💎 FIVE $1.9M Call Spread - Betting on Teen Retail Turnaround! 🛡️

📅 December 2, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Smart money just locked in a $1.9 MILLION bet that Five Below rallies 25%+ by mid-January! At 11:15:05 this morning, a sophisticated trader executed a massive call spread - buying 1,250 contracts of the $165 calls for $1.4M while simultaneously selling 2,500 of the $200 calls for $500K. Net cost: $900K for a defined-risk bullish play on the teen retailer's turnaround under new CEO Winnie Park. This isn't some speculative YOLO - this is a structured bet that FIVE breaks out from its current $160.86 price to $165+ by January 16th.

📊 Company Overview

Five Below (FIVE) is a high-growth specialty value retailer targeting the tween and teen demographic:

- Market Cap: $8.92 Billion

- Industry: Retail - Variety Stores

- Current Price: $160.86

- Store Count: 1,800+ locations across 46 states (expanding to 3,500+ by 2030)

- Primary Business: Curated merchandise priced at $1-$5+ targeting Gen Z shoppers (think treasure hunt meets dollar store meets cool)

- Employees: 23,200

Five Below is like if a dollar store had a baby with Hot Topic - trendy products for teens at unbeatable prices. They're growing FAST with 150 new stores planned this year alone.

💰 The Option Flow Breakdown

The Tape (December 2, 2025 @ 11:15:05):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:15:05 | FIVE | BID | BUY | CALL $165 | 2026-01-16 | $1.4M | $165 | 1,300 | 96 | 1,250 | $160.86 | $10.80 | FIVE 165C 01/16 |

| 11:15:05 | FIVE | ASK | SELL | CALL $200 | 2026-01-16 | $500K | $200 | 2,500 | 1,100 | 2,500 | $160.86 | $2.00 | FIVE 200C 01/16 |

🤓 What This Actually Means

This is a bullish call spread with a twist - it's structured 2:1 (selling 2x the contracts they bought). Here's the breakdown:

- 💸 Net Investment: $900K ($1.4M paid - $500K collected)

- 🎯 Profit Zone: Stock needs to hit $165-$200 range (2.6% to 24.3% upside from $160.86)

- ⏰ Time Frame: 45 days to January 16th expiration

- 📊 Max Profit Scenario: Stock rallies to exactly $200 = enormous profit (we'll calculate below)

- 🛡️ Risk Management: Defined risk structure, not naked calls

- 🏦 Sophisticated Positioning: This is NOT a beginner trade - ratio spread requires active management

What's really happening here: This trader is making a SPECIFIC bet on Five Below's price trajectory. They expect:

- Stock breaks above $165 in next 45 days (triggering profit on long calls)

- Stock stays BELOW $200 by January 16th (short calls expire worthless or minimal value)

- Sweet spot is anywhere from $175-$195 where long calls are deep in-the-money but short calls still out-of-the-money

Why the 2:1 ratio? By selling 2,500 contracts against 1,250 longs, they're reducing net cost from $1.4M to $900K BUT capping max upside if stock explodes past $200. This structure says: "I'm bullish but want to finance the trade and don't think we're going to $250 in 45 days."

Unusual Score: 🔥 EXTREMELY UNUSUAL - The $165 calls show 75x average size (Z-score of 74.92) and the $200 calls are 437x average size (Z-score of 436.37). This happens a few times a year for FIVE. Combined $1.9M notional across both legs makes this one of the largest single option plays in FIVE's recent history.

The Timing Factor: Positioned AFTER the stock's huge YTD recovery but BEFORE critical Q2 earnings in late August 2025. This trader believes new CEO Winnie Park's turnaround initiatives (launched December 2024) are gaining traction and will show up in upcoming results.

