EQT $645K Put Position - Natural Gas Giant Gets Defensive Hedge

December 10, 2025 | Unusual Activity Detected

The Quick Take

A sophisticated trader just deployed $645,000 on EQT puts this morning at 09:41:57, purchasing 12,900 contracts of January 23rd $51 strike puts while the stock trades at $57.96. This substantial bearish hedge protects against a 12% downside move in America's largest natural gas producer over the next 44 days. With EQT up nearly 50% over the past year and natural gas prices facing winter volatility, smart money is locking in downside protection below key gamma support levels. Translation: Institutions are buying insurance on their natural gas exposure as we enter peak heating season with uncertain demand and pricing dynamics.

Company Overview

EQT Corporation (EQT) is America's largest natural gas production company, operating exclusively in the prolific Marcellus and Utica shale formations of the Appalachian Basin:

- Market Cap: $36.52 Billion

- Industry: Natural Gas Production & Midstream

- Current Price: $57.96 (52-week range: $42.27 - $62.23)

- Primary Business: Natural gas production, gathering, and transmission infrastructure

- Strategic Position: Vertically integrated following July 2024 Equitrans Midstream merger

- Production Scale: 2,100+ Bcfe (billion cubic feet equivalent) annually

- Reserve Base: 26.3 Tcfe across 2.1 million gross acres

- Employees: 1,461

EQT dominates the Appalachian Basin, which accounts for 31% of total U.S. natural gas production. The company operates the lowest-cost natural gas production in America with a breakeven price of approximately $2.00/MMBtu, providing substantial margin cushion even in weak pricing environments.

The Option Flow Breakdown

The Tape (December 10, 2025 @ 09:41:57):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:41:57 | EQT | ASK | BUY | PUT $51 | 2026-01-23 | $645K | $51 | 13,000 | 0 | 12,900 | $57.96 | $0.50 |

What This Actually Means

This is a defensive hedge on an existing long position in EQT. Here's the breakdown:

- Premium paid: $645,000 ($0.50 per contract x 12,900 contracts x 100 shares)

- Protection strike: $51 provides 12% downside cushion below current $57.96 price

- Strategic timing: 44 days to expiration captures natural gas winter volatility, potential weather disappointments, and LNG export uncertainty

- Size matters: 12,900 contracts represents 1.29 million shares worth approximately $75 million at current prices

- Institutional insurance: Opening interest of 0 means this is a fresh position, not closing an existing trade

- Cost structure: At $0.50 per share, the trader is paying 0.86% of the stock price for protection against 12% downside

What's really happening here:

This trader likely holds a substantial long position in EQT stock accumulated during the rally from the low-$40s to near $60. Now, with the stock trading at $57.96 (down from recent highs of $62.23), they're paying $0.50 per share for January 23rd $51 puts as portfolio insurance. If EQT drops below $51 by January expiration, these puts pay off dollar-for-dollar below the strike.

The $51 strike is strategically positioned just above the major $50 gamma support level (5.2M total gamma), suggesting the trader expects that if EQT breaks the critical $55 support zone, momentum could accelerate quickly toward $50-51.

Key insight: The relatively modest premium ($0.50) reflects current implied volatility and out-of-the-money positioning. This isn't a bearish bet on collapse - it's prudent risk management protecting against a 10-15% pullback scenario if natural gas fundamentals disappoint during winter heating season.

Technical Setup / Chart Analysis

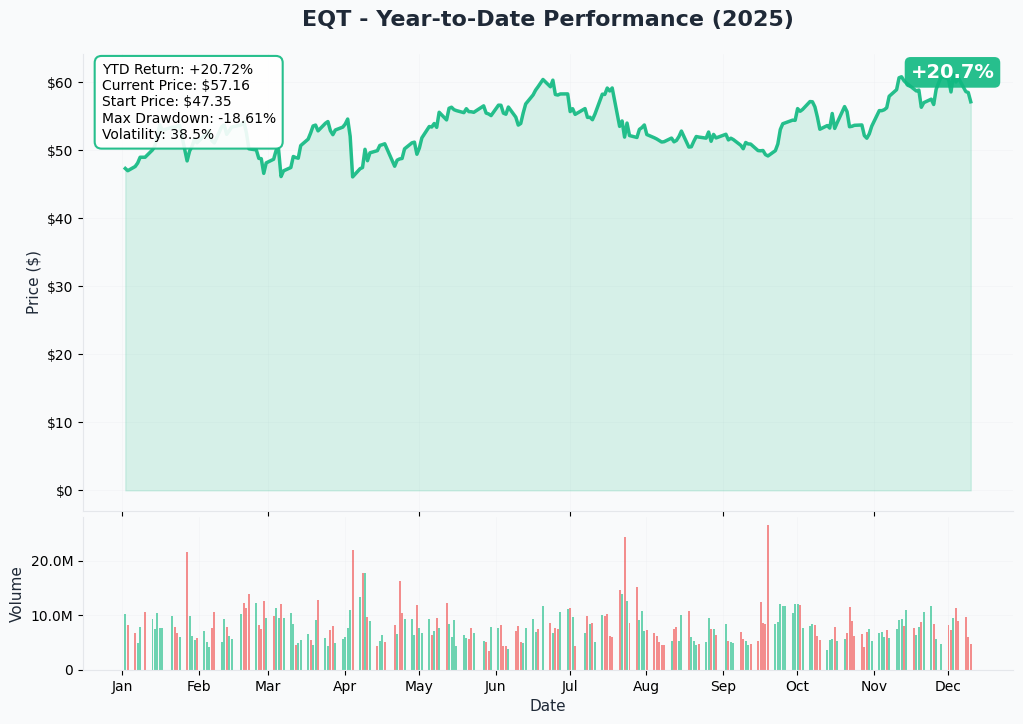

YTD Performance Chart

EQT has delivered strong performance in 2025, though recent action shows consolidation near resistance. Current price of $57.96 sits well above the year's starting point, reflecting positive sentiment around natural gas demand growth from LNG exports and AI data center expansion.

