DDOG Unusual Options Activity - Institutional Hedging Amid Upgrade Rally!

January 22, 2026 | Unusual Activity Detected

The Quick Take

Someone just made a $3.6 MILLION dual options play on Datadog today - closing out a short put while simultaneously opening a massive long put! This isn't your average day trader - this is sophisticated institutional positioning happening on the same day DDOG surged 7.3% following a Stifel upgrade. With earnings on February 10th and the stock rallying hard, smart money is locking in protection at the peak. Translation: Big players are taking profits AND buying downside insurance all at once!

Company Overview

Datadog (DDOG) is a cloud-native company that focuses on analyzing machine data. The platform enables clients to monitor IT infrastructure and ingest large amounts of machine-generated data in real time for various business applications:

- Market Cap: $43.29 Billion

- Industry: Services-Prepackaged Software

- Current Price: $132.55 (up 7.3% on the day)

- Primary Business: Cloud observability, infrastructure monitoring, AI observability, security monitoring

The Option Flow Breakdown

The Tape (January 22, 2026):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order Type | Strategy | Z-Score | Signal |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-22 | 09:44:20 | DDOG | BUY | PUT $100 | 2026-06-18 | $100 | 3,500 | $1,800,000 | BTO | Long Put | 171.01 | EXTREMELY UNUSUAL |

| 2026-01-22 | 09:44:20 | DDOG | SELL | PUT $120 | 2026-02-20 | $120 | 3,600 | $1,800,000 | STC | Close Short Put | 2.06 | HIGHLY UNUSUAL |

What This Actually Means

This is a sophisticated two-part trade happening at the exact same moment! Here's what went down:

Trade 1 - Closing Short Put (Profit Taking):

- Sold 3,600 contracts of the $120 February puts for $1.8M

- This CLOSES a previously short put position - they were bullish before and collected premium

- Now they're buying back (closing) that short position on the rally day - LOCKING IN PROFITS

- Z-Score of 2.06 signals highly unusual activity but not off-the-charts

Trade 2 - Opening Long Put (NEW Downside Protection):

- Bought 3,500 contracts of $100 June puts for $1.8M

- This is a BRAND NEW bearish hedge at the $100 strike (24.5% below current price!)

- Five months to expiration captures Q4 earnings (Feb 10), Q1 2026 earnings, and any macro surprises

- Z-Score of 171.01 - this is EXTREMELY UNUSUAL (happens maybe a few times per year!)

- The Vol/OI ratio of 12.9 confirms this is massive new positioning

The Combined Picture: This trader is ROLLING their exposure - closing a near-term bullish bet (short $120 puts) and simultaneously opening FAR out-of-the-money downside protection ($100 puts). They're:

- Taking profits on the winning short put position during today's 7.3% surge

- Using those profits to buy cheap, long-dated disaster insurance at $100

Why $100? That strike is 24.5% below current price - this isn't betting on a normal pullback. This is CATASTROPHE insurance protecting against a worst-case scenario through June (covers two earnings cycles).

