 max profit per spread)

- 🎯 Targets the $67-$77 range where Delta likely trades through January

- ⏰ 39 days to expiration gives time for holiday data + Q4 earnings preview

- 💰 Captures profit if stock moves 5-15% higher (very achievable given catalysts)

- 🛡️ Max loss defined and limited (unlike naked calls)

Estimated P&L (based on current pricing):

- 💵 Net debit: ~$2.30-2.50 per spread ($230-250 per spread)

- Buy $70 call: ~$2.70-2.90

- Sell $80 call: ~$0.40-0.50

- 📈 Max profit: $7.50-7.70 per spread if DAL above $80 at Jan 16 (300%+ ROI!)

- 📉 Max loss: $2.30-2.50 if DAL below $70 at Jan 16 (100% loss of premium)

- 🎯 Breakeven: ~$72.30-72.50

- 📊 Risk/Reward: Risk $250 to make $750 (1:3 ratio - excellent!)

Position sizing:

- Start with 2-5 spreads ($500-1,250 risk)

- Can add 2-3 more if stock pulls back to $65-66

- Total position: 5-8 spreads max ($1,250-2,000 total risk)

Profit scenarios:

- Stock at $75 on Jan 16: Spread worth $5.00, profit = $2.50-2.70 per spread (100%+ ROI)

- Stock at $77 on Jan 16: Spread worth $7.00, profit = $4.50-4.70 per spread (180%+ ROI)

- Stock at $80+ on Jan 16: Spread worth $10.00, profit = $7.50-7.70 per spread (300%+ ROI)

- Stock at $72 on Jan 16: Spread worth $2.00, loss = -$0.30 to -$0.50 (12-20% loss)

- Stock at $68 on Jan 16: Spread worthless, loss = -$2.30 to -$2.50 (100% loss)

Entry timing:

- ✅ Can enter NOW at current levels (institutional trade TODAY signals conviction)

- ⚖️ Or wait for minor pullback to $65-66 for better entry (if it comes)

- ❌ Don't wait too long - time value decays and if stock rallies, entry gets worse

Management:

- 🎯 Take profits at 100% gain (spread worth $5+) if hit before Jan

- 🚀 Let winners run if stock momentum strong through $72

- 📉 Close at 50% loss (-$1.25) if stock breaks below $65 gamma support

- ⏰ Don't hold to expiration - close position Jan 12-15 to avoid gamma risk

Risk level: Moderate (defined risk, directional bullish) | Skill level: Intermediate

🚀 Aggressive: Short-Term Holiday Catalyst Play (ADVANCED!)

Play: Buy near-term $72.50 calls betting on holiday travel data

Structure: Buy $72.50 calls (December 19 expiration - SAME as the 60K call buy!)

Why this could work:

- 🎄 Peak holiday travel period happening RIGHT NOW (Dec 8-19)

- 💥 If travel data exceptional, Delta could preannounce strong Q4 results this week

- 📊 Institutional buyer paid $1.87M for 60K of these - they know something about near-term catalyst

- 🎯 Only needs 8.7% move from $66.71 to $72.50 (achievable with good news)

- ⏰ 11 days to expiration = massive gamma if stock approaches $72.50

- 📈 Implied move upper range for Dec 19 is $72.00 - betting on exceeding expectations

Why this could blow up (SERIOUS RISKS):

- 💸 TIME DECAY KILLER: Only 11 days left - theta burns ~5-7% of value per day

- ⏰ Binary outcome: Either works or doesn't - no middle ground with OTM calls expiring soon

- 😱 Need BIG move: Stock must rally 8.7% in 11 days just to get to strike (doesn't guarantee profit!)

- 📉 High probability of total loss: If no catalyst emerges, calls expire worthless

- ⚠️ Vega risk: Any decline in volatility crushes option value even if stock rises modestly

Estimated P&L:

- 💰 Cost: ~$0.30-0.40 per call ($30-40 per contract)

- 📈 Profit scenario: Stock at $73-75 by Dec 19 = $0.50-2.50 profit (125-625% ROI)

- 🚀 Home run: Stock at $77+ by Dec 19 = $4+ profit (1000%+ ROI)

- 📉 Most likely: Stock at $68-70 by Dec 19 = total loss (-100%)

- 💀 Worst case: Stock at $66 by Dec 19 = total loss (-100%)

Breakeven: $72.80-72.90 (need 9.2% rally in 11 days)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can afford to lose ENTIRE premium (70%+ probability of total loss!)

- ✅ Understand this is pure speculation on near-term catalyst, not investment

- ✅ Have experience with short-dated options and gamma risk

- ✅ Are disciplined enough to take profits quickly if it works (don't get greedy!)