Key observations:

- Strong uptrend: Rally from $42 low to $62 high demonstrates 47% appreciation

- Recent consolidation: Trading below recent $62.23 peak suggests profit-taking

- Volume patterns: Increased institutional participation evident in recent months

- Volatility range: Stock has shown capacity for sharp 10-15% moves in both directions

- Support test: Currently holding above mid-$50s support zone

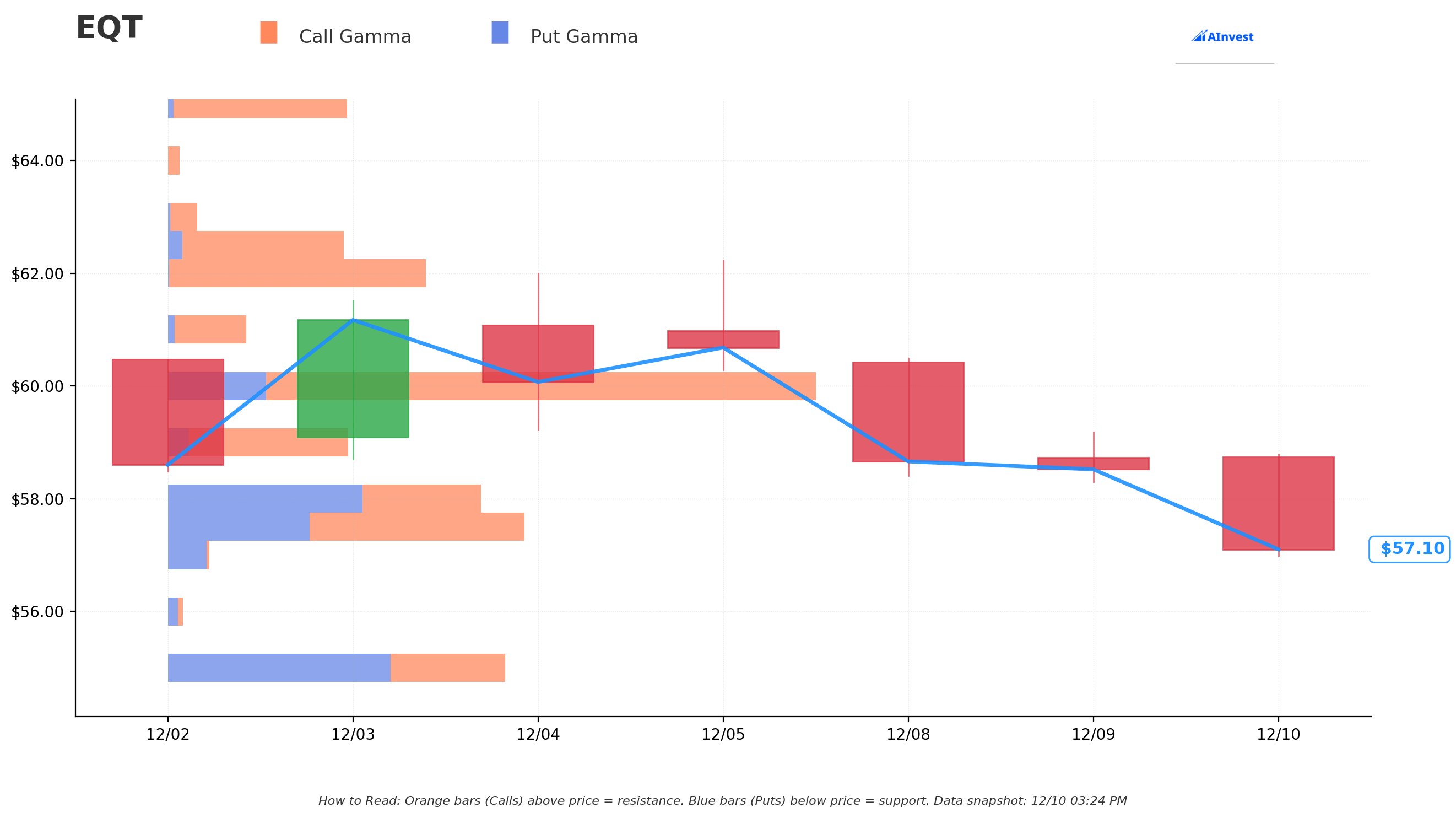

Gamma-Based Support & Resistance Analysis

Current Price: $57.34

The gamma exposure map reveals critical price levels that will govern near-term trading dynamics:

Support Levels (Put Gamma Below Price):

-

$55.00 - Strongest nearby support with 8.98M total gamma (2.79M net put gamma)