Technical Setup / Chart Check-Up

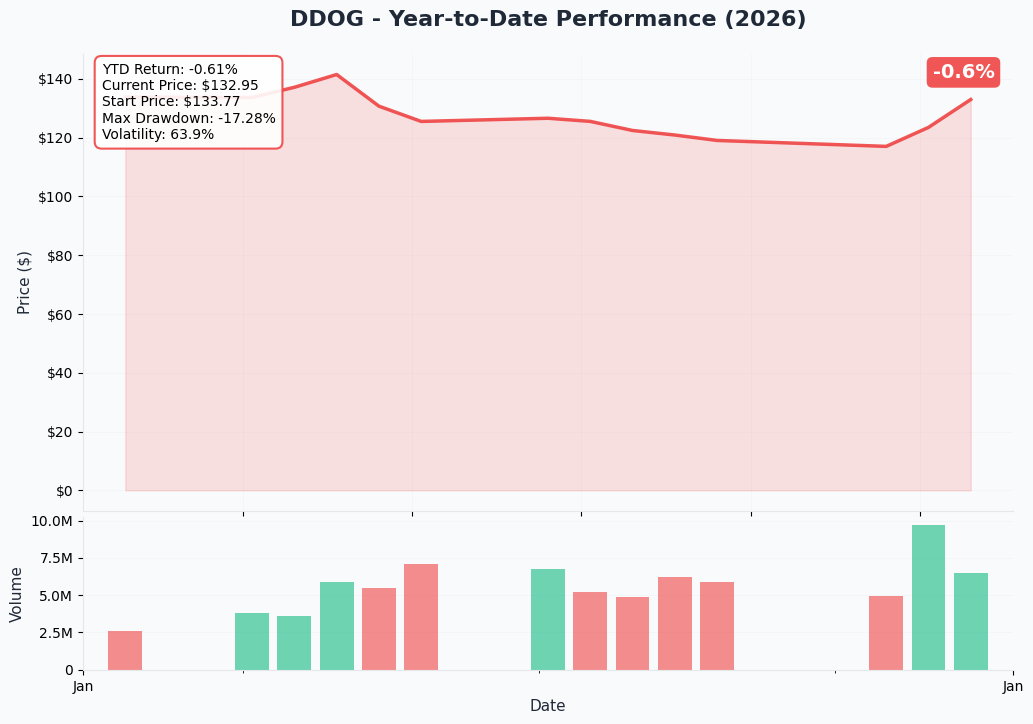

YTD Performance Chart

DDOG had a rough start to 2026 - down about 1.3% YTD at the start of today before the Stifel upgrade sparked a major rally. The stock is trading 33.9% below its November 2025 high of $199.72, showing significant multiple compression despite strong fundamentals. Today's 7.3% surge to $132+ is the first major bullish catalyst since the Q3 earnings pop in November.

Key observations:

- Current price of $132 sits in the middle of the 52-week range ($81.63 - $201.69)

- Stock bounced hard off $123 support level earlier this month

- Volume explosion today on the Stifel upgrade signals institutional interest returning

