🐉 FXI: Someone Just Bet $1.4M China Explodes Higher by February!

📅 December 19, 2025 | 🔥 Extreme Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $1.4 million on FXI February calls with a Z-Score of 18.56 - that's not your neighbor trading on lunch break! This massive bet (26,000 contracts) targets a 6% rally in Chinese stocks by February 20, betting that China's historic monetary stimulus and trade stabilization will finally ignite a sustained rally in large-cap Chinese equities.

💰 The Option Flow Breakdown

📊 What Just Happened

| Time | Symbol | Side | Type | Expiration | Strike | Premium | Volume | Z-Score | Option Chart |

|---|---|---|---|---|---|---|---|---|---|

| 10:34:33 | FXI | 🟢 BUY | CALL | 2026-02-20 | $41 | $1.4M | 26,000 | 18.56 | View Chart |

- 🎯 Strategy: Long Call (standalone directional bet)

- 📊 Signal: OPEN (new position established)

Current Market Context:

- 💹 FXI Price: $38.68

- 🎯 Distance to Strike: +6.0% upside needed

- 📊 Breakeven: ~$41.54 (strike + premium paid)

🤓 What This Actually Means

Real talk: This trader is betting that China's largest companies - think Alibaba, Tencent, China Construction Bank - are about to rally at least 6% over the next two months. With China's historic shift to "moderately loose" monetary policy (first time since 2010!) and U.S. tariffs stabilized at reduced levels through November 2026, someone with serious capital thinks the stars are finally aligning for Chinese equities.

This isn't a gamble on earnings or a single catalyst - it's a macro bet that China's combination of aggressive stimulus, trade stabilization, and the December 18 Hainan Free Trade Port launch will push large-caps through resistance.

Why February 20? That's the monthly OPEX target - giving China's policy measures time to show results while capturing any pre-Lunar New Year momentum.

🏢 What is FXI?

The iShares China Large-Cap ETF (FXI) tracks the 50 largest Chinese companies listed in Hong Kong, giving investors direct exposure to China's economic heavyweights:

Top Holdings (as of December 2025):

- 🛒 Alibaba (9.37%) - E-commerce giant, up 46% YTD through May

- 🎮 Tencent (8.66%) - Gaming/social media powerhouse, up 23% YTD

- 🏦 China Construction Bank (7.01%) - Banking infrastructure

- 📱 Xiaomi (6.73%) - Consumer electronics leader

- 🍔 Meituan (5.06%) - Food delivery platform

- 🏦 ICBC (4.82%) - Industrial & Commercial Bank of China

Fund Stats:

- 📊 Assets Under Management: $6.54 billion

- 📈 YTD Performance: +30.17% (strong recovery from 2024 lows)

- 💰 Market Cap Exposure: Large-cap focus ($38+ billion average)

- 🌏 Geographic Focus: Hong Kong-listed Chinese equities

- 📉 Recent Flows: -$2.36 billion outflows over 1 year (contrarian signal?)

