🛡️ GOOGL $1.5M Deep OTM Put Bet - Someone's Buying Heavy Insurance on Alphabet!

📅 March 3, 2026 | 🔥 Unusual Activity Detected

🎯 The Quick Take

Someone just dropped $1.5 MILLION on 10,000 GOOGL $215 puts expiring May 15th - that's 28% below the current price. This isn't a casual hedge; the Z-Score of 306 makes this one of the most statistically unusual trades we've tracked on $GOOGL, appearing only a handful of times per year. With an ad tech antitrust ruling looming, massive capex concerns, and the stock already down 11% from its all-time high, an institutional player is paying up for serious downside protection.

📊 Company Overview

Alphabet Inc. Class A Common Stock (GOOGL) is the holding company behind Google, the world's dominant search engine and advertising platform:

- Market Cap: $3.71 Trillion

- Industry: Services - Computer Programming, Data Processing, Etc.

- Exchange: NASDAQ

- Current Price: ~$302.30 (down ~11% from ATH of $343.69)

- Employees: 190,820

- Primary Business: Google Search & Advertising (~90% of revenue), Google Cloud (~10%), YouTube, Waymo autonomous vehicles, and other bets

Alphabet derives roughly 90% of its revenue from Google services, the vast majority of which is advertising. Google Cloud has been the growth engine lately, up 48% YoY with a $240B backlog. Meanwhile, Waymo just raised $16B at a $126B valuation, making it one of the most valuable "other bets" in corporate history.

💰 The Option Flow Breakdown

The Tape (March 3, 2026 @ 09:52:11):

| Time | Symbol | Side | Buy/Sell | Call/Put | Expiration | Premium | Strike | Volume | OI Signal | Size | Option Symbol |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 09:52:11 | GOOGL | ASK | BUY | PUT | 2026-05-15 | $1.5M | $215 | 10K | HIGH_ACTIVITY | 10,000 | GOOGL20260515P215 |

🤓 What This Actually Means

This is a buy-to-open (BTO) long put - a protective or speculative bearish position. Let's break it down:

- 💸 Premium paid: $1.5M ($15.00 per contract x 10,000 contracts)

- 🎯 Deep out-of-the-money: $215 strike is ~28% below the current price of ~$302

- 📊 Massive position: 10,000 contracts = 1,000,000 shares of notional exposure (~$302M worth of stock)

- 🔥 Vol/OI ratio: 14.62x - This is fresh, deliberate positioning, not rolling an existing hedge

- 🏦 Z-Score: 306.34 - EXTREMELY UNUSUAL. This kind of size at this distance from the money shows up only a few times per year

What's really happening here:

This trader is buying deep OTM portfolio insurance. At $215, $GOOGL would need to crash ~28% in about 10 weeks for these puts to land in the money. That's not a casual hedge - this is the kind of protection you buy when you're sitting on a massive long position and want catastrophic downside coverage. Think of it like buying fire insurance on a $300M house - you don't expect the fire, but if it happens, you want to be covered.

The timing is interesting: there's an ad tech antitrust ruling expected in H1 2026 that could force Google to divest its AdX exchange, Q1 earnings are coming in late April, and the EU DMA review is due by May 3rd. Any combination of negative outcomes across these events could create the kind of 20%+ drawdown this put buyer is hedging against.

Unusual Score: 🔥🔥🔥 EXTREMELY UNUSUAL (Z-Score: 306.34) - A trade this far out of the ordinary in terms of volume relative to historical patterns is exceptionally rare. The 10,000-contract clip bought on the ASK side confirms aggressive buying intent.

