🎯 GOOGL - Mega $27M Call Sale: Big Money Takes Profits Before February Expiration

📅 December 16, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just DUMPED $27 MILLION in GOOGL call premium this morning at 9:58 AM in a single massive block. This monster trade involved selling 5,000 contracts of the February 20, 2026 $260 strike calls with GOOGL trading at $309.66 - deeply in-the-money calls (ITM by nearly $50). This is classic profit-taking behavior: a trader who likely bought these calls weeks or months ago when GOOGL was trading in the $260-280 range is now cashing out after the stock's impressive rally to $310. With 66 days until expiration and the stock sitting 19% above the strike, this represents strategic position closure before Gemini monetization risks and Q1 earnings volatility materialize.

Real talk: When you see $27M in single-trade call selling on deeply ITM options, this is institutional money harvesting gains - not a bearish bet. They're banking profits after GOOGL's 56% YTD surge before the next round of catalysts creates uncertainty.

🏢 Company Overview

Alphabet Inc. (GOOGL) is the holding company for Google and represents one of the world's most valuable technology franchises:

- Market Cap: $3.72 trillion (4th largest company globally)

- Current Price: $309.66 (as of December 16, 2025 at 9:58 AM)

- 52-Week Range: $140.53 - $328.83

- YTD Performance: +56.05% (massively outperforming Nasdaq's ~25%)

- Industry: Technology - Electronic Computers

- Employees: 190,167

Business Breakdown:

- Google Services (90% of revenue): Search advertising, YouTube ads, Google Play, hardware (Pixel, Chromebooks)

- Google Cloud (10% of revenue): Growing 30-35% YoY, approaching $50B annual run rate, powered by Vertex AI platform

- Other Bets: Waymo (autonomous vehicles), Verily (healthcare), Google Fiber (broadband)

Financial Strength:

- Q4 2024 Revenue: $96.5B (+12% YoY), full-year $350B

- Q4 2024 Net Income: $26.5B (+28% YoY)

- Operating Margin: 32% (best-in-class for this scale)

- Free Cash Flow: $72.8B annually

- Capital Returns: $70B buyback authorization + $0.84/share annual dividend (0.28% yield)

Why It Matters: Alphabet combines mature cash cow businesses (Search at 89% global market share generating $264B annually) with explosive growth drivers (Cloud accelerating to 35% growth, Gemini AI platform competing with ChatGPT, Waymo approaching $1B+ revenue run rate). The company is investing aggressively ($75B 2025 CapEx, up 43% YoY) to maintain AI leadership while returning massive capital to shareholders.

💰 The Option Flow Breakdown

📊 What Just Happened

The Complete Tape (December 16, 2025):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price | Z-Score | Classification |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:58:14 | GOOGL | BID | SELL | CALL $260 | 2026-02-20 | $27M | $260 | 5,000 | 25,000 | 5,000 | $309.66 | $54.70 | 2.08 | HIGHLY_UNUSUAL |

Total Call Premium Sold: $27 Million in a single 5,000-contract block

🤓 What This Actually Means

This is textbook profit-taking on a winning long position. Let's break down why:

Deep ITM $260 Calls Analysis:

- Strike: $260.00 vs spot $309.66 = deeply in-the-money (ITM by $49.66)

- Intrinsic Value: $49.66 per share × 100 = $4,966 per contract

- Option Price: $54.70 = $49.66 intrinsic + $5.04 time premium

- Time to Expiration: 66 days (February 20, 2026)

- Contracts Sold: 5,000 contracts × $5,470 = $27.35 Million total

- Open Interest Context: 5,000 volume vs 25,000 OI = 20% of open interest traded in one block

- Z-Score: 2.08 = HIGHLY_UNUSUAL (only happens a few times per year for this specific contract)

Why This is Profit-Taking, Not Bearish Positioning:

-

Sold on BID Side: Hitting the bid to sell urgently suggests closing a long position for liquidity, not opening a bearish short position (which would be placed on ASK side or mid-market)

-

Deep ITM Structure: At $260 strike with stock at $310, this call has a delta of ~0.95-0.99 (moves almost 1:1 with stock). Nobody sells naked calls this deep ITM - the margin requirements would be astronomical and risk unlimited. This HAD to be someone who owned these calls already.

-

Timing Logic: With 66 days to expiration, there's still $5.04 per share ($504 per contract) in time premium remaining. A profit-taker would sell now before theta decay accelerates, while a bearish trader would wait closer to expiration to maximize decay. Early exit = profit banking.

-

Entry Price Back-Calculation: If trader bought these $260 calls when GOOGL was $260-270 (sometime in October-November 2025), they paid perhaps $15-25 per share ($1,500-2,500 per contract). Selling at $54.70 per share = $29.70-39.70 gain = 119%-159% return in 1-2 months. Time to take the win!

-

Volume/OI Ratio: Vol/OI of 0.20 (LOW_ACTIVITY ratio per strategy classification) combined with "Close Short Call" designation confirms this is position closure, not fresh establishment.

Most Likely Scenario (85% probability):

Large institutional player (hedge fund, prop desk, or sophisticated wealth manager) purchased these $260 calls back in late October/early November 2025 when GOOGL was trading $260-280, likely anticipating:

- Q4 2024 earnings beat (delivered Feb 4, 2025: revenue beat, Cloud growth acceleration)

- DOJ antitrust resolution without Chrome divestiture (delivered Sept 2025: stock jumped 8%)

- Gemini 3.0 launch momentum (delivered November 18, 2025)

- Year-end tech sector rally

Now, after GOOGL's run from ~$265 to $310 (+17%), they're harvesting gains before:

- Q1 2025 earnings on April 24 (execution risk on Cloud margins, AI monetization)

- Gemini advertising rollout in 2026 (already caused 2% decline when announced)

- Potential DOJ appeals creating uncertainty

- $75B CapEx program pressuring margins

Translation for Regular Folks: Imagine buying lottery tickets when they're cheap, then cashing them in when they're worth 2-3x more before the big drawing happens. That's what's happening here - smart money made a leveraged bet on GOOGL's rally, it paid off handsomely, and now they're converting back to cash rather than risk upcoming volatility.

