💎 GOOGL Massive $28M Call Sale - Institutional Profit Taking Before Q4! 🛡️

📅 December 12, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just locked in $28 MILLION in profits on GOOGL this morning at 10:41:38! This massive closing trade sold 5,000 contracts of February 20, 2026 $260 strike calls at $55.05 each - cashing out a huge winning position accumulated during GOOGL's historic run past the $3.77 trillion market cap milestone. With GOOGL at $309.04 and Q4 earnings just 52 days away (February 3), smart money is taking chips off the table at all-time highs. Translation: Institutional winners are banking 7-figure gains rather than risking the next earnings lottery!

📊 Company Overview

Alphabet/Google (GOOGL) is the world's third-largest company and the undisputed leader in internet search and digital advertising:

- Market Cap: $3.77 Trillion (3rd largest globally, behind Apple and Microsoft)

- Industry: Computer Programming & Data Processing Services

- Current Price: $309.04 (near 52-week high of $328.83)

- Primary Business: Google Search, YouTube, Google Cloud, Android, Chrome browser, AI products (Gemini)

- Employees: 190,167 worldwide

Alphabet is the holding company for Google and generates approximately 90% of revenue from Google's advertising and subscription services, with Google Cloud contributing roughly 10% and growing rapidly at 34% year-over-year.

💰 The Option Flow Breakdown

The Tape (December 12, 2025 @ 10:41:38):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10:41:38 | GOOGL | MID | SELL | CALL $260 | 2026-02-20 | $28M | $260 | 5K | 35K | 5,000 | $309.04 | $55.05 |

🤓 What This Actually Means

This is a massive profit-taking position close on a deep in-the-money call! Here's what went down:

- 💸 Huge cash-out: $28M premium received ($55.05 per contract × 5,000 contracts)

- 💰 Deep ITM close: $260 strike calls with $49 of intrinsic value ($309.04 spot - $260 strike)

- 📊 Theta value: $6.05 time premium remaining ($55.05 option price - $49 intrinsic)

- 🎯 Position size: 5,000 contracts represents 500,000 shares worth ~$154.5M

- ⏰ Strategic timing: 70 days to expiration, closing BEFORE Q4 earnings on February 3, 2026

- 🏦 Institutional profit booking: This is sophisticated portfolio management - locking in gains at peak

What's really happening here: This trader likely bought these $260 calls months ago when GOOGL was trading between $260-$280. Now, with GOOGL at $309 and up +36.5% in just 3 months (from ~$229 on September 12 to $309 today), they're banking MASSIVE profits. At current prices, these calls have gained roughly $49 per share in intrinsic value alone!

Back-of-envelope P&L calculation: If they originally bought these calls at $30-35 when GOOGL was ~$270-280, they're now selling at $55.05 - that's a 57-83% gain or roughly $12.5-25M in profits on this single position. The decision to close 70 days before expiration (with plenty of time value left) signals they're prioritizing capital preservation over squeezing every last dollar.

Unusual Score: 🔥 HIGHLY UNUSUAL (Z-score 2.2) - This trade volume is 2.2 standard deviations above normal for GOOGL, indicating this is significantly larger than typical institutional activity. The classification shows this happens only a few times per year based on historical patterns.

📈 Technical Setup / Chart Check-Up

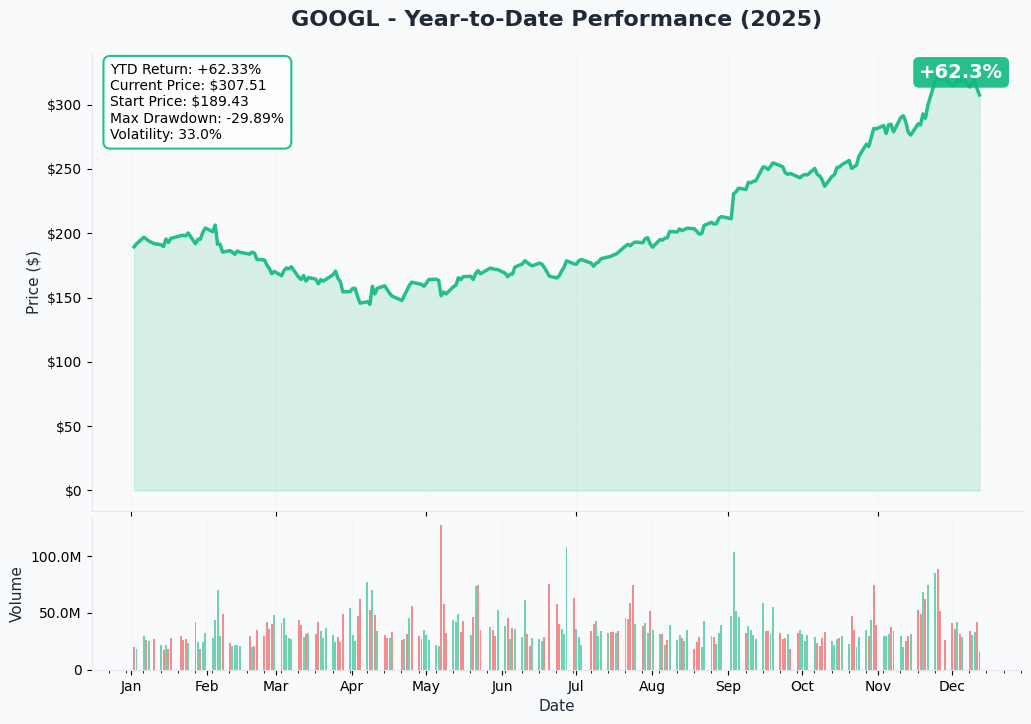

YTD Performance Chart

GOOGL is having a spectacular year with the stock currently trading at $309.04, showcasing powerful AI-driven momentum. The chart reveals a strong uptrend with recent acceleration:

