🚨 GFS: $6.1M Short Call Play on Semiconductor Giant - Bulls Betting on Cap at $40!

📅 January 6, 2026 | 🔥 EXTREMELY Unusual Activity Detected

🎯 The Quick Take

Someone just sold $6.1 MILLION worth of July calls on GlobalFoundries (GFS) - the world's fifth-largest semiconductor foundry! This massive 12,036-contract short call position suggests big money is betting GFS stays below $40 through July, with the option trade showing a z-score of 4,322 - that's 555x the average trade size! With the stock trading at $38.94 and gamma walls forming right at the $40 strike, this could be a sophisticated covered call play by a major holder, or a strategic bet that the chip sector's "elongated down cycle" continues.

💰 The Option Flow Breakdown

📊 What Just Happened

Here's the actual tape from this morning:

| Field | Details |

|---|---|

| Date | January 6, 2026 |

| Time | 10:43:54 AM ET |

| Symbol | GFS |

| Strategy | Short Call (Sell to Open) |

| Contract | GFS July 17, 2026 $40 Calls |

| Strike Price | $40.00 |

| Expiration | July 17, 2026 (193 days out) |

| Size | 12,036 contracts |

| Premium Collected | $6,100,000 ($6.1M) |

| Option Price | $5.10 per share ($510 per contract) |

| Underlying Price | $38.94 |

| Previous Open Interest | 48 contracts |

| Volume | 13,000 contracts |

| Z-Score | 4,322.21 ⚡ |

🤓 What This Actually Means

This is premium collection on steroids. Let's break it down in plain English:

🔹 The Trade: Someone sold 12,036 call options, collecting $6.1M in premium upfront. That's not your neighbor Bob's Robinhood account - this is institutional-level positioning.

🔹 The Bet: The seller profits if GFS stays below $45.10 by July expiration (the $40 strike + $5.10 premium collected). They keep the full $6.1M if GFS closes below $40.

🔹 The Context: With GFS trading at $38.94, this $40 strike is just 2.7% out of the money. The seller is basically saying "I'll take $6.1M today in exchange for capping my upside at $40."

🔹 Covered or Naked? Most likely this is a covered call - meaning they own 1.2 million shares of GFS (worth ~$47M). They're willing to sell their shares at $40 while collecting income. If it's naked, they're making a massive directional bet that requires serious margin.

🔹 Unusualness Factor: The z-score of 4,322 means this trade is 555 times larger than the typical GFS options trade. We see activity at this scale maybe a few times per year across all stocks. This isn't speculation - it's strategic positioning by someone with deep pockets.

🏢 Company Quick Facts

What GFS Does: GlobalFoundries is the world's fifth-largest semiconductor foundry - they manufacture chips designed by other companies. Think of them as the contract manufacturer for the chip industry, specializing in "mature node" technologies (older but proven chip-making processes) used in automotive, IoT, smartphones, and data centers.

By The Numbers:

- Market Cap: $21.9 billion

- Sector: Semiconductor Manufacturing/Foundry Services

- Current Price: $38.94 (as of trade time)

- 52-Week Range: $29.77 - $47.69

- Year-over-Year: Down 15.8% from $43.78

Key Context: GFS was spun out of AMD in 2009 and is now majority-owned (81.5%) by Mubadala, a UAE sovereign wealth fund. Unlike TSMC or Samsung, GFS focuses on mature nodes rather than bleeding-edge 3nm chips.

