💎 GOOG Massive $6.2M Put Hedge - Institutional Defense Before Feb Earnings! 🛡️

📅 January 7, 2026 | 🔥 EXTREME Unusual Activity Detected

🎯 The Quick Take

Someone just deployed $6.2 MILLION on GOOG puts at 11:20:32 this morning! This whale purchased 5,000 contracts of ATM $320 strike puts expiring February 6th - precisely protecting a massive position ahead of Google's Q4 earnings on February 3rd. With GOOG up 65% in 2025 (best year since 2009) now trading at $320.09, this is textbook institutional portfolio insurance at peak valuations. The Z-score of 495.54 is EXTRAORDINARILY rare - we're talking once-every-few-months unusual. Translation: Smart money is buying earthquake insurance on their mansion before the storm!

📊 Company Overview

Alphabet Inc. (GOOG) is the world's dominant search and advertising powerhouse, now pivoting aggressively into AI:

- Market Cap: $3.797 Trillion (4th largest globally)

- Industry: Internet Information Providers & Search Engines

- Current Price: $320.09 (near 52-week high of $328.83)

- Primary Business: Search advertising, YouTube, Google Cloud, Android, Waymo autonomous vehicles

- 52-Week Range: $140.53 - $328.83

- P/E Ratio: 31.30 (trailing), 28.25 (forward)

💰 The Option Flow Breakdown

The Tape (January 7, 2026 @ 11:20:32):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:20:32 | GOOG | MID | BUY | PUT $320 | 2026-02-06 | $6.2M | $320 | 5,000 | 54 | 4,882 | $320.09 | $12.70 |

🤓 What This Actually Means

This is INSTITUTIONAL HEDGING AT ITS FINEST - here's the breakdown:

- 💸 Massive premium: $6.2M ($12.70 per contract × 5,000 contracts effective size)

- 🎯 ATM strike: $320 is essentially AT-THE-MONEY (current price $320.09) - maximum directional sensitivity

- ⏰ Perfect timing: 30 days to expiration captures Q4 earnings on February 3rd (after close)

- 📊 Size explosion: Volume of 5,000 vs Open Interest of just 54 = 92.593x Vol/OI ratio (EXTREME activity)

- 🏦 Z-Score off the charts: 495.54 means this is literally in the 99.99th percentile of unusual trades

- 🛡️ Strategic hedge: Represents protection for approximately 500,000 shares worth ~$160M at current price

What's really happening here: This trader almost certainly holds a GIGANTIC long position in GOOG accumulated during the historic 65% rally from $194 to $328. Now, trading at all-time valuations just 27 days before the critical Q4 earnings event, they're paying $12.70 per share for ATM puts as insurance. If GOOG drops below $320 by Feb 6th, these puts pay off dollar-for-dollar. Think of it like buying a $6.2M insurance policy when your portfolio just doubled.

Why ATM puts specifically: The $320 strike at current price gives maximum delta exposure (~0.50) - meaning these puts gain $0.50 for every $1 GOOG drops. This isn't a deep OTM "lottery ticket" - this is serious, professional downside protection expecting potential 5-15% correction.

Unusual Score: 🔥🔥🔥 EXTREME UNUSUAL (Z-Score 495.54, Vol/OI 92.593x) - This happens literally 2-3 times per year maximum! We're witnessing institutional fear manifesting in real-time. Only 54 contracts of open interest existed before this trade - now there are 5,054. This single trade IS the market at this strike.

📈 Technical Setup / Chart Analysis

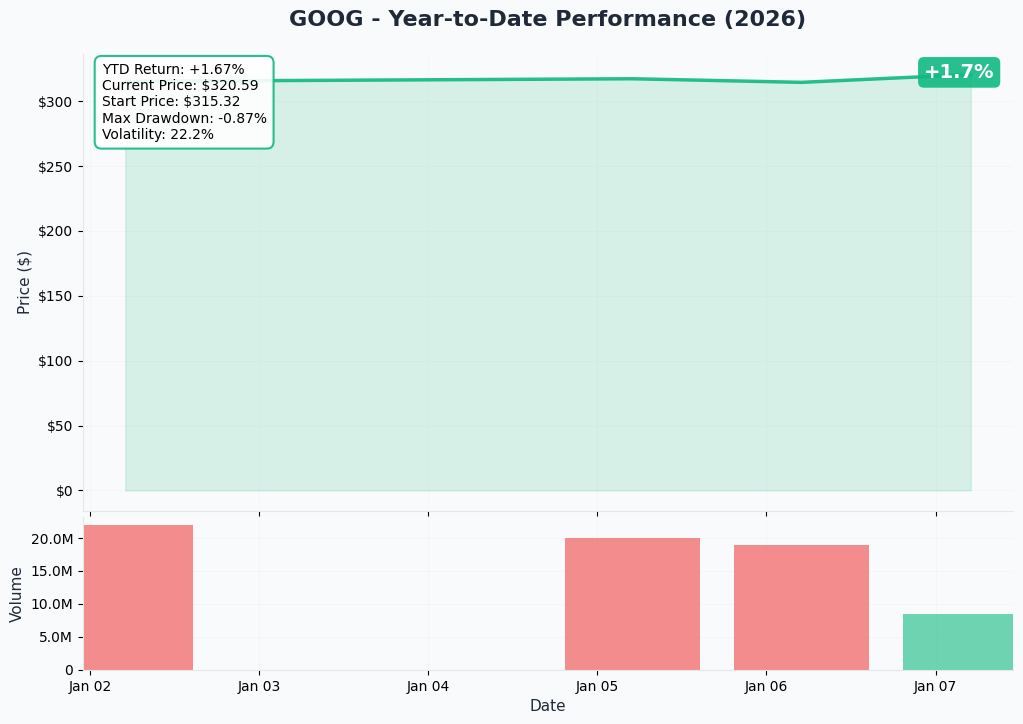

YTD Performance Chart

GOOG delivered an HISTORIC 2025 - up +65% with current price of $320.09 (started year at ~$194). This was Alphabet's best annual performance since 2009. The chart tells a powerful AI pivot story - after the favorable antitrust ruling in September (no Chrome breakup), GOOG rocketed from $250 to $328 in just 3 months.

Key observations:

- 🚀 Explosive Q4 rally: Vertical move from $280 in October to $328 highs on AI momentum and OpenAI competition narrative

- 📈 Breakout confirmed: Smashed through $280 resistance in November, accelerated into year-end

- 🎯 Multiple expansion: P/E expanded from 25x to 31x as market reprices AI opportunity

- 📊 All-time high territory: Trading within 3% of absolute peak at $328.83

- ⚠️ Overbought signals: After 65% rally, technical pullback increasingly likely even without fundamental catalyst

- 💰 Valuation concerns: At 31x P/E, GOOG now trading at premium to 5-year average (23-27x range)

Gamma-Based Support & Resistance Analysis

Current Price: $320.09

The gamma exposure map reveals critical magnetic levels where dealer hedging will accelerate price movements:

🔵 Support Levels (Put Gamma Below Price):

- $320 - IMMEDIATE FLOOR with massive gamma concentration (exactly where this put is struck!)

