🔋 EOSE: $21.2M Bullish Bet on Energy Storage Boom!

📅 December 22, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just loaded up $21.2 MILLION in long-dated EOSE call options across two monster trades - targeting both 2027 and 2028 expirations. This is pure institutional money betting big that Eos Energy's zinc-battery technology will capitalize on the AI data center power surge. With the stock trading around $13, these strikes at $12.50 and $20 show conviction that EOSE could nearly double over the next 2-3 years.

💰 The Option Flow Breakdown

📊 What Just Happened

Here's the institutional money trail that caught our attention:

Trade #1 - The 2027 Play (10:11:37 AM):

- 🔵 9,000 contracts EOSE Jan 2027 $12.50 calls → $5.4M premium

- 🔵 9,000 contracts EOSE Jan 2028 $20 calls → $5.3M premium

- Stock trading at: $13.02

- Total flow: $10.7M bullish

Trade #2 - Doubling Down (11:14:34 AM):

- 🔵 8,992 contracts EOSE Jan 2027 $12.50 calls → $5.3M premium

- 🔵 8,992 contracts EOSE Jan 2028 $20 calls → $5.2M premium

- Stock trading at: $13.10

- Total flow: $10.5M bullish

Combined Position:

- Total premium deployed: $21.2M

- Jan 2027 $12.50 calls: 18,000 contracts

- Jan 2028 $20 calls: 18,000 contracts

👉 View detailed option charts:

🤓 What This Actually Means

Real talk: This isn't some YOLO trader throwing darts. Someone with deep pockets just made a structured, multi-year bet on EOSE with $21.2M. Here's what makes this fascinating:

✅ The Smart Structure: They split the bet between two timeframes - the 2027 $12.50 calls are barely out-of-the-money (stock at $13), basically saying "I want to own this stock long-term but with leverage." The 2028 $20 calls are the home run swing - a 54% gain target over 3 years.

✅ Why This Isn't Hedging: These are all BUY orders opening new positions (BTO). This is directional conviction, not some complex hedge. The confidence level is classified as "LOW" in the data because there's no prior open interest history - this IS the new position being built.

✅ The Timing: Coming right after EOSE closed a $1.04 billion financing package in late November and announced a strategic partnership with Talen Energy for AI data center power. The money is betting the company finally has the runway to execute.

✅ Volume vs Open Interest: The Jan 2027 $12.50 calls now have 20,000 volume on just 81,000 open interest - that's a 25% daily volume ratio, highly unusual. The Jan 2028 $20 calls have 20,000 volume on just 20,000 OI - meaning this single buyer IS the entire open interest. That's institutional-level commitment.

Translation for us regular folks: Someone who can afford to tie up $21M for 2-3 years thinks EOSE's zinc-battery tech is about to win big in the energy storage wars. They're not trying to flip this next week - they're building a position for the long haul.

📈 Technical Setup

📊 YTD Performance Check

EOSE has been on an absolute tear in late 2025, surging from a 52-week low of $2.99 to a high of $19.86 - that's a 564% move. Currently trading around $12.95, the stock has pulled back from the November highs but is still up +208% over 3 months according to TradingView data.

Key Technical Levels:

- 52-week high: $19.86 (hit in November 2025)

- Current price: $12.95

- 52-week low: $2.99

- Recent support: $11.50-$12.00 zone held multiple times

The chart shows a healthy consolidation after the explosive November rally driven by the Talen Energy partnership announcement (stock jumped 14% that day per Bloomberg). Now we're seeing smart money accumulate in this $12-13 range through options rather than pushing the stock higher immediately.

