📈 GOOG $8.2M Covered Call Roll - Smart Money Capping Upside on Alphabet! 💰

📅 March 6, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just rolled $8.2 MILLION in covered call premium on Alphabet this morning, selling 3,699 contracts of the December $360 calls for $7M and 1,149 contracts of the September $370 calls for $1.2M. With GOOG trading at ~$296, this institutional player is capping their upside at 22-25% above current levels while collecting massive premium heading into ex-dividend (March 9) and Q1 earnings (April 23). Translation: A big fund is saying "I love GOOG long-term, but I'll take the income now and let someone else chase the top."

📊 Company Overview

Alphabet Inc. (GOOG) is the holding company behind Google, one of the most dominant technology franchises on Earth:

- Market Cap: $3.64 Trillion (one of the largest companies in the world)

- Industry: Computer Programming, Data Processing & Related Services

- Current Price: ~$296 (trading ~10% below the all-time high of $349 set in early February 2026)

- Primary Business: Google Search & Ads (~90% of revenue), Google Cloud (~10%), and Other Bets (Waymo, Verily, Google Fiber)

💰 The Option Flow Breakdown

The Tape (March 6, 2026):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:36:19 | GOOG | BID | SELL | CALL $360 | 2026-12-18 | $7M | $360 | 3,700 | 5,800 | 3,699 | $295.95 | $18.90 |

| 09:35:41 | GOOG | BID | SELL | CALL $370 | 2026-09-18 | $1.2M | $370 | 1,200 | 1,600 | 1,149 | $296.78 | $10.25 |

🤓 What This Actually Means

This is a covered call roll - a classic institutional income play! Here's the breakdown:

- 💸 Total premium collected: $8.2M ($7M from Dec $360 calls + $1.2M from Sept $370 calls)

- 🔄 The roll: The trader appears to be rolling shorter-dated Sept $370 calls into longer-dated Dec $360 calls, extending their covered call position while lowering the strike and picking up more premium

- 📊 Size is significant: The Dec leg alone is 3,699 contracts = 369,900 shares of GOOG exposure, worth roughly $109M at current prices

- 🎯 Upside cap: The $360 strike on Dec 18 means the trader is comfortable handing off shares at $360 (about 21.7% above the current ~$296 price)

- ⏰ Strategic timing: Sold just before the March 9 ex-dividend date ($0.21/share) and well ahead of Q1 earnings on April 23

- 🏦 This is institutional portfolio management: Think pension fund or large asset manager generating income on a core holding

What's really happening here: This trader owns a massive block of GOOG stock and is systematically selling calls against it to generate income. By rolling from the September $370 calls down to December $360 calls, they're saying: "I think GOOG might rally, but probably not past $360 by year-end." They're collecting $18.90/share on the Dec leg alone - that's 6.4% of the current stock price in pure premium income. On top of dividends, that's a beautiful yield play on a mega-cap tech stock.

Unusual Score: 🔥 EXTREMELY UNUSUAL - The Dec $360 call leg posted a Z-score of 4.95 (size is about 0.64x open interest) and the Sept $370 leg hit 9.29 (0.75x open interest ratio). Volume dwarfing open interest on both legs tells us this is fresh, aggressive positioning - these aren't normal daily flows. Trades of this combined size happen maybe a few times per quarter on GOOG options.

