🛩️ DAL: $5.6M Bull Call Spread Bets on Delta's Flight to $75 by June! 🚀

📅 December 12, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

A sophisticated trader just deployed $5.6 MILLION into a Delta Air Lines bull call spread this morning at 10:00:19! They simultaneously bought 3,000 contracts of the $65 calls for $3.6M and sold 3,000 contracts of the $75 calls for $2M - netting a $1.6M debit on a spread expiring June 18, 2026. With Delta trading near all-time highs at $71.04 following blowout Q3 earnings, this is smart money betting the airline rally has serious legs for another 6+ months. Translation: Institutional players see DAL hitting $75+ by mid-2026 on continued travel demand and premium revenue growth!

📊 Company Overview

Delta Air Lines (DAL) is one of the world's largest and most profitable airlines, operating a global network spanning over 300 destinations:

- Market Cap: $46.07 Billion (largest U.S. airline by market cap)

- Industry: Air Transportation (Scheduled)

- Sector: Transportation

- Current Price: $71.04 (near all-time high close of $69.93 on December 10, 2025)

- Employees: 103,000

- Headquarters: Atlanta, GA

Primary Business: Delta operates a hub-and-spoke network centered around major connection points in Atlanta, New York, Salt Lake City, Detroit, Seattle, and Minneapolis-St. Paul. The carrier generates substantial international revenue from transatlantic operations and has been crushing it with premium cabin revenue, which is on track to eclipse main cabin sales in 2026.

💰 The Option Flow Breakdown

The Tape (December 12, 2025 @ 10:00:19):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:00:19 | DAL | ASK | BUY | CALL $65 | 2026-06-18 | $3.6M | $65 | 3,000 | 3,700 | 3,000 | $71.04 | $11.98 |

| 10:00:19 | DAL | BID | SELL | CALL $75 | 2026-06-18 | $2M | $75 | 3,000 | 2,100 | 3,000 | $71.04 | $6.56 |

🤓 What This Actually Means

This is a classic bull call spread - a defined-risk directional bet on continued upside! Here's what went down:

-

💸 Net debit paid: $1.6M ($5.42 per spread × 3,000 spreads)

- Bought $65 calls for $11.98 each = $3.6M

- Sold $75 calls for $6.56 each = $2M collected

- Net cost: $5.42 per spread × 3,000 = $1,626,000

-

🎯 Profit zone: Stock needs to be above $70.42 at June expiration to breakeven

-

💰 Max profit: $4.58 per spread ($10 spread width - $5.42 cost) × 3,000 = $1,374,000 (85% ROI!)

-

🛡️ Max loss: Limited to $1.6M premium paid (defined risk)

-

⏰ Time horizon: 188 days to expiration (June 18, 2026)

-

📊 Current position: Already $6.04 in-the-money on the long $65 calls ($71.04 - $65 = $6.04 intrinsic value)

What's really happening here:

This trader is making a BULLISH bet that Delta continues its monster rally from the current $71 level toward $75+ by June 2026. The structure is sophisticated - by selling the $75 calls, they're capping their upside at $75 but reducing their cost basis from $11.98 down to $5.42. This improves their probability of profit dramatically.

Think of it like buying a ticket to ride Delta from $65 to $75, but getting a discount because you agreed not to participate in gains above $75. With Delta up 103.5% from its 52-week low of $34.74 and recently hitting all-time highs, this trader sees the airline rally extending through mid-2026.

Unusual Score: 🔥 EXTREMELY UNUSUAL (Z-scores of 22.36 and 11.94) - These trades are 11-22x larger than typical Delta options activity! Both legs executed simultaneously with HIGH_ACTIVITY signals, showing this is coordinated institutional positioning, not retail dabbling. The fact that they structured this as a spread (not naked calls) shows sophisticated risk management - they're bullish but disciplined about cost and risk.