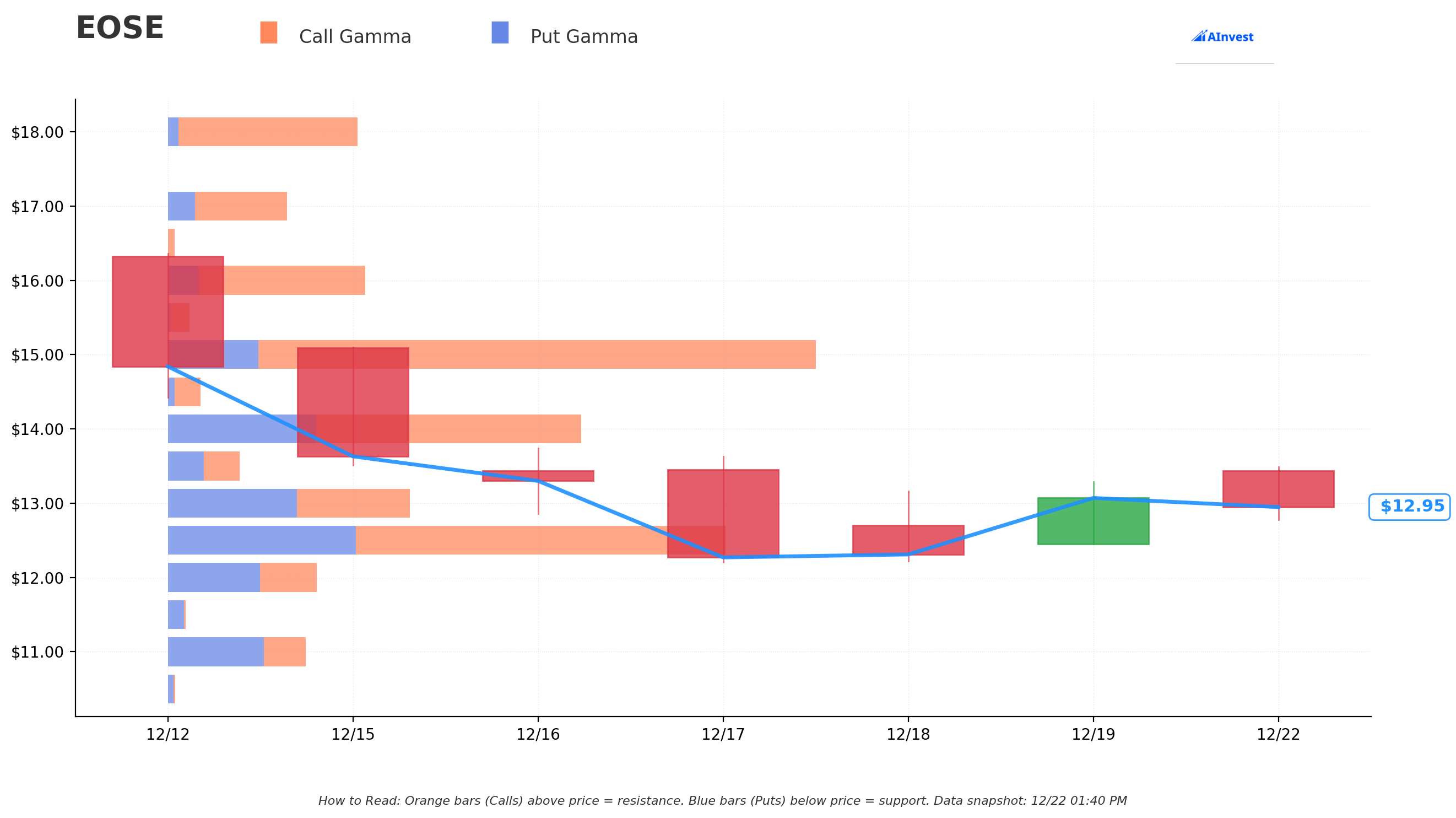

🎯 Gamma-Based Support & Resistance Analysis

Current Market Dynamics:

- Stock Price: $12.95

- Net GEX Bias: Bullish (Total Call GEX: $54.03M vs Total Put GEX: $18.84M)

Key Support Levels (Blue - Put Gamma):

- 💎 $12.50 (Strongest Support): $8.61M total GEX, $2.85M net bullish - This is exactly where the big money bought their 2027 calls. It's 3.5% below current price and should act as a magnet.

- 🛡️ $12.00: $2.29M total GEX - Secondary support 7.3% down

- 🛡️ $11.00: $2.11M total GEX - Major floor 15% below

Key Resistance Levels (Orange - Call Gamma):

- 🚀 $13.00 (Nearest Resistance): $3.76M total GEX - Just 0.4% above current price

- 🚀 $14.00: $6.40M total GEX, $1.84M net bullish - 8% upside target

- 🚀 $15.00 (Major Resistance): $10.09M total GEX, $7.30M net bullish - This is the ceiling at 16% upside

- 🎯 $20.00: Where the big 2028 calls are positioned

What This Means: The gamma profile shows heavy call positioning (bullish bias), but the stock is pinned between $12.50 support and $13.00 resistance in the near term. Market makers will likely keep price range-bound until a catalyst breaks it free. The $15 level is where things get interesting - massive call gamma there could accelerate any breakout.