- Still well below the $160 price target from today's upgrade

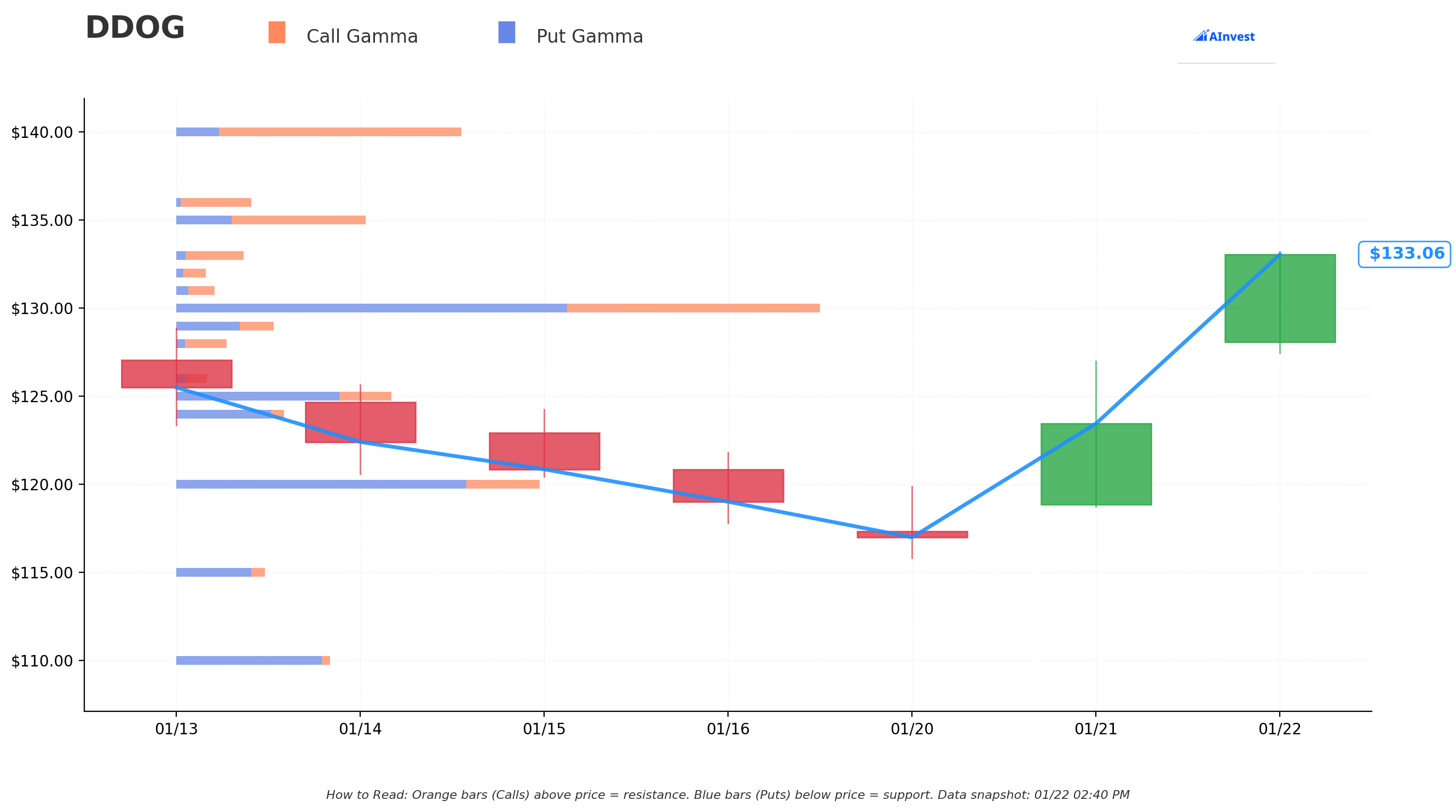

Gamma-Based Support & Resistance Analysis

Current Price: $133.10

The gamma exposure map reveals critical price magnets and barriers that will govern near-term price action:

Support Levels (Put Gamma Below Price):

- $130 - Strongest nearby support with 6.35B total gamma exposure (2.3% below)

- $129 - Secondary support at 0.94B gamma (3.1% below)

- $125 - Major structural floor with 2.39B gamma (6.1% below)

- $120 - Deep support at 3.58B gamma (this is where the closed short put was struck!)

- $110 - Extended support zone with 1.51B gamma

Resistance Levels (Call Gamma Above Price):

- $135 - Immediate ceiling with 1.84B gamma (1.4% overhead - FIRST hurdle!)

- $140 - Major resistance at 2.83B gamma (5.2% above - KEY level to watch)

- $145 - Secondary resistance at 1.71B gamma (8.9% above)

- $150 - Extended upside target at 1.24B gamma (12.7% rally required)

What this means for traders: DDOG just broke through the $130 gamma support level on today's upgrade rally and is now testing $135 resistance. The gamma data shows market makers holding significant positions at $140 which creates natural selling pressure as price approaches. If bulls can clear $135 and push toward $140, that would be a major technical breakout. The $130 level below now becomes critical support - breaking back below would signal the rally is failing.

Net GEX Bias: Bullish (20.3B call gamma vs 17.9B put gamma) - Overall positioning is slightly bullish, supporting continued upside momentum if fundamentals cooperate.

