EWY Massive $3.3M Bullish Call Buying - Smart Money Betting Big on Korean Semiconductor Rally!

January 15, 2026 | Unusual Activity Detected

The Quick Take

Someone just loaded up on $3.3 MILLION in EWY call options targeting the February 20th expiration! Two separate trades bought 9,700+ contracts betting that South Korea's semiconductor-heavy ETF continues its explosive rally past $115-$116 by next month. With EWY already up +105% in 2025 riding the AI memory chip supercycle and Samsung's record Q4 earnings just two weeks away, institutional money is making aggressive bullish bets on Korean equities. Translation: Big money thinks Korea's AI chip rally has more room to run!

ETF Overview

iShares MSCI South Korea ETF (EWY) provides concentrated exposure to South Korea's export-driven economy, dominated by semiconductor giants:

- AUM: $9.61 Billion

- Current Price: $111.77 - $111.84

- 52-Week Range: $48.49 - $112.20

- Expense Ratio: 0.59%

- Dividend Yield: 1.1%

- P/E Ratio: 17.37

- 2025 Full Year Return: +105.16%

Top Holdings (What You're Actually Buying)

| Holding | Weight | Why It Matters |

|---|---|---|

| Samsung Electronics | 26.12% | World's largest memory chipmaker, just posted record Q4 earnings guidance |

| SK Hynix | 19.40% | #1 HBM supplier with 62% market share, Nvidia's primary memory partner |

| Hyundai Motor | 2.42% | Benefiting from US trade deal tariff reduction |

| KB Financial Group | 2.26% | Leading Korean bank |

| SK Square | 2.06% | SK Hynix holding company |

| Hanwha Aerospace | 2.04% | Defense sector boom from global rearmament |

The top 10 holdings account for 60.76% of the portfolio, with Technology comprising 50.84% of sector allocation. This is essentially a leveraged bet on Samsung and SK Hynix - if you're bullish on AI memory chips, this is your ETF.

The Option Flow Breakdown

What Just Happened

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Z-Score |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12:58:06 | EWY | ASK | BUY | CALL $116 | 2026-02-20 | $1.8M | $116 | 5,000 | 0 | 5,000 | $111.77 | $3.50 | - |

| 10:11:06 | EWY | MID | BUY | CALL $115 | 2026-02-20 | $1.5M | $115 | 4,700 | 112 | 4,215 | $111.84 | $3.61 | 308.89 |

Total Bullish Premium: $3.3 Million

What This Actually Means

These are aggressive directional bets on EWY moving higher by mid-February. Here's the breakdown:

- Trade 1 ($116 strike): Brand new position (0 OI before) - someone initiated a fresh $1.8M bullish bet that EWY breaks above $116 (3.8% higher) within 36 days

- Trade 2 ($115 strike): Z-score of 308.89 classified as "EXTREMELY UNUSUAL" - this is roughly 309x more activity than normal for this contract

- Paid at ASK/MID: Both trades filled at or above mid-price, showing urgency to get positioned - not patient limit orders

- Same expiration: February 20th is a monthly OPEX, capturing Samsung's full Q4 earnings release (January 29th) and any HBM4 contract news

The bet structure: For these calls to be profitable at expiration, EWY needs to trade above:

- $118.50 for the $115 calls to double (breakeven ~$118.61)

- $119.50 for the $116 calls to double (breakeven ~$119.50)

That's roughly 6-7% upside needed in 36 days. Aggressive but achievable given the catalyst density.

