🛡️ DDOG $4.5M Double Put Hedge - Smart Money Protecting Cloud Software Gains!

📅 December 16, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $4.5 MILLION on DDOG puts this morning at 11:01:02 in a sophisticated two-legged defensive position! This bearish spread bought 5,755 contracts across two strikes - $140 puts expiring January 16th ($2.8M) and $120 puts expiring February 20th ($1.7M) - protecting a massive position just days before quarterly earnings and December 19th OPEX. With DDOG down -2.9% YTD at $139.45 and trapped in a downtrend from November's $201 peak, institutional money is buying insurance at critical support levels. Translation: Smart money expects more downside through Q1 2026!

📊 Company Overview

Datadog (DDOG) is a cloud-native software company dominating the infrastructure monitoring and observability space:

- Market Cap: $49.8 Billion (7th largest in software infrastructure)

- Industry: Prepackaged Software (Cloud Monitoring & Observability)

- Current Price: $139.45 (down from $201.69 52-week high)

- Primary Business: Cloud-based infrastructure monitoring platform processing machine-generated data, enabling clients to monitor servers, applications, and entire IT infrastructure with 450+ integrations

💰 The Option Flow Breakdown

The Tape (December 16, 2025 @ 11:01:02):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:01:02 | DDOG | ASK | BUY | PUT $140 | 2026-01-16 | $2.8M | $140 | 5.8K | 8.1K | 5,755 | $141.16 | $4.90 |

| 11:01:02 | DDOG | MID | BUY | PUT $120 | 2026-02-20 | $1.7M | $120 | 5.8K | 72 | 5,755 | $141.16 | $2.90 |

🤓 What This Actually Means

This is a defensive diagonal put spread on a massive long position! Here's what went down:

- 💸 Total premium invested: $4.5M ($2.8M + $1.7M across 5,755 contracts each)

- 🛡️ Near-term protection: $140 Jan puts provide 0.8% downside cushion (nearly at-the-money!)

- 📉 Deep protection: $120 Feb puts provide 14.8% downside cushion (catastrophic insurance)

- ⏰ Strategic timing: 31 days (Jan) and 66 days (Feb) capture December OPEX, Q4 earnings season, and January monthly expiration

- 📊 Identical size: 5,755 contracts on BOTH legs represents 575,500 shares worth ~$81M at current price

- 🏦 Institutional hedging: This is sophisticated portfolio protection, not a directional bearish bet

What's really happening here: This trader likely holds a MASSIVE long position in DDOG stock or calls accumulated during the rally from $82 to $201. Now, with DDOG trading in a confirmed downtrend and approaching critical support at $135-140, they're paying $4.90 per share for January $140 puts (nearly at-the-money protection!) and $2.90 per share for February $120 puts (disaster insurance). The two-legged structure shows they're worried about BOTH near-term breakdown below $140 AND a deeper correction to $120 if cloud software continues selling off.

The strategy breakdown:

- Leg 1: Jan $140 puts protect against immediate breakdown below current price (expires just after January OPEX)

- Leg 2: Feb $120 puts protect against extended selloff scenario (expires after potential Q4 earnings impact)

- Why diagonal? Different expirations create time-spread that's cheaper than buying same-dated protection at both strikes

- Total shares protected: 575,500 shares worth $81M - this is SERIOUS institutional positioning

Unusual Score: 🔥 EXTREME (8.91x average size for $140 put, 489x average size for $120 put!) - The $120 put trade is literally off the charts unusual with a z-score of 489.4. This happens maybe a few times per year. The $140 put with z-score of 8.91 is also extremely unusual. Combined premium of $4.5M for protection signals institutional fear at these levels.

📈 Technical Setup / Chart Check-Up

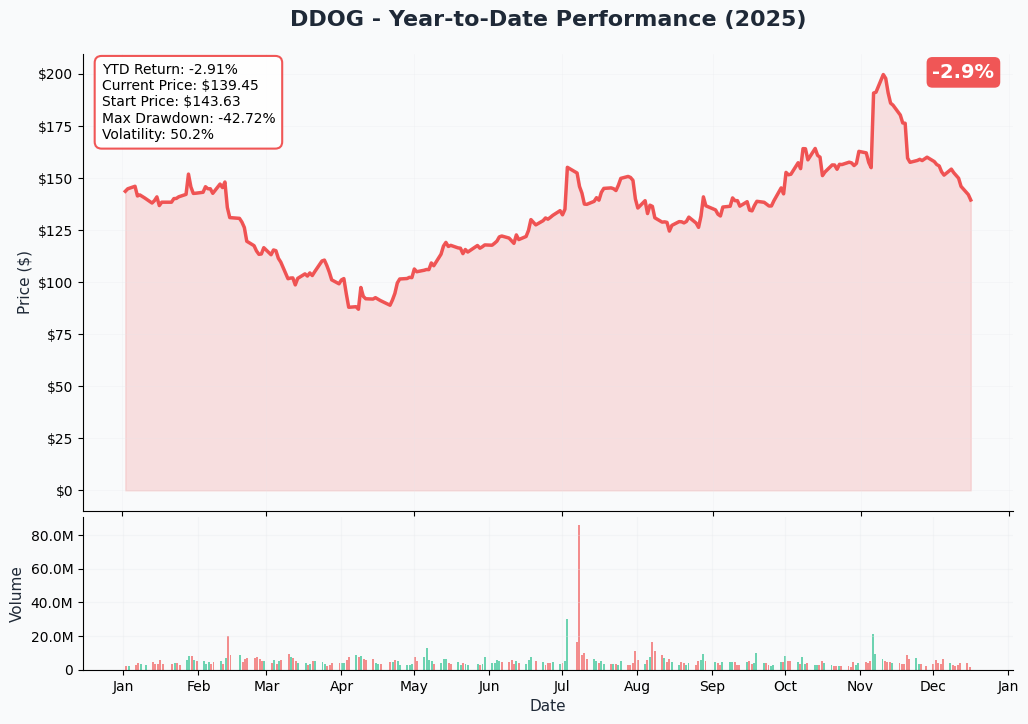

YTD Performance Chart

DDOG is struggling in 2025 - down -2.9% YTD with current price of $139.45 (started the year at $143.63). The chart tells a concerning story - after hitting an all-time high of $201.69 in November 2024, the stock has entered a confirmed downtrend, dropping 30.9% from peak to current levels.