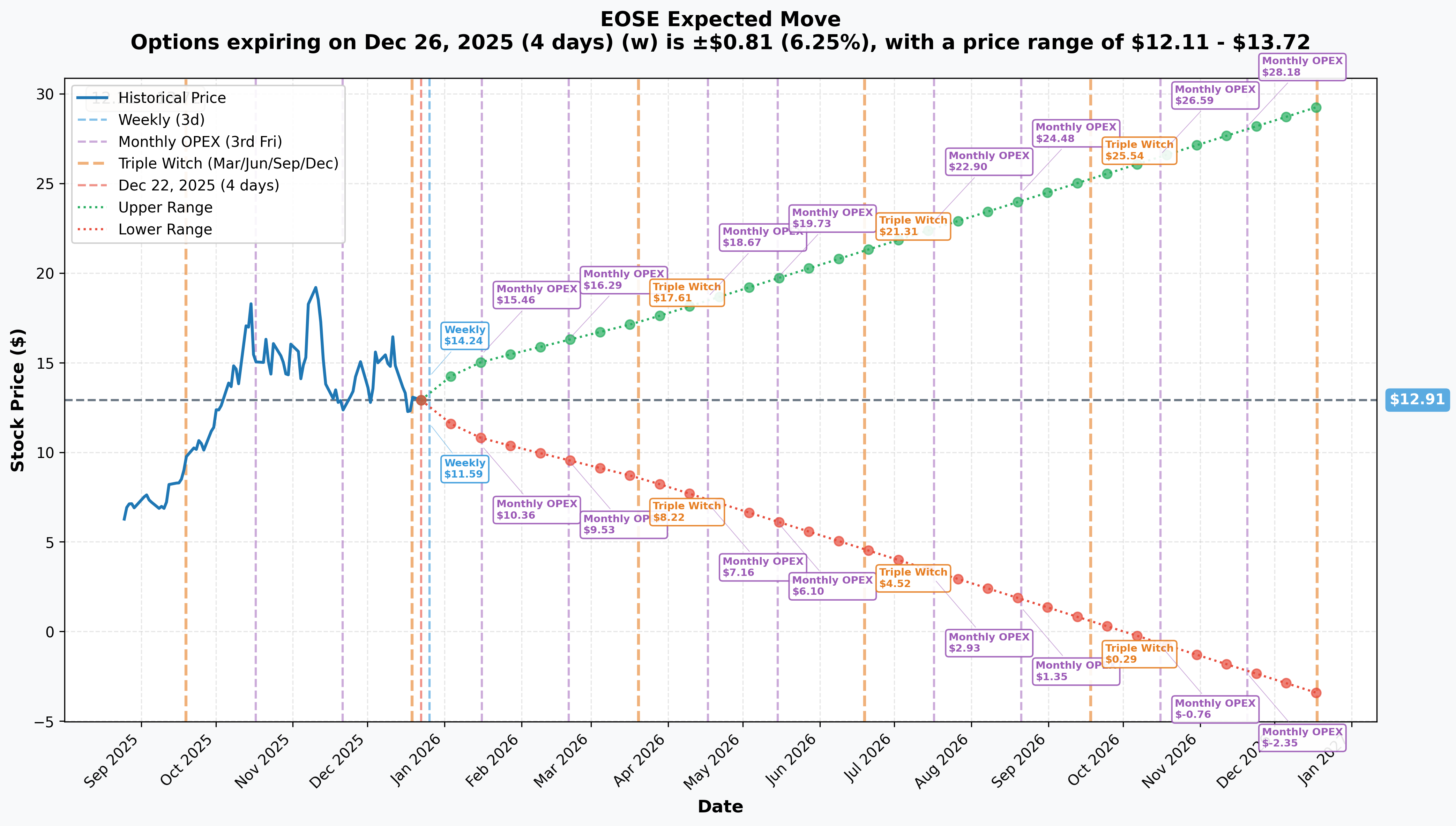

📊 Implied Move Analysis

Expected Price Ranges:

Weekly (Dec 26, 2025 expiration):

- Implied Move: ±6.25% ($0.81)

- Range: $12.11 - $13.72

- Translation: Market expects EOSE to stay relatively calm this week, likely range-bound between $12-14.