📈 Technical Setup / Chart Check-Up

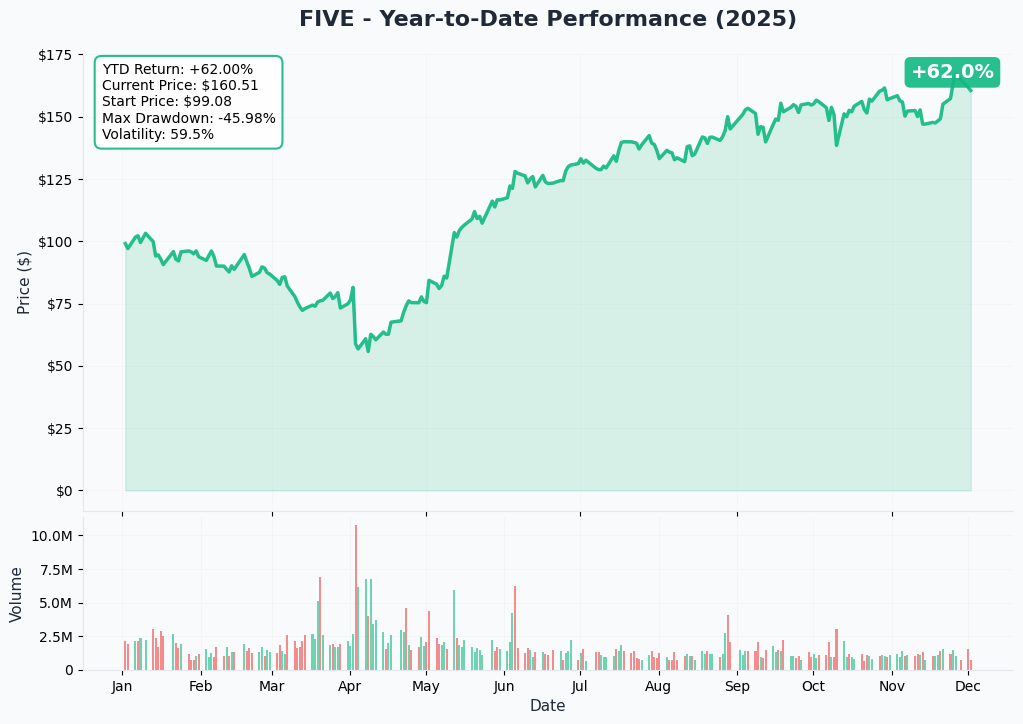

YTD Performance Chart

FIVE has had a WILD ride - the stock crashed 40%+ over the 12 months prior to this year, bottoming around $72-76 in spring 2025 during the multi-quarter comp sales decline. But then came the REVERSAL: new CEO Winnie Park took over in December 2024, and Q1 FY2025 results in June absolutely CRUSHED it with +19.5% revenue growth and +7.1% comp sales (vs guidance for flat to +2%!).

Key observations:

- 🚀 Massive recovery rally: From $72 lows to current $160.86 = 123% gain off bottom

- 📈 Turnaround confirmed: Q1 earnings beat reversed three straight quarters of negative comps

- 🎢 High volatility: This isn't stable blue-chip - FIVE moves FAST on news

- 📊 Critical level: Trading near recent resistance around $160-165 zone

- ⚠️ Make or break zone: Stock needs to break $165 convincingly to resume rally toward $180-200

The chart shows FIVE is at a technical inflection point - either breaks out above $165 resistance and runs to $180-200, OR fails here and pulls back to $140-150 support. The call spread buyer is clearly betting on the BREAKOUT scenario.

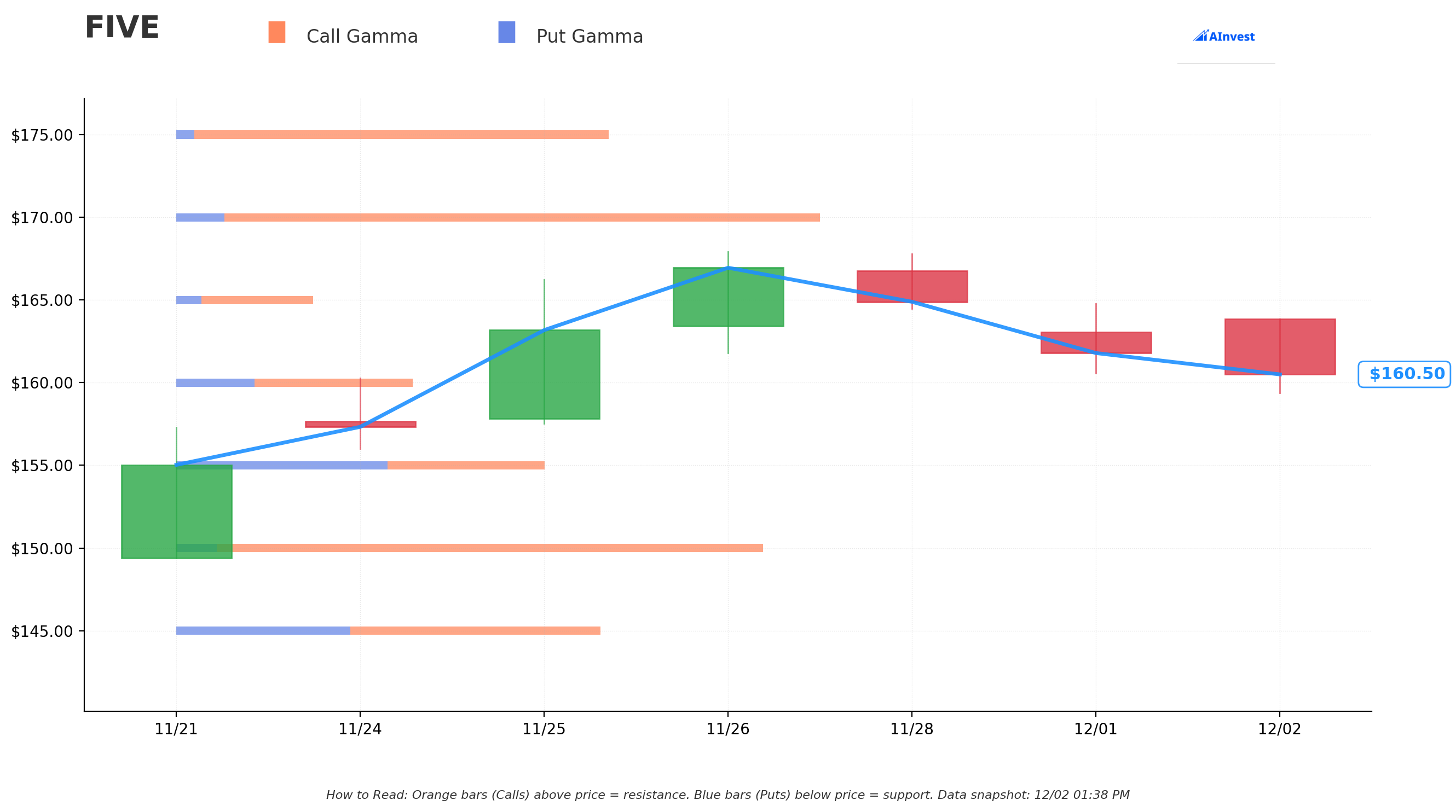

Gamma-Based Support & Resistance Analysis

Current Price: $160.51

The gamma exposure map shows where options dealers are positioned and where price will find natural magnets:

🔵 Support Levels (Put Gamma Below Price):

- $160 - Immediate support with 0.19B total gamma (0.06B net GEX - modest floor)

- $155 - Secondary support at 0.30B gamma (actually BEARISH net -0.04B GEX from put dominance)

- $150 - Major structural floor with 0.47B gamma (0.41B net GEX - STRONGEST PUT GAMMA support!)

- $145 - Deep support at 0.34B gamma (dealers will defend this level)

- $130 - Extended disaster floor at 0.18B gamma

🟠 Resistance Levels (Call Gamma Above Price):

- $165 - IMMEDIATE CEILING with 0.11B gamma (0.07B net GEX - THIS IS THE BREAKOUT LEVEL! Where the call spread is struck!)

- $170 - Major resistance zone with 0.52B gamma (0.44B net GEX - MASSIVE barrier at +5.9% above current)

- $175 - Secondary ceiling at 0.35B gamma (dealers will sell rallies aggressively)

- $180 - Extended resistance at 0.26B gamma

- $185 - Upper target zone at 0.13B gamma

What this means for traders: FIVE is trading JUST BELOW the critical $165 breakout level where there's significant call gamma. The option flow we're tracking is positioned EXACTLY at this technical inflection point. If stock breaks above $165, next stop is $170 where there's MASSIVE 0.52B gamma resistance (the biggest call gamma level on the board).

Notice the setup? The trader bought $165 calls right at resistance, betting on breakout, then sold $200 calls WAY above all meaningful resistance zones. The $170 gamma wall at 0.52B is THE key level - if FIVE clears that, path to $185-200 opens up.

Downside protection comes at $150 (0.47B gamma - strongest support level). If FIVE breaks below $150, could flush quickly to $145 or even $130.

Net GEX Bias: Bullish (2.79B call gamma vs 0.81B put gamma = 3.4:1 ratio) - Overall market positioning leans bullish, which supports the call spread thesis.

