🔥 FCX Massive $4.1M Bullish Bet - Smart Money Loading Up on Copper Rally! ⛏️

📅 January 5, 2026 | 🐋 Unusual Activity Detected

🎯 The Quick Take

Someone just loaded up $4.1 MILLION worth of FCX call options this morning at 11:09! This massive bullish bet bought 7,600 contracts of $55 strike calls expiring June 18th - positioning for a breakout above current $54 levels over the next 5 months. With copper fundamentals firing on all cylinders and FCX's Grasberg mine restart coming in Q2 2026, institutional money is betting BIG that this stock pushes through $55 resistance. Translation: Smart money expects FCX to rally 15-20% by summer on copper strength and production recovery!

📊 Company Overview

Freeport-McMoRan (FCX) is the world's second-largest publicly traded copper producer with a massive global mining footprint:

- Market Cap: $74.57 Billion (metal mining giant)

- Industry: Metal Mining (copper, gold, molybdenum)

- Current Price: $53.99 (near 52-week high of $53.77)

- Primary Assets:

- 49% stake in Indonesia's Grasberg facility (world's #2 copper mine)

- 55% ownership of Peru's Cerro Verde mine

- 72% ownership of Arizona's Morenci mine (largest U.S. copper producer)

- 2024 Production: ~1.2 million metric tons of copper, 900K oz gold, 70M lbs molybdenum

- Copper Reserves: 25 years of proven reserves

FCX controls one of the world's most valuable copper mining portfolios, with the Grasberg mine containing 50% of proven reserves and ~70% of forecast production through 2029.

💰 The Option Flow Breakdown

The Tape (January 5, 2026 @ 11:09:27):

| Date | Time | Symbol | Buy/Sell | Call/Put | Expiration | Strike | Volume | Premium | Order_Type | Z_Score | Z_Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2026-01-05 | 11:09:27 | FCX | BUY | CALL $55 | 2026-06-18 | $55.00 | 7,600 | $4.1M | BTO | 10.92 | EXTREMELY_UNUSUAL |

🤓 What This Actually Means

This is a massive directional bullish bet on FCX rallying to $55+ by mid-year! Here's the breakdown:

- 💸 Huge premium paid: $4.1M ($5.39 per contract × 7,600 contracts)

- 🎯 Breakout target: $55 strike sits exactly at major gamma resistance (more on this below)

- ⏰ Strategic timing: 164 days to expiration captures Q4 earnings (Jan 28), Grasberg restart update (Q2 2026), and full copper rally cycle

- 📊 Position size: 7,600 contracts represents 760,000 shares worth ~$41M at current price

- 🏦 Institutional conviction: This is sophisticated positioning ahead of major catalysts

What's really happening here: This trader is making a leveraged bet that FCX breaks through the $55 resistance level and runs higher over the next 5 months. With the stock at $53.99, they're paying $5.39/share for the right to participate in any upside above $55. The positioning ahead of Q4 earnings (Jan 28) and the critical Grasberg restart timeline suggests they expect MAJOR positive catalysts to drive the stock 15-20% higher by summer.

Profit scenarios:

- Stock at $60 by June: Calls worth $5.00, breakeven = $5.39, LOSS of -$0.39/share (-7%)

- Stock at $65 by June: Calls worth $10.00, profit = $4.61/share × 7,600 = $3.5M gain (86% ROI!)

- Stock at $70 by June: Calls worth $15.00, profit = $9.61/share × 7,600 = $7.3M gain (178% ROI!)

- Stock below $55 by June: Calls expire worthless, total loss of $4.1M (-100%)

Breakeven price: $60.39 (11.9% above current price)

Unusual Score: 🔥 EXTREMELY UNUSUAL (10.92 Z-score) - This happens only a few times per year! The massive size (7,600 contracts) combined with the concentrated timing shows institutional conviction that hasn't been seen in FCX for months. Z-score of 10.92 means this is literally 11 standard deviations above normal FCX option activity - this is NOT retail traders, this is smart money making a major statement.