Technical Setup / Chart Check-Up

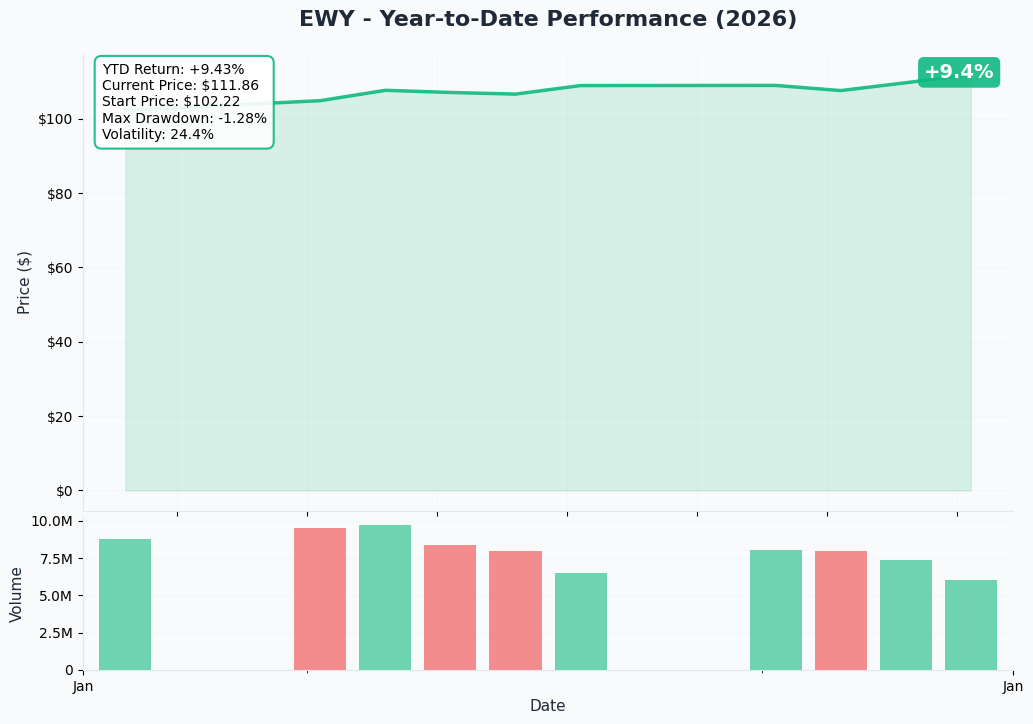

YTD Performance Chart

EWY has been on an absolute tear - up +105% in 2025 riding the AI memory supercycle. The ETF started 2025 around $54 and now trades near all-time highs above $111. After the December 2024 martial law crisis briefly tanked Korean markets, the political stabilization under President Lee Jae-myung combined with Samsung and SK Hynix's record earnings created a relentless bid.

Key observations:

- Sharp recovery from December 2024 political crisis lows near $48

- Nearly uninterrupted rally throughout 2025 as memory prices surged

- Currently consolidating just below all-time highs - potential breakout setup

- Volume patterns suggest institutional accumulation continues

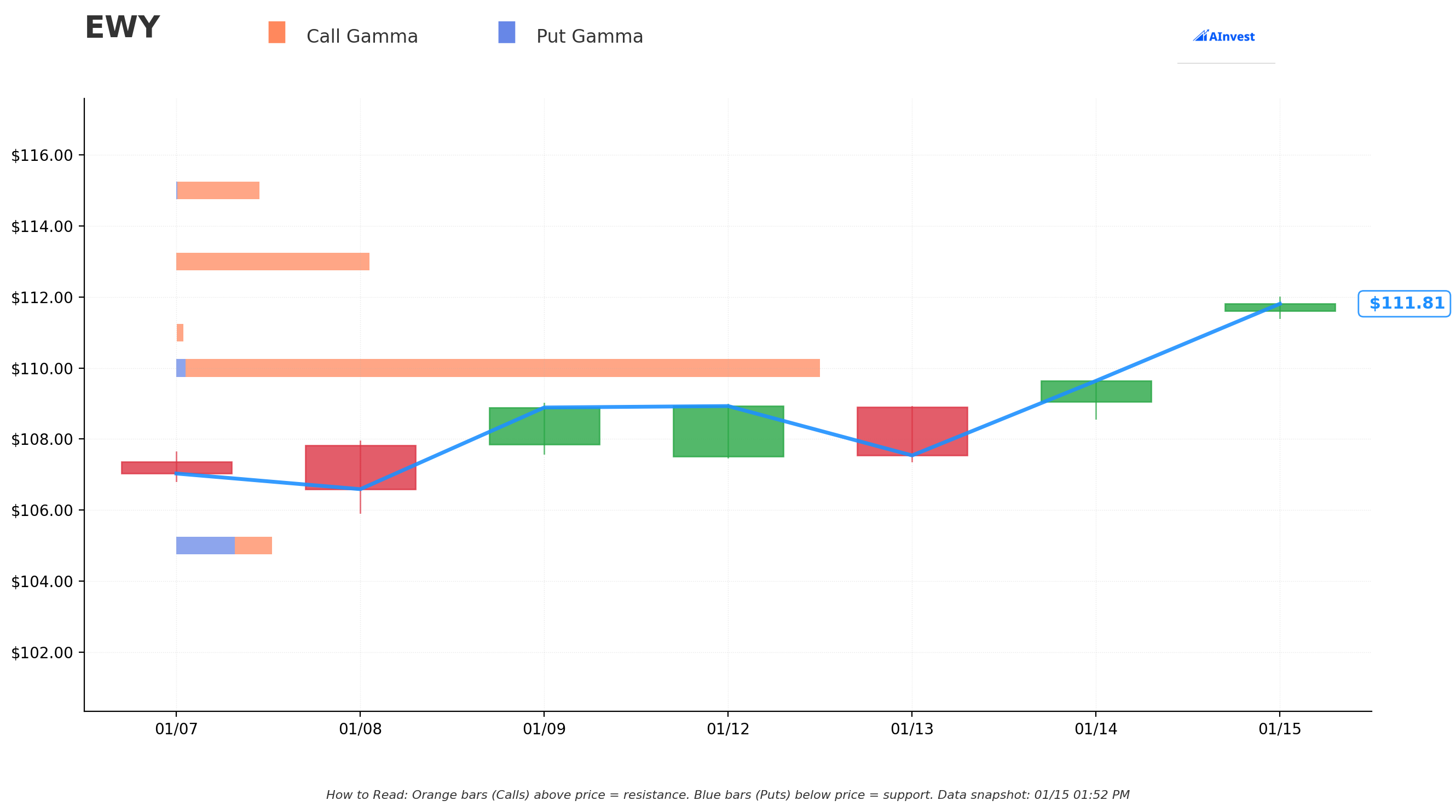

Gamma-Based Support & Resistance Analysis

Current Price: $111.80

The gamma exposure map reveals critical price levels where market maker hedging will create natural support and resistance:

Support Levels (Blue - Put Gamma):

- $111 - Immediate support (0.7% below) with moderate gamma exposure

- $110 - Major gamma floor with 14.74B total exposure - this is THE line in the sand

- $105 - Secondary support (6% below current)

- $100 - Deep support (10.5% below) if broader selloff occurs

Resistance Levels (Orange - Call Gamma):

- $113 - First ceiling (1.1% above) with 4.2B gamma - expect selling pressure here

- $115 - Key resistance (2.9% above) with 1.8B gamma - matches the lower strike of today's trades

- $120 - Extended target (7.3% above) with 2.0B gamma - breakout territory

- $130 - Moonshot level (16.3% above) - requires sustained momentum

Net GEX Bias: BULLISH (27.5B call gamma vs 6.5B put gamma)

The gamma structure strongly favors bulls - there's much more call gamma above price than put gamma below, meaning market makers will need to BUY stock as price rises (positive feedback loop) rather than sell into strength.