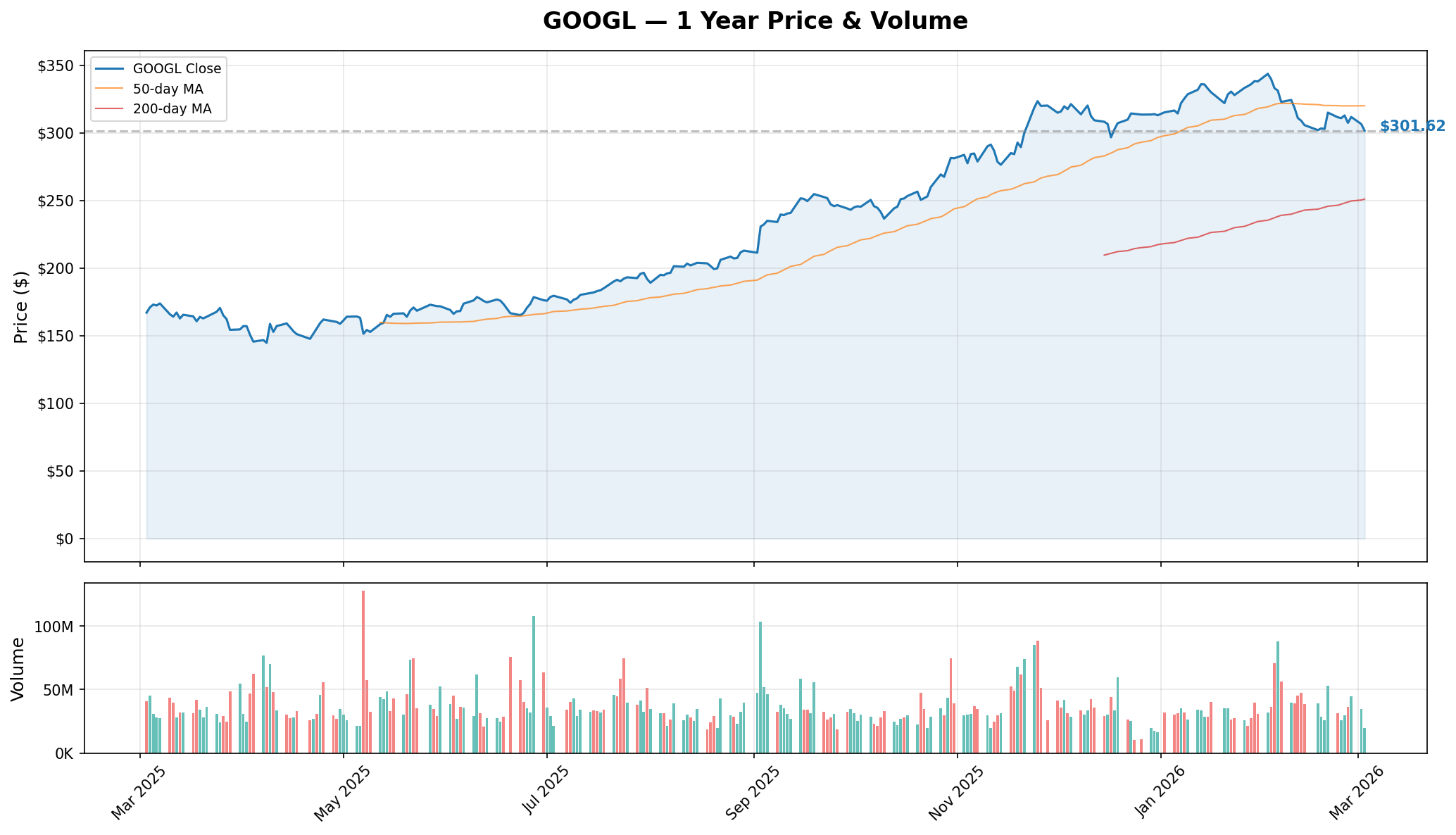

📈 Technical Setup / Chart Check-Up

YTD Performance Chart

Alphabet has had a rough start to 2026 after an incredible 2025 run. The stock peaked at $343.69 on February 2nd - the day before Q4 earnings - then got smacked 7% lower despite beating on both revenue and EPS. Why? A jaw-dropping $175B-$185B capex guidance for 2026 that more than doubles 2025 spending.