📈 Technical Setup / Chart Check-Up

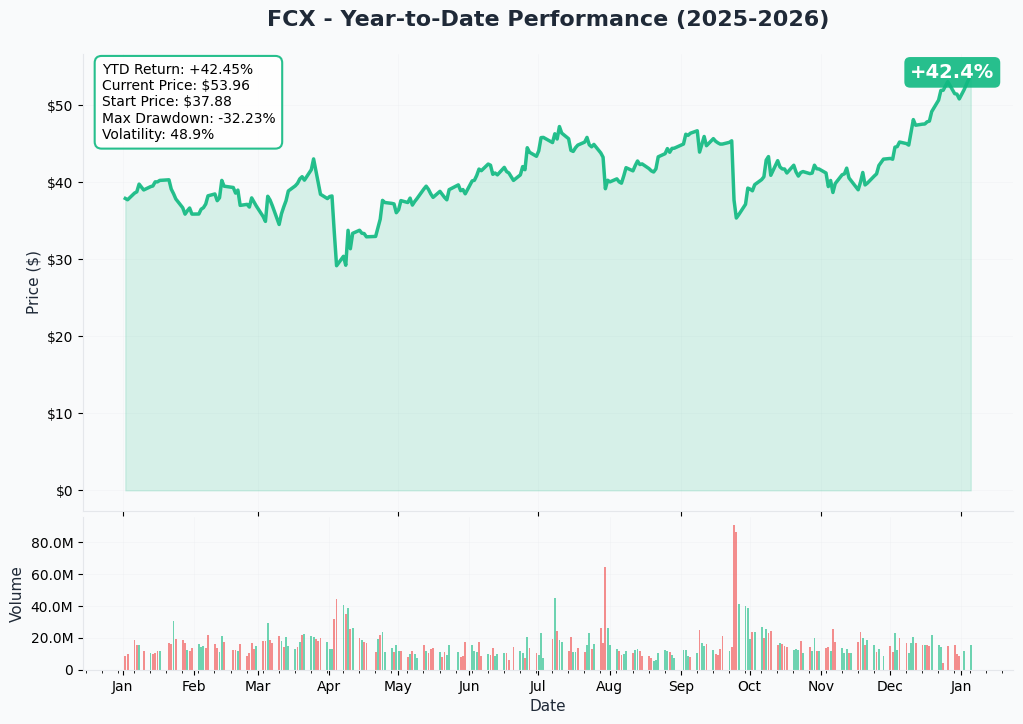

YTD Performance Chart

FCX has been on an ABSOLUTE tear - up massively from the $27.66 52-week low with current price of $53.99 approaching the all-time high of $53.77. The chart tells a powerful copper recovery story.

Key observations:

- 🚀 Strong uptrend: Steady climb from sub-$30 levels earlier in 2025 to current $54

- 📈 Breakout setup: Testing all-time highs despite Grasberg production disruption

- 💪 Momentum confirmed: Persistent buying pressure into resistance shows institutional accumulation

- 📊 Volume strength: Heavy trading volume on up days indicates conviction buying

- ⚠️ At resistance: Trading at 52-week highs - needs catalyst to break out vs. pullback risk

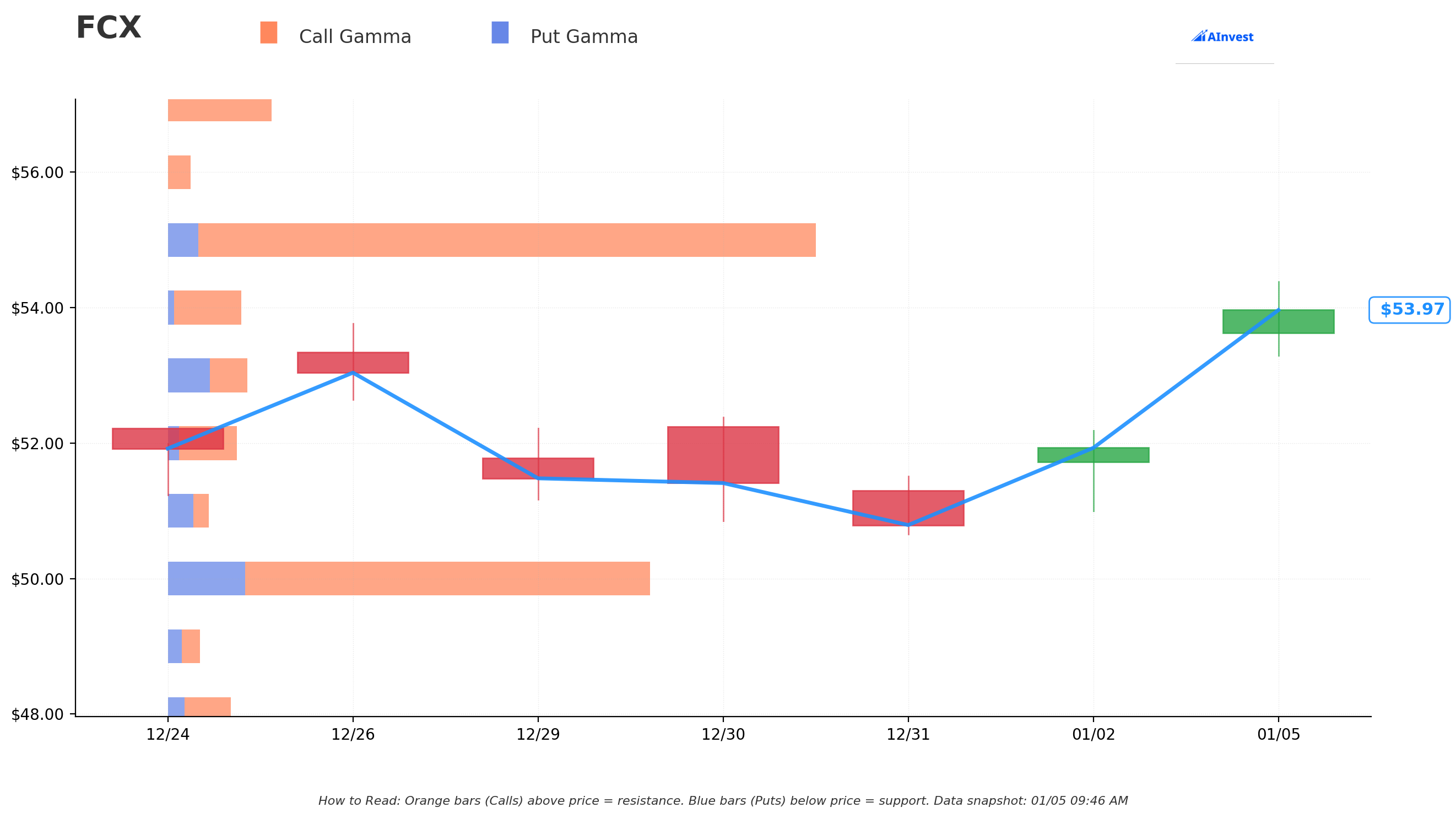

Gamma-Based Support & Resistance Analysis

Current Price: $53.99

The gamma exposure map reveals the critical price zones that will determine FCX's near-term trajectory:

🔵 Support Levels (Put Gamma Below Price):

- $53.00 - Immediate support with 4.9B total gamma exposure (holding above 2024 highs)

- $52.00 - Secondary support at 4.2B gamma (dealers defend this level)

- $50.00 - MAJOR structural floor with 28.6B gamma (STRONGEST SUPPORT - this is the LINE IN THE SAND!)