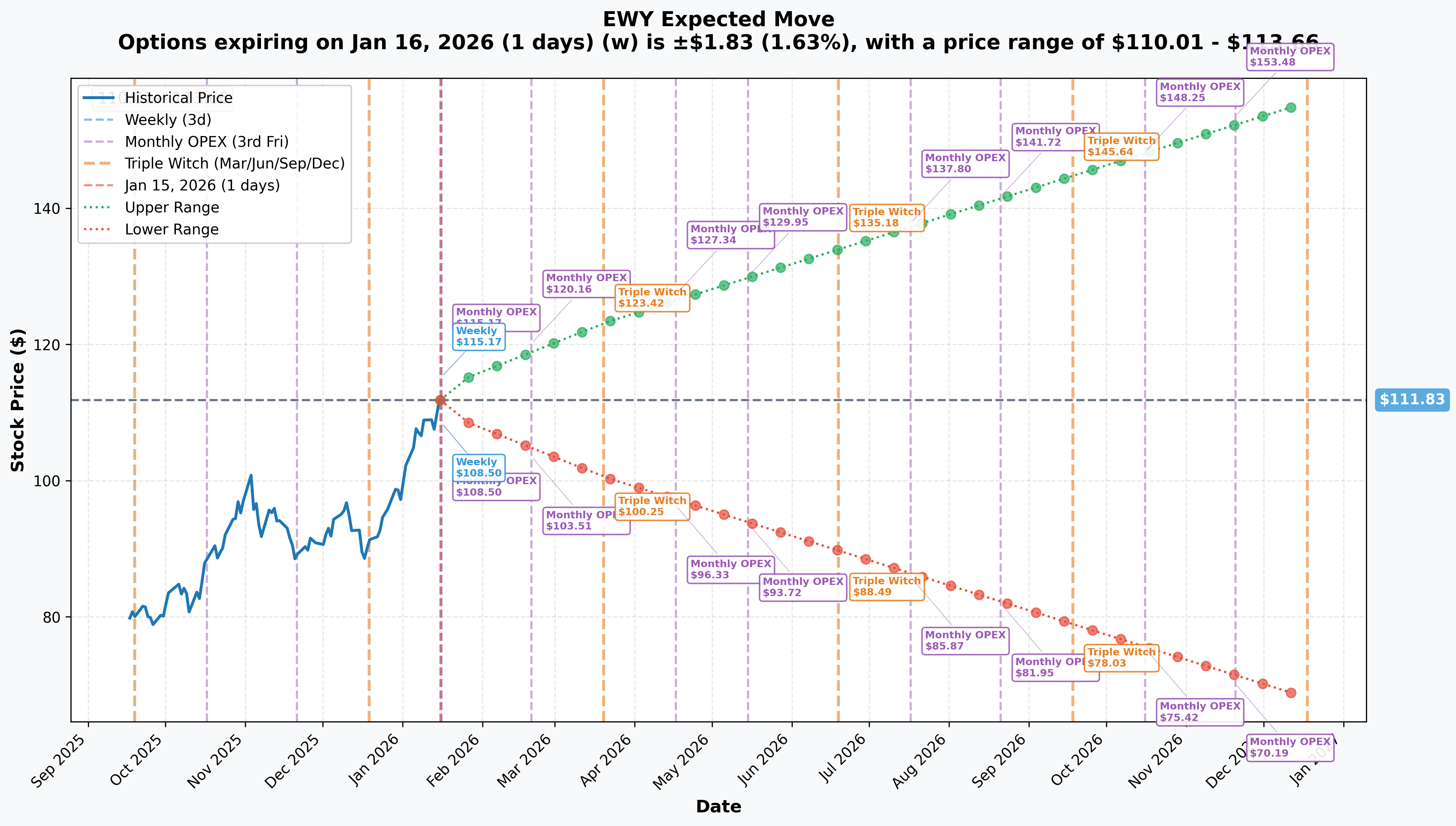

Implied Move Analysis

Options market pricing for February 20th expiration:

| Timeframe | Expiry | Days | Implied Move | Range |

|---|---|---|---|---|

| Weekly | Jan 16 | 1 | +/-1.63% ($1.83) | $110.01 - $113.66 |

| February OPEX | Feb 20 | 36 | +/-7.5% | $103.51 - $120.16 |

| Triple Witch | Mar 20 | 64 | +/-10.15% ($11.35) | $100.49 - $123.18 |

| LEAPS | Dec 18 | 337 | +/-39.15% ($43.78) | $68.05 - $155.62 |

Translation: The options market is pricing in a $103.51 to $120.16 range by February 20th. Both call strikes ($115 and $116) sit comfortably within the upper half of this expected range, suggesting the market views these targets as achievable but not guaranteed.

The February implied move of ~7.5% ($8.32 up or down) means:

- Bullish target: $120.16 upper range aligns with the $120 gamma resistance

- The $115-$116 strikes represent roughly 3-4% moves - well within one standard deviation

- These aren't lottery tickets - they're calculated bets on continued momentum

Catalysts

Upcoming Catalysts (Driving the Trade)

Samsung Electronics Q4 2025 Full Earnings - January 29, 2026 (14 DAYS!)