Key observations:

- 📉 11% off ATH: From $343.69 to ~$302, a meaningful correction for a $3.7T company

- 🎢 Range-bound since mid-February: Trading in the $296-$315 corridor

- 💹 $300 psychological support: Stock has gravitated around the $300 level recently

- 📊 Volume spike on earnings gap-down: Institutional repositioning is clearly underway

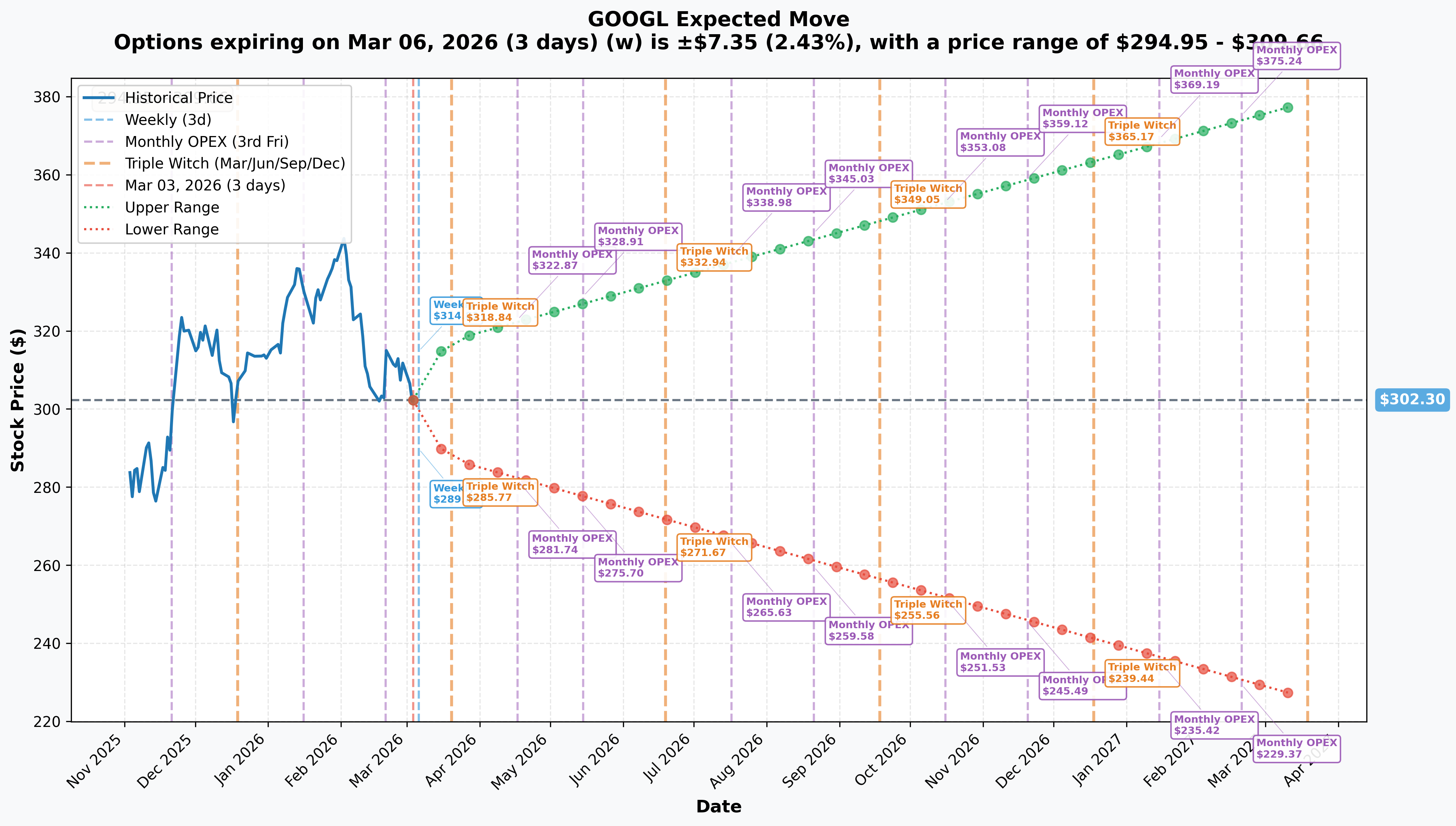

Implied Move Analysis

Options market pricing for upcoming expirations:

- 📅 Weekly (Mar 6 - 3 days): +/-$7.35 (+/-2.43%) --> Range: $294.95 - $309.66

- 📅 Monthly OPEX / Triple Witch (Mar 20 - 17 days): +/-$15.36 (+/-5.08%) --> Range: $286.94 - $317.67

- 📅 May OPEX (May 15 - trade expiration): +/-$26.61 --> Range: $275.70 - $328.91

- 📅 LEAPS (Mar 2027 - 381 days): +/-$76.46 (+/-25.29%) --> Range: $225.85 - $378.76

Translation for regular folks:

Options traders are pricing in a 2.4% move ($7.35) by this Friday and a 5.1% move ($15.36) through March OPEX. By the May 15 expiration of this put trade, the market expects $GOOGL could move as much as $26.61 in either direction - that's a range of roughly $276 to $329.

