🚨 GOOGL Major Bearish Bets Signal Profit-Taking Ahead!

📅 December 22, 2025 | 🔥 $41M in Unusual Activity Detected

🎯 The Quick Take

Someone just dumped $41 million worth of GOOGL calls expiring January 2026 - this isn't retail traders taking profits. Two massive bearish sweeps targeting the $165 and $220 strikes signal institutional players are either closing winning positions or hedging against downside after GOOGL's incredible 74% run to $309. With ChatGPT capturing 17% of search queries and Q4 earnings not until February 3, 2026, smart money might be locking in gains before year-end.

💰 The Option Flow Breakdown

📊 What Just Happened

| Time | Type | Strike | Expiry | Premium | Volume | Spot | Chart |

|---|---|---|---|---|---|---|---|

| 10:28 AM | 🔴 SELL CALL | $165 | 2026-01-16 | $29.0M | 2,000 | $307.53 | View Chart |

| 10:31 AM | 🔴 SELL CALL | $220 | 2026-01-16 | $12.0M | 1,300 | $307.53 | View Chart |

Total Premium: $41,000,000

🤓 What This Actually Means

Real talk - this is profit-taking season at its finest! Here's what's going down:

🔴 $165 Strike Short Calls ($29M): This strike is deep in-the-money with GOOGL at $309, meaning someone paid massive premium to exit these calls. These were likely purchased months ago when GOOGL was in the $165-$180 range and are now worth serious money. Selling 2,000 contracts worth $14,500 each suggests a large fund or wealthy trader cashing out before year-end for tax reasons.

🔴 $220 Strike Short Calls ($12M): Same story here - these $220 calls are trading at $88 each ($88 x 100 shares x 1,300 contracts = $11.4M). Someone's closing positions that were likely opened when GOOGL was trading in the $220-$240 range earlier this year. The timing right before the holidays screams tax harvesting.

Translation for us regular folks: When you see $41M in call SELLING after a 74% yearly run, institutions aren't betting on a crash - they're booking wins. This is particularly notable because:

- January 2026 is 25 days away (plenty of time value remaining)

- Both strikes are profitable (stock at $309 vs $165 and $220 strikes)

- Volume of 3,300 contracts represents serious size for GOOGL options

This doesn't mean the stock's tanking - it means smart money is taking chips off the table after an incredible run.