Monthly OPEX (Jan 16, 2026):

- Implied Move: ±16.82% ($2.17)

- Range: $10.74 - $15.08

- Translation: Next month's expiration expects potential 17% swings - positioning for Q4 earnings volatility.

Quarterly (March 20, 2026):

- Implied Move: ±33.64% ($4.34)

- Range: $8.57 - $17.26

- Translation: First quarter of 2026 could see massive volatility as the company ramps production and reports Q4 results.

LEAPS (Dec 2026):

- Implied Move: ±126.71% ($16.36)

- Range: $29.28 downside protection, upside unlimited

- Translation: Over the next year, options market is pricing in the potential for EOSE to nearly triple OR cut in half - this is the "execute or die" timeframe.

Key Insight: The short-term implied moves are modest (6-17%), but as you extend the timeline, volatility expectations explode. This validates the institutional play we saw - they're not betting on next week's movement, they're betting on 2-3 year execution. The 126% annual implied move aligns perfectly with the $20 strike target on the 2028 calls.

🎪 Catalysts

📅 Upcoming Events (What Could Light the Fuse)

Q4 2025 Earnings - February 20, 2026 Before Market Open 🔥

- Expected Revenue: $104M-$114M for Q4 (company guided $150M-$160M full-year per Q3 earnings release)

- Consensus Estimate: $91.61M next quarter per TipRanks

- Key Metric: Company expects positive contribution margin for the first time in Q4 2025

- Why It Matters: If EOSE hits guidance, Q4 revenue would be 5x the current quarterly run rate - proving the production ramp is real. Missing again (like Q2 and Q3) would be catastrophic for the stock.

World Economic Forum 2026 - January 21-24, 2026

- Eos will present at Davos showcasing zinc-battery technology

- Opportunity to engage global energy leaders and potential customers

- Focus on AI/data center energy resilience amid rising power demands

- Why It Matters: Visibility with decision-makers who control multi-billion dollar infrastructure budgets. Think of it as a trade show for people who buy GWh-scale battery systems.

New Factory Launch - Mid-2026 🏭

- $75M Pittsburgh factory adding 2 GWh annual capacity (doubling current output)

- Creating 735 new jobs, backed by $24M Pennsylvania economic package per Governor Shapiro's announcement

- Why It Matters: Production capacity is the bottleneck. Doubling output is how they convert the $22.6B pipeline into actual revenue.

IRA Tax Credits - Throughout 2026 💰

- Eligible for $35/kWh battery cell credits, $10/kWh module credits under 45X manufacturing credits

- Potential 10% domestic content bonus; EOSE targeting 100% U.S. sourcing by 2026 per Solar Power World analysis

- Why It Matters: These credits dramatically improve unit economics. Every GWh produced generates millions in tax credits, directly improving margins.

Talen Energy Projects - Q1-Q2 2026

- Multiple gigawatt-hours of energy storage projects across Pennsylvania per partnership announcement

- Focused on powering AI and cloud computing data centers

- Projects at operating and retired fossil fuel plant sites

- Why It Matters: Talen owns the land and power infrastructure - this is a built-in customer with urgent needs and deep pockets. First revenue from this partnership validates the model for future data center deals.

📜 Past Events (What Got Us Here)

$1.04 Billion Financing - Closed November 24, 2025 ✅

- $600M convertible notes at 1.75% due 2031

- $458.2M registered direct offering (35.9M shares at $12.78/share)

- Net proceeds: ~$474M added to balance sheet

- Impact: Removed near-term bankruptcy risk, funded factory expansion, retired expensive 2030 notes

Q3 2025 Earnings - November 6, 2025 ✅

- Revenue: $30.5M (100% QoQ growth, 35x YoY) per earnings release

- Commercial pipeline: $22.6B (+21% QoQ, +59% YoY) representing 91 GWh

- Backlog: $644.4M in firm orders

- Impact: Proved revenue inflection is happening, though still missed analyst estimates. Stock rose 6.19% in premarket as investors focused on trajectory over absolute numbers per Investing.com coverage.