Here's the key insight: the $215 put strike is about $61 below the lower bound of the May implied move range ($275.70). That means even the options market doesn't expect $GOOGL to get anywhere near $215 in normal conditions. This buyer is hedging against a tail-risk event - something catastrophic like a forced AdX divestiture combined with a broader market sell-off.

Gamma-Based Support & Resistance Analysis

Key Gamma Levels:

🔵 Support Levels (Put Gamma - blue bars):

- $260 - Significant put gamma concentration; a major downside floor

- $240 - Maximum gamma strike; heavy options activity clustered here

- $215 - Today's put strike; now an active institutional interest level

- $175 - Deep support from longer-dated options

🟠 Resistance Levels (Call Gamma - orange bars):

- $325 - First major call gamma wall above current price

- $345 - Near the all-time high; heavy call positioning

- $410 - Longer-dated upside target zone

What this means for traders:

The gamma landscape shows $GOOGL sitting in a relatively balanced zone with key gamma strikes spread out above and below. The $240 level has the densest gamma concentration, which acts as a gravitational pull if the stock weakens meaningfully. Above current price, the $325 level is the first significant resistance where call gamma builds up. The $300-$325 corridor is where most of the near-term action is concentrated - matching the current consolidation range perfectly.

🎪 Catalysts

🔥 Upcoming Catalysts

Dividend Ex-Date - March 9, 2026 💰

$0.21/share quarterly dividend - minor but worth noting for income-focused holders.

March 20 - Triple Witch OPEX 📅

Major options expiration with elevated hedging flows. Implied move prices a $287-$318 range through this date.

Google Cloud Next - April 22-24, 2026 ☁️

Major enterprise AI product announcements expected in Las Vegas. Cloud partnership wins and infrastructure scaling updates could be a catalyst for re-rating the cloud business, especially with the $240B backlog as a tailwind.

Q1 2026 Earnings - Expected April 23-28, 2026 📊

Consensus Revenue: $106.73B, EPS: $2.60-$2.62. Key metrics to watch:

- 📊 Google Cloud growth rate (can it sustain ~40% YoY?)

- 💸 Capex run-rate vs. $175B-$185B full-year guide

- 🤖 Gemini monetization progress (750M MAU base)

- 📈 Operating margins amid rising depreciation

Ad Tech Antitrust Remedies Ruling - Expected H1 2026 ⚖️

Judge Brinkema's decision on whether to force Google to divest its AdX exchange. This is the big one. A forced divestiture could reduce Alphabet revenue by 5-8%, while behavioral remedies (60% probability based on search case precedent) would be a relief rally catalyst.

EU DMA Legislative Review - Due by May 3, 2026 🇪🇺

European Commission review of Digital Markets Act compliance. Maximum fine exposure: up to 10% of global annual revenue (~$35B+). Probability of material fine in 2026 estimated at ~30%.

Google I/O - May 19-20, 2026 🤖

Annual developer conference in Mountain View. Expect Gemini model updates, Android platform evolution, and AI-powered search/advertising innovations. Historically a significant sentiment catalyst - and it falls just 4 days after this put expires.

⏪ Recent Catalysts (Already Happened)

Q4 2025 Earnings Beat / Capex Shock (February 4, 2026):

Revenue of $113.8B (+18% YoY) beat consensus, and EPS of $2.82 vs. $2.64 expected was a solid beat. But the $175B-$185B capex guide more than doubled 2025 spend and sent the stock down 7%.

Waymo $16B Funding Round (February 2, 2026):

Waymo raised $16B at a $126B valuation from Dragoneer, DST Global, Sequoia, and Alphabet. Now operating in 10 US cities with plans for 20+ cities and international expansion (London, Tokyo) in 2026.

Search Antitrust Remedies Finalized & Appealed:

Judge rejected Chrome divestiture and forced Android sale in December 2025 - a win for Alphabet. However, DOJ and states filed an appeal in February 2026 seeking stronger structural remedies, keeping this risk alive.