Key observations:

- 🚀 Explosive Q4 rally: Massive move from ~$229 in September to all-time high of $328.83 on November 25, 2025

- 📈 +36.5% in 3 months: Vertical rally driven by Q3 earnings beat ($102.3B revenue milestone) and Gemini 3 AI launch momentum

- 🎯 Technical breakout confirmed: Smashed through $300 psychological resistance with authority

- 📊 Volume surge: Institutional accumulation accelerated in October-November on AI catalysts

- ⚠️ Modest pullback: Currently consolidating 6% below all-time high after meteoric rise

The recent pullback from $328.83 to $309 represents healthy profit-taking after an unsustainable vertical move. Smart money (like this $28M call seller) is capitalizing on the rally.

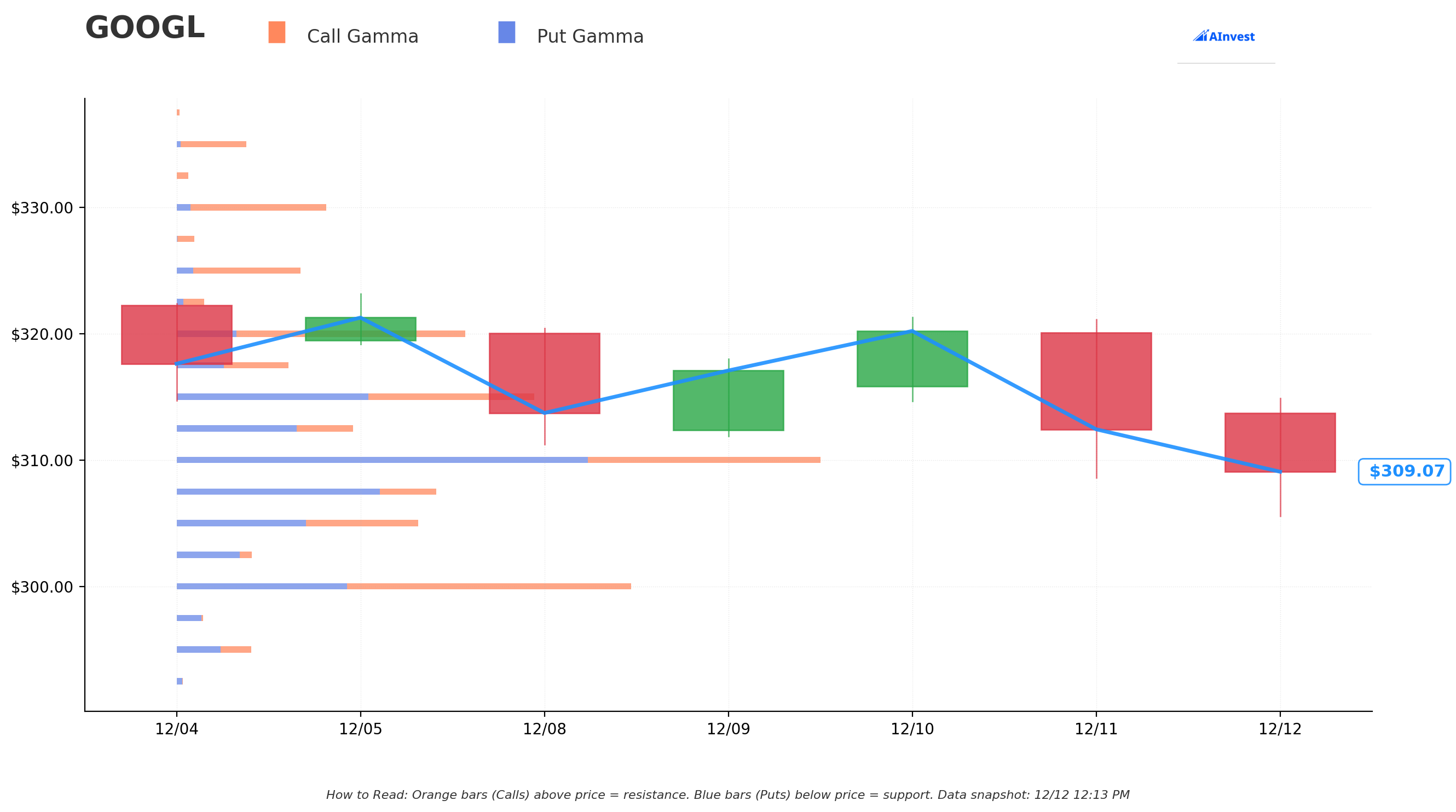

Gamma-Based Support & Resistance Analysis

Current Price: $309.20

The gamma exposure map reveals critical price magnets that will govern near-term trading:

🔵 Support Levels (Put Gamma Below Price):

- $307.50 - Immediate support with 31.8B total gamma (0.55% below price - STRONGEST nearby floor!)

