DASH Options Analysis - February 11, 2026

🏢 Company Overview

DoorDash, Inc. (DASH) is an online delivery demand aggregator founded in 2013 that operates a marketplace connecting consumers with restaurants and other merchants. The platform enables food delivery, in-store pickup, and services for grocery, retail, and pet supplies. DoorDash has expanded internationally through acquisitions including Wolt (2022) and Deliveroo (October 2025), and is exploring innovations like drone delivery technology and autonomous robot delivery (Dot).

| Metric | Value |

|---|---|

| Market Cap | $80.01 billion |

| Sector | Business Services |

| Employees | 23,700 |

| Headquarters | San Francisco, CA |

| Current Price | $176.37 |

| 52-Week Range | $155.40 - $285.50 |

| YTD Performance | -9.7% |

📊 Today's Notable Options Activity

A significant institutional-sized options trade hit the tape this morning that deserves attention ahead of next week's earnings.

| Time | Symbol | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:29:29 | DASH | SELL | CALL | 2027-01-15 | $5,500,000 | $200.00 | 2,000 | 1,200 | 2,000 | $176.62 | $27.70 |

Strategy: Short Call (STO)

🔍 Trade Breakdown

This is a $5.5 million premium collection on a short call position with nearly a year until expiration. Let's unpack what this tells us:

Key Metrics:

- Strike: $200 (13.4% above current price)

- Premium Collected: ~$27.50 per contract ($5.5M / 2,000 contracts)

- Volume/OI Ratio: 1.67x (HIGH_ACTIVITY signal)

- Z-Score: 321.83 (EXTREMELY_UNUSUAL - this trade is a statistical outlier)

- Position Type: Sell-to-Open (new short position)

What This Trade Likely Represents:

-

Covered Call Strategy - An institution holding DASH shares is selling upside calls to generate income, willing to cap gains at $200 (a ~51% premium to consensus price targets would need to be exceeded for assignment pain).

-

Overwrite on Existing Long - With earnings on February 18, this could be a fund selling premium against a long equity position, betting that even a positive earnings reaction won't push shares above $200 by January 2027.

-

Outright Bearish/Neutral Bet - The trader is expressing a view that DASH won't reach $200 within a year, collecting rich premium in the interim.

Why It Matters: The seller is essentially saying "I don't think DASH breaks $200 in the next 11 months." Given the stock is down 36% from October 2025 highs and faces elevated 2026 investment spending, this isn't an unreasonable view. However, if Deliveroo synergies materialize faster than expected or the advertising business accelerates, this trade could be underwater.

