🐋 GOOG $11M LEAP Call Buy — Someone Just Bet Big on Alphabet Through 2028!

📅 March 2, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just loaded up $11 MILLION in Alphabet LEAP calls — buying 2,008 contracts of the $350 strike expiring January 21, 2028. That is nearly two full years of time value on a bet that GOOG climbs 15% past its current price and keeps going. With a breakeven at $402.70 (32% above today's $304.82), this is a high-conviction, long-horizon bullish position likely anchored around Alphabet's AI and Cloud growth thesis.

📊 Company Overview

Alphabet Inc. (GOOG) is the parent company of Google and one of the most valuable companies on Earth:

- Market Cap: $3.67 Trillion (3rd largest globally)

- Industry: Internet Search, Cloud Computing, Advertising, AI

- Current Price: ~$305 (down ~13% from $350.15 ATH on February 3, 2026)

- Primary Business: Google Search & Ads, YouTube, Google Cloud, Waymo, Gemini AI

- Trailing P/E: 28.82 | Forward P/E: 27.31

💰 The Option Flow Breakdown

The Tape (March 2, 2026 @ 11:30:50):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:30:50 | GOOG | MID | BUY | CALL | 2028-01-21 | $11M | $350 | 2.1K | 1.4K | 2,008 | $304.82 | $52.70 | GOOG20280121C350 |

🤓 What This Actually Means

This is a straight-up bullish LEAP purchase — no hedging, no spread, just raw conviction. Let's break it down:

- 💸 $11M in premium paid: $52.70 per contract × 2,008 contracts = ~$10.6M at the door

- 🎯 15% out-of-the-money: $350 strike with GOOG trading at $304.82 — the stock needs to rally just to get to break-even

- ⏰ Nearly 2 years of runway: January 2028 expiration gives this trade 693 days to work

- 📊 Volume crushed OI: 2,100 contracts traded vs 1,400 open interest — a Vol/OI ratio of 1.5x, signaling fresh positioning

- 🏦 Institutional fingerprints all over this: MID-price execution on 2,008 contracts is patient, sophisticated capital — not someone mashing "market buy" on their phone

The math on this trade:

- 🎯 Breakeven at expiration: $350 + $52.70 = $402.70 (32.1% above current price)

- 📈 At the ATH ($350.15): The calls would be roughly at-the-money — but the trader still needs more upside to profit

- 💰 If GOOG hits $420 by Jan 2028: Each contract worth ~$70 intrinsic + time value, yielding roughly 40-50% return on the $52.70 paid

- 💔 Max loss: The full $11M premium — but only if GOOG is below $350 at expiration

Z-Score: 26.23 (EXTREMELY UNUSUAL) 🔥 — This trade is in rarefied air. A z-score above 26 means this kind of size shows up maybe a handful of times per year across the entire GOOG options chain. This is serious institutional money making a deliberate long-term bet.