📈 Technical Setup / Chart Check-Up

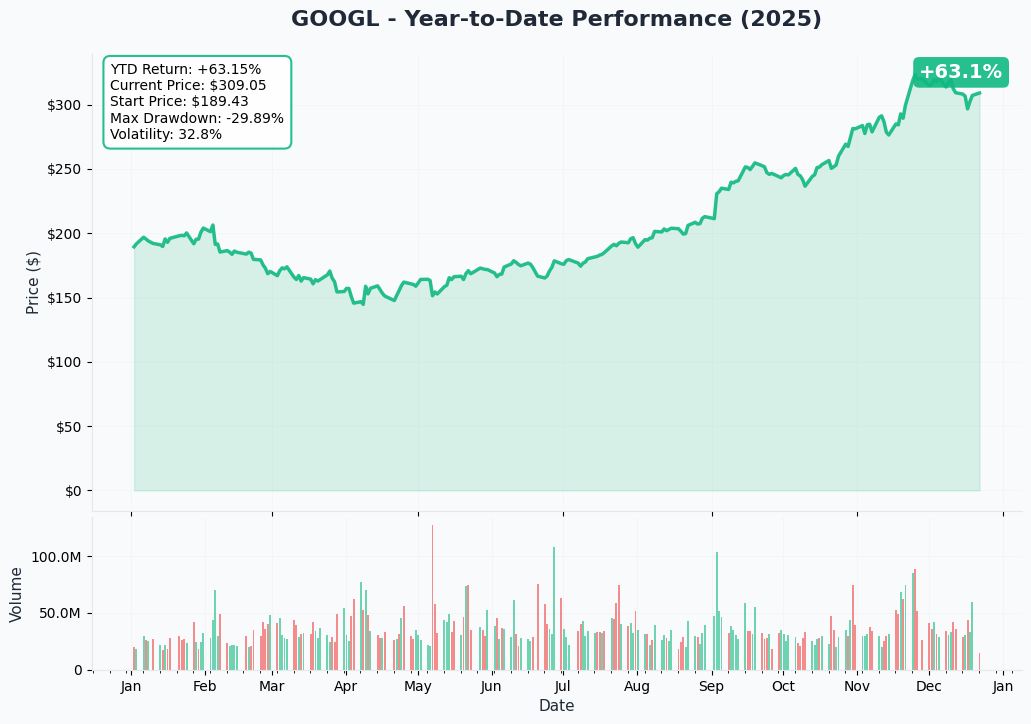

YTD Chart Performance

GOOGL has delivered an absolute monster year with a 74% gain, climbing from around $194 on December 23, 2024 to current levels near $309. The stock hit an all-time high of $323.23 on November 25, 2025 according to MacroTrends data, making Alphabet the 3rd largest company globally with a $3.74 trillion market cap.

The chart shows a clear uptrend throughout 2025 with several consolidation periods:

- Q1 2025: Strong breakout above $200 resistance

- Q2 2025: Consolidation in the $240-$260 range

- Q3 2025: Explosive move to $300+ on strong earnings

- November Peak: Topped at $323 before modest pullback

- Current: Trading at $309, just 4.3% below all-time highs

The stock has been consolidating in the $305-$315 range over the past month, digesting the massive gains while holding above the psychologically important $300 level.