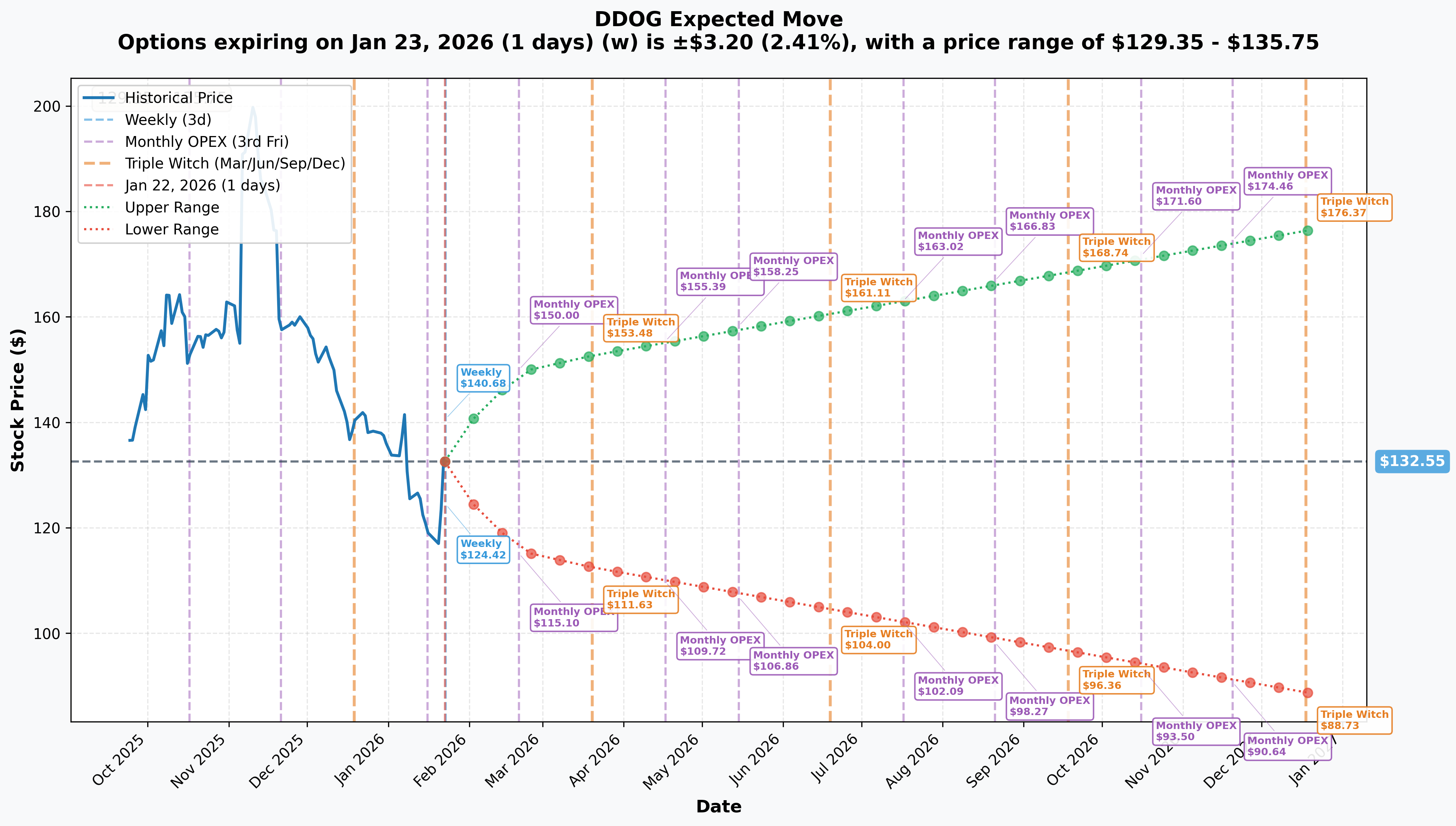

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Jan 23 - 1 day): +/-$3.20 (+/-2.41%) -> Range: $129.35 - $135.75

- Monthly OPEX (Feb 20 - 29 days): +/-$17.00 (+/-12.83%) -> Range: $115.55 - $149.55

- Quarterly Triple Witch (Mar 20 - 57 days): +/-$20.14 (+/-15.2%) -> Range: $112.41 - $152.70

- Yearly LEAPS (Dec 18 - 330 days): +/-$43.82 (+/-33.06%) -> Range: $88.73 - $176.37

Translation for regular folks: Options traders are pricing in a 12.8% move ($17) through February OPEX which includes Q4 earnings on February 10th. The market expects meaningful fireworks around earnings - that's a sizable implied move for a $43B company!