📈 Technical Setup / Chart Check-Up

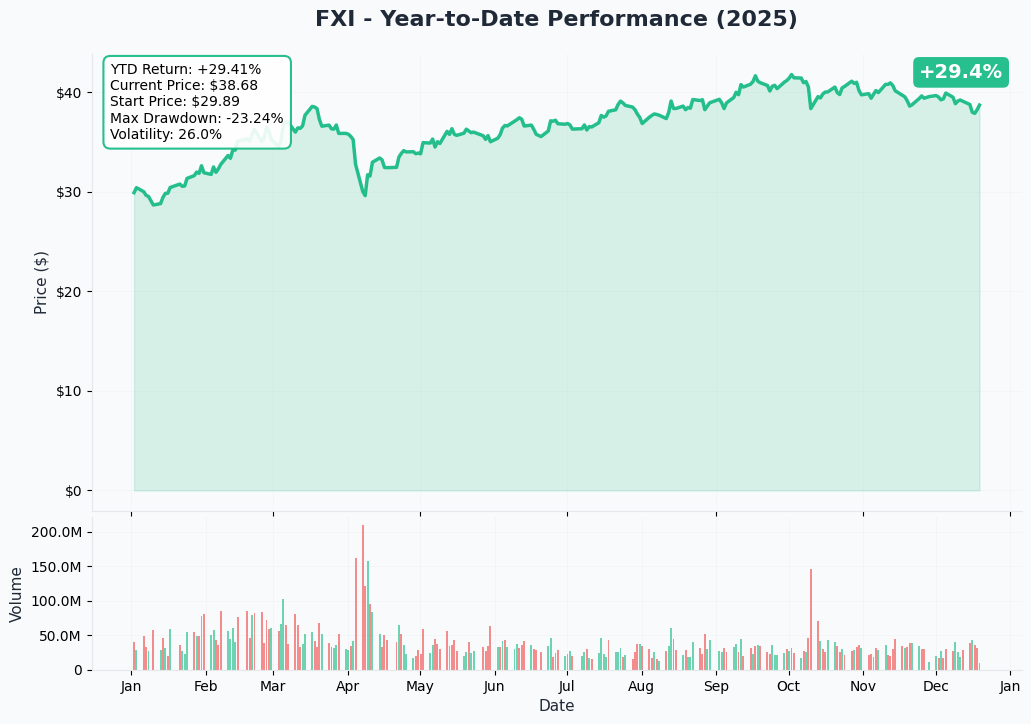

📊 YTD Chart Analysis

FXI has delivered a 30.17% return year-to-date, recovering from its October 2024 lows around $28.41 to current levels near $38.68. The ETF hit 52-week highs at $42.00 in October before pulling back on tax-rumor jitters affecting Hong Kong tech stocks in mid-December.

The current consolidation near $38-39 represents a healthy pullback after the September-October rally, creating a technical setup for the next leg higher if China's stimulus measures gain traction.