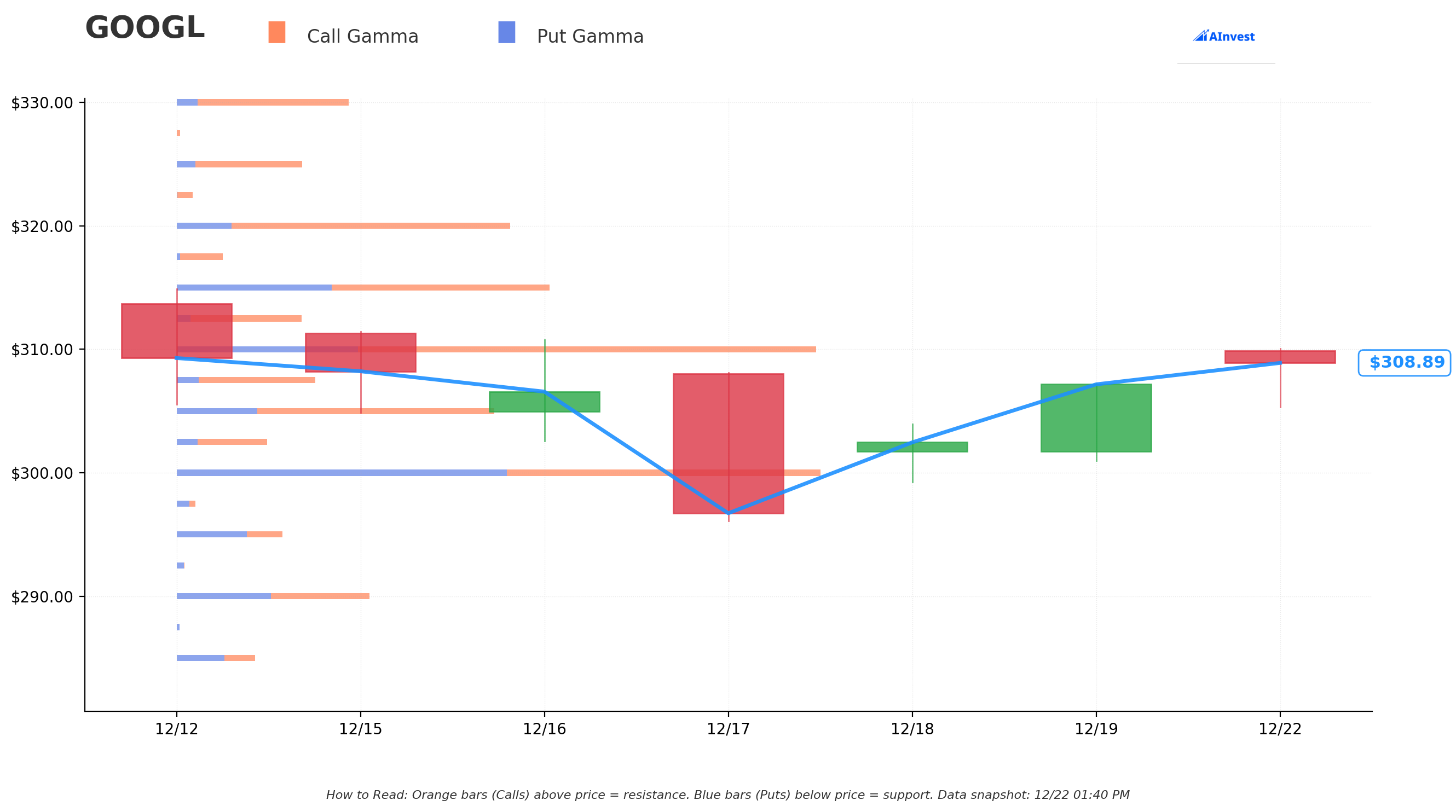

Gamma-Based Support & Resistance Analysis

Key Gamma Levels:

The gamma exposure map shows GOOGL in a tight squeeze zone with significant positioning on both sides:

Resistance Levels (Call Gamma - 🟠):

- $310 (Immediate Ceiling): Strongest resistance with $38.6M in call gamma and $53.9M total GEX - this is just 0.34% above current price and acting as the near-term cap

- $315 (Secondary Resistance): $18.5M call gamma sits 1.96% higher - breaking above $310 opens path to $315

- $320 (Major Resistance): $23.6M call gamma at 3.57% upside - this was tested during the November rally

- $330 (Extended Resistance): $12.8M call gamma at 6.81% upside - aligns with the psychological round number

- $350 (Moonshot Level): $15.9M call gamma at 13.3% upside - would represent new all-time highs

Support Levels (Put Gamma - 🔵):

- $307.50 (Immediate Floor): Closest support at just 0.47% below with $11.6M total GEX - should hold on minor pullbacks

- $305 (Key Support): $26.6M total GEX at 1.28% downside - important psychological level

- $300 (Major Support): The big kahuna with $53.9M total GEX at 2.90% downside - this is the line in the sand

- $290 (Secondary Support): $16.0M total GEX at 6.14% downside - would signal bearish shift

- $280 (Deep Support): $12.2M total GEX at 9.37% downside - extreme bearish scenario

Net GEX Bias: Bullish (+$148.4M favoring calls over puts)

The gamma profile shows GOOGL trapped in a $307.50-$310 compression zone. The massive gamma wall at $310 combined with strong put support at $300 suggests the stock will likely trade in a narrow $300-$315 range through year-end unless a major catalyst breaks the pin.