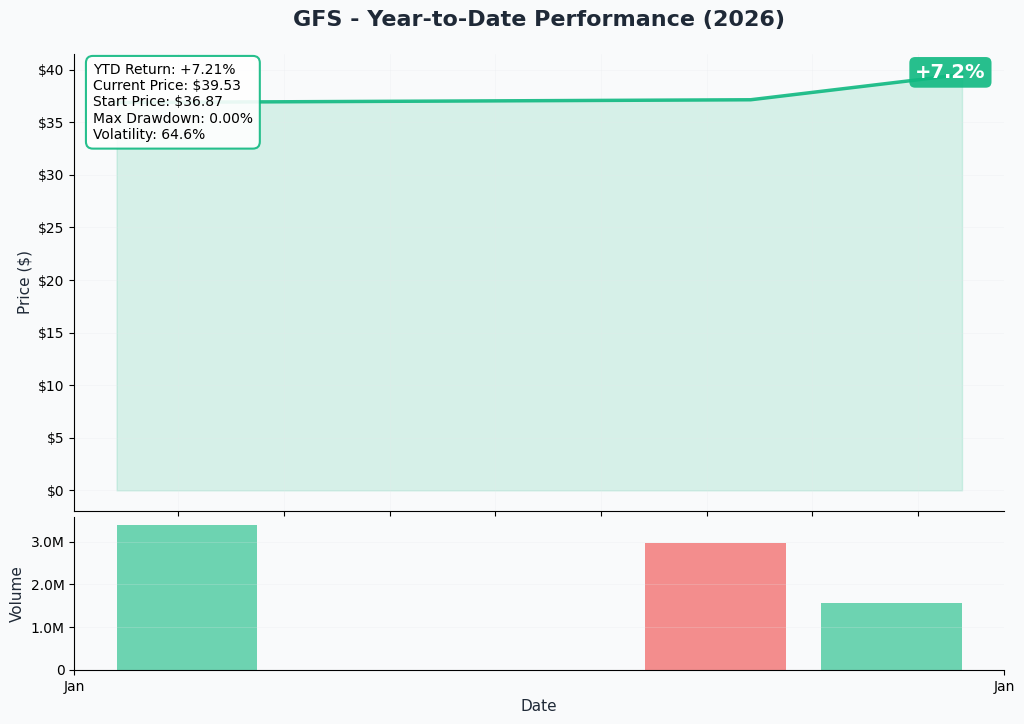

📈 Chart Check-Up

YTD Performance

The chart tells a story of struggle in 2025. After reaching $47+ in the spring, GFS has been grinding lower, recently breaking below its 50-day moving average on December 31. The stock's down about 16% year-over-year, reflecting broader weakness in the semiconductor sector. Current price around $39 sits right in the middle of the recent consolidation range.