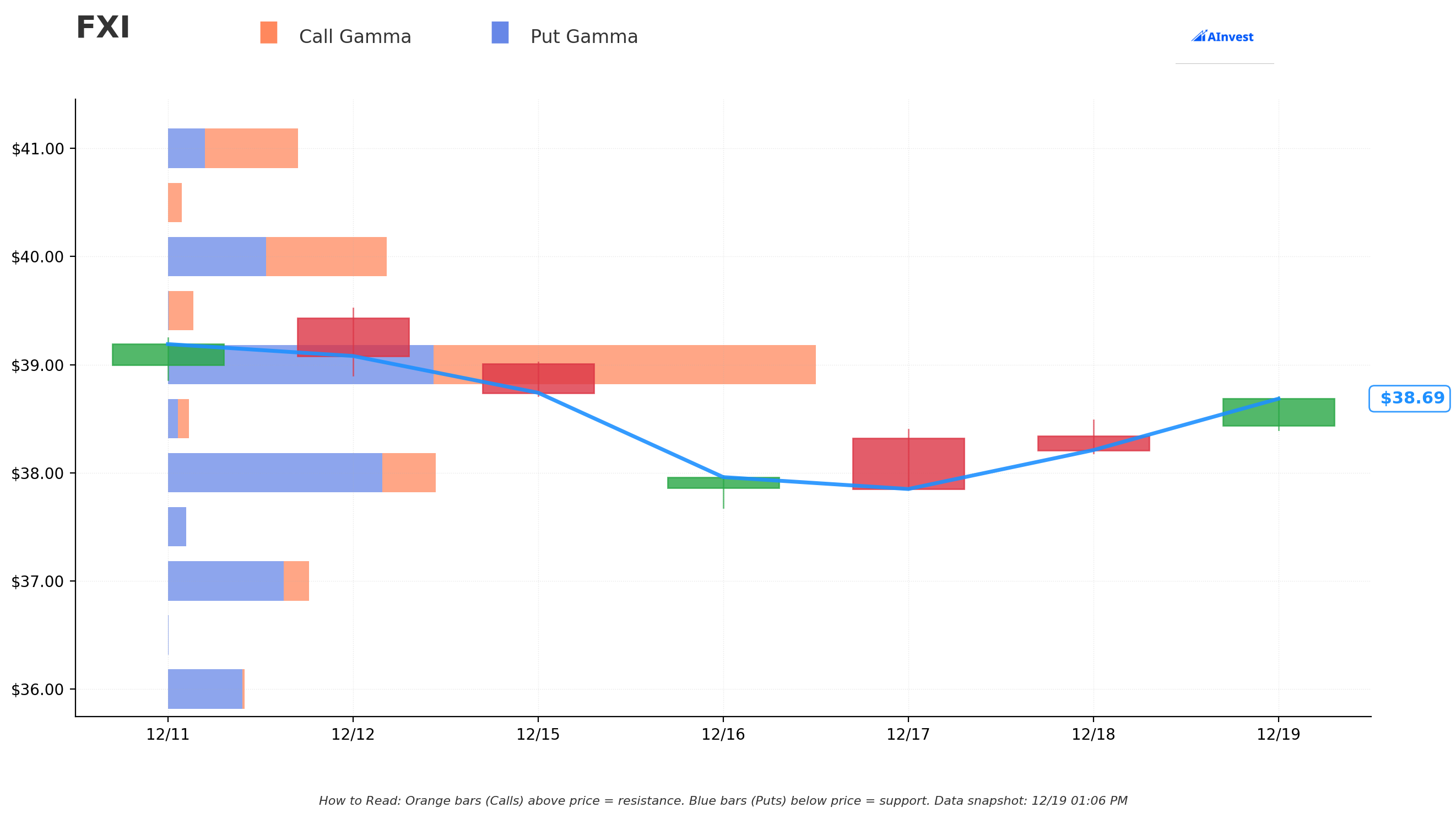

🎯 Gamma-Based Support & Resistance Analysis

Key Gamma Levels:

Very Strong Support:

- 🔵 $38.00 - Net GEX: -126.7M (Put Wall)

- This is your floor! Massive put gamma concentration means market makers need to buy stock if FXI drops here, creating natural buying pressure

- Currently just $0.68 below current price - acting as immediate downside cushion

Very Strong Resistance:

- 🟠 $39.00 - Net GEX: +91.0M (Call Wall)

- First major resistance just $0.32 above current price

- Heavy call gamma concentration means dealers will sell stock to hedge if we push through here

- Breaking $39 with conviction could trigger short-covering rally

Trading Implications: FXI is currently trapped in a tight $38-$39 gamma channel. The $1.4M call buyer is betting on a breakout above $39 that accelerates through $41 by February OPEX. With such tight gamma walls, a catalyst could create explosive moves in either direction.