📈 Technical Setup / Chart Check-Up

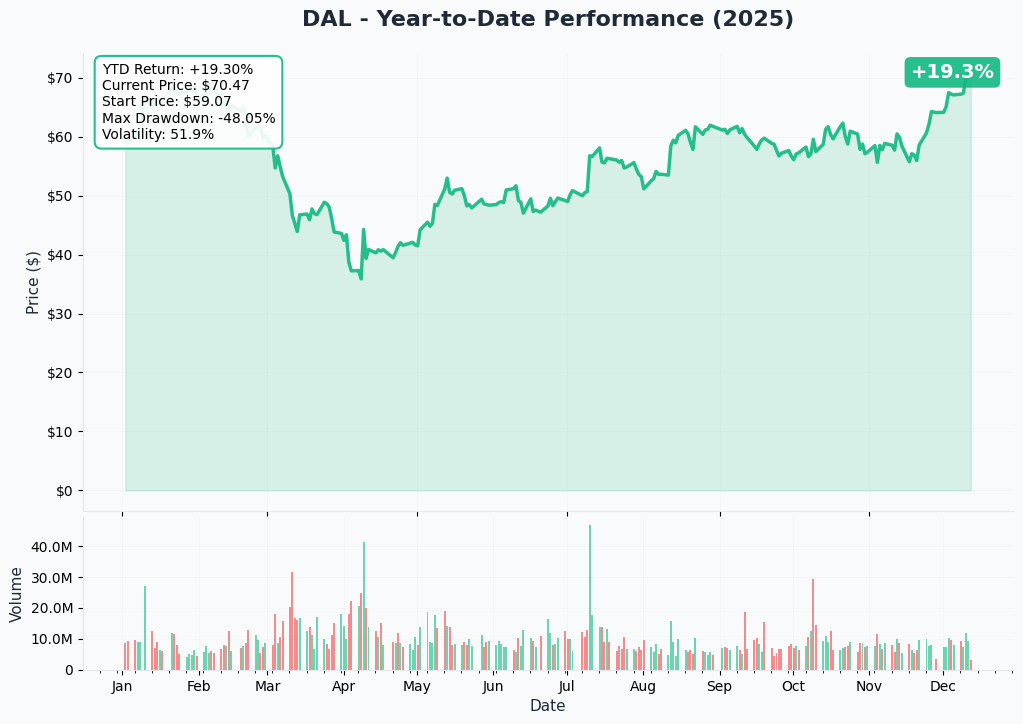

YTD Performance Chart

Delta is absolutely flying - currently trading at $70.70, up 103.5% from its 52-week low of $34.74! The chart tells a powerful recovery and growth story - after bottoming in the low $30s earlier this year, DAL staged an explosive rally throughout 2025, recently hitting an all-time high close of $69.93 on December 10, 2025.

Key observations:

- 🚀 Sustained uptrend: Consistent higher highs and higher lows throughout 2025

- 📈 Breakout confirmed: Smashed through $60 resistance in Q4 2025, never looked back

- 💪 Momentum strong: Recent consolidation at $70-71 after reaching all-time highs suggests healthy base-building

- 📊 Volume confirmation: Strong institutional accumulation following Q3 earnings beat on October 9

- ⚡ Next target clear: $75 represents logical next resistance (5.6% upside from current levels)

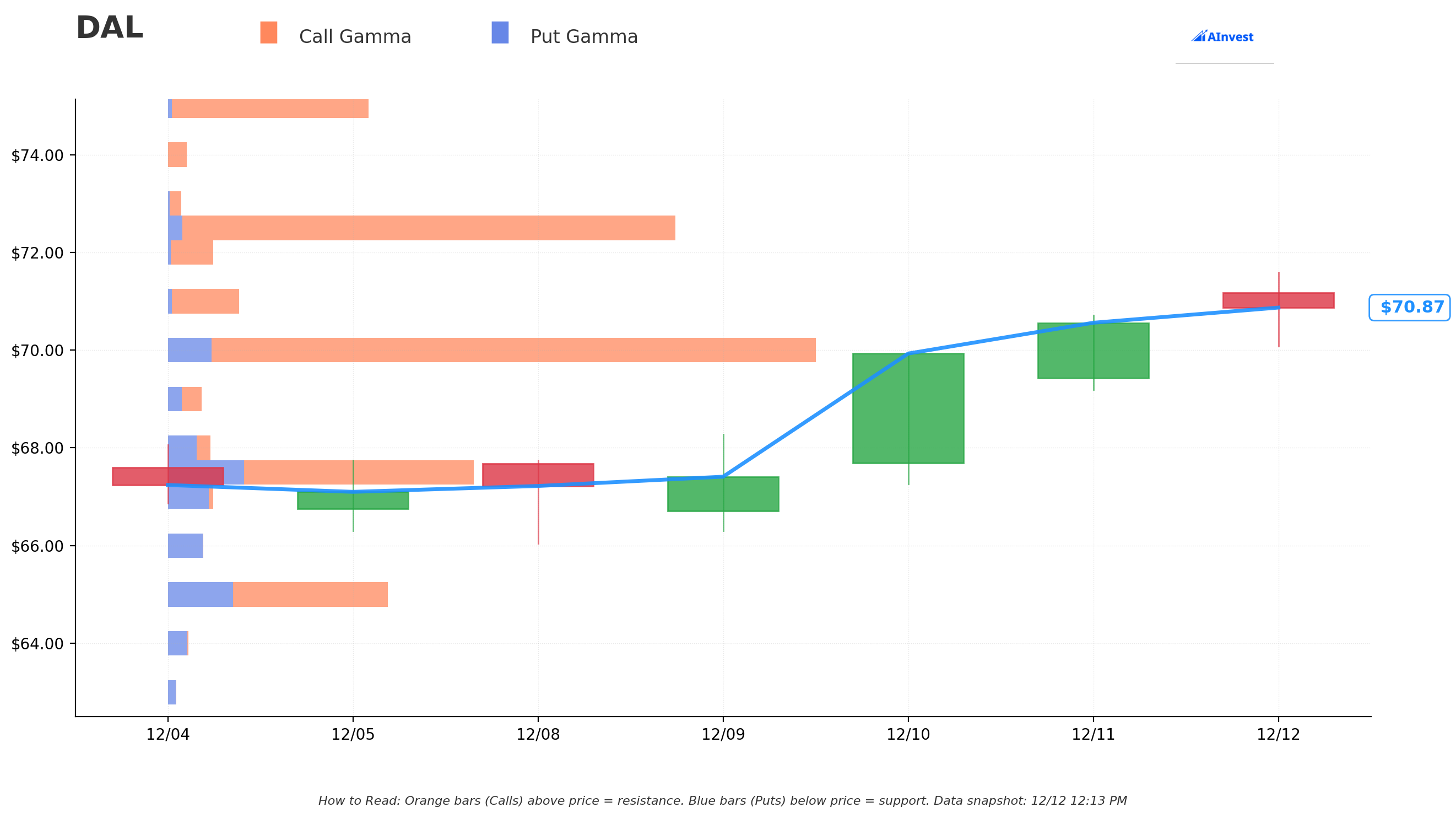

Gamma-Based Support & Resistance Analysis

Current Price: $70.83 (spot reference price)

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

🔵 Support Levels (Put Gamma Below Price):

-

$70.00 - STRONGEST IMMEDIATE SUPPORT with 17.1M total gamma exposure (14.9M net gamma!)