Key observations:

- 📉 Downtrend confirmed: Steady decline from November $201 peak through December, now testing critical $135-140 support zone

- 🎢 High volatility: 50.2% annualized volatility shows this isn't a stable blue-chip software name

- 💔 Massive drawdown: -42.7% max drawdown from January highs demonstrates significant technical damage

- 📊 Volume spikes: Heavy volume in July and November during key inflection points (July recovery, November peak)

- ⚠️ Failed breakout: November rally to $201 couldn't hold - classic "bull trap" reversal pattern

- 🔴 Lower highs, lower lows: Classic downtrend structure since November - momentum clearly bearish

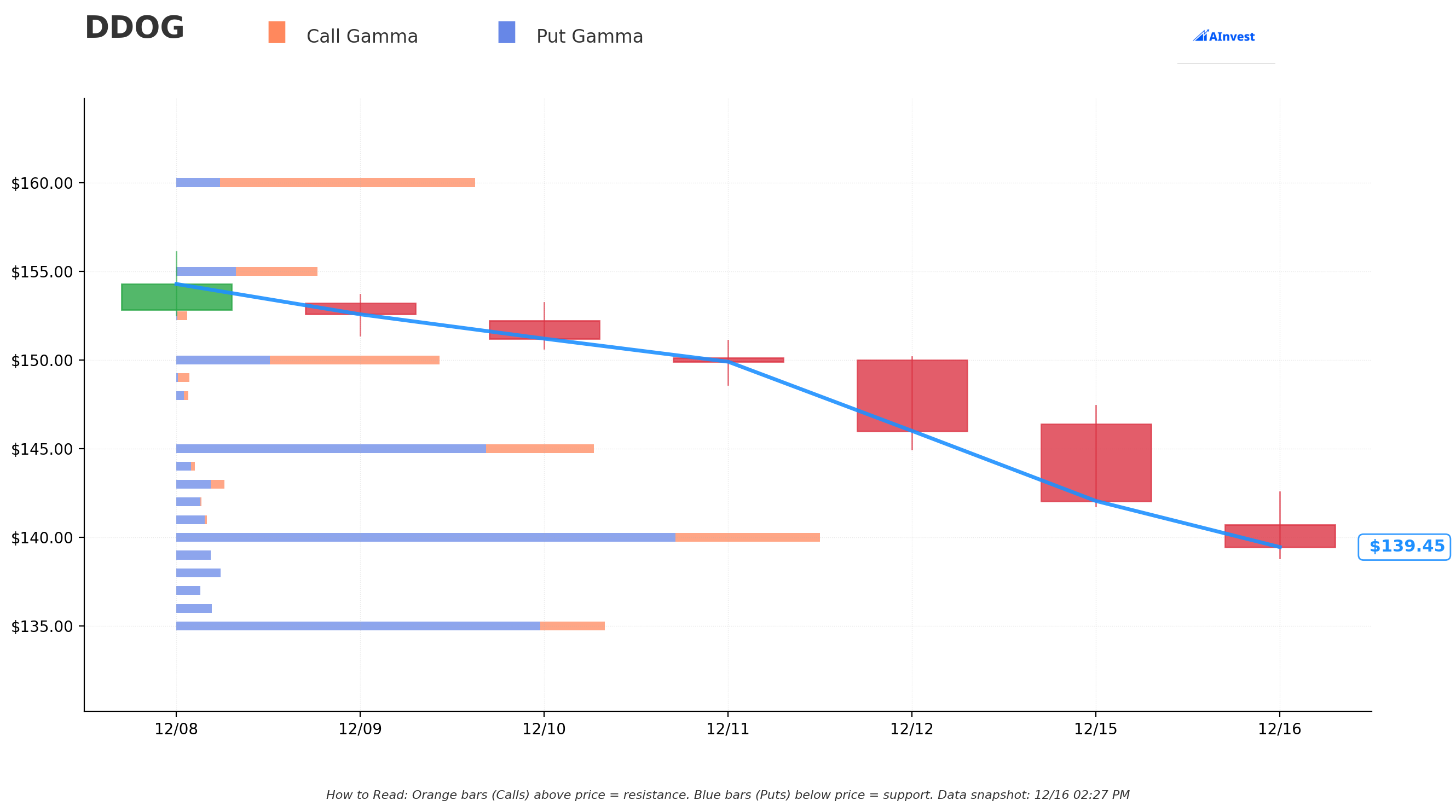

Gamma-Based Support & Resistance Analysis

Current Price: $139.45

The gamma exposure map reveals critical price magnets and barriers governing near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $135 - Immediate support with 4.19B total gamma exposure (STRONGEST NEARBY FLOOR!)

- $130 - Major structural floor with 6.41B gamma (dealers will aggressively defend this level)

- $125 - Secondary support at 1.93B gamma

- $120 - Deep support at 1.49B gamma (exactly where the second put is struck! Not coincidental)

🟠 Resistance Levels (Call Gamma Above Price):

- $140 - Immediate ceiling with 6.27B gamma (MAJOR RESISTANCE - exactly where first put is struck!)

- $145 - Secondary resistance at 4.09B gamma (3.3% overhead)

- $150 - Major ceiling zone with 2.83B gamma (positive net GEX here - first bullish level)

- $155 - Extended resistance at 1.39B gamma (11% rally required)

- $160 - Major upside target at 2.91B gamma (14.8% rally needed)

What this means for traders: DDOG is trading in a CRITICAL zone between $135 support and $140 resistance. The gamma data shows massive positioning at $140 (6.27B - the single largest nearby level) which creates natural selling pressure. This is exactly where the first put buyer struck their protection - they're betting DDOG can't break above $140 and expects downside toward $135, then potentially $130.