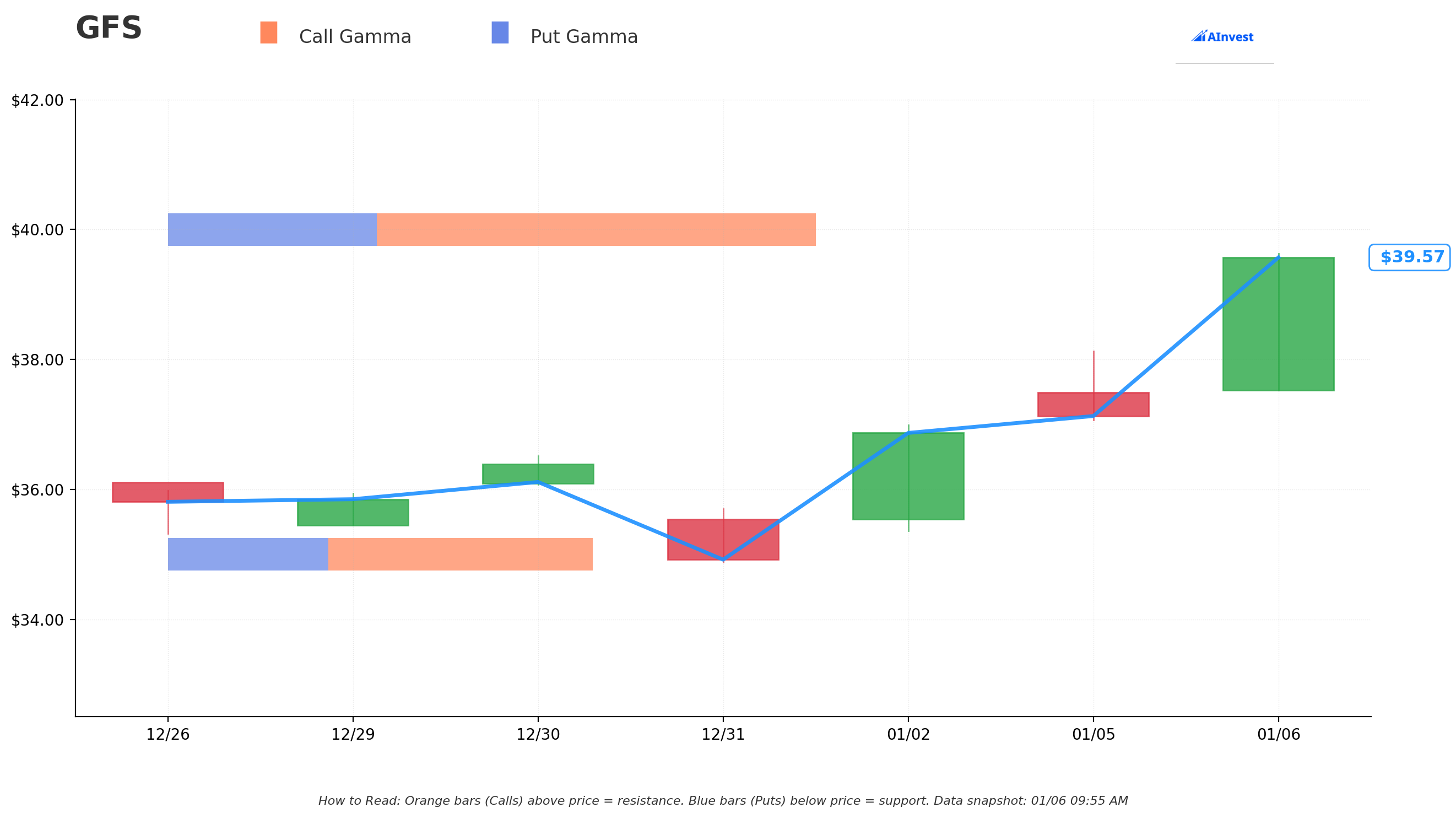

🎯 Gamma-Based Support & Resistance Analysis

The Gamma Wall Story:

Real talk - the options market is creating some fascinating price boundaries for GFS:

🔵 Support Below ($35 Strike): There's a massive 2.1 billion in total gamma sitting at the $35 level. This represents put buyers protecting downside - think of it as a trampoline that gets stronger as the stock falls toward it. If GFS tests $35, market makers hedging those puts will create natural buying pressure.

🟠 Resistance Above ($40 Strike): Here's where it gets interesting - there's 3.3 billion in gamma right at the $40 strike (exactly where our whale sold calls!). This creates a "ceiling" effect where market makers' hedging activity dampens upside momentum as the stock approaches $40. It's no coincidence that big money chose this exact strike.

🟠 Secondary Resistance ($45 Strike): Further out, there's 0.7 billion in gamma at $45, but it's much lighter than the $40 wall.

Net GEX Bias: Bullish overall, but the concentration at $40 suggests the market expects GFS to gravitate toward that level and potentially stall out there.

What This Means: The options market structure is essentially creating a "trading range" between $35 support and $40 resistance. The seller of these $6.1M in calls is betting that this $40 ceiling holds through July.