- $315 - Major structural support with high put gamma density

- $310 - Secondary support zone (3% below current) - critical hold level

- $305 - Extended support floor (5% drawdown)

- $300 - Psychological major support (6.3% correction) - would trigger broader selloff concerns

🟠 Resistance Levels (Call Gamma Above Price):

- $325 - Immediate ceiling with substantial call gamma (1.5% overhead)

- $330 - Secondary resistance (3% above current) - prior all-time high proximity

- $335 - Major gamma wall (5% rally needed) - would represent new all-time high breakout

- $340 - Extended upside target (6% above) - analyst consensus target cluster

What this means for traders: GOOG is trading at a CRITICAL inflection point. The put buyer struck EXACTLY at $320 where major gamma support exists - this isn't random. They're positioning at the precise level where, if broken, dealer hedging could accelerate selling pressure toward $315 then $310. The $315 level is THE line in the sand - hold here and GOOG consolidates; break it and momentum could flush toward $305-310.

Notice the setup: Massive call gamma overhead at $325-335 creates natural resistance, while the ATM $320 put gamma creates a "floor-ish" level. This screams "range-bound consolidation" into earnings unless a catalyst breaks the range either way.

Net GEX Bias: Neutral to slightly bullish (elevated call gamma overhead balanced by building put support) - Market makers positioned for sideways action with earnings volatility spike ahead.

Implied Move Analysis

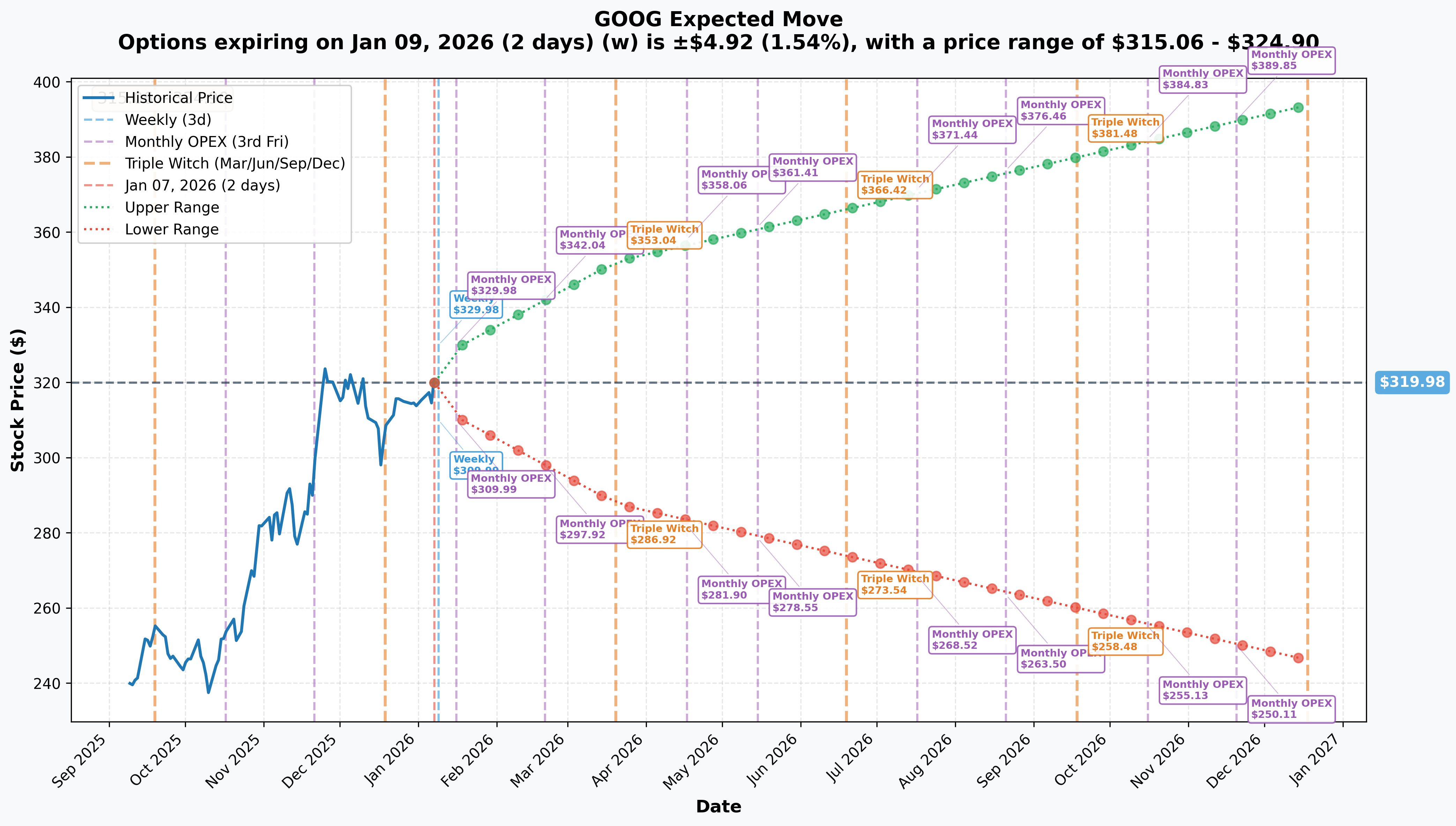

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 9 - 2 days): ±$4.92 (±1.54%) → Range: $315.06 - $324.90

- 📅 Monthly OPEX (Jan 16 - 9 days): ±$9.27 (±2.90%) → Range: $310.72 - $329.25

- 📅 February OPEX (Feb 6 - 30 days - THIS TRADE!): ~±$14.50 (±4.53%) → Range: $305.59 - $334.59 (estimated)

- 📅 Quarterly (Mar 20 - 72 days): ±$32.30 (±10.09%) → Range: $287.68 - $352.28

Translation for regular folks: Options traders are pricing in a 1.5% move ($5) by Friday for weekly expiration, but a more significant 2.9% move ($9) through monthly OPEX. However, the February 6th expiration (when this $6.2M trade expires) includes Q4 earnings on February 3rd - the market is likely pricing in a ~4.5% earnings move which represents significant volatility for a $3.8T mega-cap.

Key insight: The February implied move suggests GOOG could trade as low as $305 or as high as $335 by expiration. This perfectly brackets the catalyst: earnings could either validate the 65% rally (pushing toward $335-340) or trigger profit-taking on disappointment (dropping toward $305-310). The put buyer is protecting against the latter scenario.