Notice the pattern? Both put strikes align PERFECTLY with key gamma levels:

- $140 put strike = Major gamma resistance (6.27B) - trader expects this ceiling to hold

- $120 put strike = Deep support level (1.49B gamma) - trader's disaster scenario floor

Net GEX Bias: BEARISH (15.44B call gamma vs 27.32B put gamma) - Overall positioning heavily bearish with nearly 2:1 put/call ratio. Dealers are short puts and long calls, creating downward pressure on rallies and muted support on dips. This setup favors continued downside.

Critical insight: The strongest nearby support at $135 (4.19B gamma) is only 3.1% below current price. If DDOG breaks $135, momentum accelerates toward $130 where the massive 6.41B gamma wall sits. This is the trader's expected path - hence the aggressive put buying.

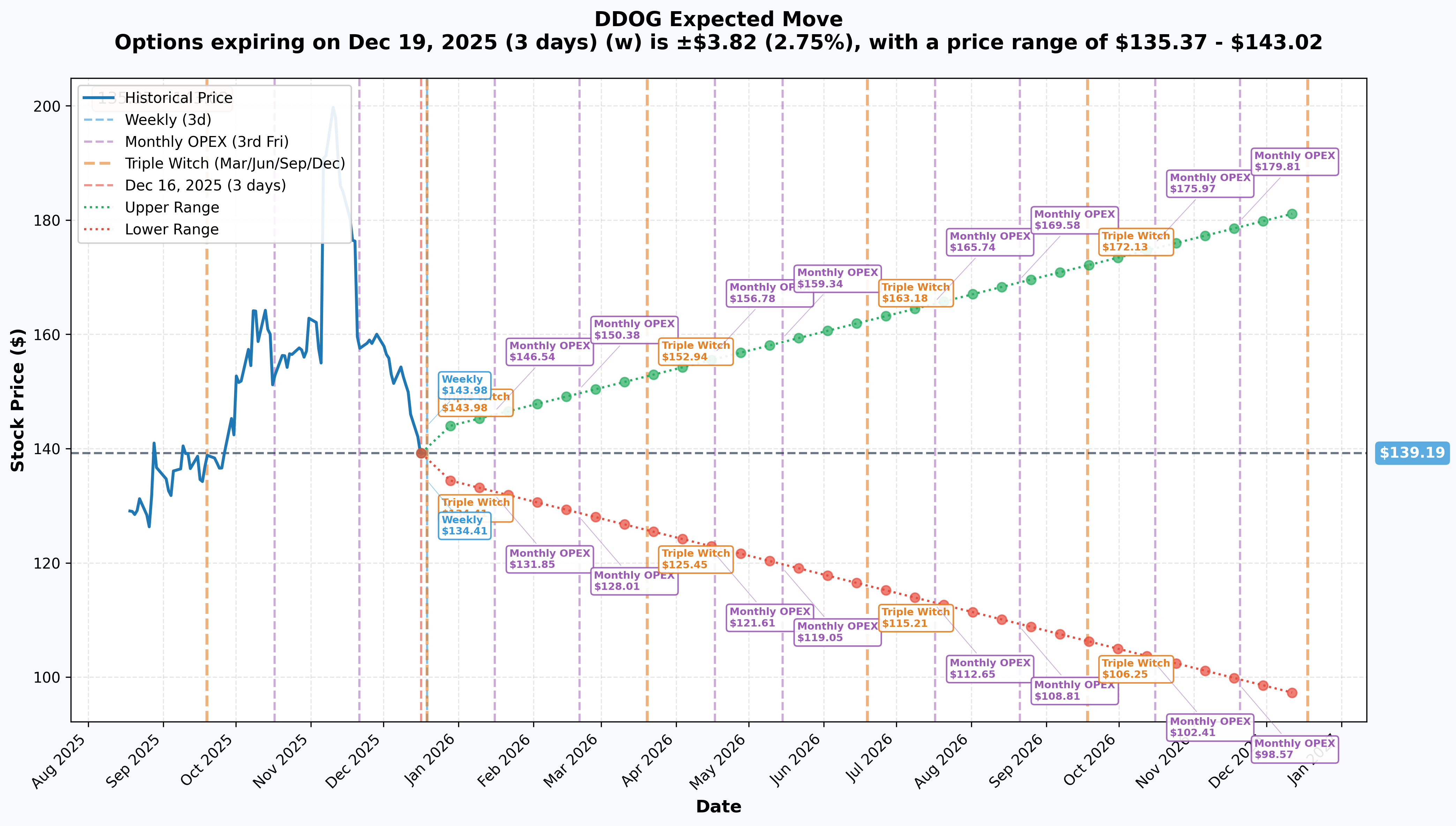

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly/OPEX (Dec 19 - 3 days): ±$3.82 (±2.75%) → Range: $135.37 - $143.02

- 📅 January OPEX (Jan 16 - 31 days - FIRST PUT EXPIRES!): ±$7.35 (±5.29%) → Range: $131.85 - $146.54

- 📅 February OPEX (Feb 20 - 66 days - SECOND PUT EXPIRES!): ±$11.19 (±8.04%) → Range: $128.01 - $150.38

- 📅 Quarterly Triple Witch (Mar 20 - 94 days): ±$13.75 (±9.88%) → Range: $125.45 - $152.94

Translation for regular folks: Options traders are pricing in a 2.75% move ($3.82) by December 19th OPEX just 3 days away, with a lower range of $135.37 - dangerously close to breaking key $135 support. The January expiration (when the first put expires) has a lower range of $131.85, meaning the market thinks there's a real possibility DDOG trades as low as $132 over the next month - that's 5.3% downside.