- This is THE line in the sand - massive put selling and call buying concentrated here

- Only 1.18% below current price - this floor should hold on any dips

-

$67.50 - Secondary support at 7.9M total gamma (3.9M net gamma)

- 4.7% below current - represents healthy pullback zone

-

$65.00 - Major structural floor at 4.6M gamma (1.2M net gamma)

- This is exactly where the bull call spread long leg is struck! Not coincidental.

- 8.2% below current - deep support where buyers would aggressively step in

-

$62.50 - Extended support at 5.5M gamma

- 11.8% below current - disaster scenario floor

🟠 Resistance Levels (Call Gamma Above Price):

-

$71.00 - Immediate ceiling with 2.1M total gamma (1.9M net gamma)

- Just 0.24% overhead - minor resistance, easily breakable

-

$72.50 - Secondary resistance at 13.7M total gamma (12.9M net gamma)

- 2.4% above current - first meaningful ceiling to overcome

-

$75.00 - MAJOR CEILING with 5.4M total gamma (5.1M net gamma)

- This is exactly where the bull call spread short leg is struck!

- 5.9% above current - this is the TARGET zone the spread is betting on

- Breaking through $75 would trigger explosive momentum

-

$80.00 - Extended upside target at 7.3M gamma

- 12.9% above current - longer-term bull case target

What this means for traders:

Delta has MASSIVE support at $70 (14.9M net gamma) - this creates a strong floor where dealers will buy aggressively on dips. The structure shows bullish bias with 67.5M total call gamma vs 25M put gamma. The spread trader structured their position perfectly: long at $65 (major support) and short at $75 (major resistance). They're essentially betting Delta trades in the $65-$75 range through June, with maximum profit if it reaches the $75 ceiling.

Notice the genius: If Delta stays above $70 (massive support) and grinds toward $75 (natural ceiling), this spread maxes out its profit. The gamma data validates the strikes they chose weren't random - they're positioned at key technical levels.

Net GEX Bias: BULLISH (67.5M call gamma vs 25M put gamma = 2.7:1 ratio) - Market makers are net short calls, meaning they'll need to buy stock as prices rise, creating positive feedback loops.

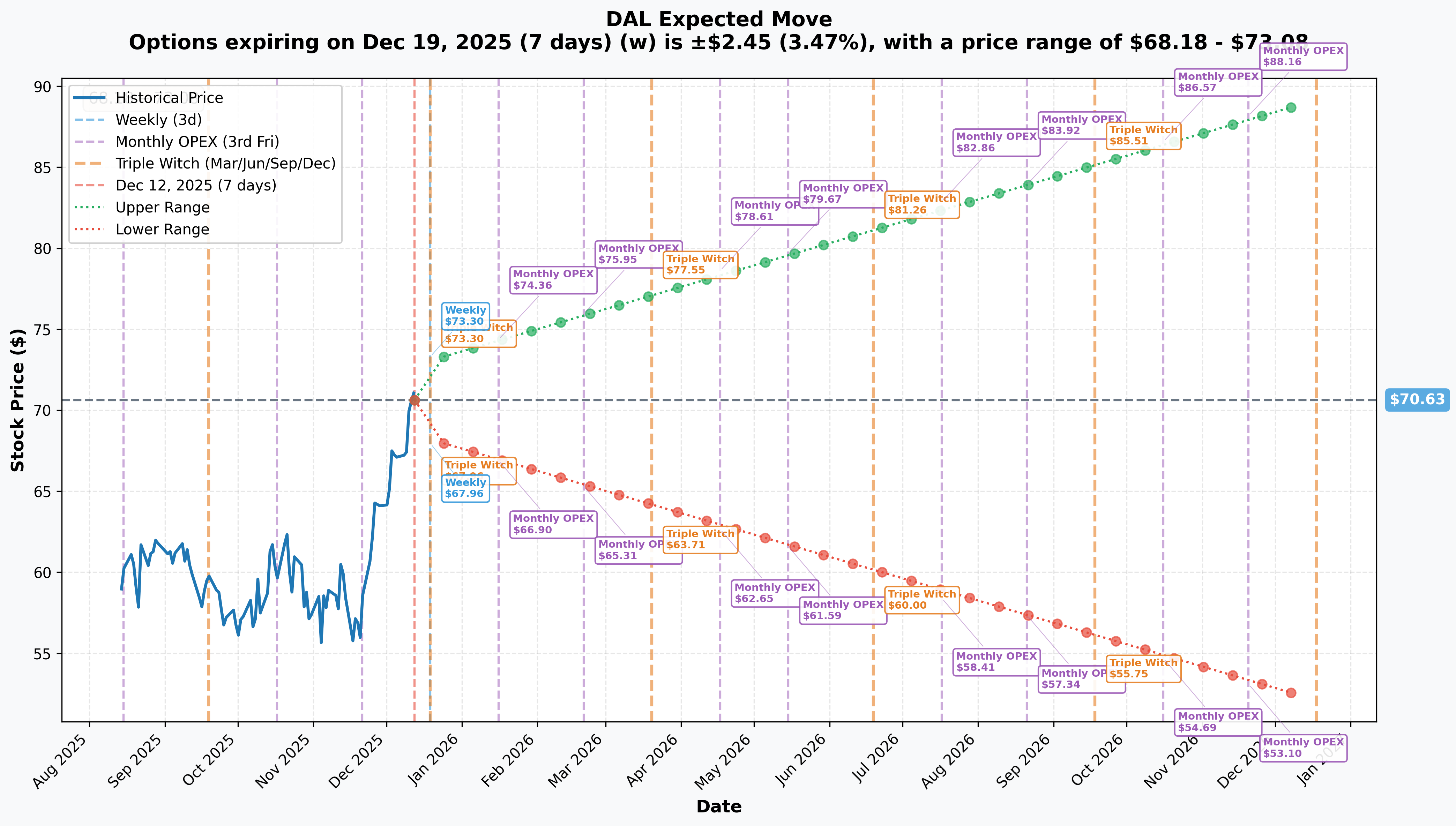

Implied Move Analysis

Options market pricing for upcoming expirations:

-

📅 Weekly (Dec 19 - 7 days): ±$2.45 (±3.47%) → Range: $68.18 - $73.08

- This is quarterly triple witch - modest volatility expected

-

📅 Q1 2026 Earnings OPEX (Jan 16 - 35 days): ±$3.73 (±5.27%) → Range: $66.90 - $74.36

- Captures Q4 2025 earnings release (January 9-10) - bigger move priced in

-

📅 June 18, 2026 OPEX (188 days - THIS TRADE!): ±$10.63 (±15.04%) → Range: $60.00 - $81.26

- Upper range of $81.26 is WELL ABOVE the $75 short call strike!

- Options market thinks there's realistic chance DAL trades $75-$81 by June

Translation for regular folks:

The market is pricing a 3.5% move ($2.45) through next week's triple witch, but a much larger 15% potential move ($10.63) through the June expiration. That $81.26 upper range validates the bull call spread thesis - the options market itself believes Delta could trade significantly above $75 by June!

The sharp increase in implied volatility from 3.5% (weekly) to 15% (6-month) reflects the reality that a LOT can happen in airline stocks over 188 days - Q4 earnings, international route expansion, fuel price swings, and the critical OpenAI OpenAI partnership progress all factor into that range.

Key insight: The $60 lower range provides a huge margin of safety. Even in a bearish scenario, the spread's long $65 calls would still have intrinsic value if Delta only pulls back to $65. The trader is protected unless Delta drops below $60 (15% decline from current levels) - unlikely given strong fundamentals.

🎪 Catalysts

🔥 Already Happened (Momentum Drivers)

Q3 2025 Earnings Blowout - October 9, 2025 📊

Delta crushed expectations in their September quarter results, setting the stage for the current rally:

- 📊 Revenue: $15.2B record September quarter revenue, up 4.1% YoY vs $15.06B expected

- 💰 Adjusted EPS: $1.71 vs $1.53 consensus (15% beat!)

- 🎯 Raised Full-Year Guidance: Adjusted EPS to ~$6 (upper half of prior $5.25-$6.25 range)

- 💵 Free Cash Flow: $830M in Q3, $2.8B YTD, targeting $3.5B-$4B for full year

The money shot: Premium revenue grew 9% to $5.8B (on track to eclipse main cabin sales in 2026!), while corporate sales surged 8% over prior year. CEO Ed Bastian: "Looking to 2026, Delta is well positioned to deliver top-line growth, margin expansion and earnings improvement."

Record Holiday Travel Performance (December 2024-January 2025) 🎄

Delta welcomed 9.3M travelers on 75,000+ flights from December 20, 2024 to January 6, 2025, with November and December 2024 marking four of the top 10 revenue days in Delta's history. This momentum carried into Q4 2025 and sets up strong Q4 earnings.

Analyst Upgrade Wave (October-December 2025) 📈

Wall Street piled into Delta following the Q3 beat:

- BMO Capital (December 2025): Initiated coverage with Outperform rating, $80 price target (12.6% upside!)

- Citigroup (December 4): Initiated Buy rating, $77 price target

- TD Cowen (December 4): Raised price target to $77 from $72

- Goldman Sachs, J.P. Morgan, B of A Securities: All reaffirmed Buy ratings

- Consensus: Average price target $72.99-$81.88, with high target of $90 from Morgan Stanley

🚀 Upcoming Catalysts (Next 6 Months)

Q4 2025 Earnings - January 9-10, 2026 (LESS THAN 1 MONTH!) 📅

Delta reports Q4 results in late January 2026 - this is THE near-term catalyst that could propel the stock through $75:

- 📊 Company Guidance: Adjusted EPS $1.60-$1.90

- 💰 Analyst Consensus: $1.75-$1.77 EPS (up 38.3% YoY!)

- 🎯 Revenue Guidance: +2% to +4% YoY

- 📈 Operating Margin: 10.5%-12% target

Key metrics to watch:

- Premium cabin revenue growth rate (Q3: +9% - can they sustain?)

- Holiday travel period results (December 2025 was massive)

- Corporate travel strength (Q3: +8% - is it accelerating?)

- 2026 full-year outlook (CEO signaled "top-line growth, margin expansion")

- CrowdStrike litigation update ($550M exposure)

Why this matters: A Q4 beat + strong 2026 guidance could easily push Delta to $75-$78, putting this spread deep in-the-money with maximum profit locked in.

Fleet Modernization & Capacity Expansion (2025-2026) ✈️

Delta is investing heavily in growth:

- 🛩️ 42 total aircraft deliveries expected for 2025 (75% narrowbodies, 25% widebodies)

- 🌟 A350-1000 Deliveries Starting 2026: First 4 of 20 A350-1000s scheduled (largest aircraft in Delta fleet!)