- Distance: 4.1% below current price

- This is the LINE IN THE SAND - dealers will aggressively buy dips here

-

$52.50 - Secondary support at 3.27M total gamma (1.66M net put gamma)

- Distance: 8.4% below current price

- Significant put protection clustered at this level

-

$50.00 - Major structural floor with 7.86M total gamma (5.16M net put gamma)

- Distance: 12.8% below current price

- Massive put gamma wall - catastrophic support level

- Just below the $51 put strike in this trade (not coincidental)

Resistance Levels (Call Gamma Above Price):

-

$57.50 - Immediate ceiling with 9.75M total gamma (2.07M net call gamma)

- Distance: 0.3% above current price

- STRONGEST NEARBY RESISTANCE - dealers will sell rallies here

-

$58.00 - Secondary resistance at 8.57M total gamma

- Distance: 1.2% above current price

-

$59.00 - Additional resistance at 5.06M total gamma (3.87M net call gamma)

- Distance: 2.9% above current price

-

$60.00 - Major ceiling zone with 18.17M total gamma (12.38M net call gamma)

- Distance: 4.6% above current price

- MASSIVE call gamma wall - psychological round number resistance

-

$62.00-$65.00 - Extended resistance cluster

- Multiple strikes with significant call gamma

- Would require major catalyst to break through

What this means for traders:

EQT is compressed in a tight range between $57.50 resistance overhead and $55 support below. The gamma structure shows heavy concentration at round numbers ($55, $60), creating natural price magnets. The $60 level stands out with 18.17M total gamma - the single largest concentration on the entire options chain - which will create intense selling pressure on rallies.

Notice the strategy: The put buyer struck at $51, positioning just above the massive $50 support level with 7.86M gamma. This suggests they expect the $55 support to hold most of the time, but want protection if that level breaks, which could trigger rapid movement toward $50-51.

Net GEX Bias: Bullish (61.6M call gamma vs 34.7M put gamma) - Overall positioning remains constructive, but immediate price action is range-bound between strong support/resistance levels.

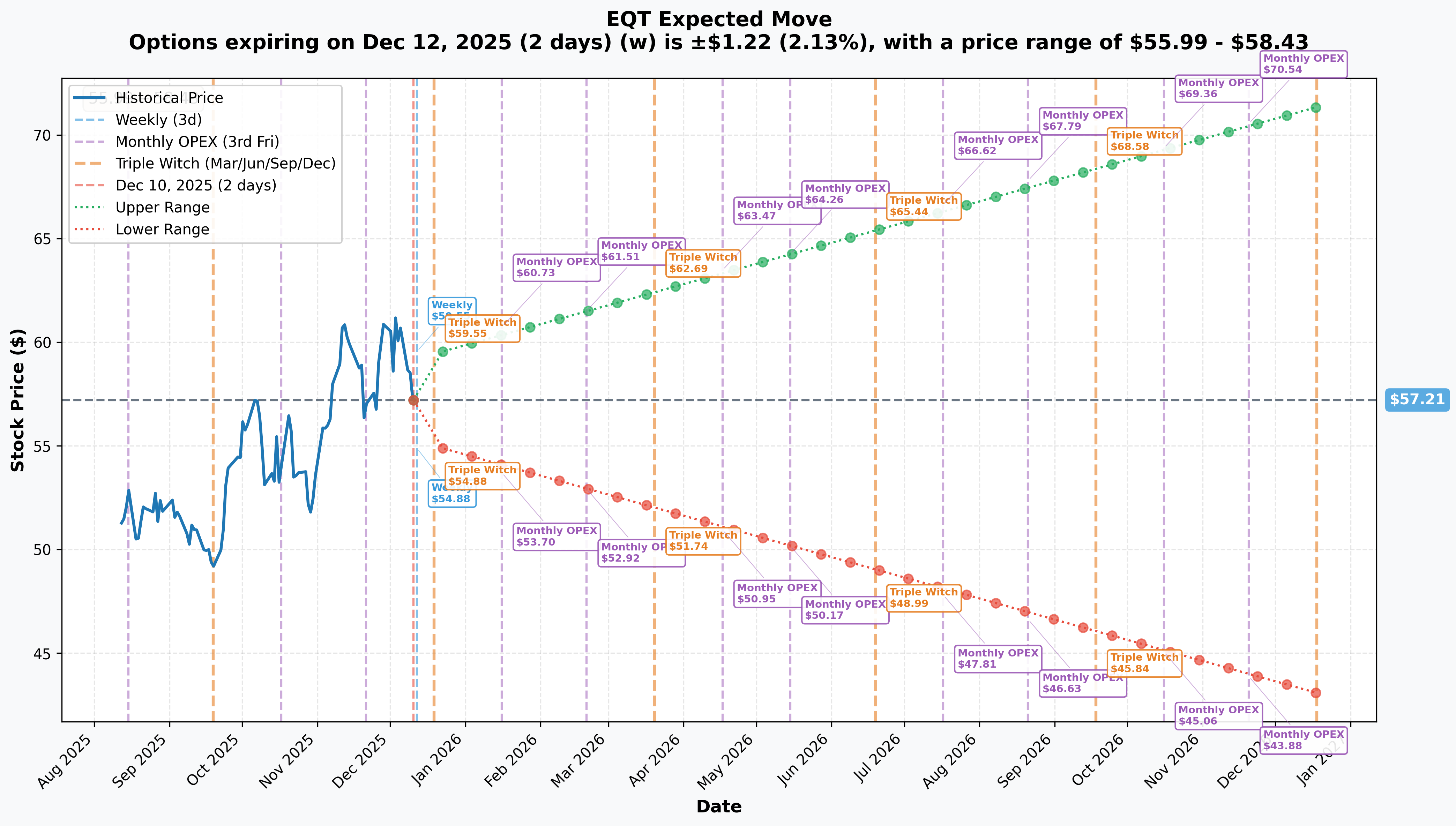

Implied Move Analysis

Options market pricing for upcoming expirations:

- Weekly (Dec 12 - 2 days): ±$1.22 (±2.13%) → Range: $55.99 - $58.43

- Monthly OPEX (Dec 19 - 9 days): ±$2.24 (±3.91%) → Range: $54.98 - $59.45

- Quarterly Triple Witch (Dec 19 - 9 days): ±$2.24 (±3.91%) → Range: $54.98 - $59.45

- January OPEX (Jan 16 - 37 days): Expected ±4-5% move

- Yearly LEAPS (Dec 2026 - 373 days): ±$14.15 (±24.74%) → Range: $43.06 - $71.36

Translation:

Options traders are pricing relatively modest near-term volatility (2-4% weekly/monthly moves), suggesting the market expects EQT to remain range-bound absent major natural gas pricing catalysts. The January timeframe (when this put trade expires on Jan 23rd) encompasses key winter heating season data points and Q4 earnings.

The $54.98 lower range on December 19th OPEX sits just below the $55 major support level, aligning with the downside risk the put buyer is hedging against. If weather disappoints or natural gas prices weaken, the stock could test that $54-55 support zone.

Key insight: The relatively low implied volatility (2-4% near-term) makes put protection relatively inexpensive, which may explain why the trader is comfortable paying $645K for this hedge rather than accepting unprotected downside risk.

Catalysts

Immediate Catalysts (Next 30 Days)

Winter Heating Season Demand (December 2025 - February 2026)

The next 60-90 days represent peak natural gas demand season, with weather patterns driving pricing and sentiment:

- Weather wildcards: Mild winter temperatures could reduce heating demand significantly, pressuring natural gas prices and EQT's revenue outlook

- Inventory dynamics: U.S. natural gas storage levels heading into winter will impact spot pricing

- Henry Hub pricing: Forecasted to average $4.30/MMBtu for winter 2024-2025 (up 22% from prior winter), but vulnerable to weather disappointment

- EQT exposure: Company's revenue highly correlated to natural gas spot prices despite low-cost production advantage

- Historical precedent: Mild winters in 2019 and 2020 caused 20-30% natural gas price declines and corresponding stock selloffs

Natural Gas Price Volatility

EQT's stock price typically moves in sympathy with natural gas futures:

- Current dynamics: Natural gas prices have been volatile, with EIA forecasting 43% increase in 2025 followed by 27% gain in 2026

- LNG export growth: U.S. LNG exports expected to increase 25% in 2025 (adding 2.1 Bcf/d demand), providing structural support

- Downside risk: Any delays in LNG facility startups (Plaquemines, Golden Pass) could remove 2+ Bcf/d of expected demand

- Appalachian basis: Regional pricing differentials remain a concern despite Mountain Valley Pipeline capacity additions

Q4 2024 Earnings Preview (Expected Late January/Early February)

While formal earnings are likely after this put expires, preliminary Q4 guidance commentary could emerge:

- Production expectations: Full-year 2024 production exceeded 2,100 Bcfe target

- Debt reduction progress: Key metric to watch - company targeting path to $7B net debt

- Integration synergies: Equitrans merger synergy realization (currently $200M+ captured)

- 2025 guidance: Initial outlook for production (2,175-2,275 Bcfe) and capital efficiency

Near-Term Catalysts (Q1 2025)

Q1 2025 Earnings (Expected Late April 2025)

First formal quarterly report after this put expires, but forward-looking statements matter:

- Expected production: 525-575 Bcfe for Q1

- Operating metrics: Cost per Mcfe, gathering cost efficiency, curtailment levels

- Free cash flow: Tracking toward $2.6B target for full year 2025

- Debt milestones: Progress toward year-end $7B net debt target from current $9.1B

- Capital allocation: Dividend growth sustainability (recently increased 5% to $0.66/share)

LNG Export Capacity Ramp

Major LNG facilities coming online create structural demand for Appalachian gas:

- Plaquemines Phase 1: Started production December 2024

- Corpus Christi Stage 3: Recently operational

- Golden Pass LNG: Preparing to start operations in 2025

- Plaquemines Phase 2: Expected online 2025

- Cumulative impact: Additional 4+ Bcf/d of natural gas demand from new LNG capacity

- EQT benefit: Marcellus/Utica gas increasingly flowing to Gulf Coast LNG terminals via improved pipeline infrastructure

Mountain Valley Pipeline Expansion

EQT planning 500 MMcf/d expansion of the critical Mountain Valley Pipeline:

- Current status: 303-mile MVP entered service June 2024, providing 2 Bcf/d takeaway capacity

- Expansion timeline: Regulatory approval process underway for 500 MMcf/d addition