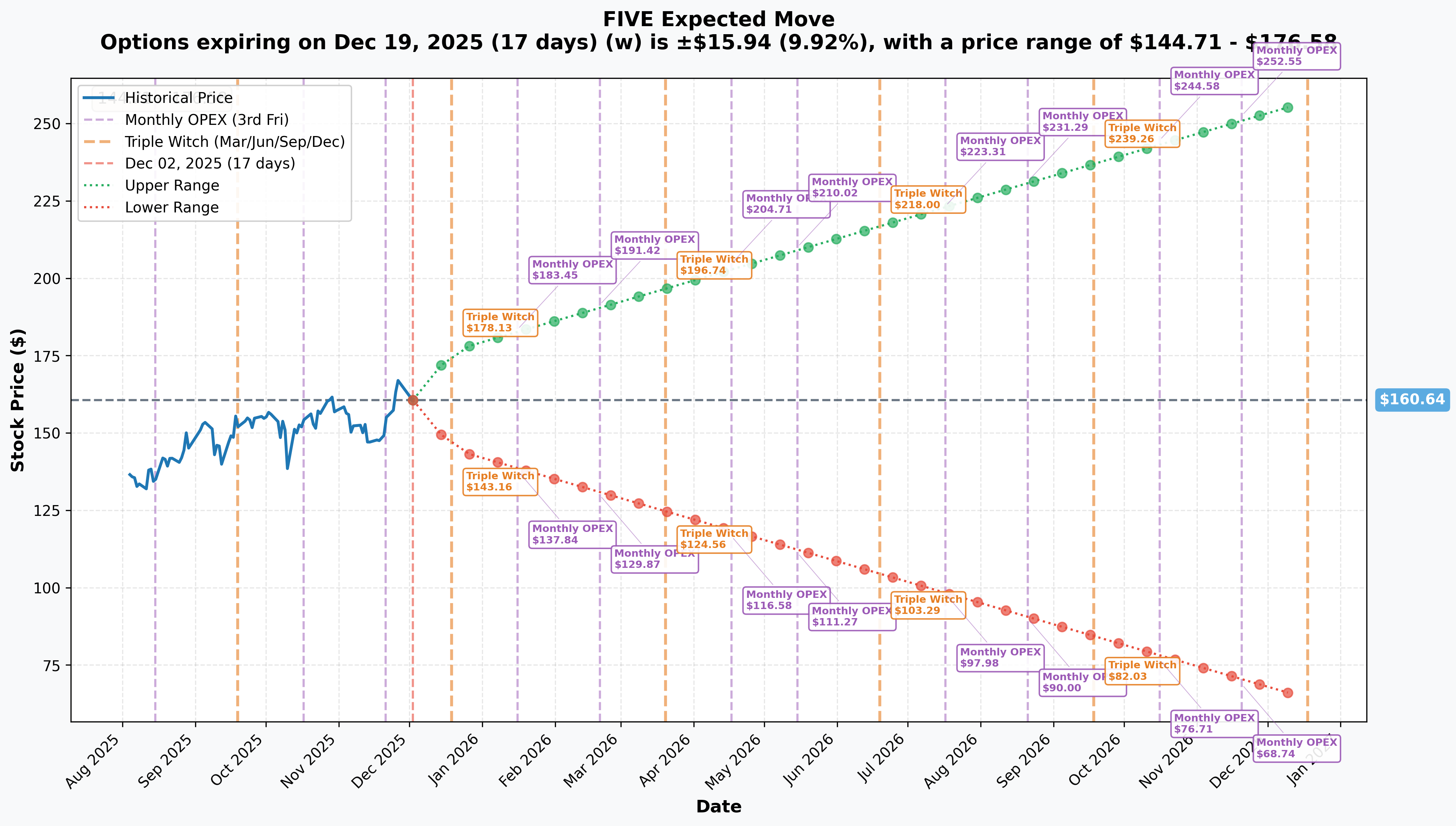

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 December 19 (17 days - Triple Witch): ±$15.94 (±9.92%) → Range: $144.71 - $176.58

- 📅 January 16 (45 days - THIS TRADE!): ±$22.81 (±14.2%) → Range: $137.84 - $183.45

- 📅 February 20 (80 days): ±$31.43 (±19.6%) → Range: $129.87 - $191.42

- 📅 LEAPS (December 2026 - 381 days): ±$96.56 (±60.1%) → Range: $64.09 - $257.20

Translation for regular folks: Options traders are pricing in a 10% move ($16) by December 19th and a 14% move ($23) by January 16th when this spread expires. The January expiration upper range of $183.45 is VERY close to our $180-185 resistance zone from gamma analysis.

This is IMPORTANT: The market thinks there's a realistic chance FIVE trades between $137-183 by January 16th. Our call spread is profitable anywhere from $165-$200, which sits RIGHT IN THE MIDDLE of this expected range ($165 = +2.6%, $183 = +13.8%).

Key insight: The trader is positioning for a move WITHIN the expected range - not betting on some crazy outlier scenario. They're saying "I think FIVE rallies 5-15% to $170-185 zone, NOT 25%+ to $200." The short $200 calls finance the trade and reflect realistic upside expectations.

🎪 Catalysts

🔥 Already Happened (Bullish Momentum Built)

Q1 Fiscal 2025 Blowout Results - June 4, 2025 📊

Five Below's most recent earnings absolutely CRUSHED expectations, validating the new CEO's turnaround:

- 📊 Revenue: $970.5M (up 19.5% YoY) - beat estimates by 0.31%

- 💰 EPS: $0.86 adjusted (vs guidance of $0.50-$0.61) - MASSIVE beat!

- 🏪 Comp Sales: +7.1% (vs initial guidance of flat to +2%) - this is the KEY metric that was broken for 3 quarters

- 🚀 Store Expansion: Opened 50 new stores in Q1, ended with 1,821 total

- 📈 Guidance Raised: Full year adjusted EPS raised to $4.25-$4.72 range

Why this matters for the trade: This established PROOF that the turnaround is real, not hopium. Comp sales going from -3% in Q4 FY2024 to +7.1% in Q1 FY2025 is a complete narrative shift.

New CEO Taking Charge - Winnie Park (December 2024) 🤝

Winnie Park became CEO on December 16, 2024 with serious credentials:

- Former Executive VP at LVMH's Duty Free Shoppers

- Led Women's Merchandising at Levi's

- McKinsey alum

- Served on Dollar Tree board 2020-2024 (brings competitive intel)

Her early initiatives focused on "elevating product, value and experience" with "encouraging" early customer response per management. The Q1 results were the FIRST full quarter under her leadership showing these initiatives are WORKING.

Analyst Upgrades Post-Q1 Beat:

- Guggenheim raised PT to $185

- Mizuho raised to $160 from $150

- JP Morgan raised to $154 from $105

- Craig-Hallum raised to $164 from $152

Average price target now $140-151 range vs current $160.86 - stock has already run PAST consensus! This suggests either: 1) Analysts are behind the curve and will raise further, OR 2) Stock has gotten ahead of itself.

🚀 Upcoming Catalysts (Next 6 Months - During Trade Window!)

Q2 Fiscal 2025 Earnings - Late August 2025 (CRITICAL!) 📊

Expected in late August/early September 2025, this will be THE catalyst that determines if this trade works:

- 📊 Q2 Guidance: Net sales $975M-$995M, comp sales +7% to +9%

- 💰 Expected EPS: $0.54 on $954.74M revenue per consensus

- 🎯 Adjusted EPS Guidance: $0.50-$0.62

What to watch:

- Comp sales sustainability - Can they deliver +7-9% again or was Q1 a one-time pop?

- Tariff impact - Company noted Q2 would show tariff effects from 60% China sourcing

- Gross margin trends - Pricing power vs tariff costs (looking for 54%+ maintained)

- MI325X customer feedback - Any color on new product initiatives under CEO Park

Upside scenario: Beat and raise again (like Q1) → stock gaps to $175-185 Downside risk: Comp sales guide down, tariff margin pressure → stock drops to $140-150

This earnings report happens AFTER this trade expires on January 16th, so it's NOT in the immediate window. BUT the ANTICIPATION and positioning for it will drive price action in December-January.