The February expiration (when the second put expires) has a lower range of $128.01 - just 8% above the $120 put strike! This aligns perfectly with the put buyer's thesis: protect against a 8-15% drawdown over the next 2 months if cloud software sector continues weakening or earnings disappoint.

Key insight: The implied volatility term structure shows INCREASING uncertainty over time - weekly IV of 2.75% expanding to 8.04% by February. This suggests the market expects catalysts (earnings, guidance, macro events) to drive volatility higher in Q1 2026. Smart money is paying up for protection into this uncertain period.

🎪 Catalysts

🔥 Immediate Catalysts (Next 7 Days)

December 19, 2025 - Triple Witch OPEX (3 DAYS AWAY!) 📊

Weekly, monthly, and quarterly options all expire simultaneously on Thursday, December 19th. This is a major technical catalyst that often creates outsized volatility:

- 📊 Implied move: ±2.75% ($135.37 - $143.02 range) through expiration

- 🎯 Critical level: $140 sits right at the top of the weekly expected range - breaking above would be bullish, failing below confirms bearish setup

- 📈 Gamma positioning: Massive gamma exposure at $135 and $140 will create pinning effects as market makers hedge

- ⚠️ Downside risk: Lower range of $135.37 is just below key $135 support - break below triggers cascade to $130

What to watch:

- If DDOG breaks below $135 before December 19th, expect accelerated selling as gamma support evaporates

- If DDOG holds above $140, could squeeze higher briefly before rolling over (typical OPEX pattern)

- Heavy put positioning suggests dealers will allow downside but resist upside

🚀 Near-Term Catalysts (Next 3 Months)

Q4 2025 & Full Year Earnings - Expected Late January/Early February 2026 📊

While DDOG hasn't announced Q4 earnings date yet, based on historical patterns (Q3 was November 7, Q4 FY2024 was February 13), expect Q4 FY2025 earnings in early February 2026 - falling between the two put expirations! According to the catalyst research, this is THE catalyst that could make or break the current technical setup.

What Wall Street is watching:

Full Year 2025 Guidance (provided February 13, 2025):

- 📊 Revenue: $3.175B - $3.195B (~19% YoY growth) - significant deceleration from 26% in FY2024

- 💰 Non-GAAP EPS: $1.65 - $1.70

- 📉 Operating Margin: ~21% (DOWN 400bps from FY2024's 25% - major compression!)

Key metrics to monitor:

- 🤖 AI-native customer revenue: Growing from 6% to 8.5% in Q1 2025 - is this trend accelerating?

- 📈 Dollar-based net retention: Currently high 110%s (down from historical 150-170% peaks) - further decline would be catastrophic

- 🏢 $1M+ ARR customers: 462 customers (+17% YoY) - growth rate slowing?

- 💸 Free cash flow: $775M annually - margins under pressure from 31% sales/marketing and 29% R&D expense growth

Upside surprise potential: 30+ new products from DASH 2025 conference (GPU Monitoring, Bits AI SRE, LLM Experiments) could drive material upsell in Q4 if adoption accelerates. Strategic acquisitions of Eppo and Metaplane expand platform capabilities in AI observability.

Downside risk factors: Conservative 2025 guidance already bakes in cloud optimization headwinds, margin compression of 400bps, and slower growth (19% vs 26%). Any incremental negative surprises on retention rates, AI monetization delays, or macro weakness could trigger sharp selloff. Intense competition from Dynatrace, Splunk, and Microsoft creates pricing pressure.

Critical timing: Q4 earnings likely lands BETWEEN the two put expirations (after Jan 16, before Feb 20). This suggests the trader expects:

- Near-term weakness into/through January expiration (first put protects this)

- Potential earnings disappointment or weak guidance drives deeper correction into February (second put protects this)

DASH 2025 Product Ramp - Q4 2025 through Q1 2026 🚀

Major product announcements from June 2025 DASH conference begin contributing to revenue:

-

AI/ML Monetization Suite:

- GPU Monitoring for AI workload optimization

- LLM Experiments for entire LLM application lifecycle

- AI Agents Console with execution flow visualization

- Expected to drive AI-native revenue beyond current 8.5%

-

Bits AI SRE (Autonomous Investigations):

- Always-on-call engineer investigating alerts autonomously

- Accelerates root cause analysis, reduces on-call fatigue

- Potential enterprise upsell opportunity

-

Security Expansion:

- Bits AI Security Analyst for SIEM signal triage

- Sensitive Data Scanning for AI training datasets

- Cloud Security for Amazon Bedrock

- IaC Security with 180+ one-click remediations

-

Enterprise Features:

- Internal Developer Portal (IDP) with Software Catalog

- Voice Interface for Incident Response

- Natural Language Queries for logs

- End User Device Monitoring

Revenue impact timeline: New products typically take 2-3 quarters to materially impact revenue. DASH 2025 products launched June 2025 likely contribute incrementally in Q4 2025, with meaningful impact expected H1 2026. If adoption disappoints or enterprise sales cycles elongate, could pressure growth expectations.

Strategic Acquisitions Integration:

- Eppo Acquisition (May 2025): Feature flagging and experimentation platform - integration execution risk through Q1 2026

- Metaplane Acquisition (April 2025): Data observability platform - cross-sell opportunity to existing customer base

⚠️ Risk Catalysts (Negative)

Cloud Optimization Headwinds (High Severity - ONGOING):

Management explicitly cited cloud optimization as persistent headwind pressuring consumption growth and dollar-based net retention:

- 🚨 Customers continue optimizing cloud spend, reducing monitoring data ingestion

- ⚖️ While intensity has moderated, risk remains structural challenge through 2025-2026

- 📉 Dollar-based net retention at high 110%s vs historical 150-170% peaks shows ongoing pressure

- 💸 Consumption-based pricing model creates revenue volatility when customers cut usage

- Impact: Growth deceleration from 26% to ~19% YoY in 2025 guidance reflects this headwind