📈 Technical Setup / Chart Check-Up

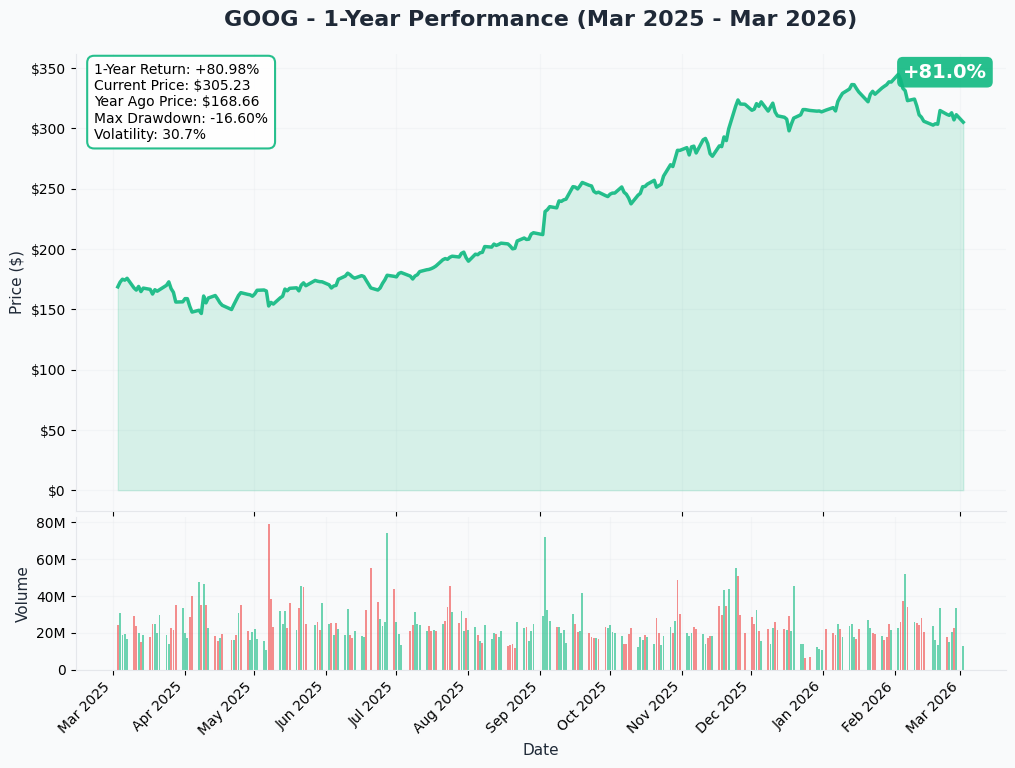

YTD Performance Chart

Alphabet is trading at ~$305, down roughly 5% YTD and about 13% off its all-time high of $350.15 set on February 3, 2026. The pullback was driven by the market's reaction to Alphabet's massive $175-185B capex guidance for 2026 — more than double 2025 spending — which overshadowed a strong Q4 earnings beat.

Key observations:

- 📉 Pullback from ATH: The $350 → $305 decline is consolidation, not collapse — shares have stabilized in the $303-$312 range through late February

- 🎯 $350 strike = the ATH: The trader is betting GOOG reclaims its all-time high and pushes well beyond it

- 📊 Elevated volume around earnings: Big institutional repositioning happened in early February, and this LEAP buy could be the next phase of that positioning

- 💹 52-week range: $152 to $350.15 — GOOG has nearly doubled in the past year, showing strong long-term momentum

Gamma-Based Support & Resistance Analysis

Current Price: ~$305

Note: Gamma exposure data was not available for today's session, so we are relying on implied move levels and recent price action for support/resistance analysis.

Key levels from recent price action:

- 🔵 $300 — Psychological round number and recent support floor

- 🔵 $290 — The lower bound of the post-earnings consolidation range

- 🟠 $312 — Upper end of the recent trading range

- 🟠 $320-$325 — Pre-earnings resistance zone

- 🟠 $350 — All-time high and the strike price of this LEAP trade

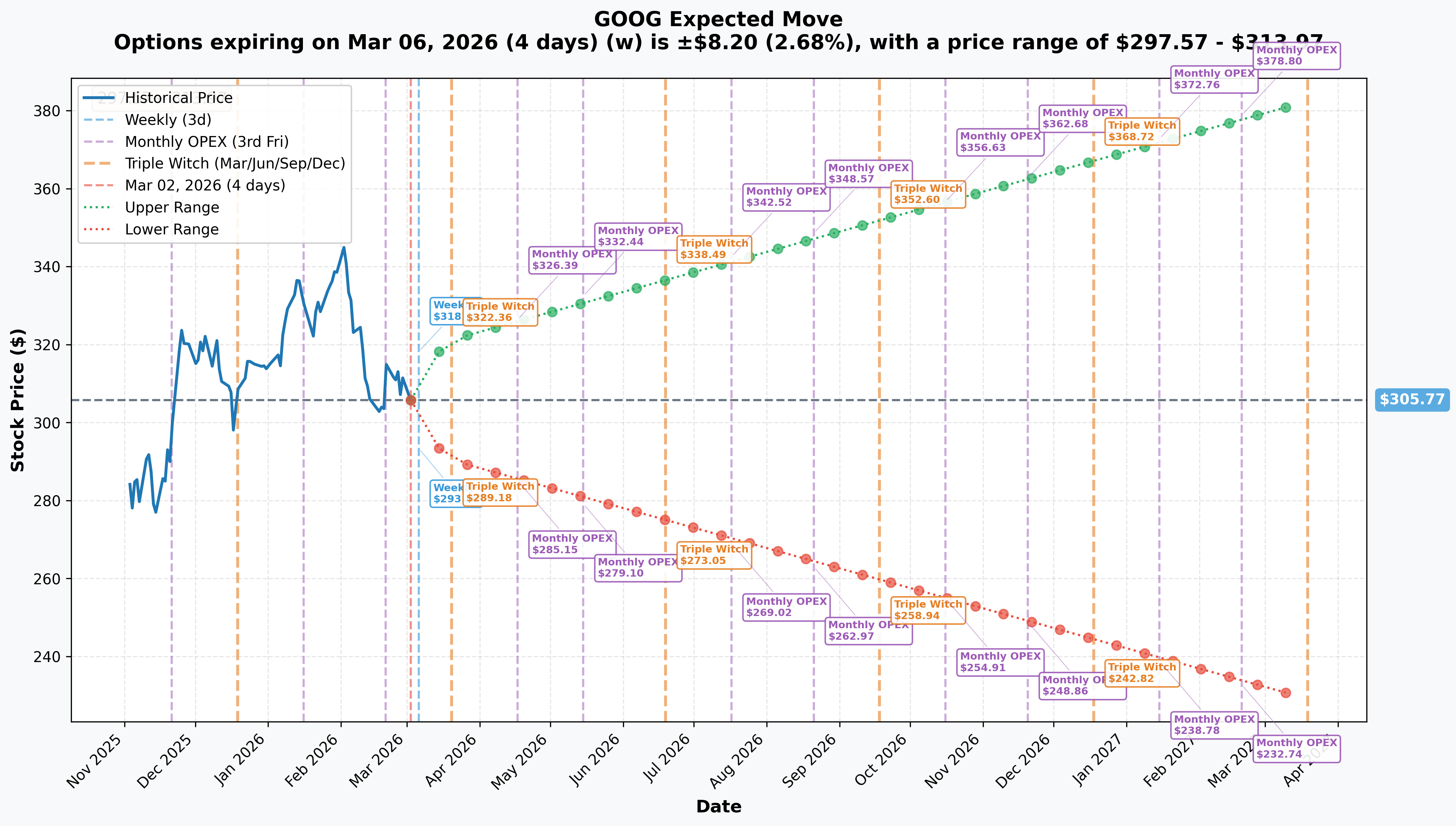

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (March 6 - 4 days): ±$8.20 (±2.68%) → Range: $297.57 - $313.97

- 📅 Monthly/Triple Witch (March 20 - 18 days): ±$15.58 (±5.09%) → Range: $290.19 - $321.35

- 📅 Yearly LEAPS (March 2027 - 382 days): ±$76.73 (±25.1%) → Range: $229.04 - $382.50

Translation for regular folks: The market is pricing in a 2.7% move by this Friday and about a 5% swing through the March 20 triple witch expiration. But the real story for this LEAP trade is the yearly implied move: the options market says there is a reasonable chance GOOG trades anywhere from $229 to $382 over the next year. The $350 strike sits comfortably within that upper range, which means the market is saying this bet is aggressive but not crazy.

Looking further out at the OPEX labels through early 2027:

- By September 2026 Triple Witch, the upper implied range reaches $352.60 — essentially at the $350 strike

- By January 2027, the upper range hits $372.76

- By February 2027, it reaches $378.80

This suggests the market itself is pricing in a plausible path to $350+ over the next 12 months, and this trader has an extra year beyond that for the thesis to play out.