Earnings volatility premium: Notice how the implied move jumps from 2.9% (Jan 16) to ~4.5% (Feb 6) - that incremental 1.6% is pure earnings uncertainty premium. Smart money recognizes this binary event risk and is paying up for protection.

🎪 Catalysts

🔥 Immediate Catalyst (27 Days Away!)

Q4 2025 Earnings - February 3, 2026 (AFTER CLOSE) 📊

GOOG reports fiscal Q4 2025 results on Monday, February 3, 2026 after market close. This is THE catalyst that will make or break this trade. Wall Street consensus and key expectations:

Revenue & Profitability Expectations:

- 📊 Total Revenue: Expected ~$95-98B (up 12-14% YoY) vs $86.3B in Q4 2024

- 💰 EPS: Consensus $2.59 - $2.63 vs $2.12 in Q4 2024 (+22% YoY growth)

- 🎯 Operating Margin: Target 33-34% (excluding one-time items)

- 💵 Free Cash Flow: Watching for $25B+ quarterly FCF to validate cash generation despite elevated CapEx

Critical Segment Metrics to Watch:

Google Search & Advertising (~$54-56B expected):

- 🔍 Search Market Share: Must defend against ChatGPT's 17% query share encroachment

- 📉 Risk Factor: YouTube ad revenue facing "tough comp" from Q4 2024 election spending (CFO explicitly warned about this)

- 🤖 AI Overviews Impact: Are ads in AI Overviews cannibalizing traditional search revenue?

- 📺 YouTube: Can it sustain $10B+ quarterly ad revenue without political tailwind?

Google Cloud (~$12-13B expected, 30-35% YoY growth):

- ☁️ Growth Sustainability: Can 34% growth rate from Q3 continue, or is deceleration inevitable?

- 💰 Profitability: Cloud operating margin expansion critical for bull case

- 🎯 AI Revenue: GenAI products revenue claimed +200% YoY in Q3 - need Q4 confirmation

- 📊 vs Competition: How does growth compare to Azure (40%) and AWS (20%)?

Other Business (~$12-14B expected):

- 🚗 Waymo Update: Any commentary on $15B funding round or path to profitability?

- 📱 Hardware: Pixel phone sales and market share trajectory

- 🎮 Play Store: Impact of Epic Games antitrust ruling on app store revenue

Guidance & Forward-Looking Commentary:

- 💸 2026 CapEx Guidance: CFO promised "significant increase" from $91-93B in 2025 - how high will it go? ($110B? $120B?)

- 🤖 AI Monetization Roadmap: Concrete metrics on AI Overviews, AI Mode revenue contribution

- 📉 YouTube Advertising: Q1 2026 outlook given tough comp from Q1 2025 political cycle

- ⚖️ Regulatory Impact: Any discussion of ad-tech antitrust trial implications

Upside Surprise Potential:

- 🚀 Cloud revenue beats $13B+ with margin expansion demonstrating operating leverage

- 🎯 Search advertising proves resilient despite ChatGPT competition - market share stabilizes

- 💰 AI Overviews/AI Mode show CLEAR monetization path with measurable revenue contribution

- 📈 2026 guidance implies revenue acceleration from AI product ramp

Downside Risk Factors:

- 😰 YouTube ad revenue misses due to election comp issue CFO already warned about

- 🚨 Search query volume declining faster than expected to ChatGPT/AI alternatives

- 💸 CapEx guidance shocks higher ($120B+) without clear ROI timeline - margin compression fears

- ⚖️ Conservative Cloud growth guidance (20-25% vs 34%) suggests competitive pressure

- 🇨🇳 China/regulatory headwinds impact outlook

- 📉 Any margin compression from aggressive AI product pricing to compete

Historical Precedent: GOOG has demonstrated 3-7% post-earnings moves on average, with larger moves (10-15%) when results significantly deviate from expectations OR when guidance surprises. After a 65% annual rally, expectations are SKY HIGH - even a "beat and raise" might not be enough if guidance disappoints.

THIS IS WHY THE PUT BUYER STRUCK HERE: February 6th expiration captures the Feb 3rd earnings event perfectly. Three days post-earnings is enough time for initial volatility to settle while still capturing the price reaction. The $320 ATM strike provides full protection if earnings disappoint and stock corrects 5-15%.

🚀 Near-Term Catalysts (Q1-Q2 2026)

Ad-Tech Antitrust Trial Remedy Decision - Mid-2026 (HIGH IMPACT) ⚖️

The second major antitrust case could materially impact Alphabet's advertising business:

Background & Status:

- 📅 Timeline: Closing arguments concluded November 2025; Judge Brinkema's remedy decision expected April-June 2026

- 💰 Revenue at Risk: AdX (ad exchange) and Google Ads platform generate estimated $60-80B annually - core profit centers

- 🎯 DOJ Request: Forced divestiture of AdX and open-sourcing of auction logic to create competition

- 🛡️ Google Defense: Arguing divestiture would be "incredibly complex," hurt publishers and advertisers, and lack willing buyers

Judge's Signaling:

- 🤔 Skepticism of Breakup: Judge Brinkema expressed doubts about structural remedies, questioning who would buy AdX

- ⚖️ Conduct Remedies Favored: Likely outcome appears to be behavioral restrictions rather than forced sale

- 📊 Monitoring Requirement: Could mandate third-party oversight of ad auction mechanics and pricing

Possible Outcomes & Probabilities:

Scenario 1: Light Conduct Remedies (50% probability)

- 📋 Interoperability requirements allowing competitor access to some Google Ads data

- 👁️ Independent monitoring of ad auction fairness for 5-7 years

- 🚫 Ban on certain anti-competitive bundling practices

- Impact: Minimal to modest (1-3% revenue headwind) - stock rallies 3-5% on relief

Scenario 2: Heavy Behavioral Restrictions (35% probability)

- 📊 Mandatory revenue sharing with competitors accessing Google's ad network

- 🔓 Open-sourcing of significant portions of auction logic

- 💰 Pricing restrictions on AdX fees and margins

- Impact: Moderate (5-8% revenue/margin headwind) - stock drops 5-10% on concern

Scenario 3: Forced Divestiture (15% probability)

- 🏢 Required sale of AdX to independent buyer within 12-18 months

- 💸 Loss of $15-25B annual high-margin revenue stream

- 🔗 Disruption to integrated advertising ecosystem

- Impact: Severe (10-15% revenue hit, margin compression) - stock drops 15-20%+

Why This Matters for the Put Trade: If Judge Brinkema signals severe remedies or divestiture in spring 2026, it could trigger a major selloff AFTER the February put expiration. However, any preliminary leaks or analyst speculation in late January could impact stock before Feb 6th expiration. The put buyer may be factoring in this tail risk.