Option Contract: DASH Jan 15 2027 $200 Call

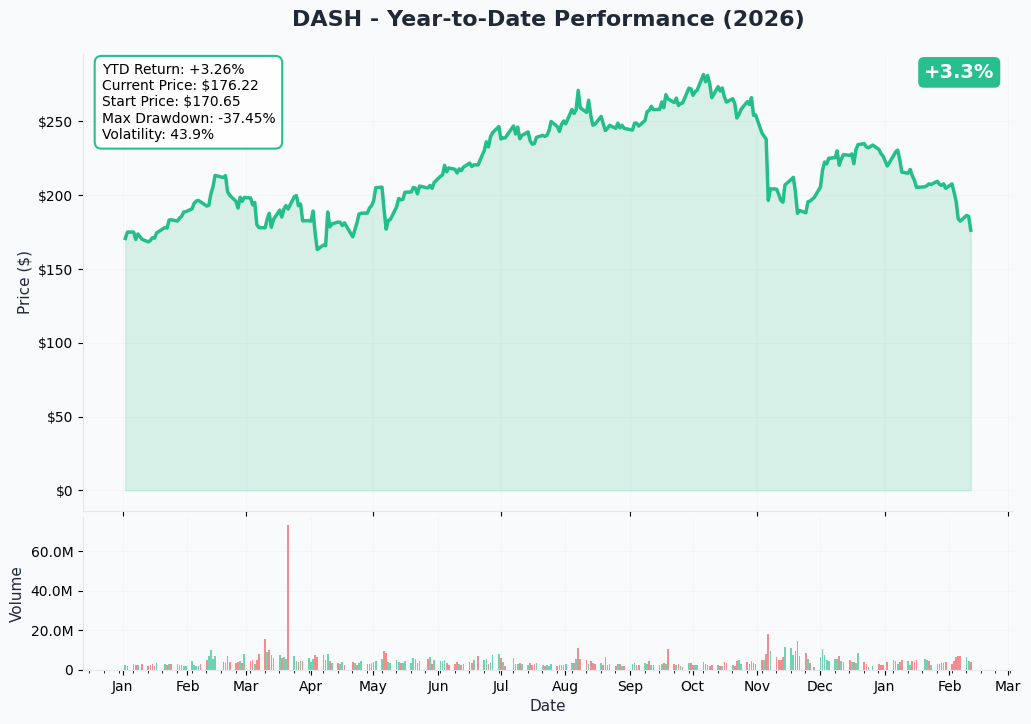

📈 YTD Price Performance

DASH has underperformed the broader market in 2026, down 9.7% year-to-date compared to the S&P 500's +1.4% gain. The pullback reflects investor concerns over management's announcement of "several hundred million dollars" in incremental 2026 investments. The stock is trading 36% below its October 2025 all-time high of $281.74.

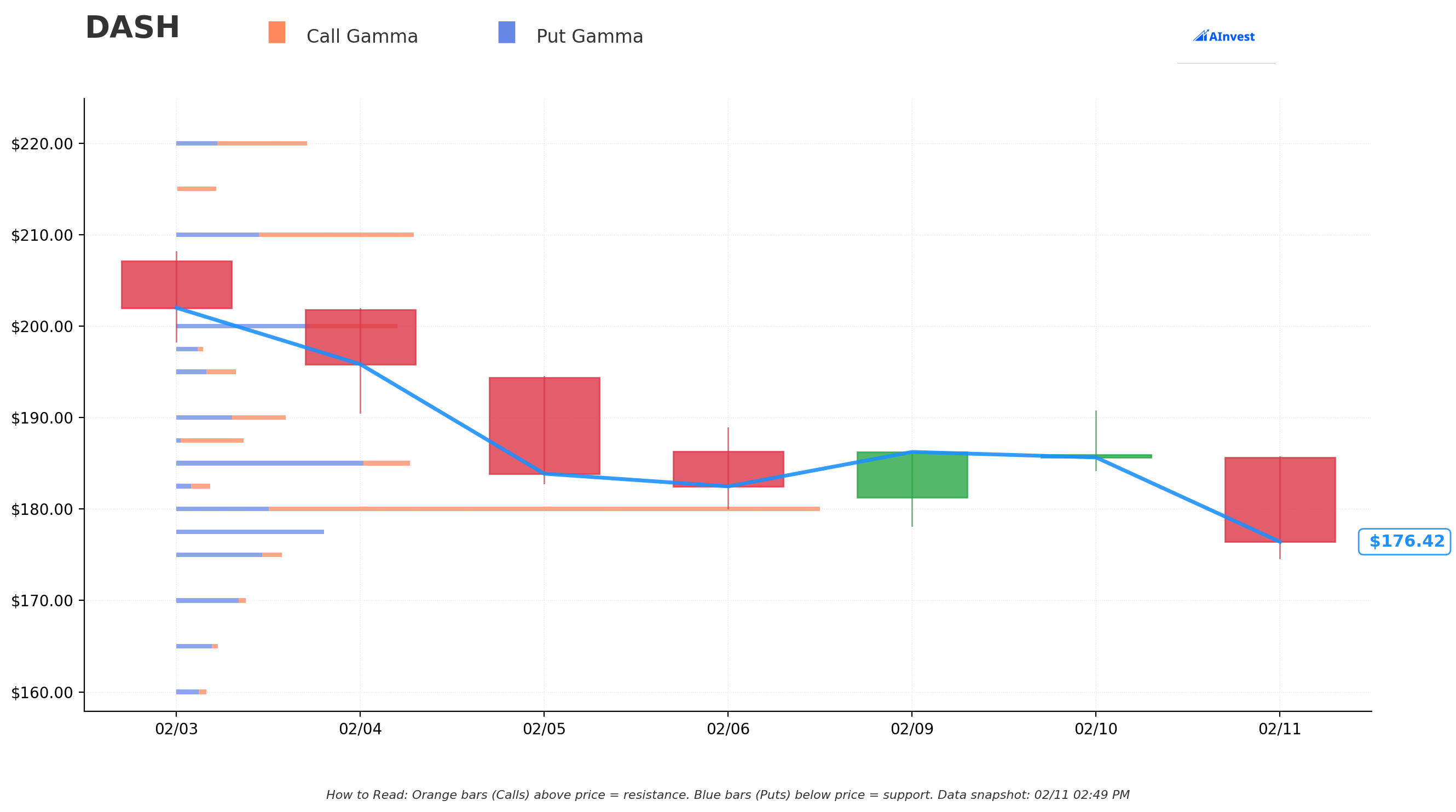

🎯 Gamma Support & Resistance Levels

Options market makers' hedging activity creates natural support and resistance zones. Here's where the gamma exposure is concentrated:

| Level | Strike | Net GEX | Distance from Spot | Significance |

|---|---|---|---|---|

| Strongest Support | $175.00 | -0.33 | -0.8% | Put gamma dominates - dealers buy dips here |

| Support | $170.00 | -0.27 | -3.6% | Secondary support zone |

| Immediate Resistance | $177.50 | -0.74 | +0.6% | Near-term ceiling |

| Key Resistance | $180.00 | +2.32 | +2.1% | Strong call gamma wall |

| Resistance | $185.00 | -0.71 | +4.9% | Aligns with recent price congestion |

| Resistance | $200.00 | -0.23 | +13.4% | Target of today's large short call |

Gamma Summary:

- Total Call GEX: 9.22 (bullish bias in aggregate)

- Total Put GEX: 6.44

- Net Bias: Slightly Bullish

The $180 strike is the most significant gamma level with strong positive GEX (+2.32), meaning dealers are net long gamma there. Expect this level to act as a magnet if the stock rallies. The $175-$177.50 zone provides near-term support.

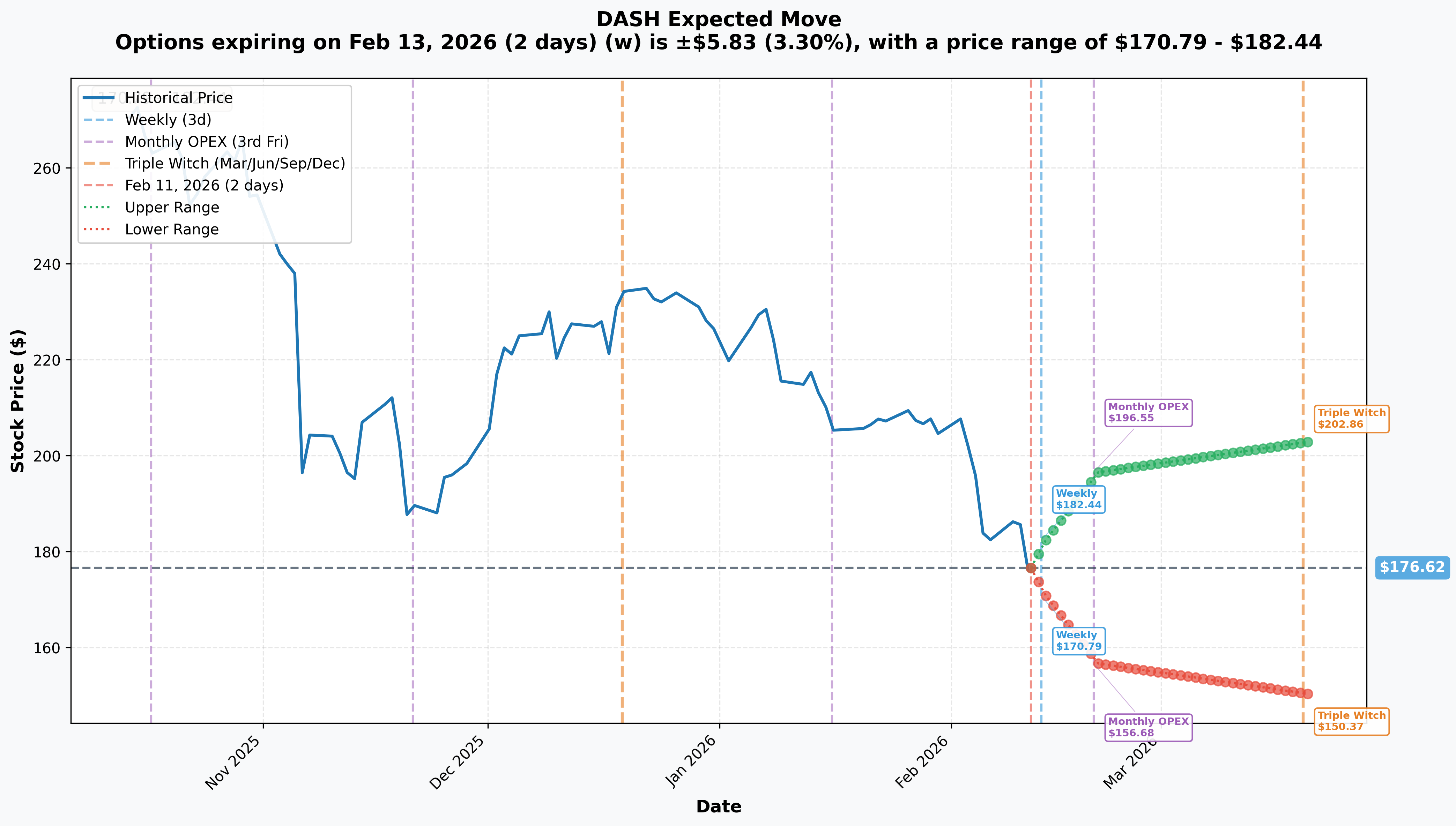

📐 Implied Move Expectations

The options market is pricing in significant volatility around earnings. Here's what the straddles imply:

| Timeframe | Expiration | Days to Expiry | Implied Move | Price Range |

|---|---|---|---|---|

| Weekly | Feb 13 | 2 | ±3.3% | $170.79 - $182.44 |

| Monthly OPEX (Earnings) | Feb 20 | 9 | ±11.3% | $156.68 - $196.55 |

| Quarterly (Triple Witch) | Mar 20 | 37 | ±14.9% | $150.37 - $202.86 |

Key Takeaway: The February 20 monthly expiration (which includes the February 18 earnings event) is pricing in an 11.3% move. This is elevated but reflects the uncertainty around 2026 guidance. The market is saying there's a reasonable probability DASH could trade anywhere from $157 to $197 post-earnings.

For context, DASH moved:

- Q3 2025 Earnings: -8% (missed EPS despite revenue beat)

- Q2 2025 Earnings: +6%

- Q1 2025 Earnings: +4%

The current implied move seems fair given the binary nature of the 2026 investment guidance that will be revealed.

🔥 Upcoming Catalysts

Confirmed Events

📅 Q4 2025 & FY 2025 Earnings Release

