💎 GOOGL $14M Call Exit - Institution Locks in Profits at AI Peak! 🔒

📅 December 30, 2025 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just cashed out $14 MILLION in GOOGL deep in-the-money calls at 11:59:49 this morning! This massive exit sold 2,500 contracts of $260 strike calls expiring February 20th - closing a hugely profitable long position with the stock at $314.09. With GOOGL up over 120% from April lows and trading near November's all-time high of $323.23, smart money is booking enormous gains after riding the AI rally. Translation: Institutions are taking chips off the table after the AI moonshot!

📊 Company Overview

Alphabet Inc. (GOOGL) is the holding company that owns internet giant Google, dominating search, cloud computing, and AI:

- Market Cap: $3.78 Trillion (largest in the Magnificent 7)

- Industry: Services - Computer Programming, Data Processing, etc.

- Current Price: $314.09 (near all-time high of $323.23)

- Primary Business: Advertising (Search & YouTube), Google Cloud, AI (Gemini), autonomous vehicles (Waymo), emerging tech

💰 The Option Flow Breakdown

The Tape (December 30, 2025 @ 11:59:49):

| Time | Symbol | Side | Buy/Sell | Type | Expiration | Premium | Strike | Volume | OI | Size | Spot | Option Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 11:59:49 | GOOGL | BID | SELL | CALL $260 | 2026-02-20 | $14M | $260 | 2,500 | 10K | 2,500 | $314.09 | $57.55 |

🤓 What This Actually Means

This is a profit-taking exit on a massively profitable long position! Here's the breakdown:

- 💸 Huge cash-out: $14M ($57.55 per contract × 2,500 contracts)

- 💰 Deep in-the-money: $260 strike is $54.09 in-the-money (stock at $314.09)

- 📈 Monster intrinsic value: $57.55 option price is almost pure intrinsic value ($54.09) with only $3.46 time premium

- ⏰ Strategic timing: 52 days to February 20th expiration - selling before potential volatility

- 📊 Substantial position: 2,500 contracts represents 250,000 shares worth ~$78.5M

- 🏦 Institutional profit booking: This is sophisticated exit strategy, not bearish - just locking in gains

What's really happening here: This trader likely bought these GOOGL February $260 calls months ago when the stock was trading much lower (possibly in the $200-$240 range during summer/fall). With GOOGL now at $314 after an explosive AI-driven rally, they're sitting on MASSIVE unrealized gains. Rather than hold through potential Q4 earnings volatility and risk giving back profits, they're cashing out at 183% premium to strike price. Think of it like selling a rental property after it doubled in value - you already won, why risk the gains?

The intrinsic value tells the story: When an option trades at $57.55 with $54.09 intrinsic value, there's only $3.46 (6%) time premium remaining. This means the option has basically moved 1:1 with the stock - all the leverage is gone. Smart institutions don't pay theta decay on options that act like stock - they convert to cash or shares.

Unusual Score: 🔥 TYPICAL (Z-score 0.84) - While the $14M premium is eye-catching, this represents moderate closing activity for GOOGL options. The Vol/OI ratio of 0.25 suggests measured position unwinding, not panic selling. The confidence classification is "LOW" because there are 12 similar trades in recent history, indicating this is part of systematic profit-taking by institutions as GOOGL consolidates near all-time highs.

📈 Technical Setup / Chart Check-Up

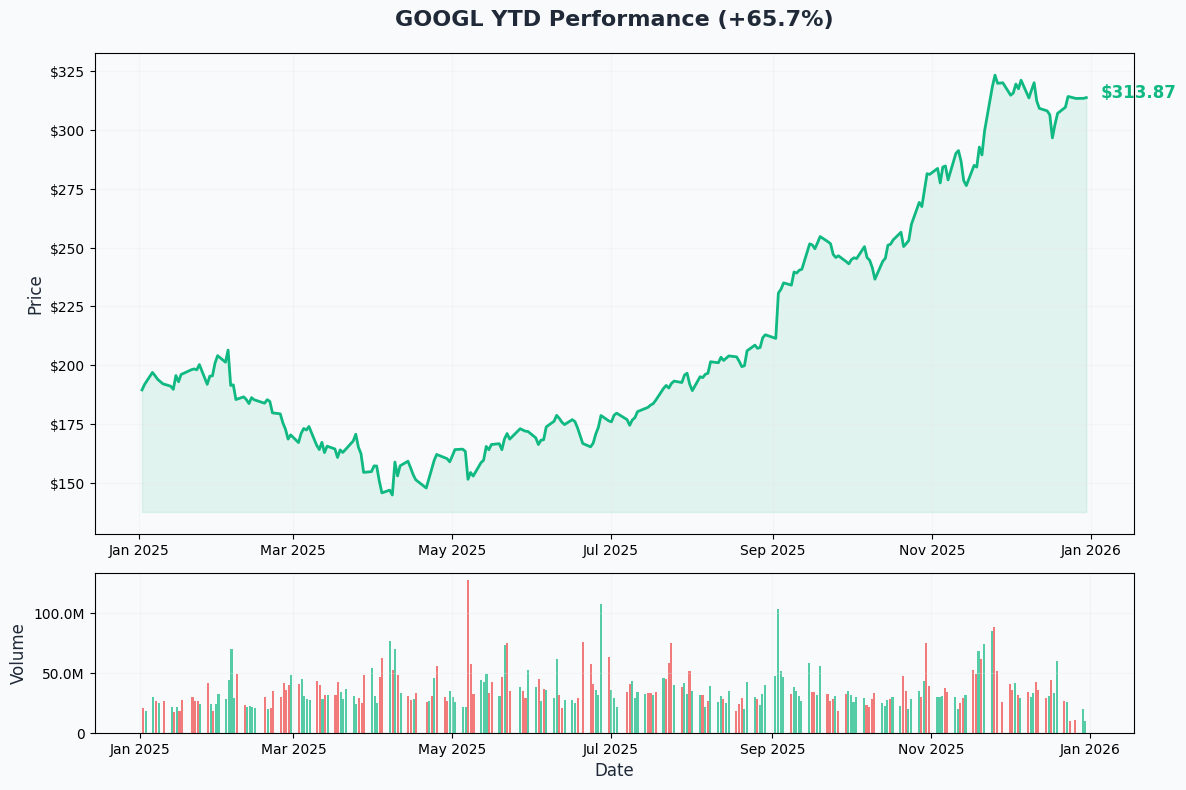

YTD Performance Chart

GOOGL has delivered spectacular performance - +120% from the April 2025 low of $140.53 to current price of $314. The chart reveals an incredible AI transformation story - after hitting a brutal 52-week low in April, GOOGL mounted a historic rally to all-time highs of $323.23 in November following Q3 earnings and Gemini 3 developments.