🎪 Catalysts

🔥 Already Happened (Priced In)

Q4 2025 Earnings Beat — February 4, 2026

Alphabet crushed it across the board: revenue of $113.8B (beat by $2.5B), EPS of $2.82 (beat by $0.19), and full-year revenue exceeded $400B for the first time. Google Cloud grew 48% YoY with a $240B backlog. YouTube total revenue (ads + subs) topped $60B for 2025. But the stock sold off because of the capex shocker — $175-185B guided for 2026, roughly double 2025.

Antitrust Search Remedies Finalized — December 5, 2025

Judge Mehta rejected structural relief — no Chrome divestiture, no Android breakup, no AI investment caps. Behavioral remedies only: no exclusive default search contracts and 5-year search data sharing. Both Google and DOJ appealed in February 2026, with hearings expected late 2026. This was a relief outcome for bulls.

Waymo $16B Funding Round — February 2026

Waymo closed a $16B round valuing the unit at $126B, with $13B coming from Alphabet. Currently at 450,000 paid rides per week and targeting 1 million by year-end. The 6th-generation "Ojai" robotaxis are deploying with improved capabilities.

Gemini AI Surge

Gemini crossed 750M monthly active users and 2 billion monthly visits in January 2026. Chatbot market share surged from 5.4% to 18.2% YoY — the fastest growth of any major AI platform — while ChatGPT's share dropped from 87.2% to 68%.

🚀 Upcoming Catalysts (Next 6-22 Months)

1. Google Cloud Next 2026 — April 22-24, 2026 📅

Registration is already live for the annual enterprise AI and cloud showcase in Las Vegas. With Cloud growing 48% and carrying a $240B backlog, expect major announcements around AI agent tools, Gemini enterprise features, and infrastructure partnerships. This event has historically been a positive catalyst for sentiment.

2. Q1 2026 Earnings — April 28, 2026 📊

Consensus: revenue $106.73B, EPS $2.60-$2.62. Key metrics to watch: Can Google Cloud sustain 48% growth? What is the capex burn rate against the $175-185B annual guide? How fast is Gemini's 750M MAU base growing? Any Waymo unit economics commentary?

3. Google I/O 2026 — May 19-20, 2026 🤖

Confirmed at Shoreline Amphitheatre, Mountain View. Expect next-gen Gemini models, Android 17 preview, AI agent capabilities, and potentially Gemini monetization updates. I/O has driven meaningful stock moves in recent years as Google showcases AI leadership.

4. Gemini Monetization / Ads in AI — H1 2026 💰

Adweek reported Google briefed advertisers on bringing ads to Gemini in 2026. AI Overviews ad placements have expanded to 11 new markets. Any formal monetization announcement for Gemini's 750M user base would be a significant revenue growth catalyst.

5. Waymo City Expansion — Throughout 2026 🚗

10 new U.S. cities planned (Dallas, Denver, Detroit, Houston, Las Vegas, Nashville, Orlando, San Antonio, San Diego, Washington D.C.) plus London as the first international market. Each city launch validates the robotaxi model and generates visibility.

6. Ad Tech Antitrust Remedies Ruling — Mid-2026 ⚖️

DOJ seeks forced divestiture of AdX exchange, but the judge appeared skeptical of divestiture mechanics. Even if ordered, ad tech is a small fraction of total revenue and appeals would take years.

7. Search Antitrust Appeal Hearing — Late 2026 ⚖️

D.C. Circuit Court of Appeals will hear both Google's and DOJ's appeals. Final resolution (including potential Supreme Court) not expected until 2027-2028. The appeals process effectively freezes implementation of current remedies.