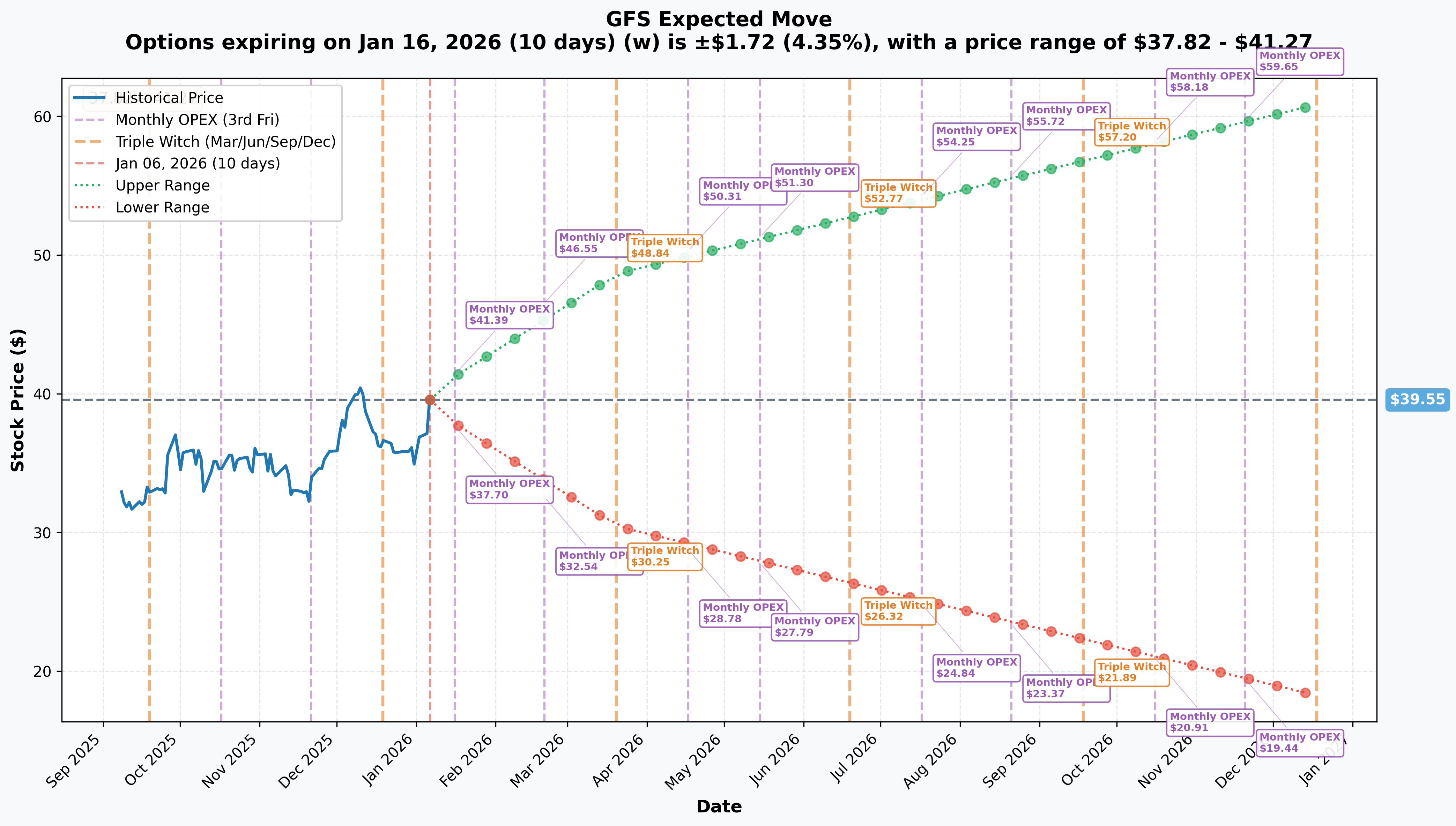

📊 Implied Move Analysis

Current Price: $39.55

The options market is pricing in some significant volatility ahead:

📅 Monthly OPEX (January 16): ±4.35% move expected

- Range: $37.82 - $41.27

- Translation: In the next 10 days, options traders expect GFS to stay in a tight ~$3.45 range

📅 Quarterly Triple Witch (March 20): ±23.05% move expected

- Range: $30.43 - $48.66

- Translation: By March (Q4 earnings will be out), the market expects potential for major movement

📅 July OPEX (July 17 - Our Trade's Expiration):

- Upper Bound: $54.25

- Lower Bound: $24.84

- Implied Range: Nearly 37% in either direction!

The Disconnect: Notice the July implied move goes all the way to $54.25 on the upside - but our seller is capping out at $40. Either they're leaving money on the table, or they don't believe in that upside scenario (more likely given recent downgrades).

🎪 Catalysts

🔮 Upcoming (Could Move the Stock)

📅 February 17, 2026 - Q4 2025 Earnings (After Close) - CONFIRMED

This is the big one. According to MarketBeat, consensus expects:

- Revenue: $1.8 billion (flat to Q3)

- EPS: $0.47 (up from $0.41 in Q3)

- Key to watch: Automotive segment trajectory, silicon photonics revenue contribution from recent acquisition

🔬 Q1 2026 - Navitas GaN Partnership Development Begins

Per GlobalFoundries' announcement, GF and Navitas are developing gallium nitride (GaN) tech for AI datacenters at the Vermont facility. Development kicks off early 2026, with production expected later this year.

🏗️ Throughout 2026 - Dresden Expansion Progress

GF's EUR 1.1 billion (~$1.27B) Dresden expansion is underway, with EUR 580 million in German state aid approved. Target: over 1 million wafers/year by end of 2028. Progress updates could provide sentiment boosts.