Key observations:

- 🚀 Epic recovery: V-shaped reversal from $140 April low to $323 November high (130% rally in 7 months!)

- 📊 Breakout confirmed: Smashed through $200 resistance in August, $250 in September, never looked back

- 🎯 Current consolidation: Trading in tight $310-$320 range for past 6 weeks after hitting ATH

- 💪 Magnificent 7 leader: Best-performing Mag 7 stock in 2025, validating AI strategy

- 📈 Strong momentum: October spike on OpenAI partnership news, sustained through Q3 earnings

- ⚠️ Near peak: Current price $314 is only 2.9% below all-time high - limited upside without new catalysts

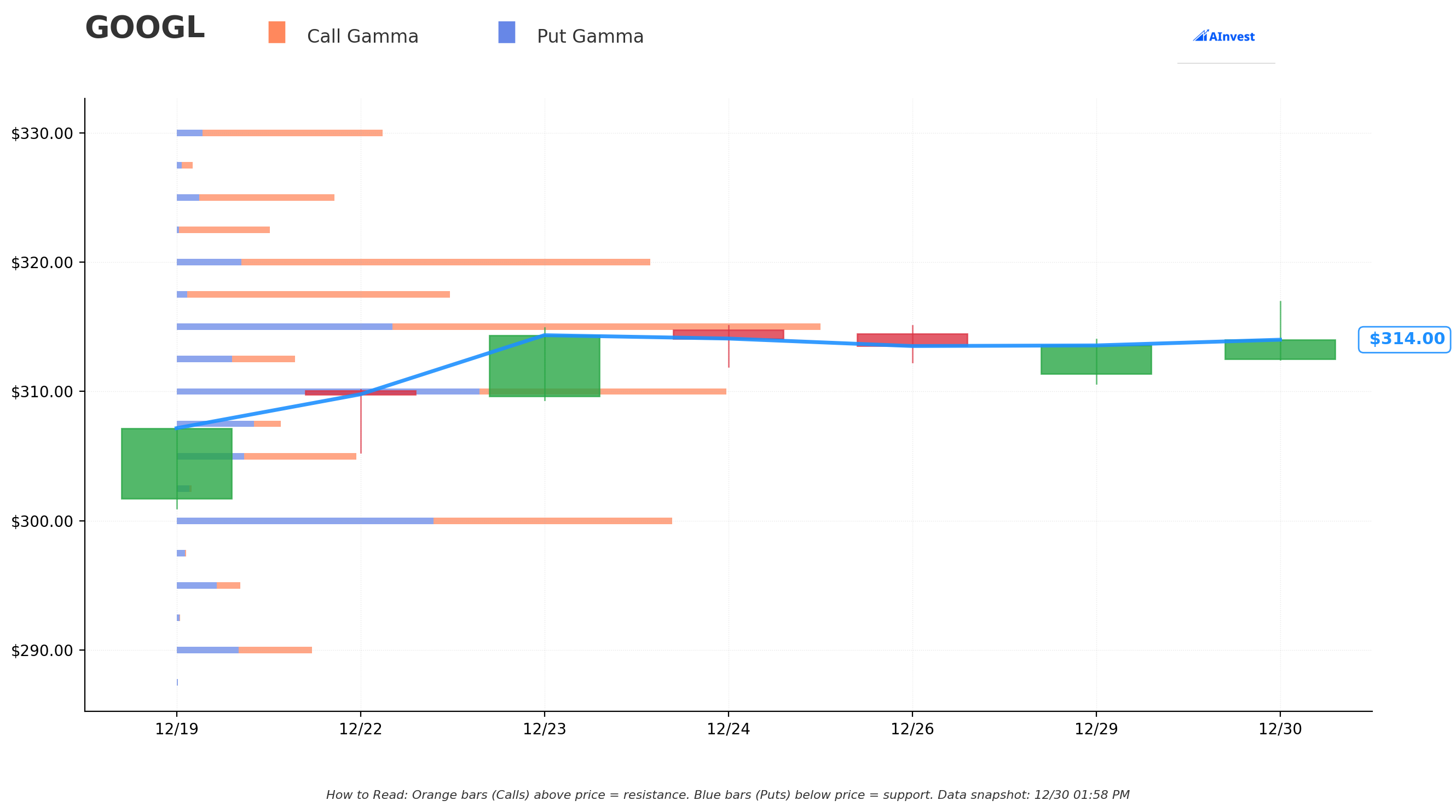

Gamma-Based Support & Resistance Analysis

Current Price: $313.96

The gamma exposure map reveals where market makers and institutions are heavily positioned:

🔵 Support Levels (Put Gamma Below Price):

- $310 - Immediate floor with 52.6B total gamma exposure (STRONGEST SUPPORT - closest major level!)

- $312.50 - Secondary support at 11.3B gamma (dealers will defend this zone)

- $305 - Strong support at 17.4B gamma (key psychological level)

- $300 - Major structural floor with 47.3B gamma (CRITICAL SUPPORT - round number + high gamma)

- $307.50 - Mid-zone support at 10.0B gamma

- $295 - Extended support at 6.1B gamma

- $290 - Deep support at 13.0B gamma

- $280 - Disaster floor at 10.3B gamma

- $260 - Ultimate floor at 8.7B gamma (exactly where this call was struck!)