- ✈️ Boeing 737 MAX 10: 20 MAX 10s projected for 2026 pending FAA certification

- ♻️ Fleet Retirements: Accelerating retirement of 30+ older aircraft to improve fuel efficiency by ~$200M annually

International Route Expansion (2025-2026) 🌍

Delta is aggressively expanding high-margin international routes:

- 🇸🇬 Asia Expansion: New long-haul routes to Singapore, Manila, enhanced Seoul connectivity

- 🇭🇰 Los Angeles-Hong Kong route announced for 2026

- 🇸🇦 Atlanta-Riyadh new route commencing 2026

- 🇵🇪 Lima Hub Strategy: New hub expected to reduce annual fuel costs by ~$200M

U.S. Government $1B AI Supercomputer Contract 🇺🇸

Delta's technology leadership is attracting high-value contracts beyond traditional airline operations - the $1 billion Department of Energy supercomputer contract demonstrates diversification and government partnership strength.

SkyMiles Loyalty Program Updates (February 1, 2025) 💳

Delta's 120M+ member loyalty program is getting strategic enhancements:

- Refined mileage-earning rules tied to ticket prices and cabin class

- Modified Medallion qualification thresholds

- Loyalty revenue already up 9% YoY with American Express contributions rising 12% to $2B

This is a HIGH-MARGIN revenue stream that compounds competitive advantages.

⚠️ Risk Catalysts (What Could Go Wrong)

CrowdStrike Litigation Uncertainty 💻

The July 2025 CrowdStrike outage cost Delta $550M (after $50M fuel savings offset), impacting 1.3M customers and causing 7,000 flight cancellations. Delta is pursuing legal claims for $500M+ damages, though CrowdStrike claims liability cap limits damages to single-digit millions. Resolution timeline uncertain - could be material positive or negative catalyst.

Export Restrictions & China Headwinds 🇨🇳

While this is more relevant to chip companies than airlines, geopolitical tensions and trade policies could impact Delta's international expansion plans, particularly Asian routes and the recently terminated Aeromexico joint venture (September 2025).

Fuel Price Volatility ⛽

Delta does not hedge jet fuel after losing $4B cumulatively over 8 years on hedges - the airline is fully exposed to crude oil price swings. Rising fuel costs could compress margins even with strong demand.

Macroeconomic Uncertainty 📉

Delta withdrew 2025 guidance in April citing "broad economic uncertainty around global trade" with CEO stating "growth has largely stalled" at the time. While momentum has recovered, recession risk remains if economic conditions deteriorate in 2026.

Southwest Premium Entry 🛫

Southwest introduced assigned seating and bag charges in 2025, directly challenging Delta's premium positioning with fleet retrofitting including premium seats. This intensifies competition in the high-margin segment Delta dominates.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through June 18, 2026 expiration:

📈 Bull Case (45% probability)

Target: $78-$85

How we get there:

- 💪 Q4 earnings CRUSH with EPS toward high-end $1.85-1.90 range, revenue at +5% YoY

- 🎯 2026 guidance surprises to upside: full-year EPS $6.50+ (vs $6.00 2025)

- ✈️ Fleet expansion on track: A350-1000 deliveries begin smoothly, MAX 10 certified

- 🌍 International route launches exceed expectations: Asia routes showing strong early bookings

- 💰 Premium revenue continues growth: reaches 40%+ of total revenue

- 📊 Corporate travel accelerates: up 10%+ as 90% of companies expecting increased/steady 2026 volume materializes

- ⚖️ CrowdStrike settlement favorable: Delta recovers $200M+, removes legal overhang

- 🛢️ Fuel prices stable or declining: jet fuel stays flat or drops, expanding margins

- 📈 Breakout above $75 gamma resistance triggers technical rally to $80+

This is the SWEET SPOT for the bull call spread: Stock reaches $75-$85 range, spread maxes out profit at $75. The trader captures full $10 spread width, turning $5.42 cost into $10.00 value = $4.58 profit per spread × 3,000 = $1.37M profit (85% ROI).

Why 45% probability: Delta has strong momentum, solid fundamentals, and clear catalysts aligned. Premium revenue growth, corporate travel rebound, and fleet expansion are high-conviction themes. The stock already broke out to all-time highs - next resistance at $75 is realistic if execution continues. Gamma support at $70 provides floor protection.

🎯 Base Case (40% probability)

Target: $70-$78 range (SLOW GRIND HIGHER)

Most likely scenario:

- ✅ Solid Q4 earnings meeting consensus ($1.75-1.77 EPS, +3% revenue)

- 📱 2026 guidance in-line: EPS $6.25-6.50 (modest improvement, no fireworks)

- ⚖️ Fleet deliveries on schedule but not early: steady capacity growth

- 🤖 Premium revenue steady but not accelerating: +6-8% range (solid but not explosive)

- 🇨🇳 International expansion mixed results: some routes strong, others slower ramp

- 🔄 Trading between $70 support and $75 resistance for months

- 📊 Market digests 103% YTD gains, waits for proof points on 2026 momentum

- 💤 Volatility normalizes post-earnings (from 15% implied to 10-12% range)

- ⛽ Fuel costs modest headwind: slight margin compression offset by volume growth

Spread performance in base case: Stock grinds from $71 to $73-$76 range by June. Spread value moves from current ~$6.04 intrinsic to $8-$11 (at $73-$76 spot). Profit range: $2.58-$5.58 per spread = $774K-$1.67M profit (48-103% ROI). Not maximum profit, but still solid return.