🤝 Ongoing - UMC Merger Speculation (Low Probability)

Bloomberg reported discussions under "Project Ultron" for a potential ~$37 billion mega-merger with Taiwan's UMC, which would create the #2 foundry globally with 9.3% market share. However, UMC has denied active talks, and regulatory hurdles are massive. Don't bet on this, but worth monitoring.

✅ Recent (Already Happened)

November 17, 2025 - Advanced Micro Foundry (AMF) Acquisition

GF acquired Singapore-based AMF, making GF the largest pure-play silicon photonics foundry by revenue. AMF will contribute >$75M initially, with GF targeting nearly $1 billion in annual silicon photonics revenue by end of decade. This is a strategic pivot toward AI datacenter markets where silicon photonics enable high-speed optical connectivity.

November 2025 - InfiniLink Acquisition

GF also acquired Egyptian startup InfiniLink, specializing in optical transceiver chiplets. This complements the AMF deal and positions GF in the AI datacenter optical connectivity space.

November 12, 2025 - Q3 2025 Earnings Beat

GF reported Q3 results that beat expectations:

- Revenue: $1.688B (vs. $1.68B expected), but down 3% YoY

- EPS: $0.44 (vs. $0.38 expected)

- Gross margin expanded to 26% (up 130 bps YoY)

- Issue: Automotive revenue down 17% sequentially, Smart Mobile Devices down 13% YoY

Recent - Analyst Downgrades Creating Headwinds

Zacks downgraded GFS to Strong Sell on January 3, citing the "elongated down cycle" in semiconductors. Wedbush also downgraded to Neutral from Outperform on December 31. Consensus among 16 analysts per The Markets Daily: Hold rating, $40.46 average price target.

🎲 Price Targets & Probabilities

Let's combine the gamma levels, implied moves, and catalyst analysis to game out three scenarios:

🐻 Bear Case ($30-35 range) - 30% Probability

Targets: Test $35 support, potentially break down to $30-32

How We Get There:

- Q4 earnings disappoint on February 17, with automotive/mobile weakness continuing

- Analyst downgrades accelerate; more firms cut to Sell

- Broader semiconductor sector selloff (if AI demand slows or macro weakens)

- The "elongated down cycle" Wedbush mentioned proves accurate

Gamma Support: The 2.1B gamma wall at $35 should provide a floor, but if that breaks, next major support is around $30 (not shown in current options structure)

Implied Move Context: July's lower bound at $24.84 seems extreme, but a move to $30-32 (-23% to -18%) is within the realm of March's quarterly implied move

Call Seller's View: They win big here, keeping the full $6.1M premium

🎯 Base Case ($35-40 range) - 50% Probability

Target: GFS consolidates in current range, gravitating toward $40 by July expiration

How We Get There:

- Q4 earnings meet expectations but don't excite (in-line with $1.8B revenue guidance)

- Silicon photonics/GaN initiatives show progress but don't materially move revenue yet

- Semiconductor cycle remains soft but doesn't deteriorate further

- Stock trades within the gamma-defined $35-40 range for next 6 months

Gamma Dynamics: This is what the options market is pricing - the concentration of gamma at $35 (support) and $40 (resistance) creates natural boundaries. As GFS approaches $40, market makers hedging will slow momentum.

Implied Move Context: The monthly and quarterly implied moves both suggest $40 is a reasonable target - January's upper bound is $41.27, March's is $48.66 (but likely front-loaded).

Call Seller's View: They still win, keeping most or all of the $6.1M. Even if GFS hits $40, they're profitable up to $45.10 (strike + premium collected).

🚀 Bull Case ($42-48 range) - 20% Probability

Targets: Break through $40 resistance, potentially reach $45-48

How We Get There:

- Q4 earnings blow out expectations with strong automotive recovery and impressive silicon photonics traction

- UMC merger talks gain traction (low probability but would be huge)

- Semiconductor cycle inflects earlier than expected

- CHIPS Act funding accelerates, creating sentiment boost

- Broader market rally lifts all semis

Gamma Challenge: The 3.3B gamma wall at $40 is a significant obstacle. Breaking through requires strong catalysts and heavy buying volume. If cleared, next resistance is $45 (0.7B gamma).