Analyst Upgrades:

Goldman Sachs raised their target to $400, J.P. Morgan to $395, and UBS lifted to $345. Consensus rating is Strong Buy with an average target of $351 - implying ~16% upside from here.

🎲 Price Targets & Probabilities

Using implied move data, gamma levels, and the catalyst calendar:

📈 Bull Case (30% probability)

Target: $330-$350

How we get there:

- ☁️ Google Cloud Next (April 22-24) delivers blockbuster enterprise AI announcements, re-rating the cloud segment

- 📊 Q1 earnings show Cloud maintaining 40%+ growth, Gemini monetization accelerating from 750M MAU

- ⚖️ Ad tech antitrust ruling comes in as behavioral remedies only (60% probability) - relief rally

- 🤖 Gemini ads begin limited testing, opening a massive new revenue channel

- 📈 Stock breaks above $325 gamma resistance, triggering dealer hedging flows and short covering

- 💪 Analyst consensus of $351 average / $400 high target starts pulling price higher

Key risk to bulls: The $175B-$185B capex overhang and DOJ appeal keep a ceiling on multiple expansion even with strong execution.

Impact on this put trade: Dead on arrival. At $330+, the $215 put expires deep out of the money and the $1.5M premium is a total loss - just the cost of insurance that wasn't needed.

🎯 Base Case (45% probability)

Target: $285-$320 range-bound

Most likely scenario:

- ✅ Stock continues consolidating in the $296-$315 range through March

- 📊 Q1 earnings are in-line with expectations, no major capex surprises

- ⚖️ Ad tech antitrust ruling gets delayed or comes with mixed signals

- 🔄 Investors wait for clearer evidence of AI spending ROI before committing

- 📉 The $287 implied move lower bound for March OPEX acts as a soft floor

- 📈 The $318 implied move upper bound caps upside through Triple Witch

This is the most likely outcome for the put trade: $GOOGL stays well above $215, the puts lose value gradually through theta decay, and the buyer accepts the $1.5M as the cost of portfolio insurance. No harm, no foul - just the price of sleeping at night.

📉 Bear Case (25% probability)

Target: $240-$275

What could go wrong:

- 😰 Ad tech antitrust ruling forces AdX divestiture - could reduce revenue by 5-8%, triggering a 10-15% sell-off

- 📉 Q1 earnings disappoint on cloud deceleration or capex overshoot, echoing the February gap-down

- 🇪🇺 EU DMA fine materializes near the ~$35B maximum exposure

- 💸 Macro deterioration: tariff-driven ad spending cuts from Chinese e-commerce advertisers (Temu, Shein) combined with recession fears

- 🔻 Multiple compression across tech sector as AI spending ROI concerns spread

- 🛡️ $260 gamma support breaks: A decisive break below this level could accelerate selling toward the $240 max gamma strike

Impact on this put trade: Getting warmer. At $260, the puts gain meaningful value as delta increases. At $240 (the max gamma strike), the puts are still OTM but would be worth significantly more than the $15 paid. Only if $GOOGL actually hits $215 does the trade fully pay off.

⚠️ Tail Risk Scenario (5-10% probability)

Target: Below $215

For the $215 puts to land in the money, you'd need a perfect storm:

- ⚖️ Forced AdX divestiture AND adverse DOJ appeal outcome

- 📉 Q1 earnings miss badly (cloud deceleration + margin compression)

- 🇪🇺 EU imposes material DMA fine

- 😰 Broader macro crisis (recession confirmation, trade war escalation)

- 💥 Combined impact: 25-30% drawdown from current levels

This is exactly what the put buyer is hedging against - a low-probability, high-impact scenario where multiple risks materialize simultaneously. At $215, $GOOGL would trade at roughly $2.6T market cap, similar to early October 2025 levels.