The June 18th expiration (when the $1.8M long put expires) would have roughly an 18-20% implied move, meaning the lower bound of the expected range would be around $106-108. The put buyer struck at $100 - BELOW that range - suggesting they're protecting against a tail risk scenario that the options market isn't fully pricing in.

Key insight: The dramatic increase in implied volatility from 2.4% (weekly) to 12.8% (monthly) reflects massive earnings uncertainty. Smart money is paying up for protection into this binary event.

Catalysts

Upcoming Catalysts

Q4 2025 Earnings - February 10, 2026 (19 DAYS AWAY!)

According to Datadog's investor relations, DDOG reports fiscal Q4 results on February 10, 2026 before market open. This is THE catalyst that could make or break the recent momentum:

- Revenue: $912-$916 million (company guidance) - 24% YoY growth

- Non-GAAP EPS: $0.54-$0.56 (company guidance)

- Key Metrics to Watch:

- AI-native customer revenue (currently 12% of total - has it grown?)

- Security ARR growth rate (currently 55% YoY)

- Customer count >$100K ARR (currently 4,060)

- Net revenue retention (currently 120%)

What Stifel Expects: According to Schaeffer's Research, channel checks indicate DDOG will post "another larger than typical" quarterly beat in Q4, driven by accelerating core growth. Firm expects 2026 revenue guidance of $4.1B implying "conservative" 19% core growth.

FY2026 Guidance (February 10, 2026)

The 2026 full-year outlook will be critical:

- Expected revenue guidance: ~$4.1 billion (19% YoY growth) per Stifel's analysis

- Any guidance below 18% growth could disappoint

- AI observability commentary will drive sentiment

Recent Catalysts (Already Happened)

Stifel Upgrade - January 22, 2026 (TODAY!)

Per Seeking Alpha, Stifel upgraded DDOG from "Hold" to "Buy" with a $160 price target (down from $205). The upgrade cited:

- "Attractive" risk-reward after 34% pullback from highs

- Channel checks showing strength

- Expectation for larger-than-typical Q4 beat

Q3 2025 Earnings Beat (November 2025)

Per Datadog's Q3 earnings release:

- Revenue: $885.7M (up 28.4% YoY, beat by 4.22%)

- Non-GAAP EPS: $0.55 (beat by 22.22%)

- Stock surged 21% post-earnings

Recent Acquisitions:

- Metaplane (April 2025) - Data observability startup

- Eppo (May 2025) - Feature-flagging platform for estimated $220M

DASH 2025 Product Launches (June 2025):

Per Datadog's DASH 2025 recap:

- AI Agent Monitoring - Generally available

- LLM Observability SDK - Auto-tracks AI operations

- Bits AI SRE - Autonomous on-call engineer

- GPU Monitoring - Track utilization and cost

Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through June 18th expiration:

Bull Case (30% probability)

Target: $150-$175

How we get there:

- Q4 earnings CRUSH expectations with revenue toward $920M+ and strong 2026 guidance

- AI observability revenue continues doubling trajectory (12% to 15%+ of total)

- Security ARR growth maintains 55%+ pace

- Analysts raise price targets following beat, multiple compression reverses

- Stock breaks through $140 gamma resistance and runs toward $160 (Stifel target)

- Implied move upper range ($149.55) reached by February OPEX

Why 30% probability: Strong Q3 momentum, Stifel upgrade signals improving sentiment, and 34% discount from highs provides multiple expansion room. But valuation (68.7x forward P/E) and competitive concerns limit upside.