- $48.00 - Extended support at 3.0B gamma

- $47.00 - Deep support zone with 3.4B gamma

- $45.00 - Disaster floor at 7.6B gamma

🟠 Resistance Levels (Call Gamma Above Price):

- $54.00 - Immediate ceiling with 4.6B gamma (0.02% overhead - BREAKING NOW!)

- $55.00 - MASSIVE resistance with 40.0B gamma (STRONGEST LEVEL - exactly where this call trade is struck! 🎯)

- $57.00 - Secondary resistance at 6.5B gamma (5.6% above current)

- $60.00 - Extended upside target at 12.1B gamma (11.1% rally required)

What this means for traders: FCX is trading at a critical inflection point - sitting RIGHT at $54 resistance with the stock trying to break out. The gamma data shows the $55 level has ENORMOUS resistance (40.0B - by FAR the largest single level) which will create natural selling pressure. Market makers holding huge short positions at $55 will fight this level hard.

THIS IS WHY THE CALL BUYER STRUCK AT $55! They're betting that once FCX clears this massive gamma wall, there's relatively light resistance until $57-60. It's the classic "break the dam" setup - if $55 breaks, momentum could accelerate FAST to $57-60 on short covering and gamma hedging flows.

On the downside, $50 with 28.6B gamma is THE critical support - the put gamma here is massive, meaning if FCX holds above $50, the bullish structure remains intact. Below $50 and the trade thesis breaks.

Net GEX Bias: Strongly Bullish (112.2B call gamma vs 32.1B put gamma) - Massive call overweight positioning confirms institutions are positioned for upside breakout.

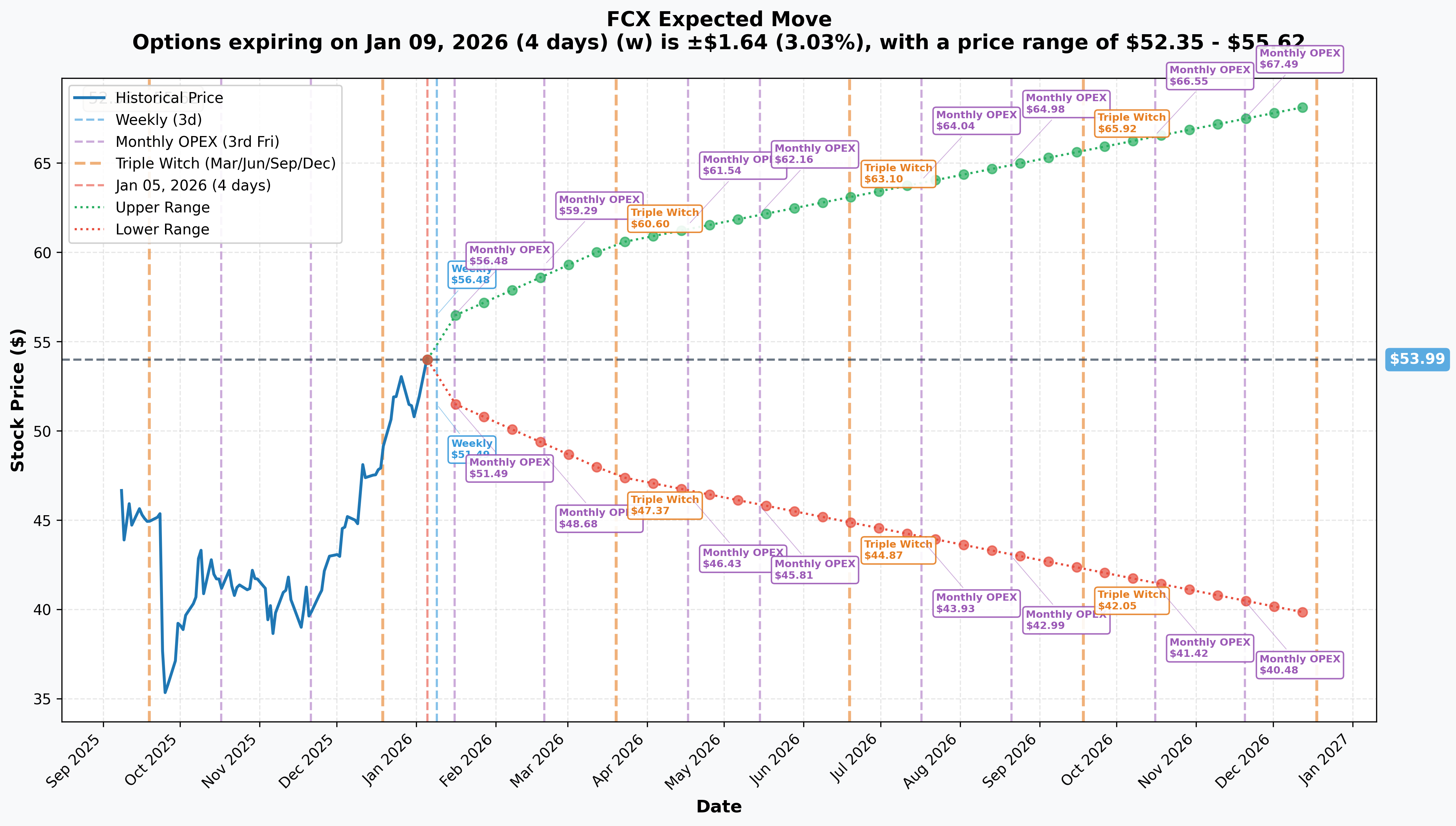

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 9 - 4 days): ±$1.64 (±3.03%) → Range: $52.35 - $55.62

- 📅 Monthly OPEX (Jan 16 - 11 days): ±$2.49 (±4.61%) → Range: $51.49 - $56.48

- 📅 Quarterly Triple Witch (Mar 20 - 74 days): ±$6.52 (±12.08%) → Range: $47.46 - $60.51

- 📅 June OPEX (Jun 19 - 165 days - THIS TRADE!): ±$8.76 (±16.2%) → Range: $45.23 - $62.75

Translation for regular folks: Options traders are pricing in a 3% move ($1.64) by Friday for weekly expiration, but a much larger 12% move ($6.52) through March quarterly OPEX which includes Q4 earnings on January 28th. The market expects significant volatility around earnings and Grasberg restart updates.