Store Expansion Milestones (Ongoing) 🏪

150 new locations planned for fiscal 2025, heavily front-loaded:

- Already opened 50 in Q1

- ~30 expected in Q2

- Geographic expansion into Pacific Northwest (Washington, Oregon)

- Target: 1,800+ stores by end FY2025, 3,500+ by fiscal 2030

Each store opening is a small positive catalyst - shows execution momentum and revenue growth drivers beyond just comp sales.

Tariff Mitigation Progress (Through 2025) 🌍

FIVE paused China shipments temporarily while evaluating options, then took action:

- Reduced China sourcing by 10 percentage points in H2 2025 (from 72% to ~62%)

- Opened office in India to diversify supplier base

- Implementing selective price adjustments on $1-$5 products

Timeline impact: Gradual improvements through fiscal 2025, but analysts estimate tariff costs could reach 90-95% on certain products with ~150 bps margin pressure risk in 2025.

Any news of successful tariff mitigation (vendor deals, India sourcing wins, price increases sticking) would be VERY bullish for the stock.

⚠️ Risk Catalysts (Negative)

Gen Z Budget Pressure 💸

FIVE's core demographic is under serious financial stress:

- Gen Z cutting overall spending 13% in early 2025

- Planned 23% holiday budget reduction in 2024 survey

- Youth unemployment and limited savings hitting discretionary spending

This is FIVE's BIGGEST fundamental risk - if your core customer is broke, doesn't matter how good your merchandise is.

Competition Intensifying 🥊

- Dollar General (~20,000 stores): Stock down 40%+ but expanding 730 new stores in 2024

- Dollar Tree/Family Dollar: Closing underperforming locations but acquired 99 Cents Only stores

- Online threats: Temu and Amazon Haul pressuring ALL physical discount retailers

FIVE has lowest customer retention (35% QoQ) among discount peers despite highest transaction value ($25). Lower shopping frequency vs Dollar General's 5.4 transactions per customer shows FIVE is more "treasure hunt occasional" vs "necessity repeat visit" positioning.

Tariff Margin Squeeze 🇨🇳

- ~60% of COGS imported from China

- Estimated 150 bps gross margin pressure from tariffs in 2025

- Current sourcing mix: China 72%, Mexico 8%, South Korea 7.3%, Vietnam 5%, India 2%

If tariff mitigation FAILS or new tariff policies hit, margins could compress significantly and force more aggressive price increases (risking volume).

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, catalyst timing, and technical setup, here are scenarios through January 16th expiration:

📈 Bull Case (35% probability)

Target: $175-$185

How we get there:

- 💪 Holiday sales results (reported mid-January) show continued strength - comp sales +5-7% range

- 🎯 Store expansion on track - 25-30 new stores opened in Q4, positive early performance

- 🌍 Tariff mitigation news - successful vendor negotiations or India sourcing wins announced

- 📊 Analyst upgrades continue as momentum builds toward Q2 earnings

- 🚀 Stock breaks $165 gamma resistance, then clears $170 massive wall on volume

- 📈 Technical breakout confirmed - trading above all moving averages with strong momentum

- 💰 Speculation builds for another Q2 earnings beat (early whispers of strong trends)

Key levels:

- Break $165 with conviction (our long call strike)

- Clear $170 gamma wall (0.52B - biggest resistance)

- Target zone $175-185 (sweet spot for spread)

Why 35%: Requires successful execution across multiple fronts but fundamentals support it. Q1 momentum is real, new CEO initiatives working, store expansion on track. Main risks are macro (Gen Z spending) and tariffs, but if those don't materialize negatively, path to $175-185 is clear.

Trade P&L in Bull Case:

- Stock at $175: Long calls worth $10 ($1.25M value), short calls worth $0 → Net gain = $350K (39% ROI)

- Stock at $180: Long calls worth $15 ($1.875M value), short calls worth $0 → Net gain = $975K (108% ROI!)

- Stock at $185: Long calls worth $20 ($2.5M value), short calls worth $0 → Net gain = $1.6M (178% ROI!!)

🎯 Base Case (45% probability)

Target: $155-$170 (CHOPPY RANGE)

Most likely scenario:

- ✅ Holiday sales decent but not spectacular - comp sales +3-5% range (good not great)

- 📊 Tariff situation remains unclear - some progress but no breakthrough

- 🏪 Store expansion proceeding but early performance mixed

- 📈 Stock consolidates in $155-170 range, respecting both gamma support and resistance

- 🤔 Market waiting for Q2 earnings proof that Q1 wasn't a fluke

- ⚖️ Volatility moderate - no major catalysts to drive big moves either way

- 💤 Premium decay works against both option positions

This is "hold and wait" territory: Stock trading range-bound between $155 support and $170 resistance for 4-6 weeks.

Trade P&L in Base Case:

- Stock at $160: Long calls worth $0 (expire worthless at-the-money), short calls worth $0 → Net loss = -$900K (100% loss)

- Stock at $165: Long calls worth $0 (at strike), short calls worth $0 → Net loss = -$900K (100% loss)

- Stock at $170: Long calls worth $5 ($625K value), short calls worth $0 → Net loss = -$275K (31% loss)

Why 45%: Most realistic given current positioning. Stock has rallied hard off lows, is consolidating near technical resistance, and needs more proof points before next leg up. Absent major catalyst in next 45 days, range-bound makes sense.