Margin Compression in 2025 (Medium Severity):

FY2025 operating margin guidance of ~21% down 400bps from FY2024's 25% raises profitability concerns:

- 💰 Heavy investments in product development and sales/marketing

- 📊 Sales & marketing expense grew 31% YoY, R&D expense grew 29% YoY in Q4 2024

- ⏰ Management frames this as "reset year" with margins expected to rebound in 2026

- ⚠️ If investments don't drive re-acceleration, market will punish stock further

- Impact: Near-term profitability pressure creates overhang on valuation multiple

Competition Intensity (High Severity):

Highly competitive market with well-funded giants and specialized vendors:

- ⚖️ Dynatrace: 4.6 Gartner rating vs DDOG's 4.5, superior AI-powered intelligence, better Kubernetes discovery

- 💪 Splunk: Leader in log management and SIEM, superior security monitoring, advanced customization

- 🏢 Microsoft, IBM: Greater financial resources, brand recognition, larger sales forces, broader IP portfolios

- 🆕 New Entrants: Market continues attracting companies with innovative approaches (Grafana Labs, Elastic)

- 💸 Pricing pressure: Competitors can leverage superior resources to discourage DDOG purchases

- Impact: Market share erosion risk if DDOG fails to maintain innovation leadership

Macroeconomic Uncertainty (Medium Severity):

Economic headwinds pose risks to enterprise IT spending:

- 📉 Inflation, higher interest rates may reduce enterprise IT budgets

- 🌍 Geopolitical risks (2025 outlook explicitly mentions this as temporary slowdown driver)

- ⏰ Deal cycle elongation and delayed purchasing decisions

- 💔 Reduced economic growth correlates with decreased IT spending

- ✅ Partial offset: Platform helps customers "save money and move faster" per management

- Impact: Revenue visibility concerns and potential guidance reductions

Valuation Risk at 18.7x EV/Sales (Medium Severity):

Trading at elevated multiples despite growth deceleration:

- 📊 EV/Sales: 18.7x (52-week range: 13.92x - 22.36x)

- 💰 Forward P/E: 70.46x - rich for software company decelerating from 26% to 19% growth

- ⚖️ Historical context: Current 18.7x vs 5-year average of 19.77 - not cheap by historical standards

- 📉 2025 guidance implies significant deceleration, yet multiple hasn't compressed proportionally

- ⚠️ Limited margin for error - any disappointment magnified at these valuations

- Impact: Downside to 13-15x EV/Sales ($100-115 price target) if execution stumbles

Insider Selling Activity (Low-Medium Severity):

Recent insider transactions raise concerns:

- 🚨 CEO Olivier Pomel sold $7.5M in shares

- 📉 Director Matthew Jacobson reduced stake by 11.7%

- ❌ All insider transactions in past 3 months have been SALES ONLY

- Impact: Potential signal of insider confidence concerns about near-term prospects

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through February 20th expiration:

📉 Bear Case (45% probability)

Target: $120-$130 (TEST BOTH PUT STRIKES!)

How we get there:

- 😰 December 19th OPEX sees DDOG break below $135 support with accelerating volume

- 📉 Failed rally attempt at $140 resistance confirms downtrend continuation

- 🚨 Q4 earnings (early February) miss or deliver weak FY2026 guidance citing prolonged cloud optimization

- 💔 Dollar-based net retention deteriorates further below 110% - structural concern emerges

- 📊 AI-native customer growth stalls or decelerates from 8.5% - AI monetization story questioned

- 🏢 Major customer(s) reduce spend or churn, announced in earnings call

- 💸 Margin compression worse than expected (below 21%) as sales/marketing costs stay elevated

- ⚖️ Competition intensifies - Dynatrace or Splunk wins key enterprise deals

- 📉 Broader tech selloff or macro recession fears pressure all cloud software

- 🔨 Break below $130 gamma support triggers cascade to $120 deep support

Key levels breakdown:

- 🛡️ $135: MUST HOLD or momentum shifts decisively bearish (4.19B gamma support)

- 🛡️ $130: Major floor (6.41B gamma) - if this breaks, free-fall to $120

- 🛡️ $120: Deep disaster support (1.49B gamma) + second put strike - likely heavy buying here

Probability assessment: 45% because multiple warning signs already flashing - confirmed downtrend from $201, negative YTD returns, margin compression guidance, slowing growth, persistent cloud optimization headwinds, and THIS MASSIVE PUT BUY. The trader clearly thinks this scenario has >45% odds or they wouldn't pay $4.5M for protection.

Put P&L in Bear Case:

- Jan $140 puts: Stock at $130 = puts worth $10.00, profit = $5.10/share × 5,755 = $2.9M gain (103% ROI on this leg!)

- Feb $120 puts: Stock at $120 = puts worth $0 (at-the-money), loss = -$2.90/share × 5,755 = -$1.7M (100% loss on this leg)

- Combined scenario (stock at $125): Jan puts profit ~$3M, Feb puts profit ~$1.4M = Total gain ~$4.4M on $4.5M investment

🎯 Base Case (35% probability)

Target: $130-$145 range (CHOPPY CONSOLIDATION IN DOWNTREND)

Most likely scenario:

- ⚖️ December 19th OPEX volatility but no decisive break of $135 support or $145 resistance

- 📊 Continued grinding action within gamma support ($130-135) and resistance ($140-145) bands

- ✅ Q4 earnings meet reduced expectations but don't inspire - "good enough" result

- 📱 AI-native customer growth continues but doesn't re-accelerate meaningfully

- 💰 Margins come in at guided 21% - no positive surprise

- 🔄 Cloud optimization headwinds persist but don't worsen dramatically

- 💤 Market digests 2025 "reset year" narrative, waits for 2026 margin recovery proof

- 📉 Overall trend remains down but not collapsing - slow bleed lower

- 🎢 Volatility remains elevated (50%+ IV) keeping options expensive

This scenario still validates the put buy: Stock consolidates in $130-140 range, January $140 puts might show small profit or loss depending on where stock settles, February $120 puts likely expire worthless but provided peace of mind during uncertain period. The $4.5M is the "insurance premium" they're willing to pay.