📈 Technical Setup / Chart Check-Up

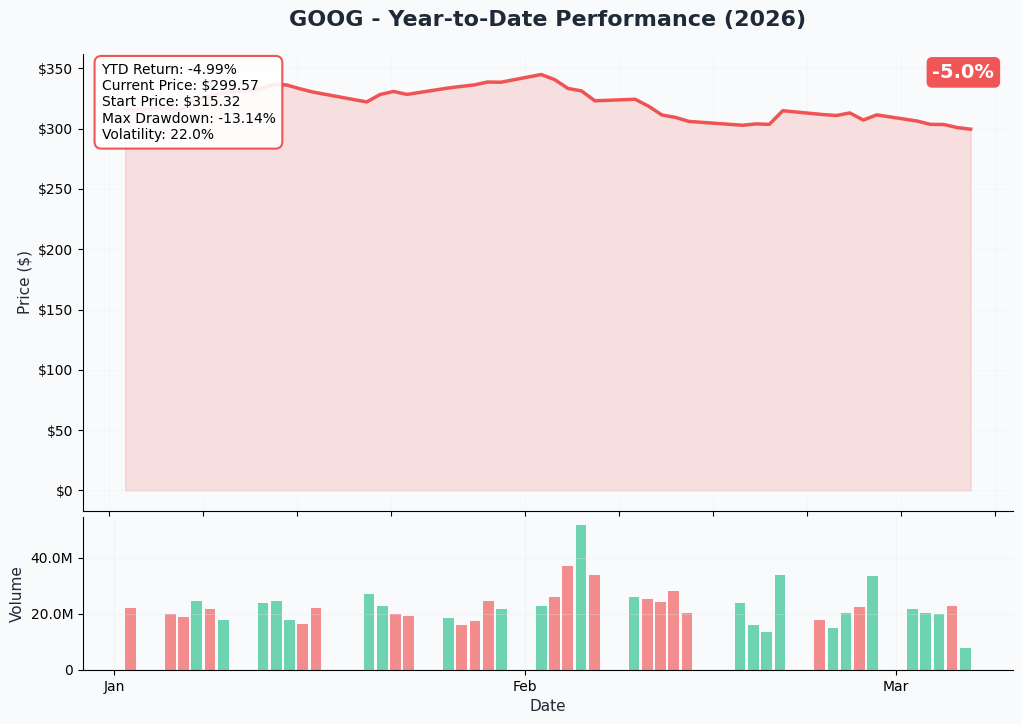

YTD Performance Chart

GOOG is the best-performing Magnificent Seven stock in 2026, up about 7.7% YTD with a market cap above $4 trillion at its peak. The stock hit an all-time high of $349 in early February before pulling back to the current ~$296 area, roughly 10% off those highs.

Key observations:

- 📈 Strong start to 2026: Led the mega-cap tech pack year-to-date

- 📉 Recent pullback: Down ~15% from the $349 February peak - healthy consolidation or start of something worse?

- 🎢 Volatile but trending: The dip from ATH created uncertainty heading into Q1 earnings

- 📊 AI catalyst momentum: Gemini deal with Apple, Wiz acquisition, and Waymo expansion all adding narrative fuel

- 🤔 Key question: Is the pullback a buying opportunity or the start of a deeper correction?