🎲 Price Targets & Probabilities

Using implied move data, analyst targets, and the catalyst calendar, here are the scenarios through the LEAP's January 2028 expiration:

📈 Bull Case (30% probability)

Target: $400-$430 by Jan 2028

How we get there:

- 🚀 Google Cloud sustains 40%+ growth and the $240B backlog converts into realized revenue, proving the $175-185B capex investment was justified

- 🤖 Gemini monetization launches successfully, opening a new multi-billion dollar revenue stream from 750M+ MAUs

- 🚗 Waymo scales to 1M+ weekly rides and the market starts valuing it as a standalone business (currently $126B)

- 📊 Capex concerns ease as ROI becomes visible in margins and cloud revenue acceleration

- 🎯 Analyst consensus target already at $351.82 with a high of $395 — and those targets would be refreshed higher

For the LEAP trade: At $420, the $350 calls would have $70 of intrinsic value plus remaining time value — a solid return on the $52.70 cost basis. This is the scenario the trader is banking on.

🎯 Base Case (50% probability)

Target: $330-$370 by Jan 2028

Most likely scenario:

- ✅ Cloud growth moderates to 30-35% but remains the fastest-growing hyperscaler

- 📈 Search revenue grows steadily with AI Overviews monetization improving

- ⚖️ Antitrust outcomes manageable — behavioral remedies, no structural breakup

- 🤖 Gemini reaches 1B+ MAUs but monetization ramp is gradual

- 💰 Capex peaks in 2026, free cash flow recovers in 2027 as infrastructure buildout decelerates

- 📊 Multiple holds steady around 25-28x forward earnings on moderate growth

For the LEAP trade: At $350-$370, the calls break even to modestly profitable. The $350 strike is right at the ATH — this scenario gives the trader a coin-flip on recovery to prior peaks. Time value erosion becomes a headwind if the stock lingers below $350 into late 2027.

📉 Bear Case (20% probability)

Target: $250-$300 by Jan 2028

What could go wrong:

- 😰 Cloud growth decelerates sharply as enterprise AI spending normalizes or competitors win share

- 💸 $175-185B capex delivers mediocre ROI, crushing free cash flow and investor confidence

- ⚖️ DOJ wins stronger remedies on appeal — forced Chrome divestiture or restrictions on default search deals ($20B+ annual payment from Apple at risk)

- 📉 Broader tech multiple compression in a higher-rate environment

- 🤖 OpenAI and Anthropic maintain enterprise AI leadership; Gemini fails to close the gap

- 📊 AI Overviews cannibalize paid search CTR faster than monetization offsets (already down 68% on affected queries)

For the LEAP trade: At $300 or below, the $350 calls expire worthless — full $11M loss. However, with 22 months of time, the trader has multiple catalyst cycles to recover from a drawdown scenario.

💡 Trading Ideas

🛡️ Conservative: The "Follow the Whale at Lower Cost" Play

Play: Buy a GOOG LEAP call spread instead of an outright LEAP

Structure: Buy $340 call / Sell $380 call, January 2028 expiration

Why this works:

- 🎯 Follows the same long-term thesis as the $11M whale trade but at a fraction of the cost

- 💰 Selling the $380 call reduces cost basis significantly (the whale is paying pure premium, you cap your upside but cut your risk)

- 📊 Max profit zone: $340-$380 by Jan 2028, which aligns with analyst consensus ($351.82 average PT)

- 🛡️ Defined risk — you know exactly what you can lose on day one

- ⏰ Same 22-month runway lets multiple catalysts (Cloud Next, I/O, earnings cycles, Waymo expansion) do the heavy lifting

Estimated cost: ~$15-20 per spread ($1,500-$2,000 per contract)

Risk level: Moderate (defined max loss) | Skill level: Intermediate

⚖️ Balanced: Post-Catalyst Entry on Stock

Play: Buy GOOG shares on a pullback to $290-$295, targeting $350+

Why this works:

- 📊 $290 is the lower end of the implied move range through March OPEX and sits near strong recent support