Implied Move Context: July's upper bound at $54.25 suggests the options market sees some path to explosive upside, but it's not the base case (otherwise $40 calls wouldn't be trading at just $5.10).

Call Seller's View: This is where they start to hurt. If GFS goes to $45, they're at their breakeven ($40 strike + $5.10 premium). Above $45, they're losing dollar-for-dollar (or forced to buy back shares if it's a covered call). At $48, they've given up $3 per share in gains on 1.2M shares = $3.6M opportunity cost against the $6.1M collected.

💡 Trading Ideas

🛡️ Conservative: "Fade the Fear" Put Selling

The Play: Sell the GFS March 21, 2026 $35 Put (cash-secured or as part of a spread)

Why This Works:

- You're getting paid to potentially buy GFS at $35 (10% below current price)

- The 2.1B gamma support at $35 provides technical floor

- Q4 earnings (Feb 17) will be out before March expiration, removing major event risk

- If assigned, you own GFS at an attractive entry with $1.5B in CHIPS Act funding as downside buffer

Estimated Credit: Approximately $0.80-1.20 per share ($80-120 per contract)

Max Risk: $3,500 per contract if GFS goes to zero (but you're obligated to buy at $35)

Breakeven: $35 minus premium collected (likely $33.80-34.20)

Probability of Profit: ~60-65% (based on current implied volatility)

Time Horizon: 74 days to March expiration

Best For: Investors who want to own GFS at a discount and are comfortable with the semiconductor sector's volatility

⚖️ Balanced: "Range Rider" Iron Condor

The Play: Sell the GFS July 17, 2026 $35/$32 Put Spread AND sell the July $42/$45 Call Spread

Structure:

- Sell GFS July $35 Put / Buy July $32 Put (collect ~$1.00)

- Sell GFS July $42 Call / Buy July $45 Call (collect ~$0.80)

- Net Credit: ~$1.80 per share ($180 per iron condor)

Why This Works:

- You're betting on the gamma-defined range ($35-40) holding, with some cushion

- Max profit if GFS stays between $35-42 at July expiration

- Gamma walls at $35 and $40 support your thesis

- Front-loaded time decay works in your favor

Max Profit: $180 per iron condor (if GFS between $35-42 at expiration)

Max Risk: $300 per iron condor - $180 collected = $120 net risk per condor

Breakeven Points: $33.20 (downside) and $43.80 (upside)

Probability of Profit: ~55-60%

Time Horizon: 193 days to July expiration

Best For: Traders comfortable with defined-risk, range-bound strategies who believe the semiconductor down cycle continues but GFS doesn't collapse

🚀 Aggressive: "Contrarian Catalyst" Bull Call Spread

The Play: Buy the GFS March 21, 2026 $40 Call / Sell the $45 Call

Structure:

- Buy GFS March $40 Call (~$2.50 debit)

- Sell GFS March $45 Call (~$1.00 credit)

- Net Debit: ~$1.50 per share ($150 per spread)

Why This Could Work:

- Q4 earnings (Feb 17) could surprise to the upside with silicon photonics traction

- Current pessimism (recent downgrades) may be overdone

- March quarterly implied move suggests $48.66 is possible

- Risk is capped at $150 per spread

- You're betting against the massive short call seller's thesis

Max Profit: $500 per spread ($5 spread width - $1.50 paid) = 233% ROI

Max Risk: $150 per spread (100% loss if GFS below $40 at expiration)

Breakeven: $41.50 (must rally 6.6% from current $38.94)

Probability of Profit: ~40-45%

Catalyst Dependency: Needs Q4 earnings beat on Feb 17 to have a realistic shot

Time Horizon: 74 days to March expiration (but real catalyst is Feb 17 earnings)

Best For: Aggressive traders willing to bet on a sentiment shift post-earnings, with defined risk

⚠️ Risk Factors

Let's be real about what could go wrong:

📉 Semiconductor Down Cycle Persists: Wedbush's downgrade explicitly cited an "elongated down cycle" affecting GF's mobile and IoT segments (which represent ~50% of revenue). If consumer electronics demand stays weak, GFS struggles to grow revenue.