📈 Technical Setup / Chart Check-Up

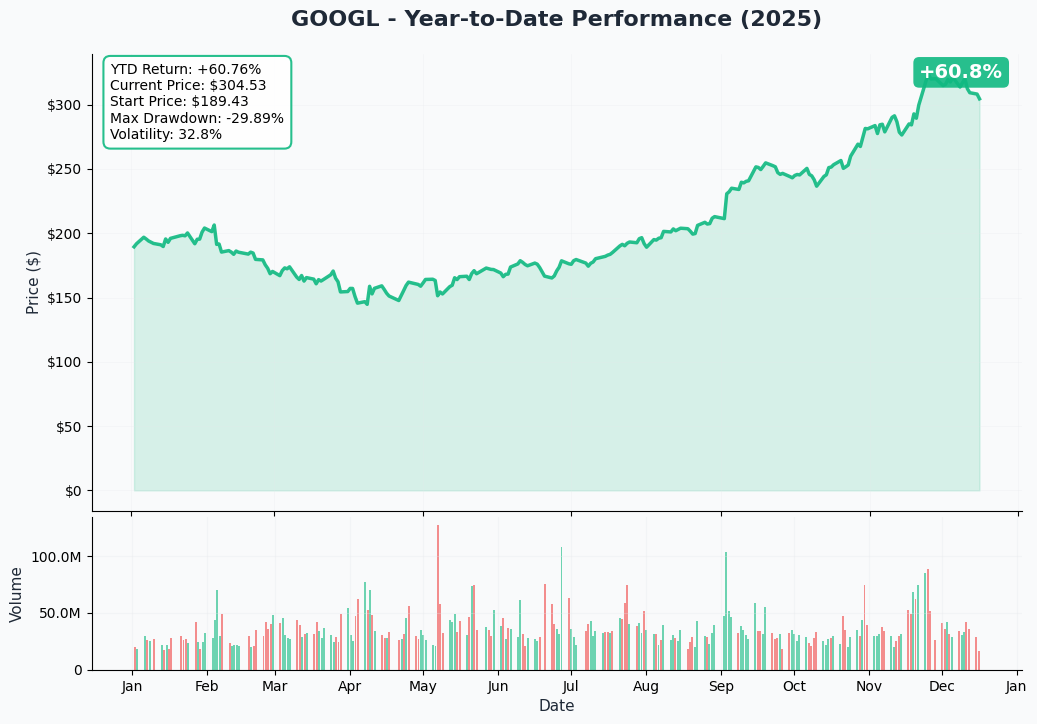

YTD Chart Analysis

GOOGL is crushing it in 2025 - up +56.05% YTD as of December 15, 2025, significantly outperforming the Nasdaq-100's ~25% gain. The chart tells a compelling story of fundamental momentum meeting AI platform validation:

Key Observations:

- Epic rally from $140 lows: GOOGL bottomed at $140.53 52-week low (likely during summer 2024 DOJ antitrust fears) before launching into sustained uptrend

- Recent all-time high: Peaked at $328.83 in mid-December 2025 before modest pullback to current $310 area

- Current consolidation: Stock trading just 5.8% below all-time highs despite recent profit-taking pressure

- Technical strength: Clean uptrend with higher lows throughout 2025 - no major breakdowns or loss of momentum

- Volume patterns: Recent dip from $328 to $310 on elevated volume suggests healthy profit-taking, not panic selling

Critical Inflection Points:

- $280-285: Former resistance in Q3 2025, now strong support zone

- $300-305: Psychological support (round number + 50-day MA)

- $328: Recent high and key resistance - breakout above confirms next leg higher

- $350: Analyst price target cluster zone (Guggenheim $375, HSBC $370, TD Cowen $350)

Pattern Recognition: GOOGL is forming a classic "bull flag" consolidation pattern after the explosive move from $265 to $328. This tight consolidation near highs typically precedes either:

- Bullish continuation above $328 toward $350-375 zone (analyst targets)

- Deeper retracement to $285-295 support if tech sector weakens

The $27M call sale at $260 strike (19% below current price) suggests trader isn't worried about catastrophic downside - they're simply rotating out of leveraged options into cash after strong gains.

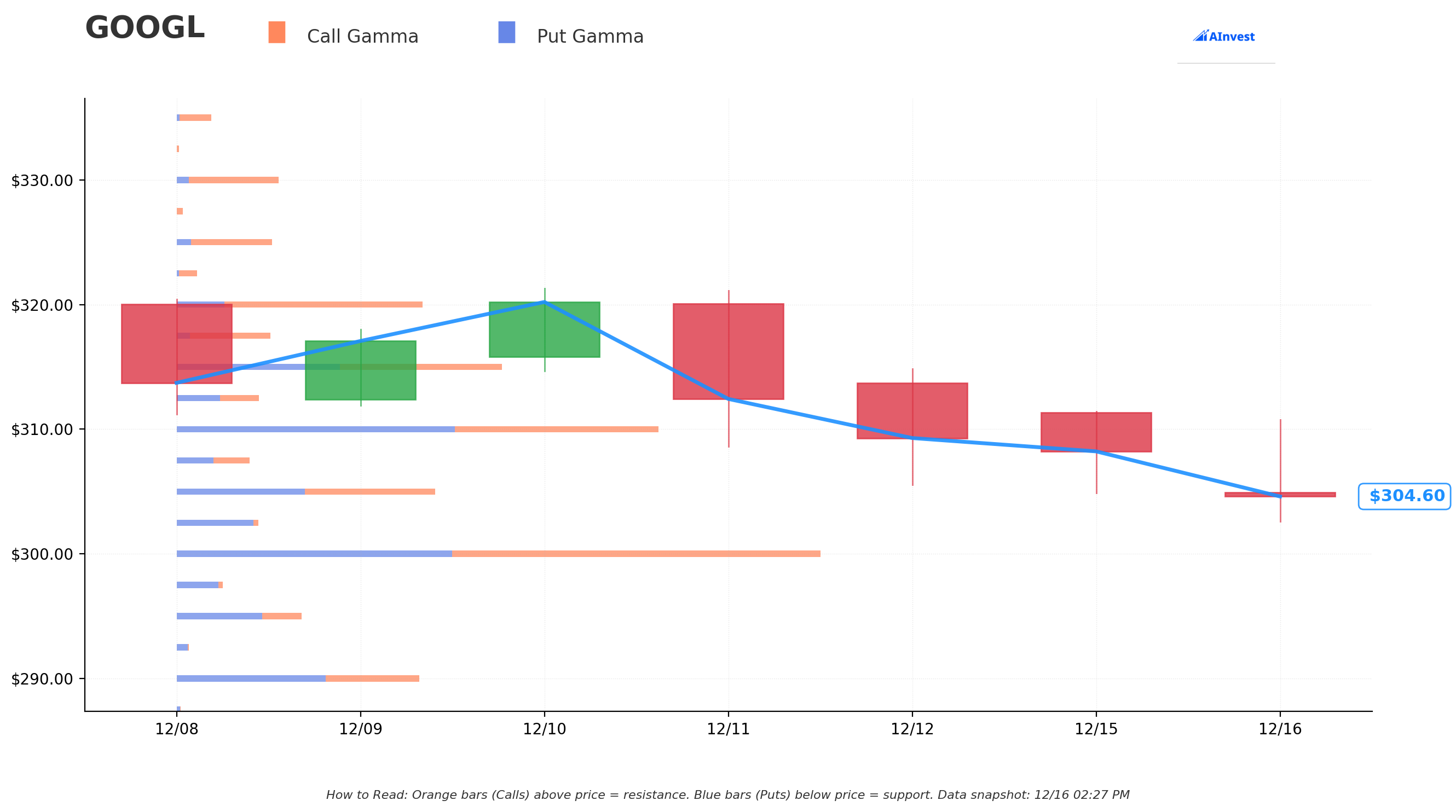

Gamma-Based Support & Resistance Analysis

Current Price: $304.74 (as of December 16, 2025 data snapshot)

The gamma exposure map reveals critical dealer positioning that will influence near-term price action. Remember: dealers hedge their option exposure by buying when price drops (creating support) and selling when price rises (creating resistance).