Analyst Views: Most analysts assign 40-50% probability to material behavioral remedies with only 15-25% probability of forced divestiture based on judge's expressed skepticism. However, the uncertainty itself creates an overhang on valuation.

ChatGPT Search Competition Intensification 🤖

The existential threat to Google's search monopoly continues escalating:

Current Market Share Battle:

- 🔍 Google Search: Dipped below 90% for most of 2025 (first time since 2015), now at ~78% of global queries

- 💬 ChatGPT: Now captures 17% of global search queries (up from single digits in 2024) - growing rapidly

- 🎯 User Behavior Shift: ChatGPT average session 14+ minutes vs Google 5 minutes - deeper engagement

- 📊 Demographics: Younger users (18-34) preferring conversational AI over traditional search

Google's Counter-Offensive:

- 🚀 Gemini Growth: Tripled AI chatbot market share from 5.4% to 18.2% in 2025 (catching up fast!)

- 🎯 AI Overviews: Now 2 billion monthly users, 10% of global search queries use AI-enhanced results

- 💡 AI Mode: 100 million MAU in just 2 months (launched Q4 2025) - impressive adoption

- 🔧 Gemini 3 Flash & Deep Think: December 2025 model releases dramatically improved competitive positioning

2026 Projections:

- 📈 Analysts expect Gemini could reach 25-30% AI chatbot share by year-end 2026

- 📉 ChatGPT may decline from 68% to 55-60% share as competition intensifies

- ⚖️ Traditional Google Search could stabilize at 75-80% but query volume mix shifts toward AI products

- 💰 Critical Question: Can Google monetize AI Mode/Overviews at similar rates to traditional search?

Revenue Impact Timeline:

- Q1-Q2 2026: Transition friction as users shift from high-monetization search to lower-monetization AI products

- H2 2026: AI product monetization improves as ad formats mature (ads in AI Overviews, AI Mode sponsorships)

- 2027: New equilibrium with diversified revenue streams across traditional search + AI products

Risks:

- 🚨 If query volume shifts faster than monetization ramps, revenue growth could decelerate materially

- 💸 Pricing pressure to compete with free ChatGPT could compress margins

- 🎯 Enterprise search deals at risk if businesses adopt ChatGPT Enterprise

Opportunities:

- 🌟 AI Overviews show +35% organic CTR and +91% paid CTR for cited brands - better engagement than traditional

- 💰 Early ads in AI Overviews performing well, suggesting monetization path viable

- 🔧 Gemini's rapid market share gains prove Google can compete effectively

Waymo Funding Round & Profitability Path 🚗

Google's autonomous vehicle subsidiary approaches major inflection:

Current Status (January 2026):

- 💰 Planned Raise: $15+ billion at $100-110 billion valuation (doubling from prior round)

- 📊 Revenue Run Rate: $350 million annually (December 2025) - still subscale

- 🚖 Operational Metrics: 450,000 paid rides/week; targeting 1 million/week by end of 2026

- 🌍 Markets: Operating in San Francisco, Los Angeles, Phoenix; expanding to Austin, Atlanta

Path to Profitability:

- 📅 CFO Guidance: Expects "meaningful" Waymo contribution to Alphabet financials by 2027

- 🎯 CEO Timeline: Sundar Pichai targets 2027-28 timeframe for material profit contribution

- 💸 Burn Rate: Currently losing ~$1-2B annually on development and operations

- 🚀 Inflection Point: Needs 2-3 million rides/week at higher utilization to approach breakeven

Investment Thesis:

- 🌟 Option Value: At $100B valuation, Waymo represents ~2.5% of Alphabet's market cap - asymmetric upside if autonomous vehicles scale

- 🏆 Technology Lead: Waymo widely considered 2-3 years ahead of Tesla, Cruise in autonomous capability

- 📈 TAM: Ride-hail + logistics market worth $2-3 trillion globally - even 5% share = $100-150B revenue opportunity

Risks:

- ⏰ Profitability timeline keeps slipping (previously projected 2025, now 2027-28)

- 💸 Requires continuous capital infusion - $15B raise dilutes Other Bets already consuming cash

- 🚧 Regulatory hurdles in new markets slowing expansion

- 🔥 Competition from Tesla FSD, Chinese players intensifying

Capital Expenditure Escalation Through 2026 💰

The AI infrastructure arms race continues accelerating:

2025 Actuals & 2026 Guidance:

- 💸 2025 CapEx: $91-93 billion (revised upward THREE times during year) - mostly AI infrastructure

- 📈 2026 Guidance: CFO Ashkenazi promises "significant increase" from 2025 levels

- 🎯 Analyst Estimates: Expecting $105-120B in 2026 (15-30% increase) for GPUs, TPUs, data centers

- 🌍 Industry Context: Hyperscaler total CapEx forecast to exceed $600B in 2026 (+36% YoY across MSFT, AMZN, GOOGL, META)

Investment Breakdown:

- 🤖 AI Infrastructure: ~75% of spend (GPUs, TPUs, data center build-out for AI training/inference)

- ☁️ Cloud Capacity: ~15% for Google Cloud geographic expansion and compute capacity

- 🏢 Other: ~10% for offices, Waymo, hardware R&D

Bull Case on CapEx:

- 🚀 Required investment to compete with Microsoft/OpenAI and maintain competitive positioning

- 💰 Cloud revenue growing 34% YoY - infrastructure spend directly enables revenue growth

- 📊 AI products revenue +200% YoY - CapEx powering fastest-growing business lines

- ⚡ Operating leverage will emerge 2027-28 as revenue scales faster than CapEx needs

Bear Case on CapEx:

- 😰 No clear ROI timeline - spending $100B+ annually with uncertain payback period

- 📉 If AI monetization disappoints, this becomes massive capital misallocation

- 💸 Free cash flow compression - CapEx rising faster than operating cash flow growth

- 🏆 Arms race with no winner - hyperscalers collectively overspending for limited market

Impact on Valuation: At 31x forward P/E, investors are implicitly assuming CapEx spending yields strong returns. If 2026 guidance comes in at $120B (upper end) WITHOUT concrete AI revenue metrics, stock could sell off 5-10% on "spending without returns" narrative. Conversely, if management articulates clear ROI path, elevated CapEx validates growth investment thesis.