Talen Energy Partnership - October 21, 2025 ✅

- Strategic collaboration for multi-GWh energy storage in Pennsylvania

- Stock jumped 14% on announcement

- Impact: Validated the AI data center thesis - real customer with urgent power needs willing to bet on EOSE's technology

DOE Loan Program - July 2025 ✅

- Second $22.7M advance from DOE Loan Programs Office

- Total facility: Up to $305.3M ($277.5M principal + capitalized interest) per DOE announcement

- Impact: Government backing provides credibility and non-dilutive capital for expansion

DawnOS Platform Launch - September 2025 ✅

- 100% U.S.-developed battery management system

- No reliance on foreign technology or cloud services

- Impact: Addresses national security concerns for critical infrastructure projects, competitive advantage in government/defense contracts

🎲 Price Targets & Probabilities

Bull Case: $18-20 (38-54% upside) - 30% Probability ✅

Path to Success:

- Q4 earnings deliver $104M+ revenue with positive contribution margin

- New factory comes online mid-2026 on schedule

- Talen partnership generates first meaningful revenue in Q1-Q2 2026

- Convert $22.6B pipeline into $1B+ of new firm orders

- IRA tax credits improve gross margins to positive by Q1 2026 as guided

Key Levels:

- $15.00 - Major gamma resistance, first psychological barrier (16% upside)

- $17.26 - March 2026 quarterly implied move upper range

- $19.86 - 52-week high, prior peak to reclaim

- $20.00 - 2028 call strike target (54% upside)

Why This Works: The institutional $21.2M bet we're analyzing is betting on THIS scenario. If EOSE executes on production ramp and converts even 10% of the $22.6B pipeline into orders over the next 18 months, revenue could hit $500M-$1B run rate by late 2026. At a 5-10x sales multiple (typical for high-growth cleantech), that justifies $15-25/share. The gamma profile shows heavy call positioning at $15, suggesting smart money is already positioned for this outcome.

Catalysts: February Q4 earnings beat, mid-2026 factory opening, Talen revenue announcement

Base Case: $11-14 (±8% range) - 50% Probability 📊

Most Likely Scenario:

- Q4 revenue comes in at low end of guidance ($104M) or slight miss

- Stock stays range-bound between gamma support at $12.50 and resistance at $15

- Factory expansion progresses but with minor delays (typical for manufacturing projects)

- Pipeline grows but conversion to firm orders slower than bulls hope

- Market remains skeptical until sustained profitability proves itself

Key Levels:

- $12.50 - Strongest gamma support (institutional call strike)

- $12.95 - Current price, equilibrium

- $14.00 - Moderate gamma resistance (8% upside)

- $15.00 - Upper bound of base case range

Why This Is Likely: EOSE has a history of missing revenue targets (Q2 and Q3 2025 both missed per Investing.com earnings coverage). The stock's implied volatility suggests the market is pricing in continued choppiness. Institutional buyers are patient (2027-2028 expirations) because they expect this to be a grinding, multi-quarter story rather than a moonshot. The $12.50 gamma support should hold on any dips, while $15 acts as a ceiling until a major catalyst breaks it.

What We're Watching: Production output metrics, backlog conversion rate, insider buying/selling patterns

Bear Case: $8-10 (22-35% downside) - 20% Probability ⚠️

Nightmare Scenario:

- Q4 revenue significantly misses (sub-$90M), company lowers 2026 guidance

- Factory delays push 2 GWh capacity target into late 2026 or 2027

- Talen partnership stalls or cancels projects

- Pipeline shrinks as customers choose Tesla/Fluence over unproven zinc-battery tech

- Additional dilution required to fund ongoing losses

Key Levels:

- $10.74 - January monthly OPEX lower implied range

- $10.00 - Psychological support

- $8.57 - March quarterly lower implied range

- $8.00 - B. Riley Securities prior price target (before upgrade to $12)

What Could Trigger This: According to JPMorgan's recent coverage initiation, analyst Mark Strouse warned: "Given combination of past execution missteps, ambitious guidance and uncertainties regarding DoE loan facility, risk/reward appears increasingly unfavorable at current share price levels." A Q4 earnings miss combined with 2026 guidance below $300M would validate these concerns and likely send the stock below $10.