This is THE catalyst these call buyers are positioning for. On January 8th, Samsung already pre-announced record Q4 earnings guidance that exceeded all expectations:

- Operating Profit: ~20 trillion KRW - nearly tripling YoY and surpassing Samsung's previous record from Q3 2018

- Revenue: ~93 trillion KRW - first time crossing 90 trillion won

- Memory prices surged 40-50% in Q4 with similar gains expected in Q1 2026

The full earnings release on January 29th will provide:

- Detailed segment breakdown (memory vs foundry vs mobile)

- HBM revenue contribution and margin profile

- 2026 guidance on memory pricing outlook

- Progress update on Nvidia HBM4 qualification

HBM4 Contract Finalization with Nvidia - Q1 2026

Both Samsung and SK Hynix are delivering paid final HBM4 samples to Nvidia, moving beyond free prototypes into a commercially-driven phase. Contract finalization expected mid-to-late Q1 2026.

Samsung is close to finalizing negotiations to supply more than 30% of HBM4 for 2026, which would be a major win after setbacks with HBM3E.

Bank of Korea Rate Decision - January 15, 2026 (TODAY)

The BOK held rates steady at 2.5% for a fifth straight meeting as expected. Governor Rhee stated the won is "markedly undervalued relative to fundamentals", suggesting potential currency appreciation ahead which benefits USD-denominated EWY holders.

Recent Catalysts (Why EWY Already Rallied 105%)

Political Stabilization Under President Lee Jae-myung

The December 2024 martial law crisis initially sent the KOSPI tumbling and the won to multi-year lows. However, President Lee's election in June 2025 marked a decisive turning point, with fiscal stimulus, expanded public spending, and consumption-boosting measures that drove the KOSPI to record highs.

AI Memory Supercycle

Bank of America defines 2026 as a "supercycle similar to the boom of the 1990s", forecasting:

- Global DRAM revenue to surge 51% YoY

- HBM market to reach $54.6 billion (+58% YoY)

- DRAM shortages projected to last until Q4 2027 or even 2028

US-Korea Trade Deal

The July 2025 trade agreement secured:

- 15% baseline tariff (down from threatened 25%)

- Annual licenses for Samsung/SK Hynix China chip equipment shipments

- Removal of major trade policy overhang

Value-Up Program Success

Korea's corporate governance initiative produced record share buybacks of 20.1 trillion KRW ($15.3B) in 2025, with the Value-Up Index surging 89.4%. The "Korea discount" is finally closing.

Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through February 20th expiration:

Bull Case (35% probability)

Target: $118-$123

How we get there:

- Samsung Q4 earnings (Jan 29) beat already-high expectations with strong 2026 guidance

- HBM4 contract announcements confirm Samsung's 30%+ share with Nvidia

- Memory price increases of 40-50% continue into Q1 as projected

- Won strengthens from "markedly undervalued" levels per BOK

- Breakout above $113 gamma resistance triggers momentum buying to $120

Key metrics needed:

- Samsung operating profit confirmation at 20T+ KRW

- SK Hynix maintains 62% HBM market share

- No negative surprises on China export restrictions

- Continued foreign inflows into Korean equities

Implied move supports this: The $120.16 upper range for February OPEX aligns with the $120 gamma resistance level. A move to $120 represents +7.3% - right at the implied move boundary.

Base Case (45% probability)

Target: $113-$117 range (CONSOLIDATION WITH UPWARD BIAS)

Most likely scenario:

- Samsung earnings meet the already-released guidance (priced in)

- Gradual grind higher as AI memory narrative continues

- EWY oscillates between $113 gamma resistance and $110 gamma support

- Call buyers profit modestly as theta decays but delta gains offset

- Market awaits March triple witch for clearer direction

This is the call buyer's minimum target: Stock needs to hold above $115 by February 20th for the trades to be meaningfully profitable. The gamma structure and implied move data suggest this is achievable.