- $305 - Secondary support at 29.5B gamma (1.36% below)

- $300 - Major psychological and technical floor with 56.6B gamma (2.98% below - this is the LINE IN THE SAND)

- $290 - Deep support at 23.6B gamma (6.2% below - disaster scenario floor)

🟠 Resistance Levels (Call Gamma Above Price):

- $310 - Immediate ceiling with 79.9B gamma (0.26% overhead - STRONGEST RESISTANCE level on entire chart!)

- $312.50 - Secondary resistance at 22.4B gamma (1.07% above)

- $315 - Major resistance zone with 46.8B gamma (1.87% above)

- $320 - Extended ceiling at 37.1B gamma (3.49% above)

- $330 - Major upside target with 18.3B gamma (6.73% above)

- $350 - Extended bull target at 16.4B gamma (13.2% above)

What this means for traders: GOOGL is pinned between massive $307.50 support and crushing $310 resistance. The gamma data shows the $310 level with 79.9B gamma is THE single largest concentration on the entire options chain - creating natural selling pressure as dealers hedge their exposure. This setup screams "tight consolidation range" before the next major catalyst.

The $300 level with 56.6B gamma is THE critical support - this combines psychological significance (round number) with massive put gamma wall. Break below $300 and momentum could accelerate toward $290.

Notice the trade positioning? The call seller closed at $260 strike - they're not making a bearish bet on GOOGL. They're simply banking profits on a position that's already $49 in-the-money. They likely see the $310 gamma ceiling creating near-term resistance and decided to lock in gains rather than wait for potential breakout.

Net GEX Bias: Bullish (307.2B call gamma vs 248.3B put gamma) - Overall positioning remains constructive, but immediate price action constrained by massive overhead resistance at $310.

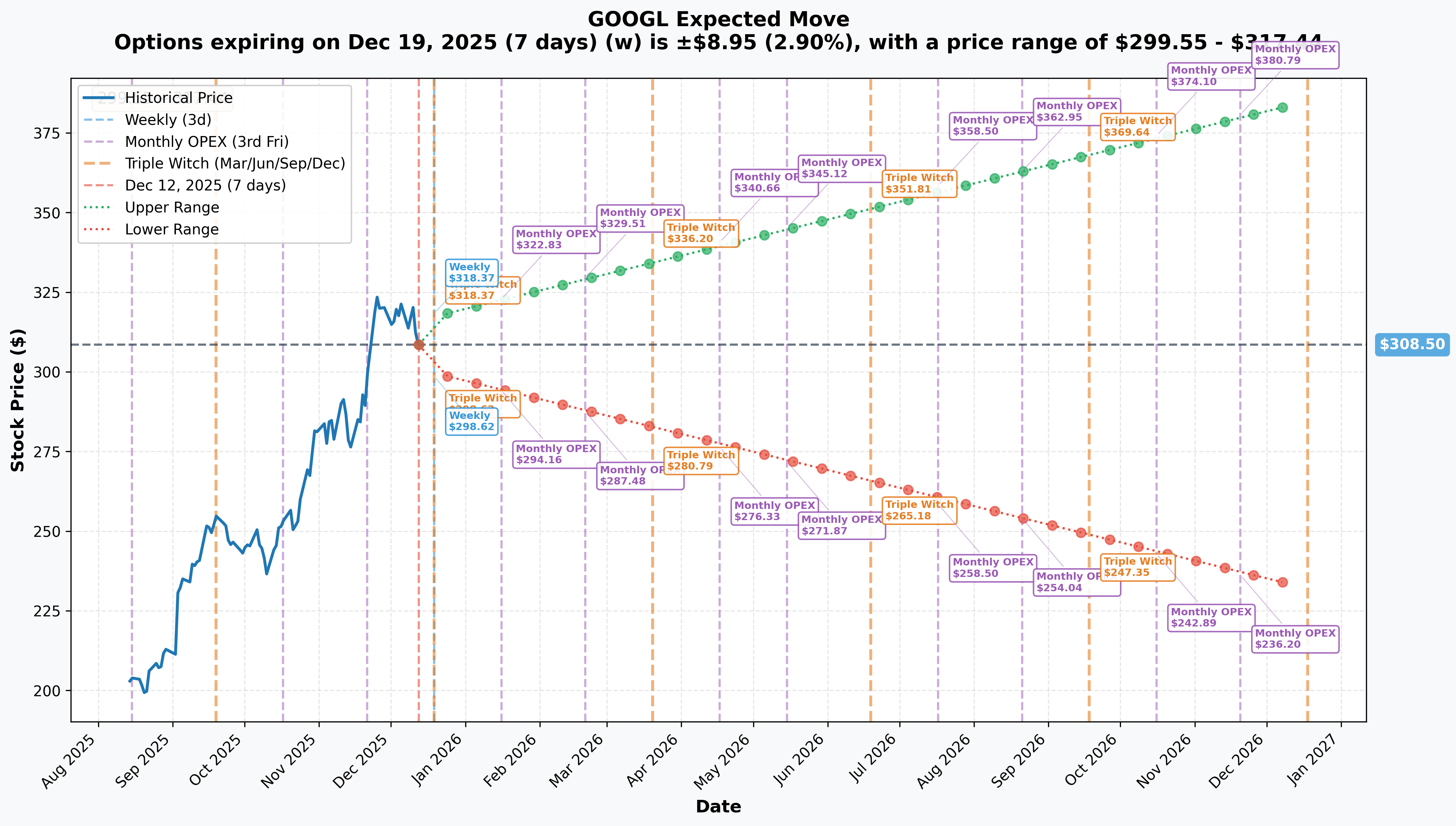

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Dec 19 - 7 days - Triple Witch!): ±$8.95 (±2.9%) → Range: $299.55 - $317.44