- 🎯 Multiple upcoming catalysts (Cloud Next April 22-24, Q1 earnings April 28, I/O May 19-20) provide multiple shots at upward re-rating

- 💰 At $290, GOOG trades at ~26x forward earnings — reasonable for a company growing revenue 15%+ with Cloud at 48%

- 🛡️ Shares don't expire — no time decay pressure like the LEAP trader faces

- 📈 If the stock reclaims its $350 ATH, that is a 20% return from $290 entry

Action plan:

- 👀 Set alerts at $295 and $290

- 🎯 Scale in: 50% at $295, 50% at $290

- ⏰ Hold through at least 2-3 catalyst events (Cloud Next + earnings minimum)

- 🛡️ Stop loss at $270 (7-8% below entry) to limit downside

Risk level: Moderate (no leverage, defined stop) | Skill level: Beginner-friendly

🚀 Aggressive: Calendar Spread Into Earnings

Play: Buy April 28 (post-earnings) / Sell March 20 $310 call calendar spread

Why this could work:

- 🎢 Captures IV expansion into earnings while limiting March expiration risk

- 📈 If GOOG rallies into Cloud Next (April 22-24) and earnings (April 28), the long April calls appreciate

- 💸 The short March calls collect premium and reduce cost basis

- 🎯 $310 strike is slightly OTM — a small rally puts you in the money

- ⚡ Implied move for March 20 is ±5.09% — if the stock stays near $305-$310, the short leg expires near worthless and you keep the long April call cheaply

Why this could blow up:

- 💥 If GOOG drops sharply below $290, both legs lose value

- 😱 March expiration pin risk — short call gets exercised if deep ITM

- 📉 If IV collapses pre-earnings, the calendar loses value

- ⚠️ Early assignment risk on short leg if deep in-the-money

Estimated cost: ~$5-8 per spread ($500-$800 per contract)

Risk level: High (requires active management) | Skill level: Advanced

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

💸 Capex overhang is real: Alphabet guided $175-185B in 2026 capex — more than double 2025 and $55-65B above Street estimates. Until investors see clear ROI from this spend (sustained Cloud growth, Gemini monetization), the stock may struggle to reclaim $350. Free cash flow will be significantly pressured throughout 2026.

-

⚖️ Antitrust is not over: While the initial search remedies were manageable, both sides appealed. If the DOJ wins stronger remedies on appeal — particularly Chrome divestiture or restrictions on default search deals (the Google-Apple deal alone is worth $20B+ annually) — it would be a material hit. The ad tech antitrust ruling expected mid-2026 adds another layer of legal uncertainty.

-

🤖 AI competition is fierce: Despite Gemini's growth, ChatGPT still holds 68% of the chatbot market and Anthropic leads enterprise AI at ~33% share. Meta's open-source Llama models could commoditize AI capabilities. Google needs to execute flawlessly to justify its infrastructure bet.

-

📉 AI Overviews cannibalizing search economics: Paid search CTR dropped 68% on AI Overview queries (from 19.7% to 6.34%). While CPC inflation partially offsets this, the long-term impact on Google's $350B+ annual ad revenue base is an open question.

-

💔 LEAP time decay is slow but relentless: The trader paid $52.70 per contract — roughly $17 of which is time value (assuming ~$35 delta-adjusted intrinsic). Over 22 months, that time value erodes to zero. If GOOG trades sideways at $305 for a year, this position will be underwater even if the stock eventually recovers.

-

🎢 Macro and sector risk: The February 2026 software selloff showed that even mega-caps are vulnerable to risk-off sentiment. At 28.82x trailing P/E (above the 12-month average of 24.06x), Alphabet trades at a premium that leaves room for multiple compression if growth disappoints or rates stay higher for longer.

-

📊 Breakeven is a long way off: The trade needs GOOG at $402.70 by January 2028 to break even at expiration — a 32.1% rally from current levels. While the trader can sell before expiration for a profit at lower prices, the math requires significant sustained upside.