📉 Bear Case (20% probability)

Target: $140-$155 (SUPPORT TEST)

What could go wrong:

- 😰 Holiday sales disappoint - comp sales flat to slightly negative (Gen Z spending weakness)

- 🚨 Negative tariff news - new policies or failed mitigation efforts

- 💸 Broader retail sector weakness drags FIVE lower

- 🇨🇳 China tensions escalate affecting supply chain

- 📊 Analyst downgrades on valuation concerns (P/E 33x on slowing growth)

- 🔨 Break below $160 gamma support triggers cascade to $155, then $150

- 💰 Profit-taking after 123% rally off lows

Critical support levels:

- 🛡️ $155: First major test (0.30B gamma)

- 🛡️ $150: MAJOR FLOOR (0.47B gamma - strongest support!)

- 🛡️ $145: Extended support if $150 breaks

Trade P&L in Bear Case:

- Stock at $150: Long calls expire worthless, short calls expire worthless → Net loss = -$900K (100% loss)

- Stock at $140: Long calls expire worthless, short calls expire worthless → Net loss = -$900K (100% loss)

Why 20%: Requires reversal of established Q1 momentum and new negative catalysts. While risks are real (Gen Z spending, tariffs, competition), the turnaround evidence from Q1 creates benefit of doubt. Break below $150 would be major red flag invalidating bullish thesis.

Maximum Risk Scenario (Above $200): If stock EXPLODES past $200 (would require extraordinary news), the short calls create UNLIMITED risk. At $220, long calls worth $55 ($6.875M) but short calls worth -$20 × 2,500 = -$5M exposure. Net would still be positive but structure breaks down above $200.

Probability of >$200: <5% - would require multiple massive positive surprises in 45-day window. Unlikely but why trader chose $200 strike for short calls (felt safe).

💡 Trading Ideas

🛡️ Conservative: Watch and Wait for Clarity

Play: Stay on sidelines until post-holiday sales data and closer to Q2 earnings

Why this works:

- ⏰ No immediate catalyst in next 3-4 weeks (holiday sales not reported until mid-January)

- 💸 Options expensive going into year-end - implied vol elevated

- 📊 Stock at technical resistance ($160-165) - not ideal entry for stock purchase

- 🎯 Better risk/reward waiting for either breakout confirmation above $170 OR pullback to $150 support

- 📉 Holiday season uncertain - Gen Z spending weakness could show up in results

- 🤔 The $1.9M institutional spread shows even smart money is HEDGING (selling upside), not going naked long

Action plan:

- 👀 Watch for holiday sales results (expected mid-January 2026)

- 🎯 If stock breaks $165 and holds above for 3+ days, consider stock entry $168-172

- ✅ If stock pulls back to $150 gamma support, that's compelling risk/reward for shares

- 📊 Monitor for additional unusual options activity - if institutions add MORE bullish bets, pay attention

- ⏰ Revisit in late January/early February as Q2 earnings anticipation builds

Risk level: Minimal (cash position) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 10-15% drawdown if support breaks. Get better entry if consolidation continues. Maintain optionality.

⚖️ Balanced: Stock Entry at Support with Defined Stop

Play: Buy shares if/when stock tests $150-155 support zone

Structure:

- Buy 100-300 shares at $150-155 (invest $15,000-$46,500)

- Set HARD stop-loss at $145 (3.3-6.5% max loss)

- Target exit $175-180 (16-20% gain)

Why this works:

- 📊 $150 is STRONGEST gamma support (0.47B) - dealers will defend this level

- 🎯 Provides 5-10% cushion from current price for entry

- 🛡️ Defined risk with stop at $145 (below all meaningful support)

- 📈 Risk/reward 3:1 to 4:1 ($5-10 risk for $20-30 gain potential)

- 💰 No theta decay like options - you own the stock

- ⏰ Can hold through Q2 earnings if thesis developing positively

Position sizing: Allocate only 5-10% of portfolio (this is speculative retail play, not core holding)

Entry trigger:

- ✅ Stock trading $150-155 range

- ✅ Volume confirms support (high volume reversal candle)

- ✅ No new negative fundamental news (tariffs, Gen Z spending collapse, etc)

Risk level: Moderate (directional stock with defined stop) | Skill level: Intermediate

Expected outcome: Capture 15-20% rally to $175-180 if turnaround thesis continues, limit downside to 5-7% if wrong.

🚀 Aggressive: Replicate the Spread at Smaller Size (ADVANCED!)

Play: Copy the institutional call spread structure but at 1/10th the size

Structure:

- Buy 1-2 contracts of $165 calls @ ~$10.80 ($1,080-$2,160 cost)

- Sell 2-4 contracts of $200 calls @ ~$2.00 ($400-$800 credit)

- Net debit: $680-$1,360 per 1:2 spread unit

- January 16, 2026 expiration (45 days)

Why this could work:

- 🤝 Copying smart money positioning - "coat-tailing" institutional trade

- 💰 Reduced cost basis by selling upside (net $680-900 per spread vs $1,080 naked call)

- 🎯 Defined max risk (can't lose more than net debit)

- 📊 Targets realistic price zone ($165-$200 = +2.6% to +24.3%)

- ⚡ Max profit zone $175-195 where spread is widest

- 📈 Benefits from breakout above $165 technical resistance

Why this could blow up (SERIOUS RISKS):

- 💸 THETA DECAY BRUTAL: Losing $15-25/day per spread as expiration approaches

- 😱 Need movement FAST: Stock must break $165 within 2-3 weeks or time decay kills you