- 📅 Monthly OPEX (Jan 16 - 35 days): ±$14.32 (±4.65%) → Range: $294.16 - $322.83

- 📅 Quarterly Triple Witch (Mar 20 - 98 days): ±$27.90 (±9.05%) → Range: $280.79 - $336.20

- 📅 Yearly LEAPS (Dec 18, 2026 - 371 days): ±$76.56 (±24.82%) → Range: $231.93 - $385.06

Translation for regular folks: Options traders are pricing in a 2.9% move ($9) through December 19 for the upcoming weekly triple witch expiration. However, the February 20th expiration (when this call seller's position expires) implies a larger move as it captures the critical Q4 earnings on February 3, 2026.

The February options are pricing approximately ±5-6% move through earnings, which is relatively modest for a mega-cap tech stock that just reported first-ever $100B+ quarterly revenue. This suggests the market expects less volatility than historical patterns might indicate.

Key insight: The call seller is exiting BEFORE the February 3rd earnings event, choosing to pocket $28M in certain profits rather than gambling on continued upside through the binary catalyst. They're trading certainty for potential upside - a classic institutional risk management move.

🎪 Catalysts

🔥 Upcoming Catalysts (Next 60 Days)

Q4 2025 Earnings - February 3, 2026 (52 DAYS!) 📊

GOOGL reports fiscal Q4 results on Tuesday, February 3, 2026 after market close. This is THE major catalyst on the calendar that could determine if the stock breaks out above $320 or pulls back to $290 support.

Wall Street consensus and key watch items:

- 📊 Consensus EPS: $2.63 for Q4

- 🤖 Google Cloud Growth: Critical to watch if 34% YoY growth trajectory continues

- 💰 AI Monetization: Impact of AI Overviews reaching 2 billion monthly users on Search revenue

- 📺 YouTube Revenue: Q4 historically faces tough comp due to election ad spend in prior year Q4 2024

- 💸 2026 CapEx Guidance: Management indicated "significant increase" expected - exact numbers matter

Key Q3 2025 performance (reported October 29) for context:

- Revenue: $102.3B (up 16% YoY) - FIRST $100B+ quarter ever

- Net Income: $35.0B (up 33% YoY)

- EPS: $2.87 (up 35% YoY) vs $2.33 estimated - major beat

- Google Cloud: $15.2B (up 34% YoY) with operating income $3.6B

- Stock reaction: +5.24% following results

Upside potential: If Google Cloud maintains 34%+ growth and management shows progress monetizing AI Overviews generating 10%+ additional queries, stock could challenge $330-340 range.

Downside risk: Any disappointment in YouTube revenue (facing election spend comp), margin compression from rising CapEx, or conservative 2026 guidance could trigger sharp selloff back to $290-300 support zone.

🚀 Recent Catalysts (Last 30 Days) - Already Happened

Gemini 3 AI Model Release - December 2025 🤖

Google launched its most powerful AI model Gemini 3 in early December 2025, marking a major milestone in the AI race:

- 🏆 Leading performance: 1487 Elo score on WebDev Arena, 54.2% on Terminal-Bench 2.0, 76.2% on SWE-bench Verified

- 🎯 Validates Google's full-stack AI approach against Microsoft/OpenAI partnership

- 💰 Provides ammunition to monetize AI products more aggressively in 2026

Gemini Deep Research Agent - December 11, 2025 🔬

Google launched Gemini Deep Research tool achieving 46.4% on Humanity's Last Exam and 66.1% on DeepSearchQA - released SAME DAY as OpenAI's GPT-5.2 in direct competitive response. Shows Google is aggressively defending AI leadership position.

U.S. Department of Defense AI Contract - December 9, 2025 🇺🇸

DOD CDAO selected Gemini for Government to power GenAI.mil platform serving 3 million military personnel. This validates Google Cloud's security and reliability at the highest national security level - major competitive advantage in government/enterprise markets.

AI Glasses Announcement - December 8, 2025 👓

Google announced first AI-powered smart glasses with Gemini to launch in 2026, competing directly with Meta's established smart glasses business. Expands AI monetization beyond search and cloud.

Antitrust Remedies Decision - December 8, 2025 ⚖️

Judge Mehta issued 95-page final decision rejecting DOJ's most severe remedy (forced Chrome divestiture) while mandating data sharing with rivals. This is BETTER than feared - avoided worst-case scenario but still creates future competitive challenges.

Key points:

- ✅ Chrome divestiture rejected - preserves search distribution channel

- ⚠️ Data sharing mandated - could erode competitive moat

- 📈 GenAI products fall within scope despite Google objections

- 🔄 Google plans appeal - multi-year process ahead

📊 Strategic Catalysts (Q1-Q2 2026)

Google Cloud Growth Acceleration 💰

Google Cloud's $155B backlog (up 82% YoY, up 46% QoQ) signals sustained revenue growth through 2026:

- 🎯 More $1B+ deals closed in 9 months of 2025 than all of 2023-2024 combined

- 📈 34% YoY customer growth

- 🤖 70%+ of existing customers use AI products

- 💼 Major contracts: $10B Meta deal (6 years), Anthropic TPU deal worth tens of billions