- Strategic importance: MVP alleviates historical Appalachian takeaway constraints, connecting EQT's core production to Southeast markets

- Demand driver: Southeast power generation growth (data centers, coal retirements) creating local demand surge

- Risk factor: MVP has faced environmental scrutiny with pollution reports and DEP violations - expansion approval uncertain

Longer-Term Catalysts (2025-2026)

AI Data Center Demand Acceleration

EQT has positioned itself as exclusive natural gas supplier to major data center developments:

- Homer City partnership: Announced July 2025 - exclusive supplier to 4.4 GW Homer City Energy Campus in Pennsylvania

- Additional projects: Shippingport Power Station conversion, West Virginia gas plants targeting AI/data center load

- Market projections: CEO Toby Rice projects 20-40% increase in U.S. natural gas demand from AI infrastructure

- Local advantage: Mountain Valley Pipeline provides unique access to growing Southeast data center corridor

- Timeline: Coal plant conversions and new gas generation expected to create 6 Bcf/d demand by 2030 in EQT's backyard

- Goldman Sachs forecast: Natural gas will supply 60% of AI/data center power demand growth through 2030

Appalachian Basin Market Dynamics

EQT's competitive positioning in the nation's most economic gas production region:

- Cost leadership: $2/MMBtu unlevered breakeven vs $3-4 for other major basins

- Vertical integration advantage: Only large-scale vertically integrated natural gas company post-Equitrans merger

- Infrastructure access: Nearly 3,000 miles of pipeline infrastructure provides midstream control

- Market share opportunity: Appalachian production has been rangebound at 34-36 Bcf/d - structural demand growth could unlock basin expansion

- Efficiency gains: Full-year 2024 gathering costs down 45% YoY to $0.35/Mcfe; total operating costs down 7.5% to $1.23/Mcfe

Free Cash Flow and Shareholder Returns

EQT's financial roadmap emphasizes cash generation and debt reduction:

- 2025 FCF target: Approximately $2.6 billion at recent strip pricing

- 2026 FCF target: Approximately $3.3 billion (27% increase)

- Five-year target: $19 billion cumulative free cash flow through 2029

- Dividend growth: 5% increase to $0.66/share (8% CAGR since 2022); four consecutive years of increases

- Debt reduction: From $9.1B net debt (end-2024) to $7B target (end-2025), ultimate goal of $5-7B range

- Asset sales program: Targeting $3-5B in upstream sales and regulated EBITDA monetization to accelerate deleveraging

Risk Catalysts (Negative)

Natural Gas Price Collapse Scenario

The primary risk to EQT remains natural gas pricing vulnerability:

- Mild winter weather: Warm temperatures in Dec-Feb could crater heating demand, sending Henry Hub to $2-2.50 range

- Oversupply dynamics: Appalachian production growth outpacing takeaway capacity additions

- LNG delays: Any postponement of planned LNG facility startups removes 2+ Bcf/d expected demand

- Roth MKM concern: Analysts expect gas prices to "disappoint vs. 2026 futures curve"

- Historical precedent: 2024 saw strategic curtailments of 27 Bcfe in Q4 due to weak prices; Q4 2025 guidance includes 15-20 Bcfe curtailments

- Stock correlation: EQT typically falls 15-25% when natural gas drops 20-30%

Debt and Leverage Execution Risk

Balance sheet remains elevated post-Equitrans merger:

- Current leverage: Net debt of $9.1B vs $5.7B year-ago (increased due to $5.4B Equitrans acquisition)

- Aggressive target: Reducing to $7B by end-2025 requires $2.1B reduction in 12 months

- Asset sale dependency: $3-5B asset sales program may face market conditions or valuation challenges

- Free cash flow assumption: $2.6B FCF projection assumes maintenance of current strip pricing (vulnerable to gas price weakness)

- Credit metrics: Total debt currently $9.3B; only $0.2B drawn on $3.5B revolver provides cushion but leverage ratios elevated

Mountain Valley Pipeline Regulatory/Environmental Risk

Critical infrastructure asset faces ongoing scrutiny:

- Violation history: Three notices of violation from DEP in 2024; 42 citizen pollution reports in Virginia since January 2024

- Operational issues: Section burst during May 2024 pressure test at Bent Mountain

- Environmental opposition: Sierra Club citing "hundreds of water quality violations"

- Expansion uncertainty: 500 MMcf/d expansion requires regulatory approvals that may be delayed or denied

- Political risk: Changing regulatory environment could increase compliance costs or limit operational flexibility

Integration and Operational Execution

Equitrans merger integration still underway:

- Integration progress: 90% complete but remaining 10% may encounter challenges

- Synergy realization: $200M+ base synergies captured; upside synergies only 35% de-risked

- Production execution: Well performance variability, weather disruptions, midstream constraints

- Olympus acquisition: Also integrating Olympus Energy Marcellus acquisition in 2025 - dual integration risk

Macroeconomic and Policy Risks

Broader economic factors could impact fundamentals:

- Recession scenario: Economic slowdown reduces industrial/commercial gas demand

- Export policy changes: Shifts in U.S. LNG export permitting or tariffs affecting gas markets

- Data center demand uncertainty: Former FERC Chairman questioned whether all projected data center power demand "is real"; some regions readjusting projections downward

- Renewable competition: 40% of data center power growth projected from renewables vs 60% from natural gas