- ✅ Accept that even institutional buyer may lose money on this leg of trade

Position sizing:

- MAX 1-2% of portfolio (this is lottery ticket, not core position)

- Buy 5-10 contracts max ($150-400 total risk)

- Think of it as "buying a lottery ticket" - fun speculation with money you can lose

Management plan:

- 🎯 Take profits at 100% gain ($0.60-0.80) if hit - don't wait for home run

- 🚀 If stock rips to $70+ this week, consider taking 50% off at 150% gain, let rest ride

- 💀 Accept total loss if no catalyst by Dec 16-17 (close then, don't wait for expiration)

- ⚡ Watch for any Delta preannouncements, route performance data, or unusual activity

Catalyst watch:

- 📰 Holiday travel performance reports (TSA numbers, load factor data)

- 💬 Management commentary at investor conferences

- 📊 Industry data showing exceptional Q4 performance

- 🚀 Analyst upgrades or raised price targets based on premium revenue trends

Risk level: EXTREME (70%+ probability of total loss) | Skill level: Advanced only

Probability of profit: ~25-30% (needs significant catalyst AND stock move in very short time)

ONLY for traders who:

- Understand options Greeks (gamma, theta, vega)

- Have traded short-dated options before

- Can handle watching position go to zero

- View this as entertainment/speculation, not investing

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

🎄 Holiday travel execution risk: We're IN peak season right now. Any operational issues (weather, IT problems, staffing) during Dec 20-Jan 5 period would be catastrophic for Q4 results. Delta's July 2024 CrowdStrike outage showed IT vulnerabilities - another tech failure during holidays would crush stock.

-

💰 Valuation dependent on premium strategy: Stock trading at premium to peers based on belief that premium revenue will exceed main cabin by 2027. If premium growth slows (recession hits corporate travel, competition intensifies), valuation re-rates lower quickly. Currently premium is 87% of main cabin - needs sustained outperformance.

-

🛢️ Oil price volatility is MASSIVE wildcard: Delta consumed 4.1B gallons in 2024 - each $1/barrel change = $100M annual impact. Oil at $75 vs $95 is $2 BILLION difference in fuel costs. Geopolitical events (Middle East conflict, Russia-Ukraine escalation) can spike prices overnight, destroying profitability assumptions.

-

🥊 United ramping up competition: United posted 64% profit growth in Q4 2024 and is aggressively targeting Delta's premium customer base with similar product enhancements. Market share battle intensifying - if United wins business travelers, Delta's premium pricing power erodes.

-

📉 Recession risk in 2026: Airlines are HIGHLY cyclical. At first sign of recession, corporate travel budgets get cut, premium cabin demand drops, and pricing power evaporates. Delta trading at premium valuation leaves no room for error if economy weakens. Unemployment ticking up or consumer confidence falling would trigger 15-20% stock correction.

-

💸 Labor cost inflation structural headwind: Industry unit costs increased 28% since pandemic, adding $37B in expenses. Pilot contracts, flight attendant negotiations, ground crew wages all rising. Delta can't offset entirely with revenue growth - margin compression risk if labor demands escalate.

-

🇨🇳 International expansion carries execution risk: Largest-ever transatlantic expansion with 7+ new routes is ambitious. If load factors on new Italy/Sicily routes disappoint (below 80%), or Shanghai service faces political headwinds, the $200-300M incremental revenue thesis fails.

-

📊 Institutional trade could be CLOSING, not opening: While we interpret this as bullish repositioning, it's possible the trader is REDUCING exposure by closing profitable $62.50 calls and only partially reinvesting. The $9.9M collected vs $7.7M deployed suggests NET reduction in delta exposure. If true, it's cautious signal, not bullish.

-

⚖️ Gamma ceiling at $67.50 and $70 creates resistance: Combined 16.2B gamma at $67.50-$70 means market makers will systematically SELL into rallies to hedge. This creates mechanical headwind - requires sustained buying pressure to overcome. Current price ($66.71) sitting right below these walls.

-

🎢 Implied move might be TOO conservative: Dec 19 implied move of ±5.35% seems reasonable, but if holiday travel data is materially different (better or worse) than expected, actual move could be 8-10%. This creates two-way risk - explosive upside OR downside beyond what options are pricing.

-

💼 Corporate travel demand concentration risk: Premium revenue strategy depends heavily on corporate travelers willing to pay for business/first class. Tech layoffs, banking sector weakness, or corporate cost-cutting would disproportionately hurt Delta vs leisure-focused competitors.

-

🌍 Geopolitical tail risks: Europe exposure (650+ weekly transatlantic flights) creates vulnerability to terrorism, political instability, or conflict escalation. Any major European security incident would crater transatlantic demand overnight. Similarly, China tensions could force route cancellations or capacity reductions.