⚠️ Risk Catalysts (Negative)

Search Antitrust Case Appeal & Uncertainty 🏛️

While September 2025 ruling was favorable (no Chrome breakup), ongoing appeals create uncertainty:

- 📅 Appeal Timeline: Google appealing liability decision; DOJ may appeal remedy aspects - could extend through 2027

- 🎯 Data Sharing Requirements: Google must share search data with "Qualified Competitors" - execution unclear

- 💰 Revenue Impact: Loss of exclusive distribution contracts (Apple, Samsung, Mozilla) worth estimated $20-30B annually

- ⚖️ Ongoing Compliance Costs: Monitoring, reporting, and system changes required for 10-year remedy period

Privacy Regulations & Advertising Headwinds 🔒

Evolving privacy landscape threatens advertising model:

- 🇪🇺 EU Regulations: GDPR enforcement intensifying, DMA (Digital Markets Act) requiring data portability

- 🇺🇸 U.S. State Laws: California, Virginia, Colorado privacy laws limiting data collection

- 🍪 Cookie Deprecation: Third-party cookie phase-out creating targeting challenges (delayed multiple times)

- 📊 Impact: Reduced ad targeting precision could lower ad prices and revenue per query

Macroeconomic Headwinds 📉

2026 macro environment poses challenges:

- 📈 Inflation Persistence: Expected to remain 3% vs 2% Fed target - consumption pressure

- 💸 Consumer Weakness: Affordability concerns could reduce discretionary spending and ad budgets

- 🏛️ Tariff Impact: Retail prices up ~5% from pre-tariff trend - dominant macro theme

- 📊 Ad Budget Cuts: Economic uncertainty typically causes advertisers to reduce spending first

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst analysis, here are scenarios through February 6th expiration:

📈 Bull Case (30% probability)

Target: $340-$360

How we get there:

- 💪 Earnings DEMOLISH expectations - revenue $98-100B (high end), EPS beats by $0.10-0.15

- 🎯 YouTube ad revenue actually grows despite election comp (CEO narrative was too conservative)

- ☁️ Google Cloud revenue $13B+ with margin expansion - proves operating leverage

- 🤖 AI Overviews/AI Mode monetization metrics EXCEED expectations - clear revenue contribution path

- 📊 Search market share stabilizes at 78-80% - ChatGPT threat contained by Gemini counter

- 💰 2026 CapEx guidance $100-105B (lower than feared) with articulated ROI timeline

- 🌍 Waymo funding round closes at $110B+ valuation - validates hidden asset value

- ⚖️ Ad-tech trial commentary suggests light remedies likely (no divestiture risk)

- 📈 Breakout above $325-330 gamma resistance triggers momentum chase to $340-350

Key metrics needed:

- Total revenue >$97B (vs $95B consensus)

- Cloud growth sustains 30%+ with improving margins

- Operating margin 34%+ (excluding one-times)

- Concrete AI monetization metrics (not just "strong momentum")

Probability assessment: 30% because it requires strong execution across ALL segments after 65% YTD rally at 31x P/E. Gamma resistance at $325-335 creates mechanical selling pressure. Elevated expectations from analyst upgrades (consensus $340 targets).

🎯 Base Case (45% probability)

Target: $305-$325 range (CONSOLIDATION)

Most likely scenario:

- ✅ Solid earnings meeting consensus - revenue $95-96B, EPS $2.60-2.65 (in-line)

- 📱 YouTube ad revenue slightly soft as warned but not disastrous - down 2-5% YoY

- ☁️ Cloud growth decelerates to 28-30% but remains healthy - in-line with expectations

- 🤖 AI metrics positive but not game-changing - incremental progress narrative

- 💸 2026 CapEx guidance $110-115B (significant increase as telegraphed) - investors shrug

- 📊 Search share stable but no improvement - ChatGPT competition ongoing concern

- 🔄 Trading within gamma support ($310-315) and resistance ($325-330) bands for weeks

- 💤 Post-earnings volatility crush (IV from 45% to 25-30%) as uncertainty resolves

- ⚖️ No major surprises either way - market digests results and waits for next catalyst

This is the put buyer's ACCEPTABLE scenario: Stock consolidates $310-320 range, puts expire worthless or minimal value ($5-10 per contract), but downside protection served purpose during earnings binary event. The $6.2M was simply insurance premium for peace of mind protecting much larger long position.

Why 45% probability: Most likely outcome for mega-cap with strong fundamentals but elevated valuation after huge rally. Neither catalyst for major breakout nor major breakdown. Investors want to see Q1 2026 results to confirm AI momentum before re-rating higher.

📉 Bear Case (25% probability)

Target: $280-$305 (TEST THE PUT STRIKE!)

What could go wrong:

- 😰 Earnings miss OR weak guidance disappoints - revenue $93-94B (below $95B consensus) and/or conservative Q1 outlook

- 🚨 YouTube ad revenue down 8-12% YoY (worse than expected) - validates competition concerns

- 📉 Cloud growth decelerates to 20-25% - loses momentum narrative to Azure/AWS

- 💸 2026 CapEx guidance $120-130B (extreme) without clear ROI articulation - FCF compression fears

- 🤖 AI monetization metrics vague or disappointing - can't quantify revenue contribution

- 🔍 Search query volume showing accelerating decline to ChatGPT - market share trajectory worsening

- ⚖️ Ad-tech trial commentary suggests harsher remedies possible - AdX divestiture back on table

- 💰 Margin compression from aggressive AI product pricing to compete

- 🌍 Broader tech selloff drags semis/mega-caps lower (rotation, recession fears, Fed policy)

- 🔨 Break below $315 gamma support triggers cascade to $310, then $305, potentially $300

Critical support levels:

- 🛡️ $315: Major gamma floor - MUST HOLD or momentum shifts bearish

- 🛡️ $310: Secondary support with substantial put gamma - likely heavy buying here

- 🛡️ $305: Extended floor (4.7% correction) - psychological level

- 🛡️ $300: Disaster scenario (6.3% drop) - breaks YTD uptrend, triggers institutional selling

Catalyst combinations: Most likely requires MULTIPLE disappointments:

- Earnings miss + weak guidance + high CapEx = -8-12% drop

- YouTube revenue collapse + Search share loss = -10-15% drop

- Ad-tech trial concerns + macro selloff = -7-10% drop

Probability assessment: 25% because requires several negatives to align simultaneously. Google's fundamentals remain strong (Cloud growth, AI positioning, fortress balance sheet), but valuation at 31x P/E offers minimal cushion. The put buyer clearly believes this scenario has >25% probability or they wouldn't pay $6.2M for protection.

Put P&L in Bear Case:

- Stock at $305 on Feb 6: Puts worth $15.00, profit = $2.30/share × 5,000 = $1.15M gain (18% ROI)

- Stock at $295 on Feb 6: Puts worth $25.00, profit = $12.30/share × 5,000 = $6.15M gain (99% ROI!)

- Stock at $280 on Feb 6: Puts worth $40.00, profit = $27.30/share × 5,000 = $13.65M gain (220% ROI!)