Trading Ideas

Conservative: Sell Cash-Secured Puts Below Support

Play: Sell $52.50 or $55 strike puts for January or February expiration, collecting premium while potentially acquiring shares at support

Structure: Sell January $55 puts, collect $2-3 premium

Why this works:

- Support-based entry: $55 represents major gamma support (8.98M total gamma) where dealers will defend

- Income generation: Collect $2-3 per share ($200-300 per contract) while waiting for better entry

- Defined risk: If assigned at $55, net basis becomes $52-53 (effectively buying 5-9% below current $57.96 price)

- Fundamental cushion: EQT's $2/MMBtu breakeven provides margin of safety even in weak gas price environment

- Technical positioning: Selling into support where institutional buyers historically emerge

Risk management:

- Position sizing: Only allocate 25-30% of intended EQT position size via short puts

- Cash backing: Maintain 100% cash to take assignment if stock falls to strike

- Exit strategy: Close puts at 50-70% profit rather than holding to expiration

- Stop loss: If stock breaks below $52.50 support decisively, buy back puts to avoid assignment in falling market

Expected outcome: 60-70% probability puts expire worthless, keeping full premium. 30-40% probability of assignment, acquiring shares 5-9% below current price with reduced cost basis from premium collected.

Risk level: Moderate (could own falling stock) | Skill level: Intermediate

Balanced: Bullish Put Spread - Play the Range

Play: After any near-term weakness, sell put spreads targeting the $52.50-$55 support zone

Structure: Sell $55 puts / Buy $52.50 puts (January or February expiration)

Why this works:

- Defined risk: Maximum risk of $2.50 per spread ($250 per contract) minus credit received

- High probability: Requires stock to stay above $55 (only 4% below current price)

- Gamma support: Both strikes sit at major put gamma concentrations where dealers buy dips

- Range-bound setup: Stock trading in $55-$60 range for weeks - spread captures premium from consolidation

- Time decay advantage: Theta erosion works in your favor as put seller

- Favorable skew: Put options trade at premium due to downside volatility concerns - selling rich volatility

Estimated P&L:

- Credit received: Approximately $0.80-1.20 net credit per spread (adjust based on entry timing)

- Max profit: $80-120 per spread if EQT stays above $55 at expiration

- Max loss: $170-130 per spread if EQT falls below $52.50

- Breakeven: Approximately $53.80-54.20

- Win rate: Approximately 70-75% based on current implied volatility

Entry timing:

- Ideal setup: Wait for pullback to $56-57 range to enter spread (improves credit received)

- Avoid: Don't enter if stock already trading at/below $55 (spread too close to at-the-money)

- Duration: 30-45 days to expiration provides optimal time decay while avoiding excessive gamma risk

Position sizing: Risk 1-3% of portfolio per spread (sell 1-3 spreads initially)

Management:

- Profit target: Close at 60-70% max profit rather than holding to expiration

- Stop loss: Exit if stock closes below $54 (spread in trouble)

- Rolling: If stock weakens, can roll spread down and out to later expiration to collect additional credit

Risk level: Moderate (defined risk, bullish assumption) | Skill level: Intermediate

Aggressive: Copy the Institutional Hedge - Disaster Insurance

Play: Buy out-of-the-money puts as portfolio insurance if holding long stock position

Structure: Buy $51 or $50 strike puts for February or March expiration (rolling protection forward from this trade)

Why this could work:

- Smart money validation: $645K institutional purchase at $51 strike signals sophisticated risk management

- Gamma alignment: $50 strike sits at massive 7.86M gamma support - if that breaks, stock could gap down quickly

- Asymmetric payoff: Small premium (likely $0.40-0.70 per contract) protects against 10-15% drawdown

- Winter volatility: Heating season weather uncertainty through Feb/March creates binary events (cold snap vs mild winter)

- Natural gas correlation: Protection against 20-30% natural gas price collapse scenario

- Debt concerns: If debt reduction targets missed or asset sales delayed, stock could test lower levels

Cost structure (estimated for February expiration):

- $51 strike puts: Approximately $0.50-0.70 per share

- $50 strike puts: Approximately $0.30-0.50 per share

- Notional protection: Each contract protects 100 shares worth $5,796 at current price

- Insurance cost: 0.5-1.2% of position value for 60-90 day protection

When this pays off:

- Mild winter scenario: Weak heating demand sends natural gas to $2.00-2.50 range; EQT falls to $48-52

- LNG delays: Plaquemines or Golden Pass postponed, removing 2+ Bcf/d demand

- Debt concerns: Company misses deleveraging targets or guidance disappoints

- Macro selloff: Broader energy sector weakness drags EQT down 15-20% despite solid fundamentals

Example P&L (using $51 puts at $0.60 cost):

- Stock at $45 in February: Puts worth $6.00, profit = $5.40 per share (900% ROI)

- Stock at $48 in February: Puts worth $3.00, profit = $2.40 per share (400% ROI)

- Stock at $51 in February: Puts worth $0 (at-the-money), loss = -$0.60 per share (100% loss)

- Stock at $55+ in February: Puts expire worthless, loss = -$0.60 per share (100% loss)

Critical considerations:

- Hedging only: This trade ONLY makes sense if you own EQT stock or are actively long the energy sector

- Cost of insurance: Expect to lose premium 70-80% of the time - that's the cost of protection