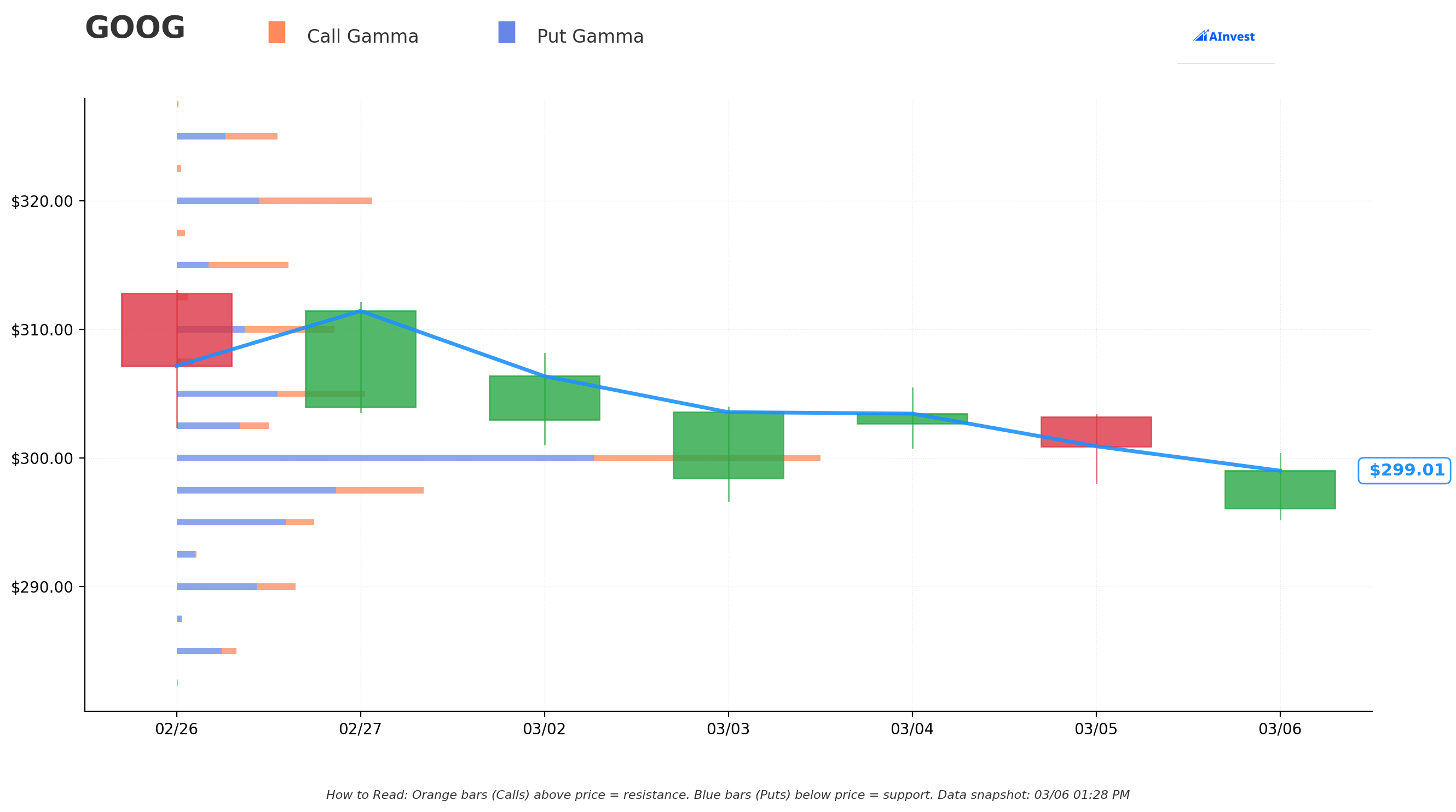

Gamma-Based Support & Resistance Analysis

Current Price: $299.56

The gamma exposure map reveals the critical price levels where dealer hedging activity will influence near-term price action:

🔵 Support Levels (Put Gamma Below Price):

- $297.50 - Immediate support with 22.3B total gamma (just 0.7% below current price - first line of defense)

- $295 - Secondary support at 13.6B gamma (1.5% below - key floor for the pullback)

- $290 - Major structural support with 12.7B gamma (3.2% below - this is the line in the sand)

🟠 Resistance Levels (Call Gamma Above Price):

- $300 - Immediate and STRONGEST resistance at 71.5B total gamma (huge psychological level right above current price!)

- $302.50 - Secondary resistance at 13.5B gamma

- $305 - Resistance at 22.7B gamma (1.8% above)

- $310 - Moderate resistance at 17.4B gamma (net GEX turns positive here - bullish flip zone)

- $315 - 12.4B gamma resistance (5.2% above)

- $320 - Strong resistance at 21.4B gamma (6.8% above)

- $330 - Extended target at 18.2B gamma (10.2% above)

What this means for traders: The $300 level is a MASSIVE gamma wall - at 71.5B total gamma, it's by far the strongest single level on the board. Market makers are going to sell into any rally toward $300, creating a natural ceiling that GOOG needs to punch through with real buying volume. On the downside, $297.50 and $295 provide decent near-term cushion, but $290 is where things get serious if sellers take control.

Notice something interesting? The covered call seller struck at $360 and $370 - both WAY above the current gamma resistance levels. They're not worried about near-term chop between $290-$310. This is a longer-term income play that only gets tested if GOOG rallies 20%+ from here. Smart positioning.

Net GEX Bias: Bearish (total put GEX of 180.4B slightly exceeds call GEX of 162.1B) - Dealers are positioned to sell rallies and buy dips in the near term, which creates a range-bound dynamic.