Base Case (45% probability)

Target: $120-$140 range (CONSOLIDATION)

Most likely scenario:

- Solid earnings meeting consensus ($912-916M revenue)

- 2026 guidance of $4.0-4.1B (19-20% growth) - in-line with expectations

- AI products growing but not explosive enough to expand multiple

- Competition concerns from Grafana and Chronosphere remain per Goldman's caution

- Stock trades in tight range between $125 gamma support and $140 resistance

- Volatility crush post-earnings as uncertainty resolves

This is likely the put seller's scenario: Short put at $120 closed profitably, and they're comfortable with stock consolidating in this range. The new $100 puts are just disaster insurance - they don't expect to need them.

Bear Case (25% probability)

Target: $100-$120 (TESTING THE PUT STRIKE!)

What could go wrong:

- Earnings miss or weak 2026 guidance disappoints at premium valuation

- Goldman's competitive pressure warnings materialize - budget optimization hurts growth

- OpenAI customer concentration risk - largest customer builds in-house

- Broader tech selloff drags cloud software lower

- Break below $120 support triggers cascade toward $110, then $100

- Macro recession concerns pressure IT spending

Why 25% probability: Fundamentals remain solid (120% NRR, 55% Security growth, AI tailwinds), but 68.7x forward P/E valuation leaves zero room for error. The institutional put buyer clearly thinks this scenario has meaningful odds.

Put P&L in Bear Case:

- Stock at $100 on June 18: Puts worth ~$0.01 intrinsic, significant time value loss

- Stock at $90 on June 18: Puts worth ~$10.00, massive profit

- Stock at $120 on June 18: Puts expire worthless, $1.8M loss (insurance cost)

Trading Ideas

Conservative: Wait for Post-Earnings Clarity

Play: Stay on sidelines until after February 10th earnings

Why this works:

- Earnings in 19 days creates binary event risk with 12.8% implied move

- Stock just surged 7.3% today - buying the rally is chasing

- Implied volatility elevated pre-earnings - options expensive

- Better entry likely post-earnings after IV crush

- The institutional activity today shows smart money is hedging, not going all-in

Action plan:

- Watch February 10th earnings for revenue ($915M+ target), 2026 guidance quality, and AI metrics

- Look for pullback to $125-130 gamma support post-earnings for stock entry

- If earnings beat AND stock breaks $140, consider calls on confirmed breakout

- Monitor unusual options activity - if institutions add more puts, stay defensive

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Balanced: Post-Earnings Put Spread

Play: After earnings, sell put spread for income if bullish

Structure: Sell $125 puts, Buy $115 puts (March 20 expiration)

Why this works:

- IV crush after earnings makes put spreads attractive

- $125 strike sits at strong gamma support

- Defined risk spread ($10 wide = $1,000 max risk per spread)

- Collect premium if stock stays above $125 through March

Estimated P&L (adjust after seeing post-earnings IV):

- Collect ~$2.50-3.50 credit per spread post-earnings

- Max profit: $250-350 if DDOG above $125 at March expiration

- Max loss: $650-750 if DDOG below $115

- Breakeven: ~$121-122

Entry timing:

- Wait until February 11-12 for full IV collapse

- Only enter if stock above $130 (gives cushion to $125 strike)

Risk level: Moderate (defined risk, bullish directional) | Skill level: Intermediate

Aggressive: Copy the Institutional Hedge

Play: Buy far OTM puts as disaster insurance (ADVANCED ONLY!)

Structure: Buy $100 June puts (same as institutional trade)

Why this could work:

- If smart money is buying $100 puts, maybe they know something

- Five months of coverage through two earnings cycles

- Cheap insurance (likely $5-8 per contract) for tail risk protection

- Protects against macro shock, competitive surprise, or major miss

Why this is risky:

- Need 24.5% crash for puts to have any intrinsic value

- Time decay will eat premium over five months

- Fundamentals remain solid - this is pure insurance, not a directional bet

- Could easily lose 100% of premium if stock stays above $100

Position sizing:

- Only risk 1-2% of portfolio maximum

- This is INSURANCE, not a core position

- Expect to lose the premium 80% of the time

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced only

Risk Factors

Don't get caught by these potential landmines:

-

Earnings binary event in 19 days: Results February 10th create massive volatility risk. Options pricing 12.8% implied move. Any guidance disappointment at 68.7x P/E could trigger sharp selloff. Historical precedent shows cloud software stocks can gap 15-20% on guidance changes.