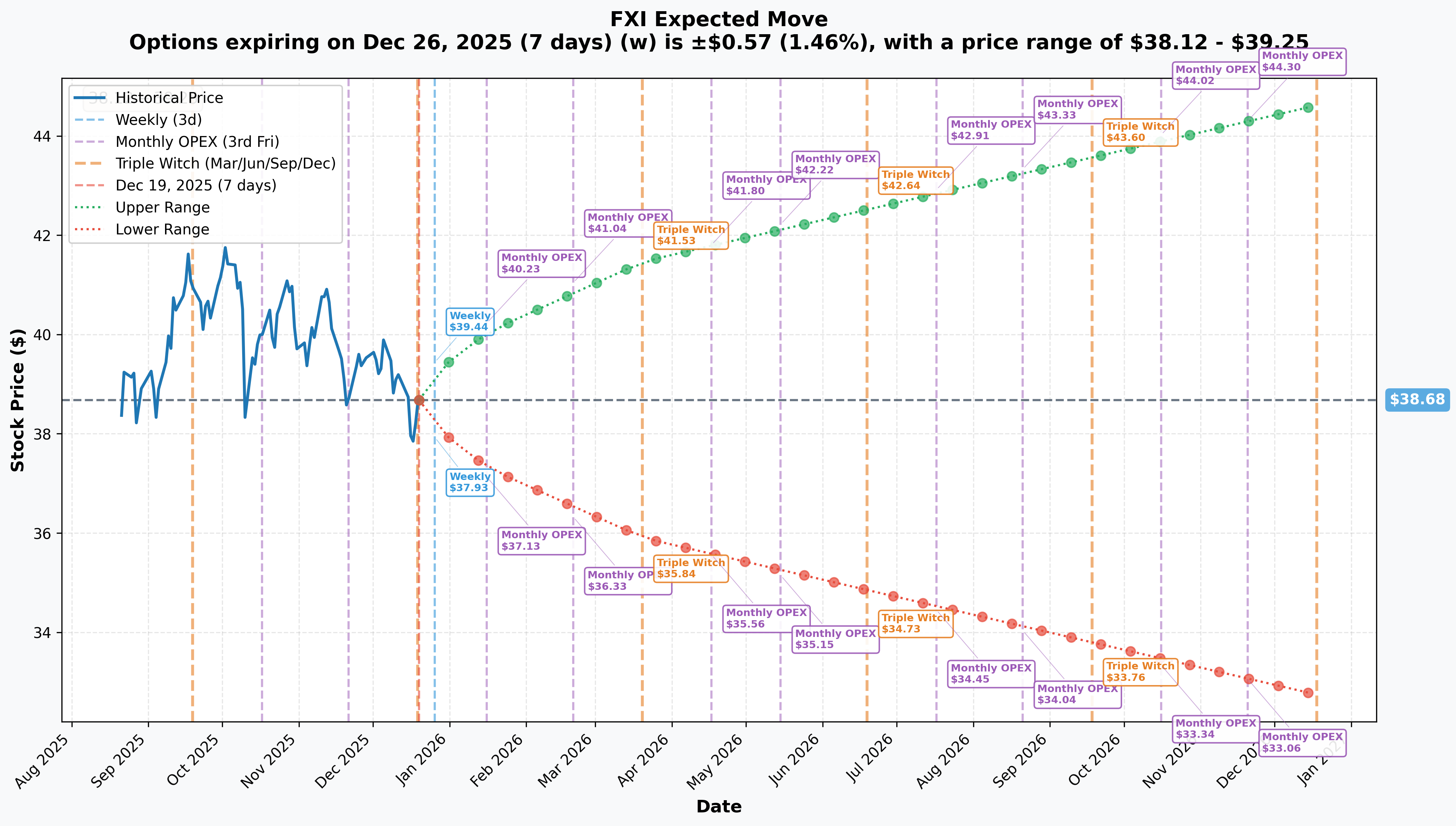

📊 Implied Move Analysis

Market-Implied Price Ranges:

Weekly (Dec 26): ±1.46%

- 📈 Upper: $39.25

- 📉 Lower: $38.12

- 💡 Narrow range suggests market expects quiet holiday trading

Monthly OPEX (Jan 16): ±3.54%

- 📈 Upper: $40.05

- 📉 Lower: $37.31

- 🎯 This is the first test zone for the call buyer's thesis

Monthly OPEX (Feb 20): ±7.2% (TARGET EXPIRATION)

- 📈 Upper: $41.47 ✅ Covers the $41 strike!

- 📉 Lower: $35.90

- 💡 The market is pricing a $41.47 upper bound - the call buyer needs FXI to reach the high end of expected range

Why This Matters: The implied move data shows the market IS pricing in the possibility of FXI hitting $41+ by February 20 - it's at the upper edge of the expected range, not some wild moonshot. This means the call buyer is betting on China outperforming expectations, not on some miracle scenario.

🎪 Catalysts

🔜 Upcoming Catalysts (Next 60 Days)

Major Policy Implementation:

📅 Q4 2025 GDP Release (Expected Mid-January 2026)

- Consensus Range: 4.3%-4.8% growth for 2026

- Goldman Sachs (upgraded): 4.8%

- Morgan Stanley: 4.8%

- UBS: 4.5%

- IMF (conservative): 4.2%

- Why It Matters: Better-than-expected GDP growth could validate the stimulus measures and ignite foreign capital inflows

- Risk: Weak manufacturing PMI (8 straight months below 50) could disappoint

📅 Monetary Policy Actions (Q1 2026)

- Expected Moves: Rate cuts, reserve requirement ratio reductions

- Context: Historic "moderately loose" policy stance announced at December 11-12 Central Economic Work Conference

- Impact: Lower rates = more liquidity = higher asset prices (especially growth stocks like Alibaba/Tencent)

📅 Consumer Stimulus "Special Action Plan" (Q1 2026)

- Budget: 300 billion RMB ($42B) for consumer goods trade-in program

- Goal: Lift consumer confidence from historic lows (CCI at 89.60 vs. 200 in 2021)