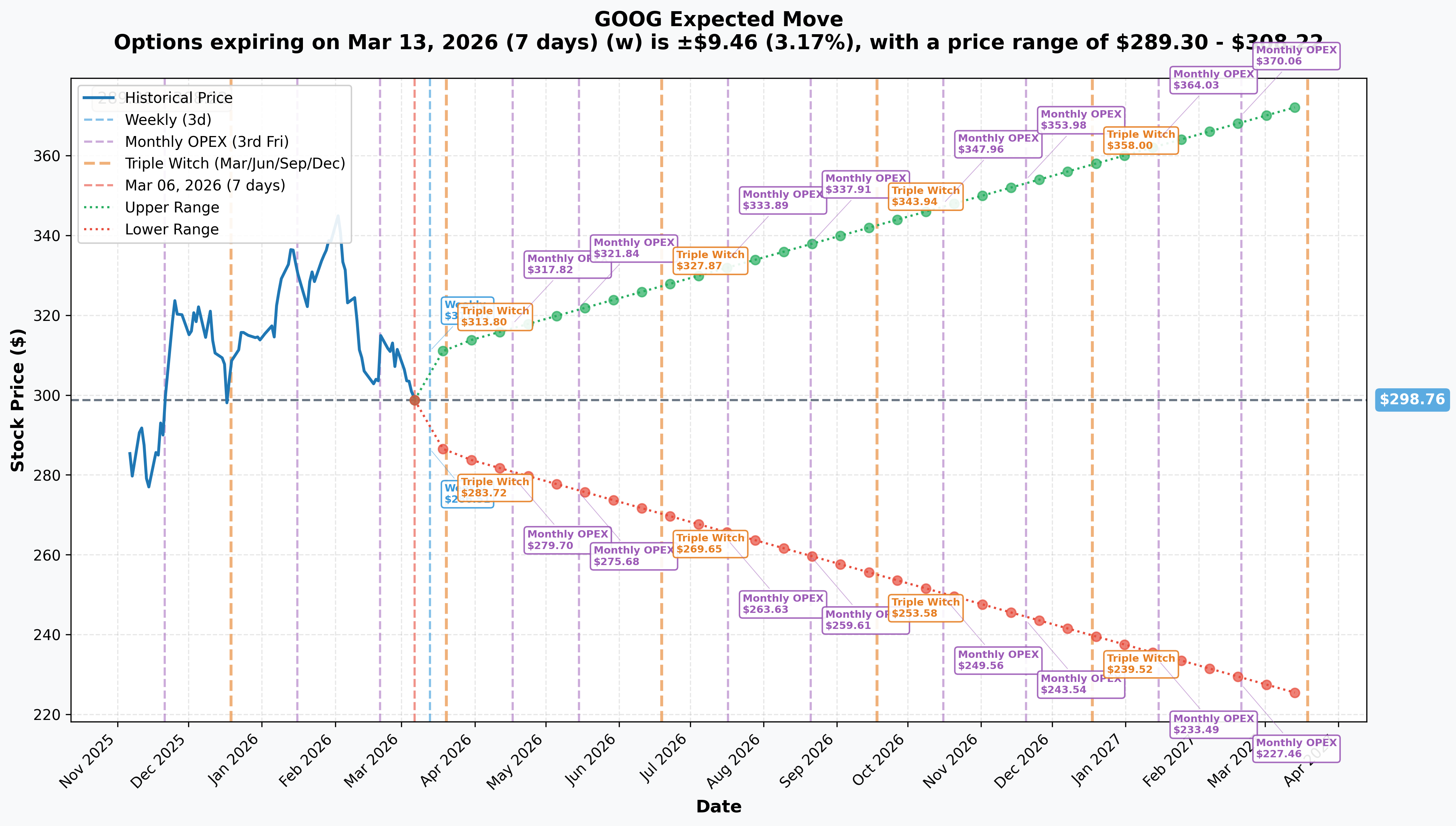

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (March 13 - 7 days): ±$9.46 (±3.17%) → Range: $289.30 - $308.22

- 📅 Monthly OPEX / Triple Witch (March 20 - 14 days): ±$13.37 (±4.47%) → Range: $285.39 - $312.13

- 📅 September Triple Witch (Sept 18 - THIS TRADE LEG 2!): ±$45.18 (±15.1%) → Range: $253.58 - $343.94

- 📅 December Triple Witch (Dec 18 - THIS TRADE LEG 1!): ±$59.24 (±19.8%) → Range: $239.52 - $358.00

Translation for regular folks: The options market is pricing in a 3.2% move ($9.46) over the next week and a 4.5% move ($13.37) by the March 20 triple witch OPEX. That's fairly normal volatility for a mega-cap stock.

But here's the key insight for this trade: The implied move for December 18 (when the big $7M leg expires) has an upper range of $358. The trader sold the $360 calls - meaning they're selling at the very TOP of what the market thinks is possible. If GOOG hits $360 by December, that's literally at the edge of the implied probability distribution. Smart strike selection.

For the September leg, the upper range is $343.94 - the $370 strike sits comfortably ABOVE that. Almost zero chance of getting called away on that leg based on current implied vol.

Key insight: Both covered call strikes are at or beyond the implied move upper bounds. This trader is collecting premium on strikes the market assigns very low probability of reaching. That's textbook professional covered call writing.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

Ex-Dividend Date - March 9, 2026 (3 DAYS AWAY!) 💰

GOOG goes ex-dividend on Monday, March 9 with a $0.21/share cash dividend. While the yield is tiny on a ~$296 stock, the timing of this covered call sale right before ex-div is no accident. The call seller captures the dividend income on top of the premium collected. Smart institutional housekeeping.