🇨🇳 Chinese Competition Intensifies: According to foundry market share data, GFS's market share has declined from 4.6% (Q4 2024) to 3.9% (Q2 2025). Chinese fabs like SMIC are aggressively expanding mature node capacity with government subsidies, creating price pressure.

🚗 Automotive Weakness: Q3 saw automotive revenue down 17% sequentially per earnings results. If EV demand continues softening or auto OEMs manage inventory down, this key segment faces headwinds.

⚖️ Regulatory/Trade Policy Risks: GFS was fined $500K for export control violations after shipping $17.1M in wafers to a Chinese entity-list company. While the fine is small, it raises compliance concerns. Additionally, U.S.-China tech decoupling creates ongoing uncertainty.

💸 Execution Risk on Acquisitions: The AMF and InfiniLink acquisitions are strategic, but integrating them and scaling silicon photonics from 200mm to 300mm is not guaranteed. If execution stumbles, the growth thesis weakens.

📊 Analyst Sentiment Deteriorating: With recent downgrades from Zacks (to Strong Sell) and Wedbush (to Neutral), the analyst community is losing conviction. Consensus is now "Hold" with a $40.46 average target per The Markets Daily - barely above current price.

🎰 That $6.1M Call Seller Knows Something: Institutional players don't put on 555x-average-size positions without strong conviction. The fact that they're willing to cap upside at $40 (with only 2.7% cushion from current price) suggests they have insight into near-term challenges or are so confident in their covered call thesis that they're willing to sacrifice upside for income.

🎯 The Bottom Line

Real talk: This $6.1M short call position is one of the most strategically interesting trades we've seen in semiconductors recently. It's not a panic move - it's calculated income generation by someone who either owns a massive GFS position or has strong conviction that the $40 level holds through July.

For Current GFS Holders: If you own GFS, this trade should make you think about your cost basis and outlook. If you're sitting on shares bought above $40, the options market is telling you that level is a meaningful resistance ceiling for the next 6 months. Consider taking cues from this institutional player - maybe it's time to sell covered calls yourself and collect premium while you wait for the semiconductor cycle to inflect. If your cost basis is below $35, you're in good shape - the gamma support there is substantial.

For Bulls Looking to Enter: Don't fight this level of institutional conviction blindly. The $40 gamma wall is real, the analyst downgrades are fresh, and Q4 earnings could disappoint. That said, if you believe in the long-term silicon photonics/GaN thesis and want exposure, look to enter on weakness toward $35 (maybe via cash-secured puts) rather than chasing here. Or play for a post-earnings bounce in March with a bull call spread (aggressive idea above).

For Bears: You've got a huge institutional player seemingly on your side, recent downgrades providing cover, and technical resistance at $40. But be careful - GFS is not going bankrupt (81.5% owned by a sovereign wealth fund, $1.5B in CHIPS Act funding secured), and the $35 gamma support is legitimate. If you're betting on further downside, use defined-risk strategies like put spreads rather than naked shorts.

Mark Your Calendar: 📅 February 17, 2026 (After Close) - Q4 2025 Earnings. This is the catalyst that could break the current range or confirm the bear thesis. Options implied move for March suggests the market expects fireworks. Position accordingly.

The Honest Assessment: This options flow is telling us institutional players are prioritizing income over upside. They're basically saying "I'll take my $6.1M today and cap my gains at $40 because I don't see a clear catalyst to drive GFS materially higher before July." That's a cautious stance on semiconductors, and given recent macro uncertainty and the "elongated down cycle" narrative, it's hard to argue with.

Unless Q4 earnings deliver a significant positive surprise, or the UMC merger materializes (low probability), GFS likely grinds sideways to slightly down in the coming months. The risk/reward isn't compelling for aggressive bulls here - better opportunities exist in the semiconductor space with clearer catalysts.

⚠️ Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational and informational purposes only and should not be considered financial advice. Past performance is not indicative of future results. The extreme size of this trade (z-score 4,322) makes it highly unusual, but unusual does not mean profitable - it simply means large institutional positioning. Always do your own due diligence, understand your risk tolerance, and consider consulting a licensed financial advisor before making investment decisions. The author may or may not hold positions in GFS or related securities.

Analysis powered by real-time option flow data, gamma exposure modeling, and comprehensive catalyst research. For more unusual options activity alerts, visit AInvest Options Lab.