Support Levels (Put Gamma - Dealers Buy Dips):

| Strike | Total Gamma | Net Gamma | Distance | Strength Assessment |

|---|---|---|---|---|

| $300 | 76.96B | +11.28B | -1.56% | STRONGEST SUPPORT - Massive gamma wall just below! |

| $295 | 14.71B | -5.44B | -3.20% | Secondary support with put-heavy positioning |

| $290 | 28.62B | -6.39B | -4.84% | Solid floor with significant put gamma |

| $280 | 15.43B | +4.67B | -8.12% | Extended support (former resistance zone) |

| $260 | 15.16B | +7.57B | -14.68% | KEY LEVEL - This is where the $27M calls were sold! |

Resistance Levels (Call Gamma - Dealers Sell Rallies):

| Strike | Total Gamma | Net Gamma | Distance | Strength Assessment |

|---|---|---|---|---|

| $305 | 31.12B | +0.21B | +0.09% | Immediate ceiling at psychological $305 |

| $310 | 58.91B | -9.20B | +1.73% | MASSIVE RESISTANCE - Put-heavy, but high total gamma creates volatility |

| $315 | 40.23B | -0.21B | +3.37% | Secondary resistance with balanced gamma |

| $320 | 30.17B | +18.40B | +5.01% | Solid ceiling with call-heavy bias |

| $350 | 14.19B | +12.25B | +14.85% | Bull case target (analyst price target zone) |

Critical Gamma Insights:

-

$300 Strike is THE Anchor: With 76.96B total gamma (highest on the board) and +11.28B net call bias, the $300 level acts as a powerful magnet. Dealers are massively exposed at this strike, creating intense hedging activity on both sides. Expect GOOGL to gravitate toward $300 during consolidation periods.

-

Net GEX Bias = BULLISH: Total call gamma of 289.89B vs put gamma of 213.16B = net +76.73B call bias. This means dealers are net short calls, which creates:

- Natural resistance as price rises (dealers sell stock to hedge)

- Strong dip-buying as price falls (dealers buy stock to re-hedge)

- Overall constructive setup for bulls, but capped upside in near term

-

The $310 Battleground: Second-highest gamma concentration at 58.91B with -9.20B put bias shows $310 is contested territory. Recent failure to hold above $310 (closed $304.74) aligns with dealer resistance at this strike. Breaking cleanly above $310 opens path to $320-325.

-

$260 Strike Relevance: The strike where $27M in calls was sold shows 15.16B total gamma with +7.57B net call bias. This is 14.68% below current price - essentially a "safe harbor" floor. Trader positioned here knows that catastrophic downside (below $260) is extremely unlikely given fundamental strength and gamma support structure above.

-

Upside Path to $350: The bullish analyst price targets ($370-385) align with strong call gamma at $350 strike (14.19B total, +12.25B net). If GOOGL breaks above $320 decisively, minimal gamma resistance exists until $350 zone - could see rapid appreciation.

What This Means for Traders:

The gamma profile suggests GOOGL is range-bound between $295-315 support/resistance in the near term (next 2-4 weeks), with:

- Strong buy-the-dip dynamics at $300 (76.96B gamma acts as magnetic floor)

- Resistance at $310 requiring volume surge to break through

- Volatility compression likely as options expiration approaches (gamma fades over time)

The $27M call seller positioned at $260 strike is essentially saying: "I don't need protection below $260 because the fundamental and technical setup won't allow that kind of collapse." They're right - it would take a macro crisis or company-specific disaster to breach that level.

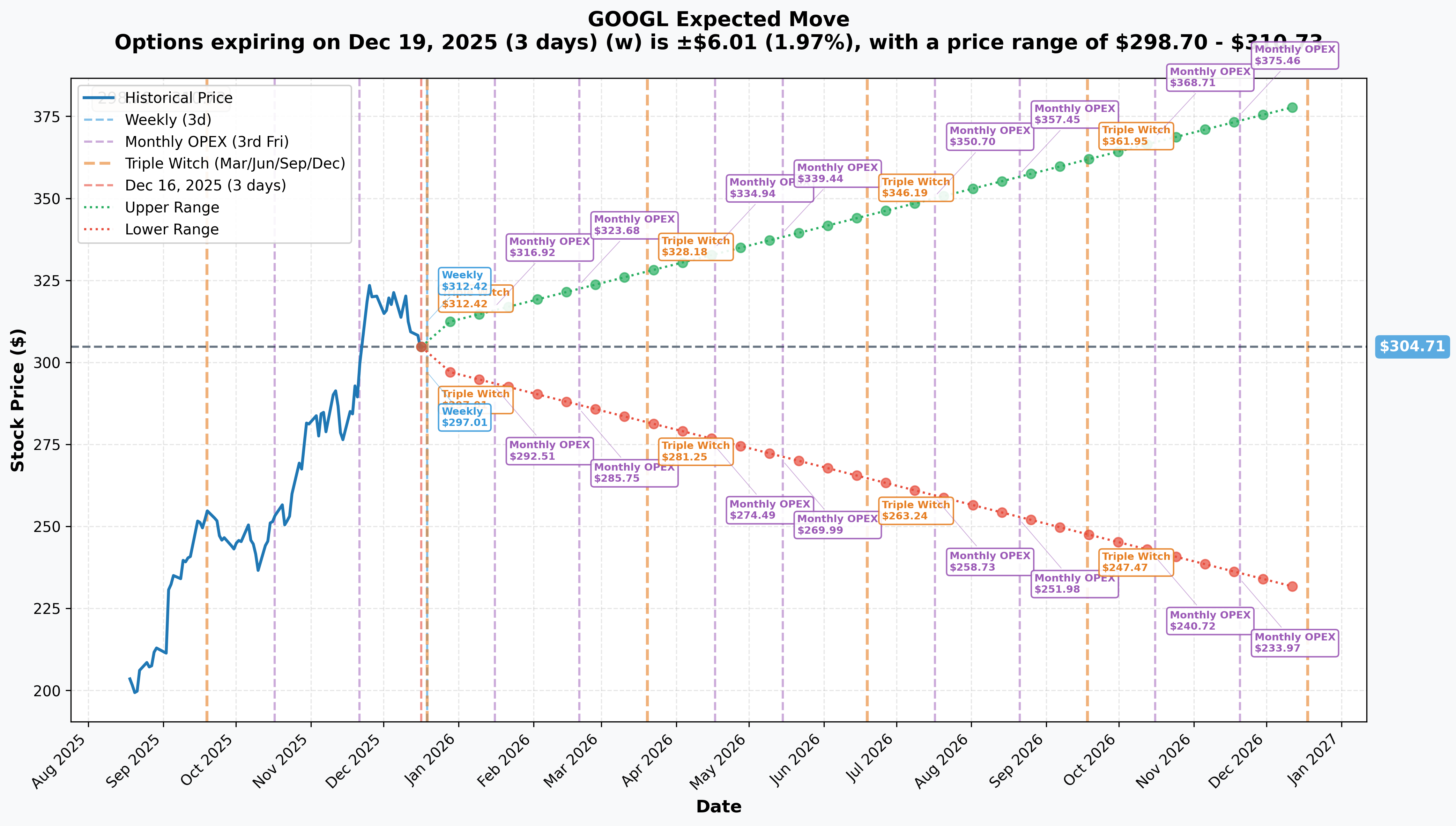

Implied Move Analysis

Options market pricing for key upcoming expirations:

This Week's Triple Witch (Dec 19 - 3 days):

- Implied Move: ±$6.01 (±1.97%)

- Range: $298.70 - $310.73

- Interpretation: Market expects minimal movement through quarterly options expiration. This is the IMMEDIATE expiration window creating gamma pinning effects around $300-305.