The June 18th expiration (when this $4.1M call trade expires) has an upper range of $62.75 - meaning the market thinks there's a real possibility FCX could trade as high as $62-63 over the next 5.5 months. This aligns PERFECTLY with the call buyer's thesis: catch a 15-20% rally through $55 resistance as copper fundamentals and Grasberg recovery materialize.

Key insight: The 4.61% monthly implied move through January OPEX shows earnings could be a MAJOR catalyst. If FCX delivers strong results and positive Grasberg guidance on Jan 28, the stock could easily gap 5-8% higher, pushing through the $55 resistance in one move.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Q4 2025 Earnings - January 28, 2026 (23 DAYS AWAY!) 📊

FCX reports fiscal Q4 results on Tuesday, January 28, 2026 before market open. This is THE immediate catalyst that could ignite this call position. Wall Street consensus according to TipRanks:

- 📊 Revenue: $5.16B (down from Q3's $6.97B due to Grasberg disruption)

- 💰 EPS: $0.21 consensus (reduced from prior $0.27 estimate by Raymond James)

- ⚠️ CRITICAL METRICS TO WATCH:

- Grasberg restart timeline: Any acceleration of Q2 2026 restart would be MASSIVELY bullish

- Manyar smelter progress: Target full operation December 2025, actual status?

- Americas production: U.S. operations carrying company during Grasberg outage

- 2026 full-year guidance: Market expects ~1.0-1.1B lbs copper, 0.9-1.04M oz gold

- Copper price outlook: Management commentary on $11,000+ copper prices

- Cost control: Cash costs and ability to maintain margins at higher volumes

Upside surprise potential: If FCX announces early Grasberg restart (late Q1 vs Q2) or accelerated ramp timeline, the stock could gap 10-15% overnight. Goldman Sachs notes Grasberg disruptions remove 250,000-260,000 tonnes annually - any improvement here is massive for 2026 earnings power.

Downside risk: Any delays to Grasberg restart beyond Q2 2026 or conservative 2026 production guidance would be extremely negative. BofA already downgraded to Neutral with $42 target citing "Grasberg operational challenges as material overhang."

Ex-Dividend Date - January 15, 2026 (10 DAYS!) 💰

FCX declares $0.15/share dividend with ex-dividend date January 15 and payment date February 2. While small (1.2% yield), this supports share price into mid-month.

🚀 Major Catalysts (Q1-Q2 2026) - TRADE TIMELINE

Grasberg Block Cave Restart - Q2 2026 (THE BIG ONE!) ⛏️

The September 8, 2025 mud rush incident at Grasberg resulted in force majeure and essentially ZERO Q4 2025 production (previously estimated 445M lbs copper, 345K oz gold lost). The restart timeline is THE make-or-break catalyst for FCX:

- 🏭 Remediation activities ongoing, phased restart planned for Q2 2026

- 📈 Production impact: Once restarted, Grasberg contributes ~1.6B lbs copper and 1.3M oz gold annually (MASSIVE - this is 50%+ of FCX total production!)

- ⏰ Timeline risk: Management expects full pre-incident operating rates "potentially achievable in 2027"

- 🎯 Why it matters: Early restart (April-May vs June-July) adds ~$500M-1B in additional 2026 revenue

THIS IS THE CATALYST THE CALL BUYER IS BETTING ON! June 18th expiration captures the Grasberg restart announcement and early production data. If restart happens in April-May and production ramps quickly, FCX could easily trade $58-62 by June as 2026-2027 earnings estimates get upgraded 20-30%.

Manyar Smelter Full Ramp - Q1 2026 🏭

FCX's Indonesian smelter (world's largest single-line) resumed operations June 2025 after fire repairs, targeting full operation December 2025:

- 💪 Capacity: 600,000 tons copper cathode annually

- 📊 2026 cathode output target: 450,000 metric tons

- 💰 Why it matters: Downstream processing adds higher-margin revenue and reduces shipping costs

- ⚠️ Risk: Aggressive timeline - any production issues extend Grasberg concentrate buildup

Copper Price Tailwinds - Throughout 2026 📈

The copper market setup is EXCEPTIONALLY bullish for 2026, supporting FCX's leveraged exposure:

| Institution | 2026 Target | Timing | Source |

|---|---|---|---|

| Goldman Sachs | $10,000-$11,000/ton | H1 average | Goldman Research |

| JPMorgan | $12,500/ton | Q2 2026 | JPM Outlook |

| UBS | $12,000-$13,000/ton | Q1-Q4 2026 | CNBC coverage |

| Citi | $13,000/ton | Early 2026 | CNBC coverage |

Supply-demand dynamics:

- 🚨 International Copper Study Group (ICSG) projects 150,000 tonne deficit in 2026 (reversed prior surplus forecast)

- 📉 JPMorgan sees 330,000 tonne deficit with tight market into 2026

- 🏭 Deutsche Bank: Global mine supply -3% in 2025, +1% in 2026 (still below 2024)

- 🤖 AI demand explosion: Hyperscale data centers require 50,000 tons copper each, 2026 data center demand ~475,000 tonnes

- ⚡ EV adoption: EVs contain 4x more copper than conventional vehicles, demand doubling by 2035

Every $1,000/ton increase in copper price = ~$0.50-0.70/share higher EPS for FCX. If copper hits UBS/Citi targets of $12,500-13,000 by mid-year, FCX's 2026 EPS could easily exceed $4.00 (vs current $2.00-2.50 estimates), justifying a stock price of $60-70.