🎯 The Bottom Line

Real talk: Big money just made a MAJOR move in Delta - spending $17.3 MILLION to roll out of winning positions into a sophisticated structure targeting $70-80 by January. This isn't random trading - it's calculated repositioning by institutions who've made serious money on Delta's 47% YTD rally and want to stay in the game while managing risk.

What this trade tells us:

- 🎯 They're STILL BULLISH (bought 60K+ calls at $70 and $72.50) but taking some chips off the table (closed 22K at $62.50)

- 💰 Near-term catalyst expected in next 11 days (hence massive Dec 19 $72.50 call buying) - likely holiday travel data

- ⚖️ Willing to own Delta stock at $57.50 (14% below current) if market crashes - shows conviction in value

- 📊 Target range $70-80 by Jan 16 (5-20% upside) with protection against downside

- ⏰ Timing matters - executed at 10:17 AM during liquid market hours for minimal slippage ($17M moved in ONE SECOND)

The setup is compelling:

- ✈️ We're IN peak holiday travel season (highest revenue period of year)

- 🚀 Transatlantic expansion operational and generating incremental revenue

- 💪 Premium revenue strategy working - 57% of total revenue with clear path to majority by 2027

- 🛢️ Potential fuel tailwinds ($1.27B savings if oil drops to $86/barrel in 2026)

- 📊 Industry-leading operational performance - 83% on-time arrival

- 💰 SkyMiles partnership generating $7.6B annually, targeting $10B by 2028

BUT - and this is important - risks are real:

- At $67, much good news already priced in (+47% YTD)

- Gamma resistance at $67.50-$70 requires catalyst to break through

- Recession risk, oil volatility, competition from United all legitimate concerns

- No margin of safety if Q4 disappoints or 2026 guidance conservative

If you own DAL:

- ✅ You're sitting on great gains - congratulations!

- 📊 Consider holding through January earnings if position size reasonable

- 🎯 Set mental stop at $65 (gamma support) to protect gains

- 💡 Could sell 25% at $70 if reached, lock in profits, let rest ride

- 🛡️ The institutional $70/$80 call spread is worth copying for additional upside exposure with defined risk

If you're on the sidelines:

- ⏰ Entry at $66-67 decent with stop below $65 (3% risk for 8-12% upside potential)

- 🎯 Better entry at $65 pullback if it comes (gamma support + better risk/reward)

- ⚖️ The $70/$80 call spread for Jan 16 offers asymmetric risk/reward (risk $250 to make $750)

- 🎄 Near-term catalyst potential (holiday data) makes December interesting

- 📈 Longer-term (6-12 months), premium revenue trajectory and fuel tailwinds support $75-85 targets

If you're bearish:

- 🤔 Fighting 47% YTD momentum with institutional money buying calls seems... unwise

- 📊 Wait for break below $65 gamma support before shorting

- ⚠️ Put spreads ($70/$60 or $65/$57.50) offer defined-risk way to play downside

- 💰 Remember: institutions SOLD $57.50 puts (willing to own stock there) - that's your floor

Mark your calendar - Key dates:

- 📅 December 19 (Thursday) - Monthly OPEX, short-term $72.50 calls expire, potential holiday travel data

- 📅 December 20-January 5 - PEAK holiday travel period (most profitable 2 weeks of year)

- 📅 January 9, 2026 (likely) - Q4 2025 earnings report

- 📅 January 16 - Monthly OPEX, long-term call spread and put positions expire

- 📅 Q2 2026 - Next round of transatlantic expansion potential

Final verdict: Delta's executing on all cylinders - operational excellence, premium strategy working, international expansion launched, balance sheet solid. The $17.3M institutional roll is a vote of confidence in continued upside to $70-80 while prudently taking some profits after a monster rally.

This isn't a "back up the truck" moment at $67 after 47% YTD gain, but it's absolutely a "stay invested with smart risk management" moment. The holiday travel catalyst in the next 11 days could provide the spark to push through $70 resistance, and the January earnings in 5 weeks could validate the premium revenue thesis for another leg higher.

Be strategic. Follow the smart money. Manage your risk. Delta's story is far from over. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. The complex roll strategy described involves sophisticated institutional positioning that may not be suitable for retail traders. Z-scores indicate statistical unusualness relative to recent history but do not guarantee profitability. Airlines are cyclical businesses subject to fuel price volatility, economic conditions, and operational risks. Always do your own research and consider consulting a licensed financial advisor before trading. The institutional trader may have portfolio considerations, tax strategies, or hedging needs not applicable to retail investors.

About Delta Air Lines: Delta Air Lines, Inc. is one of the world's largest airlines, with a network of over 300 destinations in more than 50 countries, operating through major hubs in Atlanta, New York, Salt Lake City, Detroit, Seattle, and Minneapolis-St. Paul. Market cap: $43.8 billion in the Air Transportation industry.