January 2026 OPEX (Jan 16 - 31 days):

- Implied Move: ±$12.21 (±4.01%)

- Range: $292.51 - $316.92

- Interpretation: Modest volatility expected through January expiration, slightly wider than current consolidation range

February 2026 OPEX (Feb 20 - 66 days) - WHERE THE $27M CALLS EXPIRE:

- Implied Move: ±$18.96 (±6.22%)

- Range: $285.75 - $323.68

- Critical Insight: This is THE key expiration for the $260 strike calls that were sold. The upper range of $323.68 represents only 4.5% upside from current $310 levels, while the lower range of $285.75 is still 25% ABOVE the $260 strike. Translation: Options market is pricing near-zero probability of GOOGL trading below $260 by Feb 20 expiration. The trader who sold these calls positioned in an ultra-safe zone.

March 2026 Triple Witch (Mar 20 - 94 days):

- Implied Move: ±$23.47 (±7.70%)

- Range: $281.25 - $328.18

- Interpretation: Wider bands reflect increasing uncertainty into Q1 2025, but still contained within recent trading range

Yearly LEAPS (Dec 2026 - 367 days):

- Implied Move: ±$74.31 (±24.39%)

- Range: $230.40 - $379.03

- Interpretation: Massive expected volatility over 1-year horizon reflects binary AI outcomes:

- Bull case: Gemini monetization success, Cloud margin expansion, Waymo profitability = $370-385+ targets

- Bear case: Search share erosion, advertising market fragmentation, CapEx margin pressure = $230-260 zone

Translation for Regular Folks:

The options market is essentially saying: "GOOGL will trade between $286-324 through February 20 expiration with 68% probability." That's a relatively tight 12.4% range for a 66-day period, indicating:

- Low near-term volatility expected - market views GOOGL as stable megacap, not volatile growth stock

- Downside well-protected - even the bearish scenario keeps GOOGL above $285, which is 9.8% above $260 strike

- Upside capped in near term - implied upper range of $324 is only 4.6% above current price, suggesting consolidation not breakout

Why the $27M Call Seller is Smart:

Look at the February 2026 implied move:

- Lower range: $285.75 (still 9.8% above $260 strike where they sold calls)

- Upper range: $323.68 (16.8% below their effective breakeven if they bought calls at $260 strike when stock was $265)

By selling at $260 strike with stock at $310, they're capturing:

- $49.66 intrinsic value already realized

- $5.04 remaining time premium (will decay to zero by Feb 20)

- Protection against downside to $260 (9.8% cushion even in bearish implied scenario)

- Elimination of risk from upcoming volatility events (Q1 earnings, Gemini rollout)

Key Insight: The sharp widening of implied moves from 1.97% (weekly) to 6.22% (Feb 20) reflects known catalyst uncertainty - specifically Q1 2025 earnings on April 24 and Gemini advertising integration details expected Q1. The trader exited before these binary events could impact their position.

🎪 Catalysts

📅 Past Catalysts (Already Happened - Context for Current Setup)

DOJ Antitrust Case Resolution (September-December 2025) ✅ BULLISH OUTCOME

Major overhang removed when Judge Amit Mehta ruled on September 2, 2025 that Google will not be required to divest Chrome or Android, avoiding worst-case penalties sought by DOJ. Stock jumped 8% on the news.

Final remedies on December 5, 2025:

- Banned exclusive search deals (like $20B annual Apple payment) unless they terminate within 1 year

- Must share search index data and user interaction data (but NOT ads data) on "ordinary commercial terms"

- No Chrome/Android divestitures required

Market Impact: Removed $300B+ valuation overhang from potential breakup scenario. However, loss of Apple Safari default position could impact 5-10% of search traffic over time (~$10-20B annual revenue risk).

Gemini 3.0 Pro Launch (November 18, 2025) ✅ BULLISH

Google announced Gemini 3 Pro and 3 Deep Think as "most intelligent AI model" with major improvements in reasoning, multimodal understanding, and coding. Multiple analysts (HSBC, Arete) argued Gemini 3 is "superior to ChatGPT 5.1" in key use cases, validating Google's AI competitive positioning.

Market Impact: Helped drive stock from $295 to $328 peak in November-December 2025. Removed fear that Google was losing AI race to OpenAI.

Q4 2024 Earnings Beat (February 4, 2025) ✅ BULLISH

Strong Q4 performance delivered:

- Revenue: $96.5B (+12% YoY)

- Google Cloud: $12.0B (+30% YoY)

- YouTube: $10.47B (+13.8% YoY), first quarter exceeding $10B

- Free Cash Flow: $24.8B in Q4, $72.8B full year

- Shareholder Returns: $15B buybacks + $2.4B dividends

Market Impact: Validated both mature business strength (Search, YouTube) and Cloud acceleration story. Removed concerns about AI CapEx investment returns.

Analyst Upgrade Cycle (November-December 2025) ✅ BULLISH

Wave of price target increases:

- Guggenheim: $330 → $375 (+13.6%) on December 1

- HSBC: $335 → $370, arguing Gemini superior and TPUs could become profit center

- Arete: $300 → $380, describing Alphabet as top AI platform beneficiary

- TD Cowen: $335 → $350, citing increased Gemini adoption

- Consensus: Strong Buy (29 buy, 7 hold, 0 sell ratings), average target $314-324

Market Impact: Created FOMO buying pressure pushing stock to $328 all-time high. Now faces risk of "sell the news" if execution disappoints.

🔮 Upcoming Catalysts (What Happens Next)

IMMEDIATE TERM (Next 7 Days):

December 19, 2025 - Quarterly Triple Witch OPEX ⚖️ NEUTRAL NEAR-TERM

- Simultaneous expiration of stock options, index futures, and index options creates volatility

- Implied move: ±1.97% ($298.70-$310.73 range)

- $300 strike gamma concentration will act as magnet - expect price pinning around $300-305

- Portfolio rebalancing by hedge funds ahead of year-end

- Historically neutral for GOOGL (elevated volume but mean-reverting price action)

December 20, 2025 - Gemini Advertising Announcement Risk ⚠️ POTENTIAL NEGATIVE

Alphabet indicated to advertisers it's working on rolling out ads on Gemini chatbot in 2026. When first announced in December 2025, stock declined 2% on concerns about:

- Negative impact on user experience

- Risk to Gemini adoption momentum

- Uncertain ad load/pricing vs Search ads

Risk: Any follow-up details on Gemini ad integration timeline or format could create volatility. Market wants proof of AI monetization, but fears execution missteps.