U.S. Copper Tariff Update - June 30, 2026 🇺🇸

Presidential action in August 2025 implemented 50% tariffs on copper semi-finished imports, with Commerce Secretary providing update by June 30, 2026:

- 💰 Potential additional tariffs: 15% on refined copper starting January 1, 2027

- 🏭 Domestic production requirements increasing through 2029

- 🎯 FCX benefit: U.S. operations (Morenci, Bagdad, Sierrita, Chino, Tyrone) protected from foreign competition

- 📈 Pricing power: Tariffs support domestic copper premium, improving FCX margins

This June timing aligns PERFECTLY with the call expiration! Any announcement of additional tariff protection or domestic production incentives would be bullish for FCX's U.S. operations.

⚠️ Risk Catalysts (Negative)

Grasberg Restart Delays 🚨

Timeline for Q2 2026 restart remains uncertain - investigation ongoing. The mud rush incident was unprecedented with 800,000 metric tons of material involved:

- ⏰ Any delay from Q2 to Q3/Q4 2026 would crater stock 15-20%

- 🔬 Post-incident safety protocols may slow ramp even after restart

- 🇮🇩 Indonesian government/regulatory approval required - could face delays

China Demand Weakness 🇨🇳

China consumes 60% of global refined copper, but property sector remains weak:

- 📉 Q4 2025 demand soft (-8% YoY) as stimulus effects wane

- 🏗️ Real estate construction (historically 30% of copper demand) still depressed

- 💸 If China stimulus disappoints or property weakness accelerates, copper demand could fall 5-10%

- ⚠️ FCX has minimal direct China revenue but copper prices would suffer

Competitive Supply Additions 📊

New supply could ease tight market:

- 🏭 Rio Tinto's Oyu Tolgoi expansion in Mongolia ramping up

- 🌍 Other producers increasing output to capitalize on high prices

- ♻️ 50% tariff exemption for scrap could increase recycled supply

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through June 18th expiration:

📈 Bull Case (40% probability)

Target: $60-$65

How we get there:

- 💪 Q4 earnings show better-than-feared results despite Grasberg outage (Americas operations crushing it)

- 🚀 GRASBERG RESTART ACCELERATED: Management announces late-Q1 or early-April restart vs June expectations

- 🤖 Copper prices rally to $12,000-12,500/ton on supply deficit and AI demand (JPM/UBS targets)

- 📊 2026 guidance surprises to upside once Grasberg timeline clarifies (~1.2-1.3B lbs vs 1.0-1.1B consensus)

- 🏭 Manyar smelter ramps smoothly to full capacity, validating downstream strategy

- 🇺🇸 June tariff update announces additional protections for domestic producers

- 📈 Break above $55 gamma resistance triggers momentum rally to $57, then $60 on short covering

Key metrics needed:

- Grasberg restart timeline pulled forward 4-8 weeks

- Copper sustained above $11,500/ton

- 2026 EPS estimates revised from $2.50 to $3.50+ on volume recovery

- Analyst upgrades from current $49-51 consensus PT to $60+ range

Call P&L in Bull Case:

- Stock at $60: Calls worth $5.00, LOSS of -$390K (-9%)

- Stock at $62: Calls worth $7.00, PROFIT of $1.2M (+30%)

- Stock at $65: Calls worth $10.00, PROFIT of $3.5M (+86%!)

Probability assessment: 40% because multiple catalysts aligned favorably. Grasberg restart is probable in Q2 (management committed), copper fundamentals genuinely strong (supply deficit real), and FCX has strong execution track record. The $55 resistance is tough but breakable on major positive news.

🎯 Base Case (35% probability)

Target: $52-$58 range (CHOPPY CONSOLIDATION)

Most likely scenario:

- ✅ Solid Q4 earnings meeting lowered expectations (~$5.2B revenue, $0.22-0.25 EPS)

- 📱 Grasberg restart timeline CONFIRMED for Q2 2026 but not accelerated (May-June window)

- ⚖️ 2026 guidance in-line with consensus (1.0-1.1B lbs copper) - cautious due to ramp uncertainty

- 🤖 Copper prices range-bound $10,500-12,000/ton - supportive but not explosive

- 🏭 Manyar smelter progressing steadily without major issues or surprises

- 🔄 Stock trades between $52 support and $55-57 resistance for months

- 📊 Market adopts "wait and see" stance until actual Grasberg restart data (late Q2)

- 💤 Consolidation pattern as earlier rally from $40s to $50s gets digested

This scenario sees the calls struggling: Stock can't decisively break $55 resistance without Grasberg actually producing. Calls lose time value (theta decay) and expire worthless or minimal value unless late rally materializes.

Call P&L in Base Case:

- Stock at $54 on June 18: Calls expire worthless, LOSS of -$4.1M (-100%)

- Stock at $57 on June 18: Calls worth $2.00, LOSS of -$2.6M (-63%)

Why 35% probability: This is the "everything goes according to plan but no positive surprises" scenario. Grasberg restarts on schedule but not early, copper stays elevated but doesn't spike, earnings meet reduced expectations. Market wants to see PROOF of production recovery before paying $60+.