- Beneficiaries: Xiaomi (electronics), Meituan (consumer spending), Alibaba (e-commerce)

📅 Alibaba & Tencent Earnings Window (Late January/Early February)

- Tencent Q4 Preview: Q3 showed 15% revenue growth with international gaming +43%

- Alibaba AI Investment: $50+ billion committed to cloud and AI development

- Combined Weight: 18% of FXI - strong earnings could drive ETF performance

✅ Recent Catalysts (Already Happened)

December 18, 2025: Hainan Free Trade Port Launch ✅

- Established world's largest free-trade zone with 74% zero-tariff coverage (up from 21%)

- Symbolic launch on anniversary of 1978 reform milestone

- Over 6,600 items now tariff-free (vs. 1,900 previously)

December 11-12, 2025: Central Economic Work Conference ✅

- First "moderately loose" monetary policy since 2010

- Budget deficit raised to 4% of GDP (highest since 2010)

- Top 2026 priority: "Vigorously boost consumption"

November 2025: U.S.-China Trade Agreement Extended ✅

- Tariffs reduced to 47.5% (from 145% peak) through November 2026

- Agricultural commitments: 12M tons soybeans in 2025, 25M tons annually 2026-2028

- Export restrictions suspended on gallium, germanium, antimony, graphite

October 2025: Hang Seng Rally ✅

- Hang Seng Index up 35% YTD, biggest annual gain since 2017

- Hang Seng Tech Index climbed 48% over the year

- FXI benefited with 30.17% YTD return

🎲 Price Targets & Probabilities

📊 Bull Case: $41-$42 (Call Buyer's Target Zone)

Path to Success:

- ✅ Break above $39 gamma resistance with volume

- ✅ Q4 GDP comes in at 4.5%+ (upper end of estimates)

- ✅ PBOC delivers meaningful rate cuts in January

- ✅ Alibaba/Tencent earnings beat expectations

- ✅ Foreign capital inflows accelerate (Southbound flows projected at $110B for 2025)

Technical Targets:

- $39.25 - Weekly implied move upper bound (immediate resistance)

- $40.05 - January OPEX implied upper range

- $41.47 - February OPEX implied upper range (covers strike + premium)

- $42.00 - Prior 52-week high (psychological resistance)

Probability Assessment: ~35-40%

- Market is pricing $41.47 as upper bound (not impossible)

- Requires multiple catalysts to align + gamma breakout

- Goldman Sachs upgraded GDP forecast supports bullish case

💼 Base Case: $37-$39 (Range-Bound Consolidation)

Most Likely Scenario:

- FXI remains trapped in $38-$39 gamma channel through year-end

- Holiday trading keeps volume light through early January

- Stimulus measures show incremental improvement but no breakthrough

- Property sector concerns persist (November developer sales -36%)

- Consumer confidence improves modestly but stays below 100

Key Levels:

- Support: $38.00 (gamma floor), $37.31 (Jan OPEX lower bound)

- Resistance: $39.00 (gamma ceiling), $39.25 (weekly upper bound)

Probability Assessment: ~45-50%

- Gamma walls create natural range

- Historical pattern: China stimulus takes 2-3 quarters to show results

- December tax rumors demonstrated market fragility

🐻 Bear Case: $35-$37 (Stimulus Disappointment)

Downside Risks:

- ❌ Property crisis deepens (Vanke systemic distress)

- ❌ Manufacturing PMI stays below 50 (8th+ straight month of contraction)

- ❌ Consumer confidence fails to respond to stimulus

- ❌ U.S.-China tensions re-escalate before November 2026 deadline

- ❌ Delisting fears resurface for Alibaba/Tencent

Technical Breakdown Levels:

- $37.31 - January OPEX lower implied bound

- $36.33 - February OPEX lower implied bound

- $35.90 - Quarterly triple witch lower range

- $35.00 - Psychological support / September rally starting point

Probability Assessment: ~15-20%

- Property sector remains biggest systemic risk (30% of bank loans exposed)

- Net FDI reversed to -$154B outflows in 2024

- Fund outflows continue (-$2.36B over past year)