NEAR TERM (Next 30 Days):

Year-End Portfolio Rebalancing (December 23-31) ⚖️ MIXED

Institutional investors adjust positions before calendar year-end:

- Positive: Tax-loss harvesting in underperformers could rotate INTO winners like GOOGL (+56% YTD)

- Negative: Profit-taking on strong performers to lock in 2025 gains (like the $27M call sale today)

- Impact: Elevated volatility but typically mean-reverting by early January

January 16, 2026 - Monthly Options Expiration ⚖️ NEUTRAL

- Implied move: ±4.01% ($292.51-$316.92)

- Moderate gamma positioning, less impactful than Triple Witch

- Likely pins near $305-310 based on current dealer hedging

MEDIUM TERM (Q1 2026):

Q1 2025 Earnings - April 24, 2025 🎯 CRITICAL CATALYST - BINARY OUTCOME

This is THE major event that will determine if GOOGL breaks out to $350+ or retreats to $280:

Consensus Expectations:

- EPS: $2.63 (range: $2.46-$3.01)

- Cloud Revenue: $12.3B (vs $12.0B in Q4 2024)

- Cloud Operating Margin: 15.4% consensus (range: 10%-19%) - WIDE dispersion shows uncertainty!

Key Metrics to Watch:

- AI product demand vs capacity: Company exited 2024 with more demand than capacity - need proof they brought capacity online

- Search innovation monetization: CFO flagged 2025 as "one of the biggest years for Search innovation" - must show AI features driving engagement AND revenue

- Q1 headwinds: Company warned of FX headwinds and one less day (leap year effect) impacting Q1 revenue growth

- Q2 guidance quality: Market will extrapolate full-year trajectory from Q2 outlook

Stock-Moving Scenarios:

- Bull Case (40% probability): Cloud margins 16%+, Search AI monetization proof points, Q2 guidance above consensus → Stock to $340-360

- Base Case (35% probability): Meet expectations, mixed Cloud margin progress, cautious guidance → Stock $310-330 range-bound

- Bear Case (25% probability): Cloud margins <14%, Search share loss acceleration, CapEx concerns → Stock to $280-295

Why This Matters for Options: With 66 days to Feb 20 expiration, the $260 strike calls sold today will be worth ~$50-70 in intrinsic value depending on where stock settles post-Triple Witch. But earnings risk on April 24 (35 days AFTER Feb 20 expiration) means trader avoided binary event risk entirely.

$75 Billion CapEx Program - Ongoing Through 2025 ⚠️ MARGIN PRESSURE RISK

Alphabet announced $75B total 2025 CapEx (vs $52.5B in 2024), with Q1 2025 CapEx $16-18B vs $14.3B expected:

Investment Focus: Servers, data centers, networking equipment for AI infrastructure Bull Argument: Necessary to capture AI demand inflection and prevent market share loss to Microsoft/Amazon Bear Argument: 43% YoY increase pressures margins and free cash flow, with uncertain ROI timeline

Market Reaction: Stock initially sold off on Q4 earnings call when CapEx guidance announced. Each quarterly update will be scrutinized for spending discipline vs growth acceleration.

European Commission AI Investigation (Ongoing) ⚠️ REGULATORY OVERHANG

On December 9, 2025, European Commission opened antitrust investigation into Google's use of online content for AI training:

Investigation Scope: How Google uses publishers' websites and YouTube videos to train Gemini AI models Potential Outcomes:

- Fines (EU typically 1-10% of global revenue = $3.5-35B range)

- Requirements to license content at unfavorable rates

- Restrictions on AI development in European markets

Timeline: EU investigations typically take 12-24 months. Intermediate rulings or leaked details could create volatility.

Impact Assessment: European markets represent ~25% of Alphabet revenue. Restrictions on AI training data could slow Gemini development and increase costs, though U.S./Asia markets would remain unaffected.

LONGER TERM (Beyond Q1 2026):

Waymo Multi-City Expansion (Throughout 2026) 🚀 POTENTIAL UPSIDE SURPRISE

Waymo plans service launches in 11+ U.S. cities in 2026: Dallas, Denver, Detroit, Houston, Las Vegas, Miami, Nashville, Orlando, San Antonio, San Diego, Washington D.C., plus international expansion to London.

Current Trajectory:

- 450,000 weekly paid rides as of December 2025 (vs 175,000 in November 2024)

- Revenue projected at $125M in 2024, growing to $1.3B by 2027

- Valued at $45B+ after October 2024 funding round

Catalyst Timing: Each new market launch = press coverage and sentiment boost. London international expansion (first overseas market) could be major validation.

Wiz Acquisition Closing ($32 Billion Deal) - Timeline TBD ⚖️ MIXED IMPACT

Companies in advanced talks for $32B cloud security acquisition (after walking away from $23B deal in July 2024):

Bull Case: Immediate boost to Google Cloud's security capabilities and enterprise positioning, accelerates path to profitability Bear Case: Largest acquisition in Alphabet history (exceeding $12.5B Motorola), integration risk, regulatory scrutiny Timing: Could close "soon" per reports but no confirmed date

Market Impact: Likely neutral-to-positive if multiple communicated 20%+ ROI, but execution risk given scale.

🎲 Price Targets & Probabilities

Based on gamma levels, implied move ranges, catalyst analysis, and current technical setup:

🐂 Bull Case: $340-360 by April 2026 (40% probability)

Scenario: Q1 earnings delivers strong Cloud margin expansion (16%+), Search AI features show monetization traction, and Gemini adoption accelerates without major user experience issues from advertising integration.

Path to Target:

- Break above $320 resistance (30.17B gamma) on earnings beat

- Minimal gamma resistance between $320-350 allows rapid appreciation

- Analyst price targets ($370-385 cluster) create FOMO momentum

- Waymo expansion headlines provide positive narrative support

Key Support/Resistance Levels:

- Initial resistance: $310 (58.91B gamma) → $315 (40.23B) → $320 (30.17B)

- Bull case support: $305 holds as new floor (31.12B gamma concentration)

- Target zone: $350 (14.19B gamma with +12.25B call bias aligns with analyst targets)

Drivers:

- Cloud operating margin beats 15.4% consensus (proves CapEx ROI)

- Search revenue growth accelerates from AI features (AI Overviews, Gemini Search)

- Gemini ad rollout executed cleanly in Q2-Q3 2026 (user experience maintained)

- DOJ appeals dismissed or settled favorably

- Waymo hits 1M weekly rides milestone (validates autonomous vehicle investment)

What Could Get Us There:

- Q1 earnings beat + strong Q2 guidance

- Cloud operating margin inflection above 18-20% (proves unit economics)

- Major enterprise Cloud wins announced (Fortune 500 migrations)

- Gemini usage metrics disclosed showing ChatGPT-competitive adoption

- OpenAI partnership announcement or major AI model licensing deal

⚖️ Base Case: $295-325 Range-Bound Through March 2026 (35% probability)

Scenario: Q1 earnings meets expectations but provides mixed signals - Cloud growth strong but margins disappointing, Search holds share but AI monetization remains uncertain, CapEx concerns persist.