📉 Bear Case (25% probability)

Target: $45-$50

What could go wrong:

- 😰 Q4 earnings worse than feared - costs elevated, Americas production disappoints

- 🚨 GRASBERG RESTART DELAYED: Timeline pushed to Q3 2026 or later due to technical/regulatory issues

- ⏰ Investigation findings reveal structural issues requiring extensive remediation

- 🇨🇳 Copper prices fall to $9,500-10,500 on China demand disappointment or global recession fears

- 💸 Manyar smelter encounters production problems, can't absorb concentrate buildup

- 📊 2026 guidance slashed to <1.0B lbs copper due to extended Grasberg outage

- 🌍 Global industrial recession emerges, crushing copper demand

- 💰 Break below $50 major gamma support triggers cascade to $47-45

- 🇮🇩 Indonesian government/regulatory complications delay restart indefinitely

Critical support levels:

- 🛡️ $52-53: Immediate floor - must hold or momentum shifts negative

- 🛡️ $50: MAJOR gamma floor (28.6B) - break here would be devastating for bulls

- 🛡️ $47-48: Deep support zone - disaster scenario

Call P&L in Bear Case:

- Stock anywhere below $55 on June 18: Calls expire worthless, TOTAL LOSS of -$4.1M (-100%)

Probability assessment: 25% because it requires multiple negative catalysts. FCX management has strong track record and Grasberg restart is highly likely given 2+ quarters of remediation time. However, execution risk is REAL - mining is unpredictable and delays happen. The BofA downgrade to $42 target shows smart analysts see material downside if Grasberg timeline slips.

💡 Trading Ideas

🛡️ Conservative: Wait for Earnings Clarity

Play: Stay on sidelines until after January 28th earnings volatility clears

Why this works:

- ⏰ Earnings in 23 days creates binary risk with Grasberg restart timeline as key focus

- 💸 Stock at 52-week highs with limited upside before Grasberg actually restarts

- 📊 Better entry likely post-earnings if stock pulls back to $50-52 on cautious guidance

- 🤔 The $4.1M institutional call buy shows conviction, but professional traders have different risk tolerance than retail

- ⚠️ Mining stocks notoriously volatile - FCX can easily swing 10-15% on operational news

Action plan:

- 👀 Watch January 28 earnings for: (1) Grasberg restart timeline specificity, (2) 2026 production guidance, (3) cost control commentary

- 🎯 Look for pullback to $50-51 post-earnings for stock entry with better risk/reward

- ✅ Need to see Grasberg restart timeline CONFIRMED (not delayed) before committing capital

- 📊 Monitor copper prices - sustained move above $11,500 would be bullish confirmation

- ⏰ Revisit in April-May when Grasberg restart approaches for next leg higher

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential -10-15% drawdown if Grasberg timeline disappoints. Get better entry if stock consolidates below $52. Maintain optionality to buy the actual restart news.

⚖️ Balanced: Post-Earnings Call Spread (Defined Risk Upside)

Play: After earnings, buy call spread targeting $55-60 breakout

Structure: Buy $55 calls, Sell $60 calls (June 18 expiration - SAME as the $4.1M trade)

Why this works:

- 🎢 Post-earnings clarity on Grasberg reduces uncertainty premium

- 📊 Defined risk spread ($5 wide = $500 max risk per spread)

- 🎯 Targets exact gamma breakout levels ($55 resistance → $60 measured move)

- 🤝 "Copies" institutional positioning at better risk/reward (spread vs naked calls)

- ⏰ 4-5 months to expiration gives time for Grasberg restart and copper rally to materialize

- 🛡️ Selling $60 call reduces cost and defines max profit - more conservative than naked calls

Estimated P&L (will depend on post-earnings prices):

- 💰 Pay ~$2.00-2.50 net debit per spread (vs $5.39 for naked calls)

- 📈 Max profit: $2.50-3.00 if FCX above $60 at June expiration (100-120% ROI!)

- 📉 Max loss: $2.00-2.50 if FCX below $55 (defined and limited -100%)

- 🎯 Breakeven: ~$57.00-57.50

- 📊 Risk/Reward: ~1:1 which is excellent for directional commodity play

Entry timing:

- ⏰ Enter 2-3 days post-earnings (by Jan 30-31) after initial volatility settles

- 🎯 Only enter if Grasberg timeline confirmed for Q2 2026 (not delayed)

- ✅ Want to see stock holding above $52 support (shows institutional support intact)

- ❌ Skip if Grasberg restart pushed to Q3+ or stock breaks below $50

Position sizing: Risk 3-5% of portfolio per spread (directional speculation on commodity recovery)

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

🚀 Aggressive: Copy the Whale - Buy June $55 Calls (ADVANCED!)

Play: Directly replicate institutional positioning with naked long calls

Structure: Buy $55 calls (June 18 expiration)

Why this could work:

- 💥 EXACT same trade as the $4.1M institutional buyer - they clearly see value here

- 🎰 Maximum leverage to Grasberg restart and copper rally - no upside cap

- 📊 If FCX breaks $55 and runs to $60-65, returns could be 100-200%+

- 🚀 Gamma resistance at $55 creates explosive potential once broken (dealers forced to buy on breakout)

- ⚡ Strike positioned at key technical level - either it works big or doesn't work at all

- 🎯 5.5 months gives ample time for multiple catalyst plays (earnings, restart, copper rally, tariff update)

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Calls currently ~$5.39 ($539 per contract, $5,390 for 10 contracts)

- ⏰ TIME DECAY KILLER: Theta burns -$15-25/day per contract as expiration approaches

- 😱 BINARY RISK: If Grasberg delayed or copper weakens, calls could lose 50-100% value

- 📊 Breakeven at $60.39: Need 11.9% rally just to break even - stock must actually break out, not just hold

- 🎢 Need stock above $60 to profit, above $65 for strong returns

- ⚠️ Mining operational risk - one bad Grasberg update and calls crash 30-50% overnight

Estimated P&L:

- 💰 Cost: ~$5.00-5.50 per call (will vary based on entry timing)

- 📈 Profit scenario: Stock rallies to $63-65 = $8-10 gain (150-180% ROI!)