🎯 The Bottom Line

Real talk: An institutional player just put $11M on the table betting Alphabet reclaims its all-time high and pushes meaningfully beyond it over the next two years. This is not a quick trade — it is a thesis-level position on Google's AI and Cloud growth trajectory. The $350 strike is literally the ATH, and the breakeven at $402.70 requires a 32% rally. That is a bold bet, but not an unreasonable one given the catalyst pipeline.

What this trade tells us:

- 🎯 Someone with deep pockets believes the capex-driven pullback is a buying opportunity, not a warning sign

- 💰 They are paying up for maximum time (22 months) rather than trying to catch a short-term bounce — this is patient money

- 📊 The z-score of 26.23 means this kind of LEAP positioning is extremely rare — this is not noise

- 🤖 The thesis likely centers on Google Cloud's 48% growth and $240B backlog proving out the AI infrastructure investment, combined with Gemini's rapid adoption and Waymo's commercial scaling

If you're bullish on GOOG:

- ✅ The 13% pullback from ATH gives you a better entry than the whale got on their strike price — but consider defined-risk strategies (spreads) instead of naked LEAPs

- 📅 April 22-28 is the next major catalyst cluster: Cloud Next followed immediately by Q1 earnings

- 🎯 Analyst consensus target of $351.82 (15% upside from here) with a high target of $395 supports the directional thesis

- 📊 A close above $320 would break the post-earnings consolidation range and signal a potential move back toward $350

If you're watching from the sidelines:

- 👀 Wait for the April catalyst cluster before committing capital — Cloud Next + earnings will give you much better visibility on whether the capex investment is paying off

- 🎯 A pullback to $290 (implied move lower bound for March OPEX) would offer a compelling entry at ~26x forward earnings

- ⏰ You have time — the whale bought 22 months of runway, and you can be more selective with your timing

If you're bearish:

- 📊 The capex concerns are legitimate — $175-185B is an enormous number and free cash flow will suffer in 2026

- ⚖️ Watch the ad tech antitrust ruling mid-2026 and search antitrust appeal late 2026 for potential negative catalysts

- 🛡️ Put spreads (e.g., $300/$280 for March or April expiration) offer defined-risk ways to play downside

Mark your calendar — Key dates:

- 📅 March 20 — Triple Witch options expiration (implied range: $290-$321)

- 📅 April 22-24 — Google Cloud Next 2026, Las Vegas

- 📅 April 28 — Q1 2026 earnings report

- 📅 May 19-20 — Google I/O 2026, Mountain View

- 📅 Mid-2026 — Ad tech antitrust remedies ruling expected

- 📅 Late 2026 — Search antitrust appeal hearing

- 📅 January 21, 2028 — This LEAP trade's expiration date

Final verdict: This $11M LEAP buy is a statement trade — a well-capitalized investor betting that Alphabet's AI infrastructure buildout will look brilliant in hindsight, that Google Cloud's growth trajectory justifies the capex, and that Gemini + Waymo + Search will compound into a stock price well above $350 over the next two years. The pullback from ATH gives the thesis some breathing room, but the breakeven at $402.70 demands strong execution across multiple business lines. For retail traders, this is a signal to pay attention to Alphabet's spring catalyst lineup (Cloud Next + earnings + I/O) — but use defined-risk strategies and smaller position sizes rather than trying to replicate an $11M institutional bet.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance does not guarantee future results. The 26.23 z-score reflects this trade's extreme unusualness relative to recent history — it does not imply the trade will be profitable or that you should follow it. LEAPs carry significant time decay risk and capital commitment. Always do your own research and consider consulting a licensed financial advisor before trading.

About Alphabet Inc. (GOOG): Alphabet is the parent company of Google, with a $3.67 trillion market cap. The company operates the world's dominant search engine, the fastest-growing major cloud platform (Google Cloud), YouTube, the Gemini AI platform (750M+ MAUs), and Waymo autonomous vehicles. Alphabet generated $403B in revenue in 2025, its first year above $400B.