DOJ Antitrust Remedy Trial - ONGOING ⚖️

The Department of Justice's antitrust case against Google regarding its search monopoly remains an active headwind. Potential structural remedies could force changes to Google's search distribution deals, which are core to the advertising revenue machine. This overhang is likely one reason the stock hasn't recovered to its February highs.

🚀 Near-Term Catalysts (Q1-Q2 2026)

Q1 2026 Earnings - April 23, 2026 (7 WEEKS AWAY!) 📊

Alphabet reports Q1 results on April 23, 2026 after close:

- 💰 Consensus EPS: $2.66

- 📊 Key focus areas: Google Cloud AI revenue growth acceleration, advertising resilience, Gemini monetization progress

- 🤖 AI narrative: The Apple Gemini deal and continued enterprise adoption of Gemini models will be closely watched

- 📈 Analyst consensus: Strong Buy from 44 analysts with average price target of $351.82-$367.18

$32B Wiz Acquisition - Expected to Close in 2026 🏢

Alphabet's blockbuster $32B acquisition of Wiz received EU unconditional antitrust clearance on February 13, 2026, after DOJ cleared it in November 2025. Final regulatory approvals are pending but the deal is expected to close this year. This massively bolsters Google Cloud's security stack and positions it as a leader in cloud security.

Gemini AI Deal with Apple 🤖

One of the biggest AI catalysts of 2026 - Alphabet announced a partnership where Gemini models and cloud technology will power Apple's next-generation AI features. This validates Gemini's competitive positioning against OpenAI's ChatGPT and gives Google unprecedented distribution across Apple's 2.3 billion device ecosystem.

Waymo Expansion to 20+ Cities 🚗

Waymo is expanding to 20+ additional cities in 2026, including international markets like Tokyo and London. While still in "Other Bets," the autonomous driving platform is approaching an inflection point for revenue contribution and potential spinoff value.

⚠️ Risk Catalysts (Negative)

DOJ Antitrust - Structural Remedy Risk ⚖️

The ongoing DOJ antitrust remedy trial regarding Google's search monopoly is the elephant in the room. Potential structural remedies could force changes to search distribution deals that generate billions in revenue. This is likely suppressing the stock's multiple and keeping GOOG trading below its February highs.

Massive AI Capex Bet 💸

Alphabet is committing roughly ~$180B in cumulative capital expenditure on AI infrastructure. While necessary to compete, this creates execution risk if AI monetization doesn't accelerate fast enough to justify the spend. Investors will be watching closely for ROI on this massive investment.

AI Search Disruption 🤖

The rise of AI-powered search alternatives (ChatGPT, and others) threatens Google's core search advertising revenue model. If consumer behavior shifts away from traditional search toward conversational AI, Google's advertising moat could erode over time.

Wiz Integration Risk 🔗

The $32B Wiz acquisition needs to deliver on its cloud security strategy. Integration of such a large acquisition carries execution risk, and the price tag is substantial even for Alphabet.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are the scenarios through the December 18 expiration (when the main covered call leg expires):

📈 Bull Case (25% probability)

Target: $340-$370

How we get there:

- 💪 Q1 earnings crush expectations with Cloud revenue accelerating past 30% YoY growth

- 🤖 Gemini Apple partnership generates massive user engagement and monetization signals

- 🏢 Wiz acquisition closes smoothly, Google Cloud wins major enterprise security contracts

- 🚗 Waymo announces profitability pathway or strategic partnership/spinoff

- ⚖️ DOJ antitrust resolution comes in lighter than feared (behavioral remedies, not structural)

- 📈 Analyst targets of $351-$367 achieved as multiple re-rates higher

- 🚀 Breaks through $300 gamma wall, then $310, $320, and $330 resistance levels on sustained buying

Key metrics needed:

- Google Cloud revenue growth >30% YoY

- Advertising revenue resilience despite AI search competition

- Positive Gemini monetization guidance

- DOJ remedy clarity that doesn't structurally impair the business

What happens to the covered call trade: The $360 Dec calls get challenged or go in-the-money. Trader's shares get called away at $360 + keeps $18.90 premium = effective exit at $378.90/share. That's a 28% return from $296 - the trader is totally fine with this outcome. The Sept $370 calls expire worthless (good outcome for the seller).