- 🚀 Home run: Stock rallies to $70 on Grasberg success = $15 gain (270% ROI!)

- 📉 Loss scenario: Stock stays $52-54 range = -50-70% loss as time decay erodes value

- 💀 Total loss: Stock below $55 at expiration = lose entire premium (-100%)

Breakeven: $60-61 depending on entry price

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand options can expire worthless - only risk capital you can afford to LOSE

- ✅ Have conviction on Grasberg restart timeline (this is THE key variable)

- ✅ Believe copper prices headed to $12,000+ (fundamental view required)

- ✅ Can handle 30-50% drawdowns without panic selling (mining stocks volatile!)

- ✅ Plan to actively manage position - take profits if stock hits $60-62, cut losses if Grasberg timeline worsens

- ⏰ Will monitor position monthly and roll/close if thesis changes

Position sizing: Risk NO MORE than 2-3% of total portfolio (this is speculative, not core holding)

Risk level: EXTREME (can lose 100% of premium) | Skill level: Advanced only

Probability of profit: ~35-40% (requires breakout above $60 which needs multiple positive catalysts)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Grasberg restart uncertainty remains THE key risk: Despite Q2 2026 target, the September 8, 2025 mud rush incident was unprecedented involving 800,000 metric tons of material with 2 fatalities and 5 missing workers. Investigation ongoing - any findings requiring extensive remediation could delay restart to Q3/Q4 2026 or beyond. Every month of delay = ~$300-400M lost revenue. BofA specifically cited "Grasberg operational challenges as material overhang to at least early 2026" when downgrading to Neutral with $42 target (22% below current price).

-

🇨🇳 China property sector weakness threatens copper demand: China consumes 60% of global refined copper, with real estate construction historically 30% of that demand. Property sector remains depressed despite stimulus efforts. Q4 2025 demand already soft (-8% YoY) as stimulus effects faded. If China property deteriorates further or stimulus disappoints in 2026, copper demand could fall 5-10%, pressuring prices below $10,000/ton and crushing FCX's 2026 estimates regardless of Grasberg restart success.

-

💰 Valuation at 36.5x P/E offers no margin of safety: FCX trading at elevated 36.5x P/E ratio (vs historical 12-18x) after rally from $27 to $54 (+100% from lows). Current valuation REQUIRES successful Grasberg restart + elevated copper prices ($11,000+) to justify. Stock is priced for perfection - any disappointment magnified. Near 52-week high of $53.77 with limited upside buffer before earnings/operational clarity.

-

🏭 Manyar smelter ramp-up execution risk: 600,000 ton/year facility resumed operations June 2025 after fire repairs, targeting full capacity December 2025. 2026 cathode output target of 450,000 metric tons is aggressive. Any technical issues, production shortfalls, or quality problems would compound Grasberg outage impact. Smelter performance critical for processing concentrate buildup once mine restarts.

-

📊 Copper price assumptions may be too optimistic: While major banks project $12,000-13,000/ton, Goldman Sachs expects prices to "decline somewhat from record highs in 2026" with H1 2026 average only $10,000-11,000. If recession emerges or China stimulus fails, copper could fall to $9,500-10,000 range. Every $1,000 drop = ~$0.50-0.70/share lower EPS for FCX. At $9,500 copper, FCX 2026 EPS might be only $1.50-2.00 (vs $2.50-3.00 needed to justify current price).

-

🌍 Competitive supply additions could ease deficit: New production from Rio Tinto's Oyu Tolgoi expansion, increased recycling (scrap tariff exemption), and other producers ramping output to capitalize on high prices could flip supply deficit to surplus by H2 2026. Deutsche Bank expects global mine supply +1% in 2026 - if demand disappoints simultaneously, market could be oversupplied.

-

🇮🇩 Indonesian regulatory/political risk: PTFI operations subject to Indonesian government policies, licensing, and relations. Grasberg contains 50% of FCX proven reserves - any adverse regulatory changes, tax increases, or nationalization pressure would devastate stock. Government could use restart approval as leverage for concessions.

-

⚖️ $55 gamma wall extremely difficult to break: With 40.0B call gamma at $55 (by FAR the largest level), market makers holding massive short positions will fight this resistance aggressively. Would need sustained institutional buying + major positive catalyst (Grasberg early restart) to overcome mechanical selling pressure. Stock has tried to break $54-55 multiple times in 2025 and failed - what makes this time different?

-

📉 Mining operational risks always present: FCX operates in politically unstable regions (Indonesia, Peru, Democratic Republic of Congo), faces environmental challenges, labor issues, and geological surprises. One major accident, environmental incident, or operational disruption at Americas operations (currently carrying company) would compound Grasberg problems. Track record includes Grasberg mud rush (2025), Manyar smelter fire (2024), various labor strikes - operational excellence not guaranteed.

-

🎢 Commodity stocks extraordinarily volatile: FCX swings wildly on copper price movements and operational news. 52-week range of $27.66-$53.77 (95% range!) shows how fast sentiment can shift. Recent rally from $40s to $50s could easily reverse 15-20% on one bad Grasberg update. Options positioned at $55 require stock to hold gains AND break higher - vulnerable to profit-taking.

-

💸 Options theta decay accelerates: With 164 days to expiration, these calls lose ~$25-35/day in time value as expiration approaches. If stock consolidates $52-55 range for 2-3 months while waiting for Grasberg restart, calls could lose 30-40% value from theta alone even if stock doesn't drop. Unlike stock, options are wasting assets.