Why 40% probability: Airlines tend to consolidate after big moves. Delta's up 103% from lows - some cooling-off period likely. Fundamentals support higher prices but multiple already expanded. Need consistent execution across several quarters to re-rate higher. $70-$75 trading range fits gamma profile perfectly.

📉 Bear Case (15% probability)

Target: $60-$68 (TEST LOWER SUPPORT)

What could go wrong:

- 😰 Q4 earnings miss or weak 2026 guidance disappoints: EPS $1.60-1.65, conservative outlook

- 🚨 Premium revenue growth decelerates: slows to +3-4%, questions 2026 outlook

- ⏰ Fleet delivery delays: Boeing MAX 10 certification pushed to 2027, capacity growth slows

- 🇨🇳 International challenges: China route restrictions impact Asia expansion

- 💸 Broader economic slowdown: recession fears reduce corporate travel demand

- ⚖️ CrowdStrike litigation goes against Delta: minimal recovery, $500M+ write-off

- 🛢️ Oil spike: crude rallies to $100+, jet fuel costs surge

- 📊 Competition intensifies: Southwest premium entry gains traction, pricing pressure

- 🔨 Break below $70 gamma support triggers cascade to $65, then $60

Critical support levels:

- 🛡️ $70: Massive gamma floor (14.9M net) - MUST HOLD or momentum shifts

- 🛡️ $67.50: Secondary support (3.9M net gamma) - 5% pullback zone

- 🛡️ $65: Deep support (1.2M net gamma) + long call strike - major buying level

- 🛡️ $60: Disaster floor (lower end of implied move range)

Spread P&L in Bear Case:

- Stock at $68 by June: Spread value $3.00 = loss of -$2.42 per spread × 3,000 = -$726K loss (45% loss)

- Stock at $65 by June: Spread value $0 (long calls at-the-money, short calls worthless) = -$1.63M loss (100% loss)

- Stock below $60: Both legs expire worthless = -$1.63M total loss (100% loss)

Why only 15% probability: Delta's fundamentals are STRONG. Premium revenue strategy working, corporate travel recovering, loyalty revenue growing 9%, and free cash flow of $3.5B-$4B provides cushion. Would require multiple negative catalysts to align. The $70 gamma support is MASSIVE - hard to see it breaking without major macro shock.

💡 Trading Ideas

🛡️ Conservative: Copy the Spread Post-Earnings

Play: Wait until after January 9-10 Q4 earnings, then enter same June $65/$75 bull call spread

Why this works:

- ⏰ Earnings binary risk removed - you'll know Q4 results and 2026 guidance before entering

- 💸 IV crush after earnings makes spreads slightly cheaper (save 5-10% on entry)

- 📊 Defined risk: maximum loss is premium paid (around $5.00-5.50 post-earnings)

- 🎯 Targets key gamma levels: long at $65 support, short at $75 resistance

- 🤝 Following sophisticated money - let them do the research, copy the trade structure

- ⏱️ Still 160+ days to expiration post-earnings gives plenty of time for thesis to play out

- 🛡️ Massive $70 gamma support provides floor protection

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Pay ~$5.00-5.50 net debit per spread (vs $5.42 original)

- 📈 Max profit: $4.50-5.00 if DAL above $75 at June expiration (82-100% ROI)

- 📉 Max loss: $5.00-5.50 if DAL below $65 (defined and limited)

- 🎯 Breakeven: ~$70.00-70.50

- 📊 Risk/Reward: ~1:1 which is acceptable for bullish defined-risk play

Entry timing:

- ⏰ Wait 1-2 days post-earnings (by Jan 11-12) for IV normalization

- 🎯 Only enter if Q4 earnings meet/beat and 2026 guidance solid

- ❌ Skip if stock gaps below $68 on weak results (thesis broken)

- ✅ Best if stock holds $70-72 range post-earnings (validates support)

Position sizing: Risk 3-5% of portfolio (this is directional speculation with airlines, not core holding)

Risk level: Low-Moderate (defined risk, following institutional trade) | Skill level: Intermediate

Expected outcome: Capture 50-80% of maximum profit if Delta continues uptrend. Avoid earnings volatility while maintaining bullish exposure.

⚖️ Balanced: Sell Cash-Secured $67.50 Puts (Income Strategy)

Play: Sell $67.50 puts expiring March 2026 (90-100 days out)

Why this works:

- 💰 Collect premium selling puts at key $67.50 gamma support level

- 🎯 You're willing to own Delta at $67.50 (5% below current, near strong support)

- 📊 Premium revenue strategy: collect ~$2.50-3.50 per contract ($250-350 per put)

- 🛡️ Margin of safety: $67.50 is 7.9M gamma support level - likely to hold

- ⏰ Capture time decay: theta works in your favor as option seller

- 🔄 Repeatable: if not assigned, roll to next month and collect more premium

- 📈 If assigned, own Delta at effective cost basis of $64-65 (strike minus premium)

Estimated P&L:

- 💰 Collect: ~$2.50-3.50 premium per put ($250-350 per contract)

- 📈 Keep premium if DAL stays above $67.50 at March expiration (4-5% return in 3 months)

- 📉 If assigned: Own 100 shares at $67.50 - premium collected reduces basis to $64-65

- 🎯 Breakeven: Effective cost $64-65 is STRONG value for Delta

Entry timing:

- ⏰ Can enter now or wait post-Q4 earnings for higher IV premiums

- 🎯 Sell when DAL is $70-72 (premium richer when stock higher)

- ❌ Don't sell if stock already at $68 (too close to strike)

Position sizing: Sell puts only on shares you'd be comfortable owning. If selling 10 puts, be ready to deploy $67,500 if assigned.