Probability assessment: Only 25% because GOOG needs to rally 20%+ from current levels, which requires multiple catalysts to fire simultaneously. The DOJ overhang and recent pullback from $349 suggest the market isn't ready to give GOOG a premium multiple yet.

🎯 Base Case (50% probability)

Target: $290-$320 range (CONSOLIDATION)

Most likely scenario:

- ✅ Solid Q1 earnings meeting consensus (EPS ~$2.66) with steady growth

- 📊 Cloud business growing but not explosive enough to re-rate the stock

- ⚖️ DOJ uncertainty continues to cap upside through year-end

- 🤖 Gemini progress is incremental - impressive tech but slow monetization

- 🏢 Wiz deal closes, market says "show me the revenue synergies"

- 🔄 Stock trades within gamma support ($290-$297) and resistance ($300-$310) bands

- 💤 Market digests the February pullback, ranges sideways waiting for 2027 catalysts

This is the covered call seller's ideal scenario: GOOG stays comfortably below $360, both call legs expire worthless, and the trader keeps the full $8.2M in premium plus dividends plus any stock appreciation. On 369,900 shares at $296, collecting $18.90/share in premium on the Dec leg alone is a 6.4% yield over 9 months. Combined with dividends and modest stock appreciation, they're looking at a 10-15% total return. Not bad for a "boring" income strategy!

Why 50% probability: The $300 gamma wall creates real near-term resistance, the DOJ case caps the multiple, and the recent 15% pullback from ATH suggests the market needs time to digest before making new highs. Consolidation is the path of least resistance.

📉 Bear Case (25% probability)

Target: $250-$290

What could go wrong:

- 😰 Q1 earnings miss on advertising weakness as AI search alternatives gain share

- ⚖️ DOJ imposes structural remedies (forced sale of Chrome, changes to search distribution) - this would be catastrophic

- 💸 AI capex spending accelerates with no clear return path, margin compression

- 🇨🇳 Regulatory risks escalate across multiple jurisdictions

- 🤖 Gemini struggles vs ChatGPT in enterprise adoption, Apple deal disappoints

- 📉 Broader tech selloff drags mega-caps lower (macro recession, rate concerns)

- 🔨 Break below $290 gamma support triggers cascade to $280, then $270

Critical support levels:

- 🛡️ $297.50: Immediate gamma floor (22.3B) - first test level

- 🛡️ $295: Secondary support (13.6B gamma) - must hold for bullish structure

- 🛡️ $290: Major structural floor (12.7B gamma) - break below this and things get ugly fast

What happens to the covered call trade: Both call legs expire deep out-of-the-money. Trader keeps the full $8.2M premium, which cushions the stock decline. Effective breakeven on the Dec leg: $296 - $18.90 = $277.10. So even with a ~7% stock decline, the covered call writer is still profitable on a total return basis. That's the beauty of the strategy.

Probability assessment: 25% because it requires DOJ worst-case outcome or meaningful advertising revenue deterioration. Alphabet's fundamentals are strong, and the stock is already 10% off highs, which builds in some margin of safety.

💡 Trading Ideas

🛡️ Conservative: Copy the Covered Call (Income Play)

Play: If you own GOOG shares, sell covered calls at the $340-$360 strikes for September or December expiration

Why this works:

- 🎯 This institutional trader is literally showing you the playbook - sell OTM calls to generate income while capping upside at a level you'd happily sell

- 💰 At current prices, you can collect roughly 3-6% in premium over 6-9 months on top of dividends

- 🛡️ Premium provides downside cushion - you're effectively buying the stock at a discount

- 📊 Both strikes are above analyst consensus targets ($351-$367), so you're not giving away much

- ⚖️ Perfect for the DOJ uncertainty period - get paid while you wait for clarity

- ⏰ Ex-dividend March 9 means you collect the dividend PLUS the call premium

Estimated P&L (per 100 shares):

- 💰 Premium collected: ~$1,000-$1,900 per contract (depending on strike and expiration)

- 📈 Max gain: Stock appreciation to strike + premium + dividends

- 📉 Max loss: Same as stock ownership, offset by premium collected

- 🎯 Breakeven: Current price minus premium collected (~$277-$286)

Risk level: Low-Moderate (you already own the stock) | Skill level: Beginner-friendly

⚖️ Balanced: Bull Call Spread Post-Earnings

Play: After Q1 earnings on April 23, buy a bull call spread targeting the $310-$330 range

Structure: Buy $310 calls, Sell $330 calls (September 18 expiration)