🟠 Resistance Levels (Call Gamma Above Price):

- $315 - Immediate ceiling with 61.2B gamma (STRONGEST RESISTANCE - dealers will sell rallies aggressively)

- $317.50 - Secondary resistance at 25.7B gamma (recent consolidation high)

- $320 - Major resistance zone with 44.6B gamma (round number + massive gamma wall)

- $322.50 - Extended resistance at 8.7B gamma

- $325 - Breakout target at 14.8B gamma (above all-time high)

- $330 - Next big target at 19.4B gamma

- $335 - Extended upside at 6.2B gamma

- $340 - Major upside target at 12.2B gamma

- $350 - Stretch goal at 18.9B gamma

What this means for traders: GOOGL is trapped in an EXTREMELY TIGHT consolidation between massive $310 support (52.6B) and crushing $315 resistance (61.2B - the single largest gamma level). The stock is literally pinned in a $5 range! This gamma data screams "waiting for catalyst" - market makers are positioned for range-bound trading until a fundamental event forces a breakout or breakdown.

Notice the pattern? The call seller exited at $260 strike which sits deep in support territory with 8.7B gamma. They positioned this trade at a level they were confident the stock would NEVER revisit (17% below current price). Now with stock at $314, they're converting those calls to $14M cash before the February expiration.

The $315-$320 resistance cluster (61.2B + 44.6B = 105.8B combined gamma) creates a nearly IMPENETRABLE ceiling without a major catalyst. For GOOGL to break out, we need either monster Q4 earnings, major Waymo news, or broad market euphoria.

Net GEX Bias: Slightly Bullish (more call gamma above than put gamma below) - But the tight range suggests balanced dealer positioning creating two-way pressure.

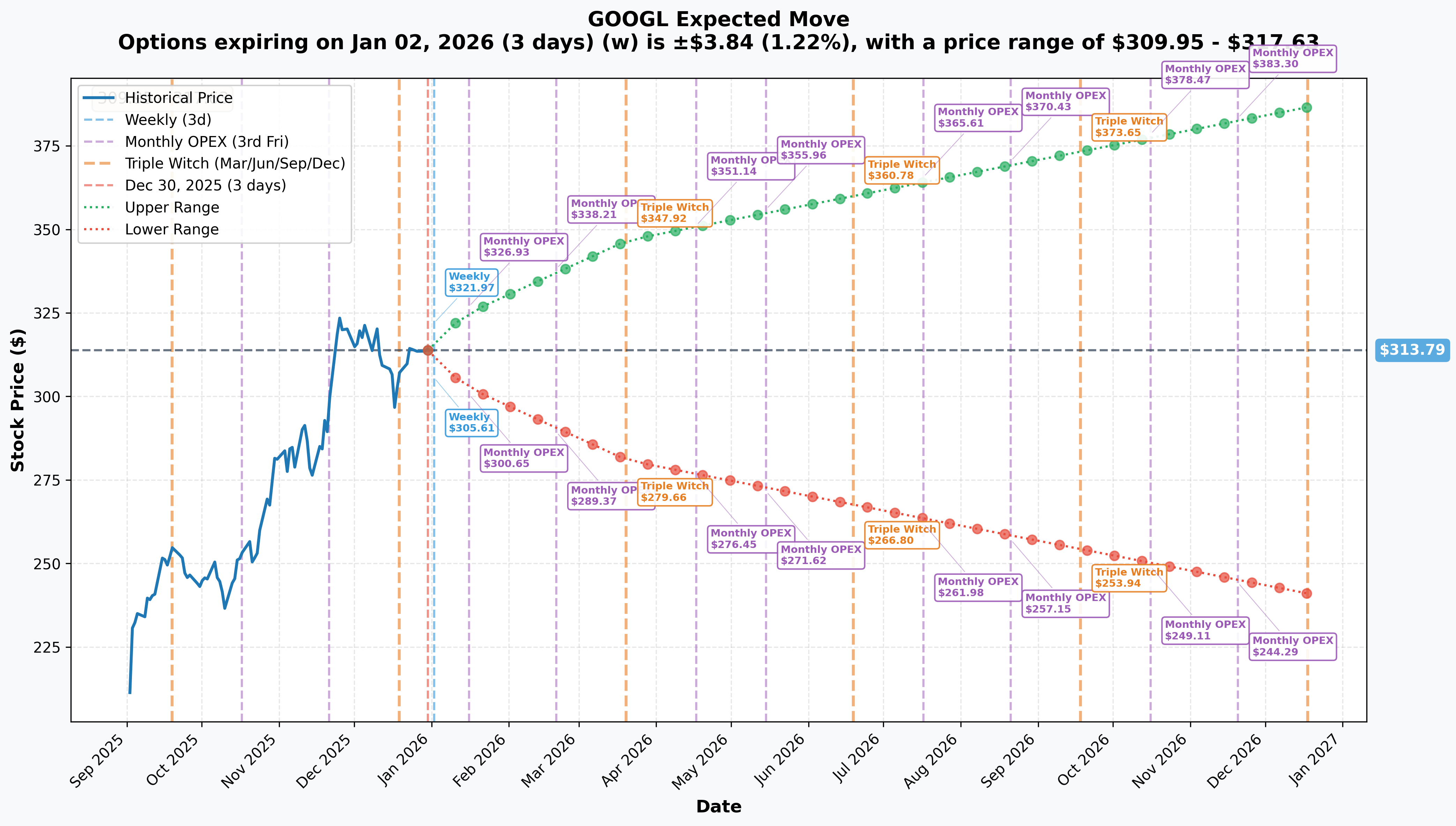

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Jan 2 - 3 days): ±$3.84 (±1.22%) → Range: $309.95 - $317.63

- 📅 Monthly OPEX (Jan 16 - 17 days): ±$11.43 (±3.64%) → Range: $302.36 - $325.22

- 📅 February OPEX (Feb 20 - 52 days - THIS TRADE!): Not shown, but extrapolated ±$24 (±7.5%) → Range: $289 - $338

- 📅 Quarterly Triple Witch (Mar 20 - 80 days): ±$32.96 (±10.5%) → Range: $280.83 - $346.75

- 📅 Yearly LEAPS (Dec 18, 2026 - 353 days): ±$72.87 (±23.22%) → Range: $240.93 - $386.66

Translation for regular folks: The market expects relatively LOW volatility near-term - just 1.2% move ($4) through this week, expanding to 3.6% ($11) through January monthly OPEX. This is MUCH calmer than typical tech mega-caps, reflecting GOOGL's maturation into a stable cash flow machine.