- 📊 Ratio risk: Selling 2x creates exposure if stock EXPLODES past $200 (unlikely but possible)

- ⏰ No catalysts for 4+ weeks: Holiday sales not reported until mid-January = dead zone

- 🎢 Stock could chop $155-165 for entire period and you lose 80-100% of premium

- ⚠️ Early assignment risk on short calls if stock gaps past $200 (would need to manage)

Profit/Loss scenarios (per 1-long/2-short spread unit):

- 💰 Stock at $175: Long call worth $10 ($1,000), short calls worth $0 → Net gain = $320 (47% ROI)

- 🚀 Stock at $185: Long call worth $20 ($2,000), short calls worth $0 → Net gain = $1,320 (194% ROI!)

- 💀 Stock at $160: Entire spread expires worthless → Net loss = -$680 (100% loss)

- 😰 Stock at $150: Entire spread expires worthless → Net loss = -$680 (100% loss)

- 🆘 Stock at $220: Long call worth $55 ($5,500), short calls worth -$20 × 2 = -$4,000 → Net gain = $820 but messy

CRITICAL REQUIREMENTS - DO NOT attempt unless you:

- ✅ Understand ratio spread mechanics and assignment risk

- ✅ Can monitor position daily and adjust if needed

- ✅ Accept you could lose ENTIRE premium (high probability actually)

- ✅ Have traded spreads through expiration before

- ✅ Won't panic if stock drops to $155 early (hold or cut loss)

- ⏰ Plan active management - this is NOT set-and-forget

Risk level: HIGH (can lose 100% of premium, ratio creates upside exposure) | Skill level: Advanced only

Probability of profit: ~35-40% (need breakout AND right timing)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💸 Gen Z spending collapse accelerating: FIVE's core demographic cut spending 13% in early 2025 and planned 23% holiday budget reduction. If this trend worsens, comp sales could turn negative again regardless of CEO initiatives. Youth unemployment and limited savings are structural issues that merchandise assortment can't fix. This is FIVE's BIGGEST existential risk - broke customers don't spend even at great stores.

-

🇨🇳 Tariff margin squeeze intensifies: With ~60% of COGS from China and potential 90-95% tariff costs on certain products, gross margins face estimated 150 bps compression in 2025. Even with India sourcing office and selective price adjustments, there's limited pricing power with budget-conscious Gen Z. New tariff policies could hit unexpectedly. Sourcing diversification takes 12-18 months - short term pain likely.

-

🥊 Competition from Temu/Amazon Haul devastating: Online discount retailers like Temu and Amazon Haul offer ultra-low prices without physical store costs. Gen Z is VERY comfortable shopping online. 63% of Gen Z opting for resale/upcycled products vs new merchandise also shifts demand away from FIVE's model. Traditional dollar stores (DG, DLTR) expanding aggressively too - market getting saturated.

-

📊 Q1 beat could be one-time pop, not sustainable: Three consecutive quarters of negative comps (Q2-Q4 FY2024) before Q1 FY2025 reversal raises question - is this REAL turnaround or temporary bounce? New CEO "honeymoon period" with easier comparisons? Fiscal 2024 EPS down 16-20% despite 9% revenue growth shows margin pressure is real. Q2 will be critical test if +7% comps can be maintained or was Q1 lucky timing.

-

😰 Customer retention weakest among peers: 35% quarter-over-quarter retention (vs Dollar General higher rate) shows FIVE is "treasure hunt occasional visit" not "weekly necessity" destination. Lower shopping frequency means more vulnerable to discretionary spending cuts. Customers love FIVE when they visit (highest $25 transaction value) but don't visit OFTEN enough for stable revenue.

-

⏰ No near-term catalyst for 4-6 weeks: Holiday sales results not reported until mid-January 2026, Q2 earnings not until late August. This is a DEAD ZONE for news flow. Stock could chop sideways in $155-165 range for entire January, bleeding theta on option positions. Requires patience and conviction to hold through quiet period.

-

📈 Valuation stretched at 33x P/E on slowing growth: Trading at premium multiple (33.01 forward P/E) vs historical 20-25x range. Already up 123% off lows with stock at $160.86 vs average analyst target $140-151. Limited upside to consensus means further gains require earnings beats AND multiple expansion (double catalyst). Downside risk if either disappoints.

-

🎯 Ratio spread creates unlimited upside risk: The 2:1 call spread structure (selling 2,500 calls vs buying 1,250) creates EXPOSURE above $200. If stock somehow EXPLODES to $220+, the short calls create large losses that could offset long call gains. While unlikely (<5% probability), it's a tail risk inherent in ratio spreads. Would require extraordinary news (major acquisition, partnership, etc).

-

🛡️ $165 gamma resistance is REAL barrier: Current gamma map shows $165 has 0.11B total gamma where dealers will sell rallies. More importantly, $170 has MASSIVE 0.52B call gamma (biggest single level) creating natural ceiling. Stock needs very strong buying pressure to break through these zones. Technical traders will short resistance, creating sell pressure.

-

📉 Macro recession risk: If U.S. economy weakens in 2025-2026, discretionary retailers get crushed first. FIVE's products are WANTS not NEEDS - first thing budget-conscious families cut. Unlike Dollar General selling food/household staples, FIVE is pure discretionary. Zero recession protection at current valuation.