Why this works:

- 🎢 Wait for post-earnings IV crush to buy options cheaper (IV typically drops 20-30% after earnings)

- 📊 Defined risk spread ($20 wide = $2,000 max risk per spread)

- 🎯 Targets the $310-$330 gamma resistance zone where upside potential exists if earnings are strong

- 🤖 Captures potential Gemini + Wiz catalysts through summer

- ⏰ September expiration gives 5 months of runway for the thesis to play out

- 💰 Significantly cheaper post-IV crush vs buying now

Estimated P&L (adjust after earnings IV crush):

- 💰 Pay ~$7-10 net debit per spread post-earnings

- 📈 Max profit: $1,000-$1,300 per spread if GOOG above $330 at Sept expiration

- 📉 Max loss: $700-$1,000 (defined, limited to debit paid)

- 🎯 Breakeven: ~$317-$320

Entry timing:

- ⏰ Wait 2-3 days post-April 23 earnings for full IV collapse

- 🎯 Only enter if earnings confirm Cloud growth and Gemini traction

- ❌ Skip if DOJ ruling comes in harsh or earnings disappoint

Risk level: Moderate (defined risk, directional) | Skill level: Intermediate

🚀 Aggressive: Pre-Earnings Straddle (High Risk!)

Play: Buy April expiration straddle ahead of Q1 earnings on April 23

Structure: Buy $300 calls + Buy $300 puts (April 17 expiration)

Why this could work:

- 💥 GOOG has multiple binary catalysts converging: Q1 earnings, DOJ remedy updates, Wiz closing, Gemini progress

- 🎯 $300 gamma wall creates a key breakout/breakdown level - the move from $300 could be explosive either direction

- 📊 Stock already 10% off highs creates pent-up energy for a big directional move

- ⚡ Any DOJ headline or earnings surprise could move stock 5-10% overnight

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Straddles on mega-caps aren't cheap - expect $15-20 per straddle ($1,500-$2,000 cost)

- ⏰ TIME DECAY: Theta burns fast approaching expiration

- 😱 IV CRUSH: Even if stock moves 3-5%, IV collapse post-earnings could still result in LOSS

- 📊 Need 5-7%+ move to breakeven after IV crush

Risk level: HIGH (can lose 100% of premium) | Skill level: Advanced only

CRITICAL WARNING: Only attempt this if you can afford to lose the entire premium, have traded straddles through earnings before, and plan to close within 24-48 hours post-earnings.

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⚖️ DOJ antitrust is the #1 risk: The ongoing remedy trial regarding Google's search monopoly could result in structural remedies (forced sale of Chrome, changes to default search agreements) that would materially impair Alphabet's advertising revenue model. This is NOT priced into the stock at current levels - a worst-case ruling could send GOOG down 15-25% overnight. The uncertainty alone is keeping the multiple compressed.

-

💸 $180B AI capex bet needs to pay off: Alphabet is making an enormous bet on AI infrastructure. If Gemini doesn't gain meaningful enterprise traction or if AI monetization disappoints, the market will punish the stock for spending too much with too little return. Watch Cloud revenue growth closely.

-

🤖 AI search disruption is real: ChatGPT and other AI-powered search alternatives are gaining users. If traditional search query volumes decline meaningfully, Google's advertising moat weakens. The Gemini partnership with Apple is a defensive move as much as it is offensive.

-

📊 $300 gamma ceiling creates near-term headwind: The 71.5B gamma wall at $300 is massive. Market makers will systematically sell into any rally to this level, creating mechanical resistance. Breaking through requires sustained institutional buying. Until $300 falls, expect chop.

-

🏢 Wiz integration risk at $32B: The largest acquisition in Alphabet's history needs to deliver on cloud security strategy. Integration failures, talent departures, or revenue shortfalls could turn this from a catalyst into a drag.

-

📉 10% pullback from ATH could accelerate: GOOG already fell from $349 to ~$296. If $290 gamma support breaks, momentum sellers and stop-losses could cascade the stock toward $270-$280. The pullback isn't necessarily "done."

-

🐋 Smart money is capping upside, not buying aggressively: This $8.2M covered call roll signals that sophisticated institutional players don't expect GOOG to significantly break above $360 by year-end. They'd rather collect premium than bet on a moonshot. When the big guys are income-seeking rather than growth-chasing, it tells you something about their forward expectations.