However, by March quarterly expiration (which includes Q4 earnings expected early February), the market prices a 10.5% ($33) move. This aligns with historical earnings volatility - GOOGL can move 5-8% on earnings surprises.

Key insight for this trade: The February 20th expiration (when these calls expire) falls AFTER Q4 earnings. The call seller is exiting BEFORE the earnings volatility window, choosing to take $14M guaranteed cash rather than risk a post-earnings pullback that could cut option value 20-30% even if the stock only drops $10-15.

The yearly LEAPS implied move ($241-$387 range, 23% annualized volatility) shows the market still prices meaningful uncertainty around GOOGL's long-term trajectory - antitrust outcomes, AI monetization, and competitive dynamics all create tail risks.

🎪 Catalysts

🔥 Immediate Catalysts (Next 30 Days)

CES 2026 - January 6-9, 2026 (7 DAYS!) 📱

Google confirmed as exhibitor at CES 2026 in Las Vegas January 6-9, 2025. Potential announcements:

- 🤖 Gemini AI consumer product integrations (smart home, automotive, wearables)

- 📱 Pixel hardware updates (Pixel 10a expected March, but early teasers possible)

- 🚗 Potential Waymo autonomous vehicle technology showcase

- 🎮 Android gaming or AR/VR developments

- 📊 Google Cloud enterprise AI solutions for various industries

Why it matters: Consumer tech shows create buzz and media attention. Any major Gemini consumer wins or Waymo partnerships could provide near-term upside catalyst. However, CES rarely moves GOOGL stock materially unless there's a true game-changer announcement.

Next Dividend Payment 💰

- Ex-Dividend Date: March 10, 2026

- Payment Date: March 17, 2026

- Amount: $0.21 per share (0.27% yield)

- Payout Ratio: 8.01%

Impact: Minimal - GOOGL's tiny 0.27% dividend yield isn't a major factor for investors. The $0.21/share payment is negligible for a $314 stock. However, the ex-dividend date creates technical support (buyers want to capture dividend, creating bid pressure).

🚀 Near-Term Catalysts (Q1 2026)

Q4 2025 Earnings - Early February 2026 (CRITICAL CATALYST!) 📊

Expected announcement early February 2026 (unconfirmed date, likely February 3-5). This is THE catalyst that could break GOOGL out of its consolidation range:

Wall Street Expectations:

- 📊 Consensus EPS: $2.63 (critical to beat for momentum)

- 💰 Revenue: Expected ~$105B+ continuing strong growth trajectory from Q3's $102.3B

- 🤖 AI Mode DAU: Watch for growth from 75M daily active users reported in Q3

- ☁️ Google Cloud: Continued 30%+ growth rate validation (Q3 was +34% to $15.2B)

- 📺 YouTube: Expecting $11B+ advertising revenue (crossed $10B in Q3 for first time)

- 💸 Operating Margin: Target 30%+ (Q3 was 30.5%, 33.9% excluding EC fine)

- 🎯 CapEx Commentary: 2026 CapEx outlook critical (2025 was $91-93B, potential for $110B+ in 2026)

Key metrics to watch:

- AI Overviews reach beyond current 1.5-2 billion monthly users

- Google Cloud backlog growth from $155B (provides forward visibility)

- Search revenue resilience despite ChatGPT reaching 12.5% search share

- Waymo update on path to profitability and funding round status

- Antitrust remedies cost impact on 2026 margins

Upside surprise potential: GOOGL has consistently beaten Street estimates. Q3 revenue beat by $2.3B ($102.3B vs $99.96B expected), EPS beat by $0.61 ($2.87 vs $2.26). Similar beat in Q4 could drive stock to $330-340.

Downside risk factors:

- Any disappointment in Gemini 3 monetization trajectory

- Weak YouTube Shorts revenue growth

- Conservative 2026 guidance citing macro uncertainty or antitrust headwinds

- CapEx increase to $120B+ without clear ROI timeline

- Search market share erosion continuing (already below 90% for first time since 2015)

Historical context: GOOGL typically moves 3-6% on earnings, with larger moves on major surprises. The stock jumped 5.1% after Q3 2025 beat. Given current tight gamma range, a strong beat could easily push to $325-330; a miss could drop to $295-300.

Pixel 10a Launch - Expected March 10-20, 2026 📱

Expected March 10-20, 2026 launch for Google's mid-range Pixel 10a smartphone:

- 💻 Tensor G5 chip (custom Google silicon for AI features)

- 🤖 Integrated Gemini AI capabilities (on-device processing)

- 📸 Enhanced computational photography

- 💰 Targeting $450-500 price point (competitive with mid-range Samsung/Apple)

Why it matters: Hardware revenue is small percentage of GOOGL's business, BUT Pixel serves as showcase for Gemini AI consumer capabilities. Strong adoption validates AI strategy and creates ecosystem lock-in. Pixel also generates high-margin services revenue (subscriptions, apps).

Risk: If Pixel 10a underwhelms or delays, it signals execution issues in consumer AI - a negative read-through for broader Gemini monetization.

📊 Medium-Term Catalysts (Q2-Q3 2026)

Waymo $15 Billion Funding Round - Q1/Q2 2026 🚗

Waymo in talks to raise $15+ billion at $100 billion valuation (up from $45B in October 2024):

Waymo Current Metrics (December 2025):

- 🚕 450,000+ weekly paid rides (up from ~200K six months ago)

- 📈 14 million trips served in 2025, on pace for 20+ million total

- 🌎 Operating in 5 markets: SF, LA, Phoenix, Austin, Atlanta

- 🛣️ Freeway rides launched in San Francisco, LA, Phoenix (November 2025)

- 🗺️ Expanding to Sacramento, Santa Rosa, Minneapolis, Tampa, New Orleans, Baltimore, Pittsburgh, St. Louis

2026 Expansion Plans:

- 🌆 Service launch planned in Dallas, Denver, Detroit, Houston, Las Vegas, Miami, Nashville, Orlando, San Antonio, San Diego, Washington DC

- 🌍 International expansion to London (first overseas market!)