- Date: Wednesday, February 18, 2026 (after market close)

- Conference Call: 2:00 PM PT / 5:00 PM ET

- Access: ir.doordash.com

Consensus Estimates:

| Metric | Consensus |

|---|---|

| Revenue | $3.98B - $4.17B |

| EPS | $0.58 - $0.59 |

What to Watch:

- 2026 EBITDA guidance specificity (how much margin compression?)

- Deliveroo integration timeline and synergy realization

- DashPass/Wolt+ subscriber count (currently 26M)

- Advertising revenue growth rate (currently $1B+ annualized at 70-90% margins)

Regulatory Headwinds

📅 NYC Minimum Pay Rate Increase

- Effective Date: April 1, 2026

- New Rate: $22.13/hour (up 3.2% from current)

- Impact: Increased operating costs in DoorDash's largest U.S. market

Recent Developments

Deliveroo Acquisition (Completed October 2, 2025)

- Deal Value: $3.9B - Creates transatlantic powerhouse with 50M+ monthly active users

- 2026 EBITDA Contribution: ~$200M projected

- Synergies: $200-300M annual cost savings expected by end of 2026

Insider Activity

- Alfred Lin (Director/Sequoia): Purchased 514,000+ shares ($100.2M) in November 2025 - largest insider purchase in company history

Analyst Sentiment

- Consensus: Strong Buy (30 Strong Buy, 2 Moderate Buy, 9 Hold, 1 Strong Sell)

- Average Price Target: $276-$281 (+57% upside from current)

- Target Range: $222 (low) to $360 (high)

🎯 Price Targets & Levels

Based on gamma exposure and implied moves, here are the key levels to watch:

| Scenario | Target | Basis |

|---|---|---|

| Downside Support | $170-$175 | Gamma support + weekly implied move low |

| Near-Term Resistance | $180 | Strong gamma wall |

| Earnings Bull Case | $196-$197 | Monthly implied move upper bound |

| Earnings Bear Case | $156-$157 | Monthly implied move lower bound |

| Analyst Consensus | $276-$281 | 12-month targets (requires execution) |

💡 Trading Ideas

These are educational examples, not recommendations. Always do your own research and size positions appropriately for your risk tolerance.