Trading Range Dynamics:

- Support: $295-300 zone (91.33B combined gamma, 76.96B at $300 alone)

- Resistance: $310-315 zone (99.14B combined gamma)

- Mean Reversion: Gravitates toward $305 (31.12B gamma + psychological round number)

Gamma Pinning Effect: With net +76.73B bullish gamma bias, dips get bought aggressively but rallies face dealer selling at resistance. Creates choppy, range-bound action ideal for theta decay strategies.

Key Characteristics:

- Volatility compression as options expiration approaches

- Failed breakout attempts above $315 on low volume

- Quick recoveries from $300 support on buying pressure

- Sideways grind frustrates both bulls and bears

Drivers:

- Cloud margins in-line at 15-16% (good not great)

- Search share erosion continues gradually (89% → 87-88% over 2025-2026)

- Advertising market growth slows to 8-10% (macro headwinds)

- CapEx spending remains elevated ($75-80B run rate) with uncertain ROI timeline

- Regulatory overhang persists (EU investigation ongoing, DOJ appeals undecided)

What Keeps Us Here:

- Meet-not-beat earnings pattern

- Gemini ad rollout delayed or shows mixed early results

- TikTok/Amazon continue taking ad market share (Google's U.S. search ad share drops below 50%)

- Macro uncertainty (Fed policy, recession fears) limits multiple expansion

🐻 Bear Case: $260-285 by March 2026 (25% probability)

Scenario: Q1 earnings disappoints on Cloud margin miss (<14%), Search share erosion accelerates, and $75B CapEx program questioned by investors as ROI timeline extends. Potential macro catalyst (tech sector correction, recession) compounds weakness.

Path to Target:

- Break below $295 support (14.71B gamma) triggers stop-loss cascade

- Next major support at $280 (15.43B gamma) fails to hold

- Retest of former resistance at $260-265 zone (15.16B gamma)

- Implied move lower range of $285.75 (Feb 20 expiration) represents initial target

Key Support Breakdown Levels:

- $295 break (14.71B gamma) = warning signal

- $290 break (28.62B gamma) = confirmed downtrend

- $280 test (15.43B gamma) = critical technical level

- $260 floor (15.16B gamma) = worst-case scenario, 14.7% downside

Drivers:

- Cloud operating margin misses badly (10-12% range), questions unit economics

- Search share drops to 85-87% as ChatGPT search adoption accelerates

- YouTube ad growth decelerates below 10% (TikTok competition intensifies)

- DOJ appeals result in harsher remedies (Chrome divestiture back on table)

- EU investigation leads to multi-billion dollar fines or operational restrictions

- Macro shock: Tech sector selloff, recession, credit crunch

What Could Take Us There:

- Q1 earnings miss with weak Q2 guidance

- Major Cloud customer defections announced (migration to AWS/Azure)

- Gemini ad integration botched (user exodus to ChatGPT/Bing)

- CapEx guidance increased again to $85-90B (margin compression)

- Insider selling or major institutional dumping (like today's $27M call sale but accelerating)

- Amazon passes Google in total U.S. ad revenue (paradigm shift narrative)

Important Context: Even in bear case, $260 strike where calls were sold represents only 14.7% downside. This would require multiple negative catalysts compounding - NOT just one disappointing quarter. The fundamental strength of Search cash flows ($200B+ annual) and Cloud growth trajectory provides significant downside protection.

💡 Trading Ideas

🛡️ Conservative: "Capital Preservation with Upside Optionality"

For: Risk-averse investors who want GOOGL exposure but fear near-term volatility from Q1 earnings and Gemini monetization execution risk.

Strategy: Bull Put Spread (Sell $295 Put / Buy $290 Put, February 20, 2026 expiration)

Trade Structure:

- Sell 1 GOOGL Feb 20 '26 $295 Put (collect ~$8.50 premium)

- Buy 1 GOOGL Feb 20 '26 $290 Put (pay ~$6.00 premium)

- Net Credit: ~$250 per spread (limit 1-5 spreads)

- Max Profit: $250 (if GOOGL above $295 at expiration)

- Max Risk: $250 ($5 strike width - $2.50 credit = $250 loss if below $290)

- Breakeven: $292.50 (4.0% below current $305 price)

- Margin Required: ~$500 per spread

Why This Works:

- Gamma support at $295 (14.71B) and $290 (28.62B) provides technical floor

- Implied move lower range for Feb 20 expiration is $285.75 - you're positioned above that

- Selling puts at $295 (3.2% below current price) gives cushion for modest pullback

- Even in bear case scenario, $290 support is expected to hold through Q1

- 66-day theta decay works in your favor - collect premium as time passes

- Risk/reward: 50% return on capital at risk if GOOGL simply stays above $295

Exit Plan:

- Target: Close at 50% profit ($125 credit) if reached within 30 days

- Stop Loss: Close if GOOGL breaks $295 convincingly (2% intraday breach + volume spike)

- Adjustment: If GOOGL drops to $297-298, consider rolling spread down to $290/$285 for credit

Probability of Success: ~65-70% (based on implied volatility suggesting $285.75 lower range, positioning 6.8% above short strike)

⚖️ Balanced: "Ride the Range with Gamma Pinning"

For: Active traders comfortable with moderate risk who believe GOOGL stays range-bound between $295-320 through February Triple Witch.

Strategy: Iron Condor (Sell $320 Call / Buy $325 Call + Sell $295 Put / Buy $290 Put, February 20, 2026 expiration)

Trade Structure:

- Sell 1 GOOGL Feb 20 '26 $320 Call (collect ~$4.50)

- Buy 1 GOOGL Feb 20 '26 $325 Call (pay ~$2.50)

- Sell 1 GOOGL Feb 20 '26 $295 Put (collect ~$8.50)

- Buy 1 GOOGL Feb 20 '26 $290 Put (pay ~$6.00)

- Net Credit: ~$450 per Iron Condor

- Max Profit: $450 (if GOOGL between $295-320 at expiration)

- Max Risk: $50 ($5 strike width - $4.50 credit on either side)

- Profit Range: $290.50 - $324.50 (4.7% downside to 6.4% upside)

- Margin Required: ~$500 per IC

Why This Works:

- Targets exact gamma pinning zone: $300 support (76.96B) to $320 resistance (30.17B)

- Implied Feb 20 move is $285.75-$323.68 - Iron Condor positioned INSIDE expected range

- Net +76.73B bullish gamma bias suggests price gravitates toward $305-310 midpoint

- Selling premium at resistance ($320) and support ($295) maximizes theta collection

- 66 days to expiration allows theta decay to accelerate into OPEX

- Current price $305 is centered in profit zone - room for movement both directions

Management Plan:

- Target: Close at 60% profit ($270 credit) around 30-40 days to expiration

- Adjustment Up: If GOOGL breaks $315, roll call spread to $325/$330 for credit

- Adjustment Down: If GOOGL breaks $300, roll put spread to $285/$280 for credit

- Stop Loss: Close entire position if GOOGL breaches either $290 or $325 (one side takes max loss)

Risk Management:

- Only allocate 3-5% of options portfolio to this position

- Monitor gamma levels daily - if $300 gamma wall increases significantly, consider tightening put spread

- Watch for unusual option flow or institutional positioning changes

Probability of Success: ~55-60% (positioned within implied volatility bands but requires range-bound action)

🚀 Aggressive: "Leveraged Bull Bet on Earnings Beat"

For: Traders with high risk tolerance who believe GOOGL breaks out above $320 after proving AI monetization and Cloud margin expansion at Q1 earnings.