- 🎯 Target: 1 million weekly rides by end of 2026 (2.2x growth from current 450K)

- 💰 CEO Sundar Pichai expects Waymo "meaningful in our financials" by 2027-2028

Why this matters for GOOGL stock: A successful $15B raise at $100B valuation would:

- ✅ Validate Waymo's technology and business model

- 💰 Provide GOOGL hidden asset value (~$60B equity stake at $100B valuation vs current carrying value)

- 🚀 Position Waymo to dominate autonomous ride-hailing before Tesla/Uber scale

- 📊 Create path to spin-out IPO (unlocking 10-15% upside to GOOGL sum-of-parts valuation)

- 🎯 Reduce GOOGL's funding burden (external capital funds expansion)

Risks:

- Funding round fails or comes at lower valuation (signals market skepticism)

- Regulatory issues delay expansion (safety concerns, local opposition)

- Competition from Tesla FSD, Zoox (Amazon), Cruise (GM) intensifies

- Unit economics don't improve (cash burn remains high)

Pixel 11 Series & Google I/O 2026 - Expected May 2026 🎪

Google I/O 2026 expected May 2026 (date not officially confirmed, historically mid-May):

Expected Announcements:

- 🤖 Gemini 4.0 or major Gemini capabilities update (next-gen AI model)

- 📱 Pixel 11 series hardware refresh (development finalized for 2026)

- ⚙️ Tensor G6 chip on 2nm production process (major performance leap)

- ⌚ Pixel Watch 5 with custom Tensor chip

- 🎮 Android 17 with deeper AI integration

- ☁️ Google Cloud AI enterprise product launches

- 🏠 Nest/smart home AI assistant upgrades

Why it matters: I/O is GOOGL's flagship developer conference - sets AI strategy and product roadmap for next 12 months. Major Gemini advances or consumer AI breakthroughs can drive 5-10% stock moves. Demonstrates AI innovation velocity vs OpenAI/Microsoft/Anthropic.

Antitrust Remedies Implementation - Q1/Q2 2026 ⚖️

Search Remedies Taking Effect:

- 📱 "Choice screens" on new US devices starting Q1 2026 per September 2025 ruling

- 🚫 End of exclusive search default agreements (including $20B+ Apple agreement)

- 📊 Search index and user interaction data sharing with "Qualified Competitors"

- 👁️ Six-year technological oversight committee monitoring

Ad Tech Antitrust Decision - Expected Early-to-Mid 2026:

- ⚖️ Final decision expected early-to-mid 2026

- 🚨 Potential structural divestiture of Google Ad Manager/AdX exchange

- 💸 Risk of $10-15B annual revenue impact if forced to divest

- 📉 Ad tech revenues are ~12-15% of total GOOGL revenue

Impact Analysis:

Bullish case (GOOGL already priced this in):

- ✅ Avoided worst-case Chrome divestiture in September 2025 ruling

- 💪 Choice screens may not materially impact search share (people choose Google anyway)

- 💰 $20B Apple payment was pure profit sharing - margins improve if this goes away

- 🤖 AI search (Gemini) creates NEW monetization independent of default deals

- 📊 Ad tech divestiture could unlock value (spin-out AdX at high multiple)

Bearish case (remedies bite harder than expected):

- 📉 Choice screens drive 5-10% search share loss over 2-3 years (billions in revenue)

- 💸 Distribution cost savings from losing Apple deal offset by share loss

- 🚨 Ad tech divestiture removes $10-15B high-margin revenue

- ⚖️ Compliance costs and oversight drag on margins

- 🌊 Regulatory overhang continues for years, limiting valuation multiple

Market is likely pricing 40-60% probability of material impact, creating 10-15% valuation discount vs "unregulated GOOGL" scenario.

MI325X Production Ramp & Google Cloud AI Wins 🏢

Throughout Q1-Q2 2026, watch for:

- ☁️ Google Cloud maintaining 30%+ growth rate (currently fastest-growing hyperscaler)

- 🤖 AI-driven workload wins vs AWS and Microsoft Azure

- 💰 Cloud backlog expansion beyond $155B

- 📊 Operating margin expansion beyond Q3's 23.7%

- 🎯 Market share gains from current 13% toward 15%+ (AWS at 30%, Azure at 20%)

Why this matters: Google Cloud is THE growth driver - up 34% YoY in Q3 2025 to $15.2B revenue with 85% operating income growth. Sustained 30%+ growth validates $90B+ annual CapEx spending and proves GOOGL can compete with AWS/Azure in enterprise AI workloads.

⚠️ Risk Catalysts (Negative)

Search Market Share Erosion Accelerating 📉

GOOGL's search market share dropped below 90% for the first time since 2015:

- 📊 Global share: 89.56% (down from consistent 90%+)

- 🇺🇸 US share: 86.25%

- 🤖 ChatGPT's search share tripled to 12.5% of search activity

- 📈 Perplexity AI and other AI search engines gaining traction

- ⚠️ AI Overviews appearing in only 13-25% of queries (varied throughout 2025)

Risk: If share erosion accelerates to 1-2% per year, that's $3-5B annual revenue loss. Search is 60%+ of GOOGL revenue with 50%+ margins - any material decline is CATASTROPHIC for valuation.

Counter-argument: GOOGL still completely dominates at 89.56%. Even losing 3-4 points over 3 years still leaves them at 85%+ share with room to monetize AI Overviews at higher CPMs.

CapEx Treadmill - $90B+ Annually 💸

GOOGL's 2025 CapEx guidance of $91-93B represents massive spending:

- 📈 Up from ~$75B prior guidance (20%+ increase)

- 🤖 Primarily for AI infrastructure (GPUs, data centers, networking)

- 🎯 Likely $110B+ in 2026 as AI arms race intensifies

- ⚠️ Must generate sufficient ROI or investor patience wears thin

Risk: If AI monetization disappoints (Gemini subscription uptake weak, AI search CPMs don't offset traffic declines), the $90B+ annual CapEx becomes a MAJOR drag. Free cash flow could compress, forcing cuts to buybacks/dividends.