Risk management:

- 🛡️ Set aside cash to cover assignment ($67.50 × 100 shares per put)

- 📊 Monitor $70 support - if broken, consider buying back puts at loss

- 🔄 Roll down and out if stock drops to $68 (buy back, sell lower strike/longer date)

Risk level: Moderate (can be assigned shares, but at attractive price) | Skill level: Intermediate

Expected outcome: Collect 4-5% return in 3 months if Delta holds above $67.50. If assigned, own shares at discount to current price with bullish long-term outlook.

🚀 Aggressive: Naked Long June $75 Calls (Levered Upside)

Play: Buy $75 calls expiring June 18, 2026 (same expiration as spread)

Why this could work:

- 💥 PURE UPSIDE play - no cap on gains unlike the spread

- 🎰 Current price $6.56 per call - cheaper than the $11.98 the spread trader paid for $65 calls

- 📊 Break above $75 gamma resistance could trigger explosive move to $80-85

- 🚀 Analysts have $77-$80 average price targets, some as high as $90

- ⚡ If Delta reaches $85 by June, calls worth $10.00 = 52% ROI (vs spread capped at 85% but at lower risk)

- 📈 Maximum gamma leverage: profit accelerates exponentially above $75

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE relative to intrinsic: Paying $6.56 for calls $4 out-of-the-money

- ⏰ TIME DECAY KILLER: Theta burns -$0.04-0.06/day ($4-6 per day per contract)

- 😱 ZERO VALUE if below $75: Stock at $74 at expiration = calls worth $0 = 100% loss

- 📊 High IV crush risk: Post-earnings IV collapse could reduce call value 20-30% even if stock flat

- 🎢 Need 12%+ rally from current $71 to $81+ just to make modest profit

- ⚠️ Stock could consolidate $70-74 range and you lose entire premium despite bullish thesis correct

Estimated P&L:

- 💰 Cost: $6.56 per call ($656 per contract)

- 📈 Profit scenario: Stock at $85 by June = calls worth $10.00 = $3.44 gain (52% ROI)

- 🚀 Home run: Stock at $90 by June = calls worth $15.00 = $8.44 gain (129% ROI!)

- 📉 Loss scenario: Stock at $74 by June = calls worth $0 = -$6.56 (100% loss)

- 💀 Total loss: Stock at/below $75 = lose entire $6.56 premium (100% loss)

Breakeven point: Need stock at $81.56 by June expiration (14.8% rally from current $71.04)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can afford to lose ENTIRE premium (real possibility!)

- ✅ Understand you need 14.8% rally just to breakeven

- ✅ Comfortable with high-risk, high-reward asymmetric bet

- ✅ Have traded naked calls before and understand time decay + IV crush

- ✅ Accept that even if Delta reaches $77 (analyst targets), you could still lose money

- ⏰ Plan to actively manage: take profits early if stock rallies to $75+ well before June

- 📊 Consider selling covered calls against position if stock rallies quickly (convert to spread)

Better Alternative: Buy the $65/$75 spread for $5.42 instead - defined risk, higher probability of profit, better risk/reward for this specific setup.

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~35% (stock needs to reach $81+ for meaningful gains)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q4 Earnings in 4 weeks (Jan 9-10): Results create MAJOR volatility risk. Stock could gap 5-10% either direction based on EPS ($1.60-1.90 range), revenue growth (+2% to +4%), and 2026 guidance quality. Historical precedent shows airline stocks can swing 10-15% on earnings surprises. Premium revenue trends and corporate travel commentary will be CRITICAL.

-

💸 Valuation Extended After 103% Rally: Trading near all-time highs after massive YTD gain. Stock is priced for CONTINUED excellence - any stumble magnified. Zero margin of safety at $71. Consensus price targets of $73-$82 suggest limited upside already priced in unless execution exceeds expectations.

-

⛽ Fuel Cost Exposure With No Hedging: Delta abandoned fuel hedging after $4B losses over 8 years - fully exposed to crude oil price swings. If crude rallies to $90-100+ (geopolitical shocks, supply cuts), margins compress dramatically even with strong demand. Each $10/barrel move impacts annual costs by hundreds of millions.

-

🇨🇳 International Expansion Execution Risk: New Asia routes (Singapore, Manila, Hong Kong) require flawless execution. Delays in A350-1000 deliveries or Boeing MAX 10 certification could derail capacity growth plans. International routes take 12-18 months to mature - near-term profitability uncertain.

-

💻 CrowdStrike Litigation Wild Card: $550M outage cost with ongoing lawsuit seeking $500M+ recovery. If CrowdStrike's liability cap prevails (single-digit millions), Delta takes $500M+ write-off. DOT investigation into response could add fines/restrictions. Resolution uncertain - could be major positive or negative catalyst.

-

🛫 Southwest Competitive Threat: Southwest's 2025 pivot to assigned seating, bag charges, and premium seats directly challenges Delta's high-margin premium strategy. If Southwest executes well, could pressure pricing and market share in key domestic markets. This is Delta's MOAT being attacked.

-

📉 Macro Recession Risk: Delta withdrew 2025 guidance in April citing "growth has largely stalled" amid trade uncertainty. While momentum recovered in Q3, recession risk remains. Corporate travel demand highly cyclical - first expense cut in downturns. 90% of companies expecting steady/increased 2026 travel could flip quickly if economy weakens.