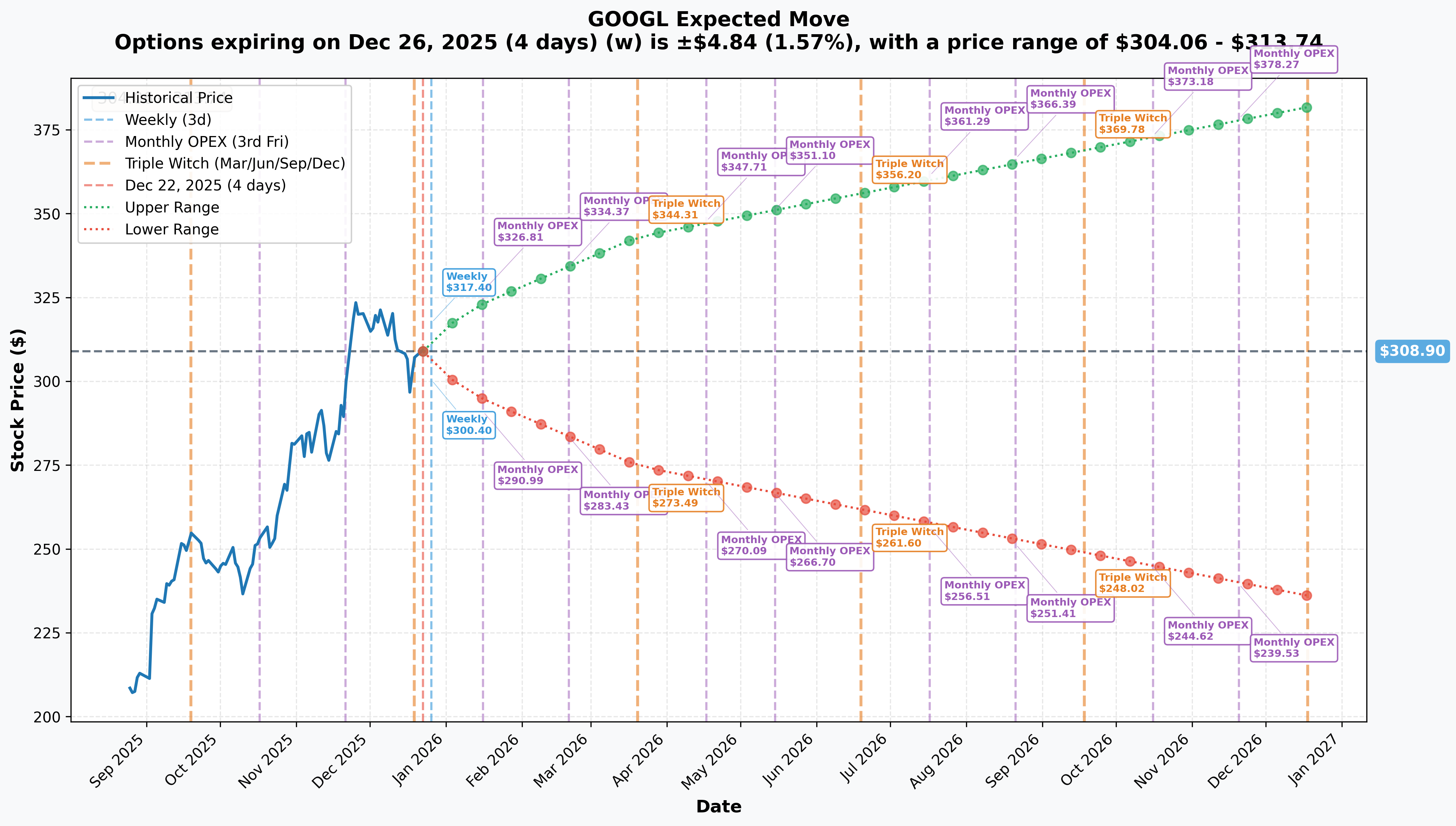

Implied Move Analysis

Market Expectations by Timeframe:

Weekly (Dec 26, 2025 Expiry):

- Implied Move: ±1.57% (±$4.84)

- Expected Range: $304.06 - $313.74

- Interpretation: Options market pricing in a quiet holiday week with most movement contained within the gamma boundaries

Monthly OPEX (Jan 16, 2026):

- Implied Move: ±4.68% (±$14.45)

- Expected Range: $294.45 - $323.35

- Interpretation: This is where the big money flow happened today! The $165 and $220 strike sales target this expiration. Market expects $309 ± $14.45 movement, which perfectly brackets our $300 support and $320 resistance levels.

Quarterly Triple Witch (Mar 20, 2026):

- Implied Move: ±11.1% (±$34.28)

- Expected Range: $274.62 - $343.18

- Interpretation: Captures Q4 2025 earnings (Feb 3) and potential follow-through. The 11% move expectation reflects significant event risk with earnings and potential catalyst news from Google I/O preparation.

Yearly LEAPS (Dec 18, 2026):

- Implied Move: ±23.6% (±$72.91)

- Expected Range: $235.99 - $381.81

- Interpretation: A full year of potential with 23.6% implied volatility suggests range from $236 (major bear case) to $382 (new all-time highs). This reflects uncertainty around AI monetization, search market share trends, and competitive positioning.

The implied move analysis confirms that options traders are pricing in relatively low near-term volatility (1.57% weekly) but significant movement potential around earnings (4.68% monthly, 11.1% quarterly).

🎪 Catalysts

Upcoming Catalysts

Near-Term (Next 30 Days):

- Year-End Positioning (Dec 31, 2025): Tax loss harvesting and fund rebalancing could create volatility

- CES 2026 (Jan 7-10, 2026): Potential AI and hardware announcements from Google's ecosystem partners

Major Events (Q1 2026):

- Q4 2025 Earnings (February 3, 2026) - HIGH IMPACT ⚡

- Confirmed after-market close

- Consensus EPS estimate: $2.63

- Key metrics to watch:

- Google Cloud revenue trajectory (was $12.26B in Q1 2025, +28% YoY)

- Gemini 3 adoption and monetization metrics

- AI infrastructure capex guidance for 2026 (expected "significant increase" from $91-93B in 2025)

- Search market share trends vs. ChatGPT competition

- YouTube advertising momentum post-election cycle

- Previous quarter (Q3 2025): Beat expectations with $102.3B revenue (+16% YoY) and EPS of $3.10 vs. consensus $2.26