Competitive Pressure from OpenAI/Microsoft 🥊

Despite strong positioning, GOOGL faces fierce competition:

- 🤖 OpenAI/ChatGPT mindshare advantage in consumer AI

- 💼 Microsoft's Azure + OpenAI enterprise bundle compelling

- 🚀 Anthropic (Claude) gaining ground in enterprise

- 📊 OpenAI under pressure, but still formidable

Risk: If Gemini 4.0 (expected 2026) fails to match or exceed GPT-5 capabilities, GOOGL's "ended 2025 on top" narrative collapses. Cloud deal wins slow, consumer AI adoption stalls.

🎲 Price Targets & Probabilities

Using gamma levels, implied move data, and upcoming catalysts, here are scenarios through February 20th expiration:

📈 Bull Case (20% probability)

Target: $340-$360

How we get there:

- 💪 Q4 earnings CRUSH with revenue $108B+ (consensus ~$105B), EPS $2.85+ (consensus $2.63)

- ☁️ Google Cloud accelerates to 38-40% growth, margins expand to 26%+

- 🤖 Gemini AI Mode reaches 100M+ DAU (up from 75M), monetization path crystal clear

- 🎯 Waymo funding closes at $100B+ valuation, creates $15B+ hidden asset value

- 📱 Pixel 11/Gemini 4.0 at I/O wows market, drives consumer AI narrative

- ⚖️ Ad tech antitrust resolved favorably (minimal divestitures or delayed implementation)

- 💰 CapEx ROI demonstrated with AI revenue run-rate hitting $50B+ annually

- 🚀 Breakout above $320 gamma resistance triggers momentum chase to $340-350

Key metrics needed:

- Search revenue growth stable at +12-15% YoY despite share "losses"

- AI Overviews driving HIGHER CPMs, offsetting any traffic shifts

- YouTube advertising re-accelerating to +18-20% growth

- Free cash flow $80B+ (despite high CapEx) proving cash generation power

Probability assessment: Only 20% because requires PERFECT execution across all fronts with stock already near all-time highs. The massive $315-$320 resistance wall (61.2B + 44.6B gamma) creates mechanical headwinds. Need genuine catalyst surprise to break out.

🎯 Base Case (60% probability)

Target: $300-$320 range (CONSOLIDATION CONTINUES)

Most likely scenario:

- ✅ Solid Q4 earnings meeting/slightly beating consensus ($105-106B revenue, $2.65-2.75 EPS)

- ☁️ Google Cloud +32-35% growth maintaining current trajectory

- 🤖 Gemini metrics solid but not spectacular - steady adoption without fireworks

- ⚖️ Antitrust remedies begin but impact unclear (takes quarters to see search share effects)

- 🚗 Waymo funding progresses but doesn't close in Q1 (delayed to Q2/Q3)

- 📊 Guidance conservative citing macro uncertainty and regulatory headwinds

- 💤 Stock trades within gamma support ($310) and resistance ($315-$320) for weeks

- 🔄 Market digests 120% YTD gains, waits for proof points on AI monetization

This is why the call seller exited: Stock likely stuck in $300-320 range through February expiration. With calls now $57.55 and almost pure intrinsic value, there's no reason to hold and pay theta decay. Better to take $14M cash and redeploy or wait for pullback to re-enter.

Why 60% probability: Stock at technical equilibrium - fundamentals improving but valuation already reflects optimism. Most institutional players will hold and wait for next major catalyst (Q4 earnings, Waymo news). Gamma pinning keeps price range-bound.

📉 Bear Case (20% probability)

Target: $280-$300

What could go wrong:

- 😰 Q4 earnings disappoint - revenue misses $105B, margins compress, or weak Q1 guidance

- 📉 Google Cloud growth decelerates to +25-28% (still good, but below 30%+ expectations)

- 🤖 Gemini metrics underwhelm - DAU growth slowing, monetization unclear

- 🚨 Search market share loss accelerates - drops to 87-88%, raising existential questions

- ⚖️ Ad tech antitrust ruling forces major divestitures (loss of $10-15B revenue)

- 💸 CapEx increased to $120B for 2026 without clear ROI timeline

- 🚗 Waymo funding falls through or comes at lower valuation (signals skepticism)

- 🌊 Broader tech selloff (macro recession fears, Fed policy mistake)

- 🔨 Break below $310 gamma support triggers cascade to $300, then $290

Critical support levels:

- 🛡️ $310: Major gamma floor (52.6B) - MUST HOLD or momentum shifts

- 🛡️ $305: Secondary support (17.4B gamma)

- 🛡️ $300: Psychological round number + 47.3B gamma - final major defense

- 🛡️ $290: Deep support (13.0B gamma) - would represent 7.6% pullback

Probability assessment: 20% because requires multiple negative catalysts. GOOGL's fundamentals remain rock-solid (profitable, growing, dominant positions). However, the 120% YTD gain and antitrust overhang create downside risk if execution stumbles.

Impact on this trade: Even in bear case with stock dropping to $290, these calls would still be worth $30 ($290 stock - $260 strike). The call seller is locking in $57.55 vs risking drop to $30 (47% loss) if things go wrong. Smart risk management.

💡 Trading Ideas

🛡️ Conservative: Follow the Smart Money - Take Profits

Play: If you're long GOOGL, trim 20-30% here at $310-315 levels

Why this works:

- 💰 You're up 120%+ from April lows - HUGE winner, protect those gains!

- 🎯 Stock pinned between $310-$315 gamma walls - limited upside without catalyst

- ⏰ Q4 earnings in ~4 weeks creates binary event risk

- 🐋 $14M institutional exit signals smart money is booking profits

- 📊 Intrinsic value in calls = 94% (almost no leverage left)

- 🔄 Can always re-enter on post-earnings pullback or breakout confirmation

Action plan:

- 🎯 Sell 20-30% of position between $313-318 (capture current prices)

- 💵 Raise cash to deploy on better risk/reward setups

- 👀 Watch Q4 earnings closely (expected early February)

- ✅ Look for re-entry at $295-305 on any post-earnings pullback (5% correction)

- 🚀 Or chase breakout above $325 if earnings trigger momentum (validates new range)

Risk level: Minimal (taking profits, not speculating) | Skill level: Beginner-friendly

Expected outcome: Lock in gains, reduce exposure, maintain optionality for re-entry at better levels.