-

⚖️ Premium Revenue Growth Sustainability: Premium revenue growing 9% and on track to exceed main cabin by 2026 is the CORE thesis. But this is highly concentrated in high-income travelers and corporate clients. Any economic stress on this segment (tech layoffs, banking contraction) disproportionately impacts Delta. 38% of revenue from premium creates concentration risk.

-

🔨 Break Below $70 Triggers Technical Damage: Massive 14.9M net gamma support at $70 creates floor, but if broken, next support not until $67.50 (7.9M gamma). Could see cascade 5%+ in days if $70 fails. Spread trader would see unrealized losses expand quickly on move toward $65 strike.

-

📊 Options Overpricing Risk: With 15% implied move through June, options are EXPENSIVE. IV could be elevated relative to actual volatility Delta realizes. Even if stock grinds higher to $75, IV crush from 15% to 10% could offset gains. The spread structure partially mitigates this (selling $75 calls reduces vega exposure), but pure call buyers get crushed.

🎯 The Bottom Line

Real talk: Someone just deployed $5.6 MILLION into a structured bullish bet on Delta reaching $75 by June 2026. This isn't a YOLO gamble - this is sophisticated institutional positioning using a defined-risk spread to maximize probability-adjusted returns. They're not betting on Delta exploding to $90+ - they're making a calculated bet on a 5-6% grind higher to $75 over the next 6 months.

What this trade tells us:

- 🎯 Professional player sees CLEAR path to $75: earnings momentum, premium revenue growth, fleet expansion all aligned

- 💰 They structured intelligently: bought $65 calls (deep support) and sold $75 calls (major resistance) to reduce cost and improve probability

- ⚖️ The timing is strategic: 188 days captures Q4 earnings (Jan 9-10), 2026 guidance, fleet deliveries, and international route launches

- 📊 They paid $1.63M for position that could return $1.37M profit (85% ROI) if Delta simply reaches $75

- ⏰ Not rushing - they have 6+ months for thesis to play out through mid-2026

This IS a "continuation of the trend" signal - it's a bet that momentum sustains through multiple quarters.

If you own Delta:

- ✅ HOLD and enjoy the ride - fundamentals support higher prices

- 📊 Consider writing covered calls at $75-78 strikes (June expiration) to collect premium

- ⏰ Don't get shaken out by earnings volatility - think 6-12 month horizon

- 🎯 If stock breaks above $75, could accelerate to $78-82 on technical momentum

- 🛡️ Set mental stop at $68 (below $70 support) to protect gains if thesis breaks

If you're watching from sidelines:

- ⏰ January 9-10 Q4 earnings is the moment of truth - wait for results before entering

- 🎯 Post-earnings dip to $69-71 would be EXCELLENT entry point for shares or spreads

- 📈 Looking for confirmation: EPS at high-end $1.75-1.90 range, 2026 guidance strong, premium revenue sustaining 8%+ growth

- 🚀 Longer-term (12-18 months), international expansion execution and premium revenue reaching 40%+ mix are legitimate catalysts for $80-85

- ⚠️ Current setup near-perfect: momentum strong, gamma support at $70, catalysts aligned

If you're bearish:

- 🎯 Wait for clear break below $70 before initiating shorts - fighting all-time high breakout is dangerous

- 📊 First support at $70 (14.9M gamma), major support at $67.50 (7.9M gamma), deeper at $65

- ⚠️ Put spreads ($72.50/$67.50 or $70/$65) offer defined-risk way to play downside

- 📉 Watch for earnings disappointment or weak 2026 guidance as entry trigger

- ⏰ Timing is EVERYTHING: Premature bearish bets risk getting steamrolled into $75

Mark your calendar - Key dates:

- 📅 December 19, 2025 - Quarterly triple witch expiration (±3.5% expected move)

- 📅 January 9-10, 2026 (Friday/Monday) - Q4 FY2025 earnings report (CRITICAL!)

- 📅 January 16, 2026 - Monthly OPEX

- 📅 February 1, 2026 - SkyMiles loyalty program updates go live

- 📅 Q1-Q2 2026 - A350-1000 first deliveries begin

- 📅 Mid-2026 - New Asia routes (Singapore, Manila, Hong Kong) launch

- 📅 June 18, 2026 - Options expiration for this $5.6M bull call spread

Final verdict: Delta's story is COMPELLING. Q3 earnings beat with 15% EPS surprise, premium revenue growing 9%, corporate travel rebounding 8%, $3.5B-$4B free cash flow, aggressive international expansion, and analyst targets of $77-$90 all support higher prices. The $5.6M institutional bull call spread is validation that smart money believes in $75+ by June.

The setup is RIGHT for bullish positioning - but be patient. Wait for Q4 earnings clarity in early January, then deploy capital intelligently using defined-risk structures like spreads rather than naked calls.

This is a quality company in a momentum phase. Respect the trend, manage your risk, and let the trade work over months, not days. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The bull call spread described represents one institutional player's positioning and does not constitute a recommendation. Airlines face significant risks including fuel costs, economic cycles, competition, and operational challenges. Earnings create binary event risk with potential for 5-10% gaps either direction. Always do your own research and consider consulting a licensed financial advisor before trading. The unusual Z-scores reflect this specific trade's size relative to recent DAL history - they do not imply the trade will be profitable or that you should follow it.

About Delta Air Lines: Delta Air Lines, Inc. operates one of the world's largest carriers with a network of over 300 destinations in more than 50 countries, employing 103,000 people with headquarters in Atlanta, GA. Market cap: $46.07 billion in the Air Transportation industry.