- Stock at $320 on Feb 6: Puts worth $0 (at-the-money), loss = -$12.70/share × 5,000 = -$6.35M (102% loss)

💡 Trading Ideas

🛡️ Conservative: Trim & Wait for Earnings Clarity

Play: If you own GOOG, take partial profits at $318-325; if sidelined, wait for post-earnings entry

Why this works:

- ✅ Lock in gains after historic 65% rally - you've already WON big if you owned GOOG in 2025

- ⏰ Earnings in 27 days creates binary event risk with ~4.5% implied move - too unpredictable

- 💸 Implied volatility elevated pre-earnings - options expensive, better to wait for IV crush

- 📊 Stock at all-time valuations (31x P/E, near $328 highs) - zero margin of safety at current level

- 🎯 Better entry likely post-earnings after volatility settles, even if stock rises (pullback opportunities)

- 🤔 $6.2M institutional put buy signals smart money is WORRIED about near-term - respect the signal

Action plan if you OWN GOOG:

- 💰 Sell 25-35% of position at $318-325 range - lock in meaningful profits from 65% rally

- 🎯 Keep core 65-75% for long-term AI thesis exposure

- 📊 Set mental stop at $310 (gamma support) to protect remaining position if earnings disappoint

- ⏰ If earnings beat AND stock breaks $330, consider re-entering trimmed shares on momentum

Action plan if you're WATCHING (no position):

- 👀 Wait for February 3rd earnings volatility to settle (2-3 days post-earnings minimum)

- 🎯 Look for pullback to $305-315 support zone for entry with 5-10% margin of safety

- ✅ Need to see: Cloud revenue $13B+, Search stabilization, concrete AI monetization metrics

- ❌ Avoid if: YouTube revenue craters, Cloud decelerates sharply, CapEx guidance extreme without ROI path

Risk level: Minimal (reducing exposure/staying in cash) | Skill level: Beginner-friendly

Expected outcome: Avoid potential 8-15% drawdown if earnings disappoint while maintaining upside optionality. If earnings beat, can re-enter at slightly higher prices with more confidence. Peace of mind worth missing 5% additional upside.

⚖️ Balanced: Post-Earnings Put Spread (Copy Smart Money)

Play: After earnings settles, replicate institutional hedging at better prices

Structure: Buy $315 puts, Sell $305 puts (March expiration - extends beyond Feb trade)

Why this works:

- 🎢 IV crush after earnings makes put spreads much cheaper - buy AFTER volatility drops from 45% to ~25-30%

- 📊 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 🎯 Targets gamma support zone at $305-315 where technical support exists

- 🤝 Essentially "copying" the smart money positioning but at 40-50% cheaper cost post-IV crush

- ⏰ March expiration gives time for any ad-tech trial developments or Q1 2026 outlook weakness

- 🛡️ Protects against "sell the news" scenario even if earnings beat (profit-taking after 65% rally)

- ⚖️ Ad-tech trial remedy decision risk (Apr-Jun) starts being priced in during March timeframe

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Pay ~$3.50-4.50 net debit per spread post-earnings (vs $6-7 now due to IV crush)

- 📈 Max profit: $550-650 if GOOG below $305 at March expiration (spread worth $10)

- 📉 Max loss: $350-450 if GOOG above $315 (lose entire debit paid)

- 🎯 Breakeven: ~$311-312 (strike minus debit paid)

- 📊 Risk/Reward: ~1.3:1 to 1.5:1 which is acceptable for defined-risk bearish play

Entry timing:

- ⏰ Wait 2-4 days post-earnings (by Feb 6-9) for FULL IV collapse

- 🎯 Only enter if stock trading $318+ (gives room for spread to work)

- ❌ Skip if stock already below $312 (spread too close to at-the-money, poor risk/reward)

Position sizing: Risk only 3-7% of portfolio (this is directional speculation on consolidation/weakness, not core holding)

Scenarios:

- Win: Stock consolidates/drifts to $308-310 by March → spread worth $5-7 → 40-80% gain

- Big win: Stock breaks down to $300-305 → spread worth $10 → 120-150% gain

- Loss: Stock rallies to $330+ → spread expires worthless → lose $350-450 per spread

Risk level: Moderate (defined risk, bearish directional) | Skill level: Intermediate

Probability of profit: ~40-45% (factoring in post-earnings momentum and gamma support at $315)

🚀 Aggressive: Earnings Straddle - Bet on MASSIVE Movement (EXPERT ONLY!)

Play: Buy straddle betting post-earnings volatility exceeds 4.5% implied move

Structure: Buy $320 calls + Buy $320 puts (Feb 20 expiration - 2 weeks post-earnings)

Why this could work:

- 💥 Implied move only 4.5% ($14-15) but GOOG could move 6-10% on earnings surprise given elevated expectations

- 🎰 Betting the Street is UNDERPRICING the risk/opportunity of YouTube revenue miss OR Cloud revenue beat

- 📊 At 31x P/E after 65% rally, stock is coiled spring - could EXPLODE either direction

- 🚀 ChatGPT competition narrative + AI monetization uncertainty = binary outcomes possible

- ⚡ Only need stock to move >5-6% either way to potentially profit

- 🤖 Multiple unknown variables: YouTube comp, Cloud growth, CapEx guidance, Search trajectory, AI metrics

Why this could BLOW UP (SERIOUS RISKS - READ THIS!):

- 💸 EXTREMELY EXPENSIVE: Straddle costs ~$22-28 ($2,200-2,800 per straddle at current IV)

- ⏰ TIME DECAY MASSACRE: Theta burns -$80-120/day as earnings approaches

- 😱 IV CRUSH DEVASTATION: Even if stock moves 4-5%, IV collapse from 45% to 25% could result in LOSS on both legs

- 📊 Two-way obliteration risk: Stock could stay in $310-330 range and you lose 50-80% of premium

- 🎢 Need 6-7%+ move to breakeven AFTER factoring in IV crush impact

- ⚠️ Earnings could be "fine" - stock gaps to $328-330 (only 3% move) and straddle loses 40-60%

- 💀 Most straddle buyers LOSE MONEY even when they're right on direction due to IV crush mechanics

Estimated P&L:

- 💰 Cost: ~$24-26 per straddle (using Feb 20 expiration to capture earnings + multi-day settle)

- 📈 Profit scenario: Stock moves to $345+ or $295- (7-8%+ move) = $20-25 gain (80-100% ROI)

- 🚀 Home run: Stock moves to $360 or $280 (12-13%+ move) = $40+ gain (155%+ ROI)

- 📉 Loss scenario: Stock ends $310-330 range = lose $12-20 (50-80% loss)

- 💀 Total loss: Stock flat at $320 = lose entire $24-26 (100% loss)

Breakeven points (accounting for IV crush):

- 📈 Upside breakeven: ~$346-348 (need 8-9% rally)

- 📉 Downside breakeven: ~$292-294 (need 8-9% drop)

CRITICAL WARNINGS - DO NOT ATTEMPT UNLESS:

- ✅ You've traded earnings straddles before and UNDERSTAND IV crush mechanics deeply

- ✅ You can afford to lose ENTIRE premium (very real possibility - happens to 60-70% of straddle buyers!)