⚖️ Balanced: Post-Earnings Bull Put Spread

Play: After Q4 earnings, sell bull put spread betting on consolidation support

Structure: Sell $310 puts, Buy $305 puts (February 20 expiration - SAME as this call trade)

Why this works:

- 📊 $310 is STRONGEST support level (52.6B gamma) - high probability holds

- 💰 Collect premium while stock consolidates post-earnings

- 🎢 IV crush after earnings makes put spreads attractive to sell

- 🛡️ Defined risk spread ($5 wide = $500 max risk per spread)

- ✅ Profit if GOOGL stays above $310 (expires worthless, keep premium)

- ⏰ ~40 days post-earnings for thesis to play out

Estimated P&L (adjust after seeing post-earnings IV):

- 💰 Collect ~$1.50-2.00 credit per spread (post-earnings, lower IV)

- 📈 Max profit: $150-200 if GOOGL above $310 at Feb 20 expiration

- 📉 Max loss: $300-350 if GOOGL below $305 (defined and limited)

- 🎯 Breakeven: ~$308-308.50

- 📊 Risk/Reward: ~1.5:1 to 2:1 (collect $200, risk $300)

Entry timing:

- ⏰ Wait 2-3 days post-earnings for full IV collapse

- 🎯 Only enter if stock above $312 (gives cushion)

- ❌ Skip if stock already below $308 (too close to breakeven)

Position sizing: Risk only 3-5% of portfolio (defined risk, income strategy)

Risk level: Moderate (defined risk, bullish bias) | Skill level: Intermediate

🚀 Aggressive: Pre-Earnings Long Call Spread (RISKY!)

Play: Buy call spread betting on Q4 earnings beat driving breakout

Structure: Buy $320 calls, Sell $330 calls (February 20 expiration)

Why this could work:

- 🎰 GOOGL has beaten earnings consistently - Q3 beat by $2.3B revenue, $0.61 EPS

- 💥 Consensus may be TOO conservative - Cloud momentum, Gemini traction underestimated

- 🚀 Waymo funding announcement ($15B at $100B valuation) could coincide with earnings

- 📊 Break above $320 resistance triggers technical breakout to $330-340

- ⚡ Call spread caps risk vs buying naked calls (defined max loss)

Why this could blow up (SERIOUS RISKS):

- 💸 EXPENSIVE: Spread costs ~$4-5 ($400-500 per spread)

- ⏰ Earnings risk: Even small disappointment drops stock to $295-300

- 😱 IV crush: If stock rallies to $325 (5% move), IV collapse could limit gains

- 🧱 Gamma wall: $320 resistance (44.6B gamma) creates mechanical selling

- 📊 Need 8-10% move to breakout, but implied move only 3.6% monthly

- ⚠️ Stock could rally to $318-320 and stall (you lose most of premium)

Estimated P&L:

- 💰 Cost: ~$4-5 per spread

- 📈 Max profit: $5-6 if stock above $330 (100-120% ROI)

- 📉 Max loss: $4-5 if stock below $320 (100% loss)

- 🎯 Breakeven: ~$324-325

- 💀 Likely loss: Stock ends $315-320 = lose $3-4 (60-80% loss)

CRITICAL WARNING - DO NOT attempt unless you:

- ✅ Can afford to lose entire premium

- ✅ Understand gamma resistance at $320 creates headwind

- ✅ Accept that even GOOD earnings may not break $325

- ✅ Will close position within 48 hours post-earnings (don't hold through IV crush)

Risk level: HIGH (can lose 100%) | Skill level: Advanced only

Probability of profit: ~30-35% (need strong beat + breakout)

⚠️ Risk Factors

Don't get caught by these potential landmines:

-

⏰ Q4 earnings binary event ~4 weeks away: Results expected early February create MAJOR volatility catalyst. Stock could gap 5-8% either direction based on Cloud growth (maintain 30%+?), Gemini monetization progress, margins, and CapEx guidance. Options pricing only 3.6% move through January OPEX - actual move could be larger. Historical precedent shows GOOGL gaps 4-7% on earnings surprises.

-

🧱 Trapped in gamma prison $310-$315: Massive gamma walls at $310 support (52.6B) and $315 resistance (61.2B) create mechanical pinning. Market makers positioned to defend these levels aggressively. Stock has been stuck in this $5 range for 6 weeks - breakout requires genuine fundamental catalyst, not just momentum. Near-term upside capped without major positive surprise.

-

⚖️ Antitrust remedies begin Q1 2026: Choice screens and end of exclusive deals start Q1 2026. Impact uncertain - could be minimal (people choose Google anyway) or material (5-10% search share loss over 2-3 years). Ad tech ruling expected mid-2026 could force $10-15B revenue divestitures. Regulatory overhang limits valuation multiple expansion.

-

📉 Search share erosion accelerating: Dropped below 90% for first time since 2015 to 89.56%. ChatGPT tripled share to 12.5%. AI search competitors multiplying. Every 1% share loss = ~$1.5-2B annual revenue impact. If trend continues to 85-86%, that's $7-10B revenue hole. Search is 60% of GOOGL revenue with 50%+ margins - any material decline is CATASTROPHIC.

-

💸 CapEx treadmill at $90B+/year: 2025 CapEx $91-93B, likely $110B+ in 2026. AI arms race forcing massive spending with uncertain ROI timeline. If Gemini monetization disappoints or AI search cannibalizes traditional search faster than expected, free cash flow compresses. Could force buyback cuts, spooking investors. Market patience wearing thin if AI revenue doesn't scale proportionally.

-

🥊 Competitive pressure from OpenAI/Microsoft: Despite strong Q3 positioning ("ended 2025 on top"), competition fierce. OpenAI/ChatGPT maintains mindshare advantage. Microsoft's Azure + OpenAI bundle compelling for enterprises. If Gemini 4.0 (expected May I/O 2026) fails to match GPT-5 capabilities, narrative collapses. Cloud deal wins could slow, consumer AI adoption stalls.