Conservative: Cash-Secured Put

Rationale: If you want to own DASH at lower prices and collect premium while you wait.

- Sell: DASH Feb 20 $165 Put

- Premium: ~$3.00-$4.00

- Max Profit: Premium collected if DASH stays above $165

- Break-even: ~$161-$162

- Assignment Risk: You buy 100 shares at $165 if below at expiration

Why This Works: The $165 strike is below the implied move lower bound ($156.68). You're getting paid to potentially buy at a 6.5% discount to current levels. Even if assigned, your cost basis would be around $161-$162.

Balanced: Put Spread for Defined Risk

Rationale: Earnings uncertainty is high. This trade profits if DASH stays above $170.

- Sell: DASH Feb 20 $170 Put

- Buy: DASH Feb 20 $160 Put

- Net Credit: ~$2.50-$3.00

- Max Profit: Credit received ($250-$300 per spread)

- Max Loss: $10 width - credit = ~$7.00-$7.50 ($700-$750 per spread)

- Break-even: ~$167-$167.50

Why This Works: Gamma support sits at $170-$175. You're selling the $170 put where dealers may defend. The long $160 put caps your downside. Risk/reward is roughly 1:3 to 1:4.

Aggressive: Pre-Earnings Call Spread

Rationale: Bullish on earnings beat with upside surprise on Deliveroo synergies.

- Buy: DASH Feb 20 $180 Call

- Sell: DASH Feb 20 $195 Call

- Net Debit: ~$4.00-$5.00

- Max Profit: $15 width - debit = ~$10-$11 ($1,000-$1,100 per spread)

- Max Loss: Debit paid (~$400-$500 per spread)

- Break-even: ~$184-$185

Why This Works: You're buying at the $180 gamma wall resistance and targeting just below the implied move upper bound ($196.55). If DASH rallies 5%+ on earnings, this could pay 2:1 or better. But if earnings disappoint, you lose the full debit.

⚠️ Risk Factors

Earnings Volatility: DASH has a history of moving on earnings. The 11.3% implied move means options are expensive, and you need a big move to profit on long premium plays.

2026 Investment Uncertainty: Management has guided for "several hundred million dollars" in incremental 2026 spending. The market wants specifics. Vague guidance could pressure shares.

Regulatory Pressure: NYC minimum pay increases take effect April 1. Gig worker classification risk persists nationally.

Competitive Intensity: Uber Eats has 95M active users globally with strong rideshare cross-sell. Amazon's grocery delivery expansion is a wildcard.

Valuation: Some analysts argue DASH is overvalued despite the 36% pullback from highs. The stock trades at a premium multiple that requires growth execution.

Today's Trade Context: The $5.5M short call at $200 suggests at least one large player is skeptical of significant upside over the next 11 months. This doesn't mean they're right, but it's a data point.

📋 Bottom Line

The Setup: DASH reports Q4 2025 earnings on February 18, with the market pricing in an 11.3% move. The stock has been under pressure (-9.7% YTD) on concerns about elevated 2026 investment spending. Today's $5.5 million short call trade at the $200 strike reflects institutional skepticism about near-term upside.

The Bull Case: DoorDash dominates U.S. food delivery with 56% market share. The Deliveroo acquisition creates a global platform with $200M+ EBITDA contribution and meaningful synergies. The advertising business ($1B+ at 70-90% margins) is a high-quality earnings driver. Alfred Lin's $100M insider purchase signals Sequoia's conviction. Analyst consensus targets imply 50%+ upside.

The Bear Case: Near-term margin compression from investment spending will weigh on profitability. NYC labor regulations increase costs in the largest U.S. market. Competitive pressure from Uber Eats and Amazon threatens market share. The stock may struggle to break above the $180 gamma wall without a meaningful earnings catalyst.

The Verdict: Earnings next week will set the tone. If management provides clearer 2026 guidance and demonstrates Deliveroo synergies are on track, the stock could reclaim $180-$190. If guidance disappoints, the $170-$175 support zone will be tested. For traders, the elevated implied volatility makes defined-risk strategies (spreads) more attractive than naked long options.

Analysis generated February 11, 2026. Options involve risk and are not suitable for all investors. This is educational content, not investment advice. Always consult with a financial advisor before trading.