- 🎯 On pace for $61B annual run rate

AI Monetization Scaling 🚀

- 🌍 AI Overviews reaching 2 billion monthly users - driving 10%+ additional queries where deployed

- 📱 Gemini app surpasses 650 million monthly users

- 🔥 GCP AI products grew 200%+ YoY in Q3

- ⚠️ Offset risk: Publisher traffic down 20-30% creating potential antitrust liability

Pixel Hardware Momentum 📱

Pixel 9 series achieving 105% YoY growth in H1 2025, breaking into top 5 premium brands globally:

- 📊 U.S. market share: 6.1% (up from 0.1% in Sept 2022)

- 🚀 Record single-month sales in September 2025 with 28% YoY growth

- 💰 Approaching profitability as business scales

Wiz Acquisition Close - 2026 🔒

$32B all-cash acquisition of cloud security company expected to close in 2026 - largest acquisition in Alphabet history. Enhances Google Cloud's security portfolio and competitive positioning against Azure/AWS.

⚠️ Risk Catalysts

Ad Tech Antitrust Case - Remedies Expected Q1 2026 ⚖️

Judge Brinkema ruled against Google in April 2025 on 2 of 3 counts, finding unlawful monopolization of publisher ad server and ad exchange markets:

- ⏰ Closing arguments held November 17, 2025 - final remedies decision expected early 2026

- 💣 DOJ seeking structural divestment of AdX - would eliminate significant revenue stream

- 💰 Network revenue: $7.4B in Q3 (~$30B annualized)

- 🔄 Google plans appeal regardless of outcome

Publisher Litigation Risk 📉

- 🇪🇺 European Commission complaint (June 30, 2025) alleges AI Overviews cause "significant harm"

- 📚 Chegg lawsuit citing 49% traffic loss and revenue decline from AI features

- ⚠️ Potential billion-dollar litigation exposure if pattern continues

Macroeconomic Headwinds 🌐

- 📺 Q4 election spend comp creates tough YoY comparison for YouTube (potential -15% headwind)

- 💵 FX volatility impacts international revenue

- ⚠️ Recession risk would impact brand advertising budgets

- 💸 $91-93B 2025 CapEx with "significant increase" in 2026 requires sustained ROI

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and catalyst timeline, here are scenarios through February 20th expiration:

📈 Bull Case (35% probability)

Target: $340-$360

How we get there:

- 💪 Q4 earnings CRUSH with revenue exceeding consensus and strong 2026 guidance

- 🚀 Google Cloud maintains 34%+ growth, converts $155B backlog faster than expected

- 🤖 AI monetization evidence accelerates - AI Overviews showing measurable revenue impact

- 📊 Operating margins expand despite CapEx increase, proving efficiency gains

- 🌐 Market share gains in cloud accelerate toward Azure's 22% from current 12%

- ⚖️ Ad tech antitrust remedies come in LIGHTER than feared

- 📈 Breakout above $320 gamma resistance triggers technical buying to $350 (yearly LEAPS upper range)

Key metrics needed:

- Google Cloud revenue $17B+ in Q4 (maintaining 30%+ growth)

- YouTube revenue growth positive despite election comp

- Operating margins 33%+ excluding one-time items

- 2026 revenue guidance $450B+ (15%+ growth)

Analyst support: JPMorgan $385 price target, Wolfe Research $350 target, Guggenheim $375 target

Probability assessment: 35% because fundamentals are excellent (Q3 beat, strong AI momentum) but stock already up 36.5% in 3 months and faces tough Q4 comp. Need perfect execution to justify higher multiple from 30.8x P/E.

🎯 Base Case (45% probability)

Target: $295-$320 range (CONSOLIDATION)

Most likely scenario:

- ✅ Solid Q4 earnings meeting or slightly beating consensus

- 📱 Google Cloud growth moderates to 28-30% YoY (still strong but decelerating)

- 🤖 AI monetization progressing but not spectacular - steady improvements without fireworks

- ⚖️ YouTube growth flat to slightly negative due to election comp as expected

- 💰 2026 guidance in-line with street expectations

- ⚠️ Antitrust overhang continues with appeal process beginning

- 🔄 Trading within $300 gamma support and $320 resistance bands for weeks

- 💤 Multiple compression from 30.8x toward 28-29x as growth moderates

- 📊 Market digests rapid 3-month rally, waits for next major catalyst

This is exactly why the call seller is taking profits: Stock likely consolidates in $300-320 range, making it optimal to lock in $49/share of intrinsic value now rather than risk giving back gains through consolidation or pullback. The $28M received represents exceptional execution on a winning trade.

Why 45% probability: Most realistic outcome given strong fundamentals offset by extended valuation after massive rally. Institutional players (like this seller) typically see limited near-term upside after vertical moves and choose to rotate capital elsewhere.