Strategic Developments:

- Intersect Acquisition Closing (H1 2026) - Google acquiring data center firm for $4.75B to accelerate AI infrastructure buildout

- Waymo Expansion - Currently providing 450,000 paid rides weekly, targeting 1M rides/week by end 2026 with expansion to 12+ new cities including Denver, Nashville, and San Diego

- Google I/O 2026 (Expected May 2026) - Major developer conference likely to feature Gemini 4 announcements, Android updates, and new Cloud services

Past Catalysts (Already Happened)

Recent Wins:

-

Gemini 3 Launch (December 2025) ✅

- Gemini 3 Flash now processing 1 trillion tokens daily, 3x faster than Gemini 2.5 Pro

- 650 million monthly active Gemini app users

- Tops WebDev Arena leaderboard with 1487 Elo score

-

Favorable Antitrust Ruling (September 2025) ✅

- Judge ruled Google would NOT be required to divest Chrome or Android

- Can continue $20B annual payments to Apple for default search

- Must share search index with competitors but avoided worst-case breakup scenario

-

Q3 2025 Earnings Beat (October 2025) ✅

- Revenue: $102.3B (+16% YoY), exceeding expectations

- Adjusted EPS: $3.10 vs. consensus $2.26 (massive beat)

- Cloud backlog grew 46% QoQ to $155 billion

- Operating margin improved 4.5 percentage points

-

Pixel 9 Success ✅

- 105% year-over-year sales growth in H1 2025, making Google fastest-growing premium smartphone brand

Headwinds:

-

Search Market Share Pressure ⚠️

- ChatGPT now commands 17% of queries globally, Google's greatest threat in 20+ years

- U.S. market share down to 85.28% from 88% in September 2024

- Desktop share at 79.1%, lowest in over two decades

-

Advertising Slowdown ⚠️

- Publisher RPM/CPM drops of 30-50% reported in November-December 2025

- Network advertising revenues declined 1% YoY in Q2 2025

- Ad revenue growth deceleration from 15% in 2024 to projected 8-10% in 2025

🎲 Price Targets & Probabilities

Based on the gamma levels, implied move data, and catalyst timeline, here's the realistic outlook:

🚀 Bull Case (30% Probability): $320-$330 by February Earnings

Path to Victory:

- Q4 earnings on Feb 3 beat expectations with Cloud revenue >$13B (+30%+ YoY)

- Gemini 3 monetization metrics show strong adoption in enterprise

- Search market share stabilizes or shows first month of recovery

- Waymo announces major partnership or funding round at >$100B valuation

Technical Setup:

- Break above $310 gamma resistance opens path to $315

- $320 was tested in November rally - revisit likely on positive earnings

- $330 represents +6.8% upside and psychological round number

- Implied move of +4.68% for Jan OPEX supports move to $323

Risks to Bull Case:

- Must overcome $310 resistance (largest gamma wall)

- Year-end profit-taking could cap upside through December

- Search competition narrative may limit multiple expansion

⚖️ Base Case (50% Probability): $300-$315 Range-Bound

Most Likely Scenario:

- Stock trades in tight range through year-end as institutions rebalance

- $300 support holds on any weakness (massive put gamma floor)

- $310-$315 resistance caps rallies without major catalyst

- Earnings meet but don't significantly beat expectations

- Market digests 74% YTD gain before next leg up

Technical Setup:

- Current consolidation pattern from $305-$315 continues

- Weekly implied move of ±1.57% keeps stock in $304-$314 range

- Gamma profile shows equal support/resistance creating equilibrium

- Net bullish gamma bias prevents sustained breakdown below $300

Trading Strategy:

- Range traders can sell $300 puts / $315 calls for premium

- Accumulation zone on dips toward $305 support

- Wait for earnings catalyst before aggressive directional bets

😰 Bear Case (20% Probability): $285-$295 Pullback

What Could Go Wrong:

- Q4 earnings disappoint with Cloud growth <25% (decelerating from 28%)

- Search market share data shows continued erosion to ChatGPT

- Advertising slowdown worse than expected with publisher CPM crashes continuing

- Regulatory headwinds escalate with new antitrust actions

- Broader tech sector correction pulls mega-cap stocks down

Technical Setup:

- Break below $300 support opens gap down to $290 (-6% from current)

- $285-$295 zone aligns with Q3 2025 consolidation area

- Would represent healthy correction after 74% run

- Quarterly implied move of ±11.1% allows for $275-$343 range

Support Levels:

- $300 is line in the sand (must hold to maintain bullish structure)

- $290 secondary support with $16M total GEX

- $280 deep support represents -9% pullback

- Below $280 would signal trend change and attract long-term buyers

Probability Assessment: Given the strong gamma support at $300, bullish net GEX, recent earnings beat, and upcoming catalysts (Intersect acquisition, Waymo expansion), the bear case requires multiple negative catalysts to materialize simultaneously. More likely to see mild pullback to $305 support rather than full breakdown.