- ✅ You understand you're betting AGAINST the options market's probability estimate

- ✅ You can monitor position night of earnings (Feb 3 after close) and take profits QUICKLY next morning

- ✅ You accept that being RIGHT on direction doesn't guarantee profit due to IV crush

- ✅ You have plan to close within 24-48 hours post-earnings (NEVER hold straddles to expiration!)

- ✅ You've calculated your breakeven INCLUDING IV crush impact (not just strike +/- premium)

Advanced technique (reduce cost):

- Consider Iron Condor instead: Sell $340 call / $300 put against the straddle

- Reduces cost to $16-18 but caps gains if move exceeds $340 or drops below $300

- Better risk/reward if you expect 5-8% move but not 10%+ explosion

Risk level: EXTREME (can lose 100% of premium easily) | Skill level: Expert only

Probability of profit: ~35-40% (LOWER than 50% due to IV crush headwinds - you need bigger move than implied)

If you INSIST on doing this: Use only 1-2% of portfolio max, set profit target of 40-50% and TAKE IT immediately, set stop loss of 40% and CUT IT quickly. Do NOT hope/pray/hold if position goes against you.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Earnings binary event in 27 days: Results Monday February 3rd after close create MASSIVE uncertainty. Stock could gap 5-12% either direction based on revenue ($95B vs $98B huge difference), YouTube ad revenue (election comp issue), Cloud growth trajectory (30%+ vs <25% changes narrative), and 2026 CapEx guidance ($110B vs $120B vastly different implications). Historical precedent shows GOOG moves 3-7% on earnings with larger moves (10%+) when guidance surprises. This is THE catalyst that makes or breaks near-term.

-

💸 Valuation at 15-year highs: Trading at 31.30x trailing P/E and 28.25x forward P/E (vs 10-year average of 23-27x) after 65% rally. Stock is priced for PERFECT AI execution - requires Cloud sustaining 30%+ growth, Search stabilizing despite ChatGPT, and AI products monetizing successfully. ANY disappointment magnified 2-3x at this valuation. Zero margin of safety for errors. Multiple compression from 31x to 25x alone would drop stock to $260-270 even if fundamentals stay strong.

-

⚖️ Ad-tech antitrust trial wildcard (mid-2026): Judge Brinkema's remedy decision expected April-June could force AdX divestiture ($15-25B annual revenue at risk) or heavy behavioral restrictions (5-8% revenue headwind). While most analysts expect light remedies (50% probability), 15-25% probability of forced divestiture creates tail risk. Any preliminary signals or analyst speculation in Jan-Feb could impact stock. DOJ's aggressive stance (requested full breakup) shows they're not backing down. Judge's final decision appeals could extend through 2027-28 creating ongoing overhang.

-

🤖 ChatGPT search competition accelerating: Google Search share dropped below 90% in 2025 for first time since 2015, now at 78% with ChatGPT capturing 17% of queries. This is EXISTENTIAL threat to $180B+ annual search revenue (58% of total). User behavior shifting - younger demographics preferring conversational AI (14+ min avg session) vs traditional search (5 min). If query volume shift accelerates faster than Google can monetize AI Overviews/AI Mode, revenue growth decelerates materially in 2026. Gemini's gains (5% to 18% chatbot share) encouraging but ChatGPT still dominates at 68%. Race is ON and outcome uncertain.

-

💰 YouTube advertising facing "tough comp" - CFO pre-announced: Management EXPLICITLY warned Q4 2025 YouTube ad revenue "will be negatively impacted by the strong spend on US elections in the fourth quarter of 2024." This is basically pre-announcing a YouTube revenue miss or deceleration. If YouTube (normally $10-11B quarterly) drops to $8-9B, it could trigger 5-8% selloff even if other segments beat. Q1 2026 faces same comp issue (election cycle). This is known headwind but magnitude unknown - could be -3-5% or could be -10-15%.

-

💸 CapEx escalation without clear ROI timeline: Spent $91-93B in 2025 (revised up 3x), CFO promises "significant increase" in 2026 likely meaning $110-130B. That's $200-220B cumulative over 2 years on AI infrastructure with uncertain payback. If 2026 guidance comes in at $120-130B (high end) WITHOUT concrete metrics showing AI revenue ramp, market could punish stock 8-12% on "spending without returns" narrative. Free cash flow compression risk - CapEx rising faster than operating cash flow growth. Bull case requires this investment yielding strong returns by 2027-28, but what if AI monetization disappoints? Then it's massive capital misallocation.

-

🏦 Institutional put buying at ATM = fear signal: When sophisticated funds managing billions pay $6.2M for ATM puts 27 days before earnings rather than staying fully long, it's MAJOR caution flag. Z-score of 495.54 means this is 99.99th percentile unusual - happens 2-3 times per year max. They're not speculating on collapse - they're protecting HUGE gains from 65% rally. The choice of ATM $320 strike (vs OTM $300 or $310) shows they expect meaningful probability of 5-10% correction, not just tail risk hedging. When smart money pays 4% of stock price for 30-day protection, retail should pay attention.

-

📊 Gamma ceiling at $325-335 creates mechanical resistance: Substantial call gamma concentration at $325 (immediate resistance) and $330-335 (major resistance) means market makers will systematically SELL into rallies to hedge their exposure. This creates mechanical selling pressure making breakouts difficult even on good news. Would need massive institutional buying flow to overcome. Current price ($320) sitting just below this ceiling - multiple attempts to break $325 have failed in past 2 weeks.

-

🌍 Macroeconomic headwinds building for 2026: Inflation persistence near 3% (vs 2% target), consumer affordability pressure, tariff impact on retail prices (+5%), potential recession signals. In economic uncertainty, advertising budgets get cut FIRST - both for brand advertising and performance marketing. If economy weakens materially in H1 2026, even strong execution won't save GOOG from 15-25% correction back to $250-270 range as ad revenue growth decelerates. Cyclical exposure underappreciated at current valuation.

-

🔒 Privacy regulations tightening globally: EU GDPR enforcement intensifying, DMA requiring data portability, U.S. state laws (CA, VA, CO) limiting data collection. Third-party cookie deprecation (delayed repeatedly but coming) will reduce ad targeting precision. Impact: Lower CPMs, reduced conversion rates, advertiser ROI declining = pressure on Google's ad pricing power. Could be 2-5% revenue headwind emerging 2026-27 as regulations bite.