Bear Case (20% probability)

Target: $105-$110

What could go wrong:

- Samsung earnings disappoint on guidance despite strong Q4 (forward-looking concerns)

- HBM4 contract delays or Samsung loses share to SK Hynix

- New US-China semiconductor tensions impact Korean suppliers

- Won weakness accelerates despite BOK commentary

- Profit-taking after 105% 2025 rally creates pullback

Support levels:

- $110: Major gamma support with 14.74B exposure - this is the line in the sand

- $105: Secondary support if $110 breaks

- $100: Disaster floor for deep selloff

Probability assessment: Only 20% because the catalyst setup is overwhelmingly positive - record Samsung earnings already pre-announced, HBM demand exceeding supply, political stability achieved, and trade deal in place.

Trading Ideas

Conservative: Shares or Call Spread

"The Sleep Well Strategy"

Play: Buy EWY shares directly OR buy the $113/$118 call spread (Feb 20 expiration)

Why this works:

- Direct exposure to Korean semiconductor rally without leverage risk

- Call spread costs ~$2.00-2.50, max gain ~$2.50-3.00 if EWY hits $118

- Defined risk: you can only lose the premium paid

- Captures Samsung earnings catalyst without excessive theta decay risk

- Gamma support at $110 provides natural floor

Position sizing:

- Shares: Allocate 3-5% of portfolio

- Call spread: Risk 1-2% of portfolio

Entry timing: Enter on any pullback toward $110-$111 gamma support

Risk level: Low to Moderate | Skill level: Beginner-friendly

Balanced: Follow the Smart Money

"Copy the Whales"

Play: Buy the same $115 calls (Feb 20 expiration) that institutional traders purchased today

Structure: Buy EWY $115 calls @ ~$3.50-3.70

Why this works:

- Z-score of 308.89 indicates extremely unusual institutional activity

- $115 strike sits at key gamma resistance - if it breaks, momentum accelerates

- 36 days captures Samsung earnings (Jan 29) and potential HBM4 news

- Breakeven at ~$118.50 is within implied move upper range ($120.16)

- 42x volume-to-OI ratio shows fresh positioning, not position closing

Estimated P&L:

- EWY at $120 by Feb 20: Calls worth ~$5.00, profit ~$1.30-1.50 (35-40% gain)

- EWY at $118 by Feb 20: Calls worth ~$3.00, small loss due to theta

- EWY at $115 by Feb 20: Calls worth ~$0.50, loss of ~$3.00 (80%+ loss)

- EWY at $110 by Feb 20: Calls expire worthless, 100% loss

Position sizing: Risk only 2-3% of portfolio (directional speculation)

Risk level: Moderate | Skill level: Intermediate

Aggressive: Double Down on the Momentum

"The Memory Supercycle Play"

Play: Buy both strikes to maximize exposure to February catalyst window

Structure:

- Buy EWY $115 calls @ ~$3.60 (50% of position)

- Buy EWY $116 calls @ ~$3.50 (50% of position)

Why this could work:

- Matches exact institutional positioning from today's flow

- $3.3M institutional premium signals high conviction

- Samsung record earnings + HBM4 contracts could spark breakout above $120

- Memory supercycle narrative has legs through 2027 per analysts

- If $115 resistance breaks, the $116 calls accelerate faster (higher delta)

Why this could blow up:

- Paying ~$7.10 combined for calls requiring 6-7% move to profit

- Theta decay of ~$0.10-0.15/day eats into position

- "Buy the rumor, sell the news" risk on Samsung earnings

- Concentrated bet on single sector (semiconductors)

Estimated P&L:

- EWY at $123 by Feb 20: Combined profit of ~$6.90 (97% gain)

- EWY at $120 by Feb 20: Combined profit of ~$1.90 (27% gain)

- EWY at $115 by Feb 20: Combined loss of ~$6.60 (93% loss)

Position sizing: Risk only 1-2% of portfolio (high-conviction speculation)

Risk level: HIGH | Skill level: Advanced

Risk Factors

Don't get blindsided by these potential landmines:

-

Semiconductor concentration risk: EWY is 45%+ Samsung and SK Hynix. Any disappointment in memory pricing, HBM4 contracts, or AI demand directly impacts the ETF. This isn't diversified Korea exposure - it's a leveraged memory chip bet.