Red Flags:

- Heavy insider selling (18 sales, 0 buys in past 6 months) per Simply Wall St data

- CEO Joe Mastrangelo sold $1.6M worth, Russell Stidolph sold $11.5M

- Persistent losses despite revenue growth ($641M net loss in Q3 2025)

- Customer preference for proven lithium-ion tech from Tesla/Fluence per Utility Dive article

💡 Trading Ideas

🛡️ Conservative: The "Show Me First" Strategy

For: Investors who want exposure but need proof of execution before committing

The Play:

- Wait for Q4 earnings on Feb 20, 2026 - Let the company prove it can hit guidance

- Entry trigger: Stock holds $12.50 support AND reports $100M+ Q4 revenue with positive contribution margin

- Position: Buy 100-200 shares at $12.50-$13.00 (Total: $1,250-$2,600)

- Stop loss: $11.00 (15% max loss, aligned with gamma support level)

- Target: $16-18 by mid-2026 (28-44% gain)

Why This Works: You're letting the institutional buyer's $21.2M bet act as a "canary in the coal mine" while protecting your downside. If EOSE executes on Q4, the stock should break $15 resistance and head toward the bull case targets. If they miss, you avoided catching a falling knife. The gamma support at $12.50 gives you a clear entry level with defined risk.

Cost to Wait: You might miss 10-15% upside if stock breaks out before earnings, but you avoid 20-35% downside if they miss. Sleep well strategy.

⚖️ Balanced: The "Leveraged Patience" Play

For: Traders who believe the thesis but want leveraged exposure with time to be right

The Play:

- Option: Buy EOSE Jan 2026 $15 calls (1 month after Q4 earnings)

- Rationale: Give yourself time to see Q4 results + initial factory progress

- Position size: 3-5 contracts (roughly $900-$1,500 based on current pricing)

- Max loss: Premium paid ($900-$1,500)

- Breakeven: $16.80-$18.00 (strike + premium)

- Target: $20+ by Jan 2026 for 100-200% return

Why This Works: You're essentially making the same bet as the institution, just with a shorter timeframe and defined risk. January 2026 expiration gives you 1 month post-Q4 earnings to see if management delivers. If they hit the $104M+ revenue target and guide aggressively for 2026, stock should easily surpass $15 resistance. You're risking $1,500 max to potentially make $3,000-$5,000.

Risk Management:

- If stock breaks $11 support before earnings, consider taking the loss early

- If earnings disappoint but stock holds $12.50, you could roll to March 2026 calls to give thesis more time

- Don't chase - if stock runs to $18+ before earnings, the risk/reward flips bearish

Probability of Success: ~40-45% based on historical earnings delivery and current setup

🚀 Aggressive: The "Institutional Copycat" Trade

For: Traders with 2-3 year time horizon and conviction in the AI data center power thesis

The Play:

- Mirror the whale: Buy EOSE Jan 2027 $12.50 calls (same strike and expiration as the $10.7M institutional buy)

- Position: 5-10 contracts (roughly $2,925-$5,850 based on $5.85-$6.00/contract pricing from the flow)

- Max loss: Premium paid

- Breakeven: $18.35-$18.50 (strike + premium)

- Target 1: $25 by Jan 2027 for 108% gain

- Target 2: $35+ by Jan 2027 for 270%+ gain (home run scenario)

Why This Is Aggressive But Smart: You're directly copying a trade from someone who can afford to lose $10M+ and has access to better research than retail traders. The 2027 expiration gives EOSE 25 months to:

- Ramp factory to 2 GWh, expand toward 8 GWh target

- Convert $22.6B pipeline into $2-3B of firm orders

- Achieve sustained gross margin profitability

- Sign 5-10 more Talen-sized partnerships

- Benefit from full IRA tax credit implementation

If the cleantech energy storage thesis plays out and EOSE captures even 5% market share of the 400 GWh/year LDES market (growing 60% annually per SolarQuarter data), the company could be doing $1-2B revenue with positive margins by 2027. At a 10x sales multiple, that's a $10-20B market cap vs today's $4.15B.

What Could Go Wrong:

- Production delays keep capacity below targets

- Lithium-ion tech improves faster than expected, making zinc-battery value proposition obsolete

- Customer preference continues favoring Tesla/Fluence despite EOSE advantages

- Additional dilution crushes per-share value

- Macro headwinds (recession, interest rates) kill infrastructure spending

Position Sizing: Only allocate 3-5% of portfolio to this trade. If it works, it could return 2-3x over 2 years. If it fails, you lose the premium but it doesn't destroy your portfolio. This is NOT a "bet the farm" trade despite the institutional size - they're diversified across hundreds of positions.