Why 35% probability: Stock at technical inflection point with confirmed downtrend but approaching major support. Fundamentals solid (strong FCF, AI growth story, competitive moat) but valuation rich and growth decelerating. Most likely path is continued weakness but not catastrophic breakdown - classic "death by a thousand cuts" software stock pattern.

📈 Bull Case (20% probability)

Target: $150-$165

How we get there (requires multiple surprises):

- 💪 December OPEX volatility creates V-bottom at $135, aggressive short covering rally

- 🚀 Q4 earnings BLOWOUT with revenue above $800M, beating deceleration narrative

- 🤖 AI-native customers surge to 10%+ of revenue, validating AI monetization thesis

- 📈 Dollar-based net retention IMPROVES back toward 120%+ - inflection point

- 💰 Margin compression story flips - company announces 2026 margin expansion to 23-25%

- 🏆 DASH 2025 products show faster-than-expected adoption with material Q4 impact

- 📊 Major strategic partnership announced (AWS deepening, Google Cloud, Microsoft)

- 🎯 Management raises FY2026 guidance dramatically above Street expectations

- 💸 Cloud optimization headwinds officially declared "behind us"

- 📈 Breakout above $145 resistance triggers short squeeze to $150, then $160

Why only 20% probability: Requires PERFECT execution across multiple fronts with stock already in confirmed downtrend after -31% decline from peak. Management explicitly guided to "reset year" with margin compression and slower growth. The $4.5M institutional put buy signals smart money does NOT expect this scenario. Gamma resistance at $140-145 creates significant technical headwinds. Would need major positive catalyst to reverse current bearish momentum.

Put P&L in Bull Case: Both puts expire worthless, total loss of $4.5M (100% of premium). But remember - the trader's underlying long position (likely $81M worth) would gain $8-18M, more than offsetting put losses. That's the whole point of hedging.

💡 Trading Ideas

🛡️ Conservative: Cash Gang Until Technical Reversal

Play: Stay on sidelines until DDOG shows clear technical reversal above $145 OR capitulation to $120

Why this works:

- ⏰ December 19th OPEX in 3 days creates binary event risk with ±2.75% implied move

- 📉 Confirmed downtrend from $201 to $139 (-31%) with no signs of reversal yet

- 💸 Options EXTREMELY expensive with 50%+ implied volatility - premium sellers' market, not buyers'

- 📊 Stock trading between major gamma levels ($135 support, $140-145 resistance) - choppy action likely

- 🛡️ The $4.5M institutional put buy signals smart money is WORRIED - why fight the tape?

- ⚖️ Better to wait for clarity: either bounce above $145 (trend change) or capitulation to $120 (value entry)

Action plan:

- 👀 Watch December 19th OPEX closely - does DDOG hold $135 or break below?

- 🎯 If breaks below $135, wait for stabilization at $120-125 deep support (15% lower) for stock entry

- ✅ If breaks above $145, consider re-entering on confirmed uptrend with stop below $140

- 📊 Monitor Q4 earnings (early Feb) for inflection in cloud optimization or retention trends

- ⏰ Until one of these catalysts provides clarity, cash is a position

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -10-20% drawdown if bear case plays out. Get better entry if stock capitulates to $120 or confirms reversal above $145. Maintain optionality.

⚖️ Balanced: Post-OPEX Put Credit Spread (Copy The Pros)

Play: After December 19th OPEX, sell put credit spread in the gamma support zone

Structure: Sell $130 puts, Buy $125 puts (January 16 expiration - SAME as first put trade)

Why this works:

- 🎢 IV crush after OPEX volatility makes put spreads attractive - collect premium as fear subsides

- 📊 Defined risk spread ($5 wide = $500 max risk per spread)

- 🎯 Targets massive gamma support zone at $130 (6.41B gamma) where institutions clearly positioned

- 🤝 Essentially betting AGAINST the extreme bearish scenario, fading the panic

- ⏰ 28 days post-OPEX to expiration gives time for any bounce or stabilization

- 💰 If DDOG holds above $130, collect full premium; even at $125-130 only partial loss

Estimated P&L (adjust after seeing post-OPEX IV):

- 💰 Collect ~$1.50-2.00 credit per spread (adjust based on where stock trades)

- 📈 Max profit: $150-200 if DDOG above $130 at January expiration (60-80% ROI)

- 📉 Max loss: $300-350 if DDOG below $125 (defined and limited)

- 🎯 Breakeven: ~$128

- 📊 Risk/Reward: ~1:2 to 1:1.5 which is favorable for defined-risk bullish play

Entry timing:

- ⏰ Wait until December 20-23 (after OPEX) for IV normalization

- 🎯 Only enter if stock trades $133-137 (gives cushion to $130 support)

- ❌ Skip if stock already below $130 (spread too close to danger zone)

- 📊 Look for RSI oversold condition or volume exhaustion signals

Position sizing: Risk only 2-5% of portfolio (this is defined-risk mean-reversion play)

Exit plan:

- ✅ Take profit at 50-60% max gain (close at $0.60-0.80 debit if sold at $1.50-2.00 credit)

- ⏰ Don't hold to expiration if stock approaching $130 - close early to limit loss

- 📉 If stock breaks below $130, accept loss and exit (don't let it ride to $125)

Risk level: Moderate (defined risk, bullish/neutral stance) | Skill level: Intermediate

🚀 Aggressive: Strangle Into Earnings Volatility (ADVANCED ONLY!)