-

🌍 Multi-jurisdiction regulatory risk: Beyond the DOJ, Alphabet faces regulatory challenges across the EU, Asia, and other markets. Any unexpected regulatory action could create headline risk.

🎯 The Bottom Line

Real talk: An institution just collected $8.2M in covered call premium on GOOG, capping their upside at $360-$370 while pocketing income on a massive stock position. This isn't a bearish signal - it's a professional portfolio manager saying: "GOOG is a great long-term hold, but the risk/reward up here doesn't justify sitting naked long. Let me get paid while I wait."

What this trade tells us:

- 🎯 Sophisticated player expects GOOG to stay below $360 through December 2026 (base case is consolidation, not breakout)

- 💰 They value income over upside - collecting 6.4% premium yield over 9 months is better than hoping for a 20%+ rally

- ⚖️ The DOJ uncertainty makes them cautious about aggressive upside positioning

- 📊 They're playing the "probability game" - both strikes are above the implied move upper bounds, meaning the options market gives these a low probability of being reached

- ⏰ Timing before ex-dividend is deliberate - capture the $0.21/share dividend plus the premium

This is a "get paid to wait" signal, not a "run for the exits" signal.

If you own GOOG:

- ✅ Consider writing covered calls at $340-$360 strikes against your shares to generate income

- 📊 Use the $290-$297 gamma support zone as your mental floor - if GOOG breaks below $290, reassess your thesis

- ⏰ Q1 earnings on April 23 is the next major catalyst - have a plan before that date

- 💰 Collect the March 9 dividend, obviously

- 🛡️ The covered call premium gives you cushion - even if the stock dips to $277, you're breakeven on a total return basis

If you're watching from the sidelines:

- ⏰ April 23 after close is the moment of truth - Q1 earnings will set the tone for the rest of 2026

- 🎯 A pullback to $280-$290 (near gamma support) would be an attractive entry point with 15-20% margin of safety

- 📈 Looking for: Google Cloud revenue growth >30%, Gemini adoption metrics, Wiz deal closing confirmation, DOJ clarity

- 🚀 Longer-term, the Gemini + Apple partnership and Waymo expansion are legitimate multi-year catalysts

- ⚠️ Analyst targets of $351-$367 suggest 18-24% upside from current levels - but that requires DOJ clarity

If you're bearish:

- 🎯 Wait for a failed breakout at $300 (gamma wall) before initiating short positions

- 📊 First support at $297.50 (gamma), major support at $290 (12.7B gamma)

- ⚠️ DOJ remedy ruling is your potential catalyst - any structural remedy announcement could be the trigger

- 📉 Put spreads ($295/$285 or $290/$280) offer defined-risk downside plays

- ⏰ Don't short into $290 support - wait for the break, then fade the move

Mark your calendar - Key dates:

- 📅 March 9 (Monday) - GOOG ex-dividend date ($0.21/share)

- 📅 March 13 - Weekly OPEX (±3.2% implied move)

- 📅 March 20 - Triple Witch quarterly OPEX (±4.5% implied move)

- 📅 April 23 (Thursday) after market close - Q1 2026 earnings report (consensus EPS: $2.66)

- 📅 September 18 - Triple Witch, expiration of the $370 call leg ($1.2M trade)

- 📅 December 18 - Triple Witch, expiration of the $360 call leg ($7M trade)

Final verdict: Alphabet is in a classic "show me" phase. The AI story (Gemini, Apple partnership, Cloud growth) is compelling, the Wiz acquisition adds strategic value, and Waymo is approaching an inflection point. But the DOJ antitrust overhang, massive capex commitments, and recent 15% pullback from highs all tell us the market wants more proof before re-rating the stock higher. The $8.2M covered call roll confirms this view: smart money is positioned for a grind, not a sprint.

Be patient. Collect income if you own it. Wait for $280-$290 if you want to buy it. And let Q1 earnings on April 23 give you the clarity you need to size up.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-scores of 4.95 and 9.29 reflect these specific trades' size relative to recent GOOG options activity - they do not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading. Covered call strategies limit upside potential in exchange for premium income. The DOJ antitrust case creates meaningful binary risk that could impact GOOG significantly in either direction.

About Alphabet Inc.: Alphabet is a holding company that wholly owns internet giant Google, deriving slightly less than 90% of its revenue from Google services (primarily advertising), with Google Cloud accounting for roughly 10% of revenue. The company also invests in technologies such as self-driving cars (Waymo) and health (Verily), with a market cap of $3.64 trillion in the Computer Programming & Data Processing industry.