💡 Trading Ideas

🛡️ Conservative: The "Collect Dividends and Chill" Put Sell

Play: Sell May 15 $275 puts on $GOOGL (at or near the implied move lower bound)

Why this works:

- 💰 Collect premium while offering to buy $GOOGL at a 9% discount to current price

- 📊 $275 is below the May implied move lower bound ($275.70), making assignment unlikely

- 🛡️ 96% of analysts rate GOOGL a Buy/Strong Buy with a $351 average target - if you get assigned, you're buying at a bargain

- ⏰ 73 days of theta decay working in your favor

- 💹 Even Waymo's standalone $126B valuation provides a value floor for the parent company

Estimated P&L:

- 💰 Collect ~$3-5 per contract in premium

- 📉 If assigned, effective purchase price = $270-$272 (~10% below current price)

- ✅ Breakeven sits well below the implied move range

Risk level: Low | Skill level: Intermediate (requires margin approval)

⚖️ Balanced: The "Antitrust Hedge" Put Spread

Play: Buy a put spread to hedge antitrust risk through the expected ruling window

Structure: Buy May $290 puts / Sell May $265 puts

Why this works:

- 🎯 Targets the 10-15% drawdown scenario from an adverse ad tech ruling

- ⚖️ Ad tech case has ~40% probability of structural remedies - enough to justify hedging

- 📊 Covers you through Q1 earnings AND the expected ruling window

- 💰 Defined risk: max loss is the net premium paid

- 🛡️ $265 short put leg aligns with gamma support zone, limiting how much you pay

Estimated P&L:

- 💰 Net debit: ~$4-6 per spread

- 📈 Max profit: $25 spread width minus premium = ~$19-21 per spread at $265 or below

- 📉 Max loss: ~$400-600 per spread (the premium paid)

- 🎯 Breakeven: ~$284-$286

Risk level: Moderate (defined risk) | Skill level: Intermediate

🚀 Aggressive: The "Cloud Catalyst" Call Spread

Play: Buy a call spread to play the Google Cloud Next and Q1 earnings double catalyst

Structure: Buy May $310 calls / Sell May $340 calls

Why this works:

- ☁️ Google Cloud Next (April 22-24) and Q1 earnings (April 23-28) are back-to-back catalysts

- 📈 Cloud backlog of $240B and GenAI revenue growing 400% YoY provide fundamental support

- 💰 $310 strike is just above current price - you need a modest move to profit

- 📊 $340 cap aligns near the $345 gamma resistance level

- 🎯 Goldman's $400 target and JPMorgan's $395 target suggest the street sees 30%+ upside

Estimated P&L:

- 💰 Net debit: ~$7-9 per spread

- 📈 Max profit: $30 spread width minus premium = ~$21-23 per spread at $340+

- 📉 Max loss: ~$700-900 per spread (premium paid)

- 🎯 Breakeven: ~$317-$319

Risk level: High (directional catalyst bet) | Skill level: Advanced

⚠️ Risk Factors

Keep these on your radar before trading $GOOGL:

-

💸 $175B-$185B capex could crush margins: This is more than double 2025 spending, and management warned of higher depreciation and data center costs impacting margins. If AI monetization doesn't scale fast enough to offset, expect continued multiple compression.

-

⚖️ Ad tech antitrust ruling is the big wildcard: DOJ is seeking a forced sale of Google's AdX exchange. A structural remedy could reduce Alphabet revenue by 5-8% and reshape the digital advertising ecosystem. This ruling is expected in H1 2026 - right in the window of this put's expiration.

-

🇪🇺 EU DMA exposure is massive: Up to 10% of global annual revenue (~$35B+) in potential fines. The Commission has already opened new proceedings on Google's compliance with interoperability and search data-sharing obligations.

-

📉 Search antitrust isn't over: The DOJ and states appealed the favorable behavioral-only remedies ruling, potentially reintroducing Chrome divestiture risk at the D.C. Circuit level.

-

🤖 AI competition is intensifying: OpenAI/Microsoft, Anthropic, and Meta are all gunning for Google's AI dominance. If Gemini falls behind on model quality, the $175B+ investment looks increasingly like an arms race with diminishing returns.

-

📊 Tariff-driven ad spending cuts: Chinese e-commerce advertisers (Temu, Shein) - among Google's top ad spenders - cut spending significantly due to tariffs. With ads making up 70%+ of revenue, this is a real headwind.

-

💸 Free cash flow at risk: 2025 trailing FCF was $73.3B, but $175B+ in capex could push FCF negative or near-zero if revenue growth doesn't accelerate. That's a hard pill for a $3.7T market cap company.