📉 Bear Case (20% probability)

Target: $270-$295 (PULLBACK TO MAJOR SUPPORT)

What could go wrong:

- 😰 Earnings miss or guidance disappoints - even small miss magnified at 30.8x P/E

- 🚨 YouTube revenue significantly negative (worse than -10%) due to election comp

- 📉 Google Cloud growth decelerates below 25% - would question AI monetization thesis

- ⏰ AI Overviews shown to cannibalize high-margin Search without adequate replacement revenue

- 💸 2026 CapEx guidance MASSIVE increase (>$120B) compressing margins without clear ROI timeline

- ⚖️ Ad tech antitrust ruling HARSH with forced divestiture ordered

- 🇪🇺 Additional publisher lawsuits or regulatory actions in EU

- 💰 Broader tech selloff (Magnificent 7 rotation) drags GOOGL lower

- 🔨 Break below $300 gamma support triggers cascade to $290, then $280

Critical support levels:

- 🛡️ $300: Major psychological/technical floor with 56.6B gamma - MUST HOLD

- 🛡️ $295: Implied move lower range support

- 🛡️ $290: Deep support with 23.6B gamma

- 🛡️ $280: Disaster scenario floor (not priced in current options)

Probability assessment: Only 20% because fundamentals remain strong (Q3 results, $155B cloud backlog, AI leadership, avoided Chrome divestiture). Requires multiple negative catalysts to align. However, the institutional call sale shows smart money is at least hedging against this scenario.

Call seller P&L already locked in:

- Sold at $55.05 with $49 intrinsic value

- Even in bear case with stock at $270 in February: calls would be worth $10 (intrinsic only)

- By selling now at $55.05 vs $10 future value = $45.05 per share better exit = additional $22.5M saved!

- This demonstrates WHY sophisticated traders don't wait for "perfect" exit - they take great profits when available

💡 Trading Ideas

🛡️ Conservative: Follow Smart Money - Book Profits

Play: If you own GOOGL stock or calls with gains, consider trimming 25-50% position

Why this works:

- 🎯 Institutional trader just showed us the playbook - take chips off table at $309 levels

- 💰 Stock up 36.5% in 3 months - that's PHENOMENAL, don't get greedy

- 📊 Trading at all-time high range with $310 massive gamma resistance overhead

- ⏰ Q4 earnings 52 days away creates binary event risk

- 🎢 Implied move only ±2.9% weekly suggests limited near-term upside before consolidation

- 🤔 When institutions book $28M profits, retail should pay attention

- 💸 Can always re-enter lower ($295-300) if pullback occurs or post-earnings

Action plan:

- 📈 Sell 25-50% of GOOGL holdings between $308-312 (current range)

- 🎯 Place limit orders to sell remaining position at $320 (gamma resistance)

- 💰 Hold cash for potential re-entry at $295-300 support post-earnings

- ✅ Lock in life-changing gains if you bought below $250

- ⏰ If holding calls, close anything with <60 days to expiration NOW (avoid theta decay through earnings)

Risk level: Minimal (taking profits) | Skill level: Beginner-friendly

Expected outcome: Bank 30%+ gains on trimmed position. Reduce exposure to earnings volatility. Maintain optionality with remaining position.

⚖️ Balanced: Post-Earnings Bull Put Spread

Play: After Q4 earnings, sell put spread targeting major gamma support

Structure: Sell $300 puts, Buy $290 puts (March 20 expiration - after earnings)

Why this works:

- 🎢 IV crush post-earnings makes put selling more attractive - collect premium after volatility drops

- 📊 $300 has massive 56.6B gamma support - dealers will defend this level aggressively

- 🎯 Defined risk spread ($10 wide = $1,000 max risk per spread)

- 💰 Targets 3% downside cushion from current price - only loses if stock drops >6%

- ⏰ March expiration gives 98 days, plenty of time for any post-earnings dip to recover

- 🛡️ Protects against modest pullback while generating income if consolidation continues

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Collect ~$2.00-2.50 credit per spread post-earnings (vs $1.50 now)

- 📈 Max profit: $200-250 if GOOGL above $300 at March expiration (keep full credit)

- 📉 Max loss: $750-800 if GOOGL below $290 (defined and limited)

- 🎯 Breakeven: ~$297.50-298

- 📊 Risk/Reward: ~1:3 (risk $750 to make $250) which is typical for credit spreads

- 🎲 Probability of profit: ~75% (stock would need to drop 6% for max loss)

Entry timing:

- ⏰ Wait 2-3 days post-earnings (February 5-6) for full IV collapse

- 🎯 Only enter if stock above $305 (gives room to work)

- ❌ Skip if stock already below $300 (too close to strike)

- 📊 Check implied volatility - want to see IV drop from current levels to 25-30% range

Position sizing: Risk 2-3% of portfolio maximum (this generates income but has defined risk)

Risk level: Moderate (defined risk, bullish assumption) | Skill level: Intermediate

🚀 Aggressive: Calendar Spread - Harvest Earnings Volatility (ADVANCED!)

Play: Sell near-term volatility, buy longer-term upside

Structure: Sell Jan 16 $310 calls, Buy Mar 20 $310 calls (calendar spread at resistance)

Why this could work:

- 💥 Sell elevated near-term premium while keeping longer-term upside exposure

- 🎯 $310 is massive gamma resistance - stock unlikely to break through before January

- ⏰ Jan 16 calls will suffer theta decay + no earnings catalyst = rapid premium erosion

- 📈 March 20 calls capture Q4 earnings reaction AND post-earnings follow-through

- 🎢 Benefit from IV crush in Jan options while maintaining March vega exposure

- 💡 Sophisticated trade that profits from time decay and volatility structure

Why this could blow up (SERIOUS RISKS):

- 🚀 Stock explodes above $310: Short Jan calls get assigned, lose shares at $310 while stock at $320+

- ⚠️ Assignment risk: If Jan calls go ITM, you could face early assignment (especially pre-earnings)

- 💸 Net debit required: Calendar spreads cost money upfront (typically $3-5 per spread)