Exit Strategy:

- Take 50% profit if stock hits $20 before mid-2026 (derisks position)

- Let remaining 50% ride for the $25-35 target into 2027

- Cut the entire position if stock breaks below $10 and stays there for 2+ weeks (thesis broken)

⚠️ Risk Factors

Execution Risk (HIGHEST RISK) 🚨

The Reality Check: EOSE needs to deliver $104M-$114M in Q4 2025 revenue - that's 5x their current quarterly run rate. According to DCFmodeling.com analysis, the company must achieve this without further cash burn despite just raising $474M.

What Could Go Wrong:

- Q3 2025 revenue of $30.5M missed analyst expectations ($39.62M consensus) per Investing.com

- Q2 2025 revenue of $15.2M missed by 37.2% ($24.2M estimate) per Investing.com earnings transcript

- History of production delays: Q3 2024 revenue severely impacted by supply chain issues for Z3 inline enclosures per Q3 2024 release

JPMorgan's Warning: Analyst Mark Strouse noted per Simply Wall St coverage: "Given combination of past execution missteps, ambitious guidance and uncertainties regarding DoE loan facility, risk/reward appears increasingly unfavorable at current share price levels."

This is why the institutional buyer used 2027-2028 expirations - they're giving management 2-3 years to prove it. Shorter-dated plays are gambling on perfect execution.

Valuation Risk 💸

The Numbers:

- Current market cap: $4.15B per Public.com data

- Expected 2025 revenue: $150M-$160M

- Implied valuation multiple: 26-28x sales

Translation: You're paying $26-28 for every $1 of revenue. Compare this to:

- Tesla Energy: ~15x sales (profitable, proven at scale)

- Fluence: ~8x sales (profitable, $4.9B backlog)

At 26-28x sales, the market is pricing in perfect execution on the production ramp, pipeline conversion, and margin improvement. Any disappointment gets punished ruthlessly. The stock went from $19.86 to $12.95 (35% drop) in just a few weeks when investors questioned the Q4 revenue ramp.

Insider Selling Red Flag 🚩

The Uncomfortable Truth: According to Simply Wall St insider data:

- 18 insider sales in past 6 months, ZERO purchases

- CEO Joe Mastrangelo sold 293,819 shares for $1.6M

- Russell Stidolph sold 766,134 shares for $11.5M

- Multiple directors selling in December 2025 at $15-16/share per Investing.com

- Insider ownership: Only 1.99% per MarketBeat

What This Means: While insider selling doesn't always signal trouble (they have bills to pay, diversification needs, tax planning), the complete absence of insider buying is concerning. If your CEO and board members thought the stock was cheap at $12-16, why aren't they buying alongside the institution that just deployed $21.2M? They have better information than anyone.

Devil's Advocate: The $1B financing created liquidity event opportunities for early shareholders. Some selling is natural after a 208% run in 3 months. But the 18-to-0 ratio is worth noting.

Technology Adoption Risk 🔬

The Zinc vs Lithium Battle: EOSE's zinc-bromine chemistry is competing against dominant lithium-ion technology that has massive scale advantages. According to Utility Dive research: "Storage providers face bankability challenge as customers prefer Tesla, other tier 1 battery suppliers."

The Challenge:

- Tesla Megapack: 50+ GWh installed globally, proven reliability per Nasdaq analysis

- Fluence: $4.9B backlog, AI-driven optimization software per InfoLink Consulting ranking

- Chinese manufacturers (Sungrow, BYD, CRRC) dominate global shipments with cost advantages

EOSE's Edge:

- Zinc is non-flammable, no cooling required, safer for urban/data center deployment

- 100% U.S.-sourced (qualifies for IRA credits, no China risk)

- 6,000 cycles vs 3,000-4,000 for lithium at equivalent depth of discharge per DOE description

- Long-duration (8-24 hours) vs lithium's 2-4 hour sweet spot

The Bet: The institutional buyer believes data centers will prioritize safety, duration, and domestic sourcing over proven track record. That's a bold bet, but the Talen partnership suggests it might be working.

Dilution Risk 📉

The Capital Intensity Problem: Even after raising $1.04B, EOSE is still losing money (Q3 net loss: $641M, mostly non-cash but still). According to ainvest analysis, scaling to 8 GWh capacity and converting the $22.6B pipeline will likely require additional capital raises.

Share Count Expansion:

- November 2025 offering: 35.9M shares at $12.78

- Outstanding shares now: 324.1M per Public.com data

- Convertible notes: Could add more shares if stock rallies above conversion price

Impact on Options: If the company issues another 30-50M shares over the next 2 years, your call options get diluted too. The $20 strike looks attractive today, but if share count grows 30%, you need the market cap to grow 30% just to maintain the same stock price. This is why patient capital (2027-2028 expiration) is required - giving the company time to grow revenue faster than share count.