Play: Sell strangle betting on range-bound action through January expiration

Structure: Sell $125 puts + Sell $150 calls (January 16 expiration)

Why this could work:

- 💰 HIGH PREMIUM: Collect $4-6 per share ($400-600 per strangle) due to elevated 50%+ IV

- ⚖️ Defined range: Betting DDOG stays between $125 and $150 (±11% range from $137 midpoint)

- 📊 Gamma support: $125 has 1.93B gamma support, $130 has 6.41B - strong floor

- 🛡️ Resistance ceiling: $145-150 has significant call gamma creating natural ceiling

- ⏰ Theta decay: Collect $20-30/day in time decay as options approach expiration

- 📈 High probability: ~65-70% chance of profit if range holds

Why this could blow up (SERIOUS RISKS):

- 😱 UNLIMITED UPSIDE RISK: If DDOG rallies above $150, losses accelerate quickly (short naked call)

- 📉 SUBSTANTIAL DOWNSIDE RISK: If DDOG crashes below $125, losses mount (though put risk capped at $0)

- 🎰 Earnings risk: Q4 earnings likely in late January/early Feb - could gap through strikes

- 💣 Two-way risk: Unlike directional trade, you lose if stock moves strongly EITHER direction

- ⚠️ Margin requirements: Need significant buying power ($5,000-10,000 per strangle)

- 🔨 Liquidity risk: DDOG options can have wide spreads - difficult to exit in panic

Estimated P&L:

- 💰 Premium collected: ~$4-6 per strangle ($400-600)

- 📈 Max profit: Full premium if DDOG between $125-150 at expiration (100% ROI)

- 📉 Upside loss: UNLIMITED if DDOG rallies through $150 (every dollar above $150 = $100 loss per contract after breakeven)

- 📉 Downside loss: Substantial if DDOG crashes below $125 (every dollar below $125 = $100 loss per contract after breakeven)

- 🎯 Breakeven points: ~$119-121 downside, ~$154-156 upside (depending on premium collected)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Have traded short strangles before and understand unlimited risk mechanics

- ✅ Can afford to take assignment of 100 shares at $125 ($12,500 per contract)

- ✅ Have sufficient margin and won't get margin call if stock moves 10-15%

- ✅ Can monitor position daily and adjust/close if stock approaches strikes

- ✅ Accept that Q4 earnings could gap stock through your strikes overnight

- ⏰ Plan to manage actively - close winner side early, roll losing side if threatened

- 🚨 Consider defined-risk iron condor instead: Add protective wings (buy $120 put, buy $160 call) to cap max loss

Alternative (Safer): Iron Condor

- Sell $125 put, buy $120 put, sell $150 call, buy $160 call

- Reduces premium collected to $2-3 but caps max loss at $500-700

- Much more appropriate for most traders

Risk level: EXTREME (unlimited upside risk, substantial downside risk) | Skill level: Advanced only

Probability of profit: ~65-70% (higher than directional trades due to range-bound thesis)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ December 19th OPEX in 3 days: Triple Witch expiration creates MASSIVE volatility risk. Implied move of ±2.75% takes stock to $135.37 - $143.02 range. Critical $135 support could break, triggering cascade to $130. Or squeeze to $143 possible if shorts cover. This binary event makes positioning extremely dangerous until resolution.

-

📉 Confirmed technical downtrend: Stock down -31% from November $201 peak to current $139 with clear pattern of lower highs and lower lows. YTD returns negative (-2.9%) despite broader tech strength. Failed breakout at $201 created "bull trap" reversal. No signs of trend reversal yet - momentum remains decisively bearish. Falling knife scenario.

-

💸 Valuation still elevated despite deceleration: Trading at 18.7x EV/Sales and 70.5x forward P/E for company decelerating from 26% to 19% growth with margin compression of 400bps to 21%. This is NOT cheap - requires perfect execution to justify. Historical average EV/Sales of 19.77x vs current 18.7x shows limited valuation support. Downside to 13-15x EV/Sales implies $100-115 price target if execution stumbles.

-

😰 Cloud optimization headwinds remain structural challenge: Management explicitly cited this as persistent pressure on consumption growth and dollar-based net retention (now high 110%s vs historical 150-170% peaks). Customers continue reducing monitoring data ingestion to cut costs. Consumption-based pricing model creates revenue volatility. This isn't temporary - it's the new normal until macro improves.

-

⚖️ Margin compression in "reset year" 2025: FY2025 operating margin guidance of ~21% down 400bps from FY2024's 25% as company invests heavily (sales/marketing +31% YoY, R&D +29% YoY). Management frames as investment cycle with rebound in 2026, but what if investments don't drive re-acceleration? Profitability concerns at these valuation multiples.

-

🏢 Intense competition from well-funded giants: Dynatrace (4.6 Gartner rating vs DDOG's 4.5) offers superior AI-powered intelligence. Splunk dominates SIEM and log management. Microsoft, IBM have greater financial resources and distribution. Market continues attracting new entrants (Grafana, Elastic). Pricing pressure and customer acquisition costs increasing. Market share erosion risk if DDOG loses innovation edge.

-

🚨 $4.5M institutional put buy is MAJOR WARNING SIGNAL: This sophisticated two-legged hedge (8.91x and 489x unusual scores) signals smart money expects downside through Q1 2026. When funds managing tens of millions pay $4.5M for protection at nearly at-the-money strikes rather than staying fully long, it's a caution flag. The $140 put is basically current price - they expect immediate weakness. The $120 put 15% below suggests disaster scenario hedging.

-

📊 Gamma positioning heavily bearish: Net GEX shows 27.32B put gamma vs 15.44B call gamma - nearly 2:1 put/call ratio. Dealers are short puts and long calls, creating mechanical downward pressure on rallies and muted support on dips. This setup favors continued downside. Strongest resistance at $140 (6.27B gamma) exactly where stock is trapped.

-

💰 Q4 earnings timing creates uncertainty: Expected late January/early February 2026 - falling between the two put expirations. This suggests trader expects potential disappointment or weak guidance. Key risks: AI monetization slowing, retention rates declining further, margin compression worse than expected, competition intensifying. Even "meet" could disappoint given elevated expectations.