- 📉 Loses if stock drops hard: If GOOGL falls to $290, BOTH legs lose value

- 🎯 Narrow profit zone: Only profits if stock stays near $310 through January, then rallies into March

- ⏰ Timing critical: Need to actively manage - can't set and forget

Estimated P&L:

- 💰 Net cost: ~$4-5 per calendar spread (buy March $310 call ~$15, sell Jan $310 call ~$10-11)

- 📈 Max profit zone: Stock at $305-315 at Jan expiration, then rallies to $320+ by March = $6-8 gain (50-100% ROI)

- 📉 Max loss: Stock moves away from $310 in either direction = lose $3-5 (60-100% of premium)

- 🎯 Optimal scenario: Stock consolidates at $308-310 through January, Jan calls expire worthless, March calls gain value from earnings rally

Management rules:

- 🛑 Close if stock breaks above $315 before January (avoid assignment)

- 📊 Take profit if spread value reaches $7-8 (don't get greedy)

- ⏰ Plan to close Jan short leg by Jan 14 regardless (avoid earnings gamma risk)

- 💰 Roll Jan short calls out and up to Feb $315 if stock stable at $310

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Understand calendar spread mechanics and assignment risk

- ✅ Have traded multi-leg spreads through earnings volatility

- ✅ Can actively monitor and adjust position daily

- ✅ Accept limited profit potential in exchange for defined risk

- ✅ Know how to handle early assignment (margin requirements, etc.)

Risk level: HIGH (multi-leg, assignment risk, requires active management) | Skill level: Advanced only

Probability of profit: ~45% (needs specific price action scenario to maximize gains)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q4 earnings binary event (52 days): Results February 3, 2026 after close create significant volatility risk. Stock could gap 5-8% either direction based on Google Cloud growth sustainability, YouTube revenue (facing election comp), AI monetization progress, and 2026 CapEx guidance. Historical precedent shows GOOGL has moved $15-20 on earnings surprises. Options pricing ±5-6% implied move through February expiration.

-

💸 Valuation at 30.8x forward P/E after 36.5% rally: While reasonable for quality, stock has limited multiple expansion room from here. Trading near 52-week high of $328.83 after vertical 3-month move. Requires continued 15%+ revenue growth and margin expansion to justify current price. Any deceleration magnified in stock reaction.

-

⚖️ Dual antitrust threats - Search AND Ad Tech: December 8 Search remedies mandated data sharing that could erode competitive moat. Ad Tech case remedies expected Q1 2026 - potential AdX divestiture would eliminate $7.4B quarterly Network revenue (~$30B annualized). Multi-year appeals process creates ongoing uncertainty. Both cases could compress margins through compliance costs and lost revenue opportunities.

-

🤖 AI monetization uncertainty - cannibalizing high-margin Search: AI Overviews reaching 2 billion users and driving 10%+ additional queries, but revenue per AI-triggered query potentially 30-50% lower than traditional search. Publisher traffic down 20-30% creates litigation risk (Chegg lawsuit 49% traffic loss, EU complaints). Net impact on profitability unclear - could be trading high-margin Search clicks for lower-margin AI interactions.

-

💰 YouTube Q4 comp headwind: Election ad spending in Q4 2024 creates tough year-over-year comparison. YouTube revenue could face potential -15% growth drag in Q4 2025 despite strong underlying trends. Even with Shorts monetization improving and CTV leadership, comp is brutal.

-

🏦 CapEx pressure on margins: $91-93B 2025 CapEx with "significant increase" expected in 2026 - could reach $110-120B. While investing in AI infrastructure, requires sustained Google Cloud growth and AI product ROI to justify. Operating margins could compress in near-term even with strong revenue growth. Street will scrutinize CapEx efficiency carefully.

-

🌐 Google Cloud still trails Azure by 10 points market share: Despite 34% growth and $155B backlog, Google Cloud at 12% market share vs Azure 22%. Azure's Office 365 integration creates powerful lock-in effect. Google needs to accelerate enterprise wins to close gap, but incumbent advantages are real.

-

🐋 Smart money booking $28M at $309 signals near-term caution: This institutional trade closing $260 calls at $55.05 shows sophisticated players taking profits rather than holding through earnings. When funds managing hundreds of millions choose certain $49 intrinsic value over potential $60-70, it signals limited near-term upside expected. The 5,000 contract size (literally unprecedented for closing trades) shows this isn't routine rebalancing - this is conviction profit-taking.

-

📊 Gamma ceiling at $310 creates mechanical resistance: Massive 79.9B call gamma at $310 (largest single level on entire chain) means market makers will systematically SELL into rallies above $310 to hedge their exposure. This creates powerful technical resistance making breakouts difficult without sustained institutional buying. Current price ($309) sitting right under this ceiling suggests near-term capping.

-

🎢 Post-rally consolidation likely even without negative catalyst: 36.5% gain in 3 months represents unsustainable vertical move. Technical pullback to $295-300 would be HEALTHY and normal after such explosive rally. Don't mistake normal consolidation for fundamental deterioration. However, if you're sitting on huge gains like this call seller, why risk giving back profits during consolidation?

-

🌍 Macroeconomic sensitivity - ad spend cyclical: At $3.77T market cap, GOOGL needs flawless execution to grow into valuation. Any macroeconomic weakness hits advertising budgets first. Recession risk would impact both Search ads and YouTube simultaneously. Unlike subscription businesses, advertising is highly cyclical. Strong balance sheet provides cushion but revenue growth would decelerate.