💡 Trading Ideas

🛡️ Conservative: "Wait for Confirmation" Strategy

The Play:

- Don't chase this trade yet - let the $39 gamma resistance get taken out first

- Entry: FXI breaks above $39.50 with volume

- Position: Buy Feb 20 $40 calls (lower strike than whale trade)

- Stop: Close position if FXI breaks below $38 (gamma support fails)

- Target: $41-$42 (5-7% upside from entry)

Why This Works:

- You're confirming the breakout before committing capital

- Lower $40 strike gives you better odds than $41

- Risk defined by gamma support level

- Still captures majority of move if bull case plays out

Probability of Success: ~40-45% Risk Profile: Medium (defined risk below $38)

⚖️ Balanced: "Fade the Range" Strategy

The Play:

- Play the $38-$39 gamma channel until it breaks

- Setup: Sell FXI $38 puts / Buy FXI $39 calls when near channel edges

- Thesis: Gamma walls create predictable mean reversion

- Time Horizon: Short-term (weekly expirations)

- Exit: Close all positions if FXI breaks out of $38-$39 range

Why This Works:

- Strong gamma walls at both $38 (support) and $39 (resistance)

- Market makers will defend these levels by delta hedging

- Collect premium while waiting for directional resolution

- Low probability of large moves during holiday season

Probability of Success: ~55-60% Risk Profile: Medium (gamma squeeze risk if range breaks)

🚀 Aggressive: "Copy the Whale" Strategy

The Play:

- Mirror the institutional trade (or at least the thesis)

- Position: Buy Feb 20 $41 calls

- Size: Risk 1-2% of portfolio max

- Thesis: China stimulus + trade deal = breakout rally

- Add: If FXI hits $40 before late January

Why This Works (If It Works):

- Someone with $1.4M capital did serious homework

- Z-Score of 18.56 = institutional conviction, not retail FOMO

- Multiple catalysts align in January-February window

- February OPEX implied move says $41.47 is possible

Why This Could Fail:

- Property crisis could spiral (Vanke warning sign)

- Consumer confidence stays depressed despite stimulus

- Manufacturing weakness persists (PMI below 50)

- Holiday volume makes it hard to sustain rally

Probability of Success: ~30-35% Risk Profile: High (defined risk = premium paid, but low probability) Position Sizing: Max 1-2% of portfolio - this is a lottery ticket

⚠️ Risk Factors

🏚️ Property Sector Contagion (HIGH RISK)

The elephant in the room: China's property crisis is getting worse, not better. November sales from top 100 developers plunged 36% year-over-year, and Vanke - the last major developer survivor - is facing systemic distress with $3.1 billion in loan obligations. With 30% of China's bank loans exposed to real estate, this could trigger financial sector contagion that overwhelms any stimulus measures.

Impact on FXI: Direct exposure through China Construction Bank (7.01%) and ICBC (4.82%) - if property crisis spreads, bank stocks get hammered.

📉 Consumer Demand Weakness (MEDIUM-HIGH RISK)

Consumer confidence is hovering near 86, down from almost 200 in 2021. Despite 300 billion RMB in stimulus, McKinsey research shows consumers are increasingly basing spending on "hard factors" like personal asset values rather than sentiment. With property prices still declining and youth unemployment elevated, it's hard to see how stimulus creates sustainable consumption growth.

Impact on FXI: Alibaba (9.37%) and Meituan (5.06%) need consumer spending to grow - weak consumption = earnings misses.

🏭 Manufacturing Contraction (MEDIUM RISK)

China just posted its 8th consecutive month of manufacturing PMI below 50 (November: 49.2 official, 49.9 Caixin). New orders fell for the 5th straight month, and employment remains weak at 48.4. This suggests China's factory sector is contracting despite government support.

Impact on FXI: Xiaomi (6.73%) depends on manufacturing strength - continued weakness could pressure margins.

🌐 U.S.-China Trade Uncertainty (MEDIUM RISK)

While the current 47.5% tariff rate is stable through November 2026, this creates a binary risk event: renegotiation could go either way. And let's be real - "business needs predictability, and that's not the story of 2025" according to former U.S. Commerce official Doug Barry. U.S. imports from China fell 22.2% in first half of 2025.