-

Valuation remains stretched: Trading at 68.7x forward P/E vs industry 28.9x. Premium valuation requires flawless execution. 1.07% ROIC vs 9.34% WACC indicates value destruction at current capital allocation rates.

-

Competitive pressures intensifying: Goldman Sachs warns 2026 is pressure year with customers focused on budget optimization. Grafana, Chronosphere (Palo Alto), and cloud-native tools from AWS/Azure/GCP gaining traction. Dynatrace and Splunk investing heavily in AI capabilities.

-

Customer concentration risk: OpenAI may build in-house observability, potentially creating $150M revenue gap in 2026. Largest customers have resources to build internal solutions.

-

Growth deceleration: 2025 full-year guidance implies 18-19% growth, down from historical 25%+ rates. Growth investors may rotate to higher-growth alternatives.

-

Smart money buying protection: The $1.8M institutional put purchase on an UP day signals sophisticated players are worried about downside despite bullish fundamentals. When funds buy disaster insurance while closing profitable positions, it's a caution flag.

-

Macro sensitivity: Usage-based revenue model vulnerable to IT spending slowdowns. Deferred cloud migrations reduce metrics/logs volume and customer spending.

The Bottom Line

Real talk: Someone just executed a sophisticated $3.6M options play on DDOG - closing out a winning short put position while simultaneously opening massive downside protection through June. This happened on the SAME DAY the stock surged 7.3% on an upgrade. That's not bearish conviction - that's prudent risk management at elevated prices.

What these trades tell us:

- Sophisticated player locked in profits on their bullish short put ($120 strike) during today's rally

- They immediately deployed those profits into far OTM disaster insurance ($100 puts through June)

- The timing shows they see Q4 earnings as binary risk - protecting against tail scenarios

- Z-score of 171 on the new put purchase is EXTREMELY unusual - this isn't normal hedging

This is NOT a "sell everything" signal - it's a "take profits and stay protected" signal.

If you're bullish on DDOG:

- Wait for post-earnings confirmation before adding

- $140 is key resistance - need to break that for sustained rally

- Stifel's $160 target implies 20%+ upside from here if execution delivers

- Consider selling cash-secured puts post-earnings for income with lower IV

If you're watching from sidelines:

- February 10th is the moment of truth - DO NOT chase today's rally!

- Post-earnings pullback to $125-130 would be attractive entry

- Need confirmation of: 2026 guidance >19% growth, AI metrics accelerating, competitive positioning stable

If you're bearish:

- Institutional activity validates concerns about downside risk

- Wait for earnings before shorting - fighting momentum is painful

- Post-earnings put spreads offer defined-risk way to play weakness

Mark your calendar - Key dates:

- February 10, 2026 - Q4 FY2025 earnings (19 days!)

- February 20, 2026 - Monthly OPEX (short put expiration)

- March 20, 2026 - Quarterly triple witch

- June 18, 2026 - Long put expiration date

Final verdict: DDOG's fundamentals remain strong - 120% net revenue retention, 55% Security ARR growth, AI observability leadership, and platform consolidation are real tailwinds. But at 68.7x forward P/E after a 7% rally day with competitive concerns mounting, the institutional move to hedge makes sense. The smart money isn't running for the exits - they're just making sure they have an exit if they need one.

Be patient. Let earnings clear. If you love DDOG long-term, a better entry will come.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-scores reflect this specific trade's unusualness relative to recent DDOG history - it does not imply the trade will be profitable. Always do your own research and consider consulting a licensed financial advisor before trading.

About Datadog: Datadog is a cloud-native company that focuses on analyzing machine data. The platform enables clients to monitor IT infrastructure and ingest large amounts of machine-generated data in real time for various business applications, with a market cap of $43.29 billion in the Services-Prepackaged Software industry.