-

💔 Insider selling raises red flags: CEO Olivier Pomel sold $7.5M in shares, Director Matthew Jacobson reduced stake by 11.7%, and ALL insider transactions in past 3 months have been sales only. When company insiders are net sellers at current levels, it signals concerns about near-term prospects. They know more than we do.

-

📉 Macroeconomic headwinds if recession emerges: 2025 outlook explicitly cites geopolitical risks and economic uncertainty. Enterprise IT spending highly cyclical - cuts come fast in downturns. Deal cycle elongation already occurring. If economy weakens in 2026, even strong execution won't prevent 30-40% correction. At 18.7x EV/Sales with slowing growth, DDOG has zero recession protection.

🎯 The Bottom Line

Real talk: Someone just spent $4.5 MILLION protecting a massive DDOG position with a sophisticated two-legged put hedge just 3 days before December OPEX and ahead of Q4 earnings in early 2026. This isn't bearish on DDOG's long-term observability leadership story - it's smart risk management by institutions who rode the rally from $82 to $201 and don't want to give back gains in the confirmed downtrend.

What this trade tells us:

- 🎯 Sophisticated player expects VOLATILITY and DOWNSIDE through Q1 2026 (not just consolidation, actual weakness)

- 💰 They're worried enough about immediate breakdown to pay $4.90 for $140 puts that are nearly at-the-money (only 0.8% out!)

- 📉 The $120 Feb puts 15% below current price signal hedging against disaster scenario if earnings disappoint or cloud optimization worsens

- ⚖️ The two-leg structure (Jan + Feb expirations) shows they're protecting BOTH near-term OPEX volatility AND post-earnings weakness

- 📊 They structured at gamma support levels ($140 resistance, $120 deep support) - expects breakdown through $135, acceleration to $130, possibly $120

- ⏰ Timing is CRITICAL: 3 days before triple witch OPEX, ahead of Q4 earnings, during confirmed downtrend

This is NOT a "sell everything" signal - it's a "the trend is your friend and it's pointing down" signal.

If you own DDOG:

- ⚠️ Consider trimming 30-50% at $139-141 levels if you're sitting on gains from lower prices

- 📊 Set HARD STOP at $134 (just below $135 gamma support) to protect remaining position

- ⏰ Don't fight the downtrend - stock needs to prove itself above $145 to reverse bearish momentum

- 🎯 If December OPEX breaks $135, expect acceleration to $130 - be prepared to exit or hedge

- 🛡️ If holding through Q4 earnings, consider buying protective $135 or $130 puts (copy structure at smaller size)

If you're watching from sidelines:

- ⏰ December 19th OPEX is first test - does DDOG hold $135 or break below?

- 🎯 Capitulation to $120-125 would be EXCELLENT entry (15% lower) with massive gamma support and discount to peak

- 📈 Looking for confirmation of: Cloud optimization moderating, retention stabilizing at 110%+, AI revenue accelerating to 10%+, margin expansion guidance for 2026

- 🚀 Longer-term (6-12 months), AI/ML observability leadership and strategic acquisitions are legitimate catalysts for $160-180 IF execution delivers

- ⚠️ Current valuation (18.7x EV/Sales) with decelerating growth and margin compression requires flawless execution - one stumble and it's $100-115

If you're bearish:

- 🎯 December OPEX provides natural setup for breakdown below $135 - watch for volume confirmation

- 📊 First target $130 (major gamma support), then $120 (deep support + second put strike)

- ⚠️ Post-OPEX put spreads ($135/$130 or $130/$125) offer defined-risk way to play continued weakness

- 📉 Watch for break below $135 - that's the trigger for cascade to $130

- ⏰ Don't overstay - if stock stabilizes at $120-125 or reverses above $145, respect the technicals

Mark your calendar - Key dates:

- 📅 December 19 (Thursday) - Triple Witch OPEX (weekly, monthly, quarterly) - MAJOR VOLATILITY EVENT

- 📅 December 20-23 - Post-OPEX price action reveals trend direction

- 📅 January 16, 2026 - Monthly OPEX, expiration of first $140 put leg ($2.8M)

- 📅 Late January/Early February 2026 - Q4 FY2025 earnings (expected, not confirmed)

- 📅 February 20, 2026 - Monthly OPEX, expiration of second $120 put leg ($1.7M)

- 📅 Q1-Q2 2026 - DASH 2025 products (GPU Monitoring, Bits AI, LLM Experiments) ramp revenue contribution

Final verdict: DDOG's long-term observability story remains compelling - 30+ new products from DASH 2025, strategic acquisitions, growing AI-native customer base (8.5% of revenue), and competitive moat with 450+ integrations. BUT, at 18.7x EV/Sales in a confirmed downtrend with cloud optimization headwinds, margin compression, decelerating growth (26% to 19%), and approaching critical support at $135, the risk/reward is NO LONGER favorable for aggressive new long positioning. The $4.5M institutional double put hedge is a CLEAR signal: smart money is protecting against near-term downside.

Be patient. Let December OPEX resolve. Look for capitulation to $120-125 or reversal above $145. The cloud observability market will still be here in 2-3 months, and you'll sleep better buying at $125 instead of $140.

This is a downtrend until proven otherwise. Respect the trend. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual scores (8.91x and 489x) reflect these specific trades' sizes relative to recent DDOG history - they do not imply the trades will be profitable or that you should follow them. Always do your own research and consider consulting a licensed financial advisor before trading. December 19th OPEX creates binary event risk with potential for 3-5% gaps either direction. The put buyer may have complex portfolio hedging needs not applicable to retail traders. Short options carry unlimited risk and margin requirements.

About Datadog: Datadog is a cloud-based software company specializing in infrastructure monitoring, enabling clients to monitor and analyze their entire information technology infrastructure from servers to applications. The company operates as a SaaS provider with a market cap of $49.8 billion in the Prepackaged Software industry, serving 30,000+ customers including 462 at $1M+ annual recurring revenue.