Impact on FXI: Export-dependent companies face ongoing uncertainty - hard to justify premium valuations.

🚫 Regulatory & Delisting Risk (MEDIUM RISK)

The delisting sword of Damocles still hangs over Chinese ADRs. Using fiscal period ending April 2025 as year one, delisting could come by 2026 - "faster than you think." Meanwhile, semiconductor export controls continue tightening, and Nasdaq now requires Chinese companies to raise at least $25M in IPOs.

Impact on FXI: Although FXI tracks Hong Kong listings (not direct U.S. delisting risk), sentiment contagion from ADR delisting fears could pressure valuations.

💸 Capital Flight & FDI Reversal (MEDIUM RISK)

Here's a stunning stat: Net FDI plummeted from $334B inflows in 2021 to -$154B outflows in 2024. Foreign investors characterize China as "too big to ignore, but too controlled and opaque to fully trust." FXI itself has experienced -$2.36B in net outflows over the past year.

Impact on FXI: Continued capital flight creates persistent selling pressure - hard to rally sustainably without foreign buying.

🎯 The Bottom Line

Real talk: This $1.4M call buyer is making a calculated macro bet that China's historic policy pivot will finally break the malaise that's gripped Chinese equities since 2021. With a Z-Score of 18.56, this is institutional money - someone who has access to research, economic data, and likely some insight into policy implementation.

The bull case is compelling: First "moderately loose" monetary policy in 14 years, trade wars cooling, Hainan Free Trade Port launching, and top holdings like Alibaba/Tencent showing genuine business momentum. The February 20 expiration gives China's stimulus measures time to show results while capturing any pre-Lunar New Year optimism.

But the bear case is real: Property crisis deepening (Vanke warning), consumer confidence near decade lows, 8 straight months of manufacturing contraction, and persistent capital flight. These aren't minor headwinds - they're structural challenges that could take years to resolve.

Here's the deal:

🟢 If you own FXI: Mark your calendar for Q4 GDP release (mid-January) and watch for $39 breakout. Add if we clear $39.50 with volume. Stop out if $38 gamma support fails.

👀 If you're watching: Don't chase here at $38.68. Let the trade prove itself by breaking $39. Consider selling puts at $38 if you want to collect premium while waiting. Be patient - if China stimulus works, you'll have plenty of time to participate in a sustained rally.

🔴 If you're bearish: The property crisis and consumer weakness are real. But shorting here means fighting China's central bank AND fighting gamma support at $38. Better risk/reward is waiting for a failed breakout above $39, then shorting back to $37.

The Three-Month Mark Your Calendar:

- Mid-January: Q4 GDP release + potential rate cuts

- Late January/Early Feb: Alibaba & Tencent earnings

- February 20: Option expiration - judgement day for this $1.4M bet

Bottom line: This is a high-conviction institutional bet on China's policy response, not a guaranteed winner. The 6% move to $41 is achievable (it's within implied move range), but requires multiple catalysts to align. Size accordingly - this is a 1-2% portfolio position max, even if you love the thesis.

China's either about to prove the stimulus skeptics wrong... or it's about to teach us (again) that you can't stimulus your way out of structural problems. The $1.4M call buyer thinks it's the former. Time will tell.

📊 Key Trade Monitoring Levels

Bullish Confirmation:

- ✅ Break above $39.00 (gamma resistance)

- ✅ Hold above $39.50 for 2+ sessions

- ✅ Volume surge (2x average) on breakout

Bearish Warning Signs:

- ❌ Break below $38.00 (gamma support)

- ❌ Close below $37.50 for 2+ sessions

- ❌ Vanke bankruptcy or major bank exposure announced

Neutral Zone:

- ⚪ Range: $38.00 - $39.00

- ⚪ Low volume during holiday season

- ⚪ Wait for directional resolution

🔗 Trade Links

Analyze This Trade:

Disclaimer: This analysis is for educational purposes only and does not constitute financial advice. Options trading involves substantial risk of loss and is not suitable for all investors. The author may or may not hold positions in the securities discussed. Past performance does not guarantee future results. Always conduct your own research and consult with a qualified financial advisor before making investment decisions.

Analysis by AInvest Options Flow Intelligence | Data as of December 19, 2025