-

⚡ AI monetization still UNPROVEN at scale: While AI Overviews have 2B users and AI Mode hit 100M MAU quickly, CONCRETE revenue contribution still unclear. Can Google monetize AI Mode at $X per query comparable to traditional search? Ads in AI Overviews performing well early but sample size small. What if AI cannibalization (users shifting from high-monetization search to low-monetization AI products) outpaces new AI monetization? Revenue growth could stall even as user engagement increases. This is THE critical unknown for 2026-27.

-

🎢 Post-rally exhaustion risk: After 65% YTD gain (best since 2009), GOOG has run HARD into year-end. Technical indicators likely overbought, investor positioning heavily long, sentiment extremely bullish. These setups OFTEN result in 5-15% correction on any disappointment as profit-taking cascades. Even without fundamental catalyst, market structure itself creates downside risk. "Buy the rumor (AI pivot), sell the news (earnings results)" is classic pattern.

🎯 The Bottom Line

Real talk: Someone just spent $6.2 MILLION on ATM puts 27 days before GOOG's most important earnings report in years. This isn't bearish on Google's 5-10 year AI story - it's sophisticated risk management by institutions who've made MASSIVE money on the historic 65% rally and refuse to give it back in one bad earnings print.

What this trade tells us:

- 🎯 Sophisticated player expects MATERIAL VOLATILITY through early February (not crash, but protecting against 8-15% downside scenario)

- 💰 They're worried enough about $320→$305-310 move to pay $12.70/share for insurance (4% of stock price!)

- ⚖️ The timing (27 days pre-earnings) shows they see BINARY RISK - earnings could go either way with massive implications

- 📊 They struck at $320 ATM (not $300 or $310 OTM) - expects that IF stock breaks, it happens FAST and significantly

- ⏰ February 6th expiration captures Feb 3rd earnings perfectly - three days post-earnings for initial volatility to settle

- 🏦 Z-score 495.54 is UNPRECEDENTED - this is 99.99th percentile unusual, happens maybe quarterly across all stocks

This is NOT a "sell everything and run" signal - it's a "take some profits, manage risk, and don't be a hero into earnings" signal.

If you own GOOG:

- ✅ STRONGLY consider trimming 25-40% at $318-325 levels (you've already made 65%+ gains - PROTECT THEM!)

- 📊 If holding through earnings, set HARD MENTAL STOP at $310 (gamma support) - don't hope/pray if it breaks

- ⏰ You've already won BIG. Up 65% YTD is PHENOMENAL. Smart money locks in gains, doesn't get greedy.

- 🎯 If earnings beat AND stock breaks $330 with momentum, can re-enter trimmed shares at $332-335 on confirmation

- 🛡️ Consider buying 1-3 protective puts per 100 shares if holding large position (copy this trade's structure scaled to your size)

- 💰 Profits aren't real until you TAKE them - don't let one earnings report wipe out a year's gains

If you're watching from sidelines:

- ⏰ DO NOT enter before February 3rd earnings - binary event risk too high at current valuation

- 🎯 Post-earnings pullback to $305-315 would be EXCELLENT entry (5-10% off highs with gamma support and earnings clarity)

- 📈 Looking for confirmation: Cloud revenue $13B+ (30%+ growth sustained), YouTube revenue not crater (only down 3-5% on comp), AI monetization metrics concrete (not vague "momentum"), 2026 CapEx $100-110B (not $120B+)

- 🚀 Longer-term (12-18 months), Google's AI positioning, Cloud growth, Waymo optionality are legitimate catalysts for $360-400 if execution delivers

- ⚠️ Current valuation (31x P/E) requires FLAWLESS execution - one stumble on YouTube, Cloud, or CapEx and it's back to $280-300

If you're bearish or considering hedging:

- 🎯 Wait until AFTER earnings to initiate bearish positions - fighting 65% momentum into ATH is suicide

- 📊 First support at $315 (gamma), major support at $310, critical support at $305

- ⚠️ Post-earnings put spreads ($315/$305 targeting gamma support zone) offer defined-risk way to play consolidation/weakness after IV crush

- 📉 Watch for break below $310 - that's the trigger for potential cascade to $305, then $300

- ⏰ Timing is EVERYTHING: Premature bearish positioning risks getting steamrolled by earnings beat; post-earnings offers 50% cheaper entry (IV crush) with better risk/reward

Mark your calendar - Key dates:

- 📅 February 3, 2026 (Monday) after market close - Q4 2025 earnings report (27 DAYS!)

- 📅 February 4 (Tuesday) - Post-earnings price action, analyst reactions, conference call commentary

- 📅 February 6 (Thursday) - Expiration of this $6.2M put trade

- 📅 February 20 - Monthly OPEX (post-earnings settle period ends)

- 📅 March 2026 - Google Assistant sunset (potential user friction)

- 📅 April-June 2026 - Ad-tech antitrust trial remedy decision expected

- 📅 Q2 2026 - Waymo $15B funding round likely closes

- 📅 Mid-2026 - Search antitrust appeal proceedings continue

Final verdict: GOOG's long-term AI transformation story remains EXTRAORDINARILY compelling - Cloud growing 34%, Gemini gaining market share fast (5%→18%), AI Overviews 2B users, Waymo approaching profitability, fortress balance sheet. The bull case for $400+ over 12-24 months is REAL if they execute. HOWEVER, at 31x P/E after 65% rally with earnings in 27 days carrying YouTube comp headwinds, ChatGPT competition uncertainty, and CapEx escalation concerns, the risk/reward for NEW AGGRESSIVE POSITIONING is NO LONGER FAVORABLE.

The $6.2M institutional ATM put purchase with Z-score 495.54 is a CLEAR, UNMISTAKABLE SIGNAL: smart money is derisking at the peak, 27 days before binary catalyst.

Be patient. Let earnings clear the air. Look for better entry $305-315 with clarity. The AI revolution will still be here in 6-8 weeks, and you'll sleep FAR better at night paying $310 after earnings vs $320 before. Those who bought GOOG at $140-180 in early 2025 are sitting on 80-130% gains - PROTECT THEM.

This is a marathon, not a sprint. Capital preservation > FOMO. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-score of 495.54 and Vol/OI ratio of 92.593x reflect this specific trade's statistical unusualness - it does NOT imply the trade will be profitable or that you should follow it. Institutional hedging needs differ vastly from retail trader objectives. Earnings create binary event risk with potential for 5-15% gaps either direction. Always do your own research and consider consulting a licensed financial advisor before trading. ATM puts are expensive insurance - most expire worthless, but occasionally prevent catastrophic losses.

About Alphabet Inc.: Alphabet Inc. is the parent company of Google, operating as a global technology leader in search, advertising, cloud computing, software, hardware, and emerging technologies including autonomous vehicles (Waymo) and life sciences (Verily), with a market cap of $3.797 trillion in the Internet Information Providers & Search Engines industry.