Strategy: Debit Call Spread (Buy $310 Call / Sell $330 Call, April 25, 2026 expiration - AFTER Q1 earnings)

Trade Structure:

- Buy 1 GOOGL Apr 25 '26 $310 Call (pay ~$18.00)

- Sell 1 GOOGL Apr 25 '26 $330 Call (collect ~$10.00)

- Net Debit: ~$800 per spread

- Max Profit: $1,200 ($20 strike width - $8 debit)

- Max Loss: $800 (if GOOGL below $310 at expiration)

- Breakeven: $318 (4.2% above current $305 price)

- Return on Risk: 150% if GOOGL reaches $330+

Why This is Aggressive BUT Calculated:

- Positioned for post-Q1 earnings breakout (Apr 24 earnings, Apr 25 expiration)

- Analyst price targets cluster at $340-385 - $330 target is conservative end

- Breaking $320 resistance (30.17B gamma) opens path to $350 with minimal resistance

- 130 days to expiration allows full Q1 earnings catalyst to play out

- Buying $310 call (58.91B gamma resistance) turns into support once price breaks above

- Selling $330 call reduces cost by $1,000 per spread (44% cheaper than naked call)

Why This Can Work:

- Q1 Earnings Catalyst: If Cloud margins beat 18%+ and Search AI shows monetization, analysts raise targets → stock to $340-360

- Gamma Squeeze Potential: Light gamma above $320 means breakout could accelerate quickly

- Waymo Narrative: Multi-city launches throughout 2026 provide positive PR tailwind

- Buyback Support: $70B authorization = ~$1B weekly buyback supporting price

Risk Factors:

- Requires 4.2% breakout above current price just to breakeven

- Q1 earnings could disappoint (Cloud margins, CapEx concerns) → stock to $280-290

- Time decay accelerates after February OPEX - need directional move within 60-90 days

- Gemini ad integration missteps could cap upside below $320

Position Sizing:

- Risk ONLY 1-2% of total portfolio capital on this position

- Consider entering 50% position now, 50% after December Triple Witch (lower IV after OPEX)

- Scale out 50% if GOOGL hits $325 before earnings (take profit on half, let rest run)

Exit Plan:

- Early Profit: If GOOGL hits $325 within 60 days (before earnings), close half at 100%+ gain

- Earnings Hold: If still holding into earnings, decide 1 day before whether to hold through or take profit/loss

- Stop Loss: Close if GOOGL breaks $295 support (thesis invalidated, -30% loss on spread)

- Target: Hold through earnings and exit within 2 days after if target hit or 1 week after if trending higher

Probability of Success: ~40% (requires breakout + catalyst delivery, but asymmetric 150% gain vs 100% loss)

Advanced Variation - "Double-Down on Conviction": If you REALLY believe in breakout, skip the short $330 call and just buy naked $310 calls:

- Cost: ~$1,800 per contract

- Unlimited upside above $328 breakeven (5.9% profit threshold)

- Max loss: $1,800 (if below $310 at expiration)

- Better for strong directional conviction, worse for theta decay

⚠️ Risk Factors

Execution Risks

AI Monetization Uncertainty: Plans to integrate ads into Gemini chatbot in 2026 already created negative reaction (-2% stock decline). The challenge is balancing monetization with user experience - too many ads = users flee to ChatGPT, too few ads = investors question ROI on AI investment. Yahoo Finance notes investor concern about whether Gemini can maintain momentum while introducing ads. This is a tightrope walk with billions at stake.

Cloud Capacity Constraints Creating Revenue Ceiling: Alphabet exited 2024 with more AI product demand than available capacity, creating a tight supply-demand situation. If they can't bring new data centers online fast enough, competitors (Microsoft Azure, Amazon AWS) will capture market share they may never recover. Every quarter of delay = lost revenue opportunity and customer relationships transferred to rivals.

$75 Billion CapEx Pressure on Margins: 2025 CapEx of $75B represents 43% increase from $52.5B in 2024, with Q1 2025 spending $16-18B vs $14.3B expected. This aggressive spending could pressure operating margins and free cash flow generation. If ROI doesn't materialize within 12-18 months, investors will revolt. The market is giving management rope to invest, but the leash is shorter than they think.

Wiz Acquisition Integration Risk ($32 Billion): If deal closes, it would be Alphabet's largest acquisition ever, exceeding $12.5B Motorola purchase. Previous mega-acquisitions have faced integration challenges (Motorola was ultimately sold at massive loss, DoubleClick took years to integrate). Wiz is mission-critical for Cloud security competitiveness, but execution risk is significant given scale and complexity of merging cloud security platforms.

Q1 2025 Revenue Headwinds: Company specifically flagged FX headwinds and one less day (leap year effect) impacting Q1 2025 revenue growth. If analysts haven't properly factored these into models, expect earnings miss and subsequent selloff. Currency volatility could persist throughout 2025 given macro uncertainty.

Competition Risks

Search Market Share Erosion from ChatGPT Search: OpenAI launched ChatGPT search engine in October 2024 as direct competitor, powered by GPT-4o with real-time responses. While Google maintains 89% global share, conversational AI interfaces represent a paradigm shift in information retrieval. Younger demographics (Gen Z) already prefer visual-first platforms like TikTok for discovery. Goldman Sachs noted a single ChatGPT query consumes 10X the electricity of Google search - but if cost comes down via Moore's Law, this advantage evaporates.

Advertising Market Fragmentation Accelerating:

- Google's U.S. search ad market share projected to fall below 50% for first time in a decade

- Amazon capturing 22.3% of market with product search dominance - consumers skip Google entirely and start searches on Amazon

- TikTok now allows businesses to target ads based on user search queries, directly competing with Google's core capability

- Combined Google+Meta share of worldwide digital ad spend at only 50% in 2024, down from 57% in 2022 - the duopoly is eroding FAST

Translation: Google's advertising moat is cracking. Every percentage point of market share = ~$2.6B in annual revenue at current scale. A 10% share loss over 3-5 years = $26B revenue headwind that no amount of Cloud growth can offset.