🎯 The Bottom Line

Real talk: Someone just banked $28 MILLION in profits on a winning GOOGL call position - and they did it 52 days BEFORE the Q4 earnings catalyst on February 3, 2026. This isn't bearish on Alphabet's incredible story (Q3 beat, AI leadership, $155B cloud backlog) - it's textbook institutional profit-taking after a 36.5% three-month moonshot.

What this trade tells us:

- 🎯 Sophisticated winner choosing CERTAINTY over GREED - locking in $49/share intrinsic value now vs gambling on $60+

- 💰 They made their money (likely bought $260 calls when stock was $270-280) and aren't interested in "squeezing last drop"

- ⚖️ The decision to exit with 70 days remaining and $6 time premium shows zero interest in holding through earnings volatility

- 📊 They see $310 gamma resistance overhead and limited near-term catalyst to push higher before consolidation

- ⏰ Closing BEFORE earnings (rather than after) reveals risk management priority over maximum profit

This is NOT a "sell everything" signal - it's a "don't be greedy, take some profits" signal.

If you own GOOGL stock:

- ✅ Consider trimming 25-40% at $308-312 levels if you have meaningful gains (lock in winners)

- 📊 Set mental stop at $300 (major gamma support with 56.6B) to protect remaining position

- ⏰ Don't fight the tape when institutions show their cards - they have more information and resources

- 🎯 Can always re-enter at $295-300 if post-earnings pullback occurs with better risk/reward

- 💰 If you're up 30-50%+ on your position, TAKE SOME CHIPS OFF THE TABLE - you already won!

If you own GOOGL calls:

- ⏰ Close ANY calls with <60 days to expiration NOW (avoid theta decay accelerating into earnings)

- 💸 Roll profitable short-dated calls out to March/April expiration to capture post-earnings move

- 🎯 Consider selling calls against stock holdings (covered calls at $315-320 strikes)

- 📊 If holding long-dated LEAPs with massive gains, trim 50% and let winners run on house money

- 🛡️ Book 7-figure gains when you have them - this institutional trader just showed you how it's done

If you're watching from sidelines:

- ⏰ February 3, 2026 after close is THE moment of truth - DO NOT chase into earnings!

- 🎯 Post-earnings dip to $295-305 would be EXCELLENT entry with 5-7% margin of safety

- 📈 Looking for confirmation: Google Cloud 30%+ growth maintained, AI monetization evidence, YouTube stability despite comp

- 🚀 Longer-term (6-12 months), cloud backlog conversion and AI product launches support $340-360 if execution delivers

- ⚠️ Current setup (massive gamma resistance at $310, recent vertical rally, pre-earnings) = TERRIBLE risk/reward for new longs

If you're bearish:

- 🎯 First test comes at $300 support (56.6B gamma wall) - that's your line in sand

- 📉 Break below $300 opens door to $290, then $280 on momentum

- ⏰ Post-earnings volatility offers better short entry than fighting current strength

- 📊 Put spreads (after earnings IV crush) offer defined-risk bearish expression

- ⚠️ Don't fight the trend until $300 breaks - premature shorts get steamrolled

Mark your calendar - Key dates:

- 📅 December 19 (Friday) - Weekly/Monthly/Quarterly Triple Witch OPEX (7 days) - potential volatility

- 📅 January 16, 2026 - Monthly OPEX (35 days)

- 📅 February 3, 2026 (Tuesday) after market close - Q4 FY2025 earnings report (52 DAYS!)

- 📅 February 4, 2026 (Wednesday) - Post-earnings price action and analyst reactions

- 📅 February 20, 2026 - Monthly OPEX, expiration of this $28M call trade

- 📅 March 20, 2026 - Quarterly Triple Witch

- 📅 Mid-2025 (Q2) - AI Glasses with Gemini launch expected

Final verdict: Alphabet's long-term trajectory remains SPECTACULAR - first $100B+ quarter, Gemini 3 AI leadership, DOD contract validation, $155B cloud backlog, and avoided Chrome divestiture are all powerfully bullish. BUT, at 30.8x P/E after 36.5% three-month rally sitting under massive $310 gamma resistance with earnings 52 days away, the risk/reward is NEUTRAL AT BEST for aggressive new positioning.

The $28M call sale is a CLEAR signal: smart money is lightening up at the peak, not pressing bets.

Be smart. Take profits if you have them. Wait for better entry ($295-300 post-earnings) if you don't. The AI revolution will still be here in February, and you'll sleep better at night buying dips than chasing rallies. This is a wealth-building marathon, not a FOMO sprint. 💪

Patience pays. Greed costs. Learn from the pros who just banked $28M by knowing when to say "that's enough." 🎯

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The unusual score reflects this specific trade's size relative to recent GOOGL history - it does not imply you should follow the trade or that it represents the "correct" market view. Always do your own research and consider consulting a licensed financial advisor before trading. Earnings create binary event risk with potential for 5-10% gaps either direction. The call seller may have complex portfolio management needs not applicable to retail traders. This trade represents profit-taking on a winning position, not a new bearish bet.

About Alphabet Inc.: Alphabet is a holding company that owns internet giant Google, generating approximately 90% of revenue from Google's advertising and subscription services (Search, YouTube, Play Store, devices) and 10% from Google Cloud. The company operates Waymo (autonomous vehicles), Verily (health tech), and other moonshot ventures, with a market cap of $3.77 trillion in the Computer Programming & Data Processing Services industry.