🎯 The Bottom Line

Real talk: Someone just spent $1.5M on deep out-of-the-money puts on Alphabet, and while that sounds alarming, let's keep perspective. For an institutional player sitting on a multi-billion-dollar $GOOGL position, $1.5M is the cost of a really good insurance policy. The Z-Score of 306 tells us this trade is statistically unusual - this kind of activity shows up only a handful of times per year - but the deep OTM nature ($215 is 28% below current price) screams portfolio hedge, not conviction bearish bet.

What this trade tells us:

- 🎯 A large portfolio holder is worried about tail risk between now and mid-May

- ⚖️ The ad tech antitrust ruling, Q1 earnings, and EU DMA review are all catalysts that fall within this window

- 💰 The $215 target level implies hedging against a 25-30% crash scenario - rare, but not impossible if multiple risks converge

- 📊 The 14.6x Vol/OI ratio confirms this is a brand new position, not a roll or adjustment

If you own GOOGL:

- ✅ Don't panic - this is likely hedging behavior, not a directional call that $GOOGL is heading to $215

- 📊 Analyst consensus is Strong Buy with a $351 average target - the fundamental story is intact

- 🛡️ Consider adding your own downside protection via put spreads if you're nervous about the antitrust ruling

- 💰 Collect the $0.21 dividend (ex-date March 9) and sell covered calls to generate income during consolidation

- 💪 Cloud backlog at $240B, Gemini at 750M MAU, and Waymo at $126B valuation are all reasons to hold long-term

If you're watching from the sidelines:

- 🎯 A pullback to $287 (March OPEX implied move lower bound) would be an interesting entry for a long-term position

- 📊 Wait for the ad tech antitrust ruling clarity before making big bets - that's the binary event to watch

- ☁️ Google Cloud Next (April 22-24) and Q1 earnings are back-to-back catalysts that could set direction for the rest of 2026

If you're bearish:

- 📉 The capex overhang and regulatory gauntlet are legitimate headwinds - this isn't just fear-mongering

- 🎯 Put spreads ($290/$265 for May) offer defined-risk downside exposure through the key catalyst window

- ⚠️ Be careful shorting a stock with 90% Buy ratings and $400 price targets from Goldman Sachs - the crowd can be right for a while

- ⏰ Sell rallies toward $315-$325 rather than chasing momentum at $302

Mark your calendar - Key dates:

- 📅 March 6 (Friday) - Weekly options expiration (implied range: $295-$310)

- 📅 March 9 - Dividend ex-date ($0.21/share)

- 📅 March 20 - Triple Witch OPEX (implied range: $287-$318)

- 📅 April 22-24 - Google Cloud Next (Las Vegas)

- 📅 Late April (est. April 23-28) - Q1 2026 earnings report

- 📅 May 3 - EU DMA legislative review deadline

- 📅 May 15 - Expiration of this $1.5M put trade

- 📅 May 19-20 - Google I/O developer conference

- 📅 H1 2026 - Ad tech antitrust remedies ruling expected

Final verdict: This $1.5M put purchase is a masterclass in institutional risk management - not a fire alarm. The trader is paying less than 0.05% of their likely portfolio value to sleep well at night while a parade of regulatory, earnings, and macro catalysts plays out. For retail traders, the takeaway isn't to panic-buy puts at $215. Instead, use this as a reminder to check your own hedges heading into a catalyst-heavy stretch. If you're long $GOOGL, the fundamental story remains compelling - $240B cloud backlog, Gemini at 750M users, Waymo scaling aggressively - but the regulatory calendar demands respect. Hedge smart, stay patient, and let the catalysts come to you.

Disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. This analysis is for educational purposes only and not financial advice. Past performance doesn't guarantee future results. The Z-Score of 306.34 reflects this specific trade's unusualness relative to recent activity - it does not imply the trade will be profitable or that you should follow it. Always do your own research and consider consulting a licensed financial advisor before trading.

About Alphabet Inc.: Alphabet is the $3.71 trillion holding company behind Google, the world's dominant search engine and advertising platform. The company derives ~90% of revenue from Google services (primarily advertising), with Google Cloud (~10%) as its fastest-growing segment at 48% YoY. Other bets include Waymo ($126B valuation autonomous vehicles), Verily (health), and Google Fiber.