- Position sizing: Buy 1 put per 100-150 shares owned (partial hedge, not 1:1)

- Rolling strategy: If puts approach expiration with stock stable, can roll to next month for continued protection

Why this could fail:

- Theta decay: Paying $0.50-0.70 for protection that decays to $0 if stock stable

- Mild downside: Stock drops to $54-55 (below current but above $51 strike) - puts still expire worthless

- Volatility crush: If natural gas stabilizes and volatility compresses, put values decline even if stock flat

- Opportunity cost: Capital tied up in insurance premiums could be deployed in positive-carry strategies

ONLY attempt this if you:

- Currently hold long EQT position worth $50K+ that you want to protect

- Understand this is insurance with negative expected value (like homeowner's policy)

- Can afford to lose 100% of premium paid (should happen 70-80% of time)

- Have specific concerns about winter weather, LNG timing, or debt execution

- Plan to hold stock position through potential volatility rather than just selling

Risk level: Low (if hedging existing long) / Extreme (if speculating without stock) | Skill level: Advanced

Probability of profit: 20-30% (low by design - this is insurance, not speculation)

Risk Factors

Don't get caught by these potential landmines:

-

Natural gas price volatility: EQT's revenue and profitability directly tied to Henry Hub natural gas prices. Winter 2024-2025 forecast of $4.30/MMBtu provides cushion above $2.00 breakeven, but mild weather could send prices to $2.50-3.00 range, compressing margins and triggering production curtailments. Historical precedent shows EQT can fall 20-25% when natural gas declines 30%+. Company curtailed 27 Bcfe in Q4 2024 and planning 15-20 Bcfe curtailments in Q4 2025 already built into guidance.

-

Debt reduction execution risk: Net debt of $9.1B (up from $5.7B pre-Equitrans merger) requires aggressive deleveraging to reach $7B year-end 2025 target. This demands $2.1B debt reduction in 12 months through combination of free cash flow generation (assumes $2.6B FCF on stable gas prices) and $3-5B asset sales program. If natural gas prices weaken or asset sales face market headwinds, debt targets could be missed, triggering credit rating concerns and stock multiple compression.

-

Mountain Valley Pipeline regulatory/environmental uncertainty: Critical infrastructure asset has received three DEP violations in 2024, 42 citizen pollution reports, and experienced a section burst during pressure testing. Ongoing environmental scrutiny from Sierra Club and local opposition creates risk for planned 500 MMcf/d expansion. Any permitting delays, additional violations, or operational restrictions could limit EQT's takeaway capacity advantage and reduce the strategic value of vertical integration.

-

Winter heating season binary event: The next 60-90 days represent peak natural gas demand period. Weather patterns during Dec 2025 - Feb 2026 will largely determine natural gas pricing through Q1. Mild winter (similar to 2019-2020) could crater demand and send natural gas prices down 20-30%, directly impacting EQT's revenue and forcing additional production curtailments beyond the 15-20 Bcfe already planned. Stock could test $50-52 support on such a scenario.

-

LNG export facility startup delays: EQT's bullish thesis heavily dependent on 25% LNG export growth in 2025 adding 2.1 Bcf/d natural gas demand. Plaquemines Phase 2, Golden Pass, and other facilities must start on schedule. Any delays, technical issues, or permitting problems could remove 1-2+ Bcf/d of expected demand, leaving natural gas market oversupplied and pressuring prices. These are complex industrial facilities with long commissioning timelines - execution risk is real.

-

Data center demand uncertainty - question marks remain: While EQT has secured exclusive supplier deals with Homer City (4.4 GW) and other projects, former FERC Chairman Willie Phillips questioned whether all data center projections "are real." Some regions have readjusted downward their power demand forecasts. Natural gas turbines are sold out through decade-end, potentially limiting supply response. If AI/data center power demand growth disappoints even 20-30% vs projections, the 6 Bcf/d by 2030 thesis weakens significantly.

-

Integration execution - two simultaneous mergers: While Equitrans integration is 90% complete with $200M+ base synergies captured, the remaining 10% may encounter unexpected challenges. Upside synergies remain only 35% de-risked. Additionally, EQT is integrating Olympus Energy Marcellus acquisition simultaneously in 2025. Dual integration creates operational complexity, potential cost overruns, and distraction from core business execution. Cultural alignment and system integration always carry hidden risks.

-

Appalachian basis differentials: Despite Mountain Valley Pipeline improving takeaway capacity, regional pricing spreads (Appalachian basis to Henry Hub) can widen during high-production periods, reducing realized prices for EQT vs NYMEX benchmarks. Limited by in-region demand and pipeline constraints, Appalachian production has been rangebound at 34-36 Bcf/d. Without significant infrastructure additions beyond MVP expansion, basin-wide growth constrained.

-

Valuation stretched after 48% run: Stock up 48.8% over past year vs S&P 500 +21.8%, trading near upper end of 52-week range ($42.27-$62.23). At current $57.96 price, much of the positive outlook (LNG demand, AI data centers, debt reduction, synergies) already priced in. Analyst average price target of $61.82 provides only 6.7% upside. Stock has limited margin of safety if any negative catalyst emerges. The $645K put purchase suggests smart money recognizes this risk.