💡 Trading Ideas

🛡️ Conservative: Cash-Secured Put Selling

The "Get Paid to Wait" Strategy

Setup:

- Sell Feb 2026 $295 Puts (6.8% below current price)

- Collect approximately $8-10 per contract ($800-1,000 per put)

- Cash secure with $29,500 per contract

Why This Works:

- $295 is below the strong $300 gamma support floor

- You get paid premium while waiting to own GOOGL at effective cost basis of $286-287

- If assigned, you're buying a company that grew revenue 16% with 30% P/E ratio

- Earnings volatility should boost premium in late January

Risk Management:

- Only sell puts on stock you'd actually want to own

- Size appropriately - don't tie up all capital in one position

- Consider selling 1-2 puts per $50K of portfolio

Best For: Investors who want to own GOOGL but think current levels are a bit rich after 74% run

⚖️ Balanced: Bull Put Spread into Earnings

The "Defined Risk, Limited Reward" Play

Setup:

- Buy Feb 2026 $295 Put / Sell Feb 2026 $305 Put

- Net credit: ~$3.50 per spread ($350 per contract)

- Max risk: $6.50 per spread ($650 per contract)

- Max profit: $3.50 per spread (54% return on risk)

Why This Works:

- Benefits from gamma support at $300 and $305 levels

- Theta decay works in your favor as time passes

- Earnings volatility crush post-Feb 3 boosts profitability

- Risk/reward ratio of 1.86:1 is attractive

- Probability of profit ~65-70% based on implied move

Risk Management:

- Max loss is defined at $650 per spread

- Exit if stock breaks below $305 decisively before earnings

- Consider taking profits at 50% of max gain ($1.75 credit)

Best For: Traders who are moderately bullish but want defined risk exposure

🚀 Aggressive: Calendar Spread for Earnings Volatility Crush

The "YOLO with Training Wheels" Strategy

Setup:

- Buy Mar 2026 $310 Call (after earnings)

- Sell Jan 2026 $310 Call (before earnings)

- Net debit: ~$4-6 per spread

Why This Works:

- Profits from implied volatility crush after earnings announcement

- Long March call benefits if stock rallies post-earnings

- Short January call funds position and captures high pre-earnings premium

- Breakeven if stock stays near $310 (current gamma pin level)

Ideal Scenario:

- Stock stays near $310 through Jan expiry (short call expires worthless)

- Earnings catalyst drives move to $320+ in February-March

- You own March $310 call cheaply to participate in upside

Risk Management:

- Max loss is net debit paid (~$400-600 per spread)

- Requires monitoring - not a set-and-forget trade

- Best executed 2-3 weeks before Jan expiry to maximize theta decay

- Exit short call if stock breaks above $315 to avoid assignment risk

Advanced Play: If you're really aggressive, consider:

- Ratio Call Spread: Buy 2x Mar $310 calls, Sell 1x Jan $310 call

- Gives you unlimited upside if GOOGL breaks out after earnings

- Higher cost but bigger payoff potential

Best For: Experienced options traders comfortable with multi-leg strategies and timing around earnings events

⚠️ Risk Factors

Let's be real about what could go wrong here:

Search Dominance Under Attack: The 17% query market share ChatGPT captured is no joke - this is the first existential threat to Google's search business in 20+ years. If this trend continues, each 1% of lost market share = billions in annual advertising revenue. The transition to AI-native search may also cannibalize traditional ad formats that print money.

Massive Capex Bet Needs to Pay Off: Google is burning through $91-93 billion in 2025 capex with "significant increases" planned for 2026. If Cloud monetization disappoints or the AI infrastructure buildout outpaces demand, margins will compress. This is a build-it-and-they-will-come strategy that requires sustained revenue growth to justify.