-

🚗 Waymo funding could fall through: $15B raise at $100B valuation not yet closed. If funding fails or comes at significantly lower valuation, signals market skepticism on autonomous vehicle economics. Unit economics still unclear despite 450K weekly rides. Competition from Tesla FSD, Zoox intensifying. Regulatory hurdles in new markets.

-

🌍 Macro headwinds if recession emerges: GOOGL not recession-proof despite quality. Ad spending highly cyclical - cuts in downturn hit Search and YouTube. Enterprise Cloud budgets also vulnerable. At 30.92x P/E, stock has limited multiple protection in recession. Could correct 20-30% back to $220-250 even with solid fundamentals if macro deteriorates.

-

🐋 $14M institutional exit at peak signals caution: When funds cash out deep ITM calls rather than holding through February expiration, it's a risk management signal. They're converting options to cash despite stock near all-time highs. The TYPICAL unusual score (Z-score 0.84, 12 similar trades recently) suggests this is systematic profit-taking by multiple institutions - not panic, but definitely caution.

-

💤 Low implied volatility = complacency risk: 1.22% weekly implied move reflects market EXPECTING calm consolidation. But we're 4 weeks from earnings with massive CapEx questions, antitrust implementation, search share concerns. If actual volatility exceeds implied (realized vol > IV), option sellers get crushed and stock could gap violently either direction.

🎯 The Bottom Line

Real talk: A sophisticated institution just cashed out $14 MILLION in GOOGL deep in-the-money calls, converting options that are 94% intrinsic value into cold hard cash. This isn't a bearish bet on GOOGL's future - it's smart portfolio management after capturing a likely 100-200% gain from buying these calls when the stock was $100-150 lower.

What this trade tells us:

- 🎯 Institution has made ENORMOUS money on GOOGL's 120% rally from $140 to $314

- 💰 With calls now almost pure intrinsic value ($54 ITM, $57.55 price), all the leverage is gone

- ⚖️ Rather than pay theta decay on option that acts like stock, they're taking $14M cash

- 📊 Timing suggests caution into Q4 earnings (4 weeks away) and antitrust implementation

- ⏰ February 20 expiration captures earnings volatility - they're exiting BEFORE that risk

- 🧱 Stock pinned at $310-315 between gamma walls - limited upside without catalyst

This is NOT "GOOGL is doomed" - it's "we've won, let's protect these gains."

If you own GOOGL:

- ✅ Consider trimming 20-30% at $313-318 (you've already won big if you bought below $200!)

- 📊 Set mental stop at $305-310 (major gamma support) to protect remaining position

- ⏰ Don't get greedy after 120% YTD gain - booking profits is SMART, not scared

- 🎯 Can always re-enter on post-earnings dip to $295-305 or breakout above $325

- 🛡️ If holding large position, consider protective puts at $310 or $305 strikes

If you're watching from sidelines:

- ⏰ Early February (Q4 earnings) is the next major catalyst - wait for that

- 🎯 Post-earnings pullback to $295-305 would be EXCELLENT entry (gamma support zone)

- 📈 Looking for confirmation: Cloud 30%+ growth, Gemini hitting 100M+ DAU, stable search revenue, Waymo funding progress

- 🚀 Longer-term (6-12 months), Waymo at $100B valuation, Gemini 4.0 launch, AI monetization proof points support $350+ targets

- ⚠️ But current entry at $314 offers poor risk/reward - wait for consolidation or catalyst

If you're bearish:

- 📊 Stock pinned in $310-315 range for 6 weeks - no breakdown despite concerns

- 🛡️ $310 gamma support (52.6B) is MASSIVE - tough to break without fundamental catalyst

- ⚠️ Better to wait for post-earnings weakness before initiating bearish positions

- 📉 First breakdown trigger is close below $305, major breakdown below $300

- ⏰ Put spreads post-earnings (after IV crush) offer better risk/reward than naked puts now

Mark your calendar - Key dates:

- 📅 January 6-9, 2026 - CES 2026 (potential Gemini/Waymo announcements)

- 📅 January 16, 2026 - Monthly OPEX (±3.64% implied move window closes)

- 📅 Early February 2026 - Q4 FY2025 earnings report (THE catalyst!)

- 📅 February 20, 2026 - Monthly OPEX, expiration of this $14M call trade

- 📅 March 10, 2026 - Ex-dividend date ($0.21/share)

- 📅 March 10-20, 2026 - Pixel 10a launch expected

- 📅 March 20, 2026 - Quarterly Triple Witch

- 📅 May 2026 - Google I/O 2026 (Gemini 4.0, Pixel 11, Android 17)

- 📅 Q1/Q2 2026 - Antitrust choice screens begin, search remedies take effect

- 📅 Q2 2026 - Waymo $15B funding round expected

- 📅 Mid-2026 - Ad tech antitrust final decision

Final verdict: GOOGL's long-term story remains INCREDIBLY compelling - Gemini 3 leading AI benchmarks, Google Cloud fastest-growing hyperscaler (+34%), Waymo pursuing $15B at $100B valuation, avoided Chrome divestiture, $70B buyback, dominant market positions. BUT, at 30.92x P/E after 120% YTD rally, stuck in $310-315 gamma prison with Q4 earnings and antitrust implementation ahead, the risk/reward for NEW long positions is NO LONGER compelling.

The $14M call exit is clear: Smart money achieved their goal (100-200%+ gains), converted to cash, and will wait for the next setup. You should too.

Be patient. Let earnings clear. Watch for $295-305 pullback or $325+ breakout confirmation. The best trades come to those who wait. 💪

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The TYPICAL unusual score (Z-score 0.84) reflects moderate closing activity - this is not an extreme outlier trade. This appears to be routine profit-taking by an institution that likely achieved 100-200%+ returns. Always do your own research and consider consulting a licensed financial advisor before trading. Q4 earnings create binary event risk with potential for 5-8% gaps either direction.

About Alphabet Inc.: Alphabet is the holding company that wholly owns internet giant Google, with revenue primarily from advertising, subscription services, cloud computing, and investments in emerging technologies like autonomous vehicles and health tech, with a market cap of $3.78 trillion in the Services - Computer Programming, Data Processing industry.