🎯 The Bottom Line

Real talk: Someone with serious capital ($1.9M notional) just made a STRUCTURED bet that Five Below breaks out above $165 and runs toward $175-195 in the next 45 days. This isn't a YOLO naked call buyer - this is sophisticated positioning with defined risk and realistic price targets. The 2:1 ratio spread structure (selling 2x upside to finance the trade) tells you they're bullish but DISCIPLINED, not chasing $250 moon-shot scenarios.

What this trade tells us:

- 🎯 Smart money believes Q1 turnaround momentum CONTINUES through holiday season and into Q2

- 💰 They see $165-170 technical breakout as HIGH PROBABILITY in next 4-6 weeks

- ⚖️ They DON'T expect vertical rally to $200+ (hence selling those calls for premium)

- 📊 They structured at gamma resistance levels, showing technical sophistication

- ⏰ January 16th expiration suggests they expect move BEFORE holiday sales results (anticipation, not reaction)

The bull case is compelling:

- ✅ New CEO Winnie Park's initiatives showed immediate results in Q1 (+19.5% revenue, +7.1% comps)

- ✅ Aggressive store expansion (150 new locations in FY2025) provides growth even if comps moderate

- ✅ Tariff mitigation progressing (China sourcing down 10 points)

- ✅ Trading near technical resistance - breakout above $165 triggers momentum to $175-185

- ✅ Gamma structure supports $150 floor (0.47B) and shows path to $170-185 (low resistance above $175)

But the bear case is REAL:

- ⚠️ Gen Z core demographic cutting spending 13-23% - broke customers are existential threat

- ⚠️ 60% China sourcing creates 150 bps margin pressure from tariffs

- ⚠️ Online competition (Temu, Amazon Haul) and dollar store saturation intensifying

- ⚠️ Q1 could be one-time pop, not sustainable trend (need Q2 confirmation)

- ⚠️ Valuation stretched (33x P/E, already above consensus targets)

- ⚠️ Weakest customer retention among peers (35% QoQ)

If you own FIVE:

- ✅ This trade validates your bullish thesis - institutions positioning for breakout

- 📊 Consider tightening stops to $155 (below gamma support) to protect gains from 123% rally off lows

- ⏰ Hold through holiday period but WATCH mid-January holiday sales report closely

- 🎯 Take partial profits at $175-180 if stock runs (lock in gains, reduce risk)

- 🛡️ Don't get greedy - you've already won big off the lows! Protecting profits is smart.

If you're watching from sidelines:

- ⏰ Wait for confirmation: Either breakout above $165-170 OR pullback to $150 support

- 🎯 Stock entry at $150-155 offers compelling risk/reward (5-7% downside to $145 stop, 15-20% upside to $175-180)

- 📈 Options are EXPENSIVE here - spread structure (like this trade) makes more sense than naked calls

- 🚀 Longer-term (6-12 months), if CEO Park executes and Q2 confirms turnaround, $200+ is achievable

- ⚠️ Current valuation requires PERFECT execution - one stumble and it's back to $140-150

If you're bearish:

- 🎯 Wait for FAILED breakout at $165-170 before shorting - don't fight momentum

- 📊 First short entry on rejection at $165 with stop at $172

- ⚠️ Better short setup is break BELOW $155 (confirms reversal)

- 📉 Target $145-150 support zone for short covering

- ⏰ Timing matters: shorting into strength before holiday sales results is suicide

Mark your calendar - Key dates:

- 📅 Mid-January 2026 - Holiday sales results for period through January 4

- 📅 January 16, 2026 - Monthly OPEX, expiration of this $1.9M call spread

- 📅 Late August/Early September 2025 - Q2 FY2025 earnings (CRITICAL CATALYST)

- 📅 Mid-2025 - Store expansion milestones (150 new locations target)

- 📅 Throughout 2025 - Tariff mitigation progress updates

Final verdict: FIVE's turnaround story is REAL but EARLY. Q1 results proved new CEO can execute, but sustainability remains unproven with major headwinds (Gen Z spending, tariffs, competition). The $1.9M call spread shows institutions are positioning for $165-185 rally but HEDGING upside (not betting on moon-shot). This is a "show-me" stock - needs to PROVE Q1 wasn't a fluke.

Smart money is betting on EXECUTION, not hoping for miracles. That's a sign of conviction based on fundamentals, not speculation.

For most retail traders, the best approach is PATIENCE - let the stock break $165 convincingly and hold for 3-5 days before entering, OR wait for pullback to $150 gamma support for lower-risk entry. The trade structure (spread, not naked calls) shows even institutions aren't willing to pay up for unlimited upside - they're taking profits at $200 to finance downside protection.

This is a marathon, not a sprint. Wait for your pitch. The teen retail revolution will still be here in 6-8 weeks. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual scores (75x and 437x average size) reflect these specific trades' sizes relative to recent FIVE history - they do not imply the trades will be profitable or that you should follow them. Ratio spreads create upside exposure above short strike that can result in significant losses if stock moves dramatically higher. Always do your own research and consider consulting a licensed financial advisor before trading.

About Five Below: Five Below operates as a specialty value retailer offering merchandise targeted at the tween and teen demographic, with a market cap of $8.92 billion in the Retail - Variety Stores industry. The company operates 1,800+ stores across 46 states with plans to expand to 3,500+ locations by fiscal 2030.