Advertising Headwinds Are Real: Publisher RPM/CPM crashes of 30-50% in late 2025 and network ad declines signal market stress. With ad growth decelerating from 15% to 8-10%, and no election spending boost in 2026, YouTube and Search ad revenue could underwhelm expectations.

Regulatory Overhang: While Google avoided the Chrome breakup, the company still faces mandatory data sharing with competitors and a 6-year ban on exclusive distribution contracts. A second antitrust case on digital advertising could force additional divestitures. Appeals could result in harsher remedies.

Waymo's Profitability Timeline Unknown: Despite impressive 105% ride volume growth to 450,000 weekly rides, Waymo is burning an estimated $1-2B+ annually. The path to profitability requires 10-20x more scale, and regulatory approval delays or safety incidents could derail expansion plans.

Valuation After 74% Run: At 30x P/E ratio after a monster year, GOOGL isn't exactly cheap. Any earnings miss or guidance cut could trigger profit-taking beyond what we saw today. The stock needs to grow into its valuation with continued Cloud acceleration and successful AI monetization.

Competition Intensifying:

- OpenAI's ChatGPT Search gaining traction

- Microsoft's OpenAI partnership creates competitive advantage in enterprise

- AWS and Azure have larger scale in cloud

- Meta's open-source Llama models reducing AI pricing power

Macro Headwinds: Ad spending is typically the first budget cut in recessions. Higher interest rates increase the discount rate for long-duration growth stocks like GOOGL. Geopolitical tensions (U.S.-China tech decoupling) limit market access.

🎯 The Bottom Line

Here's the deal: Today's $41M in call selling represents smart money booking profits after GOOGL's incredible 74% run, not a bearish bet on the company's future. The timing makes sense - year-end tax harvesting, consolidation after reaching $323 all-time highs in November, and 25 days until January OPEX with no major catalysts until February earnings.

If You Own GOOGL Stock:

- Hold for long-term - company fundamentals remain strong

- Consider trimming 10-20% of position to lock in gains if you're overweighted

- Use any pullback to $300-305 support as accumulation zone

- Mark your calendar for February 3 earnings (after-hours)

If You're Watching from Sidelines:

- Wait for clearer setup - stock is in no-man's land between $300 support and $310 resistance

- $305 dip would offer better risk/reward entry point

- Post-earnings volatility may create attractive entry in February

If You're Bearish:

- Don't fight the tape - GOOGL has strong gamma support at $300 and bullish net GEX

- Wait for breakdown below $300 before aggressive short positions

- Better to play range-bound with put credit spreads than outright puts

Action Plan for Next 30 Days:

- Week of Dec 23-27: Expect quiet holiday trading in $305-$315 range (1.57% implied weekly move)

- Week of Dec 30-Jan 3: Year-end rebalancing could create volatility - watch for $300 test

- Early January: Theta decay accelerates on Jan 16 options - premium sellers benefit

- Late January: Pre-earnings positioning begins - implied volatility rises into Feb 3 event

What Could Change the Thesis: ✅ Bullish catalyst: Google announces major AI partnership or Waymo funding round at >$100B valuation ✅ Bullish catalyst: Early Cloud/Gemini metrics showing stronger than expected adoption ❌ Bearish catalyst: December search market share data shows continued ChatGPT gains ❌ Bearish catalyst: Q4 guidance from peers (Microsoft, Meta) suggests ad market deterioration

Final Thought: The $41M call sale is a tactical profit-taking move, not a strategic shift. GOOGL remains a dominant force in digital advertising (90% global search share), is successfully building an AI infrastructure moat, and has multiple growth vectors (Cloud, Waymo, Pixel hardware). The stock deserves a premium valuation - the question is whether 30x P/E is reasonable after a 74% run or if we need consolidation before the next leg up.

Smart money is taking some chips off the table. That doesn't mean the game is over - it means they're managing risk after a winning year. Follow their lead: lock in some gains, keep core position, and get ready for the February earnings catalyst that will likely determine if GOOGL can push to new all-time highs above $330 or if we get a healthy 10-15% correction first.

Disclaimer: Options trading involves substantial risk and is not suitable for all investors. The strategies discussed here are for educational purposes only and do not constitute financial advice. Past performance does not guarantee future results. Always consult with a qualified financial advisor before making investment decisions, and never risk more than you can afford to lose.

Analysis based on unusual options activity detected December 22, 2025. Market conditions and company fundamentals can change rapidly. Trade at your own risk.