🎯 The Bottom Line

Real talk: Someone just committed $4.1 MILLION to betting that FCX breaks through $55 resistance and rallies to $60-65+ by mid-year. This isn't a hedge or complex spread - this is a leveraged BULLISH bet that requires the stock to actually perform.

What this trade tells us:

- 🎯 Institutional conviction that Grasberg restart happens on schedule (Q2 2026) and ramps successfully

- 💰 Belief that copper prices rally to $12,000+ zone on supply deficits and AI demand

- ⚖️ Willingness to risk $4.1M on $55 breakout - they see limited downside risk from current $54 levels

- 📊 Positioned EXACTLY at major gamma resistance ($55 with 40.0B gamma) - betting on breakout cascade to $57-60

- ⏰ June 18th expiration captures ALL key catalysts: Q4 earnings, Grasberg restart, copper rally, tariff update

This is NOT a "buy FCX at any price" signal - it's a "major positive inflection coming in Q1-Q2 2026" signal.

The bull case is genuinely compelling:

- ✅ Grasberg restart in Q2 adds ~1.6B lbs copper + 1.3M oz gold (50%+ production increase!)

- ✅ Copper supply deficit of 150,000-330,000 tonnes projected for 2026 by multiple banks

- ✅ AI data center demand adding 110,000 tonnes in 2026, accelerating to 1.1M tonnes by 2030

- ✅ U.S. tariff protection (50% on semi-finished, potential 15% on refined) benefits domestic operations

- ✅ Strong balance sheet ($4.3B cash, $3B credit facility) to weather extended Grasberg recovery

- ✅ Analyst consensus $49-51 price targets conservative if Grasberg restarts on time

But the execution risks are REAL:

- ⚠️ Grasberg timeline still uncertain - delays to Q3/Q4 would be catastrophic

- ⚠️ China demand critical (60% of copper) - property weakness threatens downside

- ⚠️ Trading at 36.5x P/E near 52-week highs - priced for perfection

- ⚠️ BofA analyst with $42 target (22% downside) sees material overhang

If you own FCX:

- ✅ Hold through earnings if you believe in Grasberg restart story - upside to $60-65 is real

- 📊 Set MENTAL STOP at $50 (major gamma support) to protect if Grasberg timeline deteriorates

- ⏰ Pay close attention to January 28 earnings - need specificity on restart timeline (not vague Q2 guidance)

- 🎯 If stock breaks $55 decisively post-earnings, could run to $57-60 quickly on short covering

- 🛡️ Consider trimming 25-30% at $56-58 if you get the breakout to lock in gains

If you're watching from sidelines:

- ⏰ January 28th earnings is the key catalyst - don't enter before this!

- 🎯 Looking for confirmation of: Grasberg Q2 restart (April-May specificity preferred), 2026 guidance 1.1B+ lbs copper, cost control maintained

- 📈 Post-earnings pullback to $50-52 would be excellent risk/reward entry for stock or call spreads

- 🚀 If you're aggressive and believe Grasberg story, $55 June calls after earnings could offer leveraged upside (but understand 100% loss risk!)

- ⚠️ Current $54 levels offer poor risk/reward - need either pullback for safety or breakout confirmation for momentum

If you're bearish:

- 🎯 Don't fight the tape at $54 - wait for failed breakout above $55 or negative Grasberg news

- 📊 Key resistance at $55 (40.0B gamma) - if stock stalls here after earnings, could be good short entry

- ⚠️ Selling put spreads ($50/$45) post-earnings offers defined-risk way to play consolidation/decline

- 📉 Watch for break below $50 major support - that's the trigger for cascade to $47-45

- ⏰ Patience required - let Grasberg timeline play out before aggressive bearish positioning

Mark your calendar - Key dates:

- 📅 January 15 (Wednesday) - Ex-dividend date ($0.15/share)

- 📅 January 28 (Tuesday) before market open - Q4 2025 earnings report (23 DAYS!)

- 📅 February 2 (Sunday) - Dividend payment date

- 📅 April-June 2026 - Grasberg Block Cave restart expected

- 📅 June 18, 2026 - Expiration of this $4.1M call trade

- 📅 June 30, 2026 - Commerce Department copper tariff update

Final verdict: FCX's setup is a classic "high risk, high reward" commodity play. IF Grasberg restarts on schedule in Q2 AND copper prices rally to $12,000+ on supply deficits, the stock could easily trade $60-70 by summer (20-30% upside). But IF Grasberg delays to Q3/Q4 OR copper weakens on China demand disappointment, the stock could revisit $45-48 levels (15-20% downside).

The $4.1M institutional call buyer clearly believes the odds favor the bull case - but they can afford to lose $4.1M. Can you?

Be smart. Wait for earnings. Let Grasberg timeline clarify. If you chase at $54 and it doesn't work, you'll regret not waiting for $50-52 entry. If it breaks out to $58-60 without you, there will be other trades. Capital preservation comes first. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The 10.92 Z-score reflects this specific trade's size relative to recent FCX history - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Mining operations involve significant operational, geological, political, and commodity price risks. Grasberg restart timeline remains uncertain and subject to regulatory approval. The call buyer may have complex portfolio positioning or hedging needs not applicable to retail traders.

About Freeport-McMoRan Inc.: Freeport-McMoRan operates a major global portfolio of copper mining assets including 49% stake in Indonesia's Grasberg facility (world's #2 copper mine), 55% ownership of Peru's Cerro Verde, and 72% ownership of Arizona's Morenci mine. In 2024, the company sold around 1.2 million metric tons of copper and 900,000 ounces of gold, with market cap of $74.57 billion in the Metal Mining industry.