-

"Priced in" risk on Samsung earnings: The Q4 guidance was already released on January 8th showing record results. The January 29th full release may be a "sell the news" event if forward guidance disappoints or merely meets expectations.

-

China export restrictions wildcard: Both Samsung and SK Hynix operate significant China manufacturing facilities. China accounts for 32.8% ($46.6B) of Korea's semiconductor exports. New US restrictions could disrupt operations without warning.

-

Currency volatility: The Korean won remains volatile despite BOK commentary about being "undervalued." EWY is USD-denominated, so won weakness benefits local earnings translation but strong dollar headwinds could persist.

-

Valuation after 105% rally: The KOSPI's P/E has expanded significantly from "Korea discount" levels. While still below US multiples, expectations are now elevated. Any growth disappointment could trigger profit-taking.

-

Geopolitical risks: North Korea tensions, US-China semiconductor cold war, and Taiwan contingency planning all create tail risks for Korean equities.

-

Theta decay on calls: These February options have 36 days to expiration. Time decay accelerates after earnings if the stock doesn't move enough. Call buyers need EWY above $118 to profit meaningfully.

The Bottom Line

Real talk: Two separate institutional traders dropped $3.3 MILLION on EWY calls today, betting that Korea's semiconductor-heavy ETF continues rallying past $115-$116 by mid-February. The timing is no accident - Samsung's full Q4 earnings release on January 29th and potential HBM4 contract announcements with Nvidia create a catalyst-rich window.

What these trades tell us:

- Smart money is ADDING to Korea exposure even after 105% 2025 gains

- They're targeting the $115-$116 zone as a breakout trigger

- February expiration captures Samsung earnings + potential HBM4 news

- The 308x Z-score on the $115 calls signals extreme conviction

- Both trades filled at ASK/MID showing urgency to get positioned

This is a bullish continuation bet, not a bottom-fishing play. The call buyers believe:

- Samsung's record earnings will exceed even the pre-announced guidance

- HBM4 contract wins will validate Korea's AI memory dominance

- The memory supercycle has legs through 2027

- Political stability and Value-Up reforms justify premium valuations

If you're bullish on AI and semiconductors:

- EWY offers concentrated exposure to the memory chip supercycle

- Consider shares for lower-risk exposure or call spreads for defined risk

- Watch for pullbacks to $110 gamma support for better entry

- Mark January 29th (Samsung earnings) as the key catalyst date

If you're cautious:

- The 105% 2025 rally creates "buy high" risk

- Wait for post-earnings clarity before committing capital

- Consider selling covered calls against existing positions

- Watch $110 support - break below signals trend change

Key dates to watch:

- January 29, 2026: Samsung Electronics full Q4 2025 earnings

- Q1 2026: HBM4 contract finalization (Samsung/SK Hynix with Nvidia)

- February 20, 2026: Monthly OPEX - expiration of these call positions

- May 2026: Korea Exchange Value-Up top performer selection

- Q3 2026: Nvidia Rubin architecture launch (HBM4 demand catalyst)

Final verdict: The $3.3M institutional call buying represents high-conviction bullish positioning ahead of a catalyst-rich February. Korea's semiconductor dominance in the AI memory supercycle is real - Samsung and SK Hynix together control 80%+ of the HBM market that's projected to reach $54.6B by 2026. The risk is that 105% 2025 gains have already captured much of the upside, and "buy the rumor, sell the news" dynamics could emerge around Samsung's earnings.

The smart money is betting this rally has more room to run. The question is whether you want to join them at these elevated levels.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. EWY's 45%+ concentration in two semiconductor companies creates significant single-sector risk. Always do your own research and consider consulting a licensed financial advisor before trading.

About iShares MSCI South Korea ETF: EWY provides exposure to South Korean equities, with heavy concentration in semiconductor manufacturers Samsung Electronics (26.12%) and SK Hynix (19.40%). The ETF has an AUM of $9.61 billion, expense ratio of 0.59%, and returned +105% in 2025 driven by the AI memory chip supercycle.