-

Macroeconomic recession scenario: At current valuation, EQT has minimal recession protection. Economic slowdown would reduce industrial/commercial natural gas demand, weaken LNG export economics (Asia/Europe demand destruction), and potentially delay data center infrastructure buildouts. Energy stocks typically underperform 20-40% in recessions regardless of individual company fundamentals. EQT's debt reduction plan assumes robust economic activity through 2025-2026.

-

Export policy and geopolitical risks: Changes in U.S. LNG export permitting under new administration could slow facility approvals, removing future demand growth. Tariffs or trade restrictions could impact natural gas markets. Geopolitical tensions affecting global LNG flows (Russia/Europe dynamics, Middle East instability) create uncertainty for U.S. LNG export economics. Policy risks largely outside EQT's control but directly impact demand outlook.

The Bottom Line

Real talk: Someone just spent $645,000 protecting a $75 million EQT position heading into the critical winter heating season. This isn't a bearish vote on EQT's long-term fundamentals - it's sophisticated risk management by institutions who understand that natural gas prices can collapse 30% in a mild winter, taking the stock down 15-20% with it, regardless of the company's operational excellence.

What this trade signals:

- Volatility ahead: Institutional player expects potential 10-15% downside move over next 44 days (through January 23rd)

- Winter uncertainty: Weather patterns through Feb 2026 will determine natural gas pricing and EQT's revenue trajectory

- Technical positioning: $51 strike sits strategically just above massive $50 gamma support (7.86M) - if $55 breaks, could accelerate to $50-51

- Timing matters: Expires January 23rd, capturing peak heating season data, December/January weather outcomes, and potential Q4 earnings guidance

- Cost-effective hedge: At $0.50 per share (0.86% of stock price), relatively inexpensive insurance against 12% downside scenario

This is NOT a "sell everything" signal - it's prudent risk management in an uncertain environment.

If you own EQT:

- Consider trimming 20-30% near current $57-58 levels to lock in gains from 48% annual run

- Set mental stop-loss at $55 (major gamma support) to protect remaining position

- If holding through winter, consider protective puts at $52.50 or $51 strikes for Feb/March expiration

- Don't get greedy - you've already won with strong YTD gains. Protecting profits is smart.

- If stock breaks above $60 on positive natural gas developments, can re-enter trimmed shares

If you're considering new positions:

- Wait for better entry: Current $57.96 price near recent highs with limited upside to $61.82 analyst target

- Target support zones: Look for pullback to $54-55 range (gamma support) for 5-9% better entry

- Post-winter clarity: Better risk/reward after Feb 2026 when winter weather outcomes known

- Cash-secured puts: Sell $55 puts to collect premium while waiting for dip to support

- Monitor catalysts: Need to see sustained natural gas prices above $3.50, LNG facilities starting on time, data center deals progressing

If you're bearish or cautious:

- Current setup offers reasonable risk/reward for bearish positioning given stock near highs

- Put spreads ($57.50/$55 or $55/$52.50) offer defined-risk downside exposure

- First support at $55 (8.98M gamma), major support at $52.50 (3.27M), critical floor at $50 (7.86M)

- Break below $55 would be technical trigger for cascade toward $52.50-$50

- Wait for any bounce toward $58-59 to initiate bearish spreads at better prices

Key dates to watch:

- December 12 (Weekly OPEX): ±2.13% implied move range ($55.99-$58.43)

- December 19 (Monthly/Quarterly OPEX): ±3.91% implied move range ($54.98-$59.45)

- January 2026: Winter heating season demand becomes clear, LNG facility startup progress known

- January 23, 2026: Expiration of this $645K put position

- Late January/Early February: Preliminary Q4 2024 earnings guidance expected

- Late April 2025: Formal Q1 2025 earnings report

Final verdict: EQT's long-term story remains compelling - America's largest, lowest-cost natural gas producer with vertical integration, positioned for LNG export surge (25% growth in 2025) and AI data center demand expansion (6 Bcf/d by 2030). The company has executed well on Equitrans integration ($200M+ synergies), debt reduction ($4.5B in Q4 2024), and operational efficiency (costs down 7.5% YoY).

BUT, near-term risk/reward is unfavorable at $57.96 after 48% annual gain with winter weather uncertainty ahead. The $645K institutional put purchase is a clear signal: smart money is protecting gains and hedging winter volatility risk. Natural gas prices could disappoint (mild winter, LNG delays), stock could test $52-55 support, and valuation provides minimal cushion.

Be patient. Let winter weather patterns clarify. Look for better entry points at $54-55 support. The natural gas demand story will still be intact in 3-6 months, and you'll sleep better paying $54 instead of $58.

This is a marathon, not a sprint. Protect your capital.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The trade size and structure reflect this specific institutional trader's portfolio needs - it does not imply the trade will be profitable or that you should follow it. Natural gas prices are highly volatile and subject to weather, geopolitical, and supply/demand factors outside anyone's control. Always do your own research and consider consulting a licensed financial advisor before trading.

About EQT Corporation: EQT Corporation is America's largest natural gas production company, operating in the Marcellus and Utica shales of the Appalachian Basin. The company is vertically integrated following its acquisition of Equitrans Midstream, controlling nearly 3,000 miles of pipeline infrastructure. With a market cap of $36.52 billion and industry-leading cost structure ($2/MMBtu breakeven), EQT is positioned to benefit from growing natural gas demand driven by LNG exports and power generation for AI data centers.