Macroeconomic Headwinds 🌪️

Rising Rate Risk: Manufacturing expansion is capital-intensive. While the $600M convertible notes are at just 1.75%, a prolonged high-rate environment makes it harder to justify multi-billion dollar infrastructure projects that EOSE's customers need to fund.

Policy Risk: The IRA tax credits (45X manufacturing credits worth $35-45/kWh) are critical to EOSE's unit economics. While the One Big Beautiful Bill maintained core provisions per Plante Moran analysis, future administrations could modify or eliminate these credits. A 2028 presidential election that changes clean energy priorities would hurt long-term outlook.

Competition Risk: The energy storage market is getting crowded. Per Coherent Market Insights research, intense pricing pressure is driving consolidation and smaller players are struggling. EOSE needs to hit scale fast before they get squeezed out by better-capitalized competitors.

🎯 The Bottom Line

Real talk: This $21.2M institutional bet on EOSE is one of the more fascinating option flows we've seen in the cleantech space. Here's the deal:

If You Own It: You're sitting on a stock that's up 208% in 3 months but pulled back 35% from highs. The $12.50 gamma support should hold if the thesis remains intact. Your decision point is February 20, 2026 earnings. If they deliver $100M+ Q4 revenue with positive contribution margin, hold through mid-2026 factory opening. Target $18-20. If they miss revenue or can't achieve positive contribution margin, consider taking profits in the $12-14 range - the 208% gain is already yours to protect.

If You're Watching (Like Me): Mark your calendar for these key dates:

- January 21-24, 2026: World Economic Forum - Watch for any major partnership announcements or customer wins

- February 20, 2026: Q4 earnings - THE inflection point that determines if the bull case is real

- Mid-2026: New factory opening - Proof the production ramp is happening

Entry points: $12.50 on any dip (gamma support), or $13.50-14.00 after a successful Q4 earnings report that confirms the trajectory.

If You're Bearish: The insider selling (18 sales, 0 buys) and history of revenue misses make this a legitimate short candidate if Q4 disappoints. Wait for confirmation that guidance is lowered, then puts in the $10-12 range could pay off handsomely. But respect the $12.50 gamma support and the fact that a well-capitalized institution just bet $21M on the upside.

My Take: The institutional buyer isn't trading this - they're investing in a 2-3 year thesis that AI data centers will drive massive demand for safe, domestic, long-duration energy storage, and EOSE's zinc-battery technology will capture meaningful share. The 2027-2028 expiration dates tell you everything: they expect bumps along the way but believe the endgame is worth the wait.

For retail traders, this is NOT a short-term flip. It's a "buy the dips, hold through volatility, sell into strength" type of play. The risk/reward is attractive IF you have patience and can stomach 20-30% drawdowns while the company executes.

The Lesson: When you see $21M deployed into long-dated calls during a pullback, pay attention. It's either a massive bet that pays off big, or an expensive lesson in execution risk. Given EOSE's $22.6B pipeline, DOE backing, Talen partnership, and perfect timing for AI power demand, I'm leaning toward the former. But I'm not betting the farm until they prove they can hit Q4 revenue guidance.

Risk Rating: 7/10 (High risk, high reward - execution-dependent with binary outcomes)

Conviction Level: Watching closely, ready to enter at $12.50 or after Q4 earnings confirm trajectory

Position Sizing: 3-5% of portfolio max, preferably through 2026+ dated calls to match institutional timeframe

⚠️ Disclaimer: This analysis is for educational and informational purposes only and does not constitute financial advice, investment recommendations, or solicitation to buy or sell securities. Options trading involves substantial risk of loss and is not suitable for all investors. Past performance does not guarantee future results. Always conduct your own due diligence and consult with a qualified financial advisor before making investment decisions. The author may or may not hold positions in the securities discussed.

📊 Data Sources: Option flow data from ThetaData, catalyst research from company filings and reputable financial news sources, gamma analysis from proprietary models, implied volatility data from options markets. All figures accurate as of December 22, 2025.

Last Updated: December 22, 2025 Analysis by ainvest Option Flow Research Team

For more unusual options activity and trade ideas, visit ainvest.com