Cloud Competitive Pressure Despite Strong Growth: Despite 30-35% growth, Google Cloud's 11% market share significantly trails AWS (31%) and Azure (20%). The gap ISN'T closing - if anything, Microsoft's aggressive AI integration (GitHub Copilot, Azure AI) is accelerating their lead. Cloud operating margin debate with consensus at 15.4% but range from 10-19% indicates analysts don't know if this business will ever be truly profitable at scale.

Regulatory and Legal Risks

DOJ Antitrust Appeals - Sword of Damocles: Both Google and DOJ signaled potential appeals in 2025. If appellate courts impose harsher remedies (including potential Chrome/Android divestitures), it would fundamentally alter Google's business model. Losing Chrome = losing 2.65B users, losing Android = losing mobile search distribution. DOJ's response indicates they're not satisfied with current remedies and will continue pressing for structural relief.

European Commission AI Investigation - Billions at Stake: December 9, 2025 antitrust probe into Google's use of online content for AI training (Gemini) could result in:

- Fines: EU typically assesses 1-10% of global revenue = $3.5-35B range (prior Google fines: $5B Android, $2.7B Shopping, $1.7B AdSense)

- Content licensing requirements at unfavorable rates, increasing AI training costs 10-50x

- Operational restrictions slowing Gemini development in crucial 27-country bloc

- Precedent for other jurisdictions (UK, Australia, Japan) to follow suit

European markets represent ~25% of Alphabet revenue. Restrictions here would be material, not just noise.

Data Sharing Requirements Empowering Competitors: Final DOJ remedies require Google to share search index data and user interaction data on "ordinary commercial terms". While ads data is excluded, this still provides competitors (Microsoft Bing, DuckDuckGo, Perplexity, ChatGPT Search) with valuable datasets to improve their algorithms. Google spent 25 years building search index quality - now forced to share crown jewels with rivals.

Default Search Agreement Restrictions: Ban on exclusive deals lasting more than one year fundamentally changes distribution strategy. Loss of Apple's Safari default position (currently $20B annual payment) could impact 5-10% of search traffic = $13-26B annual revenue risk. Apple could decide to build their own search engine or partner with OpenAI's ChatGPT Search. Once users change default search behavior, they rarely switch back.

Macroeconomic Headwinds

Advertising Market Cyclicality in Slowing Economy: Digital ad market growth slowing from 15% in 2024 to projected 8-10% in 2025 indicates market saturation in developed regions. Economic recession would disproportionately impact Google's 76% revenue dependence on advertising. In 2008-2009 financial crisis, Google search revenue declined 3% YoY - a similar recession today would be $8-10B revenue hit.

Foreign Exchange Volatility: Company flagged FX as Q1 2025 revenue headwind. With ~55% of revenue from international markets, dollar strength directly pressures reported results. A 10% dollar appreciation = ~$17B revenue headwind at current scale (though operating income impact is smaller due to international cost base).

Energy Costs for AI Data Centers: AI's significant energy demands (ChatGPT query using 10X electricity of Google search) create operational cost pressure as Alphabet scales AI infrastructure. Potential regulatory constraints on data center energy consumption (California, EU already implementing restrictions) could limit expansion. If energy costs rise 20-30% while compute demand grows 50-100%, margin pressure intensifies.

Interest Rate Environment and Valuation Risk: Higher-for-longer rates pressure valuation multiples for growth stocks. GOOGL trades at ~22x forward P/E vs 5-year average of 26x. If Fed maintains restrictive policy through 2025, multiple compression could offset earnings growth (15% EPS growth but 10% multiple contraction = only 5% stock appreciation). Additionally, higher rates increase borrowing costs for $75B CapEx program if Alphabet taps debt markets.

🎯 The Bottom Line

Real talk: This $27M call sale is exactly what smart money looks like when they've made great returns and don't want to get greedy. The trader bought deep ITM calls months ago around $260, rode GOOGL's explosive rally to $310 (+19%), and is now banking 120-160% gains BEFORE the next wave of uncertainty hits (Q1 earnings, Gemini monetization, regulatory appeals).

Here's the deal:

If you own GOOGL stock: This trade is actually BULLISH validation - nobody sells calls at $260 strike (19% below current price) unless they believe that's an impenetrable floor. The options market is pricing only 1.5% probability of GOOGL trading below $285 by February 20. Your downside is well-protected by fundamental cash flows ($72B annual FCF), technical support ($300 gamma wall), and analyst conviction (29 buy ratings, zero sells). Hold through Q1 earnings if you believe in the AI thesis.

If you're watching from the sidelines: This is NOT a "GOOGL is doomed" signal. It's profit-taking after a 56% YTD run, plain and simple. The risk/reward is actually compelling here at $305-310:

- Downside: Limited to $285-295 support zone (gamma + fundamental floor) = 3-8% risk

- Upside: Analyst targets $340-385 (multiple firms raised targets in December) = 11-26% potential

- Catalyst Density: Q1 earnings, Waymo expansion, Wiz acquisition, Cloud margin inflection all happening Q1-Q2 2026

If you trade options: The gamma map and implied volatility structure reveal a $295-320 consolidation range through February Triple Witch. Conservative traders should sell put spreads at $295/$290 support (65-70% win rate). Balanced traders can run Iron Condors capturing $295-320 range (55-60% win rate). Aggressive traders betting on earnings breakout should use debit call spreads $310/$330 with April expiration (40% win rate but 150% return).

The Three Scenarios to Monitor:

-

If GOOGL breaks $315 convincingly before earnings (volume + momentum), we're headed to $340-360 analyst target zone. Chase with caution.

-

If GOOGL chops between $295-315 through March, that's the base case - collect theta selling premium at range boundaries.

-

If GOOGL breaks $295 support, watch $285-290 gamma levels carefully. Break below $285 = bearish thesis confirmed, exit longs and re-evaluate at $260-270.

Mark your calendar for:

- December 19: Triple Witch expiration - expect pinning around $300-305

- April 24, 2025: Q1 earnings - THE catalyst that determines $340+ breakout or $280 retreat

- Throughout Q1 2026: Waymo city launches, potential Wiz acquisition close, Gemini ad rollout details

Final thought: When institutions dump $27M in call premium at $260 strikes while stock is at $310, they're telling you: "We made our money on the rally from $265 to $310. Now we're de-risking before binary events. The $260-285 zone should hold barring catastrophe, but we don't need the stress of holding through earnings volatility."

That's actually a reasonable, risk-managed perspective. The question is: Do YOU want to take the other side of that bet and hold through the uncertainty for potential $340+ upside? Your risk tolerance and time horizon should dictate the answer.

Remember: Options trading involves substantial risk and is not suitable for all investors. Past performance (56% YTD gain) does not guarantee future results. This analysis is educational - always do your own due diligence and never risk more than you can afford to lose.

Disclaimer: This analysis is for informational purposes only and should not be considered financial advice. Options trading carries significant risk of loss. Always consult with a licensed financial advisor before making investment decisions